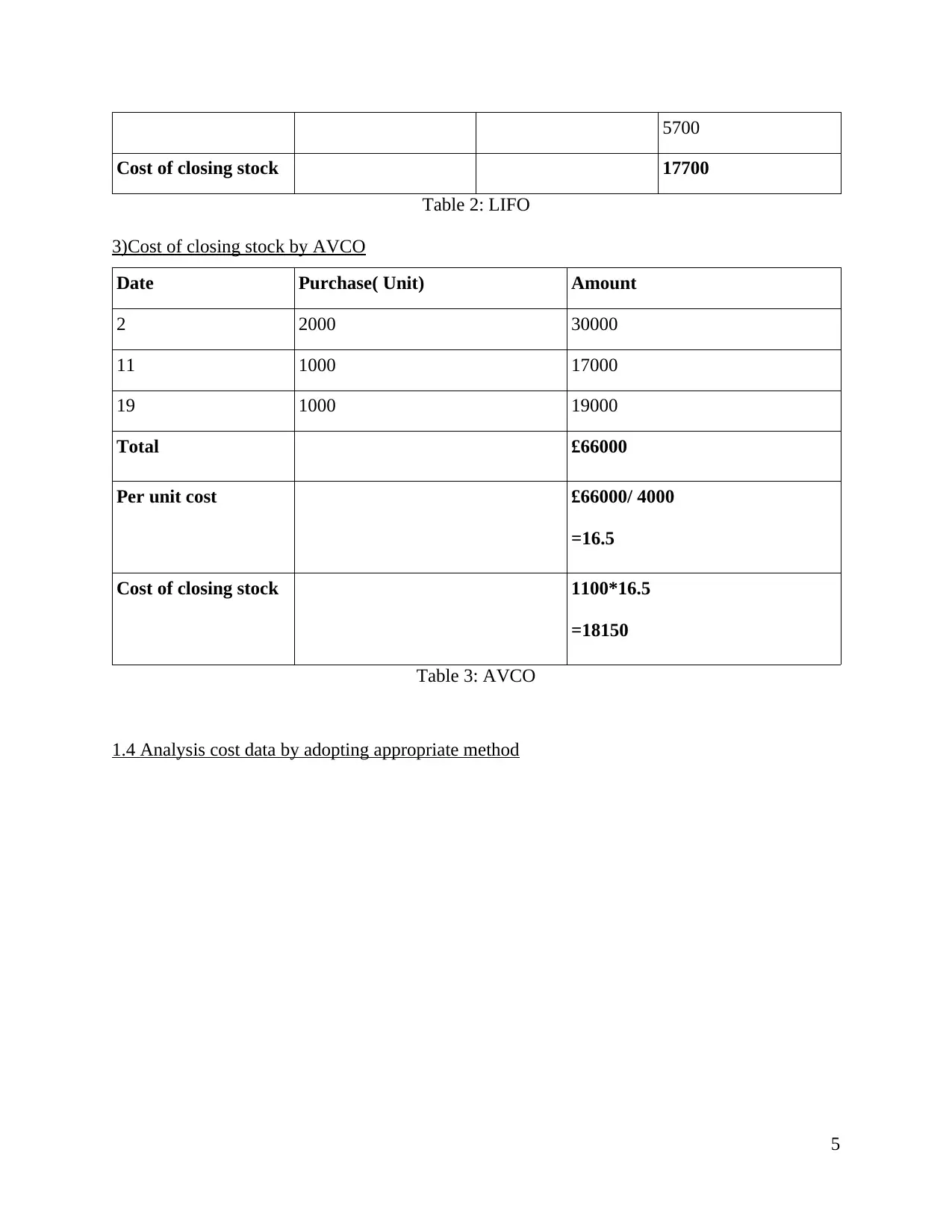

Detailed Report on Costing, Budgeting, and Performance: ABC Company

VerifiedAdded on 2020/06/05

|19

|4032

|53

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to ABC Company. It begins with a classification of costs, exploring fixed, variable, direct, indirect, and functional cost categories. The report then delves into various costing methods, including job costing, batch costing, process costing, contract costing, and service costing. Calculations for closing stock using FIFO, LIFO, and AVCO methods are presented. Furthermore, the report analyzes cost data, employing both absorption and marginal costing techniques. The analysis extends to the preparation of routine cost reports, variance analysis, and the identification of potential improvements through performance indicators like benchmarking. Finally, the report covers the purpose and types of budgeting, budget preparation (sales, production, material usage, and purchases), cash budgeting, and the calculation of variances, concluding with recommendations for enhanced financial performance.

MANAGEMENT ACCOUNTING,

COSTING AND BUDGETING

COSTING AND BUDGETING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.2 Use of costing methods....................................................................................................2

1.3 Calculation of closing stock.............................................................................................3

1.4 Analysis cost data by adopting appropriate method.........................................................5

TASK 2............................................................................................................................................6

2.1 Preparation and analysing routine cost.............................................................................6

2.2 Identification of potential improvements for a company by adopting performance

indicators................................................................................................................................7

2.3 Suggestion for improvements to minimize, improves values and quality to the firm......7

TASK 3............................................................................................................................................8

3.1 Purpose and nature of budgeting process.........................................................................8

3.2 Types of budgeting methods............................................................................................9

3.3 Preparation of budgets......................................................................................................9

3.4 Prepare cash budget........................................................................................................11

TASK 4..........................................................................................................................................12

4.1 Calculation of variances.................................................................................................12

