Cost and Revenue Analysis Report - Financial Accounting, Semester 1

VerifiedAdded on 2020/11/23

|17

|4216

|126

Report

AI Summary

This report provides a comprehensive overview of cost and revenue analysis within a business context. It begins by exploring the purpose of internal reporting and the relationship between various costing systems, including job and process costing. The report identifies different types of responsibility, cost, profit, and investment centres and classifies various cost classifications, differentiating between marginal and absorption costing. Task 2 delves into the recording and analysis of cost information for materials, labour, and expenses, covering inventory stages and valuation methods (FIFO, LIFO, weighted average). The report then examines the behavior of different cost types (fixed, variable, semi-variable, and stepped) and the application of different costing systems (job, batch, unit, process, and service). Task 3 focuses on the attribution of overhead costs, including direct and step-down methods, calculating overhead absorption rates, and making adjustments for under or over recovered costs. It also covers methods of cost allocation, apportionment, and absorption. Task 4 explores variance analysis, comparing budgeted and actual costs, analysing variances for management reports, and communicating significant variances to budget holders. The report concludes with Task 5, which addresses the estimation of future income and costs for decision-making, the effect of changing activity levels on unit costs, and the identification of factors affecting short and long-term decision-making.

Cost and Revenue

Table of Contents

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose of internal reporting and providing accurate information to management..............1

1.2 Relationship between various costing systems.....................................................................1

1.3 Identification of responsibility, cost, profit and investment centres.....................................2

1.4 Characteristics of different types of cost classifications and their use..................................2

1.5 Difference between marginal and absorption costing...........................................................2

TASK 2............................................................................................................................................3

2.1 Record of cost information for material, labour and expenses.............................................3

2.2 Analysis of cost information for material, labour and expenses...........................................3

2.3 Various stages of inventory...................................................................................................3

2.4 Valuation of inventory using different methods...................................................................4

2.5 Description of behaviour of different types of costs.............................................................5

2.6 Record of cost information using different costing systems.................................................6

TASK 3............................................................................................................................................6

3.1 Attribution of overhead cost to production and service cost centres using agreed bases.....6

3.2 Calculation of overhead absorption rates according to suitable bases of absorption............7

3.3 Adjustments for under or over recovered costs.....................................................................7

3.4 Methods of allocation, apportionment and absorption at regular intervals...........................8

3.5 Communication with staff to resolve queries related to overhead cost data.........................9

TASK 4............................................................................................................................................9

4.1 Comparison of budgeted and actual costs noting any variances...........................................9

4.2 Analysis of variances for management reports...................................................................10

4.3 Information for budget holders of any significant variances..............................................10

4.4 Formulation of management reports in an appropriate format...........................................10

TASK 5..........................................................................................................................................11

5.1 Estimation of future income and costs for decision making using difference elements.....11

5.2 Effect of changing activity levels on unit costs..................................................................12

5.3 Calculation of the effect of changing activity levels on unit costs.....................................12

5.4 Identification of factors that are affecting short and long term decision making...............13

CONCLUSION..............................................................................................................................13

TASK 1............................................................................................................................................1

1.1 Purpose of internal reporting and providing accurate information to management..............1

1.2 Relationship between various costing systems.....................................................................1

1.3 Identification of responsibility, cost, profit and investment centres.....................................2

1.4 Characteristics of different types of cost classifications and their use..................................2

1.5 Difference between marginal and absorption costing...........................................................2

TASK 2............................................................................................................................................3

2.1 Record of cost information for material, labour and expenses.............................................3

2.2 Analysis of cost information for material, labour and expenses...........................................3

2.3 Various stages of inventory...................................................................................................3

2.4 Valuation of inventory using different methods...................................................................4

2.5 Description of behaviour of different types of costs.............................................................5

2.6 Record of cost information using different costing systems.................................................6

TASK 3............................................................................................................................................6

3.1 Attribution of overhead cost to production and service cost centres using agreed bases.....6

3.2 Calculation of overhead absorption rates according to suitable bases of absorption............7

3.3 Adjustments for under or over recovered costs.....................................................................7

3.4 Methods of allocation, apportionment and absorption at regular intervals...........................8

3.5 Communication with staff to resolve queries related to overhead cost data.........................9

TASK 4............................................................................................................................................9

4.1 Comparison of budgeted and actual costs noting any variances...........................................9

4.2 Analysis of variances for management reports...................................................................10

4.3 Information for budget holders of any significant variances..............................................10

4.4 Formulation of management reports in an appropriate format...........................................10

TASK 5..........................................................................................................................................11

5.1 Estimation of future income and costs for decision making using difference elements.....11

5.2 Effect of changing activity levels on unit costs..................................................................12

5.3 Calculation of the effect of changing activity levels on unit costs.....................................12

5.4 Identification of factors that are affecting short and long term decision making...............13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Cost and revenues are two separate elements of a business. Cost is the total amount which

is involved in the manufacturing process of a products and revenues are the incomes that are

generated by a business entity on the sales of those items. All the expenses that are related to

material, labour and other overheads are considered by the companies while deciding prices of

their manufactured products. This assignment is based on the concept of these two components.

