ACCY801 - Cost-Volume-Profit Analysis & Capital Investment

VerifiedAdded on 2023/06/18

|9

|1423

|498

Report

AI Summary

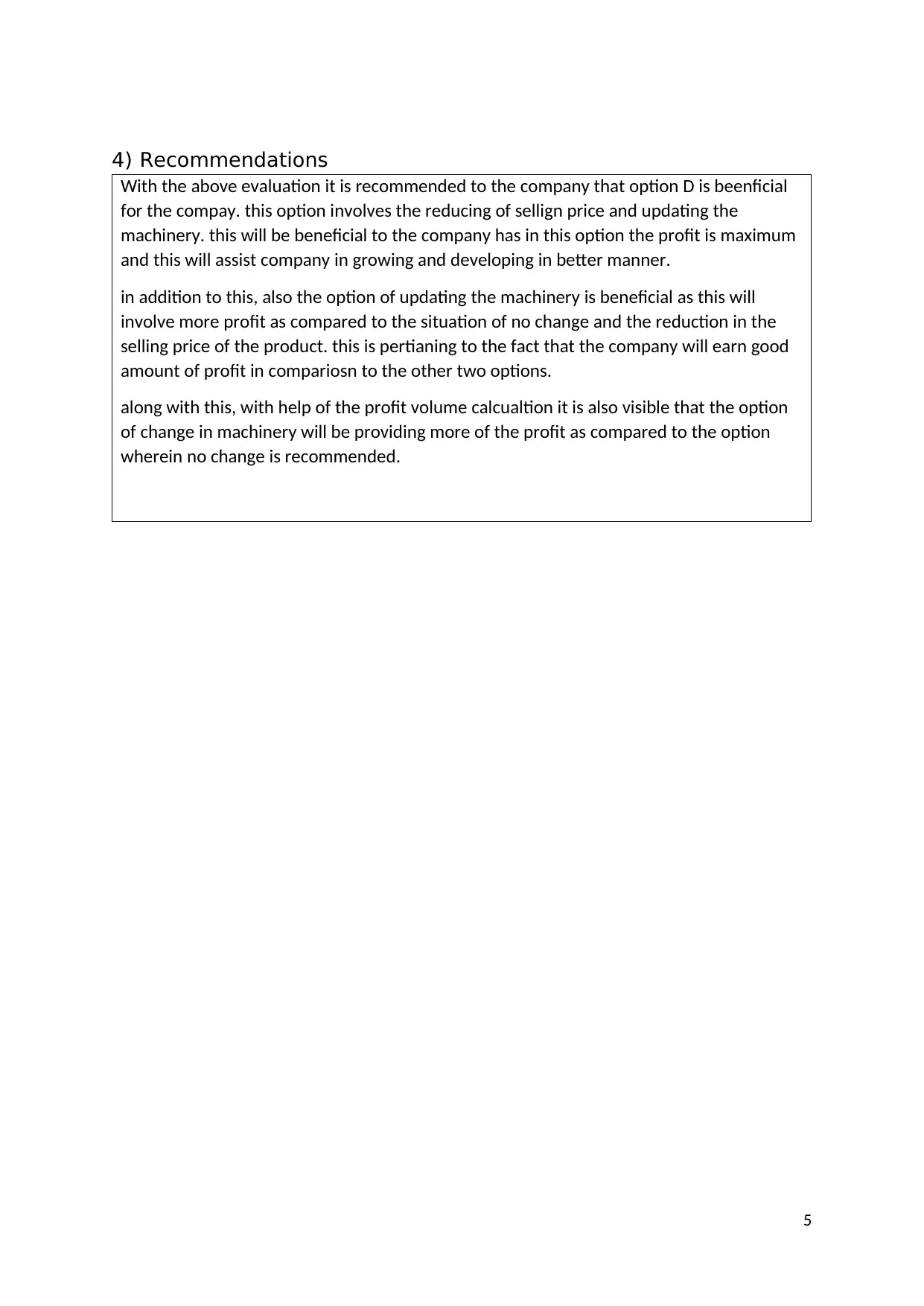

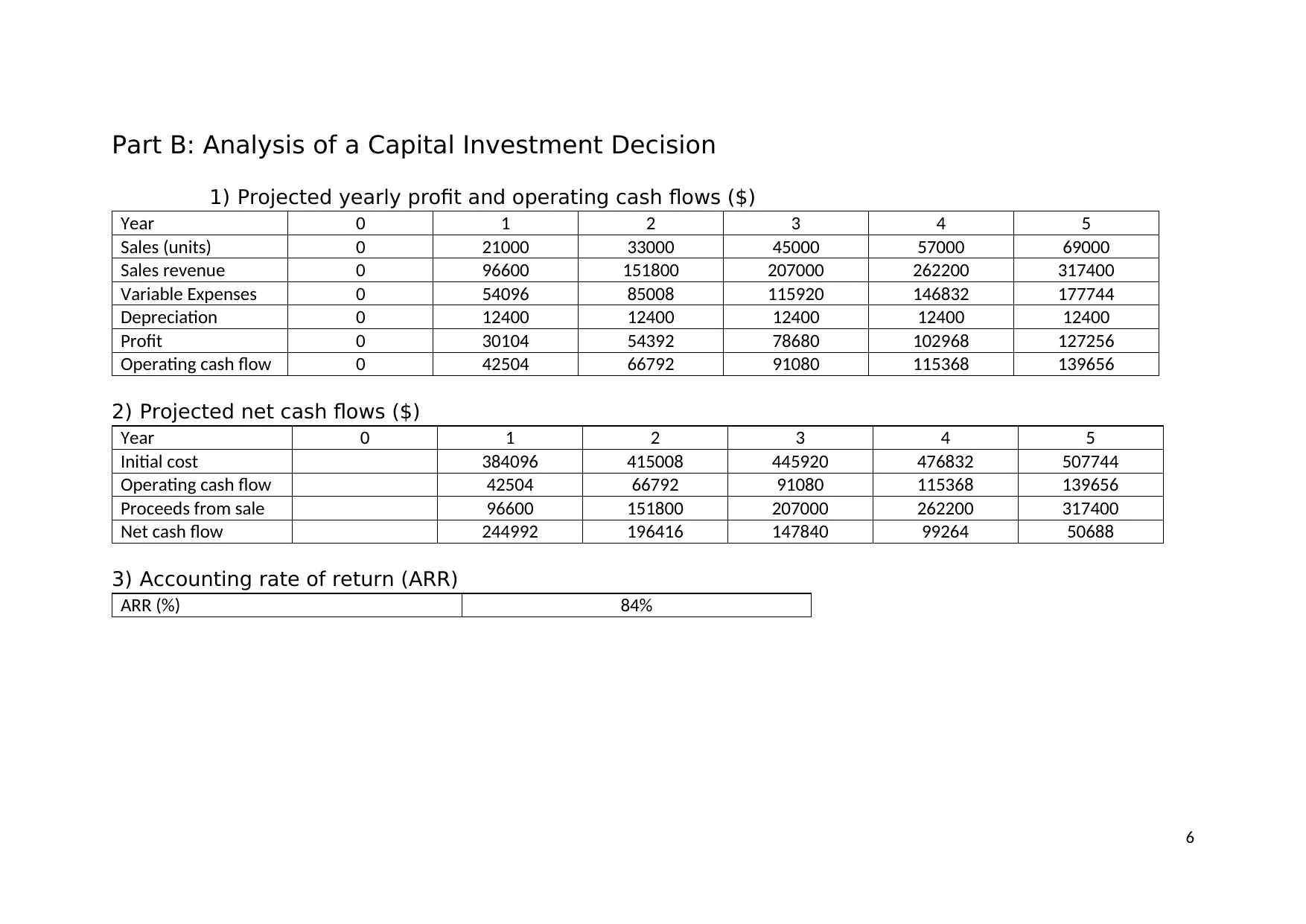

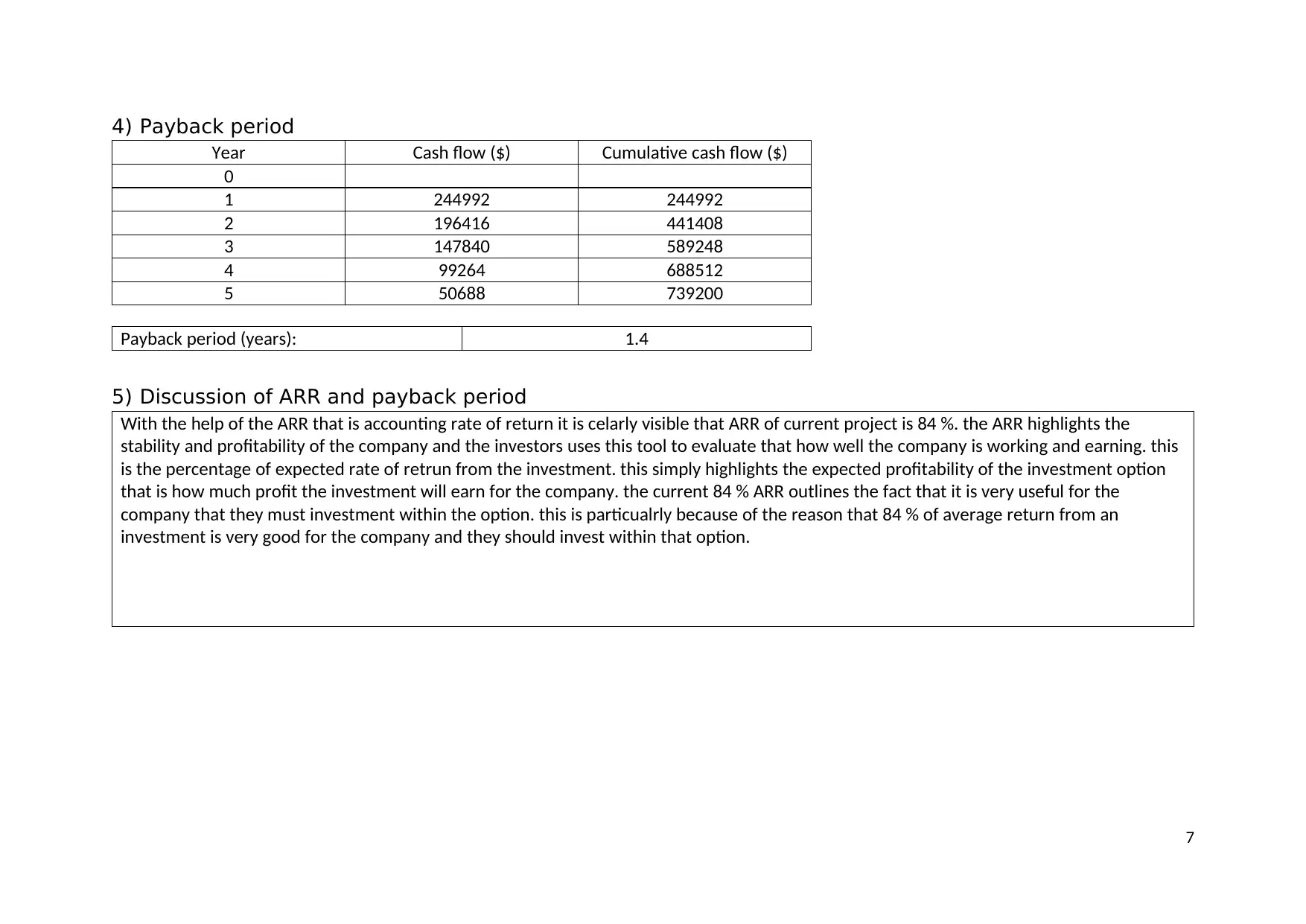

