Comprehensive Cost and Revenue Analysis Report for ABC Ltd, UK

VerifiedAdded on 2020/11/12

|17

|4150

|352

Report

AI Summary

This report provides a comprehensive analysis of cost and revenue for ABC Ltd, a UK-based organization. It begins with an introduction to internal reporting and the relationships between various costing systems, including standard, marginal, and absorption costing. The report identifies responsibility centers and explores different cost classifications, such as fixed, variable, and semi-variable costs. It details the recording and analysis of cost information for materials, labor, and expenses, along with an examination of inventory valuation methods like FIFO, LIFO, and weighted average. Furthermore, the report addresses overhead cost allocation, absorption rates, and variance analysis, comparing budget costs with actual costs. Finally, it explores the effect of changing activity levels on unit costs and factors affecting short-term and long-term decision-making processes. The report utilizes data and examples relevant to ABC Ltd's operations, providing a practical perspective on financial management.

COST AND REVENUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose of internal reporting.................................................................................................1

1.2 Relationship between various costing system within organisation.......................................1

1.3 Identify the responsibility centres, cost centres, profit centres and investment centres........2

Cost centres:................................................................................................................................2

Profit centres:..............................................................................................................................2

1.4 Characteristics of different types of cost classification and its uses in costing.....................2

1.5 Explain the difference between marginal and absorption costing. ......................................3

TASK 2............................................................................................................................................3

2.1 Record cost information for material, labour and expenses in accordance with organisation

costing procedures.......................................................................................................................3

2.2 Analyse cost information for material, labour and expenses in accordance with

organisation's costing procedures................................................................................................3

2.3 Define various stages of inventory........................................................................................3

2.4 Value of inventory.................................................................................................................4

2.5 Behaviour of costs.................................................................................................................6

2.6 Record cost information using cost system...........................................................................6

TASK 3............................................................................................................................................7

3.1 Attribute overhead costs to production and services cost centre..........................................7

3.2 Calculate overhead absorption rates......................................................................................7

3.3 Adjustments for under or over recovered overhead costs.....................................................8

Adjustments:...............................................................................................................................8

3.4 Methods of allocation, apportionment and absorption at regular intervals, implementing

agreed changes to methods..........................................................................................................8

3.5 Communicate with relevant staff to resolve any queries in overhead cost data...................9

TASK 4..........................................................................................................................................10

4.1 Compare budget costs with actual costs, noting any variances..........................................10

4.2 Analyse variances for management reports........................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose of internal reporting.................................................................................................1

1.2 Relationship between various costing system within organisation.......................................1

1.3 Identify the responsibility centres, cost centres, profit centres and investment centres........2

Cost centres:................................................................................................................................2

Profit centres:..............................................................................................................................2

1.4 Characteristics of different types of cost classification and its uses in costing.....................2

1.5 Explain the difference between marginal and absorption costing. ......................................3

TASK 2............................................................................................................................................3

2.1 Record cost information for material, labour and expenses in accordance with organisation

costing procedures.......................................................................................................................3

2.2 Analyse cost information for material, labour and expenses in accordance with

organisation's costing procedures................................................................................................3

2.3 Define various stages of inventory........................................................................................3

2.4 Value of inventory.................................................................................................................4

2.5 Behaviour of costs.................................................................................................................6

2.6 Record cost information using cost system...........................................................................6

TASK 3............................................................................................................................................7

3.1 Attribute overhead costs to production and services cost centre..........................................7

3.2 Calculate overhead absorption rates......................................................................................7

3.3 Adjustments for under or over recovered overhead costs.....................................................8

Adjustments:...............................................................................................................................8

3.4 Methods of allocation, apportionment and absorption at regular intervals, implementing

agreed changes to methods..........................................................................................................8

3.5 Communicate with relevant staff to resolve any queries in overhead cost data...................9

TASK 4..........................................................................................................................................10

4.1 Compare budget costs with actual costs, noting any variances..........................................10

4.2 Analyse variances for management reports........................................................................10

4.3 Information for budget holders of any significant variances, making valid suggestion.....10

4.4 Prepare management reports in an appropriate format, presenting these within the required

timescales..................................................................................................................................10

TASK 5..........................................................................................................................................11

5.1 Preparation estimates of future income and costs for decision making using:...................11

5.2 The effect of changing activity levels on unit costs............................................................11

5.3 Calculate the effect of changing activity levels on unit costs.............................................11

5.4 Identify factors affecting short-term and long-term decision making................................12

REFERENCES..............................................................................................................................13

4.4 Prepare management reports in an appropriate format, presenting these within the required

timescales..................................................................................................................................10

TASK 5..........................................................................................................................................11

5.1 Preparation estimates of future income and costs for decision making using:...................11

5.2 The effect of changing activity levels on unit costs............................................................11

5.3 Calculate the effect of changing activity levels on unit costs.............................................11

5.4 Identify factors affecting short-term and long-term decision making................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In every organisation cost and revenue is the essential financial components to produce,

retail, research and manufacture something. Cost in monetary values which has to be paid in

order to buy something.(Clotfelter, 2014).Revenue is the income that company earn from selling

of product and services. Organisation chosen for this report is ABC Ltd. which is located in

London, UK. The aim of report is to identify nature and role of costing system in organisation.

