Costing Analysis: Comparing Traditional and ABC Costing Models

VerifiedAdded on 2021/06/15

|14

|2470

|95

Report

AI Summary

This report provides a comprehensive analysis of costing methods, comparing traditional and activity-based costing (ABC) techniques. It begins with calculations of cost per unit under both methods, followed by income statements for Sewing Easy using each costing system. The analysis highlights the impact of different costing approaches on financial outcomes, including net income and overhead allocation. The report further explores the importance of accurate product costing and differentiates between applied and actual overhead costs. It also discusses the advantages and disadvantages of the ABC model, emphasizing its relevance in modern manufacturing environments. The report concludes with a bibliography of relevant sources.

Running Head: COSTING ANALYSIS

0

Costing Analysis

Traditional and ABC Costing

0

Costing Analysis

Traditional and ABC Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

1

Table of Contents

Answer to Question-1................................................................................................................2

Answer to Question-2................................................................................................................4

Answer to Question-3................................................................................................................6

Analysis..................................................................................................................................8

Importance of accurate product costing.................................................................................8

Answer to Question 4.................................................................................................................9

Answer to Question 5...............................................................................................................10

Advantages...........................................................................................................................10

Disadvantages.......................................................................................................................11

Bibliography.............................................................................................................................13

1

Table of Contents

Answer to Question-1................................................................................................................2

Answer to Question-2................................................................................................................4

Answer to Question-3................................................................................................................6

Analysis..................................................................................................................................8

Importance of accurate product costing.................................................................................8

Answer to Question 4.................................................................................................................9

Answer to Question 5...............................................................................................................10

Advantages...........................................................................................................................10

Disadvantages.......................................................................................................................11

Bibliography.............................................................................................................................13

