Management Accounting Report: Smart Looks Case Study

VerifiedAdded on 2020/02/03

|19

|5696

|316

Report

AI Summary

This report analyzes management accounting principles applied to the case of Smart Looks, a clothing manufacturer. It begins by classifying costs (variable, fixed, semi-variable, direct, and indirect) and computing total and unit costs at different production levels, including graphical analysis. Inventory valuation methods (FIFO, LIFO, and average cost) are compared, and a report on cost of goods sold is prepared. The report then identifies critical success factors and KPIs for measuring success, including ways to minimize costs and strategies to enhance value and quality. The second task focuses on budgeting, defining its purpose and outlining various budgeting methods, followed by the preparation of sales, production, raw materials, labor, and overhead budgets. The final task involves variance analysis, calculating budgeted and actual profit, material and labor variances, and preparing an operating statement. A managerial report summarizing the findings concludes the analysis.

Management accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

Q1. (A) Classification of the costs into fixed, variable and semi-variable.......................................3

(B) Explaining other ways of costs classification.............................................................................4

Q2. (A) Computing the total costs and unit costs for the production level......................................4

(B) Analyzing costs data using graphical format..............................................................................5

Q3.(1) First-in-First out....................................................................................................................6

(2) Last-in-first out...........................................................................................................................6

(3) Average costs method..................................................................................................................7

Q4. Preparing a report presenting costs of goods sold under different inventory methods..............7

Q5. Indicators to be used for measuring the success........................................................................8

(A) Two critical success factor & KPIs............................................................................................8

(B)(i) Ways to minimize costs..........................................................................................................8

(ii) Strategies to enhance value & quality.........................................................................................8

TASK 2.................................................................................................................................................9

Q6.....................................................................................................................................................9

(A) Budget definition........................................................................................................................9

(B) Purpose of budget.......................................................................................................................9

(C) Different kind of methods for preparation of budget...............................................................10

Q7....................................................................................................................................................11

(A) Sales budget..............................................................................................................................11

(B) Production budget.....................................................................................................................11

(C) Raw material budget.................................................................................................................12

(D) Labour budget..........................................................................................................................12

(E) Total overheads budget.............................................................................................................12

Q8. Cash budget and its analysis....................................................................................................13

TASK 3...............................................................................................................................................14

Q9. (A) Calculation of budgeted profit for the month of March, 2017..........................................14

(B) Calculation of actual profit for the month of March, 2017......................................................14

(C). Calculation of material & labour variances.............................................................................15

(D). Preparation of an operating statement reconciling the targeted and actual results.................16

Q10. Managerial report...................................................................................................................16

CONCLUSION..................................................................................................................................17

REFERENCES...................................................................................................................................18

2

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

Q1. (A) Classification of the costs into fixed, variable and semi-variable.......................................3

(B) Explaining other ways of costs classification.............................................................................4

Q2. (A) Computing the total costs and unit costs for the production level......................................4

(B) Analyzing costs data using graphical format..............................................................................5

Q3.(1) First-in-First out....................................................................................................................6

(2) Last-in-first out...........................................................................................................................6

(3) Average costs method..................................................................................................................7

Q4. Preparing a report presenting costs of goods sold under different inventory methods..............7

Q5. Indicators to be used for measuring the success........................................................................8

(A) Two critical success factor & KPIs............................................................................................8

(B)(i) Ways to minimize costs..........................................................................................................8

(ii) Strategies to enhance value & quality.........................................................................................8

TASK 2.................................................................................................................................................9

Q6.....................................................................................................................................................9

(A) Budget definition........................................................................................................................9

(B) Purpose of budget.......................................................................................................................9

(C) Different kind of methods for preparation of budget...............................................................10

Q7....................................................................................................................................................11

(A) Sales budget..............................................................................................................................11

(B) Production budget.....................................................................................................................11

(C) Raw material budget.................................................................................................................12

(D) Labour budget..........................................................................................................................12

(E) Total overheads budget.............................................................................................................12

Q8. Cash budget and its analysis....................................................................................................13

TASK 3...............................................................................................................................................14

Q9. (A) Calculation of budgeted profit for the month of March, 2017..........................................14

(B) Calculation of actual profit for the month of March, 2017......................................................14

(C). Calculation of material & labour variances.............................................................................15

(D). Preparation of an operating statement reconciling the targeted and actual results.................16

Q10. Managerial report...................................................................................................................16

CONCLUSION..................................................................................................................................17

REFERENCES...................................................................................................................................18

2

INTRODUCTION

Management accounting is a field or segment of accounting which deals with the

information collection, accounting and reporting it to the management to aware them about the

results of detailed operations in order to make effective plans and decisions in various operational

areas. Smart Looks is a retailing organization that satisfy apparel requirement of the clients by

manufacturing cloths focusing consumer specification. The report emphasize upon costs behaviour,

stock valuation, budgeting planning and controlling and variances analysis in order for making good

decisions for the betterment of the firm.

TASK 1

Q1. (A) Classification of the costs into fixed, variable and semi-variable

In simple words, cost has been defined as a sum of total payments or spending amount made

by the firm to produce a specific quantity of goods & service. Smart Looks manufactures clothing

goods for the users, therefore, it incur expenses on three element, material, labour and overheads.

Costs behaviour, as its name, presents the movement in the spending with the increase or decrease

in the final output, mainly categorized into three types mentioned below:

Variable costs: As name implies, it directly moves in the same direction, in which, total

production moves. It means that if Smart looks produce high quantity of clothing goods to meet

exceeding demand then the total variable costs will also go up or vice-versa (Ryan and et.al., 2017).