Cost information for material, labour and expenses records and analysis are mentioned in this

report. Various stages of inventory and value inventory are explained by using FIFO AND LIFO.

Absorption cost are mentioned according to ABC Ltd. Analysis deviation from budget and report

along with this for decision making assist to costing systems are mentioned in this report.

TASK 1

1.1 Purpose of internal reporting.

Internal reporting is an important financial components and collection of other data which

is accumulated by employees and distributed within company to improve the performance. It

helps organisation to understand performance of business at operational level. The purpose of

this report is to provide the clear information about financial position of business. ABC Ltd. used

this report to know that performance of enterprises which helps them to take strategic decisions.

Also, it provides accurate information about the using of cash, financial, internal audit, budget

reports, variance analysis. It provides accurate information to management as this reports are

prepared after preparing cash report, budget books, internal audit reports and variance reports.

1.2 Relationship between various costing system within organisation.

Costing system is the framework used to estimation of product cost for valuation of

inventory, cost control and profit analysis (Jeziorski, 2014). Some of various costing system used

in the ABC Ltd. are mentioned below:

Standard costing system:

In this system standard cost are determined and variance analysis and measurement are

done to control the cost. In ABC Ltd. this system is used as it provides them base for stock

valuation and work in progress.

Marginal costing:

1

In every organisation cost and revenue is the essential financial components to produce,

retail, research and manufacture something. Cost in monetary values which has to be paid in

order to buy something.(Clotfelter, 2014).Revenue is the income that company earn from selling

of product and services. Organisation chosen for this report is ABC Ltd. which is located in

London, UK. The aim of report is to identify nature and role of costing system in organisation.

Cost information for material, labour and expenses records and analysis are mentioned in this

report. Various stages of inventory and value inventory are explained by using FIFO AND LIFO.

Absorption cost are mentioned according to ABC Ltd. Analysis deviation from budget and report

along with this for decision making assist to costing systems are mentioned in this report.

TASK 1

1.1 Purpose of internal reporting.

Internal reporting is an important financial components and collection of other data which

is accumulated by employees and distributed within company to improve the performance. It

helps organisation to understand performance of business at operational level. The purpose of

this report is to provide the clear information about financial position of business. ABC Ltd. used

this report to know that performance of enterprises which helps them to take strategic decisions.

Also, it provides accurate information about the using of cash, financial, internal audit, budget

reports, variance analysis. It provides accurate information to management as this reports are

prepared after preparing cash report, budget books, internal audit reports and variance reports.

1.2 Relationship between various costing system within organisation.

Costing system is the framework used to estimation of product cost for valuation of

inventory, cost control and profit analysis (Jeziorski, 2014). Some of various costing system used

in the ABC Ltd. are mentioned below:

Standard costing system:

In this system standard cost are determined and variance analysis and measurement are

done to control the cost. In ABC Ltd. this system is used as it provides them base for stock

valuation and work in progress.

Marginal costing:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This system categorized cost into fixed cost and variable cost. This system is used by

ABC Ltd. as it helps them to make decision for internal management. There is no any relation

between the standard and marginal (Zoltan and Erzsebe, 2017 ). Because, marginal is the method

that can describe the method of per unit cost of incremented production. Whereas standard

costing is the part of budgetary control that helps in forecasting process.

1.3 Identify the responsibility centres, cost centres, profit centres and investment centres.

Responsibility centre is the functional part of organisation and it is headed by manager,

who holds the responsibilities. ABC Ltd. has this centre as manager of this centre have

responsibility to controls the profit, cost, revenues and investments.

Cost centres:

Cost centre is a part of company where manager is accountable for cost incurred. In ABC

Ltd. has this centre give detailed about the cost which is incurred during business operations.

Profit centres:

Profit centre is a section whose manager is answerable for cost as well as revenue. In

ABC Ltd. has this centre as it makes manger to find ways so that revenue of centre may increase

by improving methods of distribution (Stephan and et.al, 2016).

Investment centres:

Investment centres is basically related with the use for the business units within an

organisation. This seems to be an important elements of an investment centre are treated as unit

which can be measure against their use of capital. ABC Ltd. has this centre as manager that can

develop credit policy for the company which ascertain the inventory investment during the

period of time.

1.4 Characteristics of different types of cost classification and its uses in costing.

Cost classification is the state of expenditure into various categorises. Cost are classified

in ABC Ltd. by following ways:

Fixed cost: It cannot vary on the change with the production activities. Fixed cost remain

constant at every level of production. Per unit cost decrease in case volume of results is

increased.

2

ABC Ltd. as it helps them to make decision for internal management. There is no any relation

between the standard and marginal (Zoltan and Erzsebe, 2017 ). Because, marginal is the method

that can describe the method of per unit cost of incremented production. Whereas standard

costing is the part of budgetary control that helps in forecasting process.

