Cost and Performance Management in Tourism and Hospitality Industry

VerifiedAdded on 2023/06/11

|11

|2425

|449

Report

AI Summary

This report provides an analysis of cost and revenue management within the hospitality industry, focusing on cost drivers, strategic pricing, revenue management, cost control techniques, and analytical reasoning. Using the case study of 'Event Hospitality & Entertainment Limited,' the report identifies fixed and variable costs, performs a vertical analysis of the income statement, and offers recommendations for increasing sales by reducing costs. Key findings highlight the significance of housekeeping expenses and propose strategies to optimize resource allocation based on occupancy rates, ultimately aiming to improve gross margins and profitability. This document is available on Desklib, a platform offering a wide range of academic resources and study tools for students.

Running head: COST AND PERFORMANCE MANAGEMENT IN TOURISM AND

HOSPITALITY

Cost and Performance Management in Tourism and Hospitality

Name of Student:

Name of University:

Author’s Note:

HOSPITALITY

Cost and Performance Management in Tourism and Hospitality

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

Table of Contents

Introduction......................................................................................................................................2

Cost Driver and Cost Behaviour......................................................................................................2

Vertical analysis...............................................................................................................................0

Marketing proposal implementation................................................................................................0

Conclusion.......................................................................................................................................2

References........................................................................................................................................3

Table of Contents

Introduction......................................................................................................................................2

Cost Driver and Cost Behaviour......................................................................................................2

Vertical analysis...............................................................................................................................0

Marketing proposal implementation................................................................................................0

Conclusion.......................................................................................................................................2

References........................................................................................................................................3

2COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

Introduction

The main assertions of the report are based on understanding of cost and revenue

management in hospitality industry. The concepts included for the assertions include cost,

strategic pricing, revenue management, cost control techniques and analytical reasonings. Some

of the main discussion of the computational aspect are based on case study of “Event Hospitality

& Entertainment Limited”. The report has been segregated into three parts. The first section of

the report deals with excerpt taken from the income statement for evaluating and identifying the

cost drivers and differentiating them as per fixed and variable costs. The second part of the report

has investigated the income statement and presented a vertical analysis is thereby stating the

recommendation for the business on how they will be able to increase the business sales by

reducing cost simultaneously. The final section has emphasised on the cost drivers and suggest

which should be adopted by the business (Kapić, 2014).