For instance, high requirement of direct material and more workers will be require maximizing the

production.

Fixed costs: It is just adverse to previous one which does not fluctuate whether Smart looks

exceed or decrease their total output volume. For instance, depreciation, insurance, rent and others

have no relation with the production volume.

Semi-variable/semi-fixed costs: It is a mixture of both the characteristics of fixed &

variable costs because such expenses do not fluctuates till a certain level and afterwards, it changes

in the same direction of production level (Novák and Popesko, 2014). For instance, electricity and

telephone bill payment, Smart Looks can apply high-low method to find out the fixed & variable

portion in the mixed cost.

With the stated scenario, the cost behaviour of different components has been identified here

as under:

Expenditures Type of cost

Clothing material VC

Rent of the factory FC

3

Management accounting is a field or segment of accounting which deals with the

information collection, accounting and reporting it to the management to aware them about the

results of detailed operations in order to make effective plans and decisions in various operational

areas. Smart Looks is a retailing organization that satisfy apparel requirement of the clients by

manufacturing cloths focusing consumer specification. The report emphasize upon costs behaviour,

stock valuation, budgeting planning and controlling and variances analysis in order for making good

decisions for the betterment of the firm.

TASK 1

Q1. (A) Classification of the costs into fixed, variable and semi-variable

In simple words, cost has been defined as a sum of total payments or spending amount made

by the firm to produce a specific quantity of goods & service. Smart Looks manufactures clothing

goods for the users, therefore, it incur expenses on three element, material, labour and overheads.

Costs behaviour, as its name, presents the movement in the spending with the increase or decrease

in the final output, mainly categorized into three types mentioned below:

Variable costs: As name implies, it directly moves in the same direction, in which, total

production moves. It means that if Smart looks produce high quantity of clothing goods to meet

exceeding demand then the total variable costs will also go up or vice-versa (Ryan and et.al., 2017).

For instance, high requirement of direct material and more workers will be require maximizing the

production.

Fixed costs: It is just adverse to previous one which does not fluctuate whether Smart looks

exceed or decrease their total output volume. For instance, depreciation, insurance, rent and others

have no relation with the production volume.

Semi-variable/semi-fixed costs: It is a mixture of both the characteristics of fixed &

variable costs because such expenses do not fluctuates till a certain level and afterwards, it changes

in the same direction of production level (Novák and Popesko, 2014). For instance, electricity and

telephone bill payment, Smart Looks can apply high-low method to find out the fixed & variable

portion in the mixed cost.

With the stated scenario, the cost behaviour of different components has been identified here

as under:

Expenditures Type of cost

Clothing material VC

Rent of the factory FC

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Factory power charged each unit of electricity VC

Supervisors’ wages (Flat plus bonus) Semi-variable

Material for packaging VC

Telephone expense Semi-variable

official rates FC

Payment to driver (Flat rate plus bonus) Semi-variable

Heating FC

(B) Explaining other ways of costs classification

Traceability/chargeability

Direct costs: Expenses which Smart Looks can allocate & assign directly to each unit

produced is called direct costs (DRURY, 2013). For instance, fabric used to make cloth and wages

of the workers who are employed in the production process.

Indirect costs: Unlike above, expenditures incurred on those items which cannot be directly

chargeable to the cloth items manufactured are known as indirect cost i.e. depreciation.

Functions/Activities:

Production/works cost: Expenditures incurred during the manufacturing or production

process are called production cost like production overheads, factory heating & others.

Administration cost: Sum of total payments made for administrating the business functions

are called administrative costs i.e. office stationery, staff salary, printing & other payment (Deegan,

2013).

Selling & distribution cost: All the efforts that are made by Smart looks to maximize their

total turnover are called selling & distribution cost i.e. packaging, marketing, advertisement.

Expenditures Direct and indirect cost Functions/Activities

Clothing material DC WC

Rent of the factory IC WC

Factory power charged each unit of electricity DC WC

Supervisors’ wages (Flat plus bonus) IC WC

Material for packaging DC

Selling and

distribution

Telephone expense IC AC

official rates IC AC

Payment to driver (Flat rate plus bonus) IC AC

Heating IC WC

4

Supervisors’ wages (Flat plus bonus) Semi-variable

Material for packaging VC

Telephone expense Semi-variable

official rates FC

Payment to driver (Flat rate plus bonus) Semi-variable

Heating FC

(B) Explaining other ways of costs classification

Traceability/chargeability

Direct costs: Expenses which Smart Looks can allocate & assign directly to each unit

produced is called direct costs (DRURY, 2013). For instance, fabric used to make cloth and wages

of the workers who are employed in the production process.

Indirect costs: Unlike above, expenditures incurred on those items which cannot be directly

chargeable to the cloth items manufactured are known as indirect cost i.e. depreciation.

Functions/Activities:

Production/works cost: Expenditures incurred during the manufacturing or production

process are called production cost like production overheads, factory heating & others.

Administration cost: Sum of total payments made for administrating the business functions

are called administrative costs i.e. office stationery, staff salary, printing & other payment (Deegan,

2013).

Selling & distribution cost: All the efforts that are made by Smart looks to maximize their

total turnover are called selling & distribution cost i.e. packaging, marketing, advertisement.