4.2 Prepare an operating statement.......................................................................................13

4.3 Recommendation............................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.2 Use of costing methods....................................................................................................2

1.3 Calculation of closing stock.............................................................................................3

1.4 Analysis cost data by adopting appropriate method.........................................................5

TASK 2............................................................................................................................................6

2.1 Preparation and analysing routine cost.............................................................................6

2.2 Identification of potential improvements for a company by adopting performance

indicators................................................................................................................................7

2.3 Suggestion for improvements to minimize, improves values and quality to the firm......7

TASK 3............................................................................................................................................8

3.1 Purpose and nature of budgeting process.........................................................................8

3.2 Types of budgeting methods............................................................................................9

3.3 Preparation of budgets......................................................................................................9

3.4 Prepare cash budget........................................................................................................11

TASK 4..........................................................................................................................................12

4.1 Calculation of variances.................................................................................................12

4.2 Prepare an operating statement.......................................................................................13

4.3 Recommendation............................................................................................................14

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

Index of Tables

Table 1: FIFO METHOD.................................................................................................................3

Table 2: LIFO..................................................................................................................................4

Table 3: AVCO................................................................................................................................4

Table 4: sales budget........................................................................................................................9

Table 5: Production budget..............................................................................................................9

Table 6: Material usage budget........................................................................................................9

Table 7: Material purchase budget.................................................................................................10

Table 8: Plastic usage budget.........................................................................................................10

Table 9: Plastic purchase budget....................................................................................................10

Table 10: Material usage variance.................................................................................................11

Table 11: Labour variance.............................................................................................................11

Table 12: Labour idle time variance..............................................................................................12

Table 13: Variable overhead variance...........................................................................................12

Table 14: Fixed overhead variance................................................................................................12

Table 1: FIFO METHOD.................................................................................................................3

Table 2: LIFO..................................................................................................................................4

Table 3: AVCO................................................................................................................................4

Table 4: sales budget........................................................................................................................9

Table 5: Production budget..............................................................................................................9

Table 6: Material usage budget........................................................................................................9

Table 7: Material purchase budget.................................................................................................10

Table 8: Plastic usage budget.........................................................................................................10

Table 9: Plastic purchase budget....................................................................................................10

Table 10: Material usage variance.................................................................................................11

Table 11: Labour variance.............................................................................................................11

Table 12: Labour idle time variance..............................................................................................12

Table 13: Variable overhead variance...........................................................................................12

Table 14: Fixed overhead variance................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

