Detailed Financial Performance Analysis: Wittgenstein Pty Ltd Budget

VerifiedAdded on 2020/05/04

|11

|2527

|84

Report

AI Summary

This report presents a comprehensive financial analysis of Wittgenstein Pty Ltd, encompassing sales, production, direct materials, direct labor, and manufacturing overhead budgets. It includes detailed calculations for each budget component, such as the sales budget, production budget, direct material purchase budget, direct labor budget, manufacturing overhead budget, and ending finished goods inventory budget. The report then delves into the cost structure analysis, evaluating relevant costs and benefits of a potential investment. Furthermore, it compares budgeted versus actual outcomes, calculating variances to assess the company's performance against its plans. Finally, the report discusses participative and imposed budgeting approaches, offering insights for the production manager. The analysis covers key financial statements like the cost of goods sold budget, budgeted income statement, and cash budget, providing a holistic view of the company's financial position and performance.

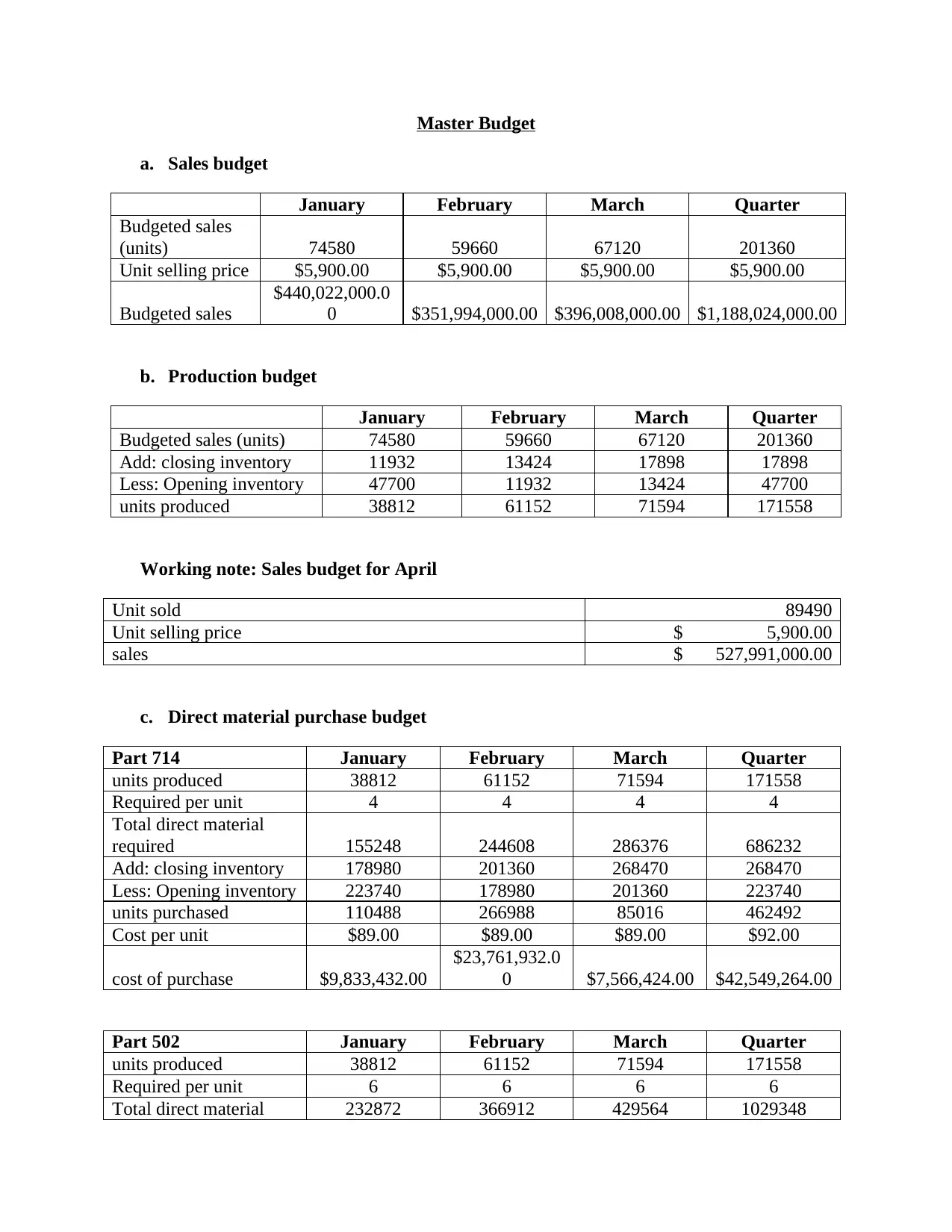

Master Budget

a. Sales budget

January February March Quarter

Budgeted sales

(units) 74580 59660 67120 201360

Unit selling price $5,900.00 $5,900.00 $5,900.00 $5,900.00

Budgeted sales

$440,022,000.0

0 $351,994,000.00 $396,008,000.00 $1,188,024,000.00

b. Production budget

January February March Quarter

Budgeted sales (units) 74580 59660 67120 201360

Add: closing inventory 11932 13424 17898 17898

Less: Opening inventory 47700 11932 13424 47700

units produced 38812 61152 71594 171558

Working note: Sales budget for April

Unit sold 89490

Unit selling price $ 5,900.00

sales $ 527,991,000.00

c. Direct material purchase budget

Part 714 January February March Quarter

units produced 38812 61152 71594 171558

Required per unit 4 4 4 4

Total direct material

required 155248 244608 286376 686232

Add: closing inventory 178980 201360 268470 268470

Less: Opening inventory 223740 178980 201360 223740

units purchased 110488 266988 85016 462492

Cost per unit $89.00 $89.00 $89.00 $92.00

cost of purchase $9,833,432.00

$23,761,932.0

0 $7,566,424.00 $42,549,264.00

Part 502 January February March Quarter

units produced 38812 61152 71594 171558

Required per unit 6 6 6 6

Total direct material 232872 366912 429564 1029348

a. Sales budget

January February March Quarter

Budgeted sales

(units) 74580 59660 67120 201360

Unit selling price $5,900.00 $5,900.00 $5,900.00 $5,900.00

Budgeted sales

$440,022,000.0

0 $351,994,000.00 $396,008,000.00 $1,188,024,000.00

b. Production budget

January February March Quarter

Budgeted sales (units) 74580 59660 67120 201360

Add: closing inventory 11932 13424 17898 17898

Less: Opening inventory 47700 11932 13424 47700

units produced 38812 61152 71594 171558

Working note: Sales budget for April

Unit sold 89490

Unit selling price $ 5,900.00

sales $ 527,991,000.00

c. Direct material purchase budget

Part 714 January February March Quarter

units produced 38812 61152 71594 171558

Required per unit 4 4 4 4

Total direct material

required 155248 244608 286376 686232

Add: closing inventory 178980 201360 268470 268470