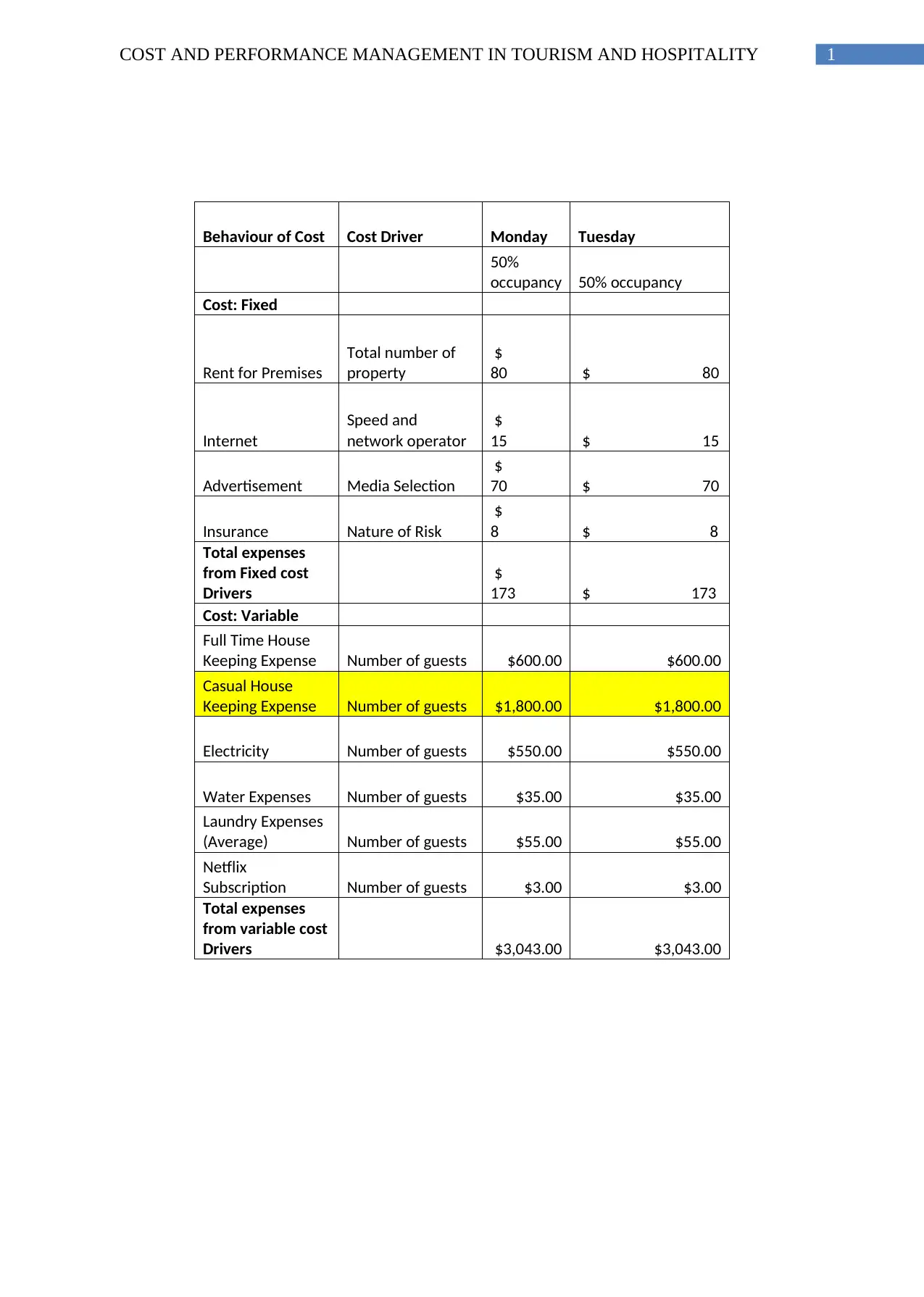

Cost Driver and Cost Behaviour

The interpretation of information of the income statement has identified the fixed cost for

hotel as “rent for premises, Internet, advertisement and insurance”. The rationale of selecting

these items as fixed cost is due to the fact that they remain constant even with an increase or

decrease in the occupancy rate. The main driver for the fixed cost rent is identified with total

number of property in possession of the “Event Hospitality & Entertainment Limited”

(McLaughlin et al., 2014). The main cost driver for Internet is dependent on the speed and

network operator, advertisement is based on media selection such as video advertisement or

picture advertisement. Based on the risk covered by the company the insurance cost will vary

accordingly (Babad et al., 2015). On the other hand, the variable costs such as “full-time

housekeeping expense, casual housekeeping expense, electricity, water expenses, laundry

expenses and Netflix subscription” will completely depend on the total occupancy rate or in

other terms number of guests in the hotel. Henceforth, the cost driver for the variable expenses is

determined with occupancy rate (Mahal & Hossain, 2015).

Introduction

The main assertions of the report are based on understanding of cost and revenue

management in hospitality industry. The concepts included for the assertions include cost,

strategic pricing, revenue management, cost control techniques and analytical reasonings. Some

of the main discussion of the computational aspect are based on case study of “Event Hospitality

& Entertainment Limited”. The report has been segregated into three parts. The first section of

the report deals with excerpt taken from the income statement for evaluating and identifying the

cost drivers and differentiating them as per fixed and variable costs. The second part of the report

has investigated the income statement and presented a vertical analysis is thereby stating the

recommendation for the business on how they will be able to increase the business sales by

reducing cost simultaneously. The final section has emphasised on the cost drivers and suggest

which should be adopted by the business (Kapić, 2014).

Cost Driver and Cost Behaviour

The interpretation of information of the income statement has identified the fixed cost for

hotel as “rent for premises, Internet, advertisement and insurance”. The rationale of selecting

these items as fixed cost is due to the fact that they remain constant even with an increase or

decrease in the occupancy rate. The main driver for the fixed cost rent is identified with total

number of property in possession of the “Event Hospitality & Entertainment Limited”

(McLaughlin et al., 2014). The main cost driver for Internet is dependent on the speed and

network operator, advertisement is based on media selection such as video advertisement or

picture advertisement. Based on the risk covered by the company the insurance cost will vary

accordingly (Babad et al., 2015). On the other hand, the variable costs such as “full-time

housekeeping expense, casual housekeeping expense, electricity, water expenses, laundry

expenses and Netflix subscription” will completely depend on the total occupancy rate or in

other terms number of guests in the hotel. Henceforth, the cost driver for the variable expenses is

determined with occupancy rate (Mahal & Hossain, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

Behaviour of Cost Cost Driver Monday Tuesday Wednesday Thursday Friday Saturday Sunday

50%

occupancy

50%

occupancy

75%

occupancy

75%

occupancy

100%

occupancy

100%

occupancy

100%

occupancy

Cost: Fixed

Rent for Premises

Total number of

property

$

80

$

80

$

80 $ 80 $ 80 $ 80 $ 80

Internet

Speed and

network

operator

$

15

$

15

$

15 $ 15 $ 15 $ 15 $ 15

Advertisement Media Selection

$

70

$

70

$

70 $ 70 $ 70 $ 70 $ 70

Insurance Nature of Risk

$

8

$

8

$

8

$

8

$

8

$

8

$

8

Total expenses from

Fixed cost Drivers

$

173

$

173

$

173

$

173

$

173

$

173

$

173

Cost: Variable

Full Time House Keeping

Expense

Number of

guests $600.00 $600.00 $1,200.00 $1,200.00 $1,200.00 $1,200.00 $1,200.00

Casual House Keeping

Expense

Number of

guests $2,700.00 $2,700.00 $2,400.00 $2,400.00 $2,400.00 $2,400.00 $2,400.00

Electricity

Number of

guests $550.00 $550.00 $850.00 $850.00 $1,250.00 $1,250.00 $1,250.00

Water Expenses

Number of

guests $35.00 $35.00 $50.00 $50.00 $150.00 $150.00 $150.00

Laundry Expenses

(Average)