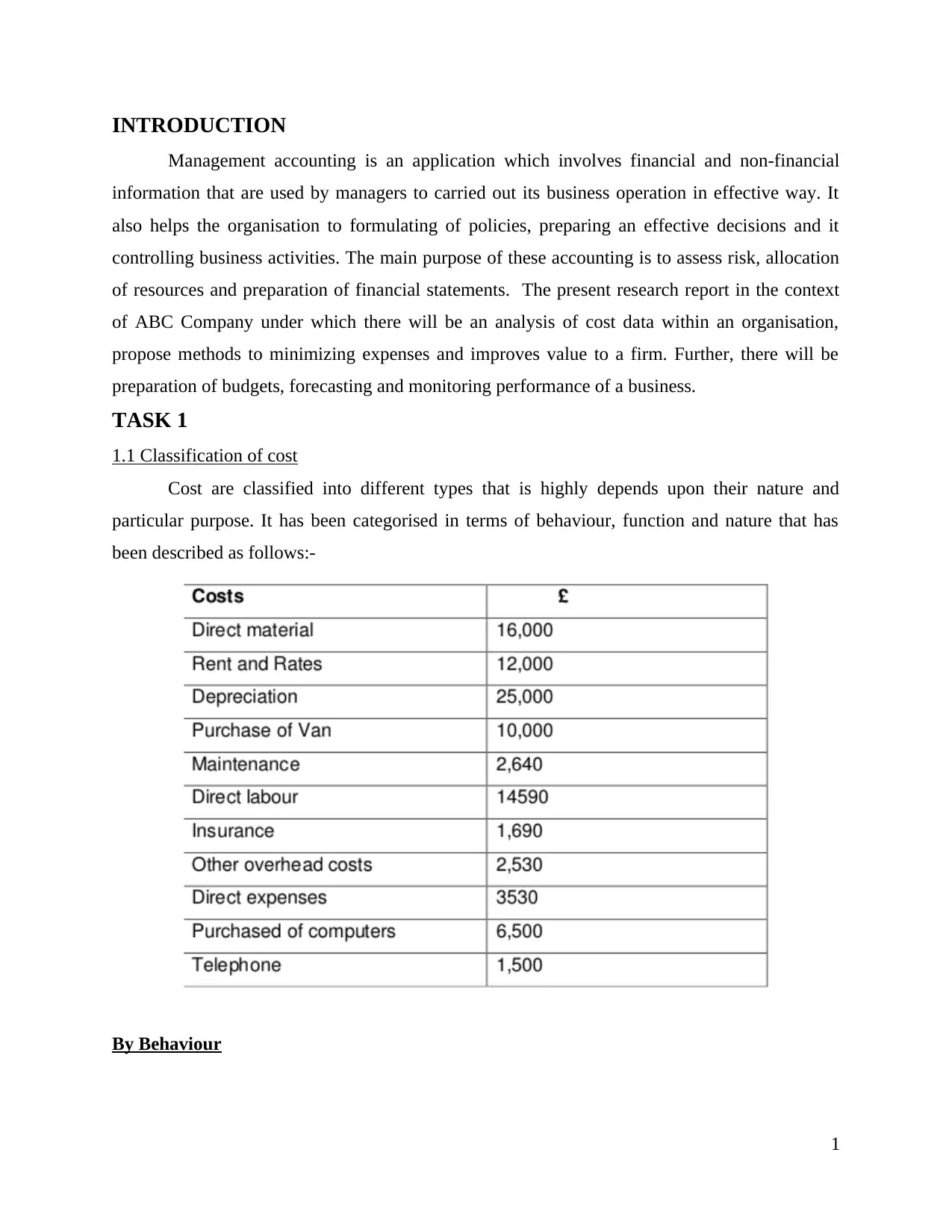

INTRODUCTION

Management accounting is an application which involves financial and non-financial

information that are used by managers to carried out its business operation in effective way. It

also helps the organisation to formulating of policies, preparing an effective decisions and it

controlling business activities. The main purpose of these accounting is to assess risk, allocation

of resources and preparation of financial statements. The present research report in the context

of ABC Company under which there will be an analysis of cost data within an organisation,

propose methods to minimizing expenses and improves value to a firm. Further, there will be

preparation of budgets, forecasting and monitoring performance of a business.

TASK 1

1.1 Classification of cost

Cost are classified into different types that is highly depends upon their nature and

particular purpose. It has been categorised in terms of behaviour, function and nature that has

been described as follows:-

By Behaviour

1

Management accounting is an application which involves financial and non-financial

information that are used by managers to carried out its business operation in effective way. It

also helps the organisation to formulating of policies, preparing an effective decisions and it

controlling business activities. The main purpose of these accounting is to assess risk, allocation

of resources and preparation of financial statements. The present research report in the context

of ABC Company under which there will be an analysis of cost data within an organisation,

propose methods to minimizing expenses and improves value to a firm. Further, there will be

preparation of budgets, forecasting and monitoring performance of a business.

TASK 1

1.1 Classification of cost

Cost are classified into different types that is highly depends upon their nature and

particular purpose. It has been categorised in terms of behaviour, function and nature that has

been described as follows:-

By Behaviour

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed cost: It is that type of expenses which cannot be vary with the increase or decrease

in the level of production. In regard to this, fixed cost of ABC Company involves from

the above all cost are rents and rates, insurance and depreciation of fixed assets etc.

Variable cost: It is that type of cost that are associated with the units and it will be varied

with the level of production changes increased or decreased. The variable expenses of a

cited company includes are direct material and direct labour etc.

Semi-variable cost: It is that type of cost in which particular portion of cost remains that

is fixed and the other balancing portion is variable cost known as semi-variable cost

(Scapens, 2016).

By Nature

Direct expenses: It is that expenses that are connected with the purchase and production

of goods or services of a business. It is mainly categorised into three parts which involves

material, labour and overhead expenses. For example, in the manufacturing process of

articles by a firm in which there is a needed to purchase material, employed labour and

paid wages to workers. All these expenses are incurred directly for a particular

commodity. From the above data of cost the direct expenses of ABC Company involves

direct material, direct labour, purchase of computer and purchase of van etc.

Indirect expenses: It is that type of cost that are incurred indirectly and these expenses

has no relationship with the buying or products or services. It occurred at the time of

operating a whole business that involves other overhead cost, insurance and rent etc.

By Function

Production cost: It is that type of expenses that can be incurred by the ABC Company at

the time of manufacturing a product or giving any kind of services (Grasso, 2016). The

firm incurred variety of cost that includes raw material, consumable manufacturing

supplies, direct material and direct labour etc.

Marketing cost: It is an associated at the time of transferring products or services to their

final consumers. The expenses are incurred at the time of promoting goods into the target

market such as advertising expenses, selling and distribution expenses etc.

1.2 Use of costing methods

The ABC Company are adopting different types of costing methods which has been

discussed as follows:-

2

in the level of production. In regard to this, fixed cost of ABC Company involves from

the above all cost are rents and rates, insurance and depreciation of fixed assets etc.

Variable cost: It is that type of cost that are associated with the units and it will be varied

with the level of production changes increased or decreased. The variable expenses of a

cited company includes are direct material and direct labour etc.

Semi-variable cost: It is that type of cost in which particular portion of cost remains that

is fixed and the other balancing portion is variable cost known as semi-variable cost

(Scapens, 2016).

By Nature

Direct expenses: It is that expenses that are connected with the purchase and production

of goods or services of a business. It is mainly categorised into three parts which involves

material, labour and overhead expenses. For example, in the manufacturing process of

articles by a firm in which there is a needed to purchase material, employed labour and

paid wages to workers. All these expenses are incurred directly for a particular

commodity. From the above data of cost the direct expenses of ABC Company involves

direct material, direct labour, purchase of computer and purchase of van etc.

Indirect expenses: It is that type of cost that are incurred indirectly and these expenses

has no relationship with the buying or products or services. It occurred at the time of

operating a whole business that involves other overhead cost, insurance and rent etc.

By Function

Production cost: It is that type of expenses that can be incurred by the ABC Company at

the time of manufacturing a product or giving any kind of services (Grasso, 2016). The

firm incurred variety of cost that includes raw material, consumable manufacturing

supplies, direct material and direct labour etc.

Marketing cost: It is an associated at the time of transferring products or services to their

final consumers. The expenses are incurred at the time of promoting goods into the target

market such as advertising expenses, selling and distribution expenses etc.

