Managerial Accounting: Costing Methods, Break-Even & Margin Analysis

VerifiedAdded on 2023/04/05

|25

|4535

|301

Report

AI Summary

This report provides a detailed analysis of managerial accounting concepts, focusing on costing methods and break-even analysis. It begins by comparing plant-wide overhead allocation with activity-based costing (ABC), highlighting the advantages of ABC in accurately allocating indirect costs. The report then delves into break-even analysis, calculating break-even points in units and sales revenue, and determining the margin of safety. A sensitivity analysis is performed to evaluate the impact of increased advertising expenses on sales and profitability. Furthermore, the report assesses the relevant and irrelevant costs associated with expanding business operations, providing a framework for informed decision-making. The analysis includes calculations and explanations to guide understanding of these essential managerial accounting techniques.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGERIAL ACCOUNTING

Table of Contents

Question No 1..................................................................................................................................3

Requirement 1a............................................................................................................................3

Requirement 1b............................................................................................................................4

Requirement 1c............................................................................................................................6

Question No 2..................................................................................................................................7

Requirement 2a............................................................................................................................7

Requirement 2a............................................................................................................................8

Requirement 2c............................................................................................................................9

Requirement 2d............................................................................................................................9

Requirement 2e..........................................................................................................................10

Question 3:.....................................................................................................................................12

Part A:........................................................................................................................................12

Requirement a:.......................................................................................................................13

Requirement b:.......................................................................................................................14

Part B:........................................................................................................................................15

Question 4:.....................................................................................................................................15

Requirement a:...........................................................................................................................15

Requirement b:...........................................................................................................................16

Question 5:.....................................................................................................................................19

MANAGERIAL ACCOUNTING

Table of Contents

Question No 1..................................................................................................................................3

Requirement 1a............................................................................................................................3

Requirement 1b............................................................................................................................4

Requirement 1c............................................................................................................................6

Question No 2..................................................................................................................................7

Requirement 2a............................................................................................................................7

Requirement 2a............................................................................................................................8

Requirement 2c............................................................................................................................9

Requirement 2d............................................................................................................................9

Requirement 2e..........................................................................................................................10

Question 3:.....................................................................................................................................12

Part A:........................................................................................................................................12

Requirement a:.......................................................................................................................13

Requirement b:.......................................................................................................................14

Part B:........................................................................................................................................15

Question 4:.....................................................................................................................................15

Requirement a:...........................................................................................................................15

Requirement b:...........................................................................................................................16

Question 5:.....................................................................................................................................19

2

MANAGERIAL ACCOUNTING

Requirement a:...........................................................................................................................19

Part (i):...................................................................................................................................19

Part (ii):..................................................................................................................................19

Requirement b:...........................................................................................................................20

Requirement c:...........................................................................................................................21

References:....................................................................................................................................23

MANAGERIAL ACCOUNTING

Requirement a:...........................................................................................................................19

Part (i):...................................................................................................................................19

Part (ii):..................................................................................................................................19

Requirement b:...........................................................................................................................20

Requirement c:...........................................................................................................................21

References:....................................................................................................................................23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGERIAL ACCOUNTING