In this report various topics are discussed such as nature and role of costing system, recording

and analysis of cost information, apportionment of costs according to organisational

requirements etc. Analysis of deviations from budgets, reporting of them to the management and

ability to use information which is gathered from costing system in decision making is also

covered in this report.

TASK 1

1.1 Purpose of internal reporting and providing accurate information to management

Purpose of internal reporting: Internal reporting is conducted in all the business entities

to analyse that organisation is performing well or not. If it is not good then strategic decisions

can be taken by the managers in order to improve it.

Purpose of providing accurate information to management: It is very important to

provide accurate, reliable and appropriate information to the management. Main purpose of this,

is to facilitate managers in making right decisions for business and its betterment.

1.2 Relationship between various costing systems

All the business entities use two major type of costing system these are job and process

costing systems. Both of them are interrelated with each other. In job costing material, labour

and overheads are recorded for every task which is performed by the company. In second method

all these elements are transcribed for entire production procedure (Yang and Chen, 2018).

When managers have any problem regarding production process as brief information is

recorded in it, then job costing can be used to get detailed information for each expense hence

both are related to each other.

1

Cost and revenues are two separate elements of a business. Cost is the total amount which

is involved in the manufacturing process of a products and revenues are the incomes that are

generated by a business entity on the sales of those items. All the expenses that are related to

material, labour and other overheads are considered by the companies while deciding prices of

their manufactured products. This assignment is based on the concept of these two components.

In this report various topics are discussed such as nature and role of costing system, recording

and analysis of cost information, apportionment of costs according to organisational

requirements etc. Analysis of deviations from budgets, reporting of them to the management and

ability to use information which is gathered from costing system in decision making is also

covered in this report.

TASK 1

1.1 Purpose of internal reporting and providing accurate information to management

Purpose of internal reporting: Internal reporting is conducted in all the business entities

to analyse that organisation is performing well or not. If it is not good then strategic decisions

can be taken by the managers in order to improve it.

Purpose of providing accurate information to management: It is very important to

provide accurate, reliable and appropriate information to the management. Main purpose of this,

is to facilitate managers in making right decisions for business and its betterment.

1.2 Relationship between various costing systems

All the business entities use two major type of costing system these are job and process

costing systems. Both of them are interrelated with each other. In job costing material, labour

and overheads are recorded for every task which is performed by the company. In second method

all these elements are transcribed for entire production procedure (Yang and Chen, 2018).

When managers have any problem regarding production process as brief information is

recorded in it, then job costing can be used to get detailed information for each expense hence

both are related to each other.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 Identification of responsibility, cost, profit and investment centres

Responsibility centre: It is subunit of a company for which a manager has responsibility

and authority. These are the different functional departments within an organisation such as

finance, marketing, human resource, IT etc.

Cost centre: It is a cost department of a business entity in which all the staff members

and managers are responsible for costs related decisions not revenues. It includes production,

maintenance and quality control divisions.

Profit centre: It is a central part of an enterprise which is responsible to make higher

contribution in organisational profits. It includes selling department of the company.

Investment centre: It is an internal department of an organisation which utilises capital

and funds appropriately in order to enhance overall profitability of the company. Sales and

manufacturing departments are considered as the part of this centre.

1.4 Characteristics of different types of cost classifications and their use

There are five types of cost classifications by nature, in relation to cost centre, by time,

for decision making and by nature of production process. Characteristics of all of them are as

follows:

It helps to make best decisions for the organisation by segregating costs in various parts.

All the classified costs helps to estimate expenses that may take place in future and then

managers can plan in advance to bear them.

Uses of classification of costs:

Classified costs are used to determine each cost which has been occurred in

manufacturing process.

These are also used to allot appropriate funds to different functional departments of the

company according to their requirements by analysing their costs.

1.5 Difference between marginal and absorption costing

Marginal costing Absorption costing

This method is used to separate fixed and

variable costs.

It is used to absorb all the expenses from the

sales of units.

In this costing technique costs are classified in

fixed and variable.

In this method overheads are classified in

production, administration, selling and

2

Responsibility centre: It is subunit of a company for which a manager has responsibility

and authority. These are the different functional departments within an organisation such as

finance, marketing, human resource, IT etc.

Cost centre: It is a cost department of a business entity in which all the staff members

and managers are responsible for costs related decisions not revenues. It includes production,

maintenance and quality control divisions.

Profit centre: It is a central part of an enterprise which is responsible to make higher

contribution in organisational profits. It includes selling department of the company.

Investment centre: It is an internal department of an organisation which utilises capital

and funds appropriately in order to enhance overall profitability of the company. Sales and

manufacturing departments are considered as the part of this centre.

1.4 Characteristics of different types of cost classifications and their use

There are five types of cost classifications by nature, in relation to cost centre, by time,

for decision making and by nature of production process. Characteristics of all of them are as

follows:

It helps to make best decisions for the organisation by segregating costs in various parts.

All the classified costs helps to estimate expenses that may take place in future and then

managers can plan in advance to bear them.

