Cost and Performance Management for Tourism and Hospitality - Analysis

VerifiedAdded on 2021/02/20

|10

|2700

|161

Report

AI Summary

This report provides a detailed analysis of cost and performance management within the tourism and hospitality industry, focusing on two distinct events. It categorizes costs, evaluates cost drivers, and differentiates cost-related pricing and control techniques. The analysis includes a breakdown of expenses, comparing cost shares and values across events, with key drivers identified as decorations and lighting. The report also explores pricing strategies, calculates break-even points, and suggests the best alternative for maximizing profitability, concluding that Event 1 seems more profitable due to the higher markup. The study uses tables to present data and calculations, offering a comprehensive overview of cost management practices and their impact on profitability within the industry.

COST AND PERFORMANCE MANAGEMENT FOR TOURISM AND

HOSPITALITY

HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

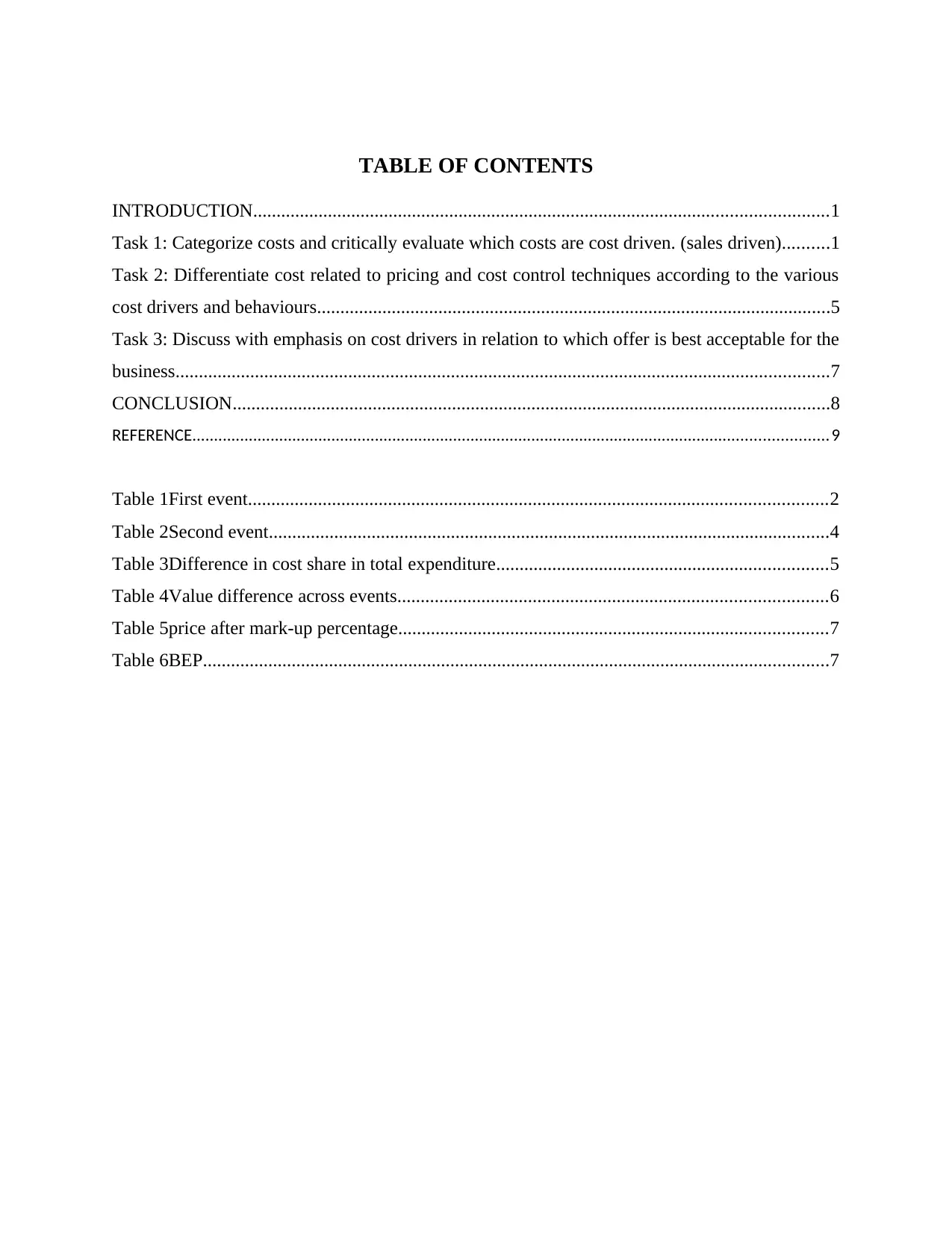

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Task 1: Categorize costs and critically evaluate which costs are cost driven. (sales driven)..........1

Task 2: Differentiate cost related to pricing and cost control techniques according to the various

cost drivers and behaviours..............................................................................................................5

Task 3: Discuss with emphasis on cost drivers in relation to which offer is best acceptable for the

business............................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCE..................................................................................................................................................9

Table 1First event............................................................................................................................2

Table 2Second event........................................................................................................................4

Table 3Difference in cost share in total expenditure.......................................................................5

Table 4Value difference across events............................................................................................6

Table 5price after mark-up percentage............................................................................................7

Table 6BEP......................................................................................................................................7

INTRODUCTION...........................................................................................................................1

Task 1: Categorize costs and critically evaluate which costs are cost driven. (sales driven)..........1

Task 2: Differentiate cost related to pricing and cost control techniques according to the various

cost drivers and behaviours..............................................................................................................5

Task 3: Discuss with emphasis on cost drivers in relation to which offer is best acceptable for the

business............................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCE..................................................................................................................................................9

Table 1First event............................................................................................................................2

Table 2Second event........................................................................................................................4

Table 3Difference in cost share in total expenditure.......................................................................5

Table 4Value difference across events............................................................................................6

Table 5price after mark-up percentage............................................................................................7

Table 6BEP......................................................................................................................................7

INTRODUCTION

Cost is the one of main factor which is given due importance by the business firms. This is

because its control lead to increase in business profit. Firms adopt multiple approaches to control

cost of the product at the workplace. In the current report two events are analysed and in respect

to them specific analysis is done through calculation and comparison of values. At end of the

report break even level is identified and best alternative is suggested that can be adopted by the

firm to earn more profit in the business.

