BUACC5933 Assignment: Cost and Management Accounting Analysis

VerifiedAdded on 2023/06/08

|12

|2769

|337

Homework Assignment

AI Summary

This assignment solution addresses key concepts in cost and management accounting. Part 1 explores activity-based costing (ABC) and its benefits for diversified organizations, calculating predetermined overhead rates and overhead costs for product lines. Part 2 delves into cost-volume-profit (CVP) analysis, discussing assumptions and its value for businesses, including a car rental company scenario. Part 3 examines the importance of sustainable reporting, outlining its benefits and comparing various local and international sustainable reporting frameworks, with a focus on Australian adoption of GRI standards. The assignment includes calculations, analysis, and a discussion of real-world applications of cost and management accounting principles.

Running head: COST AND MANAGEMENT Accounting

1

Cost and Management Accounting

Name

Institution

1

Cost and Management Accounting

Name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COST AND MANAGEMENT ACCOUNTING

2

PART 1

Question 1

a. As an organization expands, it is common for their product offering to become

diversified. Explain the reasons that would cause management to change to an activity

based costing system and the benefits that could be expected by the organization.

One of the advantages of diversification is expansion into new product niches and provision of

effective paths for growth. With the expansion of the product and service ranges, it is easier for a

company to sell more products to the both existing customers or markets as well as the potential

customers and establishing new markets at the same time. This reason among others explains

why it is common for businesses to diversify their products and services upon expansion

(Barkemeyer, Holt, Preuss, & Tsang, 2014).

There are several other reasons for diversification. Among them is for survival reason whereby a

company focuses on a wide range of products to have access to a massive number of customers.

In most cases, a market may not be big enough to support several competing firms and the cost

of running the business may be very high and overcome the expected revenue. Under such cases,

most companies take advantage of their expansion rate to survive through diversification into

new product lines for long term viability of the company (Aras & Crowther, 2016).

Diversification can also be used to cushion cash flow throughout the year. More than that new

product and service niches enables a company to generate more revenues through increased sales

and help the company to penetrate markets that would have been closed to the company if it

remained focused on single product line. Following an intense approach of choosing, analysis of

diversification, internal sources, risk evaluation and consumer research, the right approach of

2

PART 1

Question 1

a. As an organization expands, it is common for their product offering to become

diversified. Explain the reasons that would cause management to change to an activity

based costing system and the benefits that could be expected by the organization.

One of the advantages of diversification is expansion into new product niches and provision of

effective paths for growth. With the expansion of the product and service ranges, it is easier for a

company to sell more products to the both existing customers or markets as well as the potential

customers and establishing new markets at the same time. This reason among others explains

why it is common for businesses to diversify their products and services upon expansion

(Barkemeyer, Holt, Preuss, & Tsang, 2014).

There are several other reasons for diversification. Among them is for survival reason whereby a

company focuses on a wide range of products to have access to a massive number of customers.

In most cases, a market may not be big enough to support several competing firms and the cost

of running the business may be very high and overcome the expected revenue. Under such cases,

most companies take advantage of their expansion rate to survive through diversification into

new product lines for long term viability of the company (Aras & Crowther, 2016).

Diversification can also be used to cushion cash flow throughout the year. More than that new

product and service niches enables a company to generate more revenues through increased sales

and help the company to penetrate markets that would have been closed to the company if it

remained focused on single product line. Following an intense approach of choosing, analysis of

diversification, internal sources, risk evaluation and consumer research, the right approach of

COST AND MANAGEMENT ACCOUNTING

3

product diversification represent an opportunity for the company to expand its product and

service ranges to penetrate other markets.

b. The following annual data related to Happy Cow Cheese manufacturing company for

July, 2018. The company produces two types of cheese namely; Happy cow Slices and

Herbs Cheese.

