Cost Report and Cash Flow Projection for Event Management

VerifiedAdded on 2023/06/18

|11

|2628

|351

Report

AI Summary

This report provides a detailed financial analysis focusing on cost reports and cash flow projections, particularly in the context of planning a launch party aimed at attracting 100 clients. The cost report meticulously evaluates various expenses such as entertainment, venue hire, decoration, stationery, transportation, and staffing, highlighting both favorable and unfavorable variances between budgeted and actual costs. The cash flow projection presents a month-by-month assessment of expected cash inflows and outflows, enabling the identification of potential financial shortages or surpluses. It emphasizes the importance of accurate forecasting for effective financial management and decision-making, ensuring the company can proactively address any financial constraints and maintain operational stability. This comprehensive analysis is crucial for event organizers and financial managers seeking to optimize budgeting and enhance profitability.

Finance Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

MAIN BODY.................................................................................................................................................3

Cost report..............................................................................................................................................3

Cash flow projection................................................................................................................................5

REFERENCES..............................................................................................................................................10

INTRODUCTION...........................................................................................................................................3

MAIN BODY.................................................................................................................................................3

Cost report..............................................................................................................................................3

Cash flow projection................................................................................................................................5

REFERENCES..............................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The transmission of financial information, such as accounting records, to accountants, such

as capital providers, is referred to as financial reporting. Corporations are commonly thought of

as producing income reports when it comes to financial accounting. A balance sheet, operating

income, summary of employee's ownership, and statement of financial position are all part of a

larger use accounting records, but financial statements is more than that (Ashafoke, Dabor and

Ilaboya, 2021). Financial reporting encompasses all financial communication from the company

to outside parties, encompassing news articles, investor meetings, organizational stakeholders

and analyses, auditor’s findings, as well as the company's financial notes. Financial reporting

refers to anything that may be used to communicate financial facts to the general public. This

report discusses the cost report and the cash flow report. The firm is throwing a launch party with

the goal of attracting 100 clients. As a result, cost and cash flow estimations should be done in

such a manner that they aid in both recruiting consumers and managing the financial cash.

MAIN BODY

Cost report

A cost report is a critical function that managers utilises to evaluate the operations in a

company; it displays the agency's production quantity and cost data. Calculate the cost of each

unit of manufacturing. Make a timetable for cost reconciling. The cost content is based on the

service, including institution features, utilisation data, cost and charges by cost centre (total and

for Medicare), Health care settlements information, and company's financial information.

Particulars Cost per unit Original Flexed Actual Variances

Units 100 20 80

Selling price 25 20000

Revenues 20000

Variable costs

:

Entertainment 2.50 250 30 280 (300)

Venue hire 4 400 40 440 (400)

Decoration 1.50 150 30 120 300

The transmission of financial information, such as accounting records, to accountants, such

as capital providers, is referred to as financial reporting. Corporations are commonly thought of

as producing income reports when it comes to financial accounting. A balance sheet, operating

income, summary of employee's ownership, and statement of financial position are all part of a

larger use accounting records, but financial statements is more than that (Ashafoke, Dabor and

Ilaboya, 2021). Financial reporting encompasses all financial communication from the company

to outside parties, encompassing news articles, investor meetings, organizational stakeholders

and analyses, auditor’s findings, as well as the company's financial notes. Financial reporting

refers to anything that may be used to communicate financial facts to the general public. This

report discusses the cost report and the cash flow report. The firm is throwing a launch party with

the goal of attracting 100 clients. As a result, cost and cash flow estimations should be done in

such a manner that they aid in both recruiting consumers and managing the financial cash.

MAIN BODY

Cost report

A cost report is a critical function that managers utilises to evaluate the operations in a

company; it displays the agency's production quantity and cost data. Calculate the cost of each

unit of manufacturing. Make a timetable for cost reconciling. The cost content is based on the

service, including institution features, utilisation data, cost and charges by cost centre (total and

for Medicare), Health care settlements information, and company's financial information.