COSTING ANALYSIS

2

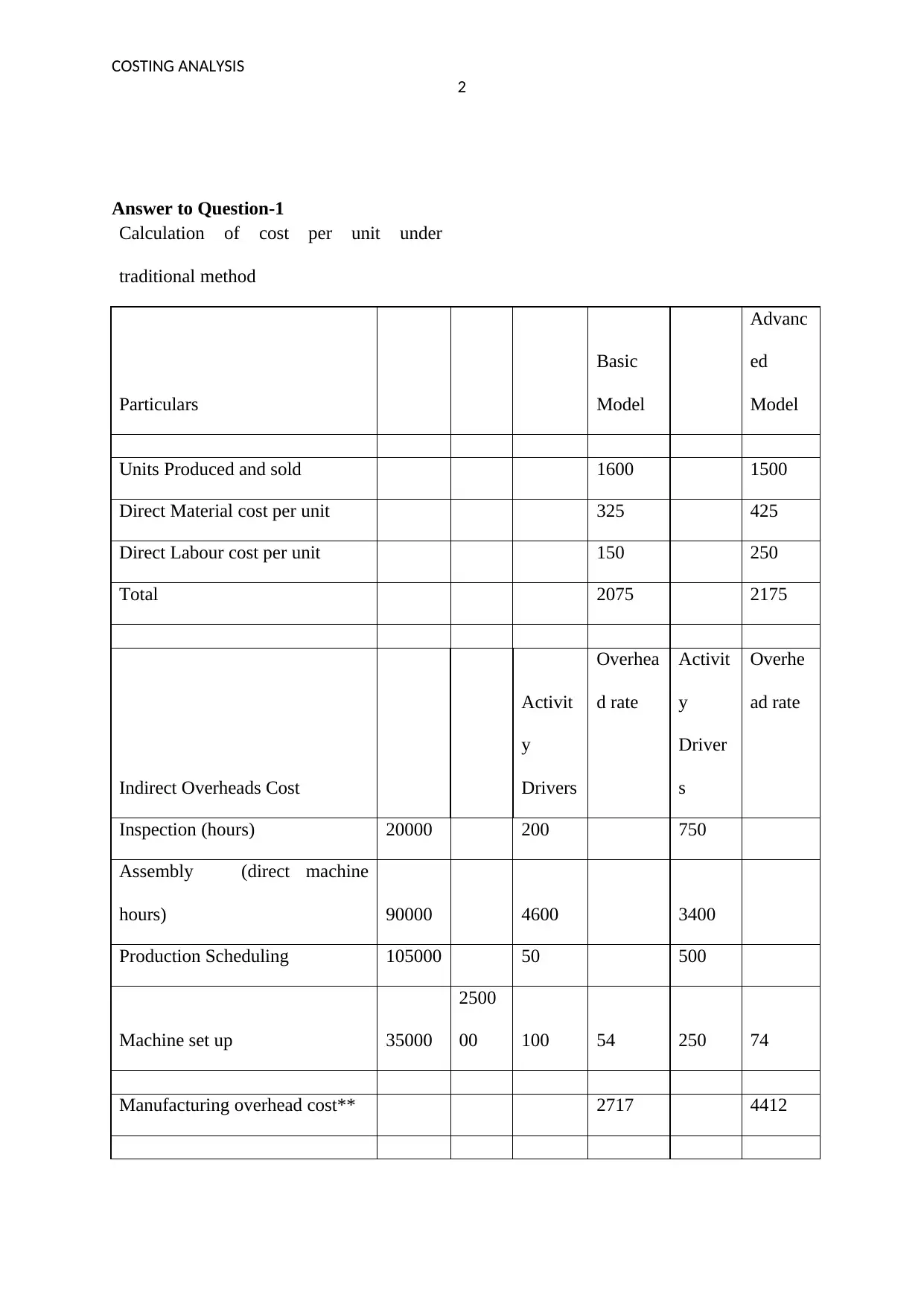

Answer to Question-1

Calculation of cost per unit under

traditional method

Particulars

Basic

Model

Advanc

ed

Model

Units Produced and sold 1600 1500

Direct Material cost per unit 325 425

Direct Labour cost per unit 150 250

Total 2075 2175

Indirect Overheads Cost

Activit

y

Drivers

Overhea

d rate

Activit

y

Driver

s

Overhe

ad rate

Inspection (hours) 20000 200 750

Assembly (direct machine

hours) 90000 4600 3400

Production Scheduling 105000 50 500

Machine set up 35000

2500

00 100 54 250 74

Manufacturing overhead cost** 2717 4412

2

Answer to Question-1

Calculation of cost per unit under

traditional method

Particulars

Basic

Model

Advanc

ed

Model

Units Produced and sold 1600 1500

Direct Material cost per unit 325 425

Direct Labour cost per unit 150 250

Total 2075 2175

Indirect Overheads Cost

Activit

y

Drivers

Overhea

d rate

Activit

y

Driver

s

Overhe

ad rate

Inspection (hours) 20000 200 750

Assembly (direct machine

hours) 90000 4600 3400

Production Scheduling 105000 50 500

Machine set up 35000

2500

00 100 54 250 74

Manufacturing overhead cost** 2717 4412

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

3

** Assuming it takes 50 hours of the direct labour in basic model and 60 hours in

advanced model

Calculation of cost per unit under traditional

method

Particulars

Basic Model Advance

d Model

Direct Material cost per unit 1600 1500

Direct Labour cost per unit 325 425