Budgeted Actual

Slices Herbs

Machine hours 22,500 900 450

Direct labour hours 45,000 1,200 900

Direct labour cost $ 630,000 $ 33.75 per hour

Manufacturing

overhead cost

$ 819,000 $ 76,500

Company uses machine hours as the cost driver.

i. Calculate the company’s predetermined plant-wide overhead rate (01 marks)

Overhead Rate = (Total budgeted overhead / Basis)

Therefore, the Predetermined plant-wide overhead rate= the estimated total Manufacturing

overhead costs/ estimated total activity base (labor hours)

=$ 819,000/ 45,000

=$18.2 per hour

ii. the overhead costs of each of the two products

3

product diversification represent an opportunity for the company to expand its product and

service ranges to penetrate other markets.

b. The following annual data related to Happy Cow Cheese manufacturing company for

July, 2018. The company produces two types of cheese namely; Happy cow Slices and

Herbs Cheese.

Budgeted Actual

Slices Herbs

Machine hours 22,500 900 450

Direct labour hours 45,000 1,200 900

Direct labour cost $ 630,000 $ 33.75 per hour

Manufacturing

overhead cost

$ 819,000 $ 76,500

Company uses machine hours as the cost driver.

i. Calculate the company’s predetermined plant-wide overhead rate (01 marks)

Overhead Rate = (Total budgeted overhead / Basis)

Therefore, the Predetermined plant-wide overhead rate= the estimated total Manufacturing

overhead costs/ estimated total activity base (labor hours)

=$ 819,000/ 45,000

=$18.2 per hour

ii. the overhead costs of each of the two products

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COST AND MANAGEMENT ACCOUNTING

4

for slices=1516500/78633.75

=19.29

For Herbs=1516500/77883.75

=19.47

iii. the actual overhead cost to the amount of overhead applied to the two products

in July

for the Slices, the applied or budgeted overhead cost to the actual cost is 1516500 to

78633.75

for the herbs, the ratio of the a ratio of the budgeted or applied overhead cost to the

actual is 1516500 to 77883.75

PART 2

QUESTION 1

Two companies have identical products, total fixed costs and variable costs per unit, yet

one company is able to set a much lower price for its product and still be as profitable as

the other company. Explain how this can happen.

The competitive element in a market involves the strategies that are adopted by individual

companies in the market. Profitability is based on the existing costs and revenues whereby

higher revenues compared to costs reflect high profit while higher costs than revenue

reflect loss (Bennett, James, & Klinkers, 2017). Fixed costs and identical products show

the uniformity of the companies except in the pricing strategy that makes them different.

4

for slices=1516500/78633.75

=19.29

For Herbs=1516500/77883.75

=19.47

iii. the actual overhead cost to the amount of overhead applied to the two products

in July

for the Slices, the applied or budgeted overhead cost to the actual cost is 1516500 to

78633.75

for the herbs, the ratio of the a ratio of the budgeted or applied overhead cost to the

actual is 1516500 to 77883.75

PART 2

QUESTION 1

Two companies have identical products, total fixed costs and variable costs per unit, yet

one company is able to set a much lower price for its product and still be as profitable as

the other company. Explain how this can happen.

The competitive element in a market involves the strategies that are adopted by individual

companies in the market. Profitability is based on the existing costs and revenues whereby

higher revenues compared to costs reflect high profit while higher costs than revenue

reflect loss (Bennett, James, & Klinkers, 2017). Fixed costs and identical products show

the uniformity of the companies except in the pricing strategy that makes them different.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COST AND MANAGEMENT ACCOUNTING

5

Pricing strategy influences demand and the volume of sales that eventually have effects on

the revenues (De Villiers, Rinaldi, & Unerman, 2014). When the price is lowered, demand

is increased and increased demand increases the volume of sales. High volumes of sales

generate more revenues that reflect to more profit than the other firm.

QUESTION 2

A car rental company rents small, medium and family-sized cars. What assumptions would

be made for the purpose of a cost volume profit analysis? Does this mean that CVP

analysis is of little value to this business? Explain your answer.

The assumptions underlying Cost volume profit analysis include

i. The cost consist of fixed and variable costs

ii. There is a linear relationship between both the costs and revenues all through the

relevant activity range

iii. The time value for money is ignored

iv. The selling price, the variable cost per unit, as well as the fixed costs are known

and are constant

v. The relative proportions of sales of the various products are also known and are

constant

The CVP analysis is very vital in financial metrics, especially for the small and medium size

firms helping their owners in improving the performances of their companies. The CVP

information is critical in budgeting, planning of profits for the business, creating controls for the

5

Pricing strategy influences demand and the volume of sales that eventually have effects on

the revenues (De Villiers, Rinaldi, & Unerman, 2014). When the price is lowered, demand

is increased and increased demand increases the volume of sales. High volumes of sales

generate more revenues that reflect to more profit than the other firm.