Particulars Cost per unit Original Flexed Actual Variances

Units 100 20 80

Selling price 25 20000

Revenues 20000

Variable costs

:

Entertainment 2.50 250 30 280 (300)

Venue hire 4 400 40 440 (400)

Decoration 1.50 150 30 120 300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

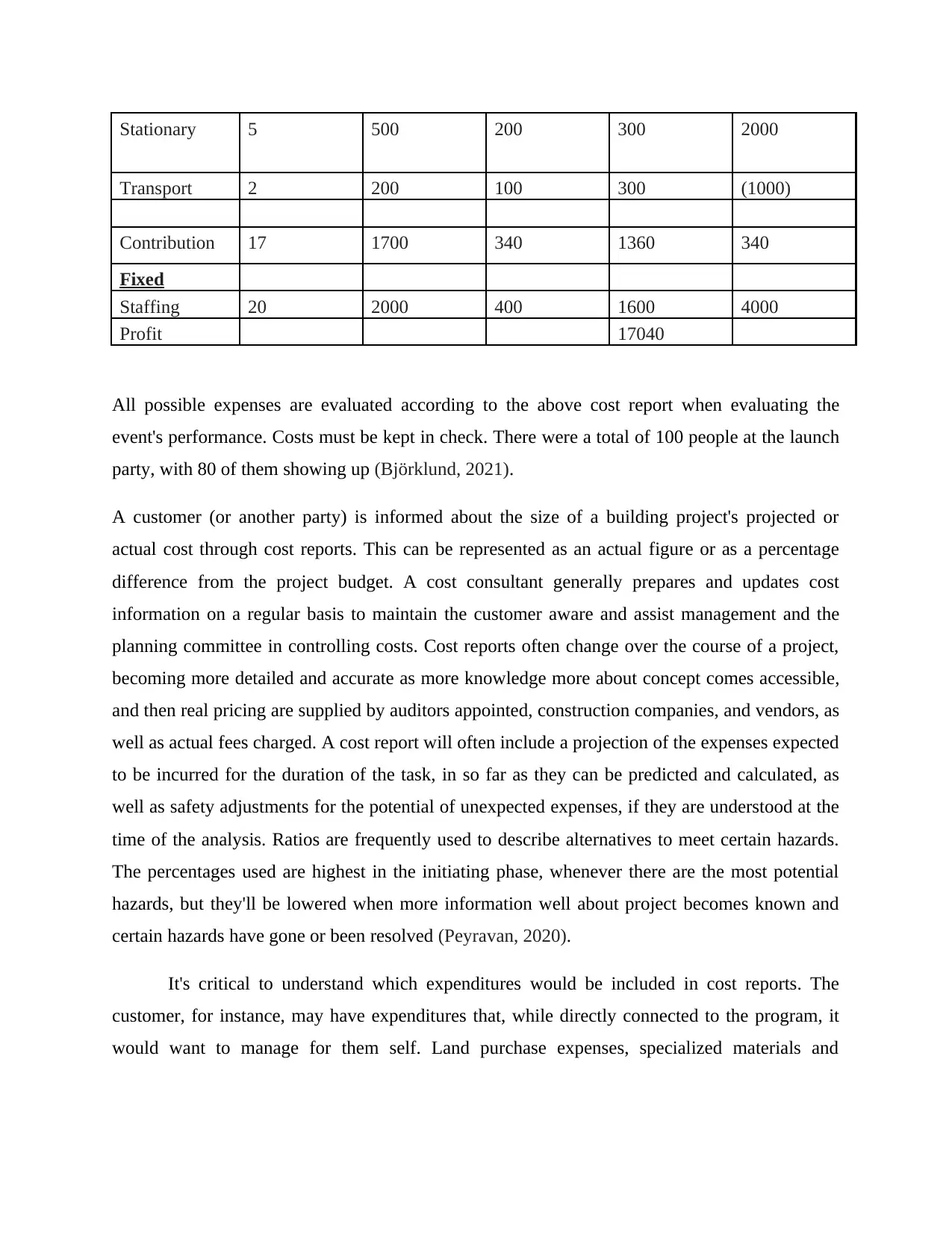

Stationary 5 500 200 300 2000

Transport 2 200 100 300 (1000)

Contribution 17 1700 340 1360 340

Fixed

Staffing 20 2000 400 1600 4000

Profit 17040

All possible expenses are evaluated according to the above cost report when evaluating the

event's performance. Costs must be kept in check. There were a total of 100 people at the launch

party, with 80 of them showing up (Björklund, 2021).

