Managerial Accounting: Costing System Analysis and Recommendations

VerifiedAdded on 2023/06/05

|12

|2132

|205

Homework Assignment

AI Summary

This assignment solution delves into managerial accounting, analyzing Pristine Limited's traditional costing system and its associated problems, such as the use of a single cost driver and missing allocations. It identifies indicators highlighting the system's flaws, including complexities in operations and inaccurate profit calculations. The solution proposes an activity-based costing (ABC) approach, detailing activity cost rates and providing an income statement comparison between metal and plastic safes under both costing methods. It emphasizes the benefits of ABC costing, such as true product costs and better decision-making, while also addressing implementation challenges. Finally, it offers suggestions for improving profitability for customers purchasing low-margin products and costly services, advocating for competitive pricing, large volume sales, and supplier discounts. Desklib provides this document and many other resources to aid students in their academic journey.

MANAGERIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Solution 1:..................................................................................................................................3

Solution 2 :.................................................................................................................................4

Solution 3:..................................................................................................................................5

Solution 4:..................................................................................................................................6

Solution 5:..................................................................................................................................7

Solution 6:..................................................................................................................................8

Solution 7:................................................................................................................................10

Bibliography.............................................................................................................................11

Solution 1:..................................................................................................................................3

Solution 2 :.................................................................................................................................4

Solution 3:..................................................................................................................................5

Solution 4:..................................................................................................................................6

Solution 5:..................................................................................................................................7

Solution 6:..................................................................................................................................8

Solution 7:................................................................................................................................10

Bibliography.............................................................................................................................11

Solution 1:

Pristine Limited (PL) is a manufacturer and seller of fireproof safes and document containers

of various shapes and sizes for home use, including safes made to Australian/New Zealand

Industry standard AS/NZS 3809 (Atkinson, 2012). When it comes to preparation of product

costing, the company uses traditional costing system, which is a weak system to get a true

cost of the product. The general problems associated with PL’s traditional costing system :

Use Of One Cost Driver: Traditional costing has a concept of using only one cost

driver so as to allocate factory overheads such as direct labour hours or manufacturing

hours. However, in actuality, there are many other cost drivers such as number of

sales order, inspections, machine set ups, etc which are used to allocate the realted

costs to each product (Berry, 2009). The more the activities are, the more are the

problems of allocating all the costs associated with different activities using one cost

driver.

Missing Allocations: Due to using of one cost driver, the costs associated with

different activities will be allocated using one cost pool and therefore, will be divided

by total production hours. Such a costing system doesn’t consider the nature

complexity of the products.For example; the overhead cost is $500/hour. If an extra

hour is used to produce a product, the cost will be up by $500. Thus, the resulting

allocations are vague or misleading.

Pristine Limited (PL) is a manufacturer and seller of fireproof safes and document containers

of various shapes and sizes for home use, including safes made to Australian/New Zealand

Industry standard AS/NZS 3809 (Atkinson, 2012). When it comes to preparation of product

costing, the company uses traditional costing system, which is a weak system to get a true

cost of the product. The general problems associated with PL’s traditional costing system :

Use Of One Cost Driver: Traditional costing has a concept of using only one cost

driver so as to allocate factory overheads such as direct labour hours or manufacturing

hours. However, in actuality, there are many other cost drivers such as number of

sales order, inspections, machine set ups, etc which are used to allocate the realted

costs to each product (Berry, 2009). The more the activities are, the more are the

problems of allocating all the costs associated with different activities using one cost

driver.

Missing Allocations: Due to using of one cost driver, the costs associated with

different activities will be allocated using one cost pool and therefore, will be divided

by total production hours. Such a costing system doesn’t consider the nature

complexity of the products.For example; the overhead cost is $500/hour. If an extra

hour is used to produce a product, the cost will be up by $500. Thus, the resulting

allocations are vague or misleading.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution 2 :

Four indicators that highlight that the current costing system is outdated and flawed :

The traditional costing system is not meant for businesses which are complex in

nature or includes a number of activities or operations (Boyd, 2013). PL, being

business with complexities past few years, is still using traditional approach of

costing. As stated in the case, such a system has been questioned on the grounds

of reliability by Christine (managing director).

There are five different activities in PL’s operations with different cost drivers.

However, PL has used asingle rate, resulting in allocation of different costs on the

basis of single average rate.