Expenditures Direct and indirect cost Functions/Activities

Clothing material DC WC

Rent of the factory IC WC

Factory power charged each unit of electricity DC WC

Supervisors’ wages (Flat plus bonus) IC WC

Material for packaging DC

Selling and

distribution

Telephone expense IC AC

official rates IC AC

Payment to driver (Flat rate plus bonus) IC AC

Heating IC WC

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

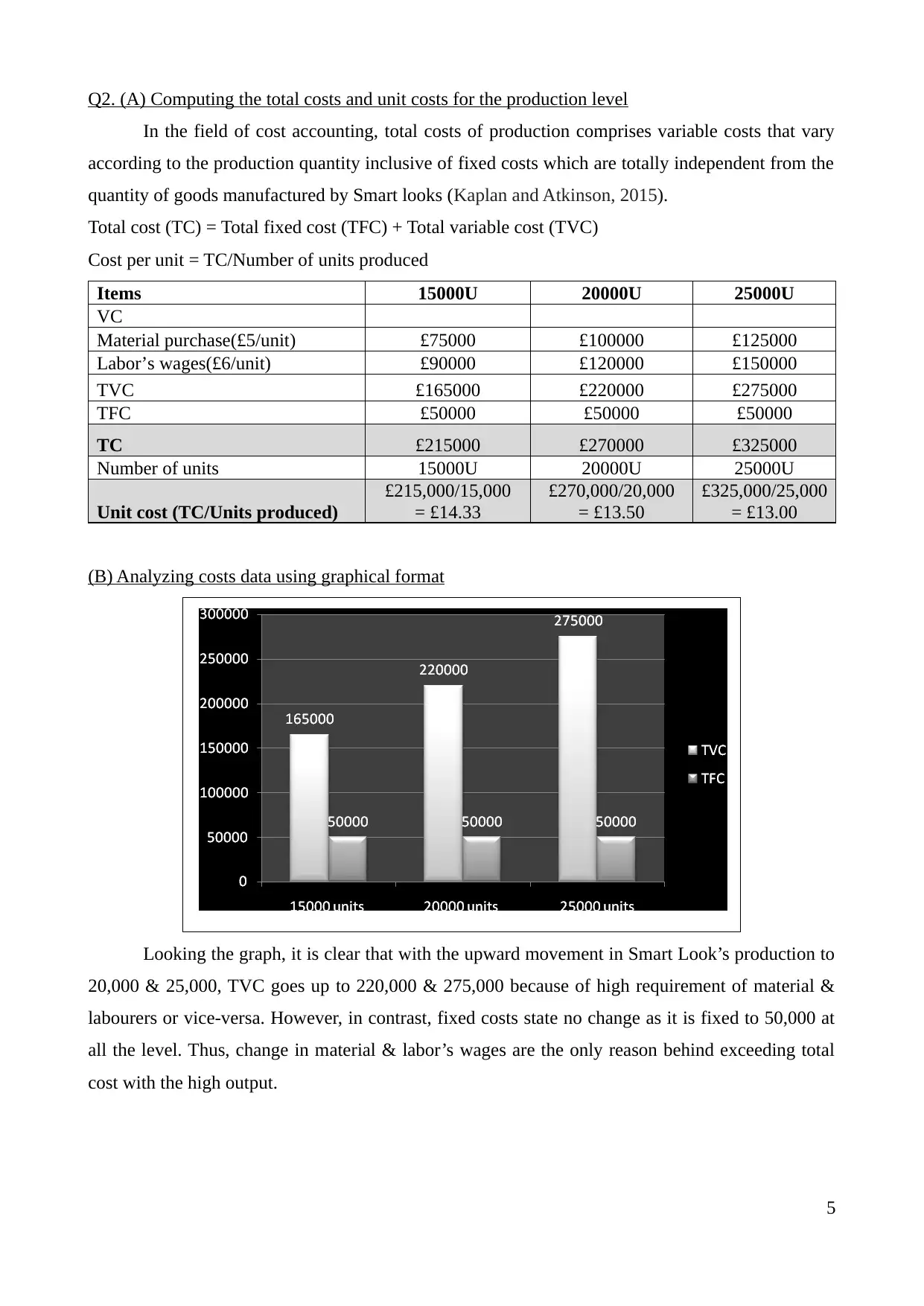

Q2. (A) Computing the total costs and unit costs for the production level

In the field of cost accounting, total costs of production comprises variable costs that vary

according to the production quantity inclusive of fixed costs which are totally independent from the

quantity of goods manufactured by Smart looks (Kaplan and Atkinson, 2015).

Total cost (TC) = Total fixed cost (TFC) + Total variable cost (TVC)

Cost per unit = TC/Number of units produced

Items 15000U 20000U 25000U

VC

Material purchase(£5/unit) £75000 £100000 £125000

Labor’s wages(£6/unit) £90000 £120000 £150000

TVC £165000 £220000 £275000

TFC £50000 £50000 £50000

TC £215000 £270000 £325000

Number of units 15000U 20000U 25000U

Unit cost (TC/Units produced)

