Budgeting, Costing, Overhead Allocation, and Financial Analysis

VerifiedAdded on 2020/02/18

|10

|2262

|54

Homework Assignment

AI Summary

This assignment solution delves into the intricacies of budgeting and cost accounting. It begins by explaining the concept of a flexible budget, its advantages, and its role in cost control. The solution then outlines the importance of various pre-cash budget preparations, including sales and purchase budgets. The discussion extends to the operating cycle and cash cycle, emphasizing their impact on working capital management. The document further explores the significance of accounting in both private and government sectors, highlighting its role in planning, decision-making, and minimizing financial risks. Finally, the assignment addresses the objectives of costing systems, particularly in determining selling prices and facilitating cost reduction. The solution also includes calculations for overhead allocation rates, product costing, and a discussion on the reasons for using budgeted overhead allocation rates. References are provided at the end of the document.

BUDGETING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1..................................................................................................................................1

(a).................................................................................................................................................1

(b).................................................................................................................................................1

(c).................................................................................................................................................2

(d).................................................................................................................................................3

(e).................................................................................................................................................3

QUESTION 2..................................................................................................................................4

(a).................................................................................................................................................4

(b).................................................................................................................................................4

(c).................................................................................................................................................4

(d).................................................................................................................................................5

(e).................................................................................................................................................6

References........................................................................................................................................7

QUESTION 1..................................................................................................................................1

(a).................................................................................................................................................1

(b).................................................................................................................................................1

(c).................................................................................................................................................2

(d).................................................................................................................................................3

(e).................................................................................................................................................3

QUESTION 2..................................................................................................................................4

(a).................................................................................................................................................4

(b).................................................................................................................................................4

(c).................................................................................................................................................4

(d).................................................................................................................................................5

(e).................................................................................................................................................6

References........................................................................................................................................7

QUESTION 1

(a)

The flexible budget is also called flex budget helps to fulfil the objective of cost control.

It makes the annual budget more efficient. It works on dual mode because it not only compares

past performance with the present performance but also helps to ascertain and revised (if

necessary) expenses (Collier, 2015).

It is generally prepared at the end of the accounting period in order to compare the actual

performance with expected performance. For example –sale of the business is $10miliion in

2015-16 which increases to $12million dollar in 2016-2017 then it shows a favourable change of

$2million. However, if company spend $1miliion on expenses in 2015-2016 which is increased

to $1.2million in 2016-2017, then it shows unfavourable changes of $200000 (Libby,

Rennekamp, and Seybert, 2015).

Firms may prepare flexible budget according to the different scenario of business which

is also known as pro forma analysis. For example- a restaurant makes a flexible budget

displaying profit and expenses if they get 1000 bookings in a year. Also, it prepares a flexible

budget if they get 800 bookings and 500 bookings. Each and every budget shows the difference

in not only earnings but it also on items related to expenses. For creating a useful budget, the

organization needs to ascertain all the factors which affect its business (Chen, TAN, and Wang,

2013).

(b)

Certain budgets are prepared before making cash budget. It includes -:

Sales budget –

The sales budget is prepared first because cash budget relies on the information given by

sales budget. It is started by estimating sales revenue generated by the company’s sales

department. Many tools are used by the management to estimate sales like economic prediction,

industry data, stats etc. Sales budget shows categorization of cash and credit transactions on the

basis of which further budgets are prepar5red. (Keune and Keune, 2016).

Purchase budget –

After getting information from sales budget and finished goods, production budget is

made. It shows how much quantity is manufactured in a given period of time. The cash budget is

1

(a)

The flexible budget is also called flex budget helps to fulfil the objective of cost control.

It makes the annual budget more efficient. It works on dual mode because it not only compares

past performance with the present performance but also helps to ascertain and revised (if

necessary) expenses (Collier, 2015).

It is generally prepared at the end of the accounting period in order to compare the actual

performance with expected performance. For example –sale of the business is $10miliion in

2015-16 which increases to $12million dollar in 2016-2017 then it shows a favourable change of

$2million. However, if company spend $1miliion on expenses in 2015-2016 which is increased

to $1.2million in 2016-2017, then it shows unfavourable changes of $200000 (Libby,

Rennekamp, and Seybert, 2015).

