Management Accounting Report: Costing Methods and Budgetary Control

VerifiedAdded on 2020/06/06

|10

|2779

|871

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on costing methods, budgetary control, and financial analysis. The report begins by examining different costing methods, including fixed and variable costs, historical costs, absorption costing, and marginal costing, with calculations and comparisons. It then explores various management accounting techniques and their application in business organizations. The report also delves into the advantages and disadvantages of planning tools in budgetary control, such as forecasting, scenario planning, and contingency tools. Furthermore, it includes an evaluation of expenses and a cash budget. Finally, the report addresses the adoption of accounting systems to determine financial issues, evaluates crucial measures to overcome these issues, and assesses the planning tools used in management accounting, offering insights into financial ratios like ROCE, operating profit margin, and asset turnover for two hypothetical companies. This report is ideal for students seeking to understand financial management and accounting principles.

Management Accounting

PART 2

PART 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1: Calculation of cost by using appropriate methods...............................................................3

1.2: Various range of management accounting techniques and develop a document ................5

1.3: Data interpretation by using costing methods which is used in an organisation.................5

TASK 2............................................................................................................................................5

2.1: Advantages and disadvantages of using planning tools in budgetary control ....................5

2.2: Evaluation of expenses for July and August........................................................................7

2.3: Cash budget .........................................................................................................................7

TASK 3............................................................................................................................................8

3.1: Adoption of accounting system to determine financial issues............................................8

3.2: Evaluating crucial measure to overcome financial issues of both the company .................9

3.3: Evaluating planning tools used in management accounting................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1: Calculation of cost by using appropriate methods...............................................................3

1.2: Various range of management accounting techniques and develop a document ................5

1.3: Data interpretation by using costing methods which is used in an organisation.................5

TASK 2............................................................................................................................................5

2.1: Advantages and disadvantages of using planning tools in budgetary control ....................5

2.2: Evaluation of expenses for July and August........................................................................7

2.3: Cash budget .........................................................................................................................7

TASK 3............................................................................................................................................8

3.1: Adoption of accounting system to determine financial issues............................................8

3.2: Evaluating crucial measure to overcome financial issues of both the company .................9

3.3: Evaluating planning tools used in management accounting................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

In recent times, management is searching for some effective system that can helpful them

to manage and control their every financial or non-financial transaction in appropriate manner.

The process of preparing administrative reports and various crucial information that would

provide accurate and reliable outcome for the company. One of the major profession that consists

of positive relation in management decision making and deliver expertise financial reporting to

build strong organisational strategies. This particular part is mostly focus on merits and demerits

of using planning tools that are effectively helpful in budgetary control. Identification of

financial issues and vital measure to overcomes those issues are discuss under this report

(Bennett, Schaltegger and Zvezdov, 2013).

TASK 1

1.1: Calculation of cost by using appropriate methods

In order to get more positive outcomes as net profit manager need to make use of

effective costing systems. These are mostly associated with production of products and services.

All the costs are either directly or indirectly related with them. Cost would be generally an

important part of every manufacturing business whether it is small or large. It is the value of

money charged for getting something. Costing is a systematic method of accounting which will

helpful in assembling and recording every component of cost those are incurred for the purpose

of accomplish a particular objectives. There are various costs which will helpful in evaluating

total costs for an organisation. Some of them are discuss underneath:

Fixed and variable costs: A cost which remain unchanged in total volume changes but

varies only on a per units basis with the increase or decrease in cost driver. Like for examples,

amortization and insurance premium. Whereas, variable costs are those costs that are constant as

per unit but modify in total production changes in output. Some crucial examples are fuel

expenses and output material (Boyns and Edwards, 2013).

Historical costs: It has been seen that assets would be indicated on the balance sheet at

their original costs of purchase instead of present value. The total cost of fixed costs are included

at the time when actually the acquisition is made. It is more consistency with current value of

resources that is being employed in an organisation.

3

In recent times, management is searching for some effective system that can helpful them

to manage and control their every financial or non-financial transaction in appropriate manner.

The process of preparing administrative reports and various crucial information that would

provide accurate and reliable outcome for the company. One of the major profession that consists

of positive relation in management decision making and deliver expertise financial reporting to

build strong organisational strategies. This particular part is mostly focus on merits and demerits

of using planning tools that are effectively helpful in budgetary control. Identification of

financial issues and vital measure to overcomes those issues are discuss under this report

(Bennett, Schaltegger and Zvezdov, 2013).

TASK 1

1.1: Calculation of cost by using appropriate methods

In order to get more positive outcomes as net profit manager need to make use of

effective costing systems. These are mostly associated with production of products and services.

All the costs are either directly or indirectly related with them. Cost would be generally an

important part of every manufacturing business whether it is small or large. It is the value of

money charged for getting something. Costing is a systematic method of accounting which will

helpful in assembling and recording every component of cost those are incurred for the purpose

of accomplish a particular objectives. There are various costs which will helpful in evaluating

total costs for an organisation. Some of them are discuss underneath:

Fixed and variable costs: A cost which remain unchanged in total volume changes but

varies only on a per units basis with the increase or decrease in cost driver. Like for examples,

amortization and insurance premium. Whereas, variable costs are those costs that are constant as

per unit but modify in total production changes in output. Some crucial examples are fuel

expenses and output material (Boyns and Edwards, 2013).