£215,000/15,000

= £14.33

£270,000/20,000

= £13.50

£325,000/25,000

= £13.00

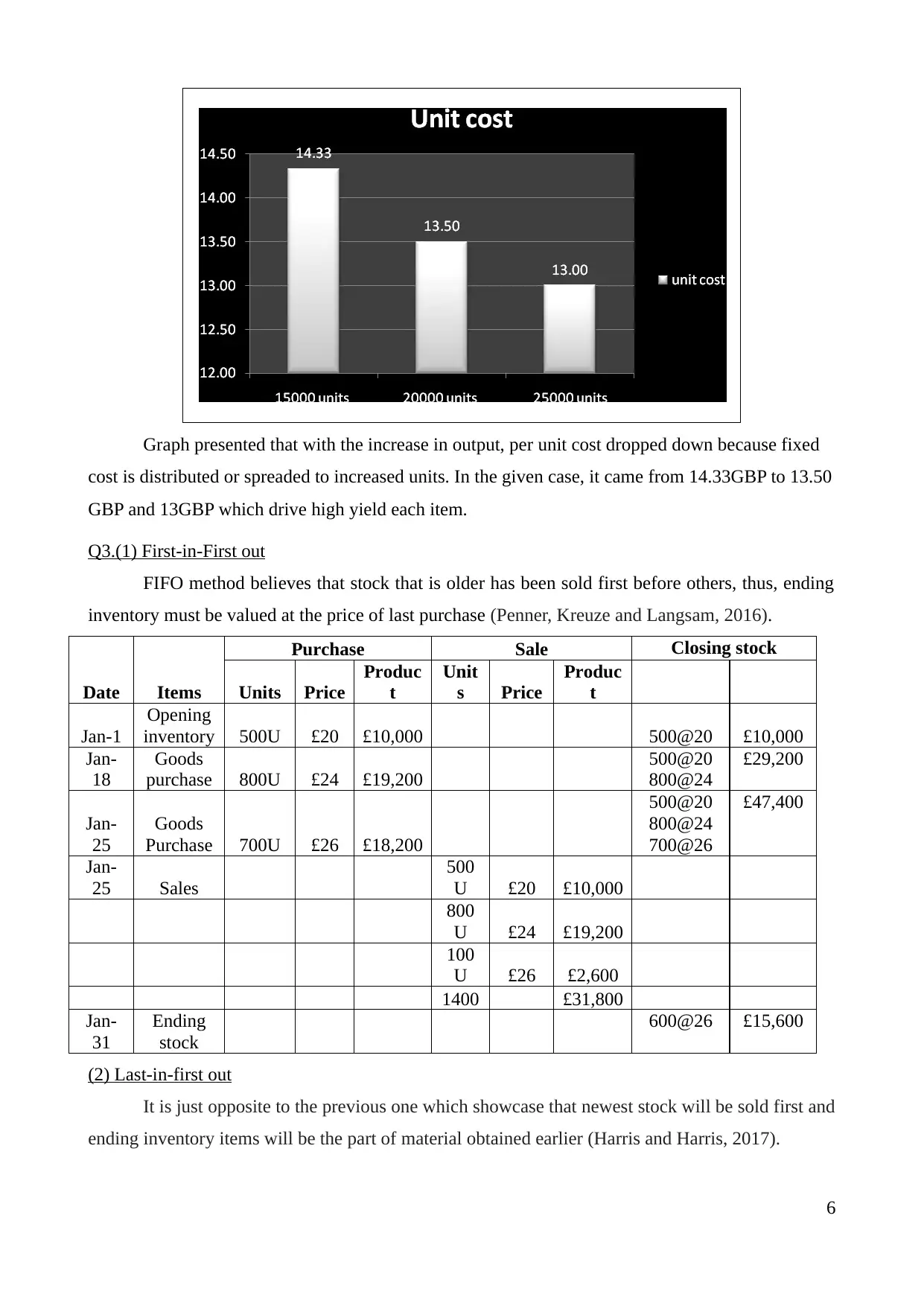

(B) Analyzing costs data using graphical format

Looking the graph, it is clear that with the upward movement in Smart Look’s production to

20,000 & 25,000, TVC goes up to 220,000 & 275,000 because of high requirement of material &

labourers or vice-versa. However, in contrast, fixed costs state no change as it is fixed to 50,000 at

all the level. Thus, change in material & labor’s wages are the only reason behind exceeding total

cost with the high output.

5

In the field of cost accounting, total costs of production comprises variable costs that vary

according to the production quantity inclusive of fixed costs which are totally independent from the

quantity of goods manufactured by Smart looks (Kaplan and Atkinson, 2015).

Total cost (TC) = Total fixed cost (TFC) + Total variable cost (TVC)

Cost per unit = TC/Number of units produced

Items 15000U 20000U 25000U

VC

Material purchase(£5/unit) £75000 £100000 £125000

Labor’s wages(£6/unit) £90000 £120000 £150000

TVC £165000 £220000 £275000

TFC £50000 £50000 £50000

TC £215000 £270000 £325000

Number of units 15000U 20000U 25000U

Unit cost (TC/Units produced)

£215,000/15,000

= £14.33

£270,000/20,000

= £13.50

£325,000/25,000

= £13.00

(B) Analyzing costs data using graphical format

Looking the graph, it is clear that with the upward movement in Smart Look’s production to

20,000 & 25,000, TVC goes up to 220,000 & 275,000 because of high requirement of material &

labourers or vice-versa. However, in contrast, fixed costs state no change as it is fixed to 50,000 at

all the level. Thus, change in material & labor’s wages are the only reason behind exceeding total

cost with the high output.

5

Graph presented that with the increase in output, per unit cost dropped down because fixed

cost is distributed or spreaded to increased units. In the given case, it came from 14.33GBP to 13.50

GBP and 13GBP which drive high yield each item.

Q3.(1) First-in-First out

FIFO method believes that stock that is older has been sold first before others, thus, ending

inventory must be valued at the price of last purchase (Penner, Kreuze and Langsam, 2016).