A customer (or another party) is informed about the size of a building project's projected or

actual cost through cost reports. This can be represented as an actual figure or as a percentage

difference from the project budget. A cost consultant generally prepares and updates cost

information on a regular basis to maintain the customer aware and assist management and the

planning committee in controlling costs. Cost reports often change over the course of a project,

becoming more detailed and accurate as more knowledge more about concept comes accessible,

and then real pricing are supplied by auditors appointed, construction companies, and vendors, as

well as actual fees charged. A cost report will often include a projection of the expenses expected

to be incurred for the duration of the task, in so far as they can be predicted and calculated, as

well as safety adjustments for the potential of unexpected expenses, if they are understood at the

time of the analysis. Ratios are frequently used to describe alternatives to meet certain hazards.

The percentages used are highest in the initiating phase, whenever there are the most potential

hazards, but they'll be lowered when more information well about project becomes known and

certain hazards have gone or been resolved (Peyravan, 2020).

It's critical to understand which expenditures would be included in cost reports. The

customer, for instance, may have expenditures that, while directly connected to the program, it

would want to manage for them self. Land purchase expenses, specialized materials and

Transport 2 200 100 300 (1000)

Contribution 17 1700 340 1360 340

Fixed

Staffing 20 2000 400 1600 4000

Profit 17040

All possible expenses are evaluated according to the above cost report when evaluating the

event's performance. Costs must be kept in check. There were a total of 100 people at the launch

party, with 80 of them showing up (Björklund, 2021).

A customer (or another party) is informed about the size of a building project's projected or

actual cost through cost reports. This can be represented as an actual figure or as a percentage

difference from the project budget. A cost consultant generally prepares and updates cost

information on a regular basis to maintain the customer aware and assist management and the

planning committee in controlling costs. Cost reports often change over the course of a project,

becoming more detailed and accurate as more knowledge more about concept comes accessible,

and then real pricing are supplied by auditors appointed, construction companies, and vendors, as

well as actual fees charged. A cost report will often include a projection of the expenses expected

to be incurred for the duration of the task, in so far as they can be predicted and calculated, as

well as safety adjustments for the potential of unexpected expenses, if they are understood at the

time of the analysis. Ratios are frequently used to describe alternatives to meet certain hazards.

The percentages used are highest in the initiating phase, whenever there are the most potential

hazards, but they'll be lowered when more information well about project becomes known and

certain hazards have gone or been resolved (Peyravan, 2020).

It's critical to understand which expenditures would be included in cost reports. The

customer, for instance, may have expenditures that, while directly connected to the program, it

would want to manage for them self. Land purchase expenses, specialized materials and

equipment, furnishings, building contracts other than the primary contract, and so on are

examples of this.

Usually cost experts will create their unique style for cost reports when there isn't a single,

standardized kind of cost written report or if the customer has particular structuring needs.

Planning for an event gives event organizers a set of guidelines to operate inside. There is

always a limit to how much money may be invested on a single event. Considering that figure, it

only helps to keep record of special occasion expenditures to obtain the total cash rose does not

beyond the allocated amount. The major goals of event assessment are to establish if the event

accomplished its specified achievable objectives. -To see if the activity satisfies all of the

attendees' objectives. -It's essential to keep record of comments in order to guide current

organization’s success (Gamayuni, 2020).

Decoration, venue hiring, entertainment, stationery, transportation, and personnel are all

possible expenditures. Personnel costs are fixed for the firm, and all other costs are fixed. A cost

report is generated by a firm in order to determine its competitiveness. All of the expenses per

unit are computed in the aforementioned cost report, and the budgeting is created

correspondingly. There are both positively and negatively or unfavorable variations in this cost

report. Positive deviations indicate that the real profit is more than expected, whereas negatives

variations indicate that the actual profits are lower than expected.

To preserve the firm's growth, the company must seek to maintain all variances positive.

The company's entertaining cost has a negative variance, which implies the real cost is 280 and

the intended cost is 250. The firm spends extra money to keep the entertaining aspect of the

event going. Variations that are undesirable are referred to as unfavorable variances. The cost of

renting a venue is likewise a variable cost with negative variations. Decoration and stationary, on

the other hand, have positive variations. This indicates that the firm did well in these two areas.

The real revenue is higher than the anticipated profit. According to the aforementioned expense

analysis, the firm is spending more money on entertainment and venue rental. By implementing

the necessary modifications, the business may cut costs. In order to enhance profit, the firm

should also concentrate on transport costs (Butar and Murniati, 2021).

examples of this.

Usually cost experts will create their unique style for cost reports when there isn't a single,

standardized kind of cost written report or if the customer has particular structuring needs.