Where the plastic safe is a complex product and also, has low sales volumes yet it

is showing an increase in profits due to issues in costing valuation. It has been

shown at a cost lower than what its actual cost should have been. In a similar way,

metal safes have been shown at a cost higher than what its actual cost should have

been. This resulted in calculation of wrong profits. Such calculations would result

in vague results such as PL wasn’t able to meet up with its sales targets.

There is more material movement in case of plastic safes than metal safes. Also

plastic safe, being a complex product, is recently facing a number of rejects. Thus,

it is the observation of PL that there is a need of increased quality control

activities.

Four indicators that highlight that the current costing system is outdated and flawed :

The traditional costing system is not meant for businesses which are complex in

nature or includes a number of activities or operations (Boyd, 2013). PL, being

business with complexities past few years, is still using traditional approach of

costing. As stated in the case, such a system has been questioned on the grounds

of reliability by Christine (managing director).

There are five different activities in PL’s operations with different cost drivers.

However, PL has used asingle rate, resulting in allocation of different costs on the

basis of single average rate.

Where the plastic safe is a complex product and also, has low sales volumes yet it

is showing an increase in profits due to issues in costing valuation. It has been

shown at a cost lower than what its actual cost should have been. In a similar way,

metal safes have been shown at a cost higher than what its actual cost should have

been. This resulted in calculation of wrong profits. Such calculations would result

in vague results such as PL wasn’t able to meet up with its sales targets.

There is more material movement in case of plastic safes than metal safes. Also

plastic safe, being a complex product, is recently facing a number of rejects. Thus,