Less: Opening inventory 223740 178980 201360 223740

units purchased 110488 266988 85016 462492

Cost per unit $89.00 $89.00 $89.00 $92.00

cost of purchase $9,833,432.00

$23,761,932.0

0 $7,566,424.00 $42,549,264.00

Part 502 January February March Quarter

units produced 38812 61152 71594 171558

Required per unit 6 6 6 6

Total direct material 232872 366912 429564 1029348

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

required

Add: closing inventory 214776 241632 268470 268470

Less: Opening inventory 268488 214776 241632 268488

units purchased 179160 393768 187932 760860

Cost per unit $119.00 $119.00 $119.00 $ 122.00

cost of purchase $21,320,040.00

$46,858,392.0

0 $22,363,908.00 $92,824,920.00

d. Direct labor Budget

January February March Quarter

Units produced 38812 61152 71594 171558

Budgeted hour per unit 9 9 9 9

Time required (hours) 349,308.00 550,368.00 644,346.00 1,544,022.00

Labor cost per hour $50.00 $50.00 $50.00 $50.00

Labor cost $17,465,400.00

$27,518,400.0

0 $32,217,300.00 $77,201,100.00

e. Manufacturing Overhead Budget

January February March Quarter

Fixed cost

Maintenance cost $11,309,475.12 $11,309,475.12 $11,309,475.12 $33,928,425.36

Supervision $41,762,000.00 $41,762,000.00 $41,762,000.00 $125,286,000.00

Depreciation $3,728,800.00 $3,728,800.00 $3,728,800.00 $11,186,400.00

Rates and utility $3,081,400.00 $3,081,400.00 $3,081,400.00 $9,244,200.00

Other $14,915,000.00 $14,915,000.00 $14,915,000.00 $44,745,000.00

Total fixed OH $74,796,675.12 $74,796,675.12 $74,796,675.12 $224,390,025.36

Variable cost

Indirect cost $62.64 $62.64 $62.64 $64.18

Power cost $5.97 $ 5.97 $ 5.97 $6.11

Maintenance cost $37.77 $37.77 $37.77 $ 37.77

Total variable OH

per hour $106.38 $106.38 $106.38 $108.06

Direct labor hours 349,308.00 550,368.00 644,346.00 1,544,022.00

Total variable OH $37,160,627.46 $58,550,105.39 $68,547,819.29 $166,852,509.09

Total

manufacturing OH $111,957,302.58 $133,346,780.51

$143,344,494.4

1 $391,242,534.46

Working note: Calculation regarding manufacturing overheads

Labor Hours Total maintenance cost

Add: closing inventory 214776 241632 268470 268470

Less: Opening inventory 268488 214776 241632 268488

units purchased 179160 393768 187932 760860

Cost per unit $119.00 $119.00 $119.00 $ 122.00

cost of purchase $21,320,040.00

$46,858,392.0

0 $22,363,908.00 $92,824,920.00

d. Direct labor Budget

January February March Quarter

Units produced 38812 61152 71594 171558

Budgeted hour per unit 9 9 9 9

Time required (hours) 349,308.00 550,368.00 644,346.00 1,544,022.00

Labor cost per hour $50.00 $50.00 $50.00 $50.00

Labor cost $17,465,400.00

$27,518,400.0

0 $32,217,300.00 $77,201,100.00

e. Manufacturing Overhead Budget

January February March Quarter

Fixed cost

Maintenance cost $11,309,475.12 $11,309,475.12 $11,309,475.12 $33,928,425.36

Supervision $41,762,000.00 $41,762,000.00 $41,762,000.00 $125,286,000.00

Depreciation $3,728,800.00 $3,728,800.00 $3,728,800.00 $11,186,400.00

Rates and utility $3,081,400.00 $3,081,400.00 $3,081,400.00 $9,244,200.00

Other $14,915,000.00 $14,915,000.00 $14,915,000.00 $44,745,000.00

Total fixed OH $74,796,675.12 $74,796,675.12 $74,796,675.12 $224,390,025.36

Variable cost

Indirect cost $62.64 $62.64 $62.64 $64.18

Power cost $5.97 $ 5.97 $ 5.97 $6.11