Overhead costs per unit 2717 4412

Total 4642 6337

3

** Assuming it takes 50 hours of the direct labour in basic model and 60 hours in

advanced model

Calculation of cost per unit under traditional

method

Particulars

Basic Model Advance

d Model

Direct Material cost per unit 1600 1500

Direct Labour cost per unit 325 425

Overhead costs per unit 2717 4412

Total 4642 6337

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

4

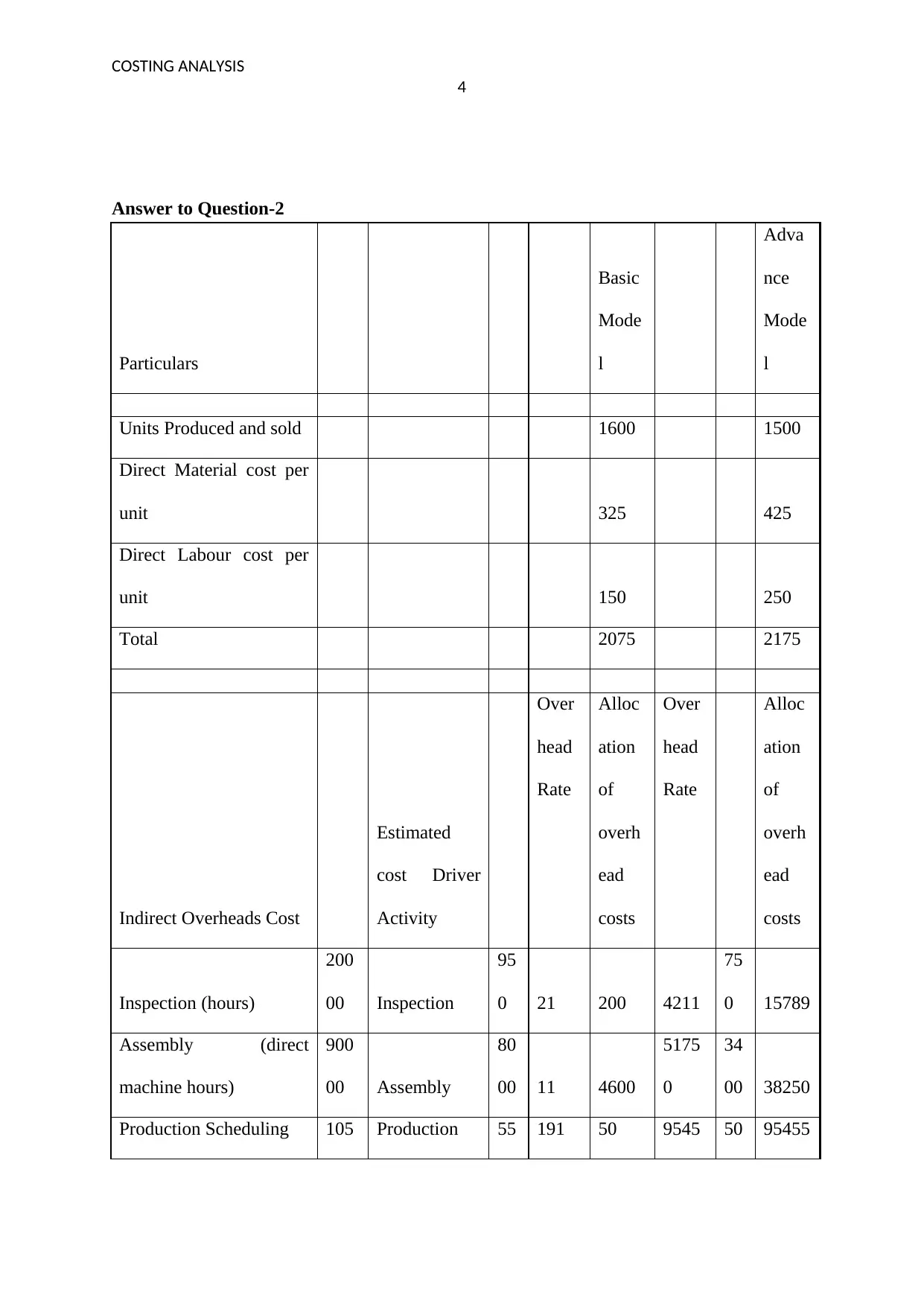

Answer to Question-2

Particulars

Basic

Mode

l

Adva

nce

Mode

l

Units Produced and sold 1600 1500

Direct Material cost per

unit 325 425

Direct Labour cost per

unit 150 250

Total 2075 2175

Indirect Overheads Cost

Estimated

cost Driver

Activity

Over

head

Rate

Alloc

ation

of

overh

ead

costs

Over

head

Rate

Alloc

ation

of

overh

ead

costs

Inspection (hours)

200

00 Inspection

95

0 21 200 4211

75

0 15789

Assembly (direct

machine hours)

900

00 Assembly

80

00 11 4600

5175

0

34

00 38250

Production Scheduling 105 Production 55 191 50 9545 50 95455

4

Answer to Question-2

Particulars

Basic

Mode

l

Adva

nce

Mode

l

Units Produced and sold 1600 1500

Direct Material cost per

unit 325 425

Direct Labour cost per

unit 150 250

Total 2075 2175

Indirect Overheads Cost

Estimated

cost Driver

Activity

Over

head

Rate

Alloc

ation

of

overh

ead

costs

Over

head

Rate

Alloc

ation

of

overh

ead

costs

Inspection (hours)

200

00 Inspection

95

0 21 200 4211

75

0 15789

Assembly (direct

machine hours)