it is the observation of PL that there is a need of increased quality control

activities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

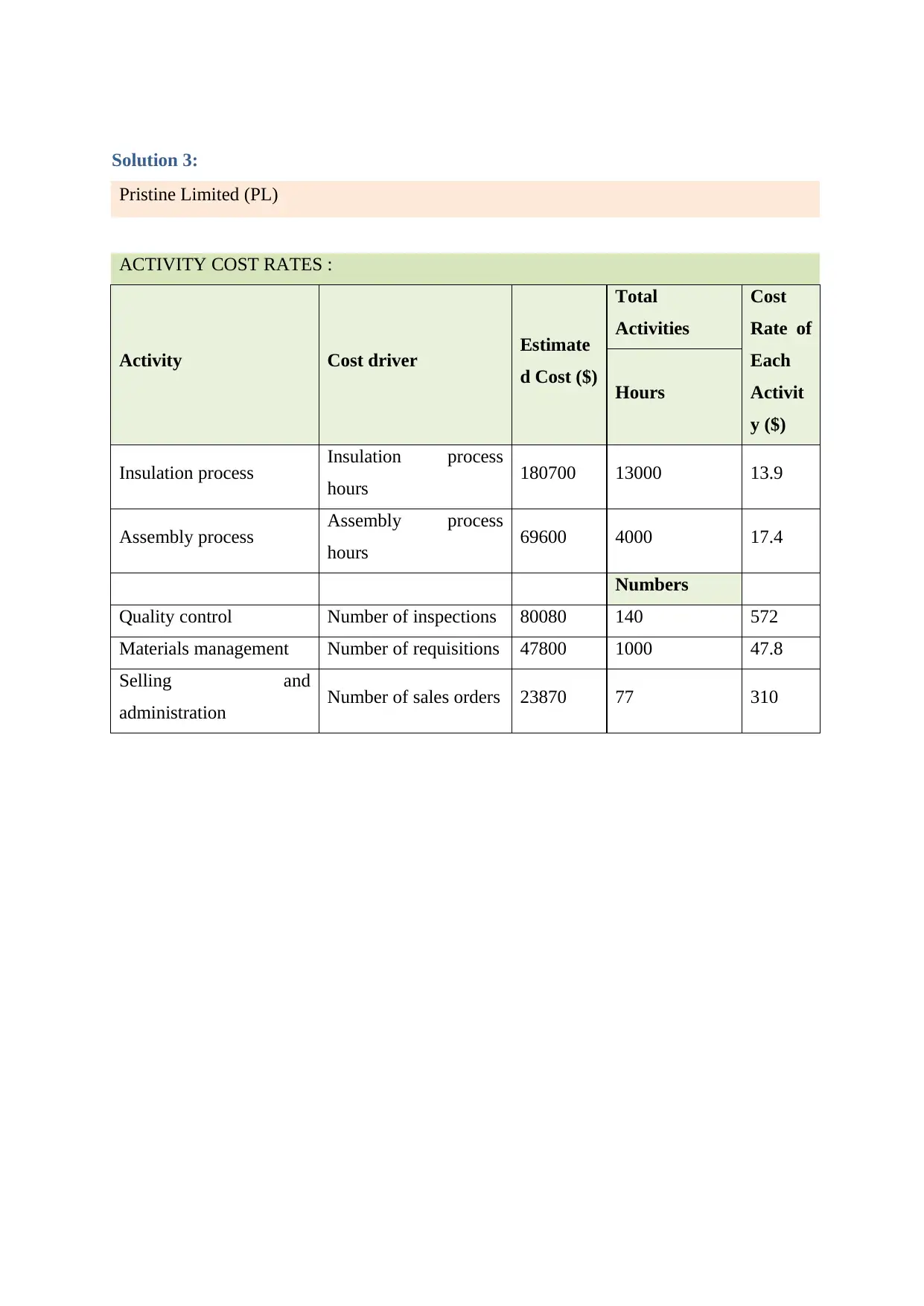

Solution 3:

Pristine Limited (PL)

ACTIVITY COST RATES :

Activity Cost driver Estimate

d Cost ($)

Total

Activities

Cost

Rate of

Each

Activit

y ($)

Hours

Insulation process Insulation process

hours 180700 13000 13.9

Assembly process Assembly process

hours 69600 4000 17.4

Numbers

Quality control Number of inspections 80080 140 572

Materials management Number of requisitions 47800 1000 47.8

Selling and

administration Number of sales orders 23870 77 310

Pristine Limited (PL)

ACTIVITY COST RATES :

Activity Cost driver Estimate

d Cost ($)

Total

Activities

Cost

Rate of

Each

Activit

y ($)