Maintenance cost $37.77 $37.77 $37.77 $ 37.77

Total variable OH

per hour $106.38 $106.38 $106.38 $108.06

Direct labor hours 349,308.00 550,368.00 644,346.00 1,544,022.00

Total variable OH $37,160,627.46 $58,550,105.39 $68,547,819.29 $166,852,509.09

Total

manufacturing OH $111,957,302.58 $133,346,780.51

$143,344,494.4

1 $391,242,534.46

Working note: Calculation regarding manufacturing overheads

Labor Hours Total maintenance cost

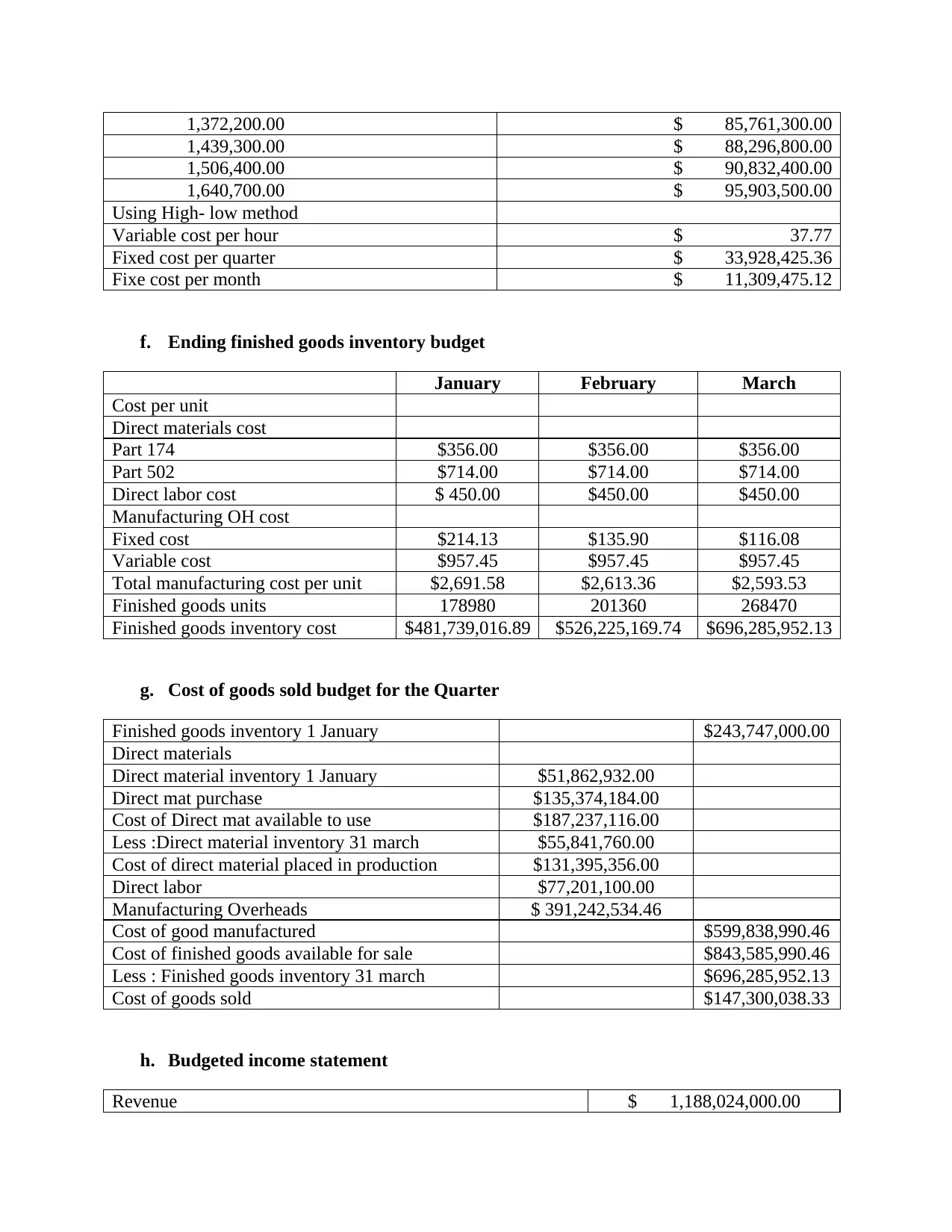

1,372,200.00 $ 85,761,300.00

1,439,300.00 $ 88,296,800.00

1,506,400.00 $ 90,832,400.00

1,640,700.00 $ 95,903,500.00

Using High- low method

Variable cost per hour $ 37.77

Fixed cost per quarter $ 33,928,425.36

Fixe cost per month $ 11,309,475.12

f. Ending finished goods inventory budget

January February March

Cost per unit

Direct materials cost

Part 174 $356.00 $356.00 $356.00

Part 502 $714.00 $714.00 $714.00

Direct labor cost $ 450.00 $450.00 $450.00

Manufacturing OH cost

Fixed cost $214.13 $135.90 $116.08

Variable cost $957.45 $957.45 $957.45

Total manufacturing cost per unit $2,691.58 $2,613.36 $2,593.53

Finished goods units 178980 201360 268470

Finished goods inventory cost $481,739,016.89 $526,225,169.74 $696,285,952.13

g. Cost of goods sold budget for the Quarter

Finished goods inventory 1 January $243,747,000.00

Direct materials

Direct material inventory 1 January $51,862,932.00

Direct mat purchase $135,374,184.00

Cost of Direct mat available to use $187,237,116.00

Less :Direct material inventory 31 march $55,841,760.00

Cost of direct material placed in production $131,395,356.00

Direct labor $77,201,100.00

Manufacturing Overheads $ 391,242,534.46

Cost of good manufactured $599,838,990.46

Cost of finished goods available for sale $843,585,990.46

Less : Finished goods inventory 31 march $696,285,952.13

Cost of goods sold $147,300,038.33

h. Budgeted income statement

Revenue $ 1,188,024,000.00

1,439,300.00 $ 88,296,800.00

1,506,400.00 $ 90,832,400.00

1,640,700.00 $ 95,903,500.00

Using High- low method

Variable cost per hour $ 37.77

Fixed cost per quarter $ 33,928,425.36

Fixe cost per month $ 11,309,475.12

f. Ending finished goods inventory budget

January February March

Cost per unit

Direct materials cost

Part 174 $356.00 $356.00 $356.00

Part 502 $714.00 $714.00 $714.00

Direct labor cost $ 450.00 $450.00 $450.00

Manufacturing OH cost

Fixed cost $214.13 $135.90 $116.08

Variable cost $957.45 $957.45 $957.45

Total manufacturing cost per unit $2,691.58 $2,613.36 $2,593.53

Finished goods units 178980 201360 268470

Finished goods inventory cost $481,739,016.89 $526,225,169.74 $696,285,952.13

g. Cost of goods sold budget for the Quarter

Finished goods inventory 1 January $243,747,000.00

Direct materials

Direct material inventory 1 January $51,862,932.00

Direct mat purchase $135,374,184.00

Cost of Direct mat available to use $187,237,116.00

Less :Direct material inventory 31 march $55,841,760.00

Cost of direct material placed in production $131,395,356.00

Direct labor $77,201,100.00

Manufacturing Overheads $ 391,242,534.46

Cost of good manufactured $599,838,990.46

Cost of finished goods available for sale $843,585,990.46

Less : Finished goods inventory 31 march $696,285,952.13

Cost of goods sold $147,300,038.33

