Costing Questions Solution: Cost Behavior, Breakeven Analysis Example

VerifiedAdded on 2023/04/26

|7

|1224

|288

Homework Assignment

AI Summary

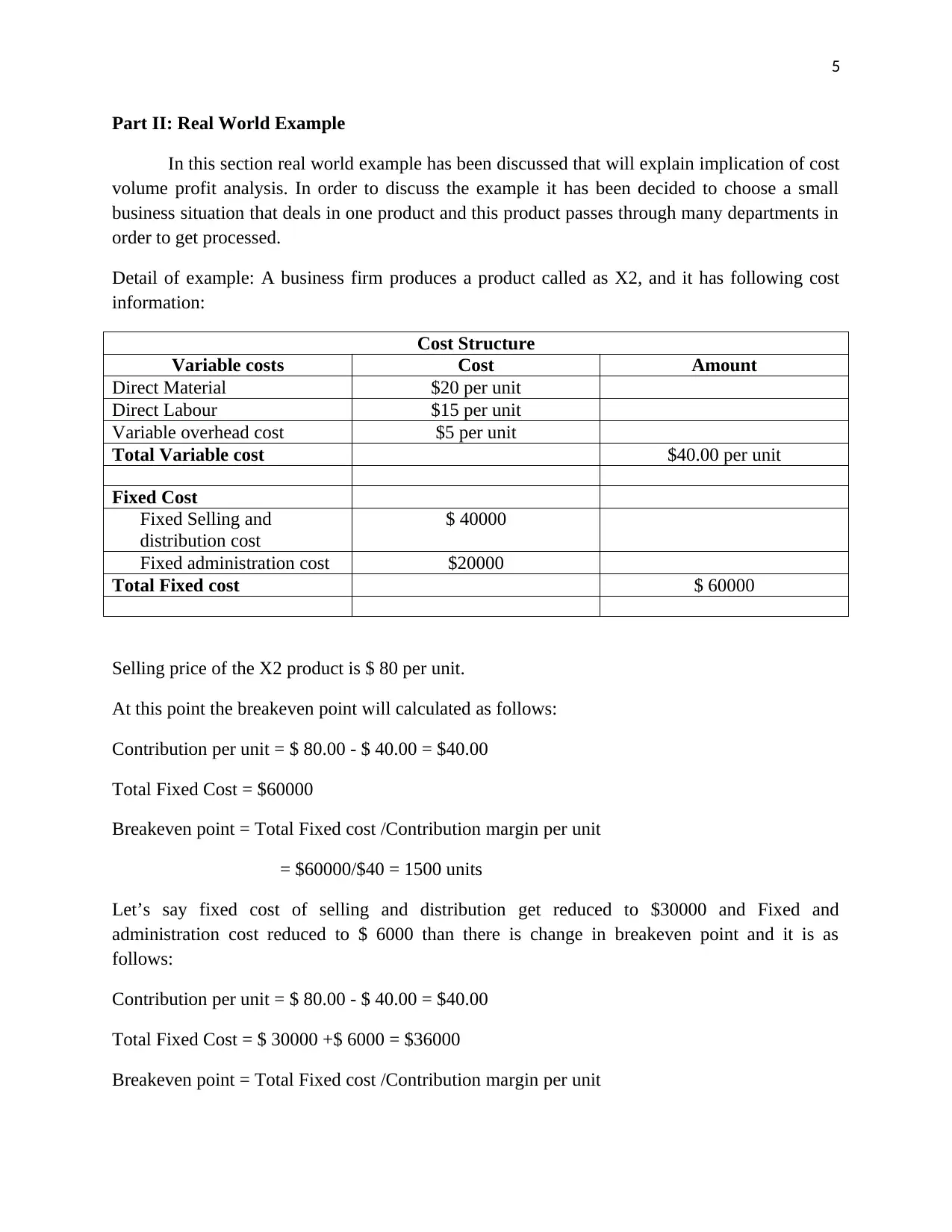

This assignment provides a comprehensive solution to costing questions, covering key concepts such as variable and fixed costs, cost behavior patterns, and the break-even point. It explains how to calculate break-even sales in both units and revenue, as well as how to determine the number of units needed to achieve a desired income level. The assignment also discusses the relevant range concept and provides practical examples to illustrate how changes in selling prices and fixed costs impact the break-even point. A real-world example using a small business scenario is included to demonstrate the application of cost-volume-profit (CVP) analysis, showing how changes in fixed costs affect the break-even point. The assignment concludes with a list of references used.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.