Hours

Insulation process Insulation process

hours 180700 13000 13.9

Assembly process Assembly process

hours 69600 4000 17.4

Numbers

Quality control Number of inspections 80080 140 572

Materials management Number of requisitions 47800 1000 47.8

Selling and

administration Number of sales orders 23870 77 310

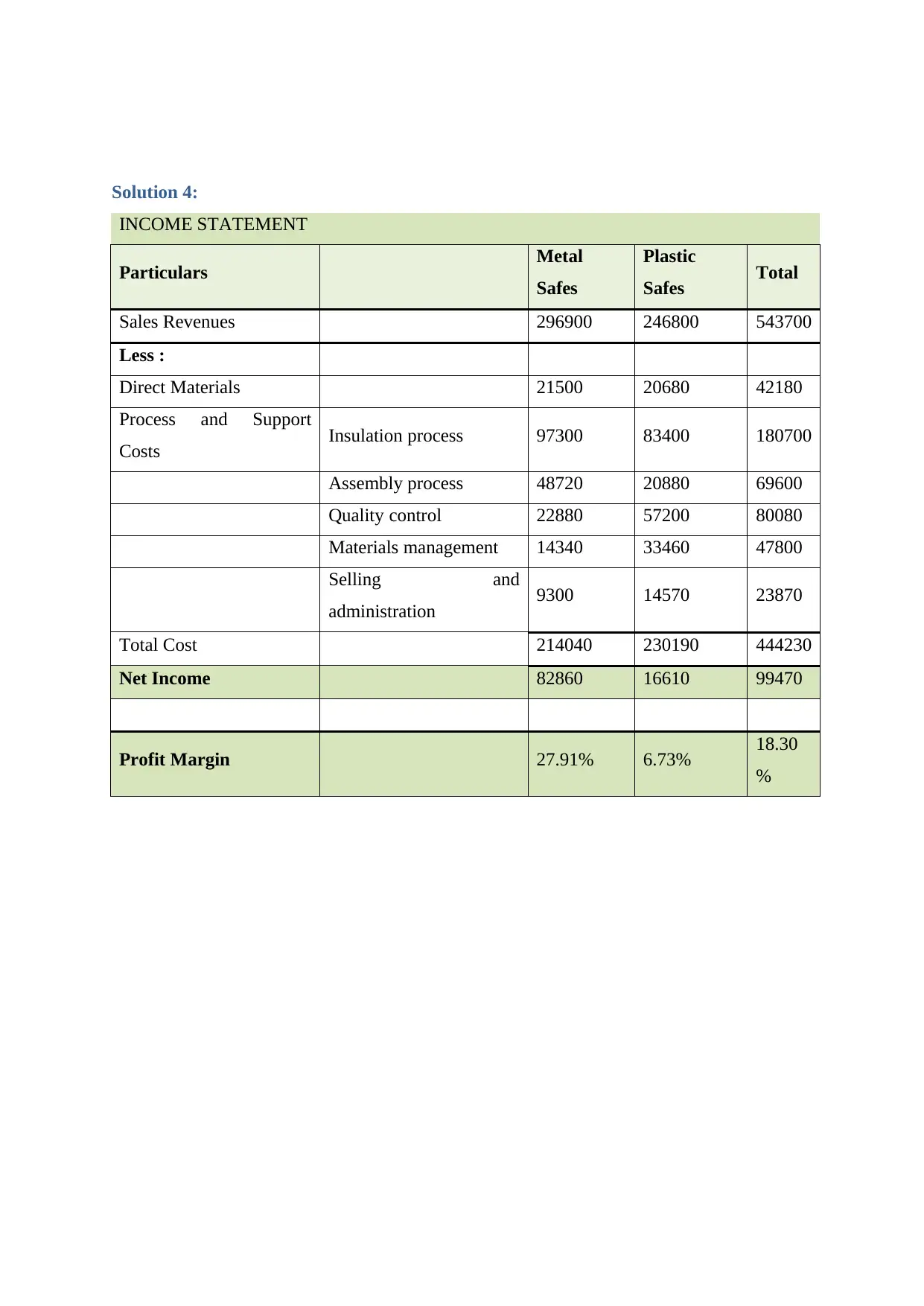

Solution 4:

INCOME STATEMENT

Particulars Metal

Safes

Plastic

Safes Total

Sales Revenues 296900 246800 543700

Less :

Direct Materials 21500 20680 42180

Process and Support

Costs Insulation process 97300 83400 180700

Assembly process 48720 20880 69600

Quality control 22880 57200 80080

Materials management 14340 33460 47800

Selling and

administration 9300 14570 23870

Total Cost 214040 230190 444230

Net Income 82860 16610 99470

Profit Margin 27.91% 6.73% 18.30

%

INCOME STATEMENT

Particulars Metal

Safes

Plastic

Safes Total

Sales Revenues 296900 246800 543700

Less :