1.3 Identify the responsibility centres, cost centres, profit centres and investment centres.

Responsibility centre is the functional part of organisation and it is headed by manager,

who holds the responsibilities. ABC Ltd. has this centre as manager of this centre have

responsibility to controls the profit, cost, revenues and investments.

Cost centres:

Cost centre is a part of company where manager is accountable for cost incurred. In ABC

Ltd. has this centre give detailed about the cost which is incurred during business operations.

Profit centres:

Profit centre is a section whose manager is answerable for cost as well as revenue. In

ABC Ltd. has this centre as it makes manger to find ways so that revenue of centre may increase

by improving methods of distribution (Stephan and et.al, 2016).

Investment centres:

Investment centres is basically related with the use for the business units within an

organisation. This seems to be an important elements of an investment centre are treated as unit

which can be measure against their use of capital. ABC Ltd. has this centre as manager that can

develop credit policy for the company which ascertain the inventory investment during the

period of time.

1.4 Characteristics of different types of cost classification and its uses in costing.

Cost classification is the state of expenditure into various categorises. Cost are classified

in ABC Ltd. by following ways:

Fixed cost: It cannot vary on the change with the production activities. Fixed cost remain

constant at every level of production. Per unit cost decrease in case volume of results is

increased.

2

Variable cost: It has been seen that variability of the total amount in direct proportion to

volume is been taken into account. Comparatively constant cost per unit in the face of changing

volume is also effective characteristic of this cost (Schofield, 2018).

1.5 Explain the difference between marginal and absorption costing

Marginal costing Absorption costing

It is method of decision making which is used

to determine total production cost.

It is the techniques which applied in whole cost

of production to all products produced.

ABC Ltd. use this costing to measure profit by

profit volume ratio.

And this is used by company for allocation of

total cost in cost centre.

This results in contribution per unit. This results in net profit per unit.

TASK 2

2.1 Record cost information for material, labour and expenses in accordance with organisation

costing procedures

Particulars Amount($)

Expenses 150000

Labour 90000

Raw Material 110000

Direct material:

These are the materials which directly identified in goods. Such materials are paper,

bricks and so on.

Direct labour:

These are individuals who works for the organisation. For examples- If it is a

manufacturing company, direct labour are employees manufacturing products.

Direct expenses:

These are expense which incurred directly according to change in product volume. Some

direct expenses are services, product lines and so on.

3

volume is been taken into account. Comparatively constant cost per unit in the face of changing

volume is also effective characteristic of this cost (Schofield, 2018).

1.5 Explain the difference between marginal and absorption costing

Marginal costing Absorption costing

It is method of decision making which is used

to determine total production cost.

It is the techniques which applied in whole cost

of production to all products produced.

ABC Ltd. use this costing to measure profit by

profit volume ratio.

And this is used by company for allocation of

total cost in cost centre.

This results in contribution per unit. This results in net profit per unit.

TASK 2

2.1 Record cost information for material, labour and expenses in accordance with organisation

costing procedures

Particulars Amount($)

Expenses 150000

Labour 90000

Raw Material 110000

Direct material:

These are the materials which directly identified in goods. Such materials are paper,

bricks and so on.

Direct labour:

These are individuals who works for the organisation. For examples- If it is a

manufacturing company, direct labour are employees manufacturing products.

Direct expenses:

These are expense which incurred directly according to change in product volume. Some

direct expenses are services, product lines and so on.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2 Analyse cost information for material, labour and expenses in accordance with organisation's

costing procedures.

Cost incurred in expenses $ 150000, labour $ 90000 and raw material 110000. After

analysing cost information, it is observed that ABC Ltd. Overheads expenses are more than

labour and raw-materials. So, it indicates that company is not controlling their expenses which

affects profitability margin.

2.3 Define various stages of inventory.

Inventory is the accumulation of unsold products which is to be sold (Sgroi, 2015). For

producing goods various stages of inventory are mentioned below:

Raw materials:

This is the initial stage of inventory, which is basic materials that are used by company to

produce finished products. ABC Ltd. use some raw materials to manufacture goods.

Work in progress:

After pulling raw materials in manufacturing the final products now ABC Ltd. Proceeds

to further stage that is work in progress, it is undergoing process which shows the progress of

work in production process (Schmid, Götze and Sygulla, 2015).

Finished goods:

After completing production process, cost related with raw materials and work in

progress are transferral to finished goods. At this stages of inventory, the products of ABC Ltd.

are successfully manufactured.