900

00 Assembly

80

00 11 4600

5175

0

34

00 38250

Production Scheduling 105 Production 55 191 50 9545 50 95455

COSTING ANALYSIS

5

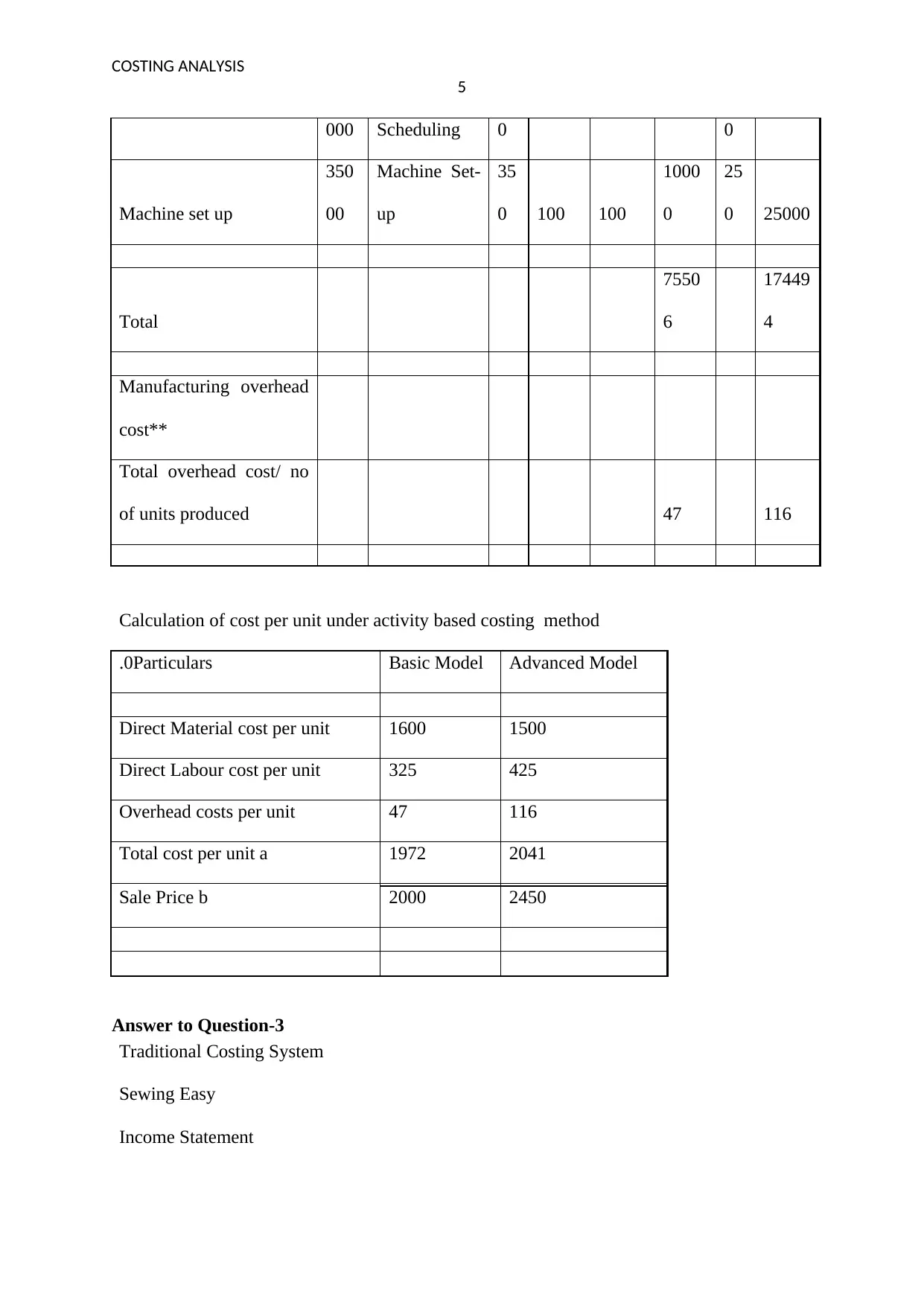

000 Scheduling 0 0

Machine set up

350

00

Machine Set-

up

35

0 100 100

1000

0

25

0 25000

Total

7550

6

17449

4

Manufacturing overhead

cost**

Total overhead cost/ no

of units produced 47 116

Calculation of cost per unit under activity based costing method

.0Particulars Basic Model Advanced Model

Direct Material cost per unit 1600 1500

Direct Labour cost per unit 325 425

Overhead costs per unit 47 116

Total cost per unit a 1972 2041

Sale Price b 2000 2450

Answer to Question-3

Traditional Costing System

Sewing Easy

Income Statement

5

000 Scheduling 0 0

Machine set up

350

00

Machine Set-

up

35

0 100 100

1000

0

25

0 25000

Total

7550

6

17449

4

Manufacturing overhead

cost**

Total overhead cost/ no

of units produced 47 116

Calculation of cost per unit under activity based costing method

.0Particulars Basic Model Advanced Model

Direct Material cost per unit 1600 1500

Direct Labour cost per unit 325 425

Overhead costs per unit 47 116

Total cost per unit a 1972 2041

Sale Price b 2000 2450

Answer to Question-3

Traditional Costing System

Sewing Easy

Income Statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

6

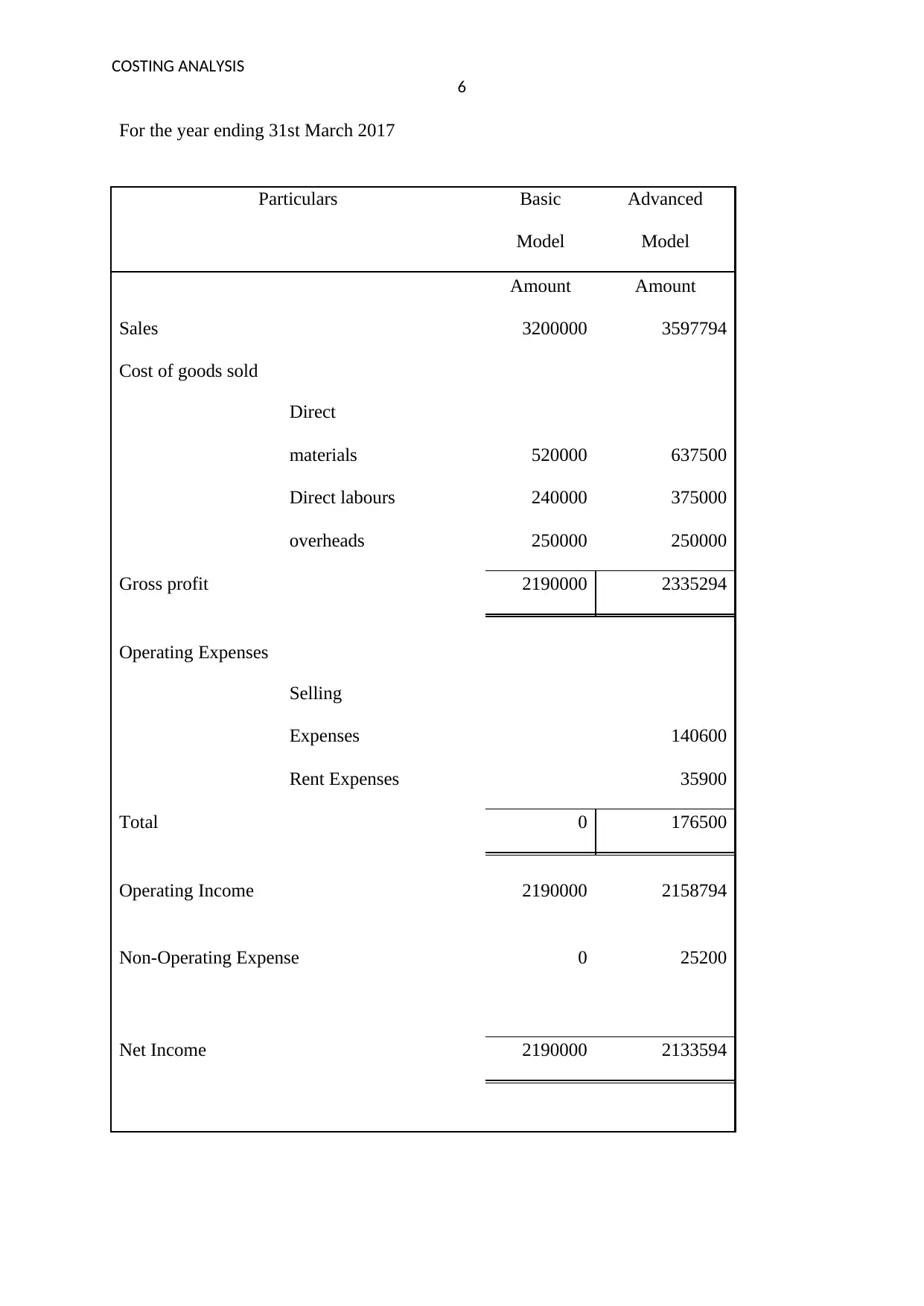

For the year ending 31st March 2017

Particulars Basic

Model

Advanced

Model

Amount Amount

Sales 3200000 3597794

Cost of goods sold

Direct

materials 520000 637500

Direct labours 240000 375000

overheads 250000 250000

Gross profit 2190000 2335294

Operating Expenses

Selling

Expenses 140600