1.2 Use of costing methods

The ABC Company are adopting different types of costing methods which has been

discussed as follows:-

2

Job costing: The organisation used this method to determine the productions in terms of

job completion. The costs are not concerned to the production units but it is related to the

cost for a work order. The elements that are mainly involves in it are prime cost such as

direct material and direct labour that are directly charges to the jobs (Greve, 2017).

Batch costing: It is a form of job costing which is used at the time when an article are

manufactured in batches. The ABC Company ascertained cost for the whole batch and

after that cost of per unit is measured. It is also used by the various industries such as

manufacturing industries, ready made garments and pharmaceuticals industry.

Process costing: It is mainly used in cost accounting that helps in accumulates and traces

direct expenses and allocating the indirect expenses of a production procedure. Thus, the

cost are assigned to goods generally in a large batch that involves a whole month's

production. It is mainly suitable for those industries who manufacture a homogeneous

good and flow continuously.

Contract costing: It is that type of costing method that are applied by ABC limited at the

time of ascertaining cost construction work according to a specification of customers

(Otley, 2016). It helps the builders, construction and mechanical engineering firms,

construction contractors to measure the total contract cost. It is a similar to the job costing

in which a separate numbers are allotted for a particular contract and records them

separately.

Service costing: It is that method of cost accounting in which it involves all types of cost

that occurred in the manufacture of a service are combined together. It will be divided by

the total number of units of services and the total expenses are divided through total units

at per cost unit. It is mainly used in providing transports, hotels, public utility services

such as telephone, water, electricity and telephone, hospitals, buses, railways and other

association where there will be services rendered (Shields, 2016).

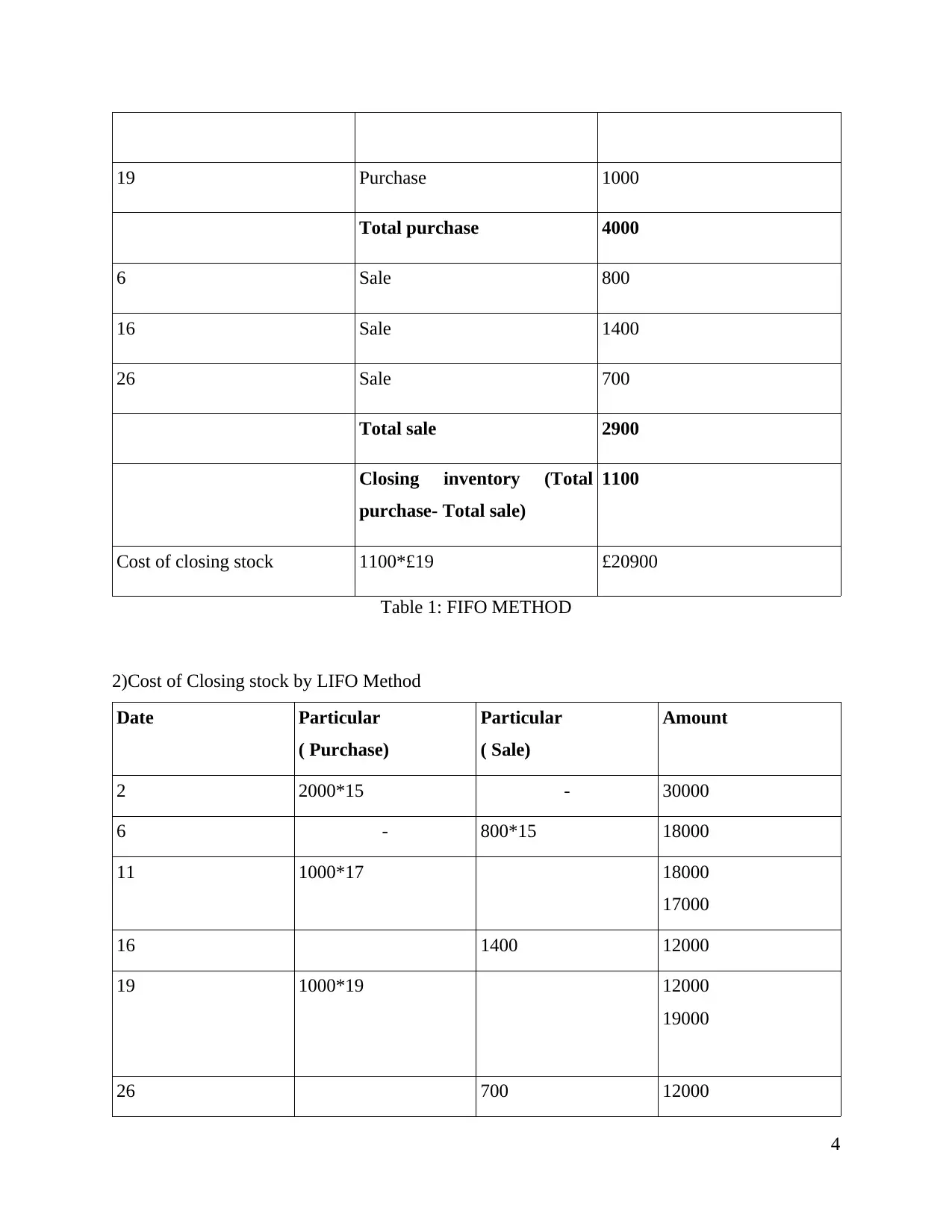

1.3 Calculation of closing stock

1) Cost of closing stock by FIFO method

Date Particular Units

2 Purchase 2000

11 Purchase 1000

3

job completion. The costs are not concerned to the production units but it is related to the

cost for a work order. The elements that are mainly involves in it are prime cost such as

direct material and direct labour that are directly charges to the jobs (Greve, 2017).