Task 1: Categorize costs and critically evaluate which costs are cost driven.

(sales driven)

Categorize the costs.

Classification of costs refers to grouping the expenses according to the characteristics that

are similar. In the field of costing, there are different ways to categorize cost on the basis of

functions, nature, traceability etc.

Classification on the basis of nature : Under this, cost can be classified into different

categorize like cost of material, labour cost and other expenses.

Material cost - It refers to the cost related with material that organization uses in

production of goods. It can be divided into other parts such as cost of packaging of the

material, cost of raw material etc.

Labour expenses - It is related with wages and salary of the labour (Priya., C., 2018).

Organization have to pay salary and wages to employees for performing different tasks.

Such as salary paid to employees for providing various services.

Expenses - This includes cost other than cost of material and labour that firm has to incur

for effective marketing of goods. Such as expenses related with social media marketing

through Instagram, Facebook, Television etc.

Classification on the basis of functions: Under this, the cost are grouped on the basis of

different functions such as selling, production, administration etc.

Production costs- Cost of production refers to the expenses related with actual

manufacturing of the products (Lomas, J., 2018). These expenses are necessary in order

to manufacture the goods.

1

Cost is the one of main factor which is given due importance by the business firms. This is

because its control lead to increase in business profit. Firms adopt multiple approaches to control

cost of the product at the workplace. In the current report two events are analysed and in respect

to them specific analysis is done through calculation and comparison of values. At end of the

report break even level is identified and best alternative is suggested that can be adopted by the

firm to earn more profit in the business.

Task 1: Categorize costs and critically evaluate which costs are cost driven.

(sales driven)

Categorize the costs.

Classification of costs refers to grouping the expenses according to the characteristics that

are similar. In the field of costing, there are different ways to categorize cost on the basis of

functions, nature, traceability etc.

Classification on the basis of nature : Under this, cost can be classified into different

categorize like cost of material, labour cost and other expenses.

Material cost - It refers to the cost related with material that organization uses in

production of goods. It can be divided into other parts such as cost of packaging of the

material, cost of raw material etc.

Labour expenses - It is related with wages and salary of the labour (Priya., C., 2018).

Organization have to pay salary and wages to employees for performing different tasks.

Such as salary paid to employees for providing various services.

Expenses - This includes cost other than cost of material and labour that firm has to incur

for effective marketing of goods. Such as expenses related with social media marketing

through Instagram, Facebook, Television etc.

Classification on the basis of functions: Under this, the cost are grouped on the basis of

different functions such as selling, production, administration etc.

Production costs- Cost of production refers to the expenses related with actual

manufacturing of the products (Lomas, J., 2018). These expenses are necessary in order

to manufacture the goods.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Commercial costs - Commercial cost refers to the total expenses for operating the

enterprise. It includes cost other than manufacturing cost. Such as selling and distribution

expenses, administration cost etc.

Classification by Traceability : It is considered as one of the most important classification of

costs. On the basis of traceability, cost can be classified under two categories. Such as -

Direct cost - It refers to the cost that can be easily associated with cost centres or cost

unit. For example – cost of material, cost of labour that are involved in the process of

manufacturing.

Indirect cost - It refers to the cost that cannot be directly identified with a particular cost

centre or a cost unit (Etkin,, 2016). Example of indirect cost is rent of building, salary of

the manager etc. Therefore, company cannot determine how to ascertain these expenses

to a particular cost unit.

Classification by Normality : Under this, the cost can be classified in two categories such as

normal and abnormal cost (Vuong, 2018). These expenses are generally occur at particular level

of output and under similar set of situations.

Normal cost - It is a part of total cost of production. It refers to the expenses that firm

incurr at normal level of output in similar conditions. These expenses are part of costing

profit and loss of the company.

Abnormal cost - These cost are not incurred by firm at a particular level of output in

given conditions. These costs are profit and loss

Cost driven is term commonly used by cost accountants and business man in order to

highlight specific point. Cost driven refers to the expenditure that play a major role in forming

entire product cost. Small change in relevant cost completely change overall cost of the product.

Hence, while talking about costing main emphasis is laid down on cost drivers.