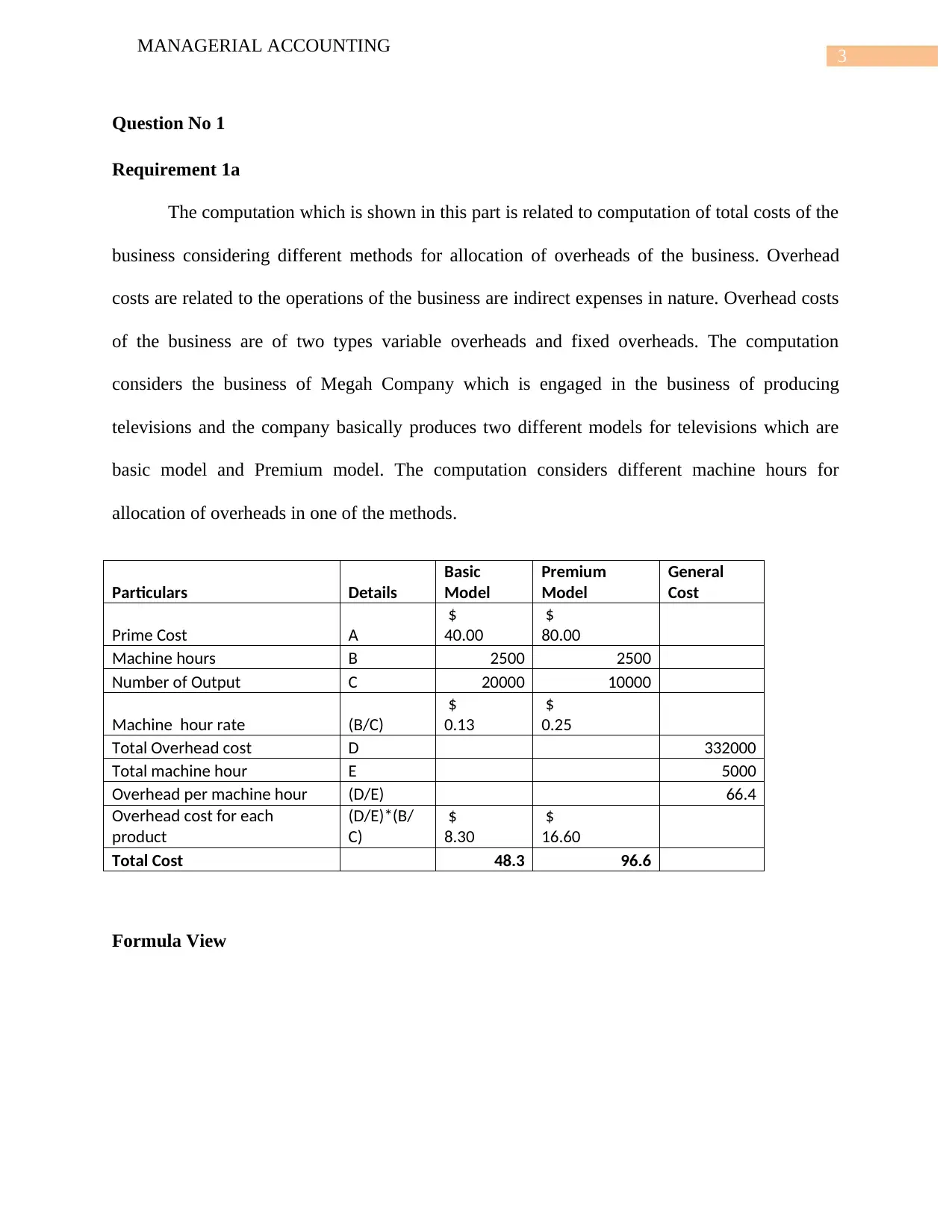

Question No 1

Requirement 1a

The computation which is shown in this part is related to computation of total costs of the

business considering different methods for allocation of overheads of the business. Overhead

costs are related to the operations of the business are indirect expenses in nature. Overhead costs

of the business are of two types variable overheads and fixed overheads. The computation

considers the business of Megah Company which is engaged in the business of producing

televisions and the company basically produces two different models for televisions which are

basic model and Premium model. The computation considers different machine hours for

allocation of overheads in one of the methods.

Particulars Details

Basic

Model

Premium

Model

General

Cost

Prime Cost A

$

40.00

$

80.00

Machine hours B 2500 2500

Number of Output C 20000 10000

Machine hour rate (B/C)

$

0.13

$

0.25

Total Overhead cost D 332000

Total machine hour E 5000

Overhead per machine hour (D/E) 66.4

Overhead cost for each

product

(D/E)*(B/

C)

$

8.30

$

16.60

Total Cost 48.3 96.6

Formula View

MANAGERIAL ACCOUNTING

Question No 1

Requirement 1a

The computation which is shown in this part is related to computation of total costs of the

business considering different methods for allocation of overheads of the business. Overhead

costs are related to the operations of the business are indirect expenses in nature. Overhead costs

of the business are of two types variable overheads and fixed overheads. The computation

considers the business of Megah Company which is engaged in the business of producing

televisions and the company basically produces two different models for televisions which are

basic model and Premium model. The computation considers different machine hours for

allocation of overheads in one of the methods.