Batch costing: It is a form of job costing which is used at the time when an article are

manufactured in batches. The ABC Company ascertained cost for the whole batch and

after that cost of per unit is measured. It is also used by the various industries such as

manufacturing industries, ready made garments and pharmaceuticals industry.

Process costing: It is mainly used in cost accounting that helps in accumulates and traces

direct expenses and allocating the indirect expenses of a production procedure. Thus, the

cost are assigned to goods generally in a large batch that involves a whole month's

production. It is mainly suitable for those industries who manufacture a homogeneous

good and flow continuously.

Contract costing: It is that type of costing method that are applied by ABC limited at the

time of ascertaining cost construction work according to a specification of customers

(Otley, 2016). It helps the builders, construction and mechanical engineering firms,

construction contractors to measure the total contract cost. It is a similar to the job costing

in which a separate numbers are allotted for a particular contract and records them

separately.

Service costing: It is that method of cost accounting in which it involves all types of cost

that occurred in the manufacture of a service are combined together. It will be divided by

the total number of units of services and the total expenses are divided through total units

at per cost unit. It is mainly used in providing transports, hotels, public utility services

such as telephone, water, electricity and telephone, hospitals, buses, railways and other

association where there will be services rendered (Shields, 2016).

1.3 Calculation of closing stock

1) Cost of closing stock by FIFO method

Date Particular Units

2 Purchase 2000

11 Purchase 1000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

19 Purchase 1000

Total purchase 4000

6 Sale 800

16 Sale 1400

26 Sale 700

Total sale 2900

Closing inventory (Total

purchase- Total sale)

1100

Cost of closing stock 1100*£19 £20900

Table 1: FIFO METHOD

2)Cost of Closing stock by LIFO Method

Date Particular

( Purchase)

Particular

( Sale)

Amount

2 2000*15 - 30000

6 - 800*15 18000

11 1000*17 18000

17000

16 1400 12000

19 1000*19 12000

19000

26 700 12000

4

Total purchase 4000

6 Sale 800

16 Sale 1400

26 Sale 700

Total sale 2900

Closing inventory (Total

purchase- Total sale)

1100

Cost of closing stock 1100*£19 £20900

Table 1: FIFO METHOD

2)Cost of Closing stock by LIFO Method

Date Particular

( Purchase)

Particular

( Sale)