Planning for an event gives event organizers a set of guidelines to operate inside. There is

always a limit to how much money may be invested on a single event. Considering that figure, it

only helps to keep record of special occasion expenditures to obtain the total cash rose does not

beyond the allocated amount. The major goals of event assessment are to establish if the event

accomplished its specified achievable objectives. -To see if the activity satisfies all of the

attendees' objectives. -It's essential to keep record of comments in order to guide current

organization’s success (Gamayuni, 2020).

Decoration, venue hiring, entertainment, stationery, transportation, and personnel are all

possible expenditures. Personnel costs are fixed for the firm, and all other costs are fixed. A cost

report is generated by a firm in order to determine its competitiveness. All of the expenses per

unit are computed in the aforementioned cost report, and the budgeting is created

correspondingly. There are both positively and negatively or unfavorable variations in this cost

report. Positive deviations indicate that the real profit is more than expected, whereas negatives

variations indicate that the actual profits are lower than expected.

To preserve the firm's growth, the company must seek to maintain all variances positive.

The company's entertaining cost has a negative variance, which implies the real cost is 280 and

the intended cost is 250. The firm spends extra money to keep the entertaining aspect of the

event going. Variations that are undesirable are referred to as unfavorable variances. The cost of

renting a venue is likewise a variable cost with negative variations. Decoration and stationary, on

the other hand, have positive variations. This indicates that the firm did well in these two areas.

The real revenue is higher than the anticipated profit. According to the aforementioned expense

analysis, the firm is spending more money on entertainment and venue rental. By implementing

the necessary modifications, the business may cut costs. In order to enhance profit, the firm

should also concentrate on transport costs (Butar and Murniati, 2021).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash flow projection

The cash flow projection depicts a month-by-month assessment of the funds normally

receive and expend for a program over a given time period. The net cash flow of a business is the

differential between some of the money in and out each month. Users can compute (predict) how

often cash will be accessible at the conclusion of a term when they include the cash position at

the beginning of the project in the spreadsheet. The balances for each quarter are given at the

foot of the standings as a total loss or gain. These data will emphasize any anticipated financial

shortages, allowing the development and financial users to communicate on recovery process.

The goal of a cash flow projection is to have a company an approximation of input and

output money over a specific period of time. In order to better identify the states that an increase

for each area, the projection, which focuses on estimated cash flow, is typically split down into

separate pieces. Companies will make a cash flow estimate for the next few months. A time

period will be selected (typically the following quarter) whereby a prediction of under further

will be displayed in the projection. The cash flow projection is used to projection a profitability

of a business over a given timeframe. The majority of these estimates are based on historical

data, cash flow, and projections (Ooi, Mayes, Dhaliwal and Shane, 2020).

Pre-

Startup

EST

Jan-

2021

Feb-

2021

Mar-

2021

Apr-

2021

May-

2021

Jun-

2021

Cash on Hand

(beginning of

month)

15,000 15,000 16,000 20,000 25,000 21000 10000

CASH

RECEIPTS

Cash Sales 10,000 10000 15000 7000 9000 2100 22500

Collections fm

CR accounts Nil nil nil Nil nil Nil nil

Loan/ other

cash inj. Nil nil nil Nil nil Nil nil

TOTAL CASH

RECEIPTS 10,000 10000 15000 7000 9000 2100 22500

Total Cash

Available

(before cash

out)

15,000 15,000 16,000 20,000 25,000 21000 10000

The cash flow projection depicts a month-by-month assessment of the funds normally

receive and expend for a program over a given time period. The net cash flow of a business is the

differential between some of the money in and out each month. Users can compute (predict) how

often cash will be accessible at the conclusion of a term when they include the cash position at

the beginning of the project in the spreadsheet. The balances for each quarter are given at the

foot of the standings as a total loss or gain. These data will emphasize any anticipated financial

shortages, allowing the development and financial users to communicate on recovery process.

The goal of a cash flow projection is to have a company an approximation of input and

output money over a specific period of time. In order to better identify the states that an increase

for each area, the projection, which focuses on estimated cash flow, is typically split down into

separate pieces. Companies will make a cash flow estimate for the next few months. A time

period will be selected (typically the following quarter) whereby a prediction of under further

will be displayed in the projection. The cash flow projection is used to projection a profitability

of a business over a given timeframe. The majority of these estimates are based on historical

data, cash flow, and projections (Ooi, Mayes, Dhaliwal and Shane, 2020).