Number of

guests $55.00 $55.00 $85.00 $85.00 $150.00 $150.00 $150.00

Netflix Subscription

Number of

guests $3.00 $3.00 $3.00 $3.00 $3.00 $33.00 $3.00

Total expenses from

variable cost Drivers $3,943.00 $3,943.00 $4,588.00 $4,588.00 $5,153.00 $5,183.00 $5,153.00

Behaviour of Cost Cost Driver Monday Tuesday Wednesday Thursday Friday Saturday Sunday

50%

occupancy

50%

occupancy

75%

occupancy

75%

occupancy

100%

occupancy

100%

occupancy

100%

occupancy

Cost: Fixed

Rent for Premises

Total number of

property

$

80

$

80

$

80 $ 80 $ 80 $ 80 $ 80

Internet

Speed and

network

operator

$

15

$

15

$

15 $ 15 $ 15 $ 15 $ 15

Advertisement Media Selection

$

70

$

70

$

70 $ 70 $ 70 $ 70 $ 70

Insurance Nature of Risk

$

8

$

8

$

8

$

8

$

8

$

8

$

8

Total expenses from

Fixed cost Drivers

$

173

$

173

$

173

$

173

$

173

$

173

$

173

Cost: Variable

Full Time House Keeping

Expense

Number of

guests $600.00 $600.00 $1,200.00 $1,200.00 $1,200.00 $1,200.00 $1,200.00

Casual House Keeping

Expense

Number of

guests $2,700.00 $2,700.00 $2,400.00 $2,400.00 $2,400.00 $2,400.00 $2,400.00

Electricity

Number of

guests $550.00 $550.00 $850.00 $850.00 $1,250.00 $1,250.00 $1,250.00

Water Expenses

Number of

guests $35.00 $35.00 $50.00 $50.00 $150.00 $150.00 $150.00

Laundry Expenses

(Average)

Number of

guests $55.00 $55.00 $85.00 $85.00 $150.00 $150.00 $150.00

Netflix Subscription

Number of

guests $3.00 $3.00 $3.00 $3.00 $3.00 $33.00 $3.00

Total expenses from

variable cost Drivers $3,943.00 $3,943.00 $4,588.00 $4,588.00 $5,153.00 $5,183.00 $5,153.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