Firms may prepare flexible budget according to the different scenario of business which

is also known as pro forma analysis. For example- a restaurant makes a flexible budget

displaying profit and expenses if they get 1000 bookings in a year. Also, it prepares a flexible

budget if they get 800 bookings and 500 bookings. Each and every budget shows the difference

in not only earnings but it also on items related to expenses. For creating a useful budget, the

organization needs to ascertain all the factors which affect its business (Chen, TAN, and Wang,

2013).

(b)

Certain budgets are prepared before making cash budget. It includes -:

Sales budget –

The sales budget is prepared first because cash budget relies on the information given by

sales budget. It is started by estimating sales revenue generated by the company’s sales

department. Many tools are used by the management to estimate sales like economic prediction,

industry data, stats etc. Sales budget shows categorization of cash and credit transactions on the

basis of which further budgets are prepar5red. (Keune and Keune, 2016).

Purchase budget –

After getting information from sales budget and finished goods, production budget is

made. It shows how much quantity is manufactured in a given period of time. The cash budget is

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

created with some assumptions about spending and receivables after making production budget.

For example – if a company ABC wants to produce 5000 pairs of shoes and one pair

manufacturing cost is $50 then it will affect the cash budget because company spend $250000 on

manufacturing shoes (Braun et al., 2014). It will vary according to changing in quantity of

manufactured shoes.

Operating budget –

It is an annual budget which includes the total value of resources required for the

expected performance of the organization. All the money which is going to be spending on

business expenditure will generate the cash flow of the company, and if money is taken as a loan,

then also it is required to be considered as it has to be paid and planning for a business is to be

done accordingly. The cash budget relies on operating budget for its detailed information

regarding allocation of funds. (DRURY, 2013).

(c)

Manufacturer view of operating cycle is a time period in which cash is converted into

products and also includes time taken for the product to be sold in the market and turned back

into cash. Both the cycle carries similar purpose, but operating cycle shows the time required to

make and sell the product where as cash cycle shows how the company is managing the cash.

Both the cycles affect each other as longer operating period leads to longer cash cycle where as

shorter operating period leads to shorter cash cycle (Bamber and Parry, 2014).

Both cycles are essential for working capital management. They determine the efficiency

of the firm. If a cash cycle of a firm is short, then it reflects good working capital conditions, but

if a cash cycle is long, then it reflects bad working capital condition. The three most important

components of the working capital are inventory, accounts receivable and account payable.

Analysts believe that these ratios are considered in analyzing working capital management

efficiency of business (Otley, 2015).

Inventory turnover ratio – It refers to the number of times in which company replaces and

sell their stock in a given period of time.

Working capital ratio – This ratio tells about the organization whether its meet their

working capital requirement or not (Abernethy, Bouwens and Lent, 2013).

2

For example – if a company ABC wants to produce 5000 pairs of shoes and one pair

manufacturing cost is $50 then it will affect the cash budget because company spend $250000 on

manufacturing shoes (Braun et al., 2014). It will vary according to changing in quantity of

manufactured shoes.

Operating budget –

It is an annual budget which includes the total value of resources required for the

expected performance of the organization. All the money which is going to be spending on

business expenditure will generate the cash flow of the company, and if money is taken as a loan,

then also it is required to be considered as it has to be paid and planning for a business is to be

done accordingly. The cash budget relies on operating budget for its detailed information

regarding allocation of funds. (DRURY, 2013).

(c)

Manufacturer view of operating cycle is a time period in which cash is converted into

products and also includes time taken for the product to be sold in the market and turned back

into cash. Both the cycle carries similar purpose, but operating cycle shows the time required to

make and sell the product where as cash cycle shows how the company is managing the cash.

Both the cycles affect each other as longer operating period leads to longer cash cycle where as

shorter operating period leads to shorter cash cycle (Bamber and Parry, 2014).

Both cycles are essential for working capital management. They determine the efficiency

of the firm. If a cash cycle of a firm is short, then it reflects good working capital conditions, but

if a cash cycle is long, then it reflects bad working capital condition. The three most important

components of the working capital are inventory, accounts receivable and account payable.

Analysts believe that these ratios are considered in analyzing working capital management

efficiency of business (Otley, 2015).