Pre-

Startup

EST

Jan-

2021

Feb-

2021

Mar-

2021

Apr-

2021

May-

2021

Jun-

2021

Cash on Hand

(beginning of

month)

15,000 15,000 16,000 20,000 25,000 21000 10000

CASH

RECEIPTS

Cash Sales 10,000 10000 15000 7000 9000 2100 22500

Collections fm

CR accounts Nil nil nil Nil nil Nil nil

Loan/ other

cash inj. Nil nil nil Nil nil Nil nil

TOTAL CASH

RECEIPTS 10,000 10000 15000 7000 9000 2100 22500

Total Cash

Available

(before cash

out)

15,000 15,000 16,000 20,000 25,000 21000 10000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASH PAID

OUT

Purchases

(merchandise) 20,000 22,000 24,200 26,620 29,282 32,210 35,431

Purchases

(specify) 15,000 16,500 18,150 19,965 21,962 24,158 26,573

Purchases

(specify) 5,000 5,500 6,050 6,655 7,321 8,053 8,858

Gross wages

(exact

withdrawal)

1,500 1,650 1,815 1,997 2,196 2,416 2,657

Payroll

expenses (taxes,

etc.)

2,100 2,310 2,541 2,795 3,075 3,382 3,720

Outside services 900 990 1,089 1,198 1,318 1,449 1,594

Supplies (office

& oper.) 1,000 1,100 1,210 1,331 1,464 1,611 1,772

Repairs &

maintenance 1,500 1,650 1,815 1,997 2,196 2,416 2,657

Advertising 2,000 2,200 2,420 2,662 2,928 3,221 3,543

Car, delivery &

travel 500 550 605 666 732 805 886

Accounting &

legal 700 770 847 932 1,025 1,127 1,240

Rent 800 880 968 1,065 1,171 1,288 1,417

Telephone 1,000 1,100 1,210 1,331 1,464 1,611 1,772

Utilities 1,500 1,650 1,815 1,997 2,196 2,416 2,657

Insurance 1,500 1,650 1,815 1,997 2,196 2,416 2,657

Taxes (real

estate, etc.) 9,000 9,900 10,890 11,979 13,177 14,495 15,944

Interest 1,200 1,320 1,452 1,597 1,757 1,933 2,126

Other expenses

(specify) 1,500 1,650 1,815 1,997 2,196 2,416 2,657

Other (specify) 1,600 1,760 1,936 2,130 2,343 2,577 2,834

Other (specify) 2,100 2,310 2,541 2,795 3,075 3,382 3,720

Miscellaneous 2,500 2,750 3,025 3,328 3,660 4,026 4,429

SUBTOTAL 72,900 80,190 88,209 97,030 106,733 117,40

6 129,147

OUT

Purchases

(merchandise) 20,000 22,000 24,200 26,620 29,282 32,210 35,431

Purchases

(specify) 15,000 16,500 18,150 19,965 21,962 24,158 26,573

Purchases

(specify) 5,000 5,500 6,050 6,655 7,321 8,053 8,858

Gross wages

(exact

withdrawal)

1,500 1,650 1,815 1,997 2,196 2,416 2,657

Payroll

expenses (taxes,

etc.)

2,100 2,310 2,541 2,795 3,075 3,382 3,720

Outside services 900 990 1,089 1,198 1,318 1,449 1,594

Supplies (office

& oper.) 1,000 1,100 1,210 1,331 1,464 1,611 1,772

Repairs &

maintenance 1,500 1,650 1,815 1,997 2,196 2,416 2,657

Advertising 2,000 2,200 2,420 2,662 2,928 3,221 3,543

Car, delivery &

travel 500 550 605 666 732 805 886

Accounting &

legal 700 770 847 932 1,025 1,127 1,240

Rent 800 880 968 1,065 1,171 1,288 1,417

Telephone 1,000 1,100 1,210 1,331 1,464 1,611 1,772

Utilities 1,500 1,650 1,815 1,997 2,196 2,416 2,657

Insurance 1,500 1,650 1,815 1,997 2,196 2,416 2,657

Taxes (real

estate, etc.) 9,000 9,900 10,890 11,979 13,177 14,495 15,944

Interest 1,200 1,320 1,452 1,597 1,757 1,933 2,126

Other expenses

(specify) 1,500 1,650 1,815 1,997 2,196 2,416 2,657

Other (specify) 1,600 1,760 1,936 2,130 2,343 2,577 2,834

Other (specify) 2,100 2,310 2,541 2,795 3,075 3,382 3,720

Miscellaneous 2,500 2,750 3,025 3,328 3,660 4,026 4,429

SUBTOTAL 72,900 80,190 88,209 97,030 106,733 117,40

6 129,147

Cash reigns supreme. It is the heartbeat of any company. A company's ability to pay workers,