Uses of classification of costs:

Classified costs are used to determine each cost which has been occurred in

manufacturing process.

These are also used to allot appropriate funds to different functional departments of the

company according to their requirements by analysing their costs.

1.5 Difference between marginal and absorption costing

Marginal costing Absorption costing

This method is used to separate fixed and

variable costs.

It is used to absorb all the expenses from the

sales of units.

In this costing technique costs are classified in

fixed and variable.

In this method overheads are classified in

production, administration, selling and

2

distribution expenses (Difference between

marginal and absorption costing, 2019).

TASK 2

2.1 Record of cost information for material, labour and expenses

Costing procedure is the activity of recording costs in appropriate accounts so that actual

expenses can be determined that have taken place in manufacturing process. There are various

types of costs that are faced by an organisation. These are material, labour and overheads (Wang

and et.al., 2015).

There are three different types of materials that are raw, work in progress and finished

goods. It includes direct and indirect and timbers for constructing house is an example of such

expenses. Labours are the workers who are working in an organisation to manufacture products.

These are the total of wages that are paid to the workforce.

There are two main types of overheads that are operating that are related to revenue

generation process and non operating that are concerned with business execution process. Power,

heat, postage, legal charges are example of them.

2.2 Analysis of cost information for material, labour and expenses

Material costs are recorded on the basis of total requirement of production or the desired

units that are going to be manufactured by the company. It is a variable expense that changes

with total production units. Labour cost is recorded on the basis of total workers who are

involved in manufacturing process. It depends upon total items that are made by the company if

it decreases or increases then wages paid to work force will also vary (Sufian and Kamarudin,

2015).

There are various types of expenses that are faced by all the business entities while

producing products. Some of them are fixed and other are variable. These are rent, depreciation,

insurance premium etc.

2.3 Various stages of inventory

There are three different stages of inventory, all of them are as follows:

Raw material: It is the first stage of inventory which is used to make a product. It is also

known as unprocessed material and feed stock.

3

marginal and absorption costing, 2019).

TASK 2

2.1 Record of cost information for material, labour and expenses

Costing procedure is the activity of recording costs in appropriate accounts so that actual

expenses can be determined that have taken place in manufacturing process. There are various

types of costs that are faced by an organisation. These are material, labour and overheads (Wang

and et.al., 2015).

There are three different types of materials that are raw, work in progress and finished

goods. It includes direct and indirect and timbers for constructing house is an example of such

expenses. Labours are the workers who are working in an organisation to manufacture products.

These are the total of wages that are paid to the workforce.

There are two main types of overheads that are operating that are related to revenue

generation process and non operating that are concerned with business execution process. Power,

heat, postage, legal charges are example of them.

2.2 Analysis of cost information for material, labour and expenses

Material costs are recorded on the basis of total requirement of production or the desired

units that are going to be manufactured by the company. It is a variable expense that changes

with total production units. Labour cost is recorded on the basis of total workers who are

involved in manufacturing process. It depends upon total items that are made by the company if

it decreases or increases then wages paid to work force will also vary (Sufian and Kamarudin,

2015).

There are various types of expenses that are faced by all the business entities while

producing products. Some of them are fixed and other are variable. These are rent, depreciation,

insurance premium etc.

2.3 Various stages of inventory

There are three different stages of inventory, all of them are as follows:

Raw material: It is the first stage of inventory which is used to make a product. It is also

known as unprocessed material and feed stock.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