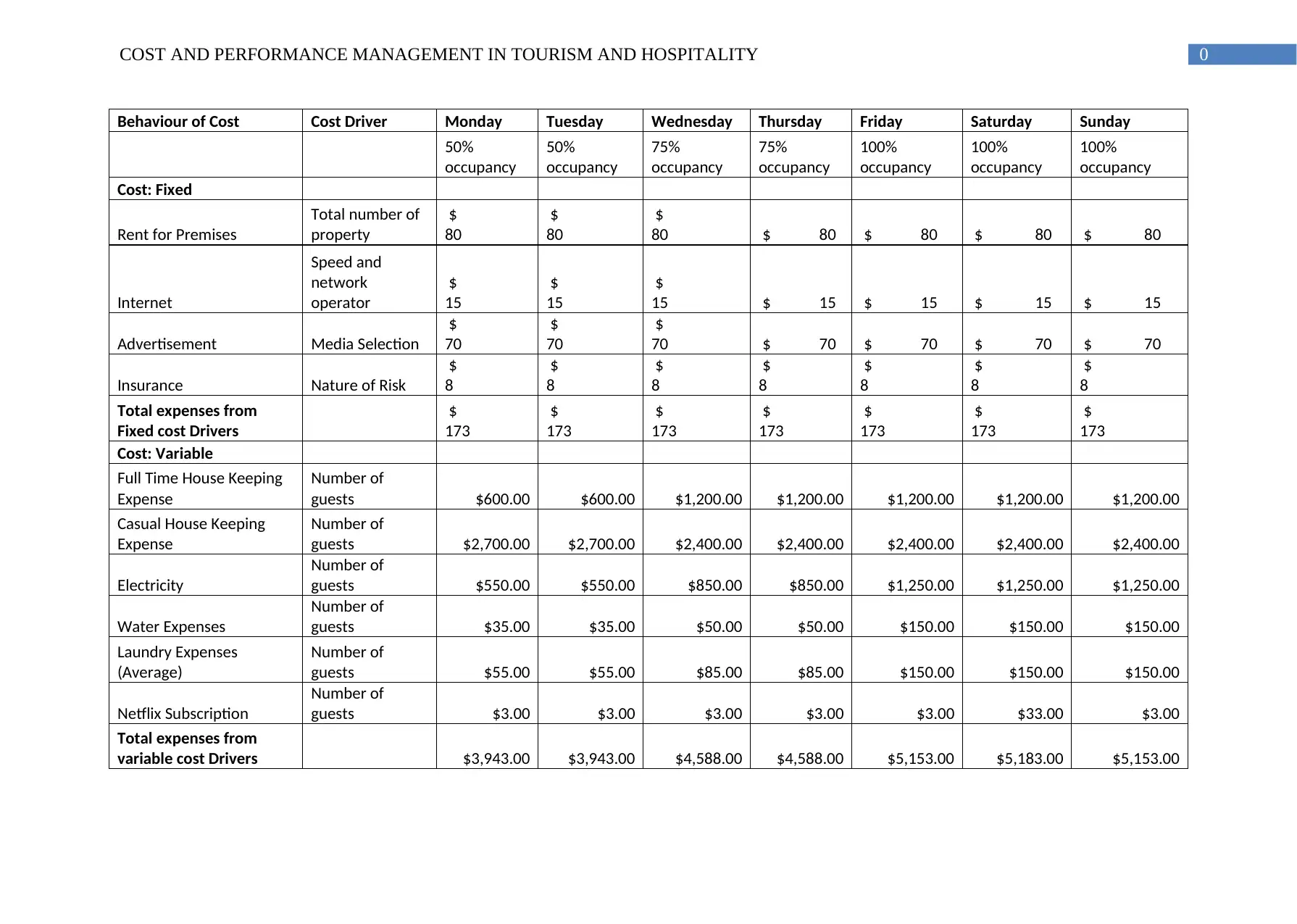

Vertical analysis

The vertical analysis performed by the excerpts taken from income statement has been

considered with the expenses, gross margin and profit before tax as a percentage of total revenue

on by the company in each day of the week. This analysis has clearly shown the net profit or loss

generated out of the revenue and the proportion of expense incurred in terms of total revenue

earned on each day of the week (Kapian & Anderson, 2014). Based on the various analysis and

synthesis of information in a quantitative manner it can be clearly seen that the housekeeping

expenses are the most significant expense incurred by the company in revenue generation. This

is inferred with housekeeping expenses percentage of 92.47% from Monday to Tuesday, 67.25%

from Wednesday to and Thursday50.44% from Friday to Sunday (NICE, 2016).

Vertical analysis

The vertical analysis performed by the excerpts taken from income statement has been

considered with the expenses, gross margin and profit before tax as a percentage of total revenue

on by the company in each day of the week. This analysis has clearly shown the net profit or loss

generated out of the revenue and the proportion of expense incurred in terms of total revenue

earned on each day of the week (Kapian & Anderson, 2014). Based on the various analysis and

synthesis of information in a quantitative manner it can be clearly seen that the housekeeping

expenses are the most significant expense incurred by the company in revenue generation. This

is inferred with housekeeping expenses percentage of 92.47% from Monday to Tuesday, 67.25%

from Wednesday to and Thursday50.44% from Friday to Sunday (NICE, 2016).

0COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

Vertical Analysis of Event

Hospitality &

Entertainment Limited

Income Statement

Particul

ars

Mond

ay

Percent

age

Particul

ars

Tues

day

Percent

age

Particul

ars

Wednes

day

Percent

age

Particul

ars

Thurs

day

Percent

age

Particul

ars

Frid

ay

Percent

age

Particul

ars

Satur

day

Percent

age

Particul

ars

Sund

ay

Percent

age

Revenu

e

3568.

75

100.00

%

Revenu

e

3568.

75

100.00

%

Revenu

e

5,353.1

3

100.00

%

Revenu

e

5,353.

13

100.00

%

Revenu

e

713

7.5

100.00

%

Revenu

e

7137.

5

100.00

%

Revenu

e

7137

.5

100.00

%

House

Keepin

g

Expens

es 3300 92.47%

House

Keepin

g

Expens

es 3300 92.47%

House

Keepin

g

Expens

es 3600 67.25%

House

Keepin

g

Expens

es 3600

100.88

%

House

Keepin

g

Expens

es

360

0

100.88

%

House

Keepin

g

Expens

es 3600

100.88

%

House

Keepin

g

Expens

es 3600

100.88

%

Gross

Margin

268.7

5 7.53%

Gross

Margin

268.7

5 7.53%

Gross

Margin 1753.13 49.12%

Gross

Margin

1753.

13 32.75%

Gross

Margin

353

7.5 49.56%

Gross

Margin

3537.