2.4 Value of inventory.

Valuation of inventory is done in ABC Ltd. By two methods:

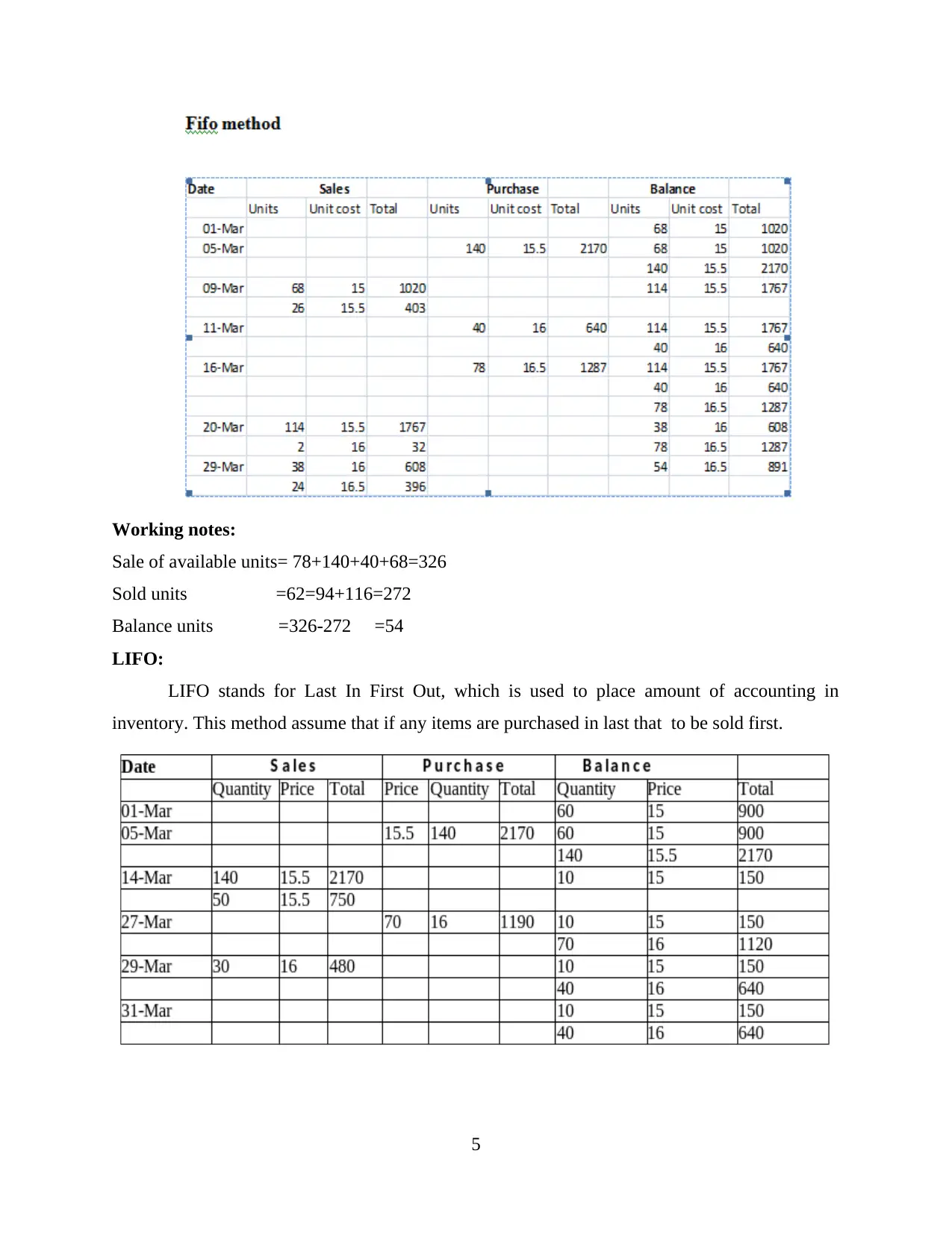

FIFO:

FIFO stands for First In First Out, it is process to find out value of inventory where

assumption of cost flow are that purchase of first products to be sold first.

4

costing procedures.

Cost incurred in expenses $ 150000, labour $ 90000 and raw material 110000. After

analysing cost information, it is observed that ABC Ltd. Overheads expenses are more than

labour and raw-materials. So, it indicates that company is not controlling their expenses which

affects profitability margin.

2.3 Define various stages of inventory.

Inventory is the accumulation of unsold products which is to be sold (Sgroi, 2015). For

producing goods various stages of inventory are mentioned below:

Raw materials:

This is the initial stage of inventory, which is basic materials that are used by company to

produce finished products. ABC Ltd. use some raw materials to manufacture goods.

Work in progress:

After pulling raw materials in manufacturing the final products now ABC Ltd. Proceeds

to further stage that is work in progress, it is undergoing process which shows the progress of

work in production process (Schmid, Götze and Sygulla, 2015).

Finished goods:

After completing production process, cost related with raw materials and work in

progress are transferral to finished goods. At this stages of inventory, the products of ABC Ltd.

are successfully manufactured.

2.4 Value of inventory.

Valuation of inventory is done in ABC Ltd. By two methods:

FIFO:

FIFO stands for First In First Out, it is process to find out value of inventory where

assumption of cost flow are that purchase of first products to be sold first.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working notes:

Sale of available units= 78+140+40+68=326

Sold units =62=94+116=272

Balance units =326-272 =54

LIFO:

LIFO stands for Last In First Out, which is used to place amount of accounting in

inventory. This method assume that if any items are purchased in last that to be sold first.