Amount

2 2000*15 - 30000

6 - 800*15 18000

11 1000*17 18000

17000

16 1400 12000

19 1000*19 12000

19000

26 700 12000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5700

Cost of closing stock 17700

Table 2: LIFO

3)Cost of closing stock by AVCO

Date Purchase( Unit) Amount

2 2000 30000

11 1000 17000

19 1000 19000

Total £66000

Per unit cost £66000/ 4000

=16.5

Cost of closing stock 1100*16.5

=18150

Table 3: AVCO

1.4 Analysis cost data by adopting appropriate method

5

Cost of closing stock 17700

Table 2: LIFO

3)Cost of closing stock by AVCO

Date Purchase( Unit) Amount

2 2000 30000

11 1000 17000

19 1000 19000

Total £66000

Per unit cost £66000/ 4000

=16.5

Cost of closing stock 1100*16.5

=18150

Table 3: AVCO

1.4 Analysis cost data by adopting appropriate method

5

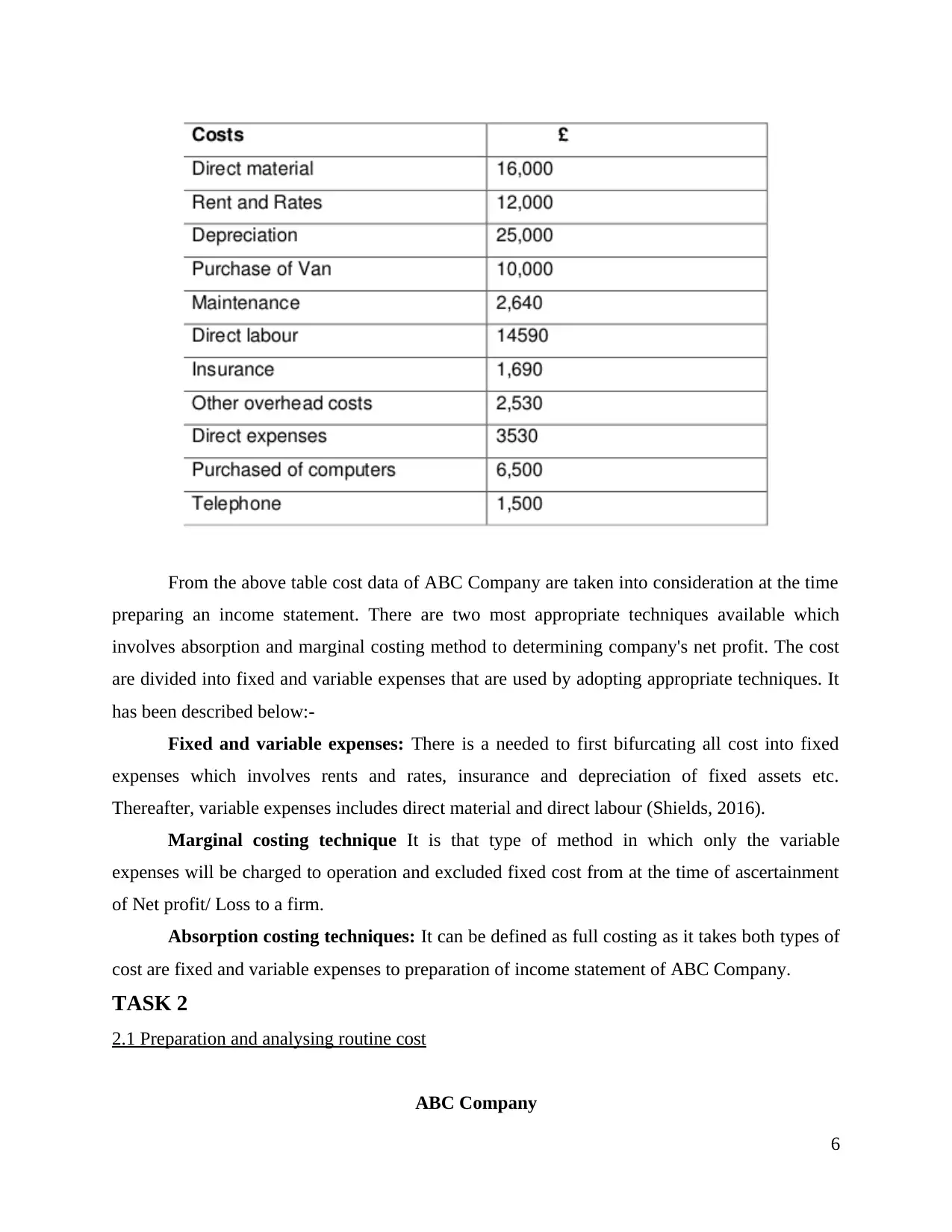

From the above table cost data of ABC Company are taken into consideration at the time

preparing an income statement. There are two most appropriate techniques available which

involves absorption and marginal costing method to determining company's net profit. The cost

are divided into fixed and variable expenses that are used by adopting appropriate techniques. It

has been described below:-

Fixed and variable expenses: There is a needed to first bifurcating all cost into fixed

expenses which involves rents and rates, insurance and depreciation of fixed assets etc.

Thereafter, variable expenses includes direct material and direct labour (Shields, 2016).

Marginal costing technique It is that type of method in which only the variable

expenses will be charged to operation and excluded fixed cost from at the time of ascertainment

of Net profit/ Loss to a firm.

Absorption costing techniques: It can be defined as full costing as it takes both types of

cost are fixed and variable expenses to preparation of income statement of ABC Company.

TASK 2

2.1 Preparation and analysing routine cost

ABC Company

6

preparing an income statement. There are two most appropriate techniques available which

involves absorption and marginal costing method to determining company's net profit. The cost

are divided into fixed and variable expenses that are used by adopting appropriate techniques. It

has been described below:-

Fixed and variable expenses: There is a needed to first bifurcating all cost into fixed

expenses which involves rents and rates, insurance and depreciation of fixed assets etc.

Thereafter, variable expenses includes direct material and direct labour (Shields, 2016).

Marginal costing technique It is that type of method in which only the variable

expenses will be charged to operation and excluded fixed cost from at the time of ascertainment

of Net profit/ Loss to a firm.

Absorption costing techniques: It can be defined as full costing as it takes both types of

cost are fixed and variable expenses to preparation of income statement of ABC Company.