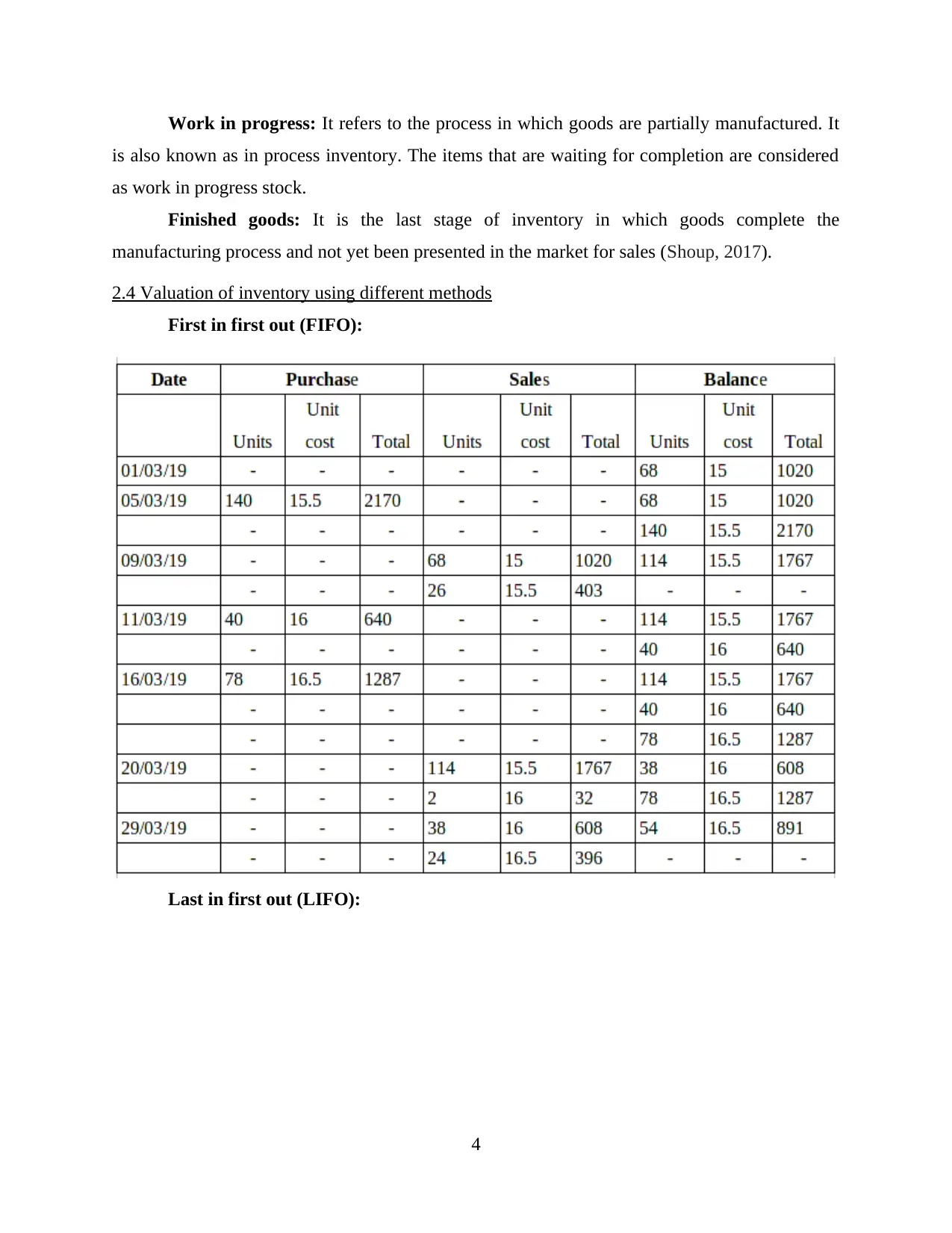

Work in progress: It refers to the process in which goods are partially manufactured. It

is also known as in process inventory. The items that are waiting for completion are considered

as work in progress stock.

Finished goods: It is the last stage of inventory in which goods complete the

manufacturing process and not yet been presented in the market for sales (Shoup, 2017).

2.4 Valuation of inventory using different methods

First in first out (FIFO):

