ACCT20076: Improving Cost Management at Sony Manufacturing Company

VerifiedAdded on 2023/06/06

|12

|1053

|315

Report

AI Summary

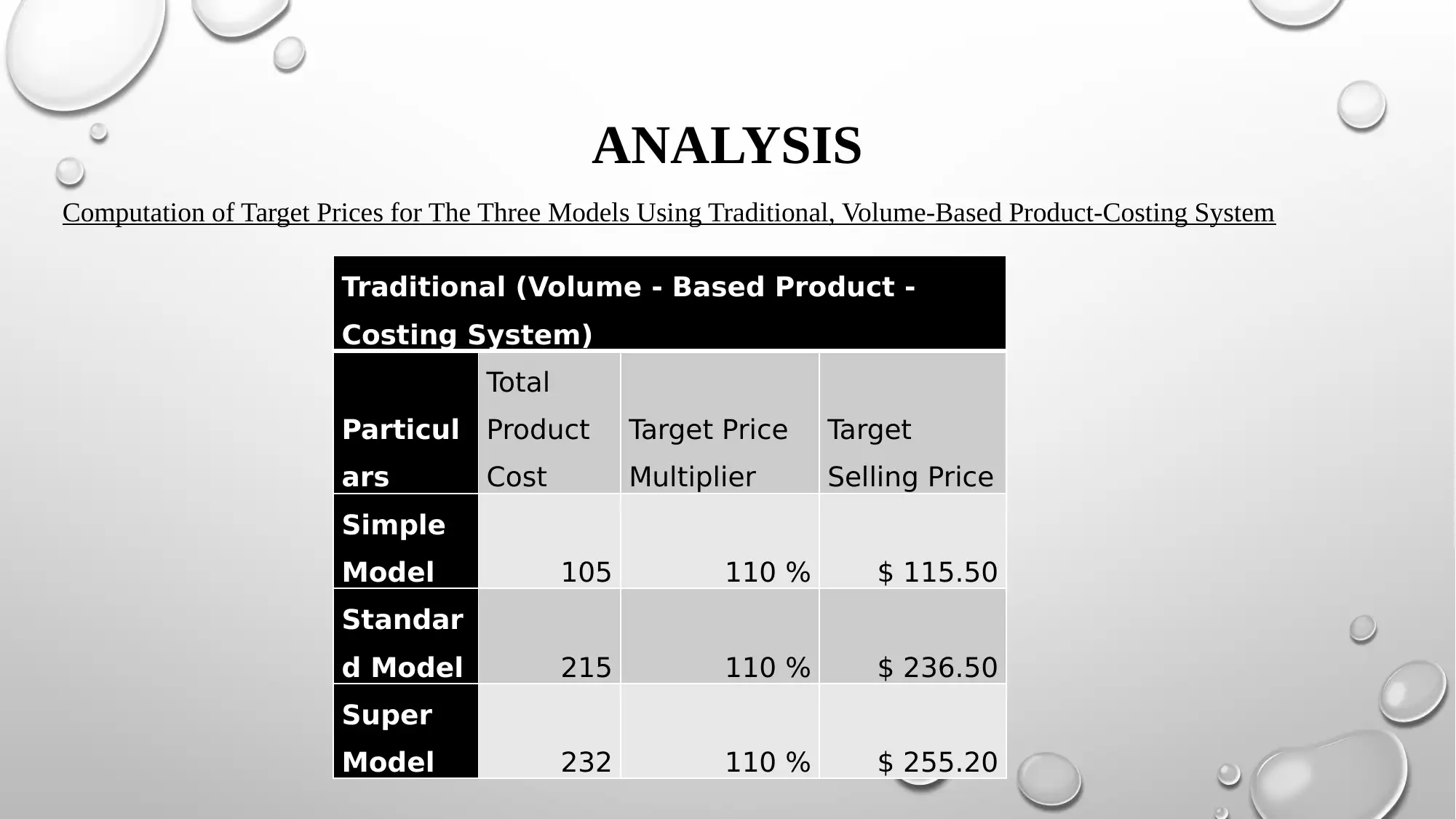

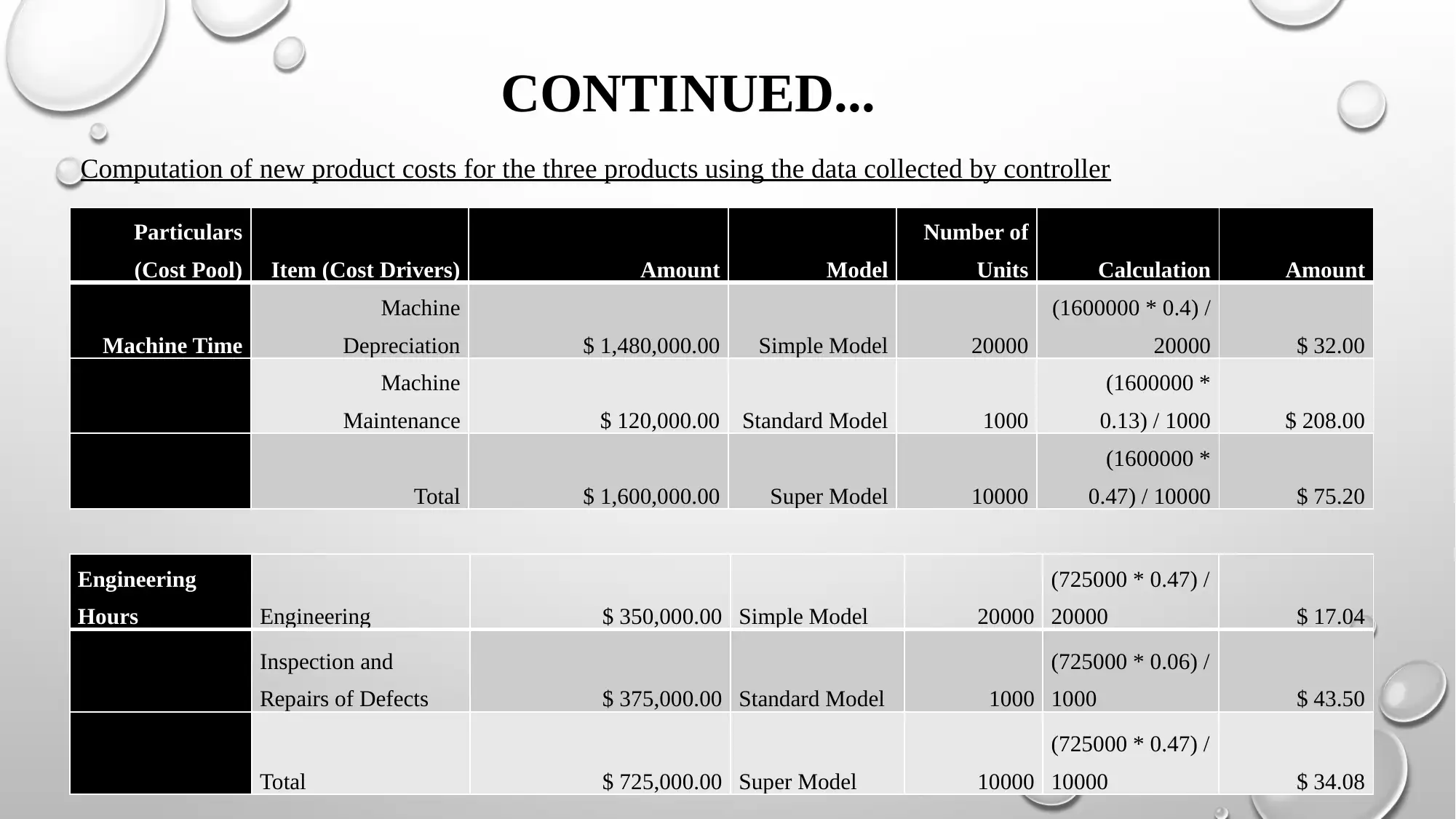

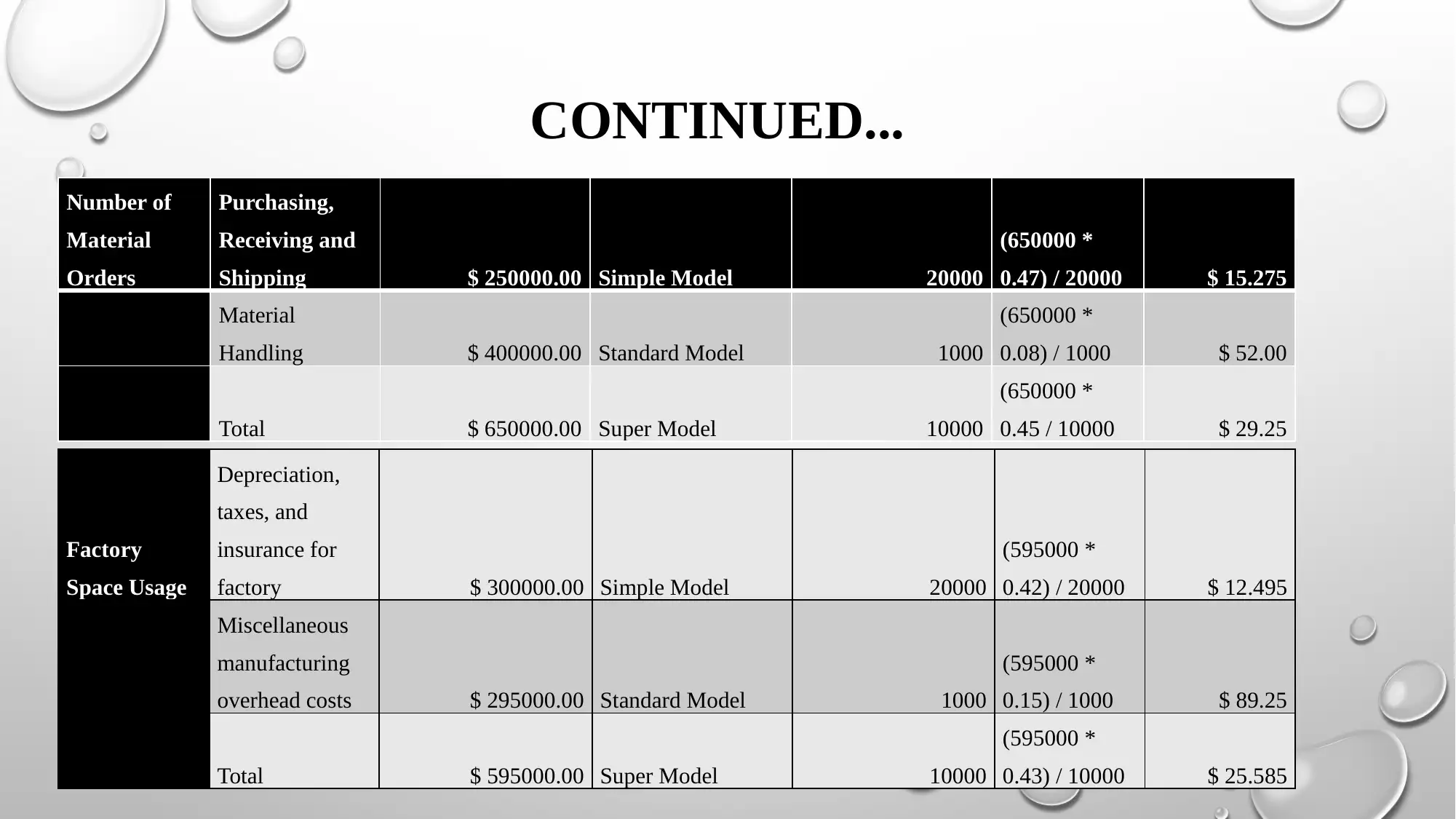