5

Sale of available units= 78+140+40+68=326

Sold units =62=94+116=272

Balance units =326-272 =54

LIFO:

LIFO stands for Last In First Out, which is used to place amount of accounting in

inventory. This method assume that if any items are purchased in last that to be sold first.

5

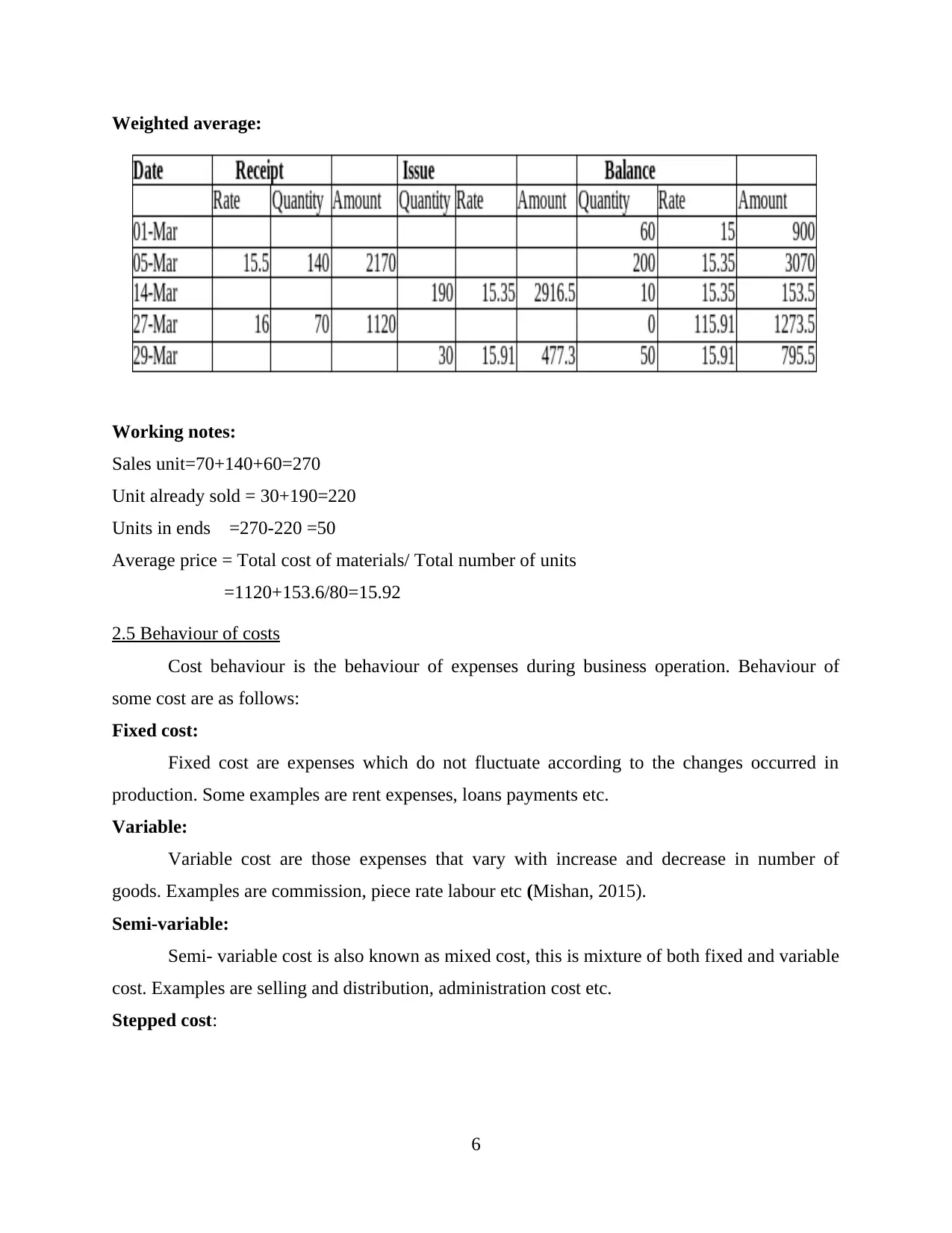

Weighted average:

Working notes:

Sales unit=70+140+60=270

Unit already sold = 30+190=220

Units in ends =270-220 =50

Average price = Total cost of materials/ Total number of units

=1120+153.6/80=15.92

2.5 Behaviour of costs

Cost behaviour is the behaviour of expenses during business operation. Behaviour of

some cost are as follows:

Fixed cost:

Fixed cost are expenses which do not fluctuate according to the changes occurred in

production. Some examples are rent expenses, loans payments etc.

Variable:

Variable cost are those expenses that vary with increase and decrease in number of

goods. Examples are commission, piece rate labour etc (Mishan, 2015).

Semi-variable:

Semi- variable cost is also known as mixed cost, this is mixture of both fixed and variable

cost. Examples are selling and distribution, administration cost etc.