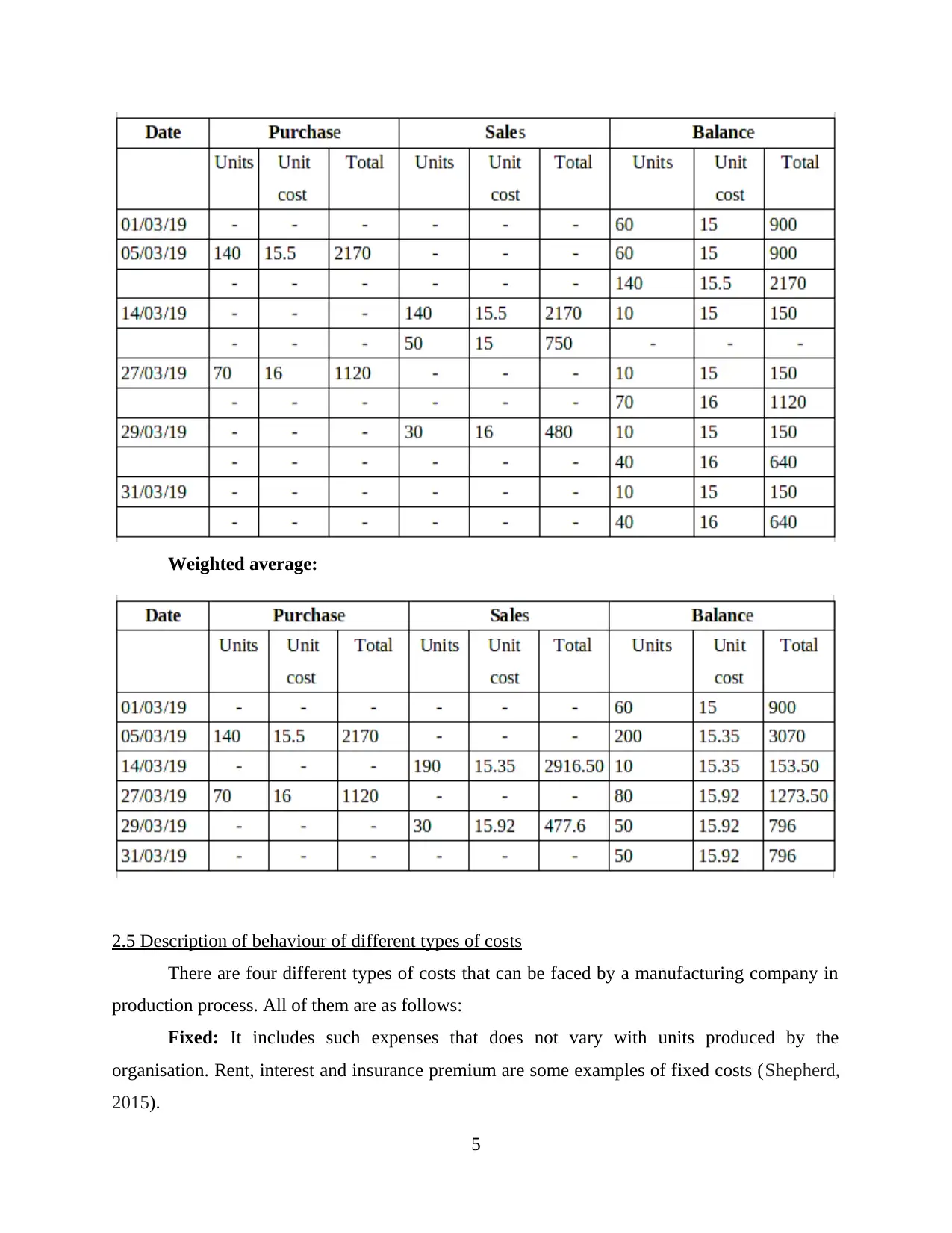

Last in first out (LIFO):

4

is also known as in process inventory. The items that are waiting for completion are considered

as work in progress stock.

Finished goods: It is the last stage of inventory in which goods complete the

manufacturing process and not yet been presented in the market for sales (Shoup, 2017).

2.4 Valuation of inventory using different methods

First in first out (FIFO):

Last in first out (LIFO):

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Weighted average:

2.5 Description of behaviour of different types of costs

There are four different types of costs that can be faced by a manufacturing company in

production process. All of them are as follows:

Fixed: It includes such expenses that does not vary with units produced by the

organisation. Rent, interest and insurance premium are some examples of fixed costs (Shepherd,

2015).

5

2.5 Description of behaviour of different types of costs

There are four different types of costs that can be faced by a manufacturing company in

production process. All of them are as follows:

Fixed: It includes such expenses that does not vary with units produced by the

organisation. Rent, interest and insurance premium are some examples of fixed costs (Shepherd,

2015).

5

Variable: The costs that changes due to increment or decrement of production units. In

other words it can be defined as the marginal expenses over all the items that are manufactured

by the organisation. It includes direct material, fright outward etc.

Semi variable: The expenses that are partially fixed and partly variable. As it is a

mixture of fixed and uncertain costs hence it is also named as mixed cost. Depreciation is the

main example of this cost.

Stepped: It is a fixed cost with some certain boundaries when the limit is crossed then it

will get changed. It is an additional investment which is required to increase the production

(Stepped cost, 2019).

2.6 Record of cost information using different costing systems

Job: In job costing method costs of every task which is performed by the organisation is

recorded. Managers may get detailed information of expenses that have taken place for that are

faced by the company.

Batch: This method is used to take homogeneous products as cost unit for organisation.

In this costing technique a batch includes a particular number of items or articles.

Unit: In this system cost that has taken place for manufacturing a specific unit of product

is recorded. All fixed and variable expenses related to one item is considered in this method.

Process: Costs related to production process is recorded in this method. It is mainly used

in those companies which manufactures products in large quantities.

Service: In this costing technique expenses related to each service rendered by a

company is recorded. It is mainly used in hospitality industry.

TASK 3

3.1 Attribution of overhead cost to production and service cost centres using agreed bases

There are two main types of attribution of overhead costs. Both of them are described

below:

Direct: It is the most popular method of cost attribution. Main purpose of this technique

top allot costs to all production departments that are related to service division (Cost allocation

methods, 2019).

6

other words it can be defined as the marginal expenses over all the items that are manufactured

by the organisation. It includes direct material, fright outward etc.

Semi variable: The expenses that are partially fixed and partly variable. As it is a

mixture of fixed and uncertain costs hence it is also named as mixed cost. Depreciation is the

main example of this cost.

Stepped: It is a fixed cost with some certain boundaries when the limit is crossed then it

will get changed. It is an additional investment which is required to increase the production

(Stepped cost, 2019).

2.6 Record of cost information using different costing systems

Job: In job costing method costs of every task which is performed by the organisation is

recorded. Managers may get detailed information of expenses that have taken place for that are

faced by the company.

Batch: This method is used to take homogeneous products as cost unit for organisation.

In this costing technique a batch includes a particular number of items or articles.

Unit: In this system cost that has taken place for manufacturing a specific unit of product

is recorded. All fixed and variable expenses related to one item is considered in this method.

Process: Costs related to production process is recorded in this method. It is mainly used

in those companies which manufactures products in large quantities.

Service: In this costing technique expenses related to each service rendered by a

company is recorded. It is mainly used in hospitality industry.

TASK 3

3.1 Attribution of overhead cost to production and service cost centres using agreed bases

There are two main types of attribution of overhead costs. Both of them are described

below:

Direct: It is the most popular method of cost attribution. Main purpose of this technique

top allot costs to all production departments that are related to service division (Cost allocation

methods, 2019).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Step Down: In this method only some specific costs are considered such as those

expenses that are incurred by human resource and maintenance department of the organisation. It

is responsible to provide rank to service divisions according to their performance.