5 49.56%

Gross

Margin

3537

.5 49.56%

Operati

ng

Expens

es 816 22.87%

Operati

ng

Expens

es 816 22.87%

Operati

ng

Expens

es 1161 21.69%

Operati

ng

Expens

es 1161 21.69%

Operati

ng

Expens

es

172

6 24.18%

Operati

ng

Expens

es 1756 24.60%

Operati

ng

Expens

es 1726 24.18%

Finance

Cost 0 0.00%

Finance

Cost 0 0.00%

Finance

Cost 0 0.00%

Finance

Cost 0 0.00%

Finance

Cost 0 0.00%

Finance

Cost 5 0.14%

Finance

Cost 0 0.00%

Profit

Before

Tax

-

547.2

5 -15.33%

Profit

Before

Tax

-

547.2

5 -15.33%

Profit

Before

Tax 592.13 11.06%

Profit

Before

Tax

592.1

3 11.06%

Profit

Before

Tax

181

1.5 25.38%

Profit

Before

Tax

1781.

5 24.96%

Profit

Before

Tax

1811

.5 25.38%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 5 0.14%

Income

Tax

Expens

es 0 0.00%

Profit

of the

day

-

547.2

5 -15.33%

Profit

of the

day

-

547.2

5 -15.33%

Profit

of the

day 592.13 11.06%

Profit

of the

day

592.1

3 11.06%

Profit

of the

day

181

1.5 25.38%

Profit

of the

day

1781.

5 24.96%

Profit

of the

day

1811

.5 25.38%

Vertical Analysis of Event

Hospitality &

Entertainment Limited

Income Statement

Particul

ars

Mond

ay

Percent

age

Particul

ars

Tues

day

Percent

age

Particul

ars

Wednes

day

Percent

age

Particul

ars

Thurs

day

Percent

age

Particul

ars

Frid

ay

Percent

age

Particul

ars

Satur

day

Percent

age

Particul

ars

Sund

ay

Percent

age

Revenu

e

3568.

75

100.00

%

Revenu

e

3568.

75

100.00

%

Revenu

e

5,353.1

3

100.00

%

Revenu

e

5,353.

13

100.00

%

Revenu

e

713

7.5

100.00

%

Revenu

e

7137.

5

100.00

%

Revenu

e

7137

.5

100.00

%

House

Keepin

g

Expens

es 3300 92.47%

House

Keepin

g

Expens

es 3300 92.47%

House

Keepin

g

Expens

es 3600 67.25%

House

Keepin

g

Expens

es 3600

100.88

%

House

Keepin

g

Expens

es

360

0

100.88

%

House

Keepin

g

Expens

es 3600

100.88

%

House

Keepin

g

Expens

es 3600

100.88

%

Gross

Margin

268.7

5 7.53%

Gross

Margin

268.7

5 7.53%

Gross

Margin 1753.13 49.12%

Gross

Margin

1753.

13 32.75%

Gross

Margin

353

7.5 49.56%

Gross

Margin

3537.

5 49.56%

Gross

Margin

3537

.5 49.56%

Operati

ng

Expens

es 816 22.87%

Operati

ng

Expens

es 816 22.87%

Operati

ng

Expens

es 1161 21.69%

Operati

ng

Expens

es 1161 21.69%

Operati

ng

Expens

es

172

6 24.18%

Operati

ng

Expens

es 1756 24.60%

Operati

ng

Expens

es 1726 24.18%

Finance

Cost 0 0.00%

Finance

Cost 0 0.00%

Finance

Cost 0 0.00%

Finance

Cost 0 0.00%

Finance

Cost 0 0.00%

Finance

Cost 5 0.14%

Finance

Cost 0 0.00%

Profit

Before

Tax

-

547.2

5 -15.33%

Profit

Before

Tax

-

547.2

5 -15.33%

Profit

Before

Tax 592.13 11.06%

Profit

Before

Tax

592.1

3 11.06%

Profit

Before

Tax

181

1.5 25.38%

Profit

Before

Tax

1781.

5 24.96%

Profit

Before

Tax

1811

.5 25.38%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 0 0.00%

Income

Tax

Expens

es 5 0.14%

Income

Tax

Expens

es 0 0.00%

Profit

of the

day

-

547.2

5 -15.33%

Profit

of the

day

-

547.2

5 -15.33%

Profit

of the

day 592.13 11.06%

Profit

of the

day

592.1

3 11.06%

Profit

of the

day

181

1.5 25.38%

Profit

of the

day

1781.