h. Budgeted income statement

Revenue $ 1,188,024,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

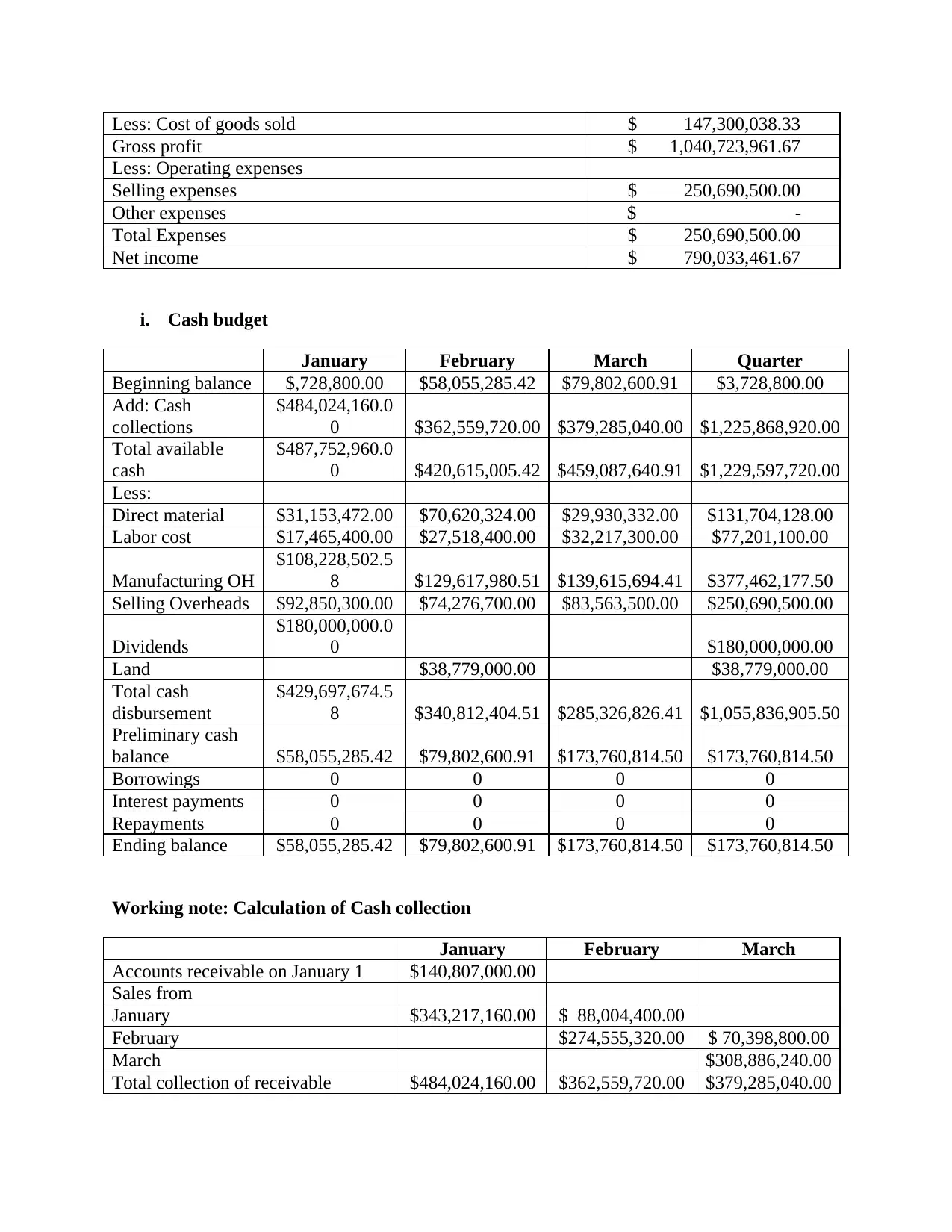

Less: Cost of goods sold $ 147,300,038.33

Gross profit $ 1,040,723,961.67

Less: Operating expenses

Selling expenses $ 250,690,500.00

Other expenses $ -

Total Expenses $ 250,690,500.00

Net income $ 790,033,461.67

i. Cash budget

January February March Quarter

Beginning balance $,728,800.00 $58,055,285.42 $79,802,600.91 $3,728,800.00

Add: Cash

collections

$484,024,160.0

0 $362,559,720.00 $379,285,040.00 $1,225,868,920.00

Total available

cash

$487,752,960.0

0 $420,615,005.42 $459,087,640.91 $1,229,597,720.00

Less:

Direct material $31,153,472.00 $70,620,324.00 $29,930,332.00 $131,704,128.00

Labor cost $17,465,400.00 $27,518,400.00 $32,217,300.00 $77,201,100.00

Manufacturing OH

$108,228,502.5

8 $129,617,980.51 $139,615,694.41 $377,462,177.50

Selling Overheads $92,850,300.00 $74,276,700.00 $83,563,500.00 $250,690,500.00

Dividends

$180,000,000.0

0 $180,000,000.00

Land $38,779,000.00 $38,779,000.00

Total cash

disbursement

$429,697,674.5

8 $340,812,404.51 $285,326,826.41 $1,055,836,905.50

Preliminary cash

balance $58,055,285.42 $79,802,600.91 $173,760,814.50 $173,760,814.50

Borrowings 0 0 0 0

Interest payments 0 0 0 0

Repayments 0 0 0 0

Ending balance $58,055,285.42 $79,802,600.91 $173,760,814.50 $173,760,814.50

Working note: Calculation of Cash collection

January February March

Accounts receivable on January 1 $140,807,000.00

Sales from

January $343,217,160.00 $ 88,004,400.00

February $274,555,320.00 $ 70,398,800.00

March $308,886,240.00

Total collection of receivable $484,024,160.00 $362,559,720.00 $379,285,040.00

Gross profit $ 1,040,723,961.67

Less: Operating expenses

Selling expenses $ 250,690,500.00

Other expenses $ -

Total Expenses $ 250,690,500.00

Net income $ 790,033,461.67

i. Cash budget

January February March Quarter

Beginning balance $,728,800.00 $58,055,285.42 $79,802,600.91 $3,728,800.00

Add: Cash

collections

$484,024,160.0

0 $362,559,720.00 $379,285,040.00 $1,225,868,920.00

Total available

cash

$487,752,960.0

0 $420,615,005.42 $459,087,640.91 $1,229,597,720.00

Less:

Direct material $31,153,472.00 $70,620,324.00 $29,930,332.00 $131,704,128.00

Labor cost $17,465,400.00 $27,518,400.00 $32,217,300.00 $77,201,100.00

Manufacturing OH

$108,228,502.5

8 $129,617,980.51 $139,615,694.41 $377,462,177.50

Selling Overheads $92,850,300.00 $74,276,700.00 $83,563,500.00 $250,690,500.00

Dividends

$180,000,000.0

0 $180,000,000.00

Land $38,779,000.00 $38,779,000.00

Total cash

disbursement

$429,697,674.5

8 $340,812,404.51 $285,326,826.41 $1,055,836,905.50

Preliminary cash

balance $58,055,285.42 $79,802,600.91 $173,760,814.50 $173,760,814.50

Borrowings 0 0 0 0

Interest payments 0 0 0 0

Repayments 0 0 0 0

Ending balance $58,055,285.42 $79,802,600.91 $173,760,814.50 $173,760,814.50

Working note: Calculation of Cash collection

January February March

Accounts receivable on January 1 $140,807,000.00

Sales from

January $343,217,160.00 $ 88,004,400.00

February $274,555,320.00 $ 70,398,800.00

March $308,886,240.00

Total collection of receivable $484,024,160.00 $362,559,720.00 $379,285,040.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