Direct Materials 21500 20680 42180

Process and Support

Costs Insulation process 97300 83400 180700

Assembly process 48720 20880 69600

Quality control 22880 57200 80080

Materials management 14340 33460 47800

Selling and

administration 9300 14570 23870

Total Cost 214040 230190 444230

Net Income 82860 16610 99470

Profit Margin 27.91% 6.73% 18.30

%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

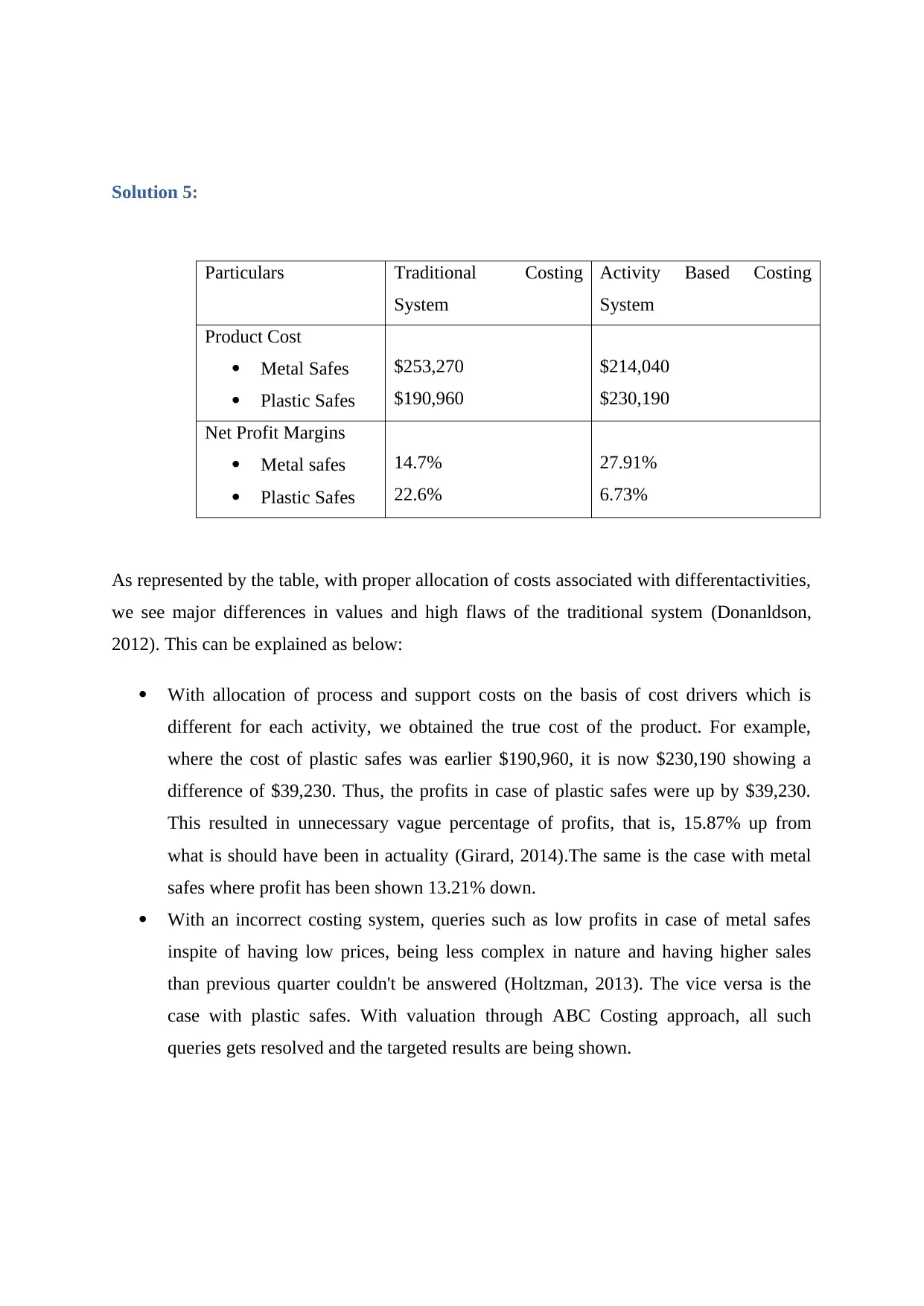

Solution 5:

Particulars Traditional Costing

System

Activity Based Costing

System

Product Cost

Metal Safes

Plastic Safes

$253,270

$190,960

$214,040

$230,190

Net Profit Margins

Metal safes

Plastic Safes

14.7%

22.6%

27.91%

6.73%

As represented by the table, with proper allocation of costs associated with differentactivities,

we see major differences in values and high flaws of the traditional system (Donanldson,

2012). This can be explained as below:

With allocation of process and support costs on the basis of cost drivers which is

different for each activity, we obtained the true cost of the product. For example,

where the cost of plastic safes was earlier $190,960, it is now $230,190 showing a

difference of $39,230. Thus, the profits in case of plastic safes were up by $39,230.

This resulted in unnecessary vague percentage of profits, that is, 15.87% up from

what is should have been in actuality (Girard, 2014).The same is the case with metal

safes where profit has been shown 13.21% down.

With an incorrect costing system, queries such as low profits in case of metal safes

inspite of having low prices, being less complex in nature and having higher sales

than previous quarter couldn't be answered (Holtzman, 2013). The vice versa is the

case with plastic safes. With valuation through ABC Costing approach, all such

queries gets resolved and the targeted results are being shown.

Particulars Traditional Costing

System

Activity Based Costing

System

Product Cost

Metal Safes

Plastic Safes

$253,270

$190,960

$214,040

$230,190

Net Profit Margins

Metal safes

Plastic Safes

14.7%

22.6%

27.91%

6.73%

As represented by the table, with proper allocation of costs associated with differentactivities,

we see major differences in values and high flaws of the traditional system (Donanldson,

2012). This can be explained as below:

With allocation of process and support costs on the basis of cost drivers which is

different for each activity, we obtained the true cost of the product. For example,

where the cost of plastic safes was earlier $190,960, it is now $230,190 showing a

difference of $39,230. Thus, the profits in case of plastic safes were up by $39,230.

This resulted in unnecessary vague percentage of profits, that is, 15.87% up from

what is should have been in actuality (Girard, 2014).The same is the case with metal

safes where profit has been shown 13.21% down.