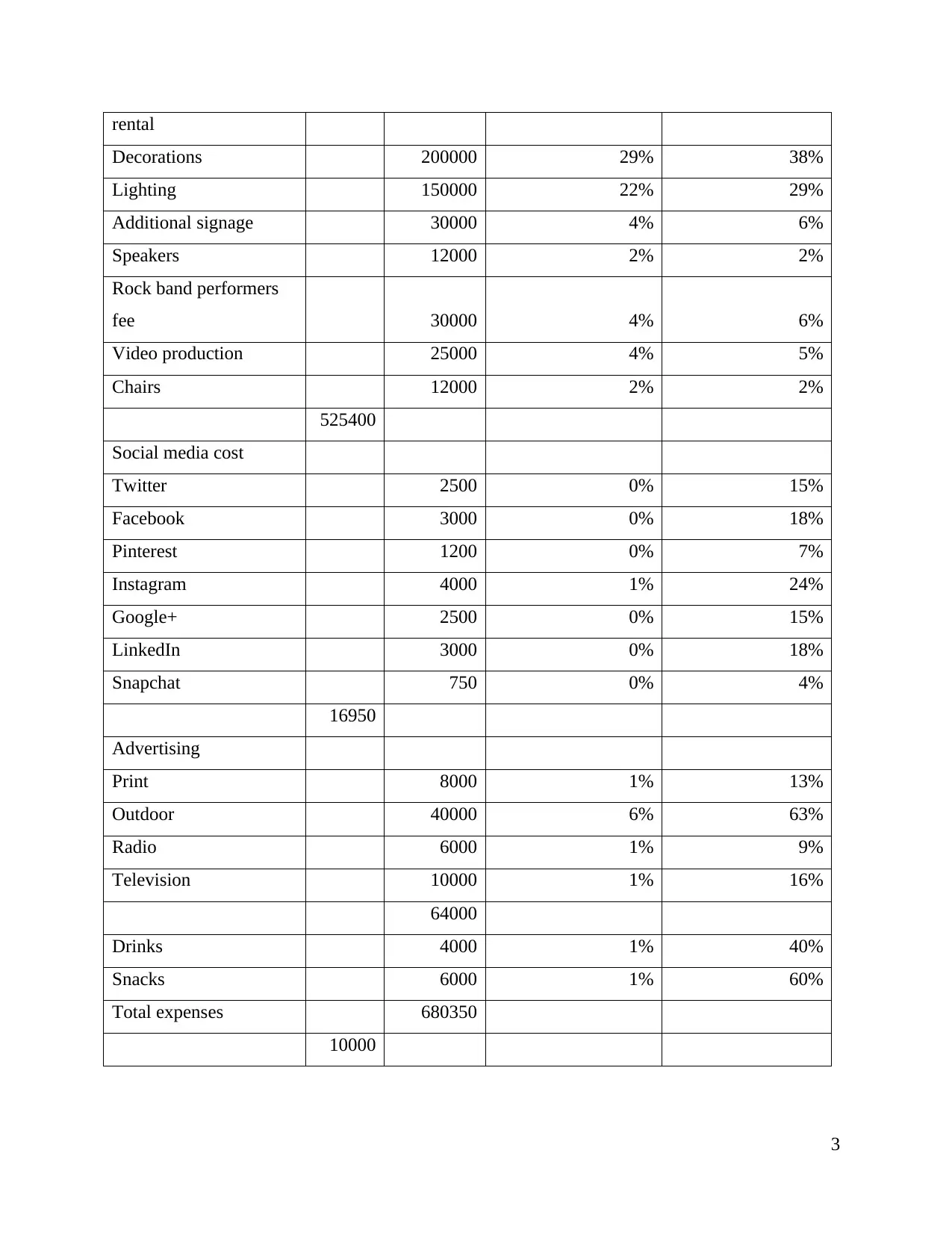

Table 1First event

Elements

Sub

total

Expenditur

e

Share in total

expenses

Share in sub

expenses

Event staff 26400 4% 5%

Different equipment 40000 6% 8%

2

enterprise. It includes cost other than manufacturing cost. Such as selling and distribution

expenses, administration cost etc.

Classification by Traceability : It is considered as one of the most important classification of

costs. On the basis of traceability, cost can be classified under two categories. Such as -

Direct cost - It refers to the cost that can be easily associated with cost centres or cost

unit. For example – cost of material, cost of labour that are involved in the process of

manufacturing.

Indirect cost - It refers to the cost that cannot be directly identified with a particular cost

centre or a cost unit (Etkin,, 2016). Example of indirect cost is rent of building, salary of

the manager etc. Therefore, company cannot determine how to ascertain these expenses

to a particular cost unit.

Classification by Normality : Under this, the cost can be classified in two categories such as

normal and abnormal cost (Vuong, 2018). These expenses are generally occur at particular level

of output and under similar set of situations.

Normal cost - It is a part of total cost of production. It refers to the expenses that firm

incurr at normal level of output in similar conditions. These expenses are part of costing

profit and loss of the company.

Abnormal cost - These cost are not incurred by firm at a particular level of output in

given conditions. These costs are profit and loss

Cost driven is term commonly used by cost accountants and business man in order to

highlight specific point. Cost driven refers to the expenditure that play a major role in forming

entire product cost. Small change in relevant cost completely change overall cost of the product.

Hence, while talking about costing main emphasis is laid down on cost drivers.