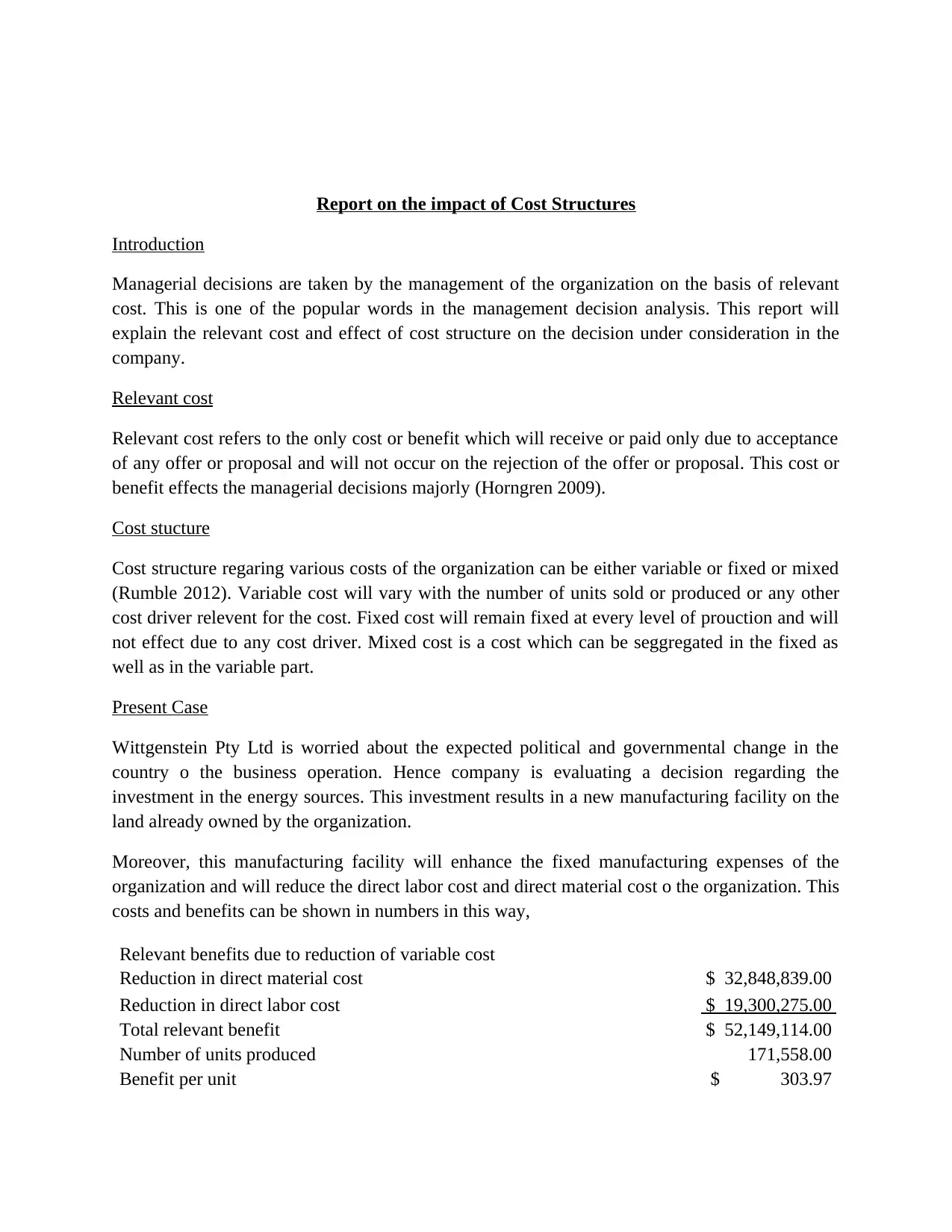

Report on the impact of Cost Structures

Introduction

Managerial decisions are taken by the management of the organization on the basis of relevant

cost. This is one of the popular words in the management decision analysis. This report will

explain the relevant cost and effect of cost structure on the decision under consideration in the

company.

Relevant cost

Relevant cost refers to the only cost or benefit which will receive or paid only due to acceptance

of any offer or proposal and will not occur on the rejection of the offer or proposal. This cost or

benefit effects the managerial decisions majorly (Horngren 2009).

Cost stucture

Cost structure regaring various costs of the organization can be either variable or fixed or mixed

(Rumble 2012). Variable cost will vary with the number of units sold or produced or any other

cost driver relevent for the cost. Fixed cost will remain fixed at every level of prouction and will

not effect due to any cost driver. Mixed cost is a cost which can be seggregated in the fixed as

well as in the variable part.

Present Case

Wittgenstein Pty Ltd is worried about the expected political and governmental change in the

country o the business operation. Hence company is evaluating a decision regarding the

investment in the energy sources. This investment results in a new manufacturing facility on the

land already owned by the organization.

Moreover, this manufacturing facility will enhance the fixed manufacturing expenses of the

organization and will reduce the direct labor cost and direct material cost o the organization. This

costs and benefits can be shown in numbers in this way,

Relevant benefits due to reduction of variable cost

Reduction in direct material cost $ 32,848,839.00

Reduction in direct labor cost $ 19,300,275.00

Total relevant benefit $ 52,149,114.00

Number of units produced 171,558.00

Benefit per unit $ 303.97

Introduction

Managerial decisions are taken by the management of the organization on the basis of relevant

cost. This is one of the popular words in the management decision analysis. This report will

explain the relevant cost and effect of cost structure on the decision under consideration in the

company.

Relevant cost

Relevant cost refers to the only cost or benefit which will receive or paid only due to acceptance

of any offer or proposal and will not occur on the rejection of the offer or proposal. This cost or

benefit effects the managerial decisions majorly (Horngren 2009).

Cost stucture

Cost structure regaring various costs of the organization can be either variable or fixed or mixed

(Rumble 2012). Variable cost will vary with the number of units sold or produced or any other

cost driver relevent for the cost. Fixed cost will remain fixed at every level of prouction and will

not effect due to any cost driver. Mixed cost is a cost which can be seggregated in the fixed as

well as in the variable part.

Present Case

Wittgenstein Pty Ltd is worried about the expected political and governmental change in the

country o the business operation. Hence company is evaluating a decision regarding the

investment in the energy sources. This investment results in a new manufacturing facility on the

land already owned by the organization.

Moreover, this manufacturing facility will enhance the fixed manufacturing expenses of the

organization and will reduce the direct labor cost and direct material cost o the organization. This

