Company Accounting: Cost Model, Fair Value, and Financial Analysis

VerifiedAdded on 2023/06/12

|8

|1428

|149

Homework Assignment

AI Summary

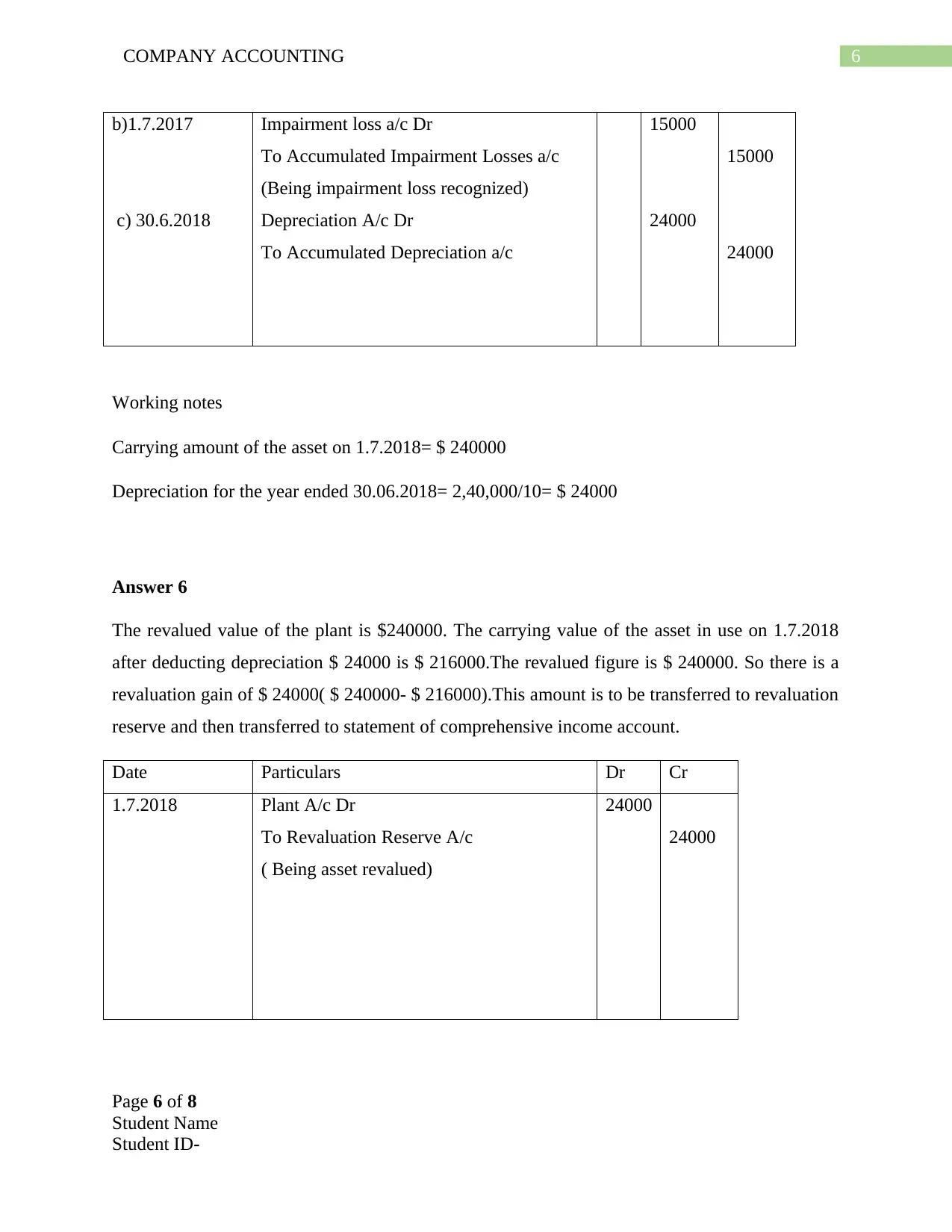

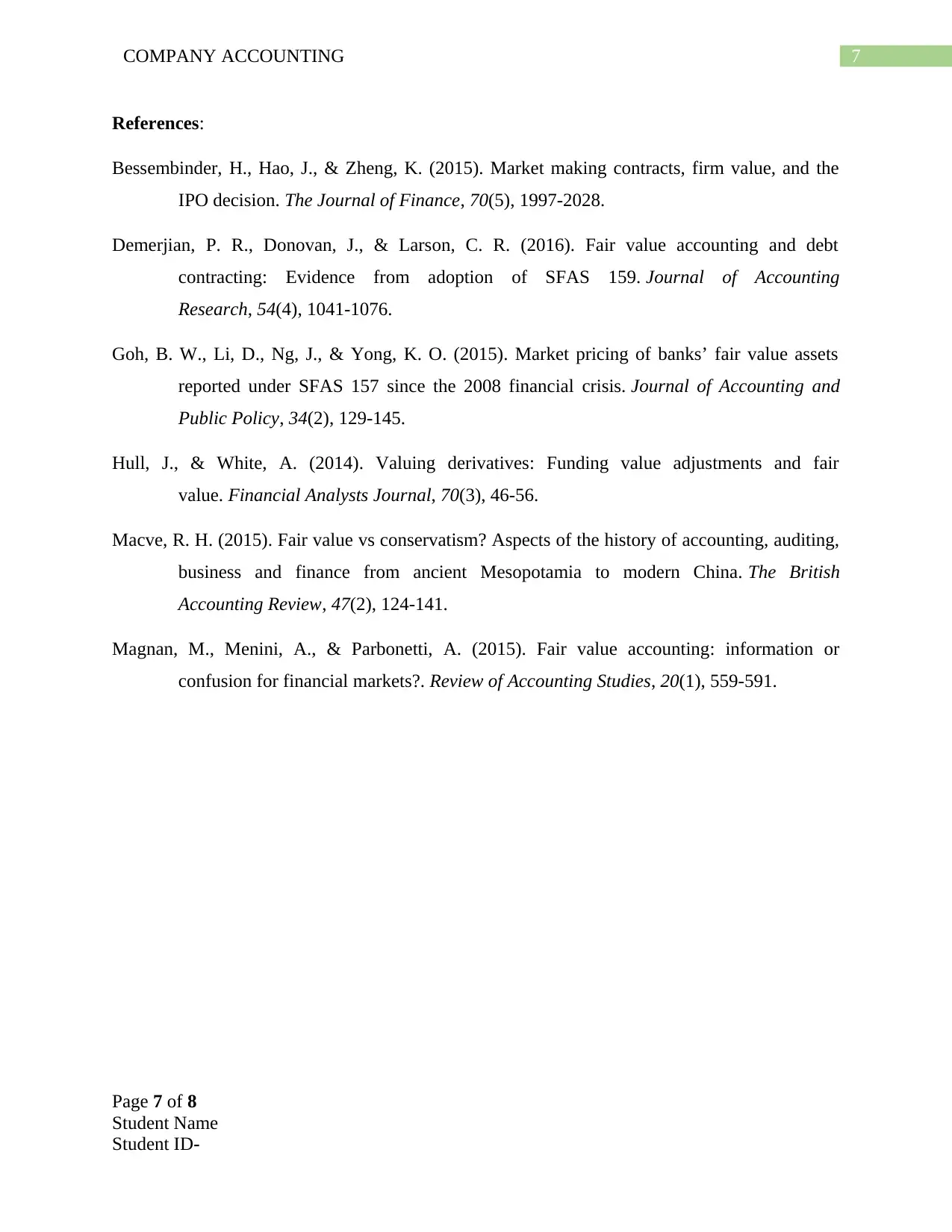

This assignment delves into various aspects of company accounting, focusing on the cost model and fair value concepts. It includes a detailed examination of journal entries, depreciation calculations, and the treatment of revaluation gains and losses. The assignment identifies and rectifies errors in provided journal entries related to asset revaluation, demonstrating the correct accounting treatment for accumulated depreciation and revaluation losses. Furthermore, it addresses the accounting for impairment losses, including the determination of recoverable amounts and the recognition of impairment losses in the financial statements. The document also covers the subsequent depreciation of revalued assets and the transfer of revaluation gains to the revaluation reserve and statement of comprehensive income. Desklib provides students with access to this solved assignment and other valuable study resources.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.