Particulars Details

Basic

Model

Premium

Model

General

Cost

Prime Cost A

$

40.00

$

80.00

Machine hours B 2500 2500

Number of Output C 20000 10000

Machine hour rate (B/C)

$

0.13

$

0.25

Total Overhead cost D 332000

Total machine hour E 5000

Overhead per machine hour (D/E) 66.4

Overhead cost for each

product

(D/E)*(B/

C)

$

8.30

$

16.60

Total Cost 48.3 96.6

Formula View

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGERIAL ACCOUNTING

It can be seen from the above calculation that company cost for its product are different.

The total cost of the product has been determined by adding prime cost and overhead cost. The

overhead cost is calculated by total productive machine hours. The overhead costs which is

computed has an important part in computing the totals costs of the business and also deciding

how much profits can be generated by the business.

Requirement 1b

The calculation of unit cost of each model with the help of four activity driver

Activity Cost Driver

Estimated

Overhead Cost

Estimated Cost Driver

Activity

Predetermined Cost

Overhead

Purchasing

Material

Purchase

Requisitions 87000 2000 43.5

Maintaining

Equipment

Maintaince

Hour 220000 8000 27.5

Setting up

Equipment Set up time 112000 40 2800

Below we can see the total cost of the product under activity based costing

Particular Details

Basic

Model

Premium

Model General

Prime Cost A

$

40.00

$

80.00

Number of Requisitions B 500 1500

Maintaince Hour C 2000 6000

Set up time D 8 32

Overhead on Maintance E 27.5

Overhead on Purchase F 43.5

MANAGERIAL ACCOUNTING

It can be seen from the above calculation that company cost for its product are different.

The total cost of the product has been determined by adding prime cost and overhead cost. The

overhead cost is calculated by total productive machine hours. The overhead costs which is

computed has an important part in computing the totals costs of the business and also deciding

how much profits can be generated by the business.

Requirement 1b

The calculation of unit cost of each model with the help of four activity driver

Activity Cost Driver

Estimated

Overhead Cost

Estimated Cost Driver

Activity

Predetermined Cost

Overhead

Purchasing

Material

Purchase

Requisitions 87000 2000 43.5

Maintaining

Equipment

Maintaince

Hour 220000 8000 27.5

Setting up

Equipment Set up time 112000 40 2800

Below we can see the total cost of the product under activity based costing

Particular Details

Basic

Model

Premium

Model General

Prime Cost A

$

40.00

$

80.00

Number of Requisitions B 500 1500

Maintaince Hour C 2000 6000

Set up time D 8 32

Overhead on Maintance E 27.5

Overhead on Purchase F 43.5

5

MANAGERIAL ACCOUNTING

Overhead on Set up G 2800

overhead chareged for all product H

$

99,150.00

$

3,19,850.00

Number of unit produced I 20000 10000

Overhead per product (H/I) 4.9575 31.985

Total cost

$

44.96

$

111.99

Formula View

Activity based costing refers to the costing which allocate the overhead as per the activity

perform. It sees the relation of the overhead, the cost and the manufacturing and through the

relationship it allocates the overhead cost. Activity based costing is considered to be one of the

most useful techniques for the purpose of identifying and accurately allocating the costs of the

business to the products. The costing technique is used in major businesses for computing anf

allocating costs of the business. As there some expenses which are of high costly nature so this

help the organization about the level of increasing the cost of the product. As there are many

costs which cannot be allocated through cost accounting method so to remove the barrier these

costs came into the picture.