QUESTION 2

A car rental company rents small, medium and family-sized cars. What assumptions would

be made for the purpose of a cost volume profit analysis? Does this mean that CVP

analysis is of little value to this business? Explain your answer.

The assumptions underlying Cost volume profit analysis include

i. The cost consist of fixed and variable costs

ii. There is a linear relationship between both the costs and revenues all through the

relevant activity range

iii. The time value for money is ignored

iv. The selling price, the variable cost per unit, as well as the fixed costs are known

and are constant

v. The relative proportions of sales of the various products are also known and are

constant

The CVP analysis is very vital in financial metrics, especially for the small and medium size

firms helping their owners in improving the performances of their companies. The CVP

information is critical in budgeting, planning of profits for the business, creating controls for the

COST AND MANAGEMENT ACCOUNTING

6

costs as well as strategies for developing sales. Based on this fact, it is prudent to argue that the

principles of Cost Volume Profit analysis are of greater value to small businesses (Hajer,

Nilsson, Raworth, Bakker, et al. 2015). In addition, the analysis of the cost volume profit helps

businesses to breakdown the various elements of fixed costs and variable costs, thereby giving

the business firms very powerful insights into the profitability of their products as well as

service. The analysis can be broken down into figuring sown the effects of the cost and volume

changes on the operating expenses as well as the net income of the company within a specific

financial period (Ioannou & Serafeim, 2017). Due to this, they are in a position to expand, grow,

and develop their business size and market position.

PART 3

The importance of sustainable reporting by organizations

In the contemporary business management, sustainable reporting is slowly becoming an

obligation rather than a responsibility. In decades that have passed, sustainable reporting was

part of corporate communication by the companies. However, today, sustainable reporting is

becoming an integral segment of the corporate world in terms of information it contains as well

as based on the benefits that organizations are likely to obtain from the reporting. According to

the information given by Leslie, Nenadovic, Sievanen, Cavanaugh, et al. (2015), financial

reporting is the fundamental genesis of reporting process in the business sectors. Therefore, the

following are some of the substantial benefits of sustainability:

Sustainability reporting in the setting that is corporate is a vital factor that improves and links the

companies’ initiatives with the customers, suppliers, and the investors among other stakeholders.

6

costs as well as strategies for developing sales. Based on this fact, it is prudent to argue that the

principles of Cost Volume Profit analysis are of greater value to small businesses (Hajer,

Nilsson, Raworth, Bakker, et al. 2015). In addition, the analysis of the cost volume profit helps

businesses to breakdown the various elements of fixed costs and variable costs, thereby giving

the business firms very powerful insights into the profitability of their products as well as

service. The analysis can be broken down into figuring sown the effects of the cost and volume

changes on the operating expenses as well as the net income of the company within a specific

financial period (Ioannou & Serafeim, 2017). Due to this, they are in a position to expand, grow,

and develop their business size and market position.

PART 3

The importance of sustainable reporting by organizations

In the contemporary business management, sustainable reporting is slowly becoming an

obligation rather than a responsibility. In decades that have passed, sustainable reporting was

part of corporate communication by the companies. However, today, sustainable reporting is

becoming an integral segment of the corporate world in terms of information it contains as well

as based on the benefits that organizations are likely to obtain from the reporting. According to

the information given by Leslie, Nenadovic, Sievanen, Cavanaugh, et al. (2015), financial

reporting is the fundamental genesis of reporting process in the business sectors. Therefore, the

following are some of the substantial benefits of sustainability:

Sustainability reporting in the setting that is corporate is a vital factor that improves and links the

companies’ initiatives with the customers, suppliers, and the investors among other stakeholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COST AND MANAGEMENT ACCOUNTING

7

In most cases, sustainability reporting is seen as shows of clear and crystal transparency and

accountability.

Most of the actual investors and potential investors recognize only the sustainability reporting as

a long term goal defining the model of business the company is poised to use. More than that, the

sustainable reports are seen by the investors and other stakeholders of a company as a means that

can help in the improvement of practices that are already in use by the company.