Inventory turnover ratio – It refers to the number of times in which company replaces and

sell their stock in a given period of time.

Working capital ratio – This ratio tells about the organization whether its meet their

working capital requirement or not (Abernethy, Bouwens and Lent, 2013).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Collection ratio – It shows the average time in which organization recover their money

due through credit sales to customers.

(d)

Every business needs to determine profit and maintain their accounts whether it is run by

the government or private sector because they are accountable to the government of state or

country. It is rightly said that no economic activity is successful with no thought of accounting.

For example, suppose we are in past when we are a child, someone gives us money to spend, but

suddenly it vanishes so how we feel? Same is happening with the government organization

(Gadave, 2017). No organization will run without knowing where their money went. Majority of

government company will ruin their economic condition due to poor financial management.

Accounting is not only essential for determining profitability but also it provides assistance to

management for better planning, decision-making and controlling. It also helps to evaluate the

performance of government organization and also minimize the risk of fraud and theft. If

organizations do not adopt the accounting system, then it will create the situation of chaos

(Edmonds et al., 2016).

Just as private companies, government companies also needed funds to meet their

working capital requirements or expansion requirements so they need to issue their financial

statement to regulatory authorities to raise the confidence of investors. At last, I want to conclude

that accounting in a government organization is necessary to run business with accuracy,

effectiveness and efficiency, so there is no replacement of accounting (Kim, 2016).

(e)

One of the most common and important purposes of the costing system is to determine

the selling price. Cost ascertainment helps managers or owner of the organization to fix the price

of a product, in making a financial statement and to develop policies. If we take an example from

the practical life, a burger maker needs to ascertain the cost of vegetables, bread, and other

ingredients to determine the price which is going to be charged from the customer so they take

the help of cost accounting (Dejong and Ling, 2013).

The second important objective is cost reduction. The organization must be able to track

their expenses and minimize inefficiency in work that’s why costing system is developed to

3

due through credit sales to customers.

(d)

Every business needs to determine profit and maintain their accounts whether it is run by

the government or private sector because they are accountable to the government of state or

country. It is rightly said that no economic activity is successful with no thought of accounting.

For example, suppose we are in past when we are a child, someone gives us money to spend, but

suddenly it vanishes so how we feel? Same is happening with the government organization

(Gadave, 2017). No organization will run without knowing where their money went. Majority of

government company will ruin their economic condition due to poor financial management.

Accounting is not only essential for determining profitability but also it provides assistance to

management for better planning, decision-making and controlling. It also helps to evaluate the

performance of government organization and also minimize the risk of fraud and theft. If

organizations do not adopt the accounting system, then it will create the situation of chaos

(Edmonds et al., 2016).

Just as private companies, government companies also needed funds to meet their

working capital requirements or expansion requirements so they need to issue their financial

statement to regulatory authorities to raise the confidence of investors. At last, I want to conclude

that accounting in a government organization is necessary to run business with accuracy,

effectiveness and efficiency, so there is no replacement of accounting (Kim, 2016).

(e)

One of the most common and important purposes of the costing system is to determine

the selling price. Cost ascertainment helps managers or owner of the organization to fix the price

of a product, in making a financial statement and to develop policies. If we take an example from

the practical life, a burger maker needs to ascertain the cost of vegetables, bread, and other

ingredients to determine the price which is going to be charged from the customer so they take

the help of cost accounting (Dejong and Ling, 2013).

The second important objective is cost reduction. The organization must be able to track

their expenses and minimize inefficiency in work that’s why costing system is developed to

3

maintain and present the money spending by each and every department of the organization.

Generally, people confused cost reduction with cost control. Cost control may affect the quality

of product whereas cost reduction retains the quality of the product as it minimize wastage in

distribution, administration and manufacturing channel (Kravet, 2014). Costing system also

contributes to developing financial statement because the information gathers by the costing

system is ultimately used by accountants for this purpose. For instance, raw material cost and

inventory prices are used by both financial accounting and cost accounting.