TASK 2

2.1 Preparation and analysing routine cost

ABC Company

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

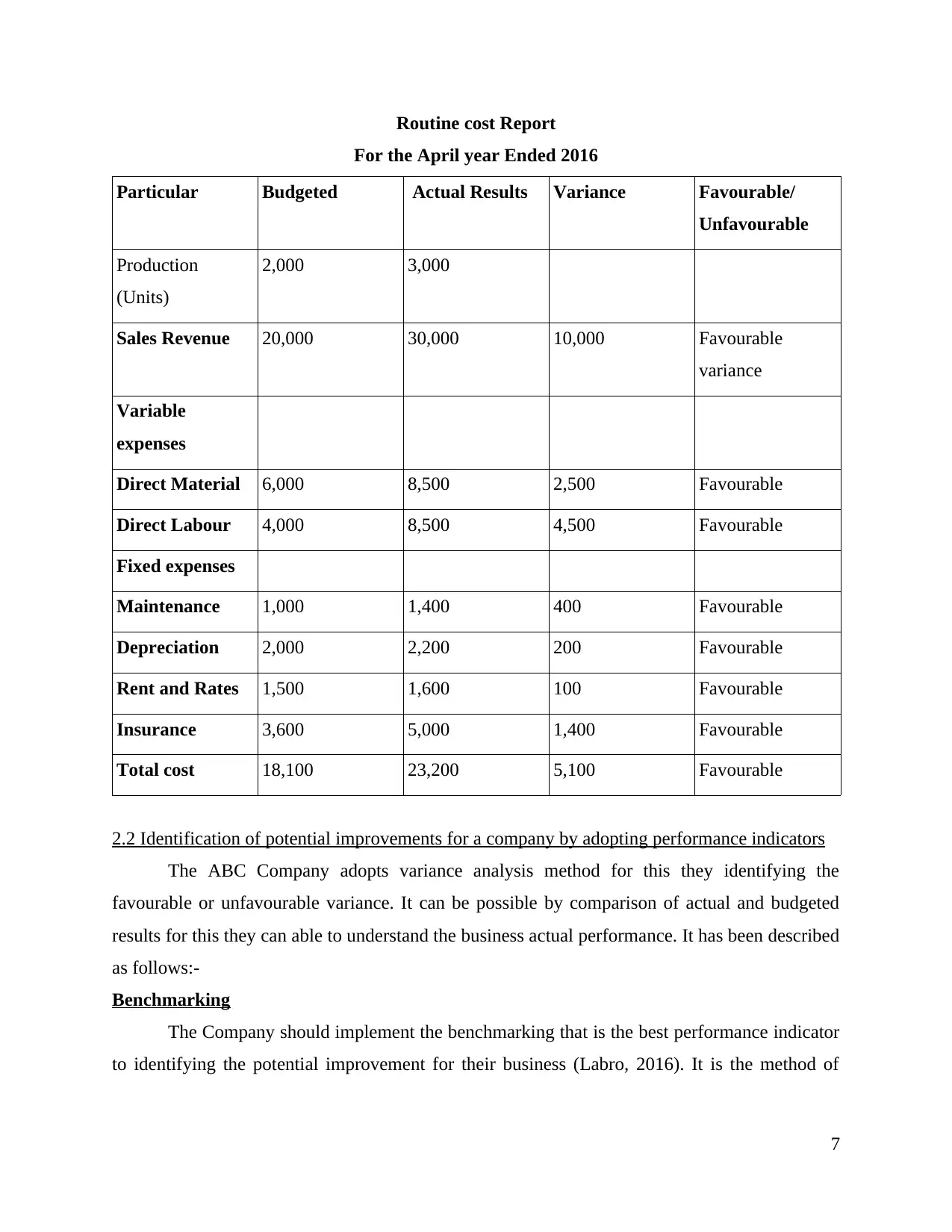

Routine cost Report

For the April year Ended 2016

Particular Budgeted Actual Results Variance Favourable/

Unfavourable

Production

(Units)

2,000 3,000

Sales Revenue 20,000 30,000 10,000 Favourable

variance

Variable

expenses

Direct Material 6,000 8,500 2,500 Favourable

Direct Labour 4,000 8,500 4,500 Favourable

Fixed expenses

Maintenance 1,000 1,400 400 Favourable

Depreciation 2,000 2,200 200 Favourable

Rent and Rates 1,500 1,600 100 Favourable

Insurance 3,600 5,000 1,400 Favourable

Total cost 18,100 23,200 5,100 Favourable

2.2 Identification of potential improvements for a company by adopting performance indicators

The ABC Company adopts variance analysis method for this they identifying the

favourable or unfavourable variance. It can be possible by comparison of actual and budgeted

results for this they can able to understand the business actual performance. It has been described

as follows:-

Benchmarking

The Company should implement the benchmarking that is the best performance indicator

to identifying the potential improvement for their business (Labro, 2016). It is the method of

7

For the April year Ended 2016

Particular Budgeted Actual Results Variance Favourable/

Unfavourable

Production

(Units)

2,000 3,000

Sales Revenue 20,000 30,000 10,000 Favourable

variance

Variable

expenses

Direct Material 6,000 8,500 2,500 Favourable

Direct Labour 4,000 8,500 4,500 Favourable

Fixed expenses

Maintenance 1,000 1,400 400 Favourable

Depreciation 2,000 2,200 200 Favourable

Rent and Rates 1,500 1,600 100 Favourable

Insurance 3,600 5,000 1,400 Favourable

Total cost 18,100 23,200 5,100 Favourable

2.2 Identification of potential improvements for a company by adopting performance indicators

The ABC Company adopts variance analysis method for this they identifying the

favourable or unfavourable variance. It can be possible by comparison of actual and budgeted

results for this they can able to understand the business actual performance. It has been described

as follows:-

Benchmarking

The Company should implement the benchmarking that is the best performance indicator

to identifying the potential improvement for their business (Labro, 2016). It is the method of

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

monitoring and collecting key indicators to finding out performance gaps and also potential areas

for the improvement of business levels.

Favourable variance: It can be occurred when the actual results are increasing the

budged results. Suppose, the ABC Company keeps the benchmarking of industry

standard practices that is ROI 8%. The favourable variance occur when the firm exceed

the ROI 8%. Thereafter, the companies can maintain their ROI at or above 8% by invest

into potential areas. It can possible through product launch by grand opening, employee

appreciation, increase customer loyalty, build brand awareness increase productivity,

enhance employee morale and clients appreciation.

Unfavourable variance: It is that type of variance in which the Company exceeds their

actual result with the budgeted results. For example, the ABC Limited can attain the

benchmarking of ROI 8% that is below the expected results that it occur unfavourable

variance. Further, they performance gaps of a company is fulfilled by identification of

their competitor's strategies. For this, they formulate its own policy and strategies that

helps to satisfy their customers effectively. Apart from this, they should invest amount on

marketing and promoting its goods or services into the potential target market (Atkinson,

2015).

2.3 Suggestion for improvements to minimize, improves values and quality to the firm.

In the competitive environment the accounting manager of ABC Company have to

provide an accurate information by focus on enhance value and eliminate wastage to a firm. For

this, they have to participated and observed an aspects by adding value for management

accounting information. These are as discussed below:-

Activity based costing: It should be used by management accountant of a Company to

provide an actual cost information regards to business process and activities. Thus, the

ABC system are mainly focused on the overall organisational activities for assessing its

cost behaviour. For this, the manager effectively allocating cost as well as resource for

the purpose of financial reporting. It is helpful for the ABC Company as the information

is integrated with continuous profit improves its activities and able to enhance value.

