Report on Costing Techniques: Variance Analysis for Anderson Ltd

VerifiedAdded on 2020/02/12

|8

|2001

|82

Report

AI Summary

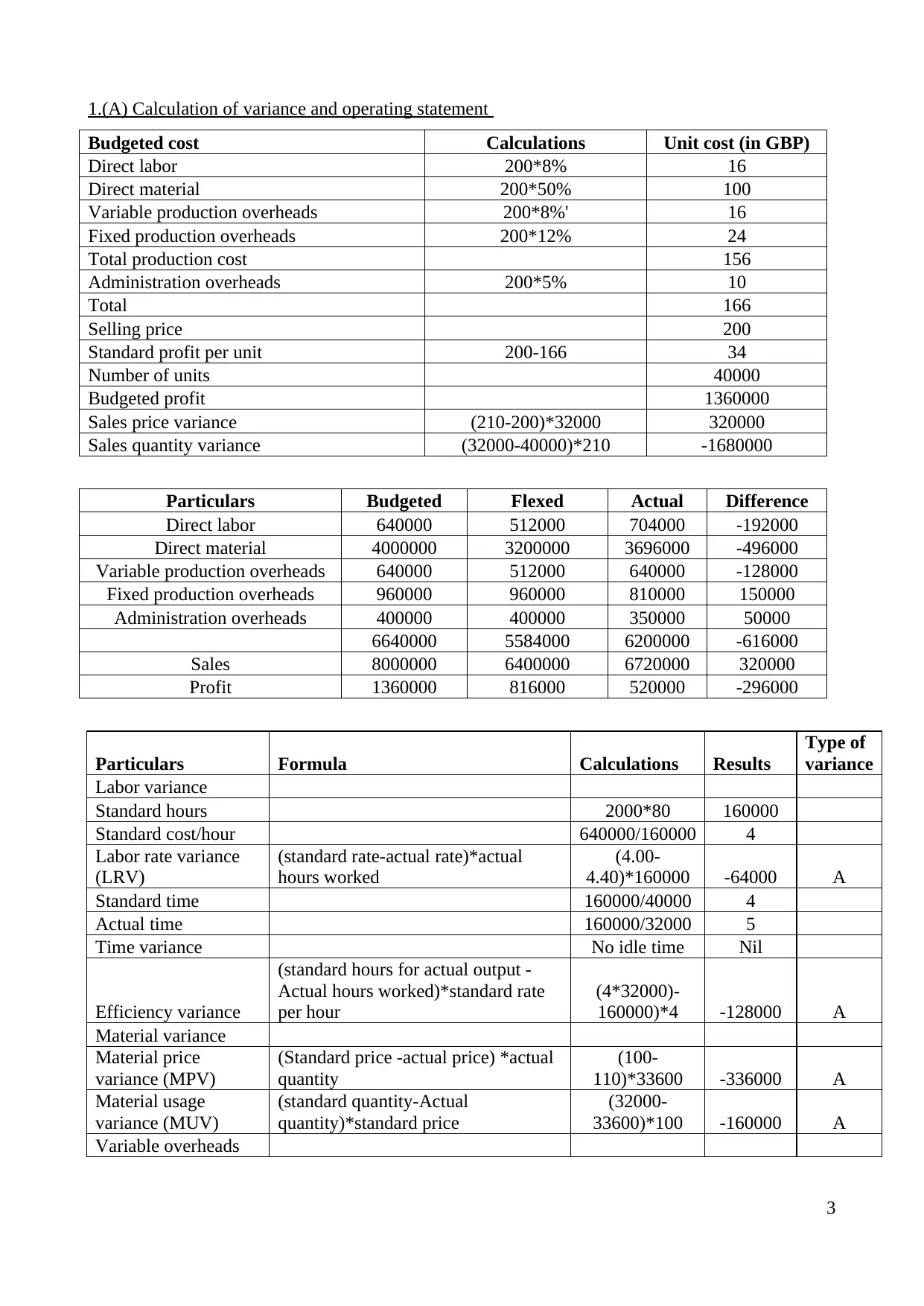

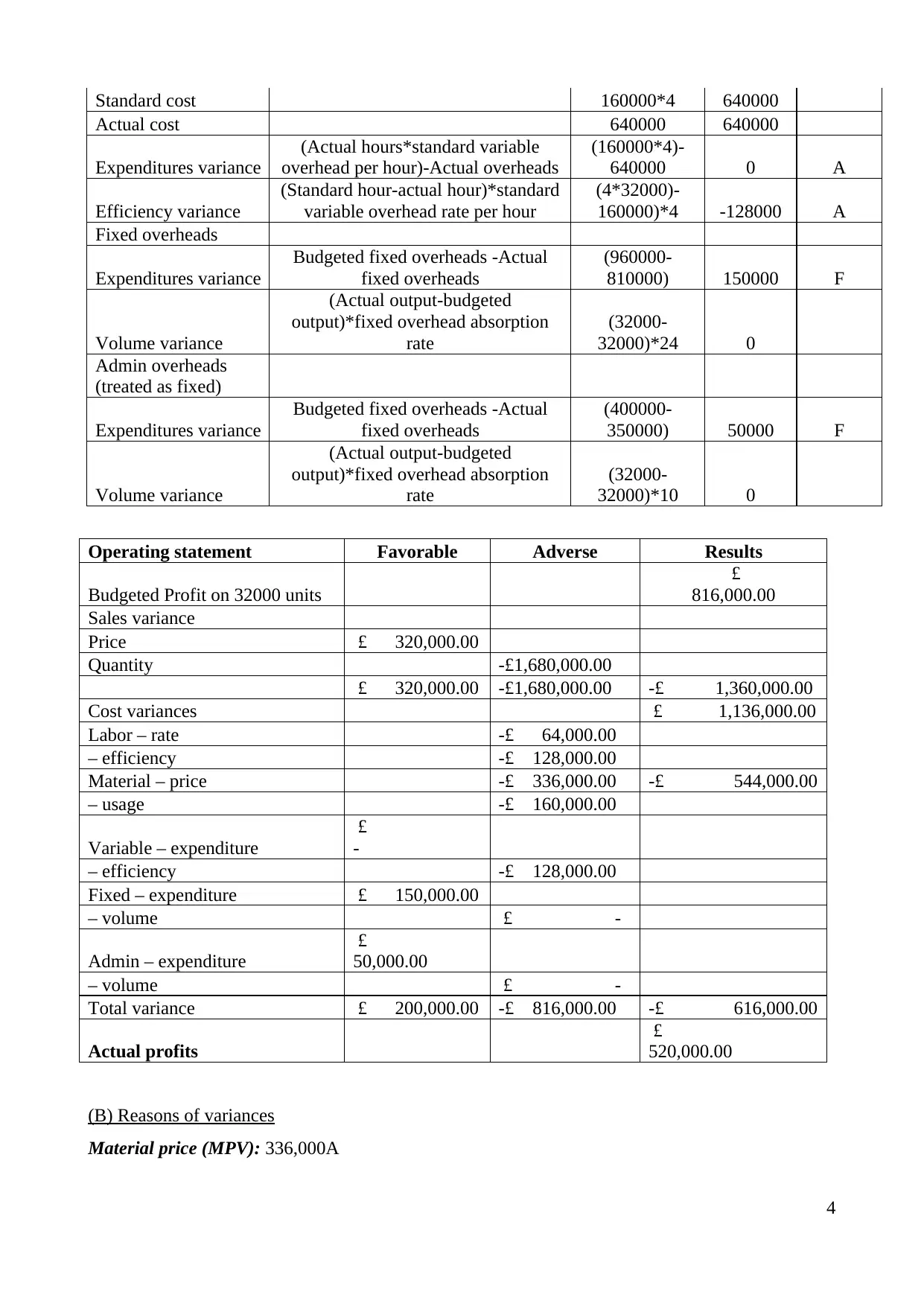

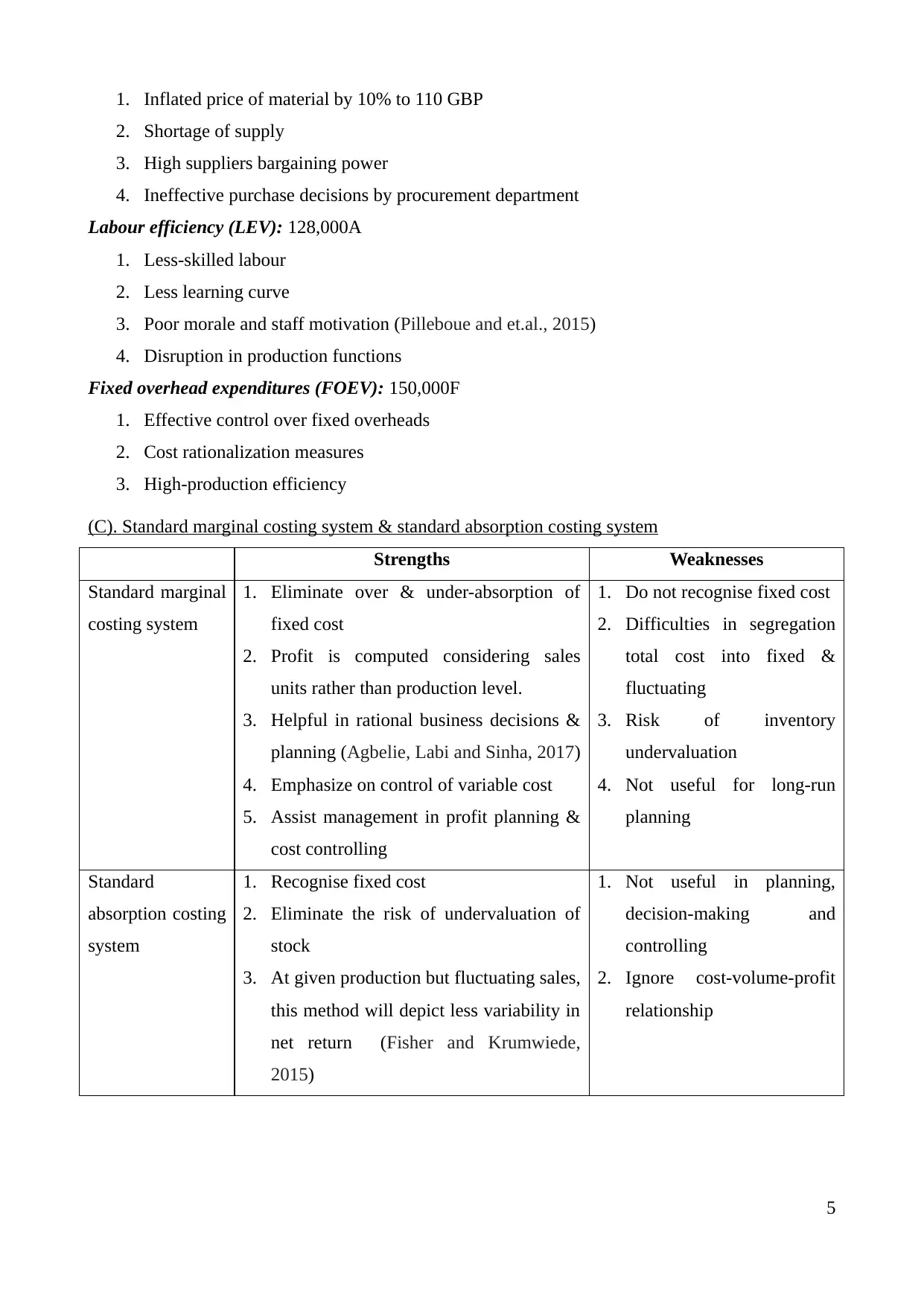

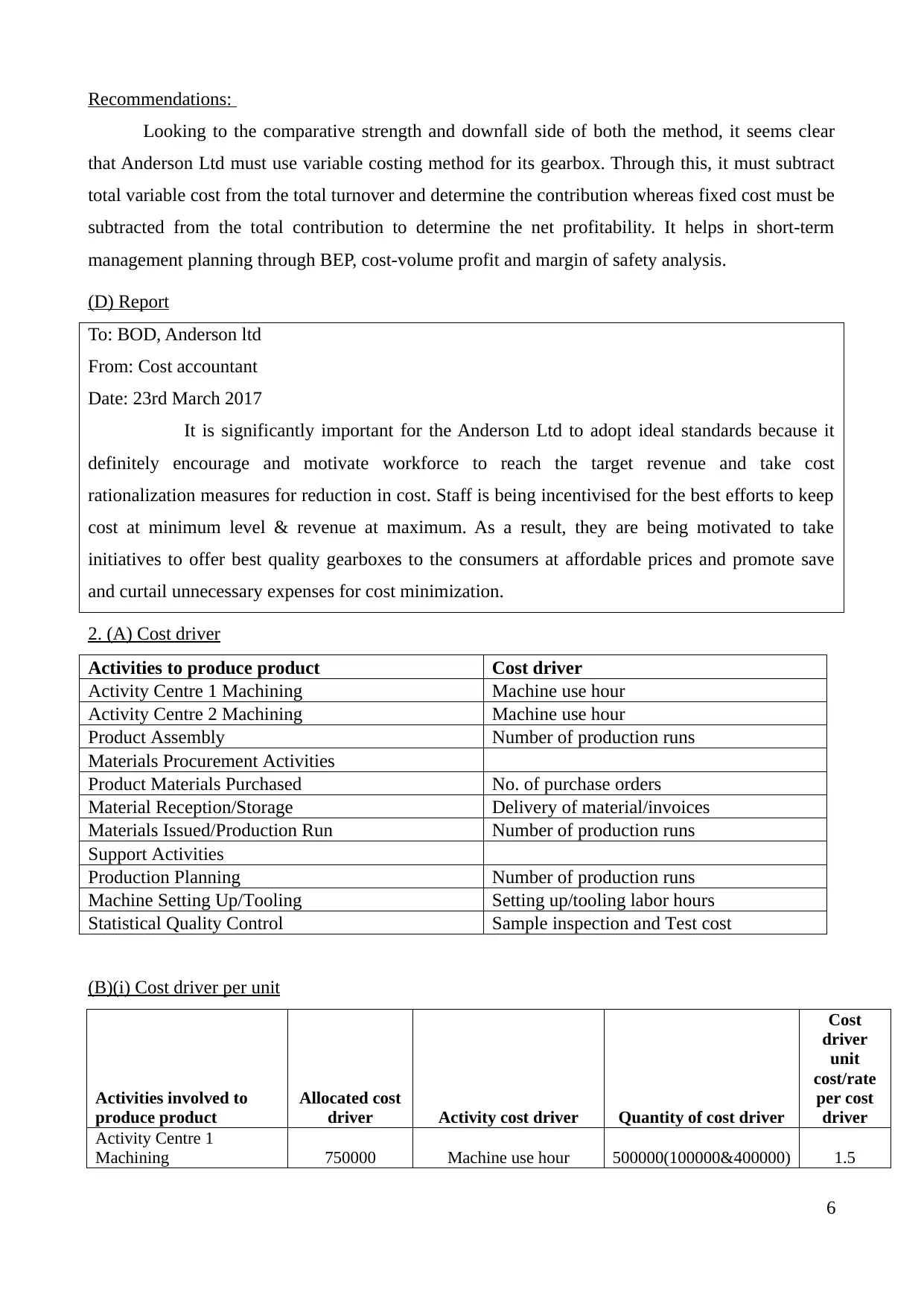

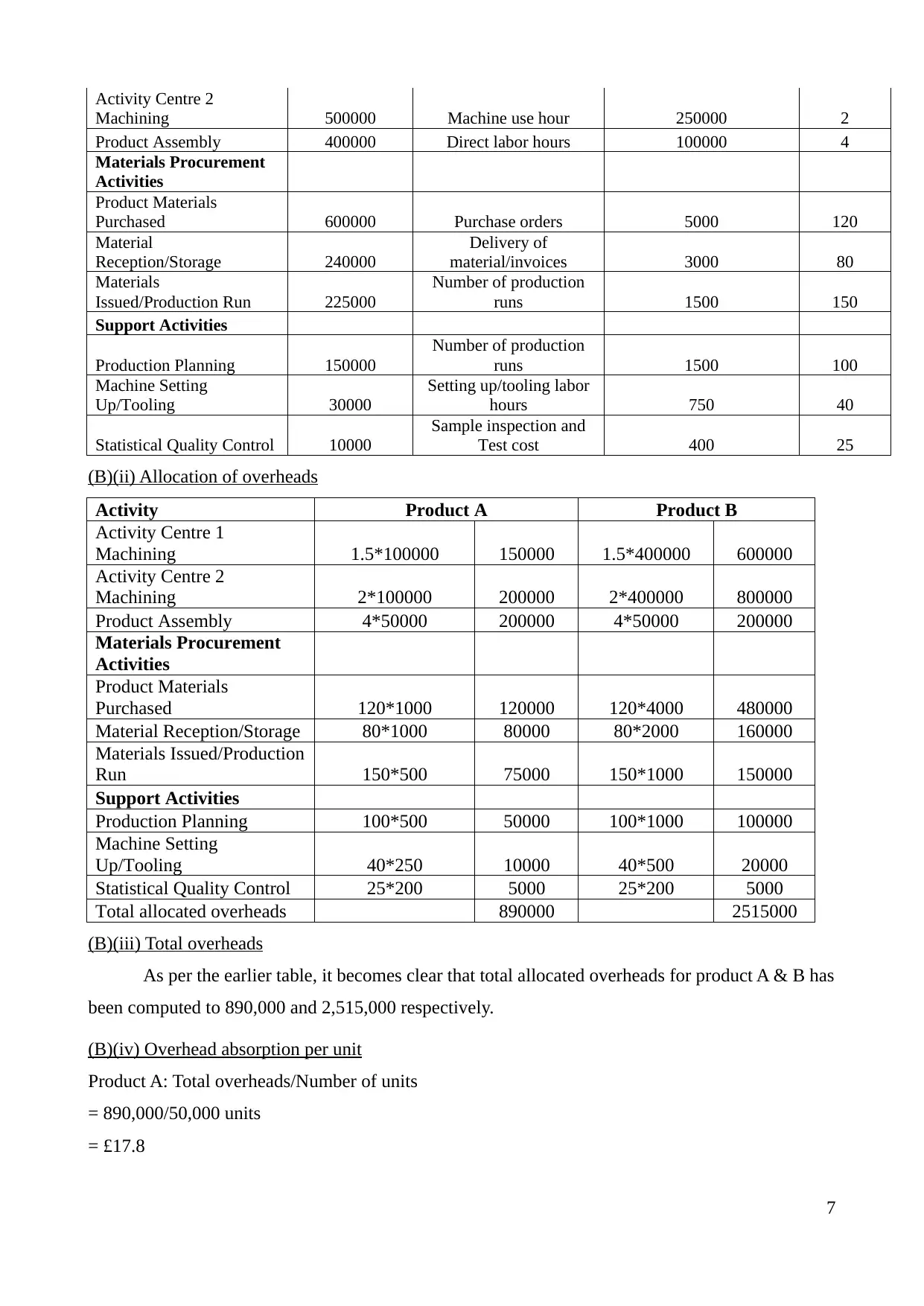

This report provides a detailed analysis of costing techniques, focusing on variance analysis and its application within Anderson Ltd. The report begins with the calculation of variances and the preparation of an operating statement, examining direct labor, direct materials, and overhead costs. It then delves into the reasons behind the variances, identifying factors such as material price inflation, labor efficiency issues, and overhead expenditure control. A comparative analysis of standard marginal costing and standard absorption costing systems is presented, leading to recommendations for Anderson Ltd. The report further explores cost drivers, including machine use hours, direct labor hours, and purchase orders, and calculates cost driver per unit. It then allocates overheads based on these cost drivers and determines overhead absorption rates for products A and B. The report concludes with a report to the Board of Directors summarizing the findings and recommendations, emphasizing the importance of adopting ideal standards to encourage cost rationalization and motivate the workforce. This report aims to provide a comprehensive understanding of costing techniques and their practical application in a business context.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.