5 24.96%

Profit

of the

day

1811

.5 25.38%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

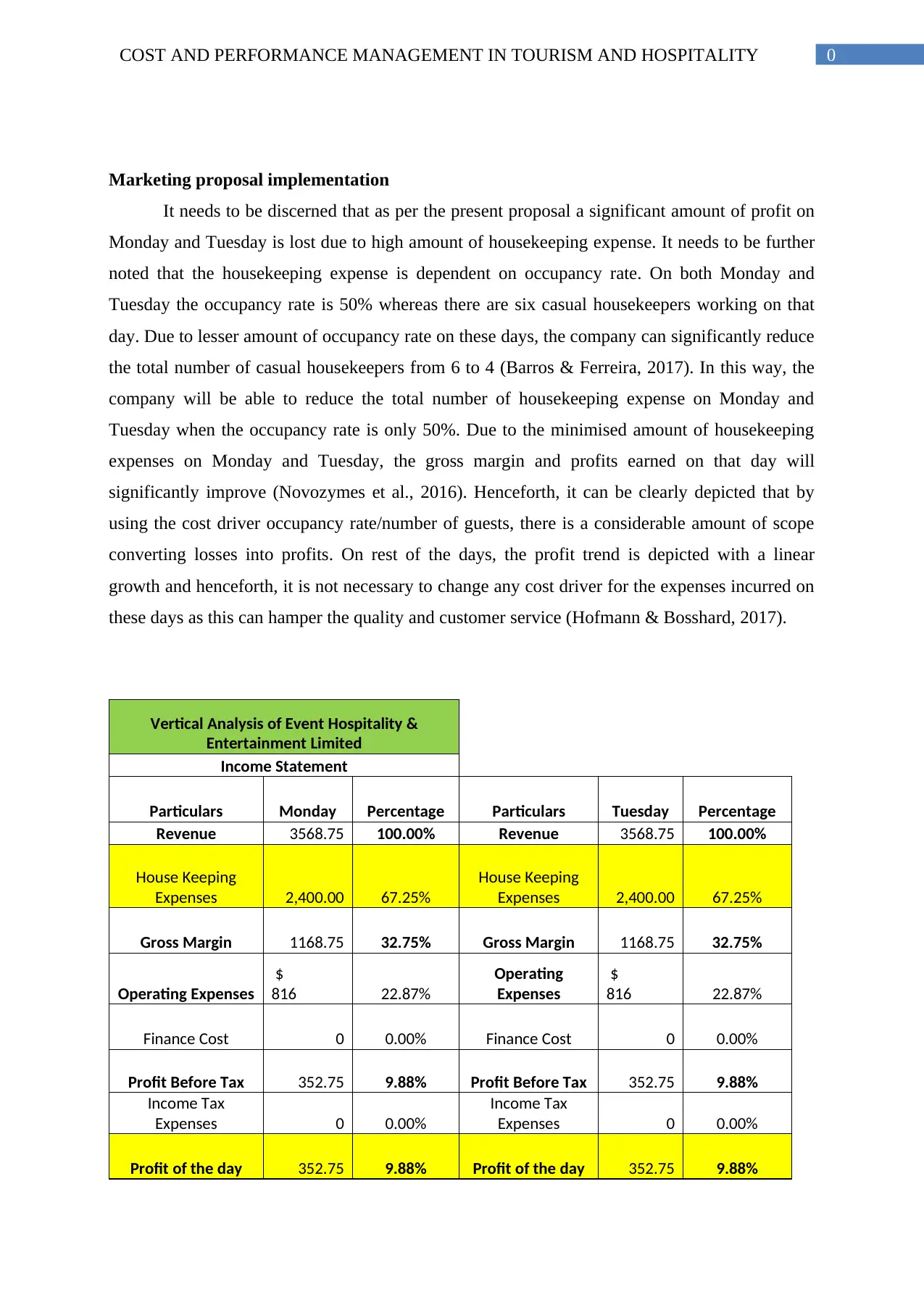

Marketing proposal implementation

It needs to be discerned that as per the present proposal a significant amount of profit on

Monday and Tuesday is lost due to high amount of housekeeping expense. It needs to be further

noted that the housekeeping expense is dependent on occupancy rate. On both Monday and

Tuesday the occupancy rate is 50% whereas there are six casual housekeepers working on that

day. Due to lesser amount of occupancy rate on these days, the company can significantly reduce

the total number of casual housekeepers from 6 to 4 (Barros & Ferreira, 2017). In this way, the

company will be able to reduce the total number of housekeeping expense on Monday and

Tuesday when the occupancy rate is only 50%. Due to the minimised amount of housekeeping

expenses on Monday and Tuesday, the gross margin and profits earned on that day will

significantly improve (Novozymes et al., 2016). Henceforth, it can be clearly depicted that by

using the cost driver occupancy rate/number of guests, there is a considerable amount of scope

converting losses into profits. On rest of the days, the profit trend is depicted with a linear

growth and henceforth, it is not necessary to change any cost driver for the expenses incurred on

these days as this can hamper the quality and customer service (Hofmann & Bosshard, 2017).

Vertical Analysis of Event Hospitality &

Entertainment Limited

Income Statement

Particulars Monday Percentage Particulars Tuesday Percentage

Revenue 3568.75 100.00% Revenue 3568.75 100.00%

House Keeping

Expenses 2,400.00 67.25%

House Keeping

Expenses 2,400.00 67.25%

Gross Margin 1168.75 32.75% Gross Margin 1168.75 32.75%

Operating Expenses

$

816 22.87%

Operating

Expenses

$

816 22.87%

Finance Cost 0 0.00% Finance Cost 0 0.00%

Profit Before Tax 352.75 9.88% Profit Before Tax 352.75 9.88%

Income Tax

Expenses 0 0.00%

Income Tax

Expenses 0 0.00%

Profit of the day 352.75 9.88% Profit of the day 352.75 9.88%

Marketing proposal implementation

It needs to be discerned that as per the present proposal a significant amount of profit on