Table 1First event

Elements

Sub

total

Expenditur

e

Share in total

expenses

Share in sub

expenses

Event staff 26400 4% 5%

Different equipment 40000 6% 8%

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

rental

Decorations 200000 29% 38%

Lighting 150000 22% 29%

Additional signage 30000 4% 6%

Speakers 12000 2% 2%

Rock band performers

fee 30000 4% 6%

Video production 25000 4% 5%

Chairs 12000 2% 2%

525400

Social media cost

Twitter 2500 0% 15%

Facebook 3000 0% 18%

Pinterest 1200 0% 7%

Instagram 4000 1% 24%

Google+ 2500 0% 15%

LinkedIn 3000 0% 18%

Snapchat 750 0% 4%

16950

Advertising

Print 8000 1% 13%

Outdoor 40000 6% 63%

Radio 6000 1% 9%

Television 10000 1% 16%

64000

Drinks 4000 1% 40%

Snacks 6000 1% 60%

Total expenses 680350

10000

3

Decorations 200000 29% 38%

Lighting 150000 22% 29%

Additional signage 30000 4% 6%

Speakers 12000 2% 2%

Rock band performers

fee 30000 4% 6%

Video production 25000 4% 5%

Chairs 12000 2% 2%

525400

Social media cost

Twitter 2500 0% 15%

Facebook 3000 0% 18%

Pinterest 1200 0% 7%

Instagram 4000 1% 24%

Google+ 2500 0% 15%

LinkedIn 3000 0% 18%

Snapchat 750 0% 4%

16950

Advertising

Print 8000 1% 13%

Outdoor 40000 6% 63%

Radio 6000 1% 9%

Television 10000 1% 16%

64000

Drinks 4000 1% 40%

Snacks 6000 1% 60%

Total expenses 680350

10000

3

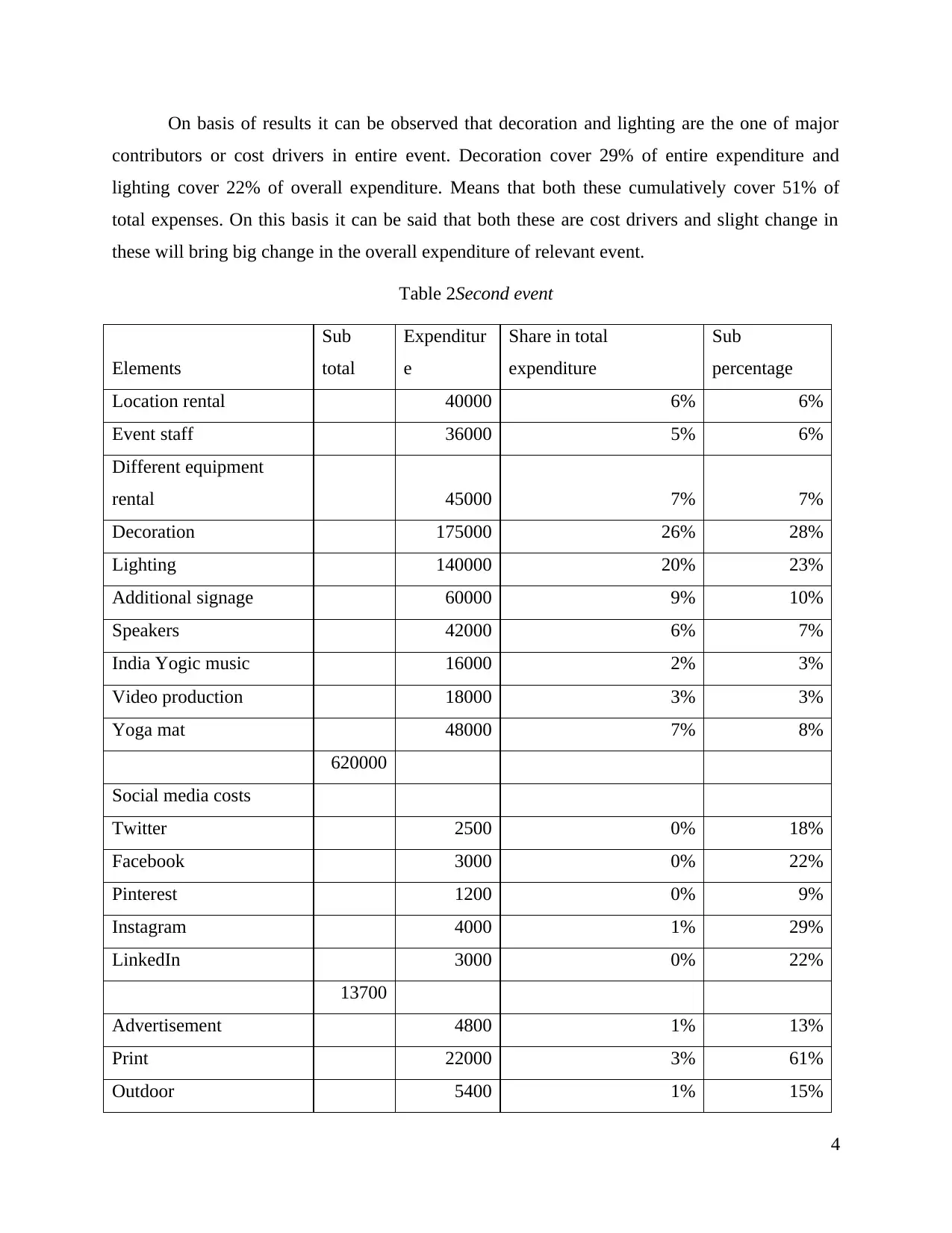

On basis of results it can be observed that decoration and lighting are the one of major

contributors or cost drivers in entire event. Decoration cover 29% of entire expenditure and

lighting cover 22% of overall expenditure. Means that both these cumulatively cover 51% of

total expenses. On this basis it can be said that both these are cost drivers and slight change in

these will bring big change in the overall expenditure of relevant event.

Table 2Second event

Elements

Sub

total

Expenditur

e

Share in total

expenditure

Sub

percentage

Location rental 40000 6% 6%

Event staff 36000 5% 6%

Different equipment

rental 45000 7% 7%

Decoration 175000 26% 28%

Lighting 140000 20% 23%

Additional signage 60000 9% 10%

Speakers 42000 6% 7%

India Yogic music 16000 2% 3%

Video production 18000 3% 3%

Yoga mat 48000 7% 8%

620000

Social media costs

Twitter 2500 0% 18%

Facebook 3000 0% 22%

Pinterest 1200 0% 9%

Instagram 4000 1% 29%

LinkedIn 3000 0% 22%

13700

Advertisement 4800 1% 13%

Print 22000 3% 61%

Outdoor 5400 1% 15%

4

contributors or cost drivers in entire event. Decoration cover 29% of entire expenditure and

lighting cover 22% of overall expenditure. Means that both these cumulatively cover 51% of

total expenses. On this basis it can be said that both these are cost drivers and slight change in

these will bring big change in the overall expenditure of relevant event.

Table 2Second event

Elements

Sub

total

Expenditur

e

Share in total

expenditure

Sub

percentage

Location rental 40000 6% 6%

Event staff 36000 5% 6%

Different equipment

rental 45000 7% 7%

Decoration 175000 26% 28%

Lighting 140000 20% 23%

Additional signage 60000 9% 10%

Speakers 42000 6% 7%

India Yogic music 16000 2% 3%

Video production 18000 3% 3%

Yoga mat 48000 7% 8%

620000

Social media costs

Twitter 2500 0% 18%

Facebook 3000 0% 22%

Pinterest 1200 0% 9%

Instagram 4000 1% 29%

LinkedIn 3000 0% 22%

13700

Advertisement 4800 1% 13%

Print 22000 3% 61%

Outdoor 5400 1% 15%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Radio 2000 0% 6%

Television 2000 0% 6%

36200

Drinks 8000 1% 53%

Snacks 7000 1% 47%

Total expenditure 15000 684900

From table given above it can be observed that decoration and lighting cover major part of

expenditure. It can be seen from the table that decoration have 26% share in overall expenses and

20% share in lighting which means that both of them cover 46% of total expenditure. On

granular level it can be observed that on social media expenditure Facebook and Instagram cover

major portion which is 22% and 29% respectively. Hence, it can be said that decoration and

lighting are common and major expenses that are incurred by the firm in both alternatives.