Date Items

Purchase Sale Closing stock

Units Price

Produc

t

Unit

s Price

Produc

t

Jan-1

Opening

inventory 500U £20 £10,000 500@20 £10,000

Jan-

18

Goods

purchase 800U £24 £19,200

500@20

800@24

£29,200

Jan-

25

Goods

Purchase 700U £26 £18,200

500@20

800@24

700@26

£47,400

Jan-

25 Sales

500

U £20 £10,000

800

U £24 £19,200

100

U £26 £2,600

1400 £31,800

Jan-

31

Ending

stock

600@26 £15,600

(2) Last-in-first out

It is just opposite to the previous one which showcase that newest stock will be sold first and

ending inventory items will be the part of material obtained earlier (Harris and Harris, 2017).

6

cost is distributed or spreaded to increased units. In the given case, it came from 14.33GBP to 13.50

GBP and 13GBP which drive high yield each item.

Q3.(1) First-in-First out

FIFO method believes that stock that is older has been sold first before others, thus, ending

inventory must be valued at the price of last purchase (Penner, Kreuze and Langsam, 2016).

Date Items

Purchase Sale Closing stock

Units Price

Produc

t

Unit

s Price

Produc

t

Jan-1

Opening

inventory 500U £20 £10,000 500@20 £10,000

Jan-

18

Goods

purchase 800U £24 £19,200

500@20

800@24

£29,200

Jan-

25

Goods

Purchase 700U £26 £18,200

500@20

800@24

700@26

£47,400

Jan-

25 Sales

500

U £20 £10,000

800

U £24 £19,200

100

U £26 £2,600

1400 £31,800

Jan-

31

Ending

stock

600@26 £15,600

(2) Last-in-first out

It is just opposite to the previous one which showcase that newest stock will be sold first and

ending inventory items will be the part of material obtained earlier (Harris and Harris, 2017).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Date Items

Purchase Sale Closing stock

Units Price

Produc

t Units

Pric

e

Produc

t

Jan-1

Opening

inventory 500U £20 £10,000 500@20 £10,000

Jan-

18

Goods

purchase 800U £24 £19,200

500@20

800@24

£29,200

Jan-

25

Goods

Purchase 700U £26 £18,200

500@20

800@24

700@26

£47,400

Jan-

25 Sales 700U £26 £18,200

700U £24 £16,800

1400

U £35,000

Jan-

31

Ending

stock

100@24

500@20

£12,400

(3) Average costs method

This technique takes into account the average material prices for valuation of inventory by

using the below presented formula:

Average rates = Total costs/Number of units

Date Items

Purchase Sale Closing stock

Units Price Product Units Price Product Units Price

Produc

t

Jan-1

Opening

inventory 500U £20 £10,000 500 20

£10,00

0

Jan-

18

Goods

purchase 800U £24 £19,200

1,300 29,200/1300

= 22.46

£29,20

0

Jan-

25

Goods

Purchase 700U £26 £18,200

2,000 47,400/2000

= 23.7

£47,40

0

Jan-

25 Sales

1400

U 23.7 £33,180

Jan-

31

Ending

stock

600 23.7 14,220

Q4. Preparing a report presenting costs of goods sold under different inventory methods

Items FIFO LIFO AC method

Units Price COGS Units Price COGS Units Price COGS

Sales on

Jabn-25

500U £20 £10,000 700U £26 £18,200 1400U £23.7 £33,180

800U £24 £19,200 700U £24 £16,800

100U £26 £2,600

COGS 1400 £31,800 1400U £35,000 1400U £23.7 £33,180

Analysis and interpretations: The above table reflects that COGS is identified highest for

7

Purchase Sale Closing stock

Units Price

Produc

t Units

Pric

e

Produc

t

Jan-1

Opening

inventory 500U £20 £10,000 500@20 £10,000

Jan-

18

Goods

purchase 800U £24 £19,200

500@20

800@24

£29,200

Jan-

25

Goods

Purchase 700U £26 £18,200

500@20

800@24

700@26

£47,400

Jan-

25 Sales 700U £26 £18,200

700U £24 £16,800

1400

U £35,000

Jan-

31

Ending

stock

100@24

500@20

£12,400

(3) Average costs method

This technique takes into account the average material prices for valuation of inventory by

using the below presented formula:

Average rates = Total costs/Number of units

Date Items

Purchase Sale Closing stock

Units Price Product Units Price Product Units Price

Produc

t

Jan-1

Opening

inventory 500U £20 £10,000 500 20

£10,00

0

Jan-

18

Goods

purchase 800U £24 £19,200

1,300 29,200/1300

= 22.46

£29,20

0

Jan-

25

Goods

Purchase 700U £26 £18,200

2,000 47,400/2000

= 23.7

£47,40

0

Jan-

25 Sales

1400

U 23.7 £33,180

Jan-

31

Ending

stock

600 23.7 14,220

Q4. Preparing a report presenting costs of goods sold under different inventory methods

Items FIFO LIFO AC method

Units Price COGS Units Price COGS Units Price COGS

Sales on

Jabn-25

500U £20 £10,000 700U £26 £18,200 1400U £23.7 £33,180

800U £24 £19,200 700U £24 £16,800

100U £26 £2,600

COGS 1400 £31,800 1400U £35,000 1400U £23.7 £33,180

Analysis and interpretations: The above table reflects that COGS is identified highest for

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the LIFO method because inventory that Smart Look bought last were purchased at inflated price

(Li and Sun, 2016). However, in FIFO, those goods has been sold first which was bought at less

prices whilst AC used average rates therefore, its COGS has been computed to 33,180 above COGS

under FIFO to 31,800 but below LIFO’s cost of sale to 35,000.

Q5. Indicators to be used for measuring the success

(A) Two critical success factor & KPIs

Customer experience: Best quality products and effective compliant handling system are the

two critical successive factors. It can be measured through using customer satisfaction score as a

key performance indicator.