Monday and Tuesday is lost due to high amount of housekeeping expense. It needs to be further

noted that the housekeeping expense is dependent on occupancy rate. On both Monday and

Tuesday the occupancy rate is 50% whereas there are six casual housekeepers working on that

day. Due to lesser amount of occupancy rate on these days, the company can significantly reduce

the total number of casual housekeepers from 6 to 4 (Barros & Ferreira, 2017). In this way, the

company will be able to reduce the total number of housekeeping expense on Monday and

Tuesday when the occupancy rate is only 50%. Due to the minimised amount of housekeeping

expenses on Monday and Tuesday, the gross margin and profits earned on that day will

significantly improve (Novozymes et al., 2016). Henceforth, it can be clearly depicted that by

using the cost driver occupancy rate/number of guests, there is a considerable amount of scope

converting losses into profits. On rest of the days, the profit trend is depicted with a linear

growth and henceforth, it is not necessary to change any cost driver for the expenses incurred on

these days as this can hamper the quality and customer service (Hofmann & Bosshard, 2017).

Vertical Analysis of Event Hospitality &

Entertainment Limited

Income Statement

Particulars Monday Percentage Particulars Tuesday Percentage

Revenue 3568.75 100.00% Revenue 3568.75 100.00%

House Keeping

Expenses 2,400.00 67.25%

House Keeping

Expenses 2,400.00 67.25%

Gross Margin 1168.75 32.75% Gross Margin 1168.75 32.75%

Operating Expenses

$

816 22.87%

Operating

Expenses

$

816 22.87%

Finance Cost 0 0.00% Finance Cost 0 0.00%

Profit Before Tax 352.75 9.88% Profit Before Tax 352.75 9.88%

Income Tax

Expenses 0 0.00%

Income Tax

Expenses 0 0.00%

Profit of the day 352.75 9.88% Profit of the day 352.75 9.88%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

Behaviour of Cost Cost Driver Monday Tuesday

50%

occupancy 50% occupancy

Cost: Fixed

Rent for Premises

Total number of

property

$

80 $ 80

Internet

Speed and

network operator

$

15 $ 15

Advertisement Media Selection

$

70 $ 70

Insurance Nature of Risk

$

8 $ 8

Total expenses

from Fixed cost

Drivers

$

173 $ 173

Cost: Variable

Full Time House

Keeping Expense Number of guests $600.00 $600.00

Casual House

Keeping Expense Number of guests $1,800.00 $1,800.00

Electricity Number of guests $550.00 $550.00

Water Expenses Number of guests $35.00 $35.00

Laundry Expenses

(Average) Number of guests $55.00 $55.00

Netflix

Subscription Number of guests $3.00 $3.00

Total expenses

from variable cost

Drivers $3,043.00 $3,043.00

Behaviour of Cost Cost Driver Monday Tuesday

50%

occupancy 50% occupancy

Cost: Fixed

Rent for Premises

Total number of

property

$

80 $ 80

Internet

Speed and

network operator

$

15 $ 15

Advertisement Media Selection

$

70 $ 70

Insurance Nature of Risk

$

8 $ 8

Total expenses

from Fixed cost

Drivers

$

173 $ 173

Cost: Variable

Full Time House

Keeping Expense Number of guests $600.00 $600.00

Casual House

Keeping Expense Number of guests $1,800.00 $1,800.00

Electricity Number of guests $550.00 $550.00

Water Expenses Number of guests $35.00 $35.00

Laundry Expenses

(Average) Number of guests $55.00 $55.00

Netflix

Subscription Number of guests $3.00 $3.00

Total expenses

from variable cost

Drivers $3,043.00 $3,043.00

2COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

Conclusion

The various depictions made on Cost Driver and Cost Behaviour has stated that the

rationale of selecting fixed cost is due to the fact that they remain constant even with an increase

or decrease in the occupancy rate. The main driver for the fixed cost rent is identified with total

number of property in possession of the “Event Hospitality & Entertainment Limited”.

Additionally, the various analysis and synthesis of information in a quantitative manner it can be

clearly seen that the housekeeping expenses are the most significant expense incurred by the

company in revenue generation. The company can significantly reduce the total number of casual

housekeepers from 6 to 4 on Monday and Tuesday. Due to the minimised amount of

housekeeping expenses on Monday and Tuesday, the gross margin and profits earned on that day

will significantly improve.

Conclusion

The various depictions made on Cost Driver and Cost Behaviour has stated that the

rationale of selecting fixed cost is due to the fact that they remain constant even with an increase

or decrease in the occupancy rate. The main driver for the fixed cost rent is identified with total

number of property in possession of the “Event Hospitality & Entertainment Limited”.