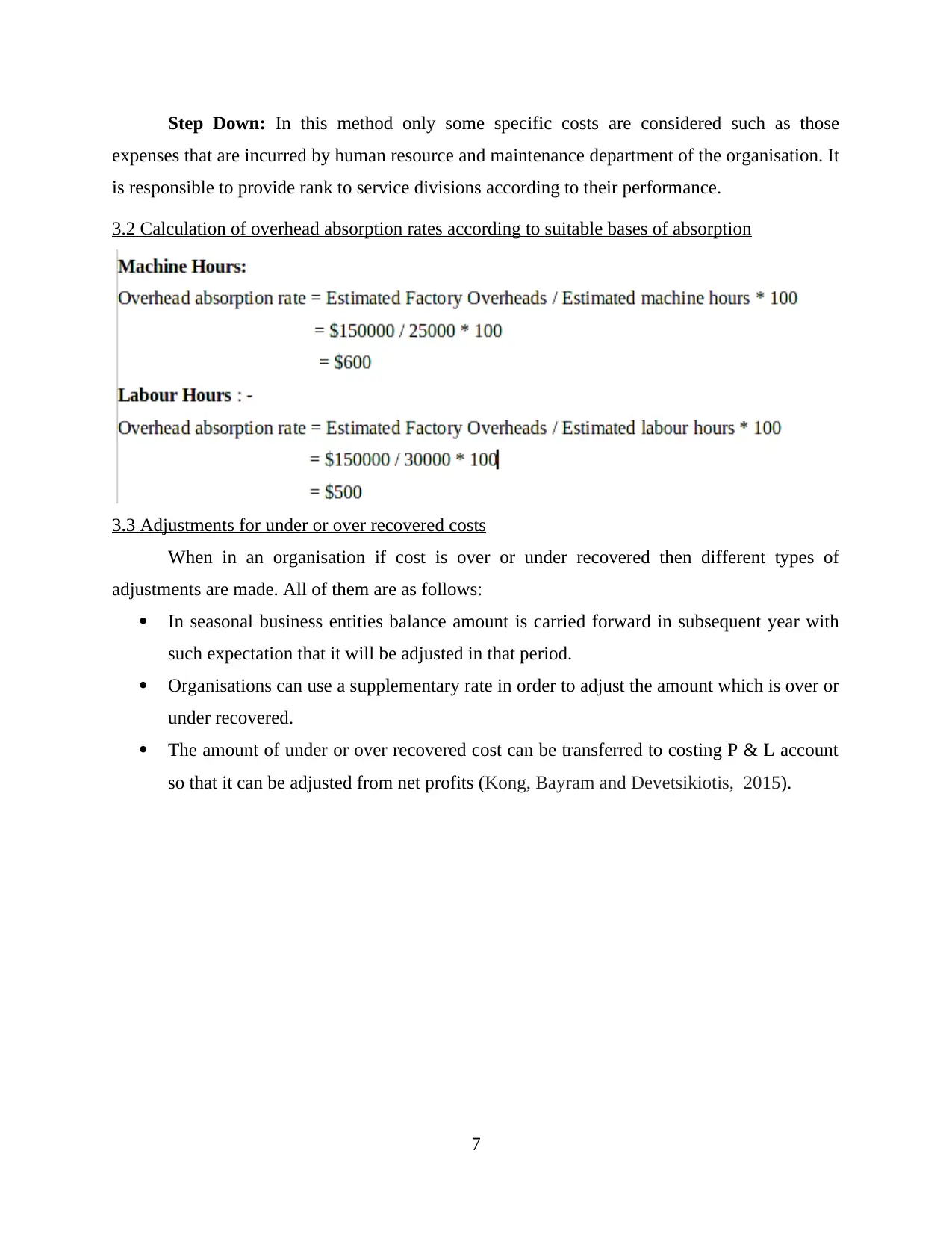

3.2 Calculation of overhead absorption rates according to suitable bases of absorption

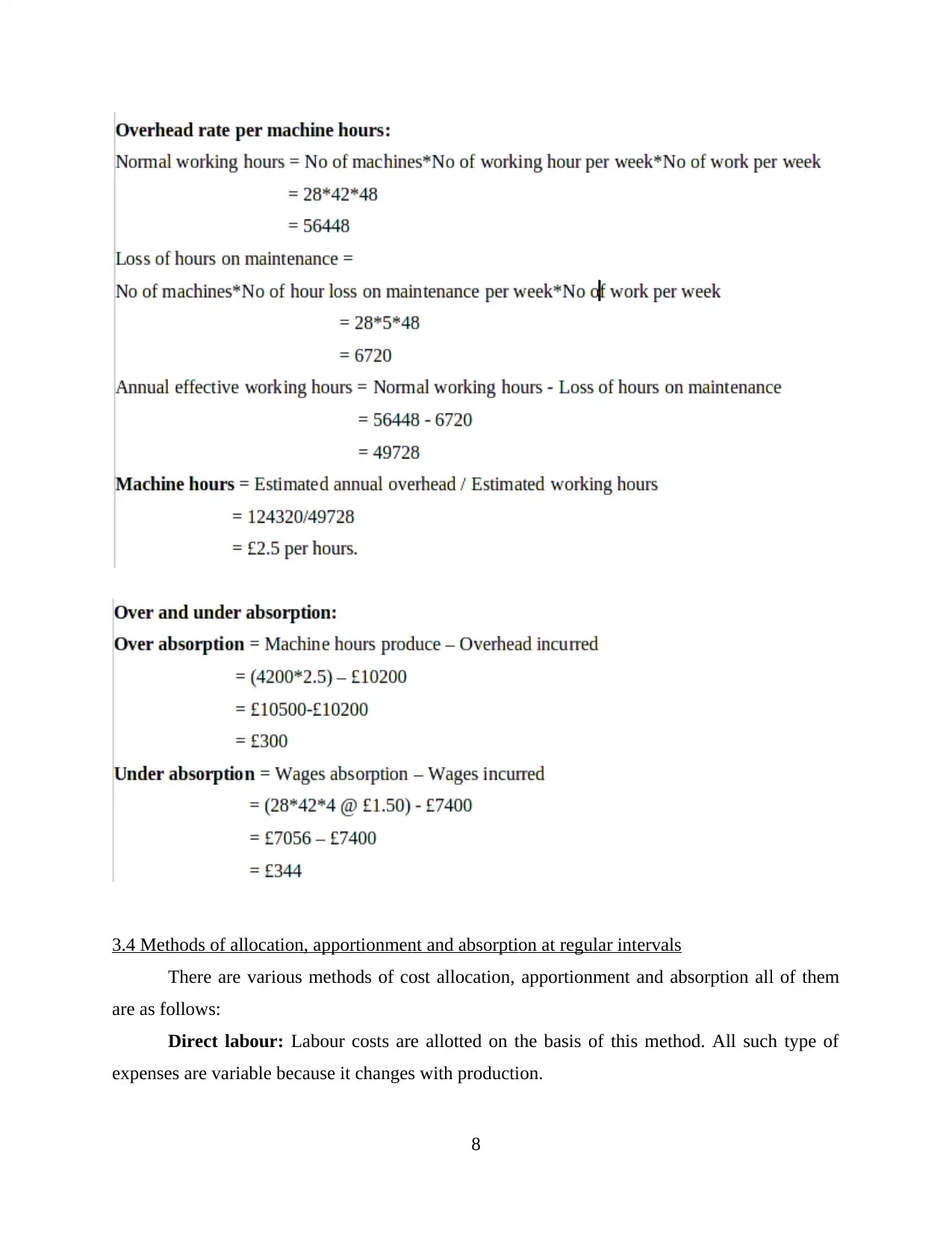

3.3 Adjustments for under or over recovered costs

When in an organisation if cost is over or under recovered then different types of

adjustments are made. All of them are as follows:

In seasonal business entities balance amount is carried forward in subsequent year with

such expectation that it will be adjusted in that period.

Organisations can use a supplementary rate in order to adjust the amount which is over or

under recovered.

The amount of under or over recovered cost can be transferred to costing P & L account

so that it can be adjusted from net profits (Kong, Bayram and Devetsikiotis, 2015).

7

expenses that are incurred by human resource and maintenance department of the organisation. It

is responsible to provide rank to service divisions according to their performance.

3.2 Calculation of overhead absorption rates according to suitable bases of absorption

3.3 Adjustments for under or over recovered costs

When in an organisation if cost is over or under recovered then different types of

adjustments are made. All of them are as follows:

In seasonal business entities balance amount is carried forward in subsequent year with

such expectation that it will be adjusted in that period.

Organisations can use a supplementary rate in order to adjust the amount which is over or

under recovered.

The amount of under or over recovered cost can be transferred to costing P & L account

so that it can be adjusted from net profits (Kong, Bayram and Devetsikiotis, 2015).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.4 Methods of allocation, apportionment and absorption at regular intervals

There are various methods of cost allocation, apportionment and absorption all of them

are as follows:

Direct labour: Labour costs are allotted on the basis of this method. All such type of

expenses are variable because it changes with production.

8

There are various methods of cost allocation, apportionment and absorption all of them

are as follows:

Direct labour: Labour costs are allotted on the basis of this method. All such type of

expenses are variable because it changes with production.

8

Machine time: It is another method of cost allocation and absorption in which expenses

are absorbed and allotted on the basis of total machine hours. When equipments are not used at

that time it becomes zero.

Square footage: Rent and other expenses are allotted on the basis of this method. These

are fixed and does not vary with manufactured units. Whether the organisation is producing

items or not it is required to be faced (Sahoo, Mehdiloozad and Tone, 2014).

3.5 Communication with staff to resolve queries related to overhead cost data

For every manager it is very important to resolve all the queries that are related to

overhead cost data so that it can be analysed that all of them are relevant to production or not.

The information can be gathered by conducting a formal meeting or evaluating reports that are

generated by the workers (Kimball, 2014).