With an incorrect costing system, queries such as low profits in case of metal safes

inspite of having low prices, being less complex in nature and having higher sales

than previous quarter couldn't be answered (Holtzman, 2013). The vice versa is the

case with plastic safes. With valuation through ABC Costing approach, all such

queries gets resolved and the targeted results are being shown.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution 6:

As discussed and represented above, we witnessed a lot of flaws in the traditional approach of

costing. The following report has been made to the managing director regarding changing the

costing approach for better results (Horngren, 2012). It is advisable that the company should

adopt activity based costing approach to prepare its books.

Activity based costing (ABC) is an approach of allocating overhead costs in a more practical

way to the products than the previous approach of allocating costs on an average rate

obtained on the basis of direct labour hours or production hours. It is a two way allocation,

that is, firstly assigning costs to the activities that together sums up the total overheads and

secondly, assigning the activities to only those products that has actually undertaken such

activities (Mattessich, 2016). The reason entities are approaching towards ABC analysis in

recent years are because (1) there is a significant increase in manufacturing overhead costs;

(2) there is no correlation between the overhead costs with the production hours; (3) entities

producing more than one products cannot use a single average rate for all its products as that

would give a false cost; (4) there is a growing diversification in products as well diversified

demands by customers. The benefits that can accrue due to activity based costing can be

explained as :

True Product Cost: It gives an accurate cost for each of the products the organization

is specializing in. This also helps in understanding the true nature of overheads.

Information about Cost Behaviour: With the correct understanding of overheads, an

entity can take into view the expenditure they are making and whether it is justifiable

or not. it helps in identification of activities that is no longer adding any value to the

product.

Control over Fixed Costs: with the correct cost information, management can

exercise control over activities that are real cause for occurrence of fixed costs. This

is possible as with proper allocation, one gets a clear picture of variable as well as

fixed costs.

Better Decision Making: The management can make decisions regarding cost

reduction or cost cutting as a more reliable product cost is available with them. This

also helps them in setting the selling prices of their products.

As discussed and represented above, we witnessed a lot of flaws in the traditional approach of

costing. The following report has been made to the managing director regarding changing the

costing approach for better results (Horngren, 2012). It is advisable that the company should

adopt activity based costing approach to prepare its books.

Activity based costing (ABC) is an approach of allocating overhead costs in a more practical

way to the products than the previous approach of allocating costs on an average rate

obtained on the basis of direct labour hours or production hours. It is a two way allocation,

that is, firstly assigning costs to the activities that together sums up the total overheads and

secondly, assigning the activities to only those products that has actually undertaken such

activities (Mattessich, 2016). The reason entities are approaching towards ABC analysis in

recent years are because (1) there is a significant increase in manufacturing overhead costs;

(2) there is no correlation between the overhead costs with the production hours; (3) entities

producing more than one products cannot use a single average rate for all its products as that

would give a false cost; (4) there is a growing diversification in products as well diversified

demands by customers. The benefits that can accrue due to activity based costing can be

explained as :

True Product Cost: It gives an accurate cost for each of the products the organization

is specializing in. This also helps in understanding the true nature of overheads.

Information about Cost Behaviour: With the correct understanding of overheads, an

entity can take into view the expenditure they are making and whether it is justifiable

or not. it helps in identification of activities that is no longer adding any value to the

product.

Control over Fixed Costs: with the correct cost information, management can

exercise control over activities that are real cause for occurrence of fixed costs. This

is possible as with proper allocation, one gets a clear picture of variable as well as

fixed costs.

Better Decision Making: The management can make decisions regarding cost

reduction or cost cutting as a more reliable product cost is available with them. This

also helps them in setting the selling prices of their products.

Adoption and implementation of ABC costing system is a costly process as it is a way

broader concept and includes a number of resources (Mattessich, 2016). The issues associated

with ABC costing can be stated below:

Complex in nature: Due to using of different cost drivers and cost pools, it is complex

in nature and this is why, it is a costly system .

Measurement Difficulties: ABC analysis requires determination of various cost

drivers and activities that can serve as the basis for cost allocation. Such

measurements require extreme expertise and therefore, are costly. In fact, a simple

ABC system also requires a lot of calculations for determining costs. Also, Activity

costing rates have to be updated regularly.

Other Difficulties : Such other difficulties that can be faced are selection of cost driver

for an activity, allocation of common costs, varying rates of cost drivers, less

knowledge of implementing ABC system properly (McLaney & Adril, 2016).

broader concept and includes a number of resources (Mattessich, 2016). The issues associated

with ABC costing can be stated below:

Complex in nature: Due to using of different cost drivers and cost pools, it is complex

in nature and this is why, it is a costly system .