Task 2: Differentiate cost related to pricing and cost control techniques

according to the various cost drivers and behaviours

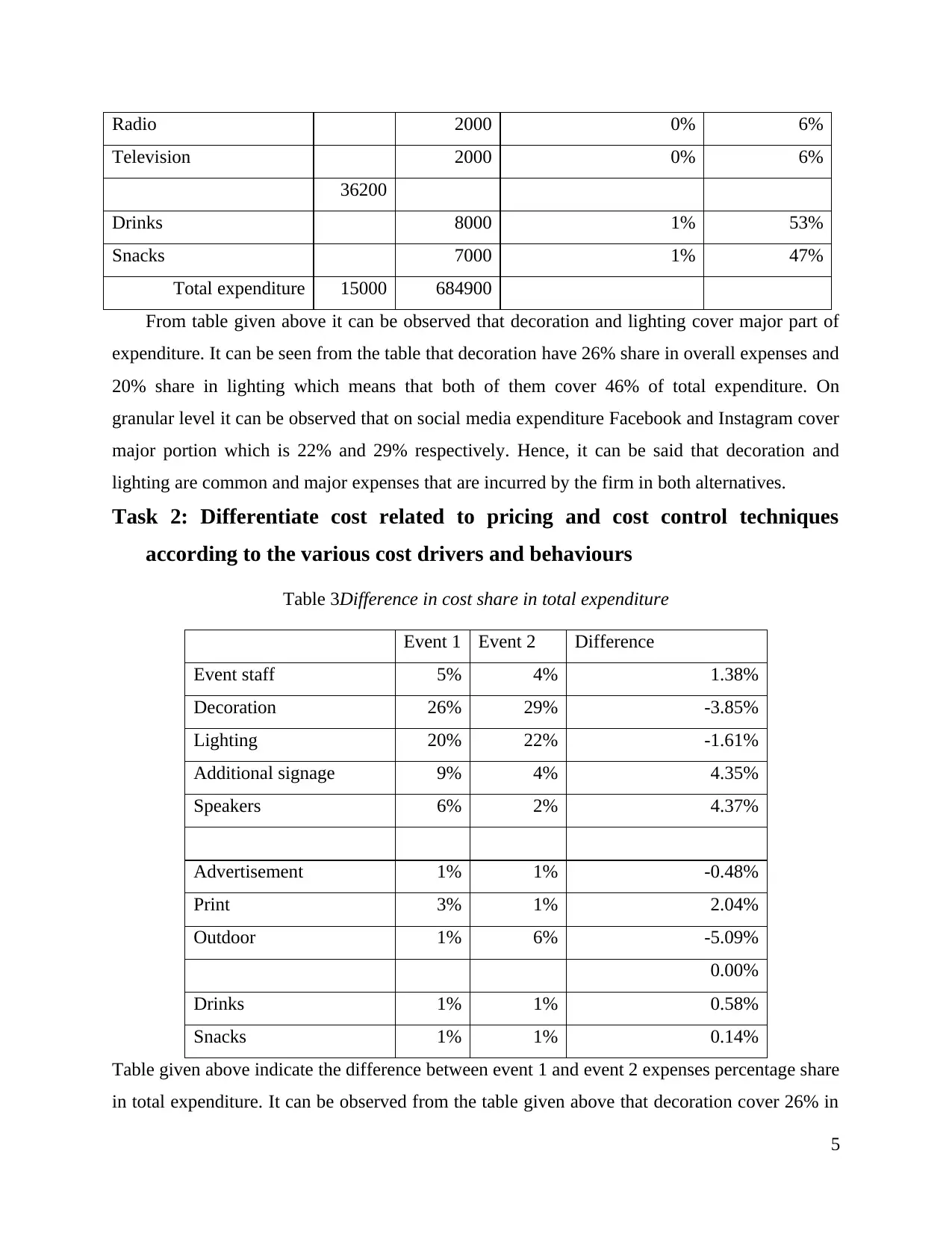

Table 3Difference in cost share in total expenditure

Event 1 Event 2 Difference

Event staff 5% 4% 1.38%

Decoration 26% 29% -3.85%

Lighting 20% 22% -1.61%

Additional signage 9% 4% 4.35%

Speakers 6% 2% 4.37%

Advertisement 1% 1% -0.48%

Print 3% 1% 2.04%

Outdoor 1% 6% -5.09%

0.00%

Drinks 1% 1% 0.58%

Snacks 1% 1% 0.14%

Table given above indicate the difference between event 1 and event 2 expenses percentage share

in total expenditure. It can be observed from the table given above that decoration cover 26% in

5

Television 2000 0% 6%

36200

Drinks 8000 1% 53%

Snacks 7000 1% 47%

Total expenditure 15000 684900

From table given above it can be observed that decoration and lighting cover major part of

expenditure. It can be seen from the table that decoration have 26% share in overall expenses and

20% share in lighting which means that both of them cover 46% of total expenditure. On

granular level it can be observed that on social media expenditure Facebook and Instagram cover

major portion which is 22% and 29% respectively. Hence, it can be said that decoration and

lighting are common and major expenses that are incurred by the firm in both alternatives.

Task 2: Differentiate cost related to pricing and cost control techniques

according to the various cost drivers and behaviours

Table 3Difference in cost share in total expenditure

Event 1 Event 2 Difference

Event staff 5% 4% 1.38%

Decoration 26% 29% -3.85%

Lighting 20% 22% -1.61%

Additional signage 9% 4% 4.35%

Speakers 6% 2% 4.37%

Advertisement 1% 1% -0.48%

Print 3% 1% 2.04%

Outdoor 1% 6% -5.09%

0.00%

Drinks 1% 1% 0.58%

Snacks 1% 1% 0.14%

Table given above indicate the difference between event 1 and event 2 expenses percentage share

in total expenditure. It can be observed from the table given above that decoration cover 26% in

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

total expenditure. On other hand, decoration cover 22% share in overall expenditure. Hence, it

can be said that more expenditure is made on decoration in event 2 then 1. Additional signage

share in total expenditure is 9% in case of event 1 and in case of event 2 share of same is 4%.

Similarly, speakers cover 6% of total expenditure in event 1 and cover just 2% of total in event 2.