MANAGERIAL ACCOUNTING

Overhead on Set up G 2800

overhead chareged for all product H

$

99,150.00

$

3,19,850.00

Number of unit produced I 20000 10000

Overhead per product (H/I) 4.9575 31.985

Total cost

$

44.96

$

111.99

Formula View

Activity based costing refers to the costing which allocate the overhead as per the activity

perform. It sees the relation of the overhead, the cost and the manufacturing and through the

relationship it allocates the overhead cost. Activity based costing is considered to be one of the

most useful techniques for the purpose of identifying and accurately allocating the costs of the

business to the products. The costing technique is used in major businesses for computing anf

allocating costs of the business. As there some expenses which are of high costly nature so this

help the organization about the level of increasing the cost of the product. As there are many

costs which cannot be allocated through cost accounting method so to remove the barrier these

costs came into the picture.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGERIAL ACCOUNTING

Requirement 1c

Costing is a process which help the company to evaluate the cost of its business and help

them to get an overview of the market. Each company follow the different method of costing.

The process of computing the costs of the business is considered to be very important as they

have direct impact on the revenue and profits which is generated by the business. In addition to

this, the costs of the business also have an important role in determination of the price for the

products which is offered by the business. There are different costing techniques which are

available to the management of the company for computing total costs of the business and also

allocation of the indirect costs of the business. In the above it has been seen that company has

used two different method of costing one is Plant Wide Rate and another one is Activity Based

Costing.

Plant wide rate –It is the rate which assign all the company manufacturing overhead cost

to its production cost. It is a simple concept as it allocates at one rate so the costing of the

overhead become very easy and no complex method is used. The method is followed by

businesses as the method does not involve any complexities and it is much easier to

understand while conducting a review of the system.

Activity based costing – Under this method the cost is allocate as per the activity. It is

done for different overhead different rates are being used. The allocation of indirect costs

of the business are done on the basis of the activities which are carried out by the

business. This is considered to be the most popular and effective method for allocation

and computation of costs of the business and in most of the situation, the method is

known to provide the most accurate estimates.

MANAGERIAL ACCOUNTING

Requirement 1c

Costing is a process which help the company to evaluate the cost of its business and help

them to get an overview of the market. Each company follow the different method of costing.

The process of computing the costs of the business is considered to be very important as they

have direct impact on the revenue and profits which is generated by the business. In addition to

this, the costs of the business also have an important role in determination of the price for the

products which is offered by the business. There are different costing techniques which are

available to the management of the company for computing total costs of the business and also

allocation of the indirect costs of the business. In the above it has been seen that company has

used two different method of costing one is Plant Wide Rate and another one is Activity Based

Costing.

Plant wide rate –It is the rate which assign all the company manufacturing overhead cost

to its production cost. It is a simple concept as it allocates at one rate so the costing of the

overhead become very easy and no complex method is used. The method is followed by

businesses as the method does not involve any complexities and it is much easier to

understand while conducting a review of the system.

Activity based costing – Under this method the cost is allocate as per the activity. It is

done for different overhead different rates are being used. The allocation of indirect costs

of the business are done on the basis of the activities which are carried out by the

business. This is considered to be the most popular and effective method for allocation

and computation of costs of the business and in most of the situation, the method is

known to provide the most accurate estimates.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGERIAL ACCOUNTING

Activity based costing is better method than plant wide method as in activity costing the

overhead are allocated as per the activity so it helps the organization to know how the product

price is rising. The main advantage of activity-based costing is that it gives an accurate

estimation of costs and appropriate allocation of overhead costs on the basis of activities which is

carried out by businesses. Therefore, it can be clearly indicated that if the business follows

activity-based costing techniques than it would give a better presentation of the total cost and

also assist in the determination of prices for the business.

Question No 2

Requirement 2a

Break even analysis is a widely used technique by management accountants and

production manager. It is based on the production costs which are divided into two parts one is

variable cost which varies with the production unit and another one is fixed cost which remain

same in respect of production unit. Both cost is combined than it is compared with sales revenue

to get the position where by selling certain amount of goods company is earning neither profit

nor loss and that point is termed as break-even point.