Stepped cost:

6

Working notes:

Sales unit=70+140+60=270

Unit already sold = 30+190=220

Units in ends =270-220 =50

Average price = Total cost of materials/ Total number of units

=1120+153.6/80=15.92

2.5 Behaviour of costs

Cost behaviour is the behaviour of expenses during business operation. Behaviour of

some cost are as follows:

Fixed cost:

Fixed cost are expenses which do not fluctuate according to the changes occurred in

production. Some examples are rent expenses, loans payments etc.

Variable:

Variable cost are those expenses that vary with increase and decrease in number of

goods. Examples are commission, piece rate labour etc (Mishan, 2015).

Semi-variable:

Semi- variable cost is also known as mixed cost, this is mixture of both fixed and variable

cost. Examples are selling and distribution, administration cost etc.

Stepped cost:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It refers to the that cost which does not change steadily with the change in overall

activities volume, but at the discrete points it gets varies. It is used in making investment

decision and to decide whether to accept extra customer order (Massiani, 2015).

2.6 Record cost information using cost system.

To record cost information ABC Ltd. Use following cost system:

Job costing:

Job costing is a process which is used to record cost of production job instead of process.

By using this system cost of job are recorded and data are maintained that is applicable to

business operations.

Batch costing:

Batch costing is the method in which product making cost is calculated by batch instead

of a single products.

Unit costing:

This unit is also called single costing, by using this methods cost per unit is determined.

(Kumar and Reinartz, 2018)

Process costing:

This system is used to determine product cost at all stages of production. It is also a kind

of operation costing.

Service costing:

System costing is method that provides services in company rather than manufacturing

products.

TASK 3

3.1 Attribute overhead costs to production and services cost centre.

For producing any product it is essential for ABC Ltd to know about different types of

cost that incurred in manufacturing process are as follows:

Direct cost:

Direct cost is that price which directly traced the cost of specific product. Some examples

are commission, direct labour, piece rate wages, indirect material and so on.(Kitao, 2015)

Step down cost:

7

activities volume, but at the discrete points it gets varies. It is used in making investment

decision and to decide whether to accept extra customer order (Massiani, 2015).

2.6 Record cost information using cost system.

To record cost information ABC Ltd. Use following cost system:

Job costing:

Job costing is a process which is used to record cost of production job instead of process.

By using this system cost of job are recorded and data are maintained that is applicable to

business operations.

Batch costing:

Batch costing is the method in which product making cost is calculated by batch instead

of a single products.

Unit costing:

This unit is also called single costing, by using this methods cost per unit is determined.

(Kumar and Reinartz, 2018)

Process costing:

This system is used to determine product cost at all stages of production. It is also a kind

of operation costing.

Service costing:

System costing is method that provides services in company rather than manufacturing

products.

TASK 3

3.1 Attribute overhead costs to production and services cost centre.

For producing any product it is essential for ABC Ltd to know about different types of

cost that incurred in manufacturing process are as follows:

Direct cost:

Direct cost is that price which directly traced the cost of specific product. Some examples

are commission, direct labour, piece rate wages, indirect material and so on.(Kitao, 2015)

Step down cost:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Step down cost the process which is used to allot service departments cost to other

sections of services and also to operation divisions. Examples, company assign ranks to service

departments like S1, S2 and so on according to that cost are allocated.