In case of event 1 it can be seen that share of lighting is 20% in total expenses. Whereas, in case

of event 2 lighting have 22% share. Thus, overall it can be said that lighting, additional signage

and speakers share is more in event 1.

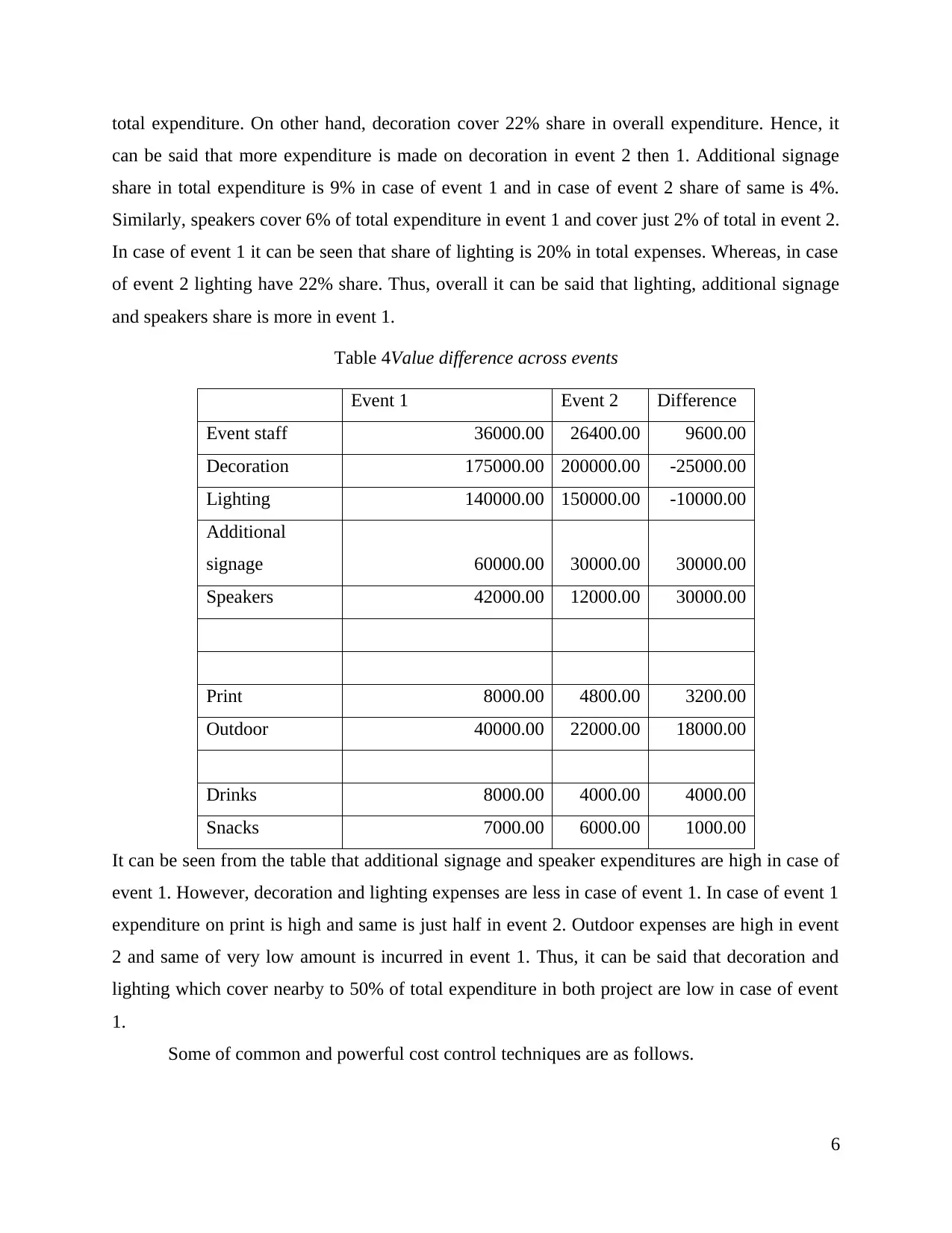

Table 4Value difference across events

Event 1 Event 2 Difference

Event staff 36000.00 26400.00 9600.00

Decoration 175000.00 200000.00 -25000.00

Lighting 140000.00 150000.00 -10000.00

Additional

signage 60000.00 30000.00 30000.00

Speakers 42000.00 12000.00 30000.00

Print 8000.00 4800.00 3200.00

Outdoor 40000.00 22000.00 18000.00

Drinks 8000.00 4000.00 4000.00

Snacks 7000.00 6000.00 1000.00

It can be seen from the table that additional signage and speaker expenditures are high in case of

event 1. However, decoration and lighting expenses are less in case of event 1. In case of event 1

expenditure on print is high and same is just half in event 2. Outdoor expenses are high in event

2 and same of very low amount is incurred in event 1. Thus, it can be said that decoration and

lighting which cover nearby to 50% of total expenditure in both project are low in case of event

1.

Some of common and powerful cost control techniques are as follows.

6

can be said that more expenditure is made on decoration in event 2 then 1. Additional signage

share in total expenditure is 9% in case of event 1 and in case of event 2 share of same is 4%.

Similarly, speakers cover 6% of total expenditure in event 1 and cover just 2% of total in event 2.

In case of event 1 it can be seen that share of lighting is 20% in total expenses. Whereas, in case

of event 2 lighting have 22% share. Thus, overall it can be said that lighting, additional signage

and speakers share is more in event 1.

Table 4Value difference across events

Event 1 Event 2 Difference

Event staff 36000.00 26400.00 9600.00

Decoration 175000.00 200000.00 -25000.00

Lighting 140000.00 150000.00 -10000.00

Additional

signage 60000.00 30000.00 30000.00

Speakers 42000.00 12000.00 30000.00

Print 8000.00 4800.00 3200.00

Outdoor 40000.00 22000.00 18000.00

Drinks 8000.00 4000.00 4000.00

Snacks 7000.00 6000.00 1000.00

It can be seen from the table that additional signage and speaker expenditures are high in case of

event 1. However, decoration and lighting expenses are less in case of event 1. In case of event 1

expenditure on print is high and same is just half in event 2. Outdoor expenses are high in event

2 and same of very low amount is incurred in event 1. Thus, it can be said that decoration and

lighting which cover nearby to 50% of total expenditure in both project are low in case of event

1.