There are several reviews of performance, strategic focuses and opportunities that are done by

the various stakeholders of a company during the sustainable reporting. Due to the interests from

these various stakeholders, they all look to the indices and performance reviews that eventually

assist them in choosing their brands (Nilsson, Griggs, & Visbeck, 2016). Through this, the

leaders in business are in a position to push for improved standards of financial and sustainable

standards in the company. In addition, during the process, they are able to generate positive

inputs and interest for the company that would also create transparency for the success that is

sustainable out of the shortcomings of the previous years.

Within the internal affairs of the company itself, sustainable reporting helps in accountability,

transparency, and performance that help in determining on the areas and operations of the

company as well as their practices that require enhancements and improvement.

It is also important to acknowledge the studies done by Meixell & Luoma (2015) that a

combination of sustainable reports and CSR are becoming vital and valuable sources of

information as well as references for the companies in their position to demonstrate its readiness

and action touching on issues that are important to the community. In this way, through the

7

In most cases, sustainability reporting is seen as shows of clear and crystal transparency and

accountability.

Most of the actual investors and potential investors recognize only the sustainability reporting as

a long term goal defining the model of business the company is poised to use. More than that, the

sustainable reports are seen by the investors and other stakeholders of a company as a means that

can help in the improvement of practices that are already in use by the company.

There are several reviews of performance, strategic focuses and opportunities that are done by

the various stakeholders of a company during the sustainable reporting. Due to the interests from

these various stakeholders, they all look to the indices and performance reviews that eventually

assist them in choosing their brands (Nilsson, Griggs, & Visbeck, 2016). Through this, the

leaders in business are in a position to push for improved standards of financial and sustainable

standards in the company. In addition, during the process, they are able to generate positive

inputs and interest for the company that would also create transparency for the success that is

sustainable out of the shortcomings of the previous years.

Within the internal affairs of the company itself, sustainable reporting helps in accountability,

transparency, and performance that help in determining on the areas and operations of the

company as well as their practices that require enhancements and improvement.

It is also important to acknowledge the studies done by Meixell & Luoma (2015) that a

combination of sustainable reports and CSR are becoming vital and valuable sources of

information as well as references for the companies in their position to demonstrate its readiness

and action touching on issues that are important to the community. In this way, through the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COST AND MANAGEMENT ACCOUNTING

8

sustainable reports, the companies indicates they are being proactive and foresee risks and are in

hand to counter the situations even before they turn out of control.

Comparison and contrast different local and international sustainable reporting frameworks

In the sustainable reporting, there are frameworks that have been devised in Australia for

adoption. This is supporting by the fact that both the national and local standards of reporting

automatically evolve along with the evolution experienced in the international frameworks.

There are certain local and national initiatives that are in consistent action in assisting the

companies with their sustainable reporting. The scope, sectors, and areas of their operations are

different, but they are all using their levels to assist the corporate sectors in their sustainable

reporting (Tschopp & Nastanski, 2014). The following are some of the international frameworks

used in sustainable reporting:

i. The United Nation global impact, also known as communication in progress

ii. The international organization for standardization, a guidance of social responsibility

iii. The international integrated reporting council, also known as the international framework

iv. Global reporting initiative, also known as the GRI sustainability reporting standards

Based on the responses that have their origin from the global players and stakeholders on

international companies, there are increasing calls for transparency and standards that are

national to work alongside the international standards. Among the national standards to work

along the international frameworks, especially in Australia include GRI and the SDG

(Sustainable development Goals).

8

sustainable reports, the companies indicates they are being proactive and foresee risks and are in

hand to counter the situations even before they turn out of control.

Comparison and contrast different local and international sustainable reporting frameworks

In the sustainable reporting, there are frameworks that have been devised in Australia for

adoption. This is supporting by the fact that both the national and local standards of reporting

automatically evolve along with the evolution experienced in the international frameworks.