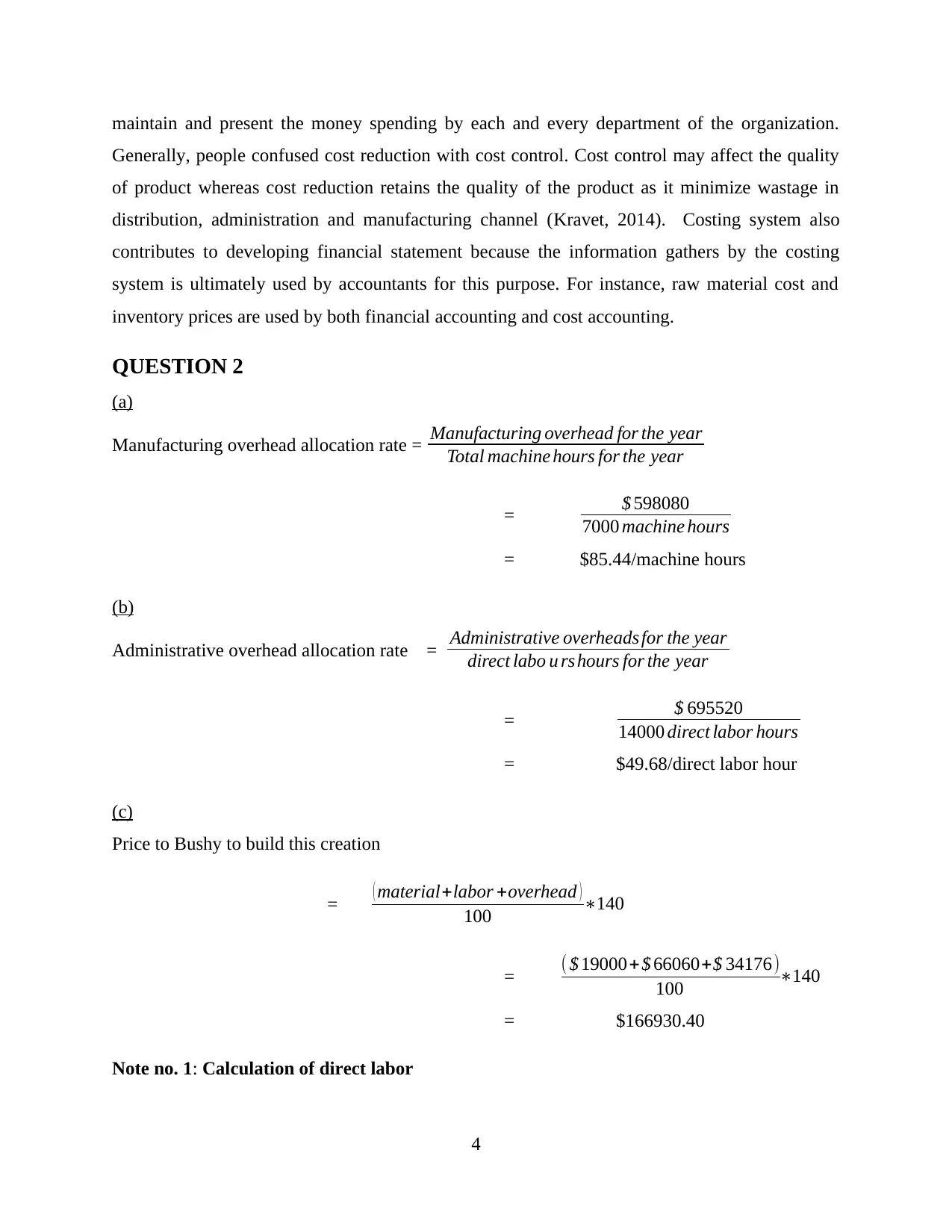

QUESTION 2

(a)

Manufacturing overhead allocation rate = Manufacturing overhead for the year

Total machine hours for the year

= $ 598080

7000 machine hours

= $85.44/machine hours

(b)

Administrative overhead allocation rate = Administrative overheads for the year

direct labo u rs hours for the year

= $ 695520

14000 direct labor hours

= $49.68/direct labor hour

(c)

Price to Bushy to build this creation

= ( material+labor +overhead )

100 ∗140

= ( $ 19000+$ 66060+$ 34176)

100 ∗140

= $166930.40

Note no. 1: Calculation of direct labor

4

Generally, people confused cost reduction with cost control. Cost control may affect the quality

of product whereas cost reduction retains the quality of the product as it minimize wastage in

distribution, administration and manufacturing channel (Kravet, 2014). Costing system also

contributes to developing financial statement because the information gathers by the costing

system is ultimately used by accountants for this purpose. For instance, raw material cost and

inventory prices are used by both financial accounting and cost accounting.