purchase merchandise, or make finance payments is hampered by a lack of cash flow. However,

cash flow may not always be predictable or regular. A cash flow projection, which is a technique

that firms in an industry may use to anticipate income, costs, and bank deposits across time, is

one effective tool for projecting cash flow. A cash flow prediction helps a company operator to

predict a financial constraint until it occurs, allowing the company to make required adjustments

to maintain the firm going properly (Kędzior, Cyganska and Syrrakos, 2020). Projection could

also provide leadership prior notice of a potential financial gap, giving them time to put in place

mitigating strategies to avoid running out of cash. Cash flow analysis allows a business to see

different possibilities and assess their economic implications. Comprehension impending

expenditures and making comparisons them to trade receivables but also future projections sales

is essential to delivering cash flow." It's critical to monitor the position of financing in and out of

your organisation on a periodic basis to ensure the economic position of company and what it

will be across several days.

There are several fundamental things to take when thinking about the most effective ways

to arrange event's cash flow. To guarantee sufficient spending depending on profitability, follow

this advice when beginning the procedure and dedicating yourself to an agreement.

Prepare paperwork in advance: This involves writing the event's first budget and establishing a

cash-flow projection. These records should communicate with one another to ensure smooth cash

movement in and out. It's also crucial to set a precise timeline for the entire event in order to

improve control and knowledge of the needs (OGOUN and EPHIBAYERIN, 2020).

Pre-funding: They must create a cash-flow projection, an event timetable, and an overall budget

in terms of understanding the quantities of water funds necessary to make the event a success.

The first funds are crucial for supporting activities like as venue deposits, website construction,

and other marketing that must be paid before any cash is received. Nevertheless, this stage can be

difficult since both organizations and clients must successfully reduce early cash outlays in order

to decrease financial problems.

Predicting money flows has a number of advantages. There are several positives to generating a

cash flow projection, as well as the opportunity to:

purchase merchandise, or make finance payments is hampered by a lack of cash flow. However,

cash flow may not always be predictable or regular. A cash flow projection, which is a technique

that firms in an industry may use to anticipate income, costs, and bank deposits across time, is

one effective tool for projecting cash flow. A cash flow prediction helps a company operator to

predict a financial constraint until it occurs, allowing the company to make required adjustments

to maintain the firm going properly (Kędzior, Cyganska and Syrrakos, 2020). Projection could

also provide leadership prior notice of a potential financial gap, giving them time to put in place

mitigating strategies to avoid running out of cash. Cash flow analysis allows a business to see

different possibilities and assess their economic implications. Comprehension impending

expenditures and making comparisons them to trade receivables but also future projections sales

is essential to delivering cash flow." It's critical to monitor the position of financing in and out of

your organisation on a periodic basis to ensure the economic position of company and what it

will be across several days.

There are several fundamental things to take when thinking about the most effective ways

to arrange event's cash flow. To guarantee sufficient spending depending on profitability, follow

this advice when beginning the procedure and dedicating yourself to an agreement.

Prepare paperwork in advance: This involves writing the event's first budget and establishing a

cash-flow projection. These records should communicate with one another to ensure smooth cash

movement in and out. It's also crucial to set a precise timeline for the entire event in order to

improve control and knowledge of the needs (OGOUN and EPHIBAYERIN, 2020).

Pre-funding: They must create a cash-flow projection, an event timetable, and an overall budget

in terms of understanding the quantities of water funds necessary to make the event a success.

The first funds are crucial for supporting activities like as venue deposits, website construction,

and other marketing that must be paid before any cash is received. Nevertheless, this stage can be

difficult since both organizations and clients must successfully reduce early cash outlays in order

to decrease financial problems.

Predicting money flows has a number of advantages. There are several positives to generating a

cash flow projection, as well as the opportunity to:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• It is possible to forecast cash shortages and surpluses.

• Over time, compare and contrast corporate expenditures and income.

• Estimate the effect of a company's modifications (e.g., hiring an employee)

• Emphasizing ability to make regular payments to borrowers.