Supplier and product quality: Qualitative material and prices negotiation can be use as a

critical successive factor and sales performance can be evaluated as KPI.

Operational efficiency: Effective utilization of resources and minimial of wastage are the

two most important factors that leads to drive high operational efficiency (Schipper, Francis and

Weil, 2017).

Reducing maintenance spending: It can be reduced by proper arrangement and maintenance

expenditure percentage as a proportion of sales can be used as a KPI.

Cost reduction and profitability increase: Cost-cutting strategies and sales maximization

are the two prior requirement for exceeding the profitability. Profitability ratio like net profit ratio is

considered as the best KPI for measuring profitability (Zahller, 2017).

(B)(i) Ways to minimize costs

Cost-cutting strategies: Smart Looks managers must look towards development of various

plans such as acquiring material at cheaper rates, recruiting skilled labor force in the production

function at managed wages rate, bargaining with the suppliers and others (Saladrigues and Tena,

2017).

Monitoring and controlling: Tighten the regular function to ensure optimum and efficient

utilization of resources enable managerial team to make strategies and put right control at the right

time through remedial measures and leads to minimize cost.

Technological up-gradation: With the help of advancement of technologies, Smart Looks

can streamline their operations and maximize efficiency, as a result, goods can be produced at less

cost.

High production: Fixed costs is spread to the total production thus, at the excessive

production volume, it will be scattered to the larger number of units, which in turn, per unit cost

goes down and drive high return.

8

(Li and Sun, 2016). However, in FIFO, those goods has been sold first which was bought at less

prices whilst AC used average rates therefore, its COGS has been computed to 33,180 above COGS

under FIFO to 31,800 but below LIFO’s cost of sale to 35,000.

Q5. Indicators to be used for measuring the success

(A) Two critical success factor & KPIs

Customer experience: Best quality products and effective compliant handling system are the

two critical successive factors. It can be measured through using customer satisfaction score as a

key performance indicator.

Supplier and product quality: Qualitative material and prices negotiation can be use as a

critical successive factor and sales performance can be evaluated as KPI.

Operational efficiency: Effective utilization of resources and minimial of wastage are the

two most important factors that leads to drive high operational efficiency (Schipper, Francis and

Weil, 2017).

Reducing maintenance spending: It can be reduced by proper arrangement and maintenance

expenditure percentage as a proportion of sales can be used as a KPI.

Cost reduction and profitability increase: Cost-cutting strategies and sales maximization

are the two prior requirement for exceeding the profitability. Profitability ratio like net profit ratio is

considered as the best KPI for measuring profitability (Zahller, 2017).

(B)(i) Ways to minimize costs

Cost-cutting strategies: Smart Looks managers must look towards development of various

plans such as acquiring material at cheaper rates, recruiting skilled labor force in the production

function at managed wages rate, bargaining with the suppliers and others (Saladrigues and Tena,

2017).

Monitoring and controlling: Tighten the regular function to ensure optimum and efficient

utilization of resources enable managerial team to make strategies and put right control at the right

time through remedial measures and leads to minimize cost.

Technological up-gradation: With the help of advancement of technologies, Smart Looks

can streamline their operations and maximize efficiency, as a result, goods can be produced at less

cost.

High production: Fixed costs is spread to the total production thus, at the excessive

production volume, it will be scattered to the larger number of units, which in turn, per unit cost

goes down and drive high return.

8

(ii) Strategies to enhance value & quality

Quality management techniques: The best way to improve quality is to use quality

management and assurance technique like total quality management, lean operations, six sigma and

others, so that, qualitative goods can be produced (Houtson, 2014).

Wealth maximization: Value can be improved by generating larger return to maximize

wealth for the shareholders. In this regards, Smart Looks’s managerial team must find out unique

ways to maximize revenues and control costs for generating larger return and satisfy the investors.

Competitive advantage: Superior quality clothing goods in attractive designs at an

affordable rates drive millennial consumer base and satisfy customers to a great extent. It drive in

competitive edge over the rivalries and assists firm to effectively run their operations without any

fear of competitive pressure (Zahller, 2017).

Market share: High consumer base leads to drive excessive sales and maximize the market

share. With the help of this, Smart Look will be able to reach their targets successfully.

TASK 2

Q6.

(A) Budget definition

Budgeting is one of the crucial and important aspects of managerial planning & decisions,

under which, Smart look’s managers forecasts the potential results of future course of actions (de

Campos and Rodrigues, 2016). Budgetary planning is a managerial tool which quantitatively

presents possible results of future operations in the form of revenue and expenditures which is

helpful in resource allocation and better corporate planning for the success.

(B) Purpose of budget

Budget is mainly constructed to attain the following aims and objectives, stated hereunder:

Forecasting: The key objective behind preparing budget is that it assists Smart Looks in

projecting the results of potential operations i.e. income that is expected to generate in future and

expenditures that it will incur to carry out their operations.

Decision-making tool: It provides a framework to take proposed course of remedial

measures for maximizing revenues, control cost and improve operational efficiency (Rubin, 2016).

Performance monitoring & controlling: In this, actual results are measured or compared

against the forecasted figures to figure out variances which allow Smart Looks directors to frame

policies and decisions to mitigate adverse results. Moreover, it also assists managerial team in

putting control over their day-to-day functions by making rationalized cost curtailment strategies

9

Quality management techniques: The best way to improve quality is to use quality

management and assurance technique like total quality management, lean operations, six sigma and

others, so that, qualitative goods can be produced (Houtson, 2014).