QUESTION 2

(a)

Manufacturing overhead allocation rate = Manufacturing overhead for the year

Total machine hours for the year

= $ 598080

7000 machine hours

= $85.44/machine hours

(b)

Administrative overhead allocation rate = Administrative overheads for the year

direct labo u rs hours for the year

= $ 695520

14000 direct labor hours

= $49.68/direct labor hour

(c)

Price to Bushy to build this creation

= ( material+labor +overhead )

100 ∗140

= ( $ 19000+$ 66060+$ 34176)

100 ∗140

= $166930.40

Note no. 1: Calculation of direct labor

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

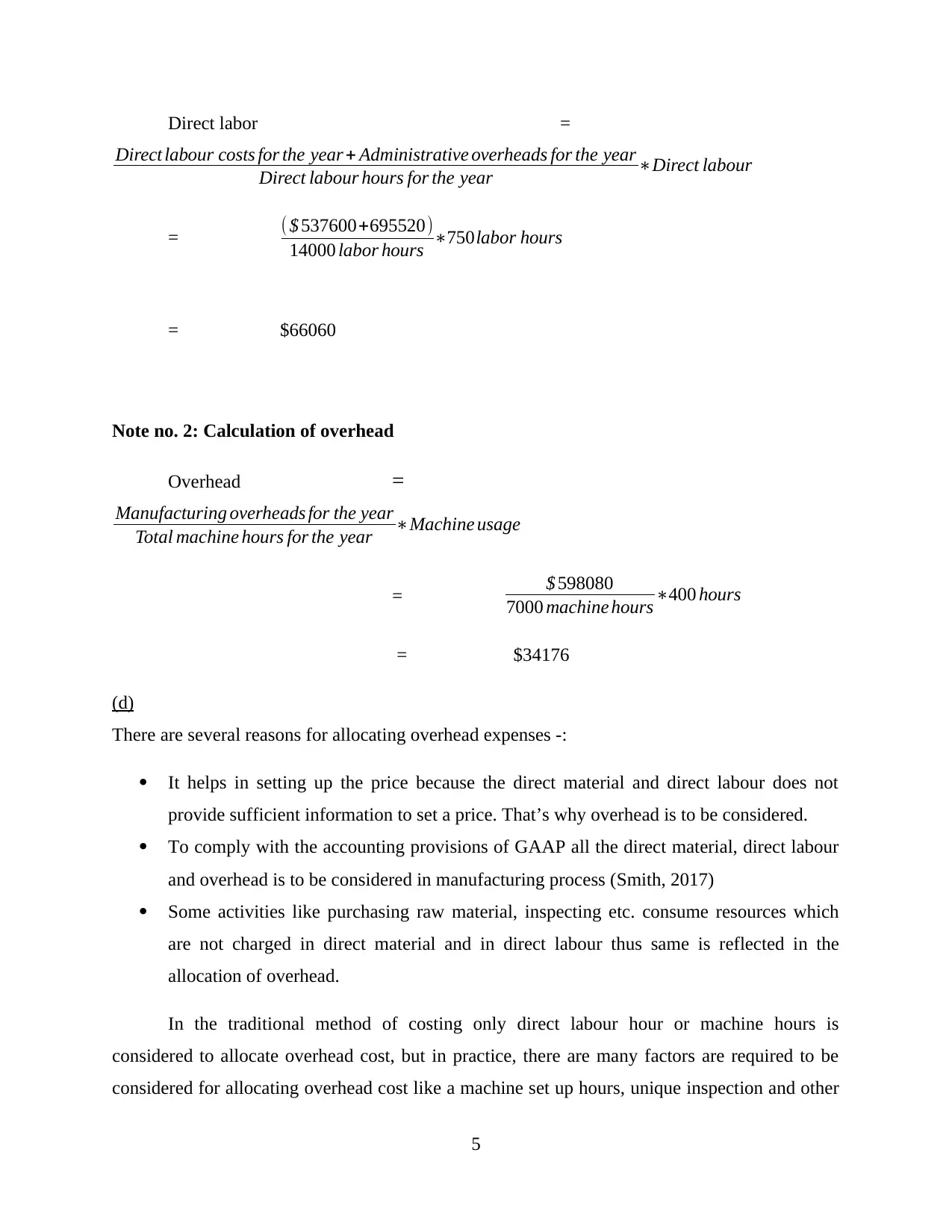

Direct labor =

Direct labour costs for the year + Administrative overheads for the year

Direct labour hours for the year ∗Direct labour

= ( $ 537600+695520)

14000 labor hours ∗750labor hours

= $66060

Note no. 2: Calculation of overhead

Overhead =

Manufacturing overheads for the year

Total machine hours for the year ∗Machine usage

= $ 598080

7000 machine hours ∗400 hours

= $34176

(d)

There are several reasons for allocating overhead expenses -:

It helps in setting up the price because the direct material and direct labour does not

provide sufficient information to set a price. That’s why overhead is to be considered.

To comply with the accounting provisions of GAAP all the direct material, direct labour

and overhead is to be considered in manufacturing process (Smith, 2017)

Some activities like purchasing raw material, inspecting etc. consume resources which

are not charged in direct material and in direct labour thus same is reflected in the

allocation of overhead.

In the traditional method of costing only direct labour hour or machine hours is

considered to allocate overhead cost, but in practice, there are many factors are required to be

considered for allocating overhead cost like a machine set up hours, unique inspection and other

5

Direct labour costs for the year + Administrative overheads for the year

Direct labour hours for the year ∗Direct labour

= ( $ 537600+695520)

14000 labor hours ∗750labor hours

= $66060

Note no. 2: Calculation of overhead

Overhead =

Manufacturing overheads for the year

Total machine hours for the year ∗Machine usage

= $ 598080

7000 machine hours ∗400 hours

= $34176

(d)

There are several reasons for allocating overhead expenses -:

It helps in setting up the price because the direct material and direct labour does not

provide sufficient information to set a price. That’s why overhead is to be considered.

To comply with the accounting provisions of GAAP all the direct material, direct labour