costs and benefits can be shown in numbers in this way,

Relevant benefits due to reduction of variable cost

Reduction in direct material cost $ 32,848,839.00

Reduction in direct labor cost $ 19,300,275.00

Total relevant benefit $ 52,149,114.00

Number of units produced 171,558.00

Benefit per unit $ 303.97

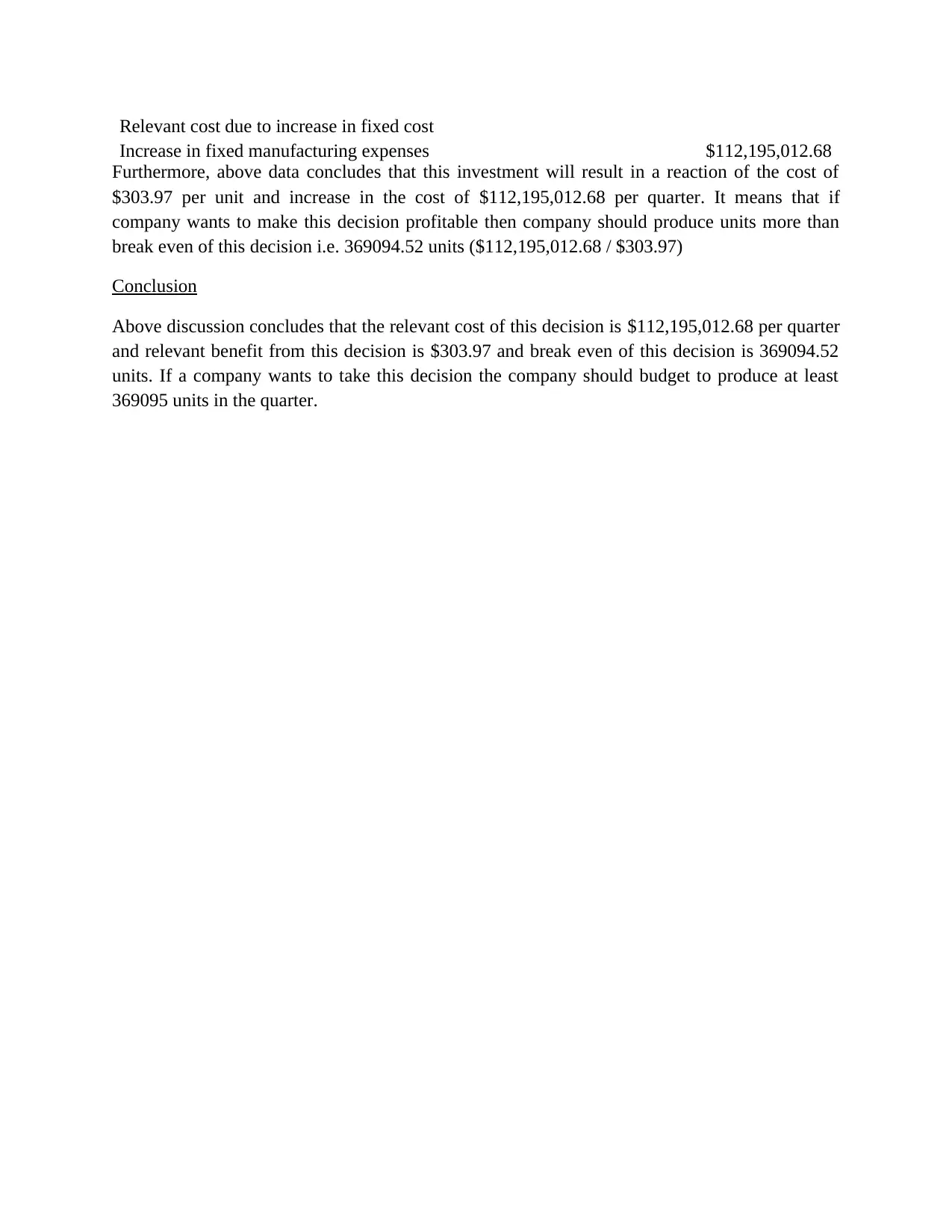

Relevant cost due to increase in fixed cost

Increase in fixed manufacturing expenses $112,195,012.68

Furthermore, above data concludes that this investment will result in a reaction of the cost of

$303.97 per unit and increase in the cost of $112,195,012.68 per quarter. It means that if

company wants to make this decision profitable then company should produce units more than

break even of this decision i.e. 369094.52 units ($112,195,012.68 / $303.97)

Conclusion

Above discussion concludes that the relevant cost of this decision is $112,195,012.68 per quarter

and relevant benefit from this decision is $303.97 and break even of this decision is 369094.52

units. If a company wants to take this decision the company should budget to produce at least

369095 units in the quarter.

Increase in fixed manufacturing expenses $112,195,012.68

Furthermore, above data concludes that this investment will result in a reaction of the cost of

$303.97 per unit and increase in the cost of $112,195,012.68 per quarter. It means that if

company wants to make this decision profitable then company should produce units more than

break even of this decision i.e. 369094.52 units ($112,195,012.68 / $303.97)

Conclusion

Above discussion concludes that the relevant cost of this decision is $112,195,012.68 per quarter

and relevant benefit from this decision is $303.97 and break even of this decision is 369094.52

units. If a company wants to take this decision the company should budget to produce at least

369095 units in the quarter.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

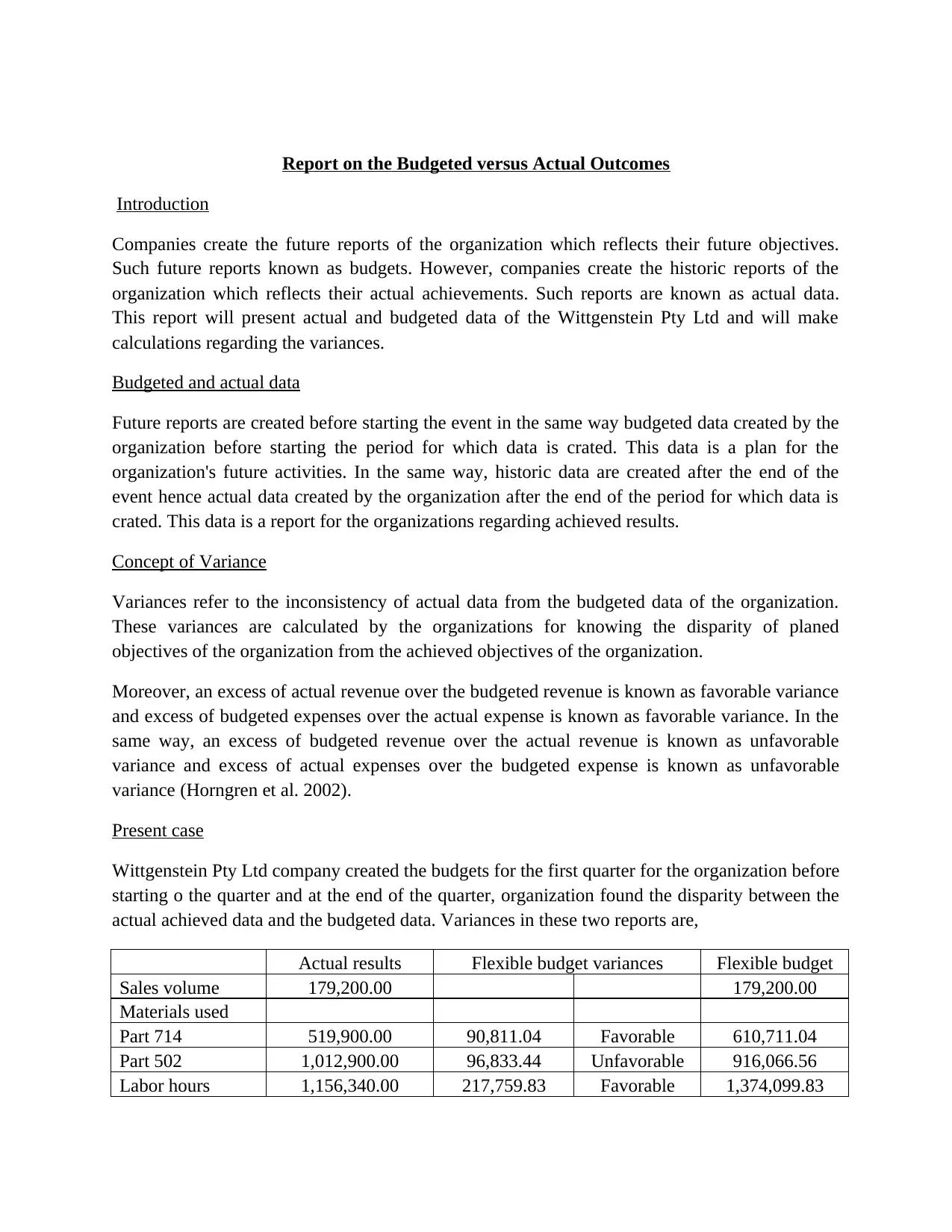

Report on the Budgeted versus Actual Outcomes

Introduction

Companies create the future reports of the organization which reflects their future objectives.

Such future reports known as budgets. However, companies create the historic reports of the

organization which reflects their actual achievements. Such reports are known as actual data.

This report will present actual and budgeted data of the Wittgenstein Pty Ltd and will make

calculations regarding the variances.

Budgeted and actual data

Future reports are created before starting the event in the same way budgeted data created by the

organization before starting the period for which data is crated. This data is a plan for the

organization's future activities. In the same way, historic data are created after the end of the

event hence actual data created by the organization after the end of the period for which data is

crated. This data is a report for the organizations regarding achieved results.

Concept of Variance

Variances refer to the inconsistency of actual data from the budgeted data of the organization.

These variances are calculated by the organizations for knowing the disparity of planed

objectives of the organization from the achieved objectives of the organization.