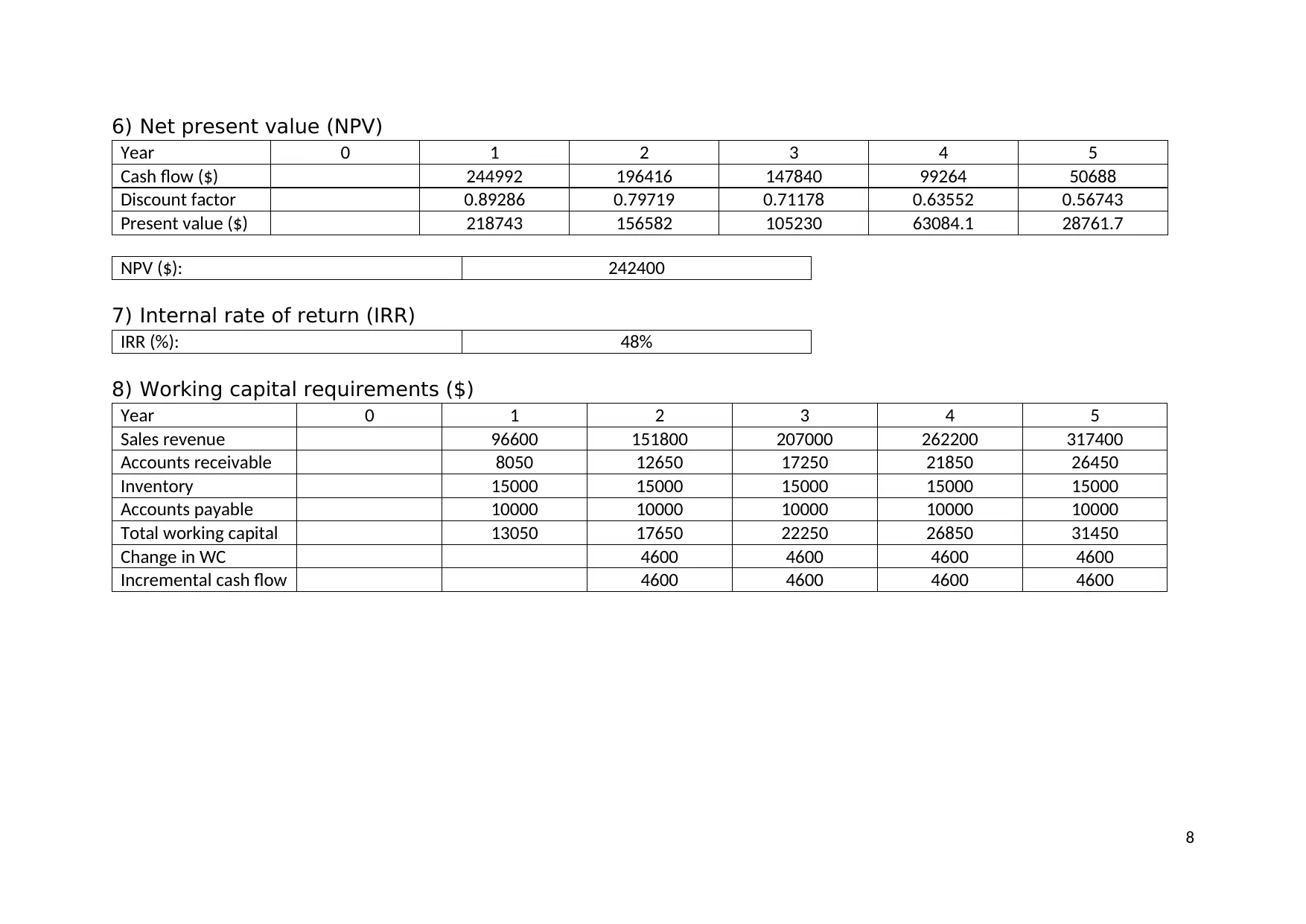

This report provides a comprehensive analysis of cost-volume-profit (CVP) scenarios and a capital investment decision. The CVP analysis explores different options, including updating machinery and reducing prices, to maximize profitability. The capital investment section evaluates projected profits, cash flows, accounting rate of return (ARR), payback period, net present value (NPV), internal rate of return (IRR), and working capital requirements to determine the viability of the investment. The report concludes with recommendations based on the financial analysis, suggesting investment in the project while closely monitoring working capital.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.