Wealth maximization: Value can be improved by generating larger return to maximize

wealth for the shareholders. In this regards, Smart Looks’s managerial team must find out unique

ways to maximize revenues and control costs for generating larger return and satisfy the investors.

Competitive advantage: Superior quality clothing goods in attractive designs at an

affordable rates drive millennial consumer base and satisfy customers to a great extent. It drive in

competitive edge over the rivalries and assists firm to effectively run their operations without any

fear of competitive pressure (Zahller, 2017).

Market share: High consumer base leads to drive excessive sales and maximize the market

share. With the help of this, Smart Look will be able to reach their targets successfully.

TASK 2

Q6.

(A) Budget definition

Budgeting is one of the crucial and important aspects of managerial planning & decisions,

under which, Smart look’s managers forecasts the potential results of future course of actions (de

Campos and Rodrigues, 2016). Budgetary planning is a managerial tool which quantitatively

presents possible results of future operations in the form of revenue and expenditures which is

helpful in resource allocation and better corporate planning for the success.

(B) Purpose of budget

Budget is mainly constructed to attain the following aims and objectives, stated hereunder:

Forecasting: The key objective behind preparing budget is that it assists Smart Looks in

projecting the results of potential operations i.e. income that is expected to generate in future and

expenditures that it will incur to carry out their operations.

Decision-making tool: It provides a framework to take proposed course of remedial

measures for maximizing revenues, control cost and improve operational efficiency (Rubin, 2016).

Performance monitoring & controlling: In this, actual results are measured or compared

against the forecasted figures to figure out variances which allow Smart Looks directors to frame

policies and decisions to mitigate adverse results. Moreover, it also assists managerial team in

putting control over their day-to-day functions by making rationalized cost curtailment strategies

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which improve performance.

Motivate workers: In the budget, firm set challenging targets for the workers and on the

basis of their actual results, they are incentivized and promoted (Gurski, Rethmann and Yilmaz,

2017). Thus, in order to take such benefits, staffs feel motivated and put their genuine efforts to

meet set goals.

(C) Different kind of methods for preparation of budget

For making budget, companies can use different techniques, some of the often used

techniques are presented here as under:

Incremental budgeting: IB is a traditional way of setting budgets, under which, either the

historical period’s standard or actual results can be taken as a base and then slightly adjustments can

be incorporated in the same by adding incremental amount to both the income and expenses to

make new budget.

Advantage:

Little changes are made therefore; budget can be designed very easily and quickly.

It does not require much time because market and industry analysis is not required.

It follows the same method of resource allocation on a consistent basis which reduces the

risk of any conflicts among departments.

Drawbacks:

Leads to high spending in the wasteful and unproductive operations

Less-challenging targets for the staff hence do not provide assistance in staff motivation

Zero-based budgeting: It uses zero as base and do not consider last year budget for creating

budget for the new period. ZBB method justifies every revenue and expenditures element by

analysing the market conditions and presents a realistic forecasting for the projected year (Sehgal,

2017).

Advantage:

Optimum and efficient way of resource allocation

Set challenging targets and motivates staff members

Respond external market changes

Drawbacks:

Expertise knowledge is required

Lengthy & time-consuming process

High cost of training (de Campos and Rodrigues, 2016)

Fixed/static budgeting: In this, Smart Looks can only set targets for a specified or fixed

10

Motivate workers: In the budget, firm set challenging targets for the workers and on the

basis of their actual results, they are incentivized and promoted (Gurski, Rethmann and Yilmaz,

2017). Thus, in order to take such benefits, staffs feel motivated and put their genuine efforts to

meet set goals.

(C) Different kind of methods for preparation of budget

For making budget, companies can use different techniques, some of the often used

techniques are presented here as under:

Incremental budgeting: IB is a traditional way of setting budgets, under which, either the

historical period’s standard or actual results can be taken as a base and then slightly adjustments can

be incorporated in the same by adding incremental amount to both the income and expenses to

make new budget.

Advantage:

Little changes are made therefore; budget can be designed very easily and quickly.

It does not require much time because market and industry analysis is not required.

It follows the same method of resource allocation on a consistent basis which reduces the

risk of any conflicts among departments.

Drawbacks:

Leads to high spending in the wasteful and unproductive operations

Less-challenging targets for the staff hence do not provide assistance in staff motivation

Zero-based budgeting: It uses zero as base and do not consider last year budget for creating

budget for the new period. ZBB method justifies every revenue and expenditures element by

analysing the market conditions and presents a realistic forecasting for the projected year (Sehgal,

2017).

Advantage:

Optimum and efficient way of resource allocation

Set challenging targets and motivates staff members

Respond external market changes

Drawbacks:

Expertise knowledge is required

Lengthy & time-consuming process

High cost of training (de Campos and Rodrigues, 2016)

Fixed/static budgeting: In this, Smart Looks can only set targets for a specified or fixed

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production level and cannot be altered accordingly to the actual output.

Advantage:

Easier implementation

Helpful in examining over and under-estimation of revenue and costs

Drawbacks:

Lack of flexibility

Not helpful in comparative analysis between actual and standard goals

Flexible/variable budgeting: Many companies prepare flexible budgets in order to adapt

and respond to the changing conditions i.e. inflation. It is comparatively superior then static budget

because target can be flexed easily on the basis of actual production output.

Advantage:

Respond to market change

Easy to adjust budget as per the actual output

Helpful in better controlling

Drawbacks:

Continuous monitoring is required which is a time-consuming process

Lack of information availability may leads to set inaccurate targets (Davoren, 2013)

Complexities and difficulties in adjustments

Recommendation: Considering all the methods, Smart looks can be suggested to follow

ZBB although, it requires extensive research and takes time, but, realistic targets with right

justifications can be ensured which is the key objective of budgetary planning.