Balance score card: It is that type of approach in which it identifies overall new process

that must necessary to attain the organisation's performance objectives (Atkinson, 2015).

The company can enhance value and quality of management accounting information at

8

for the improvement of business levels.

Favourable variance: It can be occurred when the actual results are increasing the

budged results. Suppose, the ABC Company keeps the benchmarking of industry

standard practices that is ROI 8%. The favourable variance occur when the firm exceed

the ROI 8%. Thereafter, the companies can maintain their ROI at or above 8% by invest

into potential areas. It can possible through product launch by grand opening, employee

appreciation, increase customer loyalty, build brand awareness increase productivity,

enhance employee morale and clients appreciation.

Unfavourable variance: It is that type of variance in which the Company exceeds their

actual result with the budgeted results. For example, the ABC Limited can attain the

benchmarking of ROI 8% that is below the expected results that it occur unfavourable

variance. Further, they performance gaps of a company is fulfilled by identification of

their competitor's strategies. For this, they formulate its own policy and strategies that

helps to satisfy their customers effectively. Apart from this, they should invest amount on

marketing and promoting its goods or services into the potential target market (Atkinson,

2015).

2.3 Suggestion for improvements to minimize, improves values and quality to the firm.

In the competitive environment the accounting manager of ABC Company have to

provide an accurate information by focus on enhance value and eliminate wastage to a firm. For

this, they have to participated and observed an aspects by adding value for management

accounting information. These are as discussed below:-

Activity based costing: It should be used by management accountant of a Company to

provide an actual cost information regards to business process and activities. Thus, the

ABC system are mainly focused on the overall organisational activities for assessing its

cost behaviour. For this, the manager effectively allocating cost as well as resource for

the purpose of financial reporting. It is helpful for the ABC Company as the information

is integrated with continuous profit improves its activities and able to enhance value.

Balance score card: It is that type of approach in which it identifies overall new process

that must necessary to attain the organisation's performance objectives (Atkinson, 2015).

The company can enhance value and quality of management accounting information at

8

each prospectives. There are four perspective that involves financial: in that they

understand how the firm can create value for its shareholders. Customers: they identify

the needs and desires of their newly as well as existing customers for which it able to

enhance their value by satisfy them effectively. Internal process: the performance of

organisation is viewed by the lenses of efficiency and quality regards to its products or

services. Learning and growth: quality of an organisation can be improves through

providing training to their employees.

TASK 3

3.1 Purpose and nature of budgeting process

Budgeting process are adopted by most of the firms that involves future planning of

expenditure and revenues by managing a financial plan. The ABC Company used budget

procedure that have some purpose and nature included in it. It has been discussed below:-

Purpose & Nature of budgeting process Forecasting business performance: It provides a financial framework of a business

through which an effective decision can be made by managers. It helps the firms to

determining their future business performance through comparison of actual and

budgeting expenditure.

Controlling and monitoring: The company applied budgeting procedure for an

identification of variance occurred if it shows unfavourable then it is negative situation of

a firm (Shields, 2016). For this, the manager control the activities that hinder the business

performance and make necessary adjustments for further improvements.

3.2 Types of budgeting methods

The ABC Company adopts the budgeting techniques for the various needs and purposes.

It can be of various types that has been described as follows:-

Incremental budgeting: It is that budgeting techniques that can be also known as

traditional method whereby it is prepared through undertaking the actual performance. It

is a base with the incremental amounts that involves inflation or planned sales and cost

increase etc. It will be added for the getting the new budget period and it is based upon

the recent budgets. The benefits of incremental budgets for a ABC Company is that it

allow them to prepare quickly, easy to understand, it takes less time and cost etc.

9

understand how the firm can create value for its shareholders. Customers: they identify

the needs and desires of their newly as well as existing customers for which it able to

enhance their value by satisfy them effectively. Internal process: the performance of

organisation is viewed by the lenses of efficiency and quality regards to its products or

services. Learning and growth: quality of an organisation can be improves through

providing training to their employees.

TASK 3

3.1 Purpose and nature of budgeting process

Budgeting process are adopted by most of the firms that involves future planning of

expenditure and revenues by managing a financial plan. The ABC Company used budget

procedure that have some purpose and nature included in it. It has been discussed below:-

Purpose & Nature of budgeting process Forecasting business performance: It provides a financial framework of a business

through which an effective decision can be made by managers. It helps the firms to

determining their future business performance through comparison of actual and

budgeting expenditure.

Controlling and monitoring: The company applied budgeting procedure for an

identification of variance occurred if it shows unfavourable then it is negative situation of

a firm (Shields, 2016). For this, the manager control the activities that hinder the business

performance and make necessary adjustments for further improvements.

3.2 Types of budgeting methods

The ABC Company adopts the budgeting techniques for the various needs and purposes.

It can be of various types that has been described as follows:-

Incremental budgeting: It is that budgeting techniques that can be also known as

traditional method whereby it is prepared through undertaking the actual performance. It

is a base with the incremental amounts that involves inflation or planned sales and cost

increase etc. It will be added for the getting the new budget period and it is based upon

the recent budgets. The benefits of incremental budgets for a ABC Company is that it

allow them to prepare quickly, easy to understand, it takes less time and cost etc.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.