and overhead is to be considered in manufacturing process (Smith, 2017)

Some activities like purchasing raw material, inspecting etc. consume resources which

are not charged in direct material and in direct labour thus same is reflected in the

allocation of overhead.

In the traditional method of costing only direct labour hour or machine hours is

considered to allocate overhead cost, but in practice, there are many factors are required to be

considered for allocating overhead cost like a machine set up hours, unique inspection and other

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

similar factors. Activities in production have different complexity and consume different

resources, but it is charged on the basis of production hour which averages the rate and

distributes an equal amount to the product. This approach misleads the cost of the product

because some product consumes more resources and time as compared to another one (Crosson

and Needles, 2013).

Activity based costing is the replacement of traditional method because it overcomes the

weakness of traditional method as it has various pools of cost and consequently it allocates the

cost in an accurate manner.

(e)

There are several reasons for companies to use (budgeted) overhead allocation rates rather than

using actual overhead costs in allocating overhead costs to units of a product is -:

Actual overhead rates are not available in a timely manner, and the budgeted overhead

rate is almost close to actual overhead rate (Braun et al., 2014).

Budgeted overhead cost is more reasonable for production costing because actual rates

are changing and have dependability upon external circumstances.

If actual overhead rates are used, then it affects reported cost of other product.

6

resources, but it is charged on the basis of production hour which averages the rate and

distributes an equal amount to the product. This approach misleads the cost of the product

because some product consumes more resources and time as compared to another one (Crosson

and Needles, 2013).

Activity based costing is the replacement of traditional method because it overcomes the

weakness of traditional method as it has various pools of cost and consequently it allocates the

cost in an accurate manner.

(e)

There are several reasons for companies to use (budgeted) overhead allocation rates rather than

using actual overhead costs in allocating overhead costs to units of a product is -:

Actual overhead rates are not available in a timely manner, and the budgeted overhead

rate is almost close to actual overhead rate (Braun et al., 2014).