Rent Expenses 35900

Total 0 176500

Operating Income 2190000 2158794

Non-Operating Expense 0 25200

Net Income 2190000 2133594

6

For the year ending 31st March 2017

Particulars Basic

Model

Advanced

Model

Amount Amount

Sales 3200000 3597794

Cost of goods sold

Direct

materials 520000 637500

Direct labours 240000 375000

overheads 250000 250000

Gross profit 2190000 2335294

Operating Expenses

Selling

Expenses 140600

Rent Expenses 35900

Total 0 176500

Operating Income 2190000 2158794

Non-Operating Expense 0 25200

Net Income 2190000 2133594

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

7

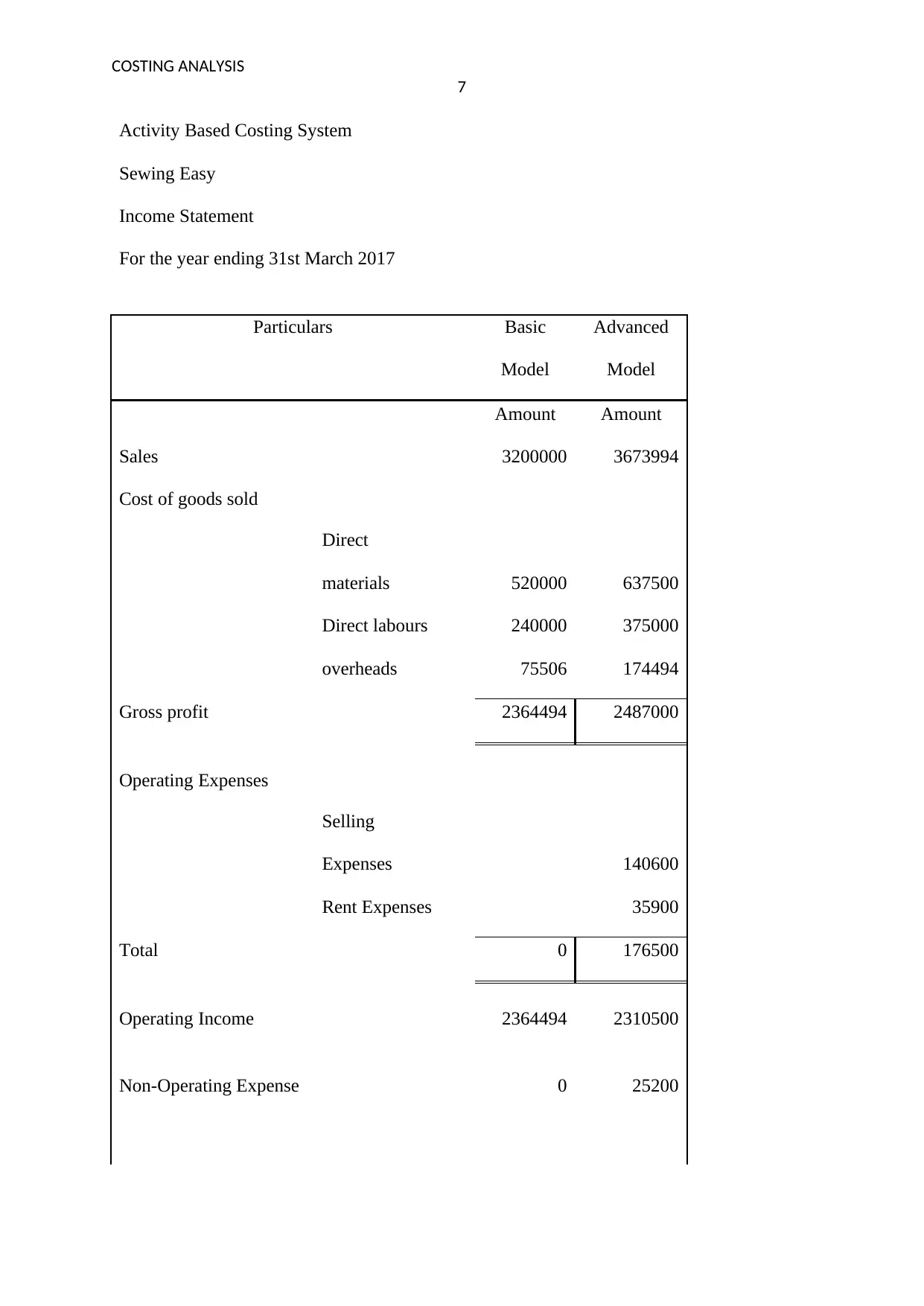

Activity Based Costing System

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Basic

Model

Advanced

Model

Amount Amount

Sales 3200000 3673994

Cost of goods sold

Direct

materials 520000 637500

Direct labours 240000 375000

overheads 75506 174494

Gross profit 2364494 2487000

Operating Expenses

Selling

Expenses 140600

Rent Expenses 35900

Total 0 176500

Operating Income 2364494 2310500

Non-Operating Expense 0 25200

7

Activity Based Costing System

Sewing Easy

Income Statement

For the year ending 31st March 2017

Particulars Basic

Model

Advanced

Model

Amount Amount

Sales 3200000 3673994

Cost of goods sold

Direct

materials 520000 637500

Direct labours 240000 375000

overheads 75506 174494

Gross profit 2364494 2487000

Operating Expenses

Selling

Expenses 140600

Rent Expenses 35900

Total 0 176500

Operating Income 2364494 2310500

Non-Operating Expense 0 25200

COSTING ANALYSIS

8

Net Income 2364494 2285300

Analysis

After analysing the calculations made above the overseas buyer, want to purchase the

advance model because of the fact that under the activity costing model, the cost of overheads

reduced by approximately $100000. Because of reduction in overhead costs the net income

increased by $151706 and in total amounts to $2285300. Under the traditional system the

cost of overheads are allocated on the basis of overall costs, whereas in the activity based

costing model the costs are allocated using the cost drivers (Manunen, 2013) Henceforth, the

overseas buyer wants to buy the advanced model under the activity based costing system.

Importance of accurate product costing

The importance of accurate product costing can be crucial for both the financial statements

and tax filings. It is also important to have an accurate product costing to provide the external

users of the financial statements with the relevant information about the net worth and the

earnings of the company to provide the internal managers with the particular information

which they need for the purpose of decision making (Patiar, 2016). Therefore, if the

inventory cost of the company which is used for the reporting of the financial statements is

accurate. It is generally and inadequate basis and it is not the reliable method to check the

profitability of the products. Hence the overall accurate product costing is necessary

(Kannaiah, 2015). This measures the gross margin, and helps in valuation of assets and

making optimal choices. It is also important because it helps in evaluating and planning the

strategies for the survival of the business. This is ultimately because without a good and

accurate product costing, a business operates in grey areas (Freiesleben, 2014).