Additionally, the various analysis and synthesis of information in a quantitative manner it can be

clearly seen that the housekeeping expenses are the most significant expense incurred by the

company in revenue generation. The company can significantly reduce the total number of casual

housekeepers from 6 to 4 on Monday and Tuesday. Due to the minimised amount of

housekeeping expenses on Monday and Tuesday, the gross margin and profits earned on that day

will significantly improve.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

References

Babad, Y. M., Balachandran, B. V., BITTENCOURT, O. N. D. A. S., Bornia, A. C., Botelho, E.,

Brimson, J. A., … Lembeck, M. (2015). Activity-based costing for hospitals. The

Accounting Review, 5(3), 3–34. https://doi.org/10.1111/j.1467-6281.2012.00366.x

Barros, R. S., & Ferreira, A. M. D. S. da C. (2017). Time-driven activity-based costing.

Qualitative Research in Accounting & Management, 14(1), 2–20.

https://doi.org/10.1108/QRAM-10-2015-0095

Hofmann, E., & Bosshard, J. (2017). Supply chain management and activity-based costing.

International Journal of Physical Distribution & Logistics Management, 47(8), 712–735.

https://doi.org/10.1108/IJPDLM-04-2017-0158

Kapian, R. S., & Anderson, S. R. (2014). Rethinking activity-based costing. Technology.

Retrieved from http://www.homeworkmarket.com/sites/default/files/q1/26/11/abc-

_company_article.pdf

Kapić, J. (2014). Activity Based Costing - ABC. Business Consultant / Poslovni Konsultant,

6(32), 9–16. Retrieved from http://poslovnikonsultant.ba/

Mahal, I., & Hossain, M. A. (2015). Activity-Based Costing (ABC) – An Effective Tool for

Better Management. Research Journal of Finance and AccountingOnline), 6(4), 2222–

2847.

McLaughlin, N., Burke, M. A., Setlur, N. P., Niedzwiecki, D. R., Kaplan, A. L., Saigal, C., …

Kaplan, R. S. (2014). Time-driven activity-based costing: a driver for provider

engagement in costing activities and redesign initiatives. Neurosurgical Focus, 37(5), E3.

https://doi.org/10.3171/2014.8.FOCUS14381

NICE. (2016). Costing Report. Rehabilitation after Critical Illness Costing Report, (February),

1–39. Retrieved from

www.nice.org.uk/guidance/CG155%0Awww.nice.org.uk/CG83%5Cnwww.nice.org.uk

Novozymes, Børsen, Drury, C., Brealey, R. A., Myres, S. C., Allen, F., … Raiborn, C. a. (2016).

Time-driven activity-based costing. Journal of Accounting Research, 18(2), 23–51.

https://doi.org/10.1287/mnsc.1100.1175

References

Babad, Y. M., Balachandran, B. V., BITTENCOURT, O. N. D. A. S., Bornia, A. C., Botelho, E.,

Brimson, J. A., … Lembeck, M. (2015). Activity-based costing for hospitals. The

Accounting Review, 5(3), 3–34. https://doi.org/10.1111/j.1467-6281.2012.00366.x

Barros, R. S., & Ferreira, A. M. D. S. da C. (2017). Time-driven activity-based costing.

Qualitative Research in Accounting & Management, 14(1), 2–20.

https://doi.org/10.1108/QRAM-10-2015-0095

Hofmann, E., & Bosshard, J. (2017). Supply chain management and activity-based costing.

International Journal of Physical Distribution & Logistics Management, 47(8), 712–735.

https://doi.org/10.1108/IJPDLM-04-2017-0158

Kapian, R. S., & Anderson, S. R. (2014). Rethinking activity-based costing. Technology.

Retrieved from http://www.homeworkmarket.com/sites/default/files/q1/26/11/abc-

_company_article.pdf

Kapić, J. (2014). Activity Based Costing - ABC. Business Consultant / Poslovni Konsultant,

6(32), 9–16. Retrieved from http://poslovnikonsultant.ba/

Mahal, I., & Hossain, M. A. (2015). Activity-Based Costing (ABC) – An Effective Tool for

Better Management. Research Journal of Finance and AccountingOnline), 6(4), 2222–

2847.

McLaughlin, N., Burke, M. A., Setlur, N. P., Niedzwiecki, D. R., Kaplan, A. L., Saigal, C., …

Kaplan, R. S. (2014). Time-driven activity-based costing: a driver for provider

engagement in costing activities and redesign initiatives. Neurosurgical Focus, 37(5), E3.

https://doi.org/10.3171/2014.8.FOCUS14381

NICE. (2016). Costing Report. Rehabilitation after Critical Illness Costing Report, (February),

1–39. Retrieved from

www.nice.org.uk/guidance/CG155%0Awww.nice.org.uk/CG83%5Cnwww.nice.org.uk

Novozymes, Børsen, Drury, C., Brealey, R. A., Myres, S. C., Allen, F., … Raiborn, C. a. (2016).

Time-driven activity-based costing. Journal of Accounting Research, 18(2), 23–51.

https://doi.org/10.1287/mnsc.1100.1175

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COST AND PERFORMANCE MANAGEMENT IN TOURISM AND HOSPITALITY

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.