Moreover, an excess of actual revenue over the budgeted revenue is known as favorable variance

and excess of budgeted expenses over the actual expense is known as favorable variance. In the

same way, an excess of budgeted revenue over the actual revenue is known as unfavorable

variance and excess of actual expenses over the budgeted expense is known as unfavorable

variance (Horngren et al. 2002).

Present case

Wittgenstein Pty Ltd company created the budgets for the first quarter for the organization before

starting o the quarter and at the end of the quarter, organization found the disparity between the

actual achieved data and the budgeted data. Variances in these two reports are,

Actual results Flexible budget variances Flexible budget

Sales volume 179,200.00 179,200.00

Materials used

Part 714 519,900.00 90,811.04 Favorable 610,711.04

Part 502 1,012,900.00 96,833.44 Unfavorable 916,066.56

Labor hours 1,156,340.00 217,759.83 Favorable 1,374,099.83

Introduction

Companies create the future reports of the organization which reflects their future objectives.

Such future reports known as budgets. However, companies create the historic reports of the

organization which reflects their actual achievements. Such reports are known as actual data.

This report will present actual and budgeted data of the Wittgenstein Pty Ltd and will make

calculations regarding the variances.

Budgeted and actual data

Future reports are created before starting the event in the same way budgeted data created by the

organization before starting the period for which data is crated. This data is a plan for the

organization's future activities. In the same way, historic data are created after the end of the

event hence actual data created by the organization after the end of the period for which data is

crated. This data is a report for the organizations regarding achieved results.

Concept of Variance

Variances refer to the inconsistency of actual data from the budgeted data of the organization.

These variances are calculated by the organizations for knowing the disparity of planed

objectives of the organization from the achieved objectives of the organization.

Moreover, an excess of actual revenue over the budgeted revenue is known as favorable variance

and excess of budgeted expenses over the actual expense is known as favorable variance. In the

same way, an excess of budgeted revenue over the actual revenue is known as unfavorable

variance and excess of actual expenses over the budgeted expense is known as unfavorable

variance (Horngren et al. 2002).

Present case

Wittgenstein Pty Ltd company created the budgets for the first quarter for the organization before

starting o the quarter and at the end of the quarter, organization found the disparity between the

actual achieved data and the budgeted data. Variances in these two reports are,

Actual results Flexible budget variances Flexible budget

Sales volume 179,200.00 179,200.00

Materials used

Part 714 519,900.00 90,811.04 Favorable 610,711.04

Part 502 1,012,900.00 96,833.44 Unfavorable 916,066.56

Labor hours 1,156,340.00 217,759.83 Favorable 1,374,099.83

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

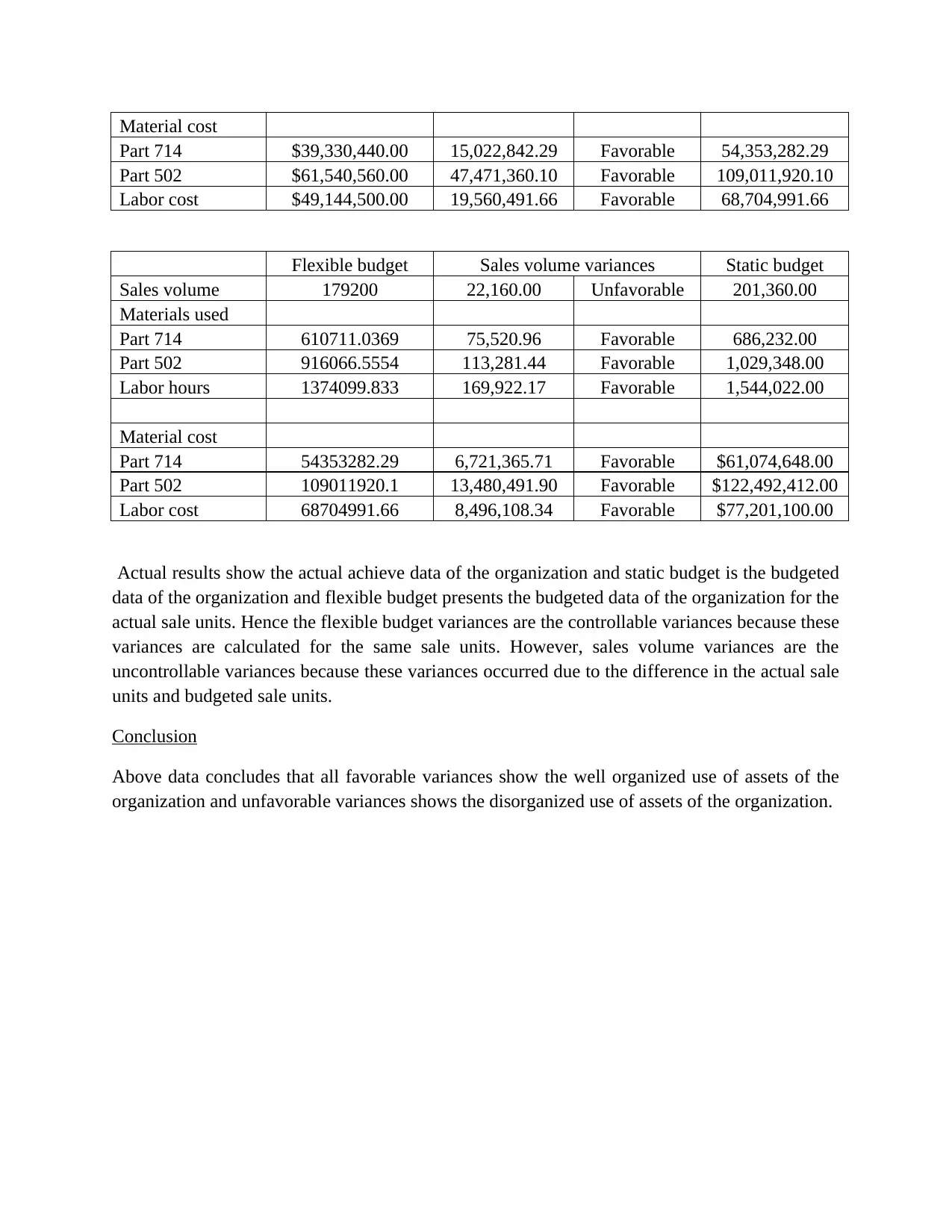

Material cost

Part 714 $39,330,440.00 15,022,842.29 Favorable 54,353,282.29

Part 502 $61,540,560.00 47,471,360.10 Favorable 109,011,920.10

Labor cost $49,144,500.00 19,560,491.66 Favorable 68,704,991.66

Flexible budget Sales volume variances Static budget

Sales volume 179200 22,160.00 Unfavorable 201,360.00

Materials used

Part 714 610711.0369 75,520.96 Favorable 686,232.00

Part 502 916066.5554 113,281.44 Favorable 1,029,348.00

Labor hours 1374099.833 169,922.17 Favorable 1,544,022.00

Material cost

Part 714 54353282.29 6,721,365.71 Favorable $61,074,648.00

Part 502 109011920.1 13,480,491.90 Favorable $122,492,412.00

Labor cost 68704991.66 8,496,108.34 Favorable $77,201,100.00

Actual results show the actual achieve data of the organization and static budget is the budgeted

data of the organization and flexible budget presents the budgeted data of the organization for the

actual sale units. Hence the flexible budget variances are the controllable variances because these

variances are calculated for the same sale units. However, sales volume variances are the

uncontrollable variances because these variances occurred due to the difference in the actual sale

units and budgeted sale units.