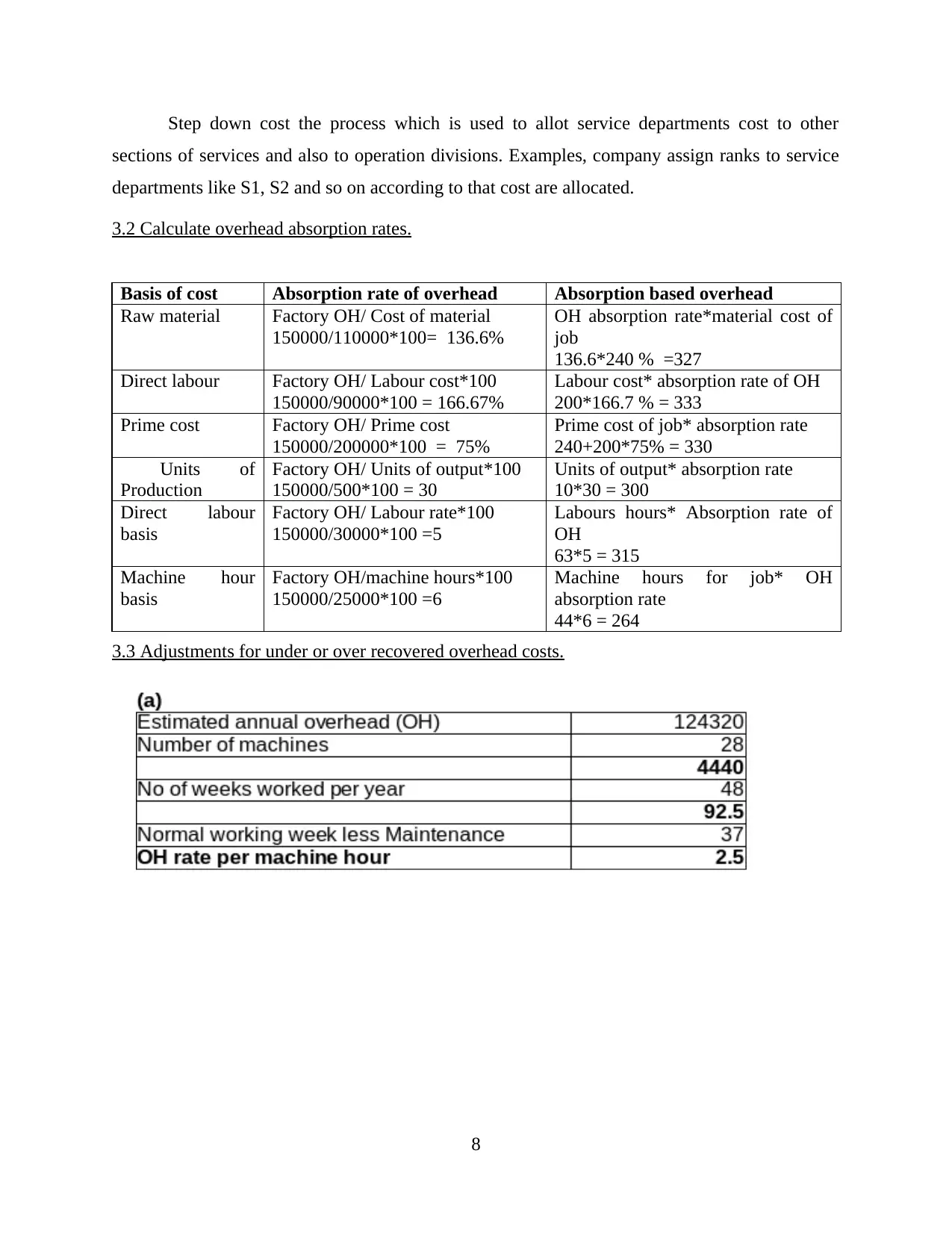

3.2 Calculate overhead absorption rates.

Basis of cost Absorption rate of overhead Absorption based overhead

Raw material Factory OH/ Cost of material

150000/110000*100= 136.6%

OH absorption rate*material cost of

job

136.6*240 % =327

Direct labour Factory OH/ Labour cost*100

150000/90000*100 = 166.67%

Labour cost* absorption rate of OH

200*166.7 % = 333

Prime cost Factory OH/ Prime cost

150000/200000*100 = 75%

Prime cost of job* absorption rate

240+200*75% = 330

Units of

Production

Factory OH/ Units of output*100

150000/500*100 = 30

Units of output* absorption rate

10*30 = 300

Direct labour

basis

Factory OH/ Labour rate*100

150000/30000*100 =5

Labours hours* Absorption rate of

OH

63*5 = 315

Machine hour

basis

Factory OH/machine hours*100

150000/25000*100 =6

Machine hours for job* OH

absorption rate

44*6 = 264

3.3 Adjustments for under or over recovered overhead costs.

8

sections of services and also to operation divisions. Examples, company assign ranks to service

departments like S1, S2 and so on according to that cost are allocated.