Some of common and powerful cost control techniques are as follows.

6

KPI: KPI stand for key performance indicator under which for each expense standard

value is determined. While incurring expenses actual amount can be compared with the

standard value and if variance identified then in that case measures can be taken to

control them (Wei and Zhang, 2015). This is one of most popular cost control measure

taken in account by most of business firms. Budget: In case of this approach budget is prepared for all sort of expenses and values are

determined within which entire expenses must be made. In budget firm can prepare

separate segment for decoration and in it multiple categories can be placed, there values

can be determined. By doing so at more granular or deep level on real time basis cost

analysis can be done and cost can be controlled by the business firm (Bies, Hansen and

Howard, 2017).

Task 3: Discuss with emphasis on cost drivers in relation to which offer is best

acceptable for the business

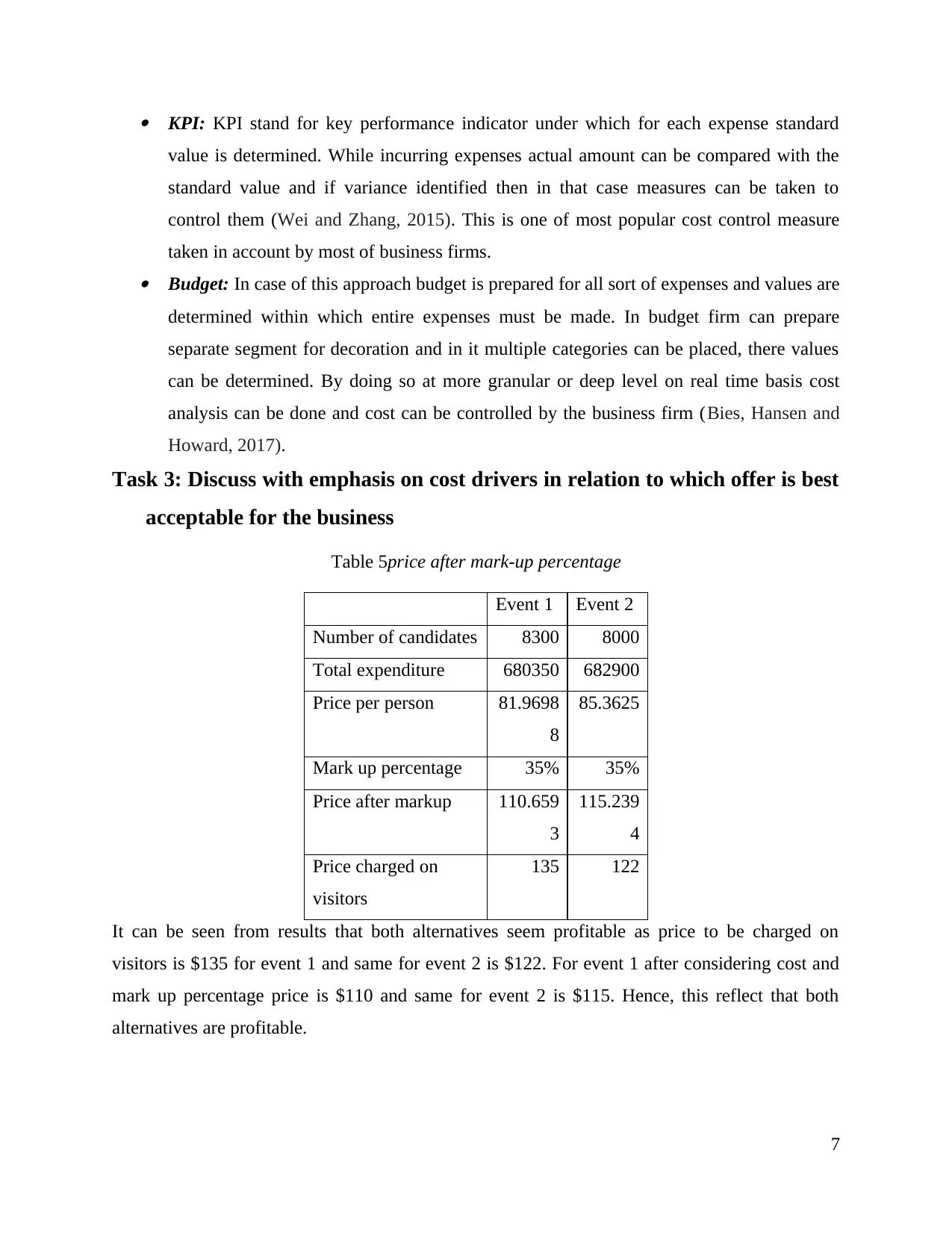

Table 5price after mark-up percentage

Event 1 Event 2

Number of candidates 8300 8000

Total expenditure 680350 682900

Price per person 81.9698

8

85.3625

Mark up percentage 35% 35%

Price after markup 110.659

3

115.239

4

Price charged on

visitors

135 122

It can be seen from results that both alternatives seem profitable as price to be charged on

visitors is $135 for event 1 and same for event 2 is $122. For event 1 after considering cost and

mark up percentage price is $110 and same for event 2 is $115. Hence, this reflect that both

alternatives are profitable.

7

value is determined. While incurring expenses actual amount can be compared with the

standard value and if variance identified then in that case measures can be taken to

control them (Wei and Zhang, 2015). This is one of most popular cost control measure

taken in account by most of business firms. Budget: In case of this approach budget is prepared for all sort of expenses and values are

determined within which entire expenses must be made. In budget firm can prepare

separate segment for decoration and in it multiple categories can be placed, there values

can be determined. By doing so at more granular or deep level on real time basis cost

analysis can be done and cost can be controlled by the business firm (Bies, Hansen and

Howard, 2017).