In other words, breakeven analysis is very useful tool for taking vital decisions of the

business. The breakeven analysis tells the management the required units or revenue which the

management of the company needs to generate in order to at least cover the costs of the business

and reach a no profit no loss situation. On the basis of breakeven analysis, the management of

the company decide what prices are to be set for the products and what quantity of products the

management needs to sell in order to reach a no profit no loss situation. In addition to this,

breakeven point needs to be achieved by the business in order to ensure that the business

MANAGERIAL ACCOUNTING

Activity based costing is better method than plant wide method as in activity costing the

overhead are allocated as per the activity so it helps the organization to know how the product

price is rising. The main advantage of activity-based costing is that it gives an accurate

estimation of costs and appropriate allocation of overhead costs on the basis of activities which is

carried out by businesses. Therefore, it can be clearly indicated that if the business follows

activity-based costing techniques than it would give a better presentation of the total cost and

also assist in the determination of prices for the business.

Question No 2

Requirement 2a

Break even analysis is a widely used technique by management accountants and

production manager. It is based on the production costs which are divided into two parts one is

variable cost which varies with the production unit and another one is fixed cost which remain

same in respect of production unit. Both cost is combined than it is compared with sales revenue

to get the position where by selling certain amount of goods company is earning neither profit

nor loss and that point is termed as break-even point.

In other words, breakeven analysis is very useful tool for taking vital decisions of the

business. The breakeven analysis tells the management the required units or revenue which the

management of the company needs to generate in order to at least cover the costs of the business

and reach a no profit no loss situation. On the basis of breakeven analysis, the management of

the company decide what prices are to be set for the products and what quantity of products the

management needs to sell in order to reach a no profit no loss situation. In addition to this,

breakeven point needs to be achieved by the business in order to ensure that the business

8

MANAGERIAL ACCOUNTING

continues its operations for a long period of time. The requirement of the part is to undertake

breakeven and sensitivity analysis for AzamJuta which is engaged in production process.

Management of a company uses breakeven analysis for the purpose of taking important decisions

relating to the business.

Requirement 2a

Calculation of break-even point in unit as well in sales revenue.

Break-even point in units = (Total fixed cost / Contribution per unit)

Particular Details Amount Unit

Contribution A

$

3,50,000.00

No of unit B 100000

Contribution per

unit (A/B)

$

3.50

Particular Details Amount UNIT

Total Fixed Cost A

$

2,10,000.00

Contribution per unit B

$

3.50

Break even in units (A/B) 60000

Break-even point in sales revenue = (Break-even in units * Sales per unit)

Particular Details Amount Unit

Sales A

$

7,50,000.00

No of unit sold B 100000

Sales per unit (A/B)

$

7.50

Break- even unit D 60000

Break-even in sales (A/B)*D

$

4,50,000.00

MANAGERIAL ACCOUNTING

continues its operations for a long period of time. The requirement of the part is to undertake

breakeven and sensitivity analysis for AzamJuta which is engaged in production process.

Management of a company uses breakeven analysis for the purpose of taking important decisions

relating to the business.

Requirement 2a

Calculation of break-even point in unit as well in sales revenue.

Break-even point in units = (Total fixed cost / Contribution per unit)

Particular Details Amount Unit

Contribution A

$

3,50,000.00

No of unit B 100000

Contribution per

unit (A/B)

$

3.50

Particular Details Amount UNIT

Total Fixed Cost A

$

2,10,000.00

Contribution per unit B

$

3.50

Break even in units (A/B) 60000

Break-even point in sales revenue = (Break-even in units * Sales per unit)

Particular Details Amount Unit

Sales A

$

7,50,000.00

No of unit sold B 100000

Sales per unit (A/B)

$

7.50

Break- even unit D 60000

Break-even in sales (A/B)*D

$

4,50,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGERIAL ACCOUNTING

Requirement 2c

Calculation of margin of safety in both units as well as sale revenue

Margin of safety in units = (Total profit / Contribution per unit)