8

Net Income 2364494 2285300

Analysis

After analysing the calculations made above the overseas buyer, want to purchase the

advance model because of the fact that under the activity costing model, the cost of overheads

reduced by approximately $100000. Because of reduction in overhead costs the net income

increased by $151706 and in total amounts to $2285300. Under the traditional system the

cost of overheads are allocated on the basis of overall costs, whereas in the activity based

costing model the costs are allocated using the cost drivers (Manunen, 2013) Henceforth, the

overseas buyer wants to buy the advanced model under the activity based costing system.

Importance of accurate product costing

The importance of accurate product costing can be crucial for both the financial statements

and tax filings. It is also important to have an accurate product costing to provide the external

users of the financial statements with the relevant information about the net worth and the

earnings of the company to provide the internal managers with the particular information

which they need for the purpose of decision making (Patiar, 2016). Therefore, if the

inventory cost of the company which is used for the reporting of the financial statements is

accurate. It is generally and inadequate basis and it is not the reliable method to check the

profitability of the products. Hence the overall accurate product costing is necessary

(Kannaiah, 2015). This measures the gross margin, and helps in valuation of assets and

making optimal choices. It is also important because it helps in evaluating and planning the

strategies for the survival of the business. This is ultimately because without a good and

accurate product costing, a business operates in grey areas (Freiesleben, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COSTING ANALYSIS

9

Answer to Question 4

The primary difference between the applied and the actual overhead is that the former one is

arrived during and after a certain period of time while the later one is arrived before a certain

period of time. In terms of accounting overheads generally refers to the manufacturing costs

which are of indirect nature. These are those manufacturing costs which are other than the

direct materials and direct labours. The actual overheads can be derived from the

manufacturing costs that actually occur and a record of the same can be kept (Tsai, 2016).

These also include the costs of electricity, water, rent, property tax, depreciation,

maintenance.

A company generally do not incur the costs of overheads uniformly. For example the cost of

heat during the winter is generally high as compared to summers. However, when the

discussion is regarding the allocation of the costs this purpose is not served fully. They are

useful for the purpose of the inventory and also in determining the profitability of the

business.

The applied overhead refers to the manufacturing costs of the indirect nature that have been

allocated to the manufactured goods. Manufactured overheads are generally allocated on the

basis of the annual over rate (Gracanin, Buchmeister and Lalic, 2014).

If too much of overhead is applied to the jobs the overhead is considered as over applied

whereas if the overhead costs are applied little, it is called as under applied. An over applied

overhead cost occurs when the cost of goods sold are inclusive of too much of overhead and

vice versa in the case of under applied overhead. An account called “Factory overhead” is

created and credited to reflect the application in the work in progress method.

How to deal with over/undervalued applied overhead.

First the amount may be carried forward to the next period’s account.

9

Answer to Question 4

The primary difference between the applied and the actual overhead is that the former one is

arrived during and after a certain period of time while the later one is arrived before a certain

period of time. In terms of accounting overheads generally refers to the manufacturing costs

which are of indirect nature. These are those manufacturing costs which are other than the

direct materials and direct labours. The actual overheads can be derived from the

manufacturing costs that actually occur and a record of the same can be kept (Tsai, 2016).

These also include the costs of electricity, water, rent, property tax, depreciation,

maintenance.

A company generally do not incur the costs of overheads uniformly. For example the cost of

heat during the winter is generally high as compared to summers. However, when the

discussion is regarding the allocation of the costs this purpose is not served fully. They are

useful for the purpose of the inventory and also in determining the profitability of the

business.

The applied overhead refers to the manufacturing costs of the indirect nature that have been

allocated to the manufactured goods. Manufactured overheads are generally allocated on the

basis of the annual over rate (Gracanin, Buchmeister and Lalic, 2014).

If too much of overhead is applied to the jobs the overhead is considered as over applied

whereas if the overhead costs are applied little, it is called as under applied. An over applied

overhead cost occurs when the cost of goods sold are inclusive of too much of overhead and

vice versa in the case of under applied overhead. An account called “Factory overhead” is

created and credited to reflect the application in the work in progress method.

How to deal with over/undervalued applied overhead.

First the amount may be carried forward to the next period’s account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COSTING ANALYSIS

10

The amount may be written off to the profit and loss account.

A supplementary rate may be evaluated and applied.

Answer to Question 5

Advantages

One of the basic advantages of the ABC model is it provides relevant information thereby

reducing the cost. The information regarding cost is provided by ABC is generally considered

more relevant in comparison to the conventional method. Due to the relevant information the

managers are able to control many costs of fixed nature and the decisions can be made

quickly (Mersy, et al 2015). This happens because in the conventional method the costs are

not visible clearly whereas under this method the costs are transparent in nature.