3.2 Calculate overhead absorption rates.

Basis of cost Absorption rate of overhead Absorption based overhead

Raw material Factory OH/ Cost of material

150000/110000*100= 136.6%

OH absorption rate*material cost of

job

136.6*240 % =327

Direct labour Factory OH/ Labour cost*100

150000/90000*100 = 166.67%

Labour cost* absorption rate of OH

200*166.7 % = 333

Prime cost Factory OH/ Prime cost

150000/200000*100 = 75%

Prime cost of job* absorption rate

240+200*75% = 330

Units of

Production

Factory OH/ Units of output*100

150000/500*100 = 30

Units of output* absorption rate

10*30 = 300

Direct labour

basis

Factory OH/ Labour rate*100

150000/30000*100 =5

Labours hours* Absorption rate of

OH

63*5 = 315

Machine hour

basis

Factory OH/machine hours*100

150000/25000*100 =6

Machine hours for job* OH

absorption rate

44*6 = 264

3.3 Adjustments for under or over recovered overhead costs.

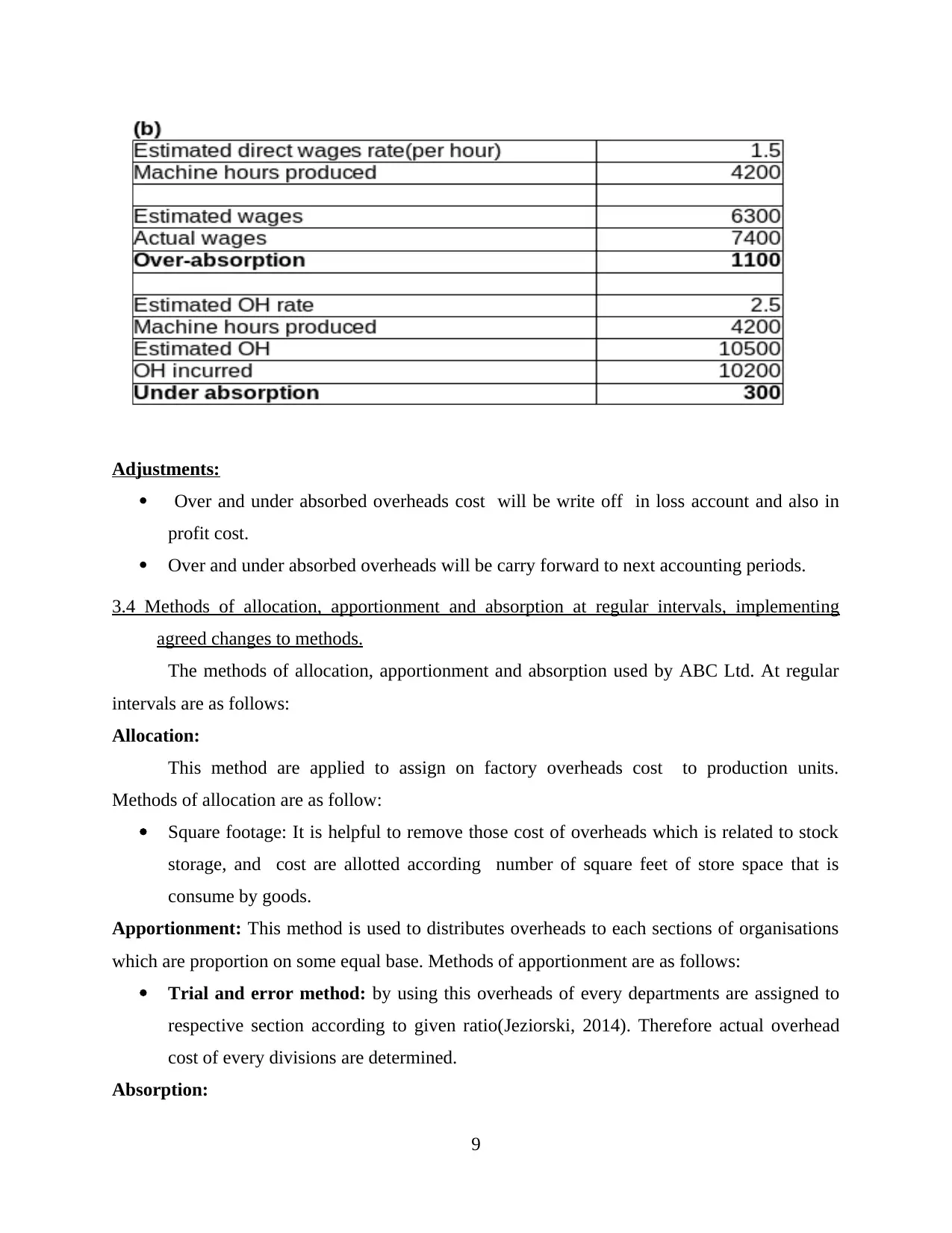

8

Adjustments:

Over and under absorbed overheads cost will be write off in loss account and also in

profit cost.

Over and under absorbed overheads will be carry forward to next accounting periods.

3.4 Methods of allocation, apportionment and absorption at regular intervals, implementing

agreed changes to methods.

The methods of allocation, apportionment and absorption used by ABC Ltd. At regular

intervals are as follows:

Allocation:

This method are applied to assign on factory overheads cost to production units.

Methods of allocation are as follow:

Square footage: It is helpful to remove those cost of overheads which is related to stock

storage, and cost are allotted according number of square feet of store space that is

consume by goods.

Apportionment: This method is used to distributes overheads to each sections of organisations

which are proportion on some equal base. Methods of apportionment are as follows:

Trial and error method: by using this overheads of every departments are assigned to

respective section according to given ratio(Jeziorski, 2014). Therefore actual overhead

cost of every divisions are determined.

Absorption:

9

Over and under absorbed overheads cost will be write off in loss account and also in

profit cost.

Over and under absorbed overheads will be carry forward to next accounting periods.

3.4 Methods of allocation, apportionment and absorption at regular intervals, implementing

agreed changes to methods.

The methods of allocation, apportionment and absorption used by ABC Ltd. At regular

intervals are as follows:

Allocation:

This method are applied to assign on factory overheads cost to production units.

Methods of allocation are as follow:

Square footage: It is helpful to remove those cost of overheads which is related to stock

storage, and cost are allotted according number of square feet of store space that is

consume by goods.

Apportionment: This method is used to distributes overheads to each sections of organisations

which are proportion on some equal base. Methods of apportionment are as follows:

Trial and error method: by using this overheads of every departments are assigned to

respective section according to given ratio(Jeziorski, 2014). Therefore actual overhead

cost of every divisions are determined.

Absorption:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.