Particular Details Amount Unit

Total profit A

$

1,40,000.00

Contribution per

unit B

$

3.50

MOS in unit (A/B) 40000

Margin of safety in sales revenue = (Total Sales – Break-Even sales)

Particular Details Amount

Total Sales A

$

7,50,000.00

Break-even sales B

$

4,50,000.00

MOS in sales (A-B)

$

3,00,000.00

Requirement 2d

As the company want to increase their sales from 8000 units and for that the company is

ready to incur for advertisement expenses. The estimation of the sales manager is that increase in

the sales of the business would be enhancing the revenue of the business. The calculations which

MANAGERIAL ACCOUNTING

Requirement 2c

Calculation of margin of safety in both units as well as sale revenue

Margin of safety in units = (Total profit / Contribution per unit)

Particular Details Amount Unit

Total profit A

$

1,40,000.00

Contribution per

unit B

$

3.50

MOS in unit (A/B) 40000

Margin of safety in sales revenue = (Total Sales – Break-Even sales)

Particular Details Amount

Total Sales A

$

7,50,000.00

Break-even sales B

$

4,50,000.00

MOS in sales (A-B)

$

3,00,000.00

Requirement 2d

As the company want to increase their sales from 8000 units and for that the company is

ready to incur for advertisement expenses. The estimation of the sales manager is that increase in

the sales of the business would be enhancing the revenue of the business. The calculations which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGERIAL ACCOUNTING

is presented below shows the extra expenses which the management of the company is willing to

undertake for the purpose of enhancing the sales of the business.

Calculation as per company new proposal

Particular Details Amount Unit

Sales in unit A 108000

Sales per unit B

$

7.50

Total sales (A*B)

$

8,10,000.00

Variable cost per unit D

$

4.00

Total variable cost (D*A)

$

4,32,000.00

Total fixed cost E

$

2,10,000.00

Advertisement cost F

$

22,000.00

Total cost (D*A)+E+F

$

6,64,000.00

Total profit (A*B)-{(D*A)+E+F}

$

1,46,000.00

It can be seen from the above calculation that previously the company was earning

$140000 when they were selling 100000 units but when they did advertisement expense of

$22000 than they able to sell 108000 and then the profit was $146000 so it can be said that by

the new proposal which company is thinking for implement than they will able to earn (146000-

140000) profit that is more $6000 profit they will able to earn if they invest $22000 on

advertisement so there income will increase by $6000.

Requirement 2e

The maximum amount which the company can invest on advertisement to increase their

sale by 8000 units and not by affecting the current profit. The amount which can be invested is

MANAGERIAL ACCOUNTING

is presented below shows the extra expenses which the management of the company is willing to

undertake for the purpose of enhancing the sales of the business.

Calculation as per company new proposal

Particular Details Amount Unit

Sales in unit A 108000

Sales per unit B

$

7.50

Total sales (A*B)

$

8,10,000.00

Variable cost per unit D

$

4.00

Total variable cost (D*A)

$

4,32,000.00

Total fixed cost E

$

2,10,000.00

Advertisement cost F

$

22,000.00

Total cost (D*A)+E+F

$

6,64,000.00

Total profit (A*B)-{(D*A)+E+F}

$

1,46,000.00

It can be seen from the above calculation that previously the company was earning

$140000 when they were selling 100000 units but when they did advertisement expense of

$22000 than they able to sell 108000 and then the profit was $146000 so it can be said that by

the new proposal which company is thinking for implement than they will able to earn (146000-

140000) profit that is more $6000 profit they will able to earn if they invest $22000 on

advertisement so there income will increase by $6000.

Requirement 2e

The maximum amount which the company can invest on advertisement to increase their

sale by 8000 units and not by affecting the current profit. The amount which can be invested is

11

MANAGERIAL ACCOUNTING

(22000+6000) = 28000 so till $28000 company can invest in advertisement and this will not

make any impact on their current profit which is $140000.

MANAGERIAL ACCOUNTING

(22000+6000) = 28000 so till $28000 company can invest in advertisement and this will not

make any impact on their current profit which is $140000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.