There are certain local and national initiatives that are in consistent action in assisting the

companies with their sustainable reporting. The scope, sectors, and areas of their operations are

different, but they are all using their levels to assist the corporate sectors in their sustainable

reporting (Tschopp & Nastanski, 2014). The following are some of the international frameworks

used in sustainable reporting:

i. The United Nation global impact, also known as communication in progress

ii. The international organization for standardization, a guidance of social responsibility

iii. The international integrated reporting council, also known as the international framework

iv. Global reporting initiative, also known as the GRI sustainability reporting standards

Based on the responses that have their origin from the global players and stakeholders on

international companies, there are increasing calls for transparency and standards that are

national to work alongside the international standards. Among the national standards to work

along the international frameworks, especially in Australia include GRI and the SDG

(Sustainable development Goals).

COST AND MANAGEMENT ACCOUNTING

9

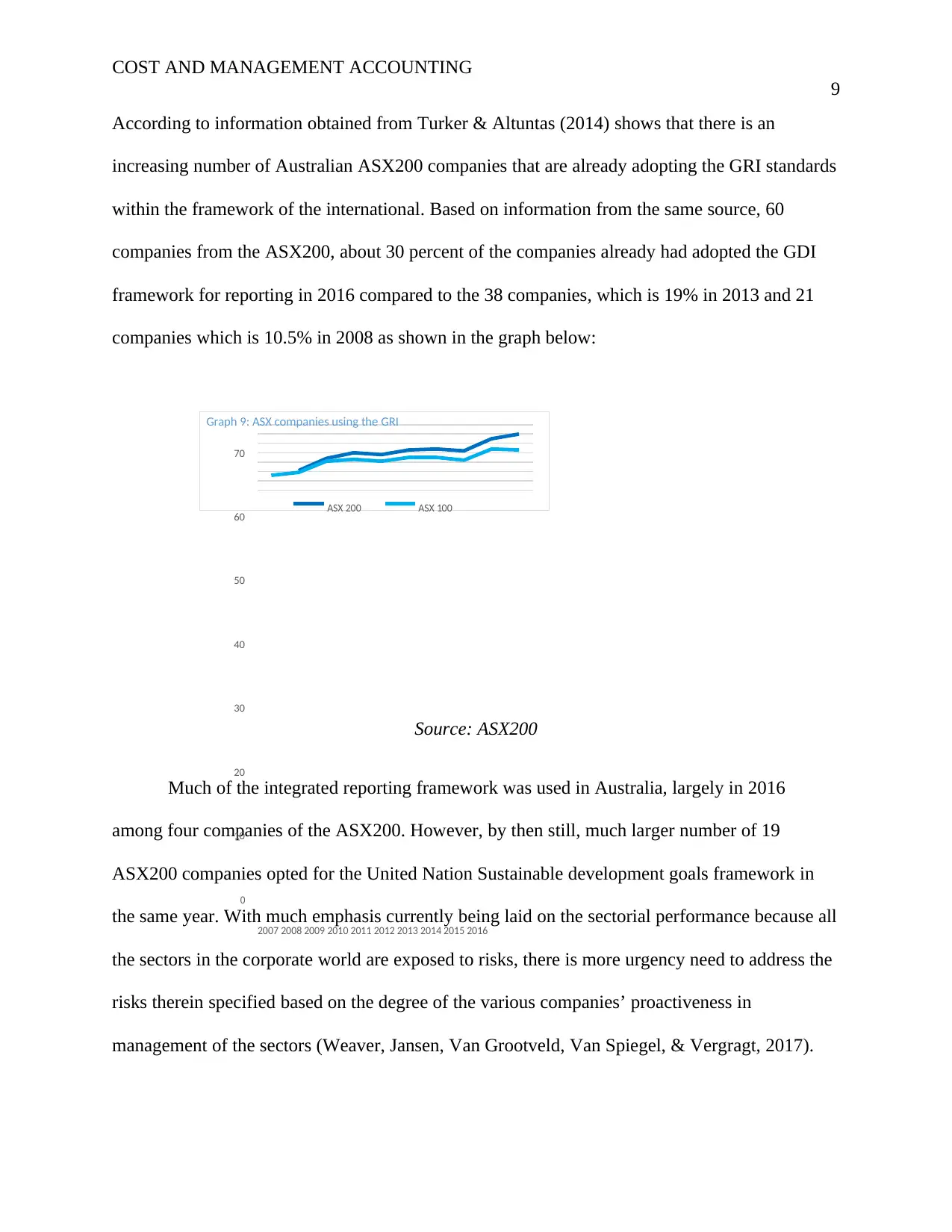

According to information obtained from Turker & Altuntas (2014) shows that there is an

increasing number of Australian ASX200 companies that are already adopting the GRI standards

within the framework of the international. Based on information from the same source, 60

companies from the ASX200, about 30 percent of the companies already had adopted the GDI

framework for reporting in 2016 compared to the 38 companies, which is 19% in 2013 and 21

companies which is 10.5% in 2008 as shown in the graph below:

Source: ASX200

Much of the integrated reporting framework was used in Australia, largely in 2016

among four companies of the ASX200. However, by then still, much larger number of 19

ASX200 companies opted for the United Nation Sustainable development goals framework in

the same year. With much emphasis currently being laid on the sectorial performance because all

the sectors in the corporate world are exposed to risks, there is more urgency need to address the

risks therein specified based on the degree of the various companies’ proactiveness in

management of the sectors (Weaver, Jansen, Van Grootveld, Van Spiegel, & Vergragt, 2017).

ASX 100ASX 200

Graph 9: ASX companies using the GRI

70

60

50

40

30

20

10

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

9

According to information obtained from Turker & Altuntas (2014) shows that there is an

increasing number of Australian ASX200 companies that are already adopting the GRI standards

within the framework of the international. Based on information from the same source, 60

companies from the ASX200, about 30 percent of the companies already had adopted the GDI

framework for reporting in 2016 compared to the 38 companies, which is 19% in 2013 and 21

companies which is 10.5% in 2008 as shown in the graph below:

Source: ASX200

Much of the integrated reporting framework was used in Australia, largely in 2016

among four companies of the ASX200. However, by then still, much larger number of 19

ASX200 companies opted for the United Nation Sustainable development goals framework in

the same year. With much emphasis currently being laid on the sectorial performance because all

the sectors in the corporate world are exposed to risks, there is more urgency need to address the

risks therein specified based on the degree of the various companies’ proactiveness in

management of the sectors (Weaver, Jansen, Van Grootveld, Van Spiegel, & Vergragt, 2017).

ASX 100ASX 200

Graph 9: ASX companies using the GRI

70

60

50

40

30

20

10

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COST AND MANAGEMENT ACCOUNTING

10

The expected disclosures in the sectors are also expected to unravel weaknesses and risks

in order to improve them over the stipulated timeframe because there is more risk awareness that

are being exposed especially in the supply chain, climate changes and other environmental issues

as well as the social issues that increase (Wood, Logsdon, Lewellyn & Davenport, 2015).

Therefore, sustainable disclosures have become recognized tool at hand for an effective

communication among the various stakeholders of the companies, especially the investors, both

current and potential investors.

References

10

The expected disclosures in the sectors are also expected to unravel weaknesses and risks

in order to improve them over the stipulated timeframe because there is more risk awareness that

are being exposed especially in the supply chain, climate changes and other environmental issues

as well as the social issues that increase (Wood, Logsdon, Lewellyn & Davenport, 2015).

Therefore, sustainable disclosures have become recognized tool at hand for an effective

communication among the various stakeholders of the companies, especially the investors, both

current and potential investors.

References

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COST AND MANAGEMENT ACCOUNTING

11

Aras, G., & Crowther, D. (2016). The durable corporation: Strategies for sustainable

development. Routledge.

Barkemeyer, R., Holt, D., Preuss, L., & Tsang, S. (2014). What happened to the ‘development’in

sustainable development? Business guidelines two decades after Brundtland. sustainable

development, 22(1), 15-32.

Bennett, M., James, P., & Klinkers, L. (Eds.). (2017). Sustainable measures: Evaluation and

reporting of environmental and social performance. Routledge.

De Villiers, C., Rinaldi, L., & Unerman, J. (2014). Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), 1042-

1067.

Hajer, M., Nilsson, M., Raworth, K., Bakker, P., Berkhout, F., de Boer, Y., ... & Kok, M. (2015).

Beyond cockpit-ism: Four insights to enhance the transformative potential of the

sustainable development goals. Sustainability, 7(2), 1651-1660.

Ioannou, I., & Serafeim, G. (2017). The consequences of mandatory corporate sustainability

reporting.