Budgeted overhead cost is more reasonable for production costing because actual rates

are changing and have dependability upon external circumstances.

If actual overhead rates are used, then it affects reported cost of other product.

6

REFERENCES

Abernethy, M.A., Bouwens, J. and Lent, L., 2013. The role of performance measures in the

intertemporal decisions of business unit managers. Contemporary accounting research, 30(3),

pp.925-961.

Bamber, M. and Parry, S., 2014. Accounting and Finance for Managers: A Decision-making

Approach. Kogan Page Publishers.

Braun, K.W., Tietz, W.M., Harrison, W.T., Bamber, L.S. and Horngren, C.T., 2014. Managerial

accounting. Pearson.

Chen, W., TAN, H.T. and Wang, E.Y., 2013. Fair value accounting and managers' hedging

decisions. Journal of Accounting Research, 51(1), pp.67-103.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Crosson, S.V. and Needles, B.E., 2013. Managerial accounting. Cengage Learning.

Dejong, D. and Ling, Z., 2013. Managers: Their effects on accruals and firm policies. Journal of

Business Finance & Accounting, 40(1-2), pp.82-114.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education.

Gadave, B.R., 2017. Glimpses on Responsibility Accounting and Reporting. Imperial Journal of

Interdisciplinary Research, 3(2).

Keune, M.B. and Keune, T.M., 2016. Do Managers Make Voluntary Accounting Changes in

Response to a Material Weakness in Internal Control? Auditing: A Journal of Practice and

Theory.

Kim, J.B., 2016. Accounting flexibility and managers’ forecast behavior prior to seasoned equity

offerings. Review of Accounting Studies, 21(4), pp.1361-1400.

Kravet, T.D., 2014. Accounting conservatism and managerial risk-taking: Corporate

acquisitions. Journal of Accounting and Economics, 57(2), pp.218-240.

Libby, R., Rennekamp, K.M. and Seybert, N., 2015. Regulation and the interdependent roles of

managers, auditors, and directors in earnings management and accounting choice. Accounting,

Organizations and Society, 47, pp.25-42.

Otley, D., 2015. in Management Control. Critical Perspectives in Management Control, p.27.

Smith, M., 2017. Research methods in accounting. Sage.

7

Abernethy, M.A., Bouwens, J. and Lent, L., 2013. The role of performance measures in the

intertemporal decisions of business unit managers. Contemporary accounting research, 30(3),

pp.925-961.

Bamber, M. and Parry, S., 2014. Accounting and Finance for Managers: A Decision-making

Approach. Kogan Page Publishers.

Braun, K.W., Tietz, W.M., Harrison, W.T., Bamber, L.S. and Horngren, C.T., 2014. Managerial

accounting. Pearson.

Chen, W., TAN, H.T. and Wang, E.Y., 2013. Fair value accounting and managers' hedging

decisions. Journal of Accounting Research, 51(1), pp.67-103.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Crosson, S.V. and Needles, B.E., 2013. Managerial accounting. Cengage Learning.

Dejong, D. and Ling, Z., 2013. Managers: Their effects on accruals and firm policies. Journal of

Business Finance & Accounting, 40(1-2), pp.82-114.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education.

Gadave, B.R., 2017. Glimpses on Responsibility Accounting and Reporting. Imperial Journal of

Interdisciplinary Research, 3(2).

Keune, M.B. and Keune, T.M., 2016. Do Managers Make Voluntary Accounting Changes in

Response to a Material Weakness in Internal Control? Auditing: A Journal of Practice and

Theory.

Kim, J.B., 2016. Accounting flexibility and managers’ forecast behavior prior to seasoned equity

offerings. Review of Accounting Studies, 21(4), pp.1361-1400.

Kravet, T.D., 2014. Accounting conservatism and managerial risk-taking: Corporate

acquisitions. Journal of Accounting and Economics, 57(2), pp.218-240.

Libby, R., Rennekamp, K.M. and Seybert, N., 2015. Regulation and the interdependent roles of

managers, auditors, and directors in earnings management and accounting choice. Accounting,

Organizations and Society, 47, pp.25-42.

Otley, D., 2015. in Management Control. Critical Perspectives in Management Control, p.27.

Smith, M., 2017. Research methods in accounting. Sage.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.