Activity based costing system works only on the activities. Therefore, it will become easy for

the management of the Sewing Easy to decide quickly without comprising on the quality

front on each activity carefully. ABC is also helpful in fixation of the selling prices as more

accurate data is available and a better understanding is developed. Due to this factor the

decision making process has become quite easy and sustainable. This helps in improvement

of processes and managers keep on focusing on revamping the efficiency and effectiveness

(Plunkett and Dale, 2018).

The cost of allocation if done accurately, leads to proper pricing policy. Therefore with the

help of proper pricing policy the company can maintain the additional products which may

also lead to profits. It has been recognized that the costs are created by activities more than

the products. In an environment where the advanced manufacturing takes place and the

support functions are forming the major portion of the cost ABC model of Sewing Easy can

provide more realistic costs (Innes and Mitchell, 2015).

10

The amount may be written off to the profit and loss account.

A supplementary rate may be evaluated and applied.

Answer to Question 5

Advantages

One of the basic advantages of the ABC model is it provides relevant information thereby

reducing the cost. The information regarding cost is provided by ABC is generally considered

more relevant in comparison to the conventional method. Due to the relevant information the

managers are able to control many costs of fixed nature and the decisions can be made

quickly (Mersy, et al 2015). This happens because in the conventional method the costs are

not visible clearly whereas under this method the costs are transparent in nature.

Activity based costing system works only on the activities. Therefore, it will become easy for

the management of the Sewing Easy to decide quickly without comprising on the quality

front on each activity carefully. ABC is also helpful in fixation of the selling prices as more

accurate data is available and a better understanding is developed. Due to this factor the

decision making process has become quite easy and sustainable. This helps in improvement

of processes and managers keep on focusing on revamping the efficiency and effectiveness

(Plunkett and Dale, 2018).

The cost of allocation if done accurately, leads to proper pricing policy. Therefore with the

help of proper pricing policy the company can maintain the additional products which may

also lead to profits. It has been recognized that the costs are created by activities more than

the products. In an environment where the advanced manufacturing takes place and the

support functions are forming the major portion of the cost ABC model of Sewing Easy can

provide more realistic costs (Innes and Mitchell, 2015).

COSTING ANALYSIS

11

Further, the activities can be segregated into the activities which create some value and

activities which do not add possess any kind of worth. The ABC model in general will help

the Sewing Easy Model to focus on the worthy activities which can generate profits and can

save time, energy and resources of the organisation (Saghafifar and Poullikkas, 2017).

There are some costs which are categorised as non-manufacturing costs for example

advertising. Even though the advertising cost does not form the part of the major cost yet

contributes majorly in the business of Sewing Easy. With the help of the advertising the

company can reach at altogether new level. It can attract more number of customers

automatically.

Disadvantages

One of the biggest disadvantages is the complex mechanism that needs skill and ability

implements the same model practically. ABC requires proper management system which can

easily evaluate the costs of the activity pools and can readily identify the best possible

measure to act as a driver for the purpose of the allocation (Pitel and Alioshkina, 2016)

Under the system of ABC the number are produced such as product margin which are totally

odd in terms of the number produced by the conventional system of costing. Yet the

managers were habitual of using the current costing system to run their business operations

which is often sued for the purpose of evaluation.

The data of the activity based costing model can be easily mislead and misinterpreted and

shall be used with utmost care when using for the purposes of decision making. The

relevancy of the costs which are assigned to the products, customers and other cost objects

are not that potential ion nature. Before making any decision it is the duty of the manager to

analyse the most important and non-important costs.

11

Further, the activities can be segregated into the activities which create some value and

activities which do not add possess any kind of worth. The ABC model in general will help

the Sewing Easy Model to focus on the worthy activities which can generate profits and can

save time, energy and resources of the organisation (Saghafifar and Poullikkas, 2017).

There are some costs which are categorised as non-manufacturing costs for example

advertising. Even though the advertising cost does not form the part of the major cost yet

contributes majorly in the business of Sewing Easy. With the help of the advertising the

company can reach at altogether new level. It can attract more number of customers

automatically.

Disadvantages

One of the biggest disadvantages is the complex mechanism that needs skill and ability

implements the same model practically. ABC requires proper management system which can

easily evaluate the costs of the activity pools and can readily identify the best possible

measure to act as a driver for the purpose of the allocation (Pitel and Alioshkina, 2016)

Under the system of ABC the number are produced such as product margin which are totally

odd in terms of the number produced by the conventional system of costing. Yet the

managers were habitual of using the current costing system to run their business operations

which is often sued for the purpose of evaluation.

The data of the activity based costing model can be easily mislead and misinterpreted and

shall be used with utmost care when using for the purposes of decision making. The

relevancy of the costs which are assigned to the products, customers and other cost objects

are not that potential ion nature. Before making any decision it is the duty of the manager to

analyse the most important and non-important costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.