Conclusion

Above data concludes that all favorable variances show the well organized use of assets of the

organization and unfavorable variances shows the disorganized use of assets of the organization.

Part 714 $39,330,440.00 15,022,842.29 Favorable 54,353,282.29

Part 502 $61,540,560.00 47,471,360.10 Favorable 109,011,920.10

Labor cost $49,144,500.00 19,560,491.66 Favorable 68,704,991.66

Flexible budget Sales volume variances Static budget

Sales volume 179200 22,160.00 Unfavorable 201,360.00

Materials used

Part 714 610711.0369 75,520.96 Favorable 686,232.00

Part 502 916066.5554 113,281.44 Favorable 1,029,348.00

Labor hours 1374099.833 169,922.17 Favorable 1,544,022.00

Material cost

Part 714 54353282.29 6,721,365.71 Favorable $61,074,648.00

Part 502 109011920.1 13,480,491.90 Favorable $122,492,412.00

Labor cost 68704991.66 8,496,108.34 Favorable $77,201,100.00

Actual results show the actual achieve data of the organization and static budget is the budgeted

data of the organization and flexible budget presents the budgeted data of the organization for the

actual sale units. Hence the flexible budget variances are the controllable variances because these

variances are calculated for the same sale units. However, sales volume variances are the

uncontrollable variances because these variances occurred due to the difference in the actual sale

units and budgeted sale units.

Conclusion

Above data concludes that all favorable variances show the well organized use of assets of the

organization and unfavorable variances shows the disorganized use of assets of the organization.

Discussion on Participative and imposed Budgeting

Introduction

Participatory approach and the imposed approach are two approaches which can be used by the

organization for budget formation process. The imposed budgetary approach means the

approach in which budgets are prepared by the top management of the organization and followed

by the all levels of the management. The participatory budgetary approach means the approach

in which budgets are prepared by the all management level of the organization and followed by

the all levels of the management. This report will explain regarding this two budgeting approach

and will explain to the production manager of the Wittgenstein Pty Ltd regarding the responses

after using these two approaches.

Participatory budgetary approach

Under this approach, budgets are applied and created by the same people because participatory

budgetary approach means the approach in which budgets are prepared by the all management

level of the organization and followed by all levels of the management (Shah 2007). This budget

includes the person going to affect directly from the budget in the budget creation process. Such

thing will enhance the motivation of employees because they feel emotionally attached to the

organization. Such enhancement of motivation creates a feeling that goals specified in the

budgets are their personal goals and they must give their 100% potential to achieve those goals.

The participatory budgetary approach is known as the bottom up approach of budget creation.

However, this approach makes budget creation process as costly and time taking process due to

the administration of all management level.

Moreover, if this budget will create by using participatory budgeting approach then production

manager of the organization should consider the fact that company’s budget was not achieved by

the organization in terms of budgeted sales volume. The Higher motivation of all employees of

the organization becomes unable to achieve objectives.

Imposed budgetary approach

Under this approach, budgets are applied and created by the different people imposed budgetary

approach means the approach in which budgets are prepared by the top management of the

organization and followed by the all levels of the management (Hansen, Mowen & Guan 2007).

This budget does not include the person going to affect directly from the budget in the budget

creation process. Such thing will reduce the motivation of employees because they feel less

irrelevant for the organization. The imposed budgetary approach is known as the top down

approach of budget creation. This approach makes budget creation process as economic and less

time taking process due to less requirement of the administration for top management. The

Introduction

Participatory approach and the imposed approach are two approaches which can be used by the

organization for budget formation process. The imposed budgetary approach means the

approach in which budgets are prepared by the top management of the organization and followed

by the all levels of the management. The participatory budgetary approach means the approach

in which budgets are prepared by the all management level of the organization and followed by

the all levels of the management. This report will explain regarding this two budgeting approach

and will explain to the production manager of the Wittgenstein Pty Ltd regarding the responses

after using these two approaches.

Participatory budgetary approach

Under this approach, budgets are applied and created by the same people because participatory

budgetary approach means the approach in which budgets are prepared by the all management

level of the organization and followed by all levels of the management (Shah 2007). This budget

includes the person going to affect directly from the budget in the budget creation process. Such

thing will enhance the motivation of employees because they feel emotionally attached to the

organization. Such enhancement of motivation creates a feeling that goals specified in the

budgets are their personal goals and they must give their 100% potential to achieve those goals.

The participatory budgetary approach is known as the bottom up approach of budget creation.

However, this approach makes budget creation process as costly and time taking process due to

the administration of all management level.

Moreover, if this budget will create by using participatory budgeting approach then production

manager of the organization should consider the fact that company’s budget was not achieved by

the organization in terms of budgeted sales volume. The Higher motivation of all employees of

the organization becomes unable to achieve objectives.

Imposed budgetary approach

Under this approach, budgets are applied and created by the different people imposed budgetary

approach means the approach in which budgets are prepared by the top management of the

organization and followed by the all levels of the management (Hansen, Mowen & Guan 2007).

This budget does not include the person going to affect directly from the budget in the budget

creation process. Such thing will reduce the motivation of employees because they feel less

irrelevant for the organization. The imposed budgetary approach is known as the top down

approach of budget creation. This approach makes budget creation process as economic and less

time taking process due to less requirement of the administration for top management. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

imposed budgetary approach worked as the device of communication between the top

management and the other level of the management of the organization.

Moreover, if this budget will create by using imposed budgeting approach then production

manager of the organization should consider the fact that company’s budget was not achieved by

the organization in terms of budgeted sales volume. Hence top management of the organization

was expected higher sales volume with the lower resources.

management and the other level of the management of the organization.

Moreover, if this budget will create by using imposed budgeting approach then production

manager of the organization should consider the fact that company’s budget was not achieved by

the organization in terms of budgeted sales volume. Hence top management of the organization

was expected higher sales volume with the lower resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bibliography

Hansen, D, Mowen, M & Guan, L 2007, Cost Management: Accounting and Control, Cengage

Learning.

Horngren, CT 2009, Cost Accounting: A Managerial Emphasis, Pearson Education India.

Horngren, CT, Bhimani, A, Datar, SM & Foster, G 2002, Management and cost accounting,

Pearson Educati, New York.

Rumble, G 2012, The costs and economics of open and distance learning, Routledge.

Shah, A 2007, Participatory Budgeting, World Bank Publications.

Hansen, D, Mowen, M & Guan, L 2007, Cost Management: Accounting and Control, Cengage

Learning.

Horngren, CT 2009, Cost Accounting: A Managerial Emphasis, Pearson Education India.

Horngren, CT, Bhimani, A, Datar, SM & Foster, G 2002, Management and cost accounting,

Pearson Educati, New York.

Rumble, G 2012, The costs and economics of open and distance learning, Routledge.

Shah, A 2007, Participatory Budgeting, World Bank Publications.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.