• Check to determine if any adjustments are necessary (e.g., cutting expenses)

• Cash flow forecasting isn't suitable for all businesses. The projected cash flow report can be

costly and time consuming if done properly (Svoboda, Poskočilová and Bohušová, 2020).

• Over time, compare and contrast corporate expenditures and income.

• Estimate the effect of a company's modifications (e.g., hiring an employee)

• Emphasizing ability to make regular payments to borrowers.

• Check to determine if any adjustments are necessary (e.g., cutting expenses)

• Cash flow forecasting isn't suitable for all businesses. The projected cash flow report can be

costly and time consuming if done properly (Svoboda, Poskočilová and Bohušová, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal

Ashafoke, T., Dabor, E. and Ilaboya, J., 2021. Do CEO Characteristics affect Financial

Reporting Quality? An Empirical Analysis. Acta Universitatis Danubius.

Œconomica. 17(1).

Björklund, J., 2021. Reviewing the Non-Financial Reporting Directive: An analysis de lege lata

and de lege ferenda concerning sustainability reporting obligations for undertakings in

the EU.

Peyravan, L., 2020. Financial reporting quality and dual-holding of debt and equity. The

Accounting Review. 95(5). pp.351-371.

Gamayuni, R. R., 2020. Implementation of E-Planning, E-Budgeting and Government Internal

Control Systems for Financial Reporting Quality at Local Governments in

Indonesia. Talent Development & Excellence. 12(1). pp.112-124.

Butar, S. B. and Murniati, M. P., 2021. How does Financial Reporting Quality Relate to Stock

Price Crash Risk? Evidence from Indonesian listed Companies. Jurnal Dinamika

Akuntansi dan Bisnis. 8(1). pp.59-76.

Ooi, B. W., Mayes, D. G., Dhaliwal, D. and Shane, P., 2020. Mandatory financial reporting

frequency and market efficiency: evidence from Malaysia. International Journal of

Corporate Governance. 11(2). pp.109-128.

Kędzior, M., Cyganska, M. and Syrrakos, D., 2020. Determinants of voluntary international

financial reporting standards adoption in Poland. Engineering Economics. 31(2). pp.155-

168.

OGOUN, S. and EPHIBAYERIN, F.A., 2020. Accounting Ethics and Quality of Financial

Reporting. International Scholars Journal of Arts and Social Science Research. 3(1).

pp.60-75.

Svoboda, P., Poskočilová, B. and Bohušová, H., 2020. Financial reporting quality: the case of

Czech and German listed companies. International Journal of Monetary Economics and

Finance. 13(3). pp.235-243.

Books and Journal

Ashafoke, T., Dabor, E. and Ilaboya, J., 2021. Do CEO Characteristics affect Financial

Reporting Quality? An Empirical Analysis. Acta Universitatis Danubius.

Œconomica. 17(1).

Björklund, J., 2021. Reviewing the Non-Financial Reporting Directive: An analysis de lege lata

and de lege ferenda concerning sustainability reporting obligations for undertakings in

the EU.

Peyravan, L., 2020. Financial reporting quality and dual-holding of debt and equity. The

Accounting Review. 95(5). pp.351-371.

Gamayuni, R. R., 2020. Implementation of E-Planning, E-Budgeting and Government Internal

Control Systems for Financial Reporting Quality at Local Governments in

Indonesia. Talent Development & Excellence. 12(1). pp.112-124.

Butar, S. B. and Murniati, M. P., 2021. How does Financial Reporting Quality Relate to Stock

Price Crash Risk? Evidence from Indonesian listed Companies. Jurnal Dinamika

Akuntansi dan Bisnis. 8(1). pp.59-76.

Ooi, B. W., Mayes, D. G., Dhaliwal, D. and Shane, P., 2020. Mandatory financial reporting

frequency and market efficiency: evidence from Malaysia. International Journal of

Corporate Governance. 11(2). pp.109-128.

Kędzior, M., Cyganska, M. and Syrrakos, D., 2020. Determinants of voluntary international

financial reporting standards adoption in Poland. Engineering Economics. 31(2). pp.155-

168.

OGOUN, S. and EPHIBAYERIN, F.A., 2020. Accounting Ethics and Quality of Financial

Reporting. International Scholars Journal of Arts and Social Science Research. 3(1).

pp.60-75.

Svoboda, P., Poskočilová, B. and Bohušová, H., 2020. Financial reporting quality: the case of

Czech and German listed companies. International Journal of Monetary Economics and

Finance. 13(3). pp.235-243.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.