Measurement Difficulties: ABC analysis requires determination of various cost

drivers and activities that can serve as the basis for cost allocation. Such

measurements require extreme expertise and therefore, are costly. In fact, a simple

ABC system also requires a lot of calculations for determining costs. Also, Activity

costing rates have to be updated regularly.

Other Difficulties : Such other difficulties that can be faced are selection of cost driver

for an activity, allocation of common costs, varying rates of cost drivers, less

knowledge of implementing ABC system properly (McLaney & Adril, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution 7:

For a customer of PL who prefers to purchase low margin products and costly services, better

profits can be made if the company can consider the following suggestions:

Sets a competitive price of products: This means having an understanding of the

market price and setting the selling price accordingly. This would help in attracting

customers. A customer has an understanding of all the selling prices set by different

sellers in the market and accordingly, makes its decision of choosing the product.

Therefore, setting prices higher than the market price would penalize the company

and setting prices lower than the market price would raise questions on the quality of

the product.

Large volume sales of products: low margin products attract customers preferring

qualitative products with low margin. Also, low margin products have more number

of customers. With increase in number and size of transactions, the company can

minimize the effect of costs by having sufficient sales and therefore, profits. The

company should conduct practices such as advertising, sales promotion etc to increase

its sales (Seal, 2012).

Discounts from Suppliers: The Company should seek for discounts from suppliers.

Discount received would result in deduction of costs and therefore, lead to more sales

value and therefore, more profits.

Making an Analysis of cost of substitute services available in the market : The

company should analyze the costs of services of different market suppliers and make

a decision based on that regarding which supplier should be selected (Taillard, 2013).

Thus, using above methods and such other similar methods, profitability can be increased or

improved.

For a customer of PL who prefers to purchase low margin products and costly services, better

profits can be made if the company can consider the following suggestions:

Sets a competitive price of products: This means having an understanding of the

market price and setting the selling price accordingly. This would help in attracting

customers. A customer has an understanding of all the selling prices set by different

sellers in the market and accordingly, makes its decision of choosing the product.

Therefore, setting prices higher than the market price would penalize the company

and setting prices lower than the market price would raise questions on the quality of

the product.

Large volume sales of products: low margin products attract customers preferring

qualitative products with low margin. Also, low margin products have more number

of customers. With increase in number and size of transactions, the company can

minimize the effect of costs by having sufficient sales and therefore, profits. The

company should conduct practices such as advertising, sales promotion etc to increase

its sales (Seal, 2012).

Discounts from Suppliers: The Company should seek for discounts from suppliers.

Discount received would result in deduction of costs and therefore, lead to more sales

value and therefore, more profits.

Making an Analysis of cost of substitute services available in the market : The

company should analyze the costs of services of different market suppliers and make

a decision based on that regarding which supplier should be selected (Taillard, 2013).

Thus, using above methods and such other similar methods, profitability can be increased or

improved.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bibliography

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Boyd, W. K. (2013). Cost Accounting For Dummies. Hoboken: Wiley.

Donanldson, T. (2012). Ethical issues in business. New Jersey: Prentice Hall.

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

Holtzman, M. (2013). Managerial Accounting For Dummies. Hoboken, NJ: Wiley.

Horngren, C. (2012). Cost accounting. Upper Saddle River, N.J.: Pearson/Prentice Hall.

Mattessich, R. (2016). Reality and accounting. [S.I.]: Routledge.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Seal, W. (2012). Management accounting. Maidenhead: McGraw-Hill Higher Education.

Taillard, M. (2013). Corporate finance for dummies. Hoboken, N.J.: Wiley.

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Berry, L. E. (2009). Management accounting demystified. New York: McGraw-Hill.

Boyd, W. K. (2013). Cost Accounting For Dummies. Hoboken: Wiley.

Donanldson, T. (2012). Ethical issues in business. New Jersey: Prentice Hall.

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

Holtzman, M. (2013). Managerial Accounting For Dummies. Hoboken, NJ: Wiley.

Horngren, C. (2012). Cost accounting. Upper Saddle River, N.J.: Pearson/Prentice Hall.

Mattessich, R. (2016). Reality and accounting. [S.I.]: Routledge.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Seal, W. (2012). Management accounting. Maidenhead: McGraw-Hill Higher Education.

Taillard, M. (2013). Corporate finance for dummies. Hoboken, N.J.: Wiley.

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.