TASK 4

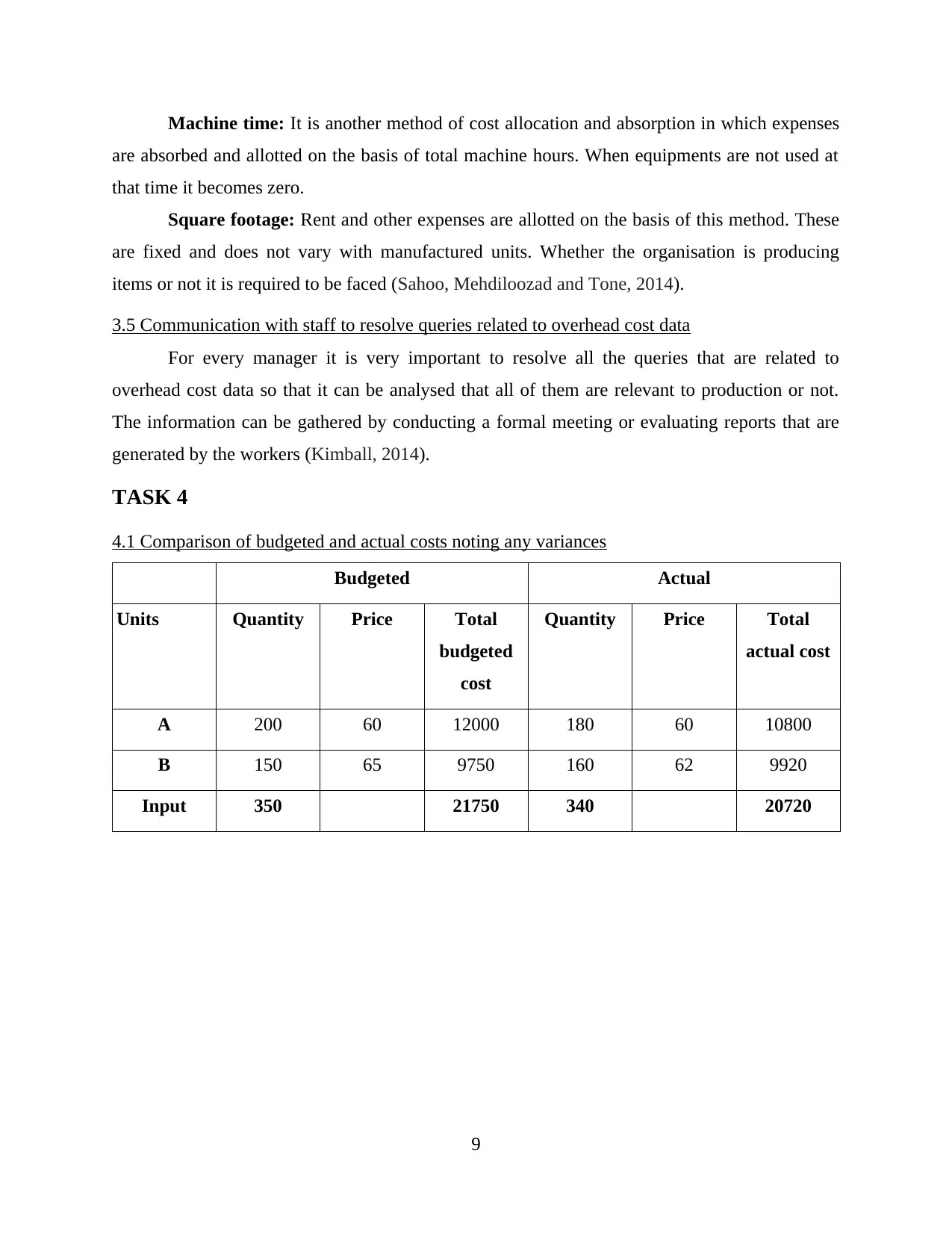

4.1 Comparison of budgeted and actual costs noting any variances

Budgeted Actual

Units Quantity Price Total

budgeted

cost

Quantity Price Total

actual cost

A 200 60 12000 180 60 10800

B 150 65 9750 160 62 9920

Input 350 21750 340 20720

9

are absorbed and allotted on the basis of total machine hours. When equipments are not used at

that time it becomes zero.

Square footage: Rent and other expenses are allotted on the basis of this method. These

are fixed and does not vary with manufactured units. Whether the organisation is producing

items or not it is required to be faced (Sahoo, Mehdiloozad and Tone, 2014).

3.5 Communication with staff to resolve queries related to overhead cost data

For every manager it is very important to resolve all the queries that are related to

overhead cost data so that it can be analysed that all of them are relevant to production or not.

The information can be gathered by conducting a formal meeting or evaluating reports that are

generated by the workers (Kimball, 2014).

TASK 4

4.1 Comparison of budgeted and actual costs noting any variances

Budgeted Actual

Units Quantity Price Total

budgeted

cost

Quantity Price Total

actual cost

A 200 60 12000 180 60 10800

B 150 65 9750 160 62 9920

Input 350 21750 340 20720

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.