Leslie, H. M., Basurto, X., Nenadovic, M., Sievanen, L., Cavanaugh, K. C., Cota-Nieto, J. J., ...

& Nagavarapu, S. (2015). Operationalizing the social-ecological systems framework to

assess sustainability. Proceedings of the National Academy of Sciences, 201414640.

Meixell, M. J., & Luoma, P. (2015). Stakeholder pressure in sustainable supply chain

management: a systematic review. International Journal of Physical Distribution &

Logistics Management, 45(1/2), 69-89.

Nilsson, M., Griggs, D., & Visbeck, M. (2016). Policy: map the interactions between Sustainable

Development Goals. Nature News, 534(7607), 320.

11

Aras, G., & Crowther, D. (2016). The durable corporation: Strategies for sustainable

development. Routledge.

Barkemeyer, R., Holt, D., Preuss, L., & Tsang, S. (2014). What happened to the ‘development’in

sustainable development? Business guidelines two decades after Brundtland. sustainable

development, 22(1), 15-32.

Bennett, M., James, P., & Klinkers, L. (Eds.). (2017). Sustainable measures: Evaluation and

reporting of environmental and social performance. Routledge.

De Villiers, C., Rinaldi, L., & Unerman, J. (2014). Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), 1042-

1067.

Hajer, M., Nilsson, M., Raworth, K., Bakker, P., Berkhout, F., de Boer, Y., ... & Kok, M. (2015).

Beyond cockpit-ism: Four insights to enhance the transformative potential of the

sustainable development goals. Sustainability, 7(2), 1651-1660.

Ioannou, I., & Serafeim, G. (2017). The consequences of mandatory corporate sustainability

reporting.

Leslie, H. M., Basurto, X., Nenadovic, M., Sievanen, L., Cavanaugh, K. C., Cota-Nieto, J. J., ...

& Nagavarapu, S. (2015). Operationalizing the social-ecological systems framework to

assess sustainability. Proceedings of the National Academy of Sciences, 201414640.

Meixell, M. J., & Luoma, P. (2015). Stakeholder pressure in sustainable supply chain

management: a systematic review. International Journal of Physical Distribution &

Logistics Management, 45(1/2), 69-89.

Nilsson, M., Griggs, D., & Visbeck, M. (2016). Policy: map the interactions between Sustainable

Development Goals. Nature News, 534(7607), 320.

COST AND MANAGEMENT ACCOUNTING

12

Tschopp, D., & Nastanski, M. (2014). The harmonization and convergence of corporate social

responsibility reporting standards. Journal of Business Ethics, 125(1), 147-162.

Turker, D., & Altuntas, C. (2014). Sustainable supply chain management in the fast fashion

industry: An analysis of corporate reports. European Management Journal, 32(5), 837-

849.

Weaver, P., Jansen, L., Van Grootveld, G., Van Spiegel, E., & Vergragt, P. (2017). Sustainable

technology development. Routledge.

Welford, R. (2016). Corporate environmental management 3: Towards sustainable development.

Routledge.

Wood, D. J., Logsdon, J. M., Lewellyn, P. G., & Davenport, K. S. (2015). Global Business

Citizenship: A Transformative Framework for Ethics and Sustainable Capitalism: A

Transformative Framework for Ethics and Sustainable Capitalism. Routledge.

12

Tschopp, D., & Nastanski, M. (2014). The harmonization and convergence of corporate social

responsibility reporting standards. Journal of Business Ethics, 125(1), 147-162.

Turker, D., & Altuntas, C. (2014). Sustainable supply chain management in the fast fashion

industry: An analysis of corporate reports. European Management Journal, 32(5), 837-

849.

Weaver, P., Jansen, L., Van Grootveld, G., Van Spiegel, E., & Vergragt, P. (2017). Sustainable

technology development. Routledge.

Welford, R. (2016). Corporate environmental management 3: Towards sustainable development.

Routledge.

Wood, D. J., Logsdon, J. M., Lewellyn, P. G., & Davenport, K. S. (2015). Global Business

Citizenship: A Transformative Framework for Ethics and Sustainable Capitalism: A

Transformative Framework for Ethics and Sustainable Capitalism. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.