Task 3: Discuss with emphasis on cost drivers in relation to which offer is best

acceptable for the business

Table 5price after mark-up percentage

Event 1 Event 2

Number of candidates 8300 8000

Total expenditure 680350 682900

Price per person 81.9698

8

85.3625

Mark up percentage 35% 35%

Price after markup 110.659

3

115.239

4

Price charged on

visitors

135 122

It can be seen from results that both alternatives seem profitable as price to be charged on

visitors is $135 for event 1 and same for event 2 is $122. For event 1 after considering cost and

mark up percentage price is $110 and same for event 2 is $115. Hence, this reflect that both

alternatives are profitable.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

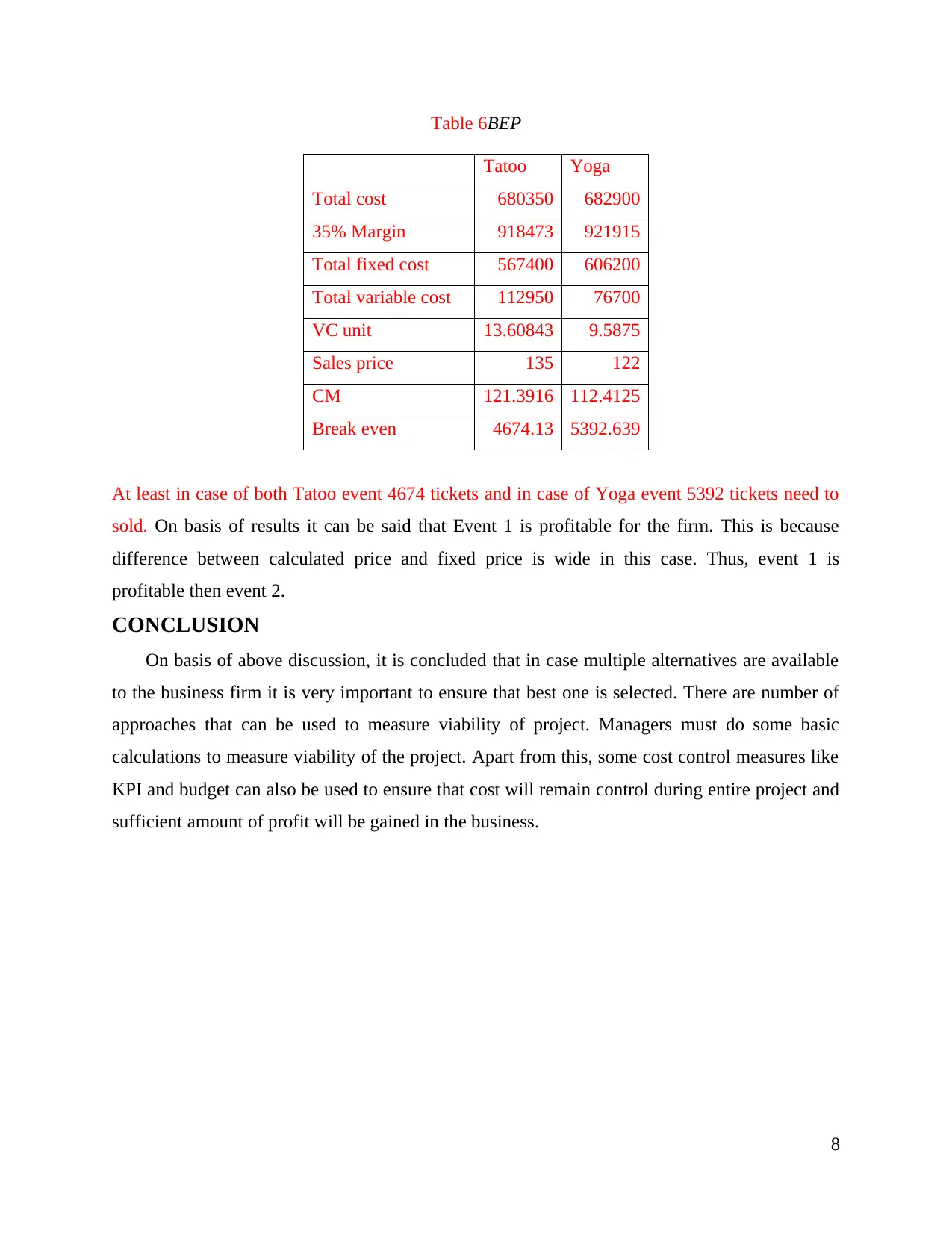

Table 6BEP

Tatoo Yoga

Total cost 680350 682900

35% Margin 918473 921915

Total fixed cost 567400 606200

Total variable cost 112950 76700

VC unit 13.60843 9.5875

Sales price 135 122

CM 121.3916 112.4125

Break even 4674.13 5392.639

At least in case of both Tatoo event 4674 tickets and in case of Yoga event 5392 tickets need to

sold. On basis of results it can be said that Event 1 is profitable for the firm. This is because

difference between calculated price and fixed price is wide in this case. Thus, event 1 is

profitable then event 2.

CONCLUSION

On basis of above discussion, it is concluded that in case multiple alternatives are available

to the business firm it is very important to ensure that best one is selected. There are number of

approaches that can be used to measure viability of project. Managers must do some basic

calculations to measure viability of the project. Apart from this, some cost control measures like

KPI and budget can also be used to ensure that cost will remain control during entire project and

sufficient amount of profit will be gained in the business.

8

Tatoo Yoga

Total cost 680350 682900

35% Margin 918473 921915

Total fixed cost 567400 606200

Total variable cost 112950 76700

VC unit 13.60843 9.5875

Sales price 135 122

CM 121.3916 112.4125

Break even 4674.13 5392.639

At least in case of both Tatoo event 4674 tickets and in case of Yoga event 5392 tickets need to

sold. On basis of results it can be said that Event 1 is profitable for the firm. This is because

difference between calculated price and fixed price is wide in this case. Thus, event 1 is

profitable then event 2.

CONCLUSION

On basis of above discussion, it is concluded that in case multiple alternatives are available

to the business firm it is very important to ensure that best one is selected. There are number of

approaches that can be used to measure viability of project. Managers must do some basic

calculations to measure viability of the project. Apart from this, some cost control measures like

KPI and budget can also be used to ensure that cost will remain control during entire project and

sufficient amount of profit will be gained in the business.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.