Q7.

(A) Sales budget

This budget helps to find out the total number of units along with the sales prices so as to

figure out the potential sales amount that Smart Looks will obtain from their target customer base

(Schipper, Francis and Weil, 2017).

Sales budget

Items April May June

Total units expected to sale £2,000.00 £1,500.00 £2,500.00

*Unit sales price £30.00 £30.00 £30.00

Total sales £60,000.00 £45,000.00 £75,000.00

(B) Production budget

In order to generate expected sales, Smart Look’s production department has to make proper

planning regarding their production function (Saladrigues and Tena, 2017). This budget facilitates

11

Advantage:

Easier implementation

Helpful in examining over and under-estimation of revenue and costs

Drawbacks:

Lack of flexibility

Not helpful in comparative analysis between actual and standard goals

Flexible/variable budgeting: Many companies prepare flexible budgets in order to adapt

and respond to the changing conditions i.e. inflation. It is comparatively superior then static budget

because target can be flexed easily on the basis of actual production output.

Advantage:

Respond to market change

Easy to adjust budget as per the actual output

Helpful in better controlling

Drawbacks:

Continuous monitoring is required which is a time-consuming process

Lack of information availability may leads to set inaccurate targets (Davoren, 2013)

Complexities and difficulties in adjustments

Recommendation: Considering all the methods, Smart looks can be suggested to follow

ZBB although, it requires extensive research and takes time, but, realistic targets with right

justifications can be ensured which is the key objective of budgetary planning.

Q7.

(A) Sales budget

This budget helps to find out the total number of units along with the sales prices so as to

figure out the potential sales amount that Smart Looks will obtain from their target customer base

(Schipper, Francis and Weil, 2017).

Sales budget

Items April May June

Total units expected to sale £2,000.00 £1,500.00 £2,500.00

*Unit sales price £30.00 £30.00 £30.00

Total sales £60,000.00 £45,000.00 £75,000.00

(B) Production budget

In order to generate expected sales, Smart Look’s production department has to make proper

planning regarding their production function (Saladrigues and Tena, 2017). This budget facilitates

11

manager to find out the total number of units that it has to manufacture to meet the demand of

consumers.

Production budget

Items April May June

Number of units expected to sale 2000 1500 2500

Add: Ending inventory 150 250 100

Less: Opening inventory 100

Units required to produce 2050 1750 2600

(C) Raw material budget

As its name, this budget provides information about the material requirement and its price, so

that, firm can find out the total cost that it will incur on material purchase.

Raw material budget

Items April May June

Material (in meter, 5 meter/unit) 10250 8750 13000

Add; Ending material 750 1000 1200

Less; Beginning material 500

Quantity of material required to produce 10500 9750 14200

Material price/per meter £1.50 £1.50 £1.50

Cost of material £15,750.00 £14,625.00 £21,300.00

(D) Labour budget

It provides an insight to the management about the expenditures that firm will incur to pay

wages to the workers for their efforts made.

Labor budget

Items April May June

Units required to produce 2050 1750 2600

Hrs required to produce one unit 1.5 1.5 1.5

Total labor hors 3075 2625 3900

Rate/hour £6.00 £6.00 £6.00

Total cost of labor £18,450.00 £15,750.00 £23,400.00

(E) Total overheads budget

Besides material and labour, Smart Looks also incur expenditures on the overheads which

may be either fixed or fluctuating/variable cost (Zahller, 2017). Overhead budget forecast the

amount of total overheads that company will incur in the forthcoming period.

Total overheads budget

Items April May June

Number of production units 2050 1750 2600

Variable hrs/unit 1.5 1.5 1.5

Hrs 3075 2625 3900

*overhead rate/unit £3.00 £3.00 £3.00

Total variable expenses £9,225.00 £7,875.00 £11,700.00

12

consumers.

Production budget

Items April May June

Number of units expected to sale 2000 1500 2500

Add: Ending inventory 150 250 100

Less: Opening inventory 100

Units required to produce 2050 1750 2600

(C) Raw material budget

As its name, this budget provides information about the material requirement and its price, so

that, firm can find out the total cost that it will incur on material purchase.

Raw material budget

Items April May June

Material (in meter, 5 meter/unit) 10250 8750 13000

Add; Ending material 750 1000 1200

Less; Beginning material 500

Quantity of material required to produce 10500 9750 14200

Material price/per meter £1.50 £1.50 £1.50

Cost of material £15,750.00 £14,625.00 £21,300.00

(D) Labour budget

It provides an insight to the management about the expenditures that firm will incur to pay

wages to the workers for their efforts made.

Labor budget

Items April May June

Units required to produce 2050 1750 2600

Hrs required to produce one unit 1.5 1.5 1.5

Total labor hors 3075 2625 3900

Rate/hour £6.00 £6.00 £6.00

Total cost of labor £18,450.00 £15,750.00 £23,400.00

(E) Total overheads budget

Besides material and labour, Smart Looks also incur expenditures on the overheads which

may be either fixed or fluctuating/variable cost (Zahller, 2017). Overhead budget forecast the

amount of total overheads that company will incur in the forthcoming period.

Total overheads budget

Items April May June

Number of production units 2050 1750 2600

Variable hrs/unit 1.5 1.5 1.5

Hrs 3075 2625 3900

*overhead rate/unit £3.00 £3.00 £3.00

Total variable expenses £9,225.00 £7,875.00 £11,700.00

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.