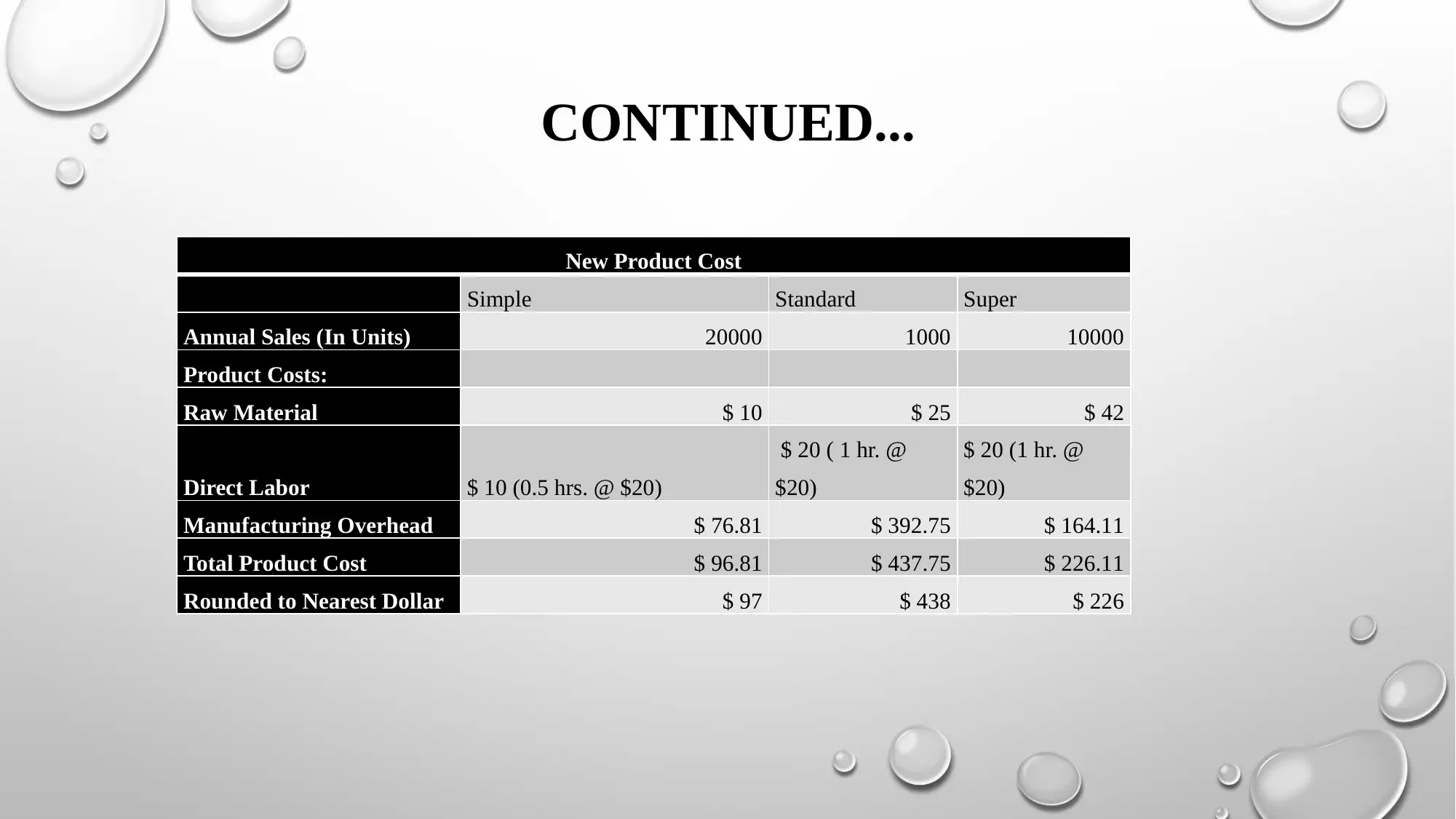

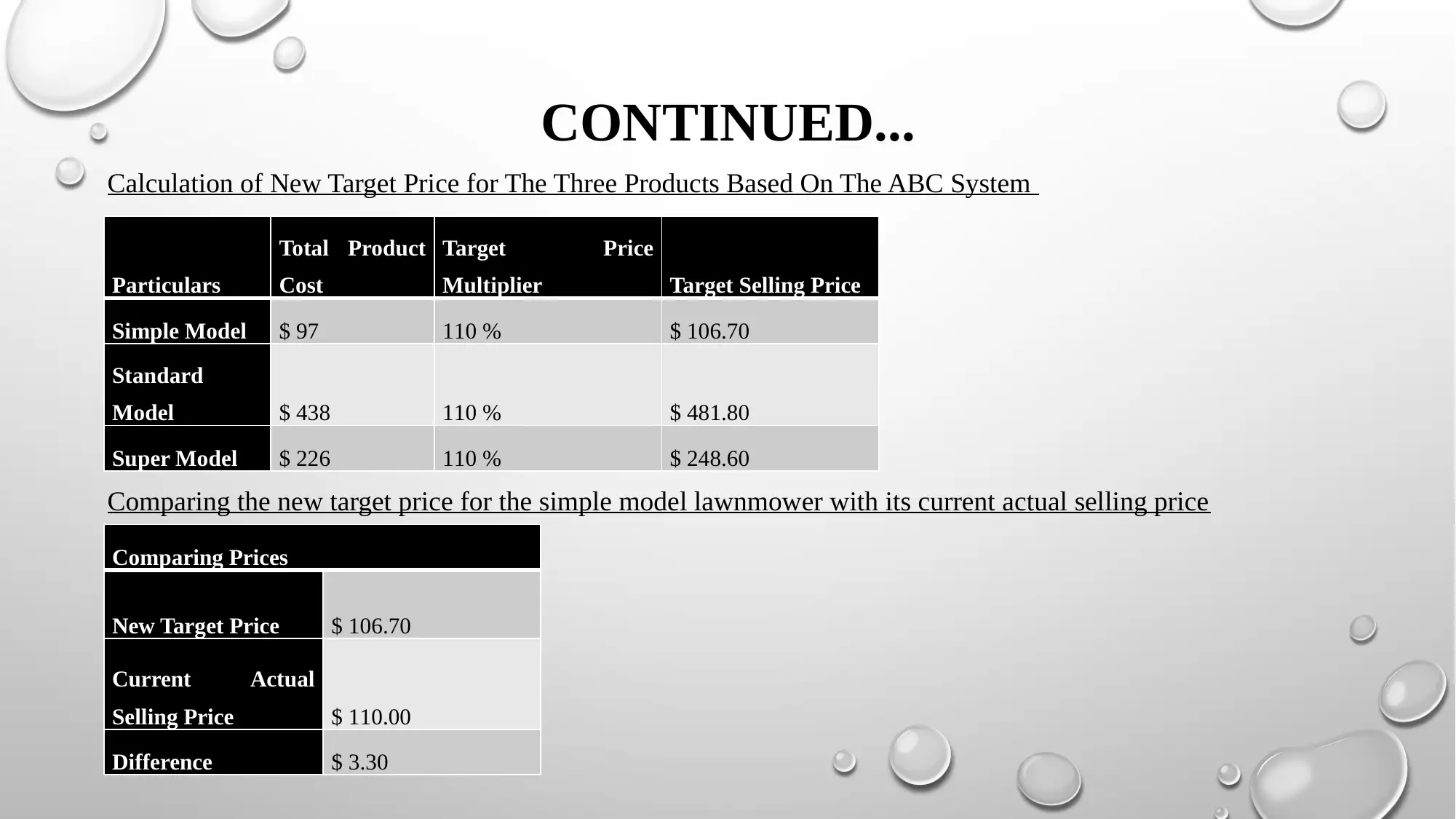

This report provides a comprehensive analysis of Sony Manufacturing's current traditional costing system and contrasts it with activity-based costing (ABC). The analysis includes computations of target prices using both methods, revealing discrepancies and inefficiencies in the traditional approach. Key findings indicate that the traditional system inadequately allocates overhead costs, leading to inaccurate product pricing. The report recommends adopting ABC to enhance cost control and improve pricing strategies. By identifying cost pools for each activity involved in production, Sony can gain better insights into its cost structure. The report concludes with actionable recommendations for implementing ABC, supported by relevant academic references. Desklib provides access to this and many other solved assignments to help students.

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.