Historical costs: It has been seen that assets would be indicated on the balance sheet at

their original costs of purchase instead of present value. The total cost of fixed costs are included

at the time when actually the acquisition is made. It is more consistency with current value of

resources that is being employed in an organisation.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

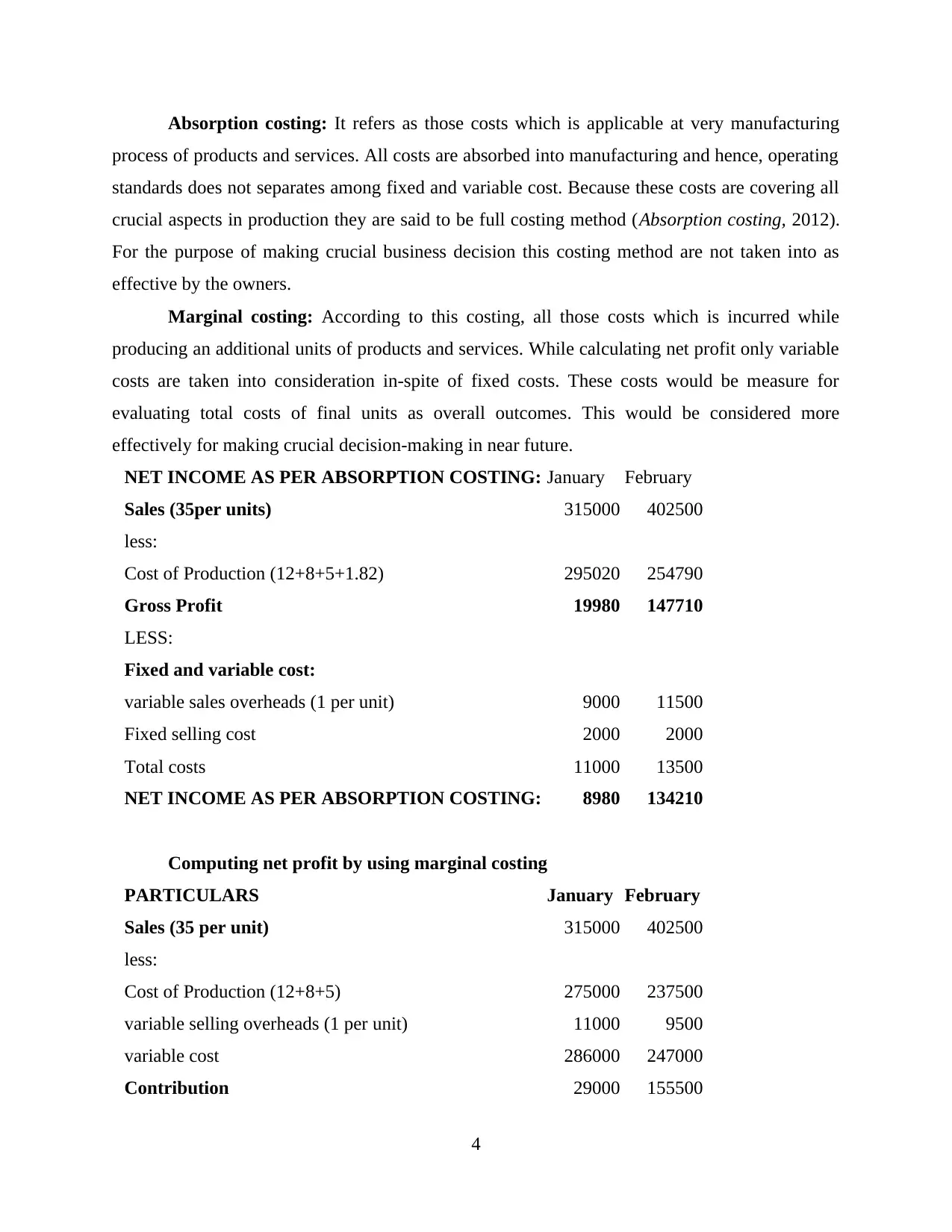

Absorption costing: It refers as those costs which is applicable at very manufacturing

process of products and services. All costs are absorbed into manufacturing and hence, operating

standards does not separates among fixed and variable cost. Because these costs are covering all

crucial aspects in production they are said to be full costing method (Absorption costing, 2012).

For the purpose of making crucial business decision this costing method are not taken into as

effective by the owners.

Marginal costing: According to this costing, all those costs which is incurred while

producing an additional units of products and services. While calculating net profit only variable

costs are taken into consideration in-spite of fixed costs. These costs would be measure for

evaluating total costs of final units as overall outcomes. This would be considered more

effectively for making crucial decision-making in near future.

NET INCOME AS PER ABSORPTION COSTING: January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

Computing net profit by using marginal costing

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

4

process of products and services. All costs are absorbed into manufacturing and hence, operating

standards does not separates among fixed and variable cost. Because these costs are covering all

crucial aspects in production they are said to be full costing method (Absorption costing, 2012).

For the purpose of making crucial business decision this costing method are not taken into as

effective by the owners.

Marginal costing: According to this costing, all those costs which is incurred while

producing an additional units of products and services. While calculating net profit only variable

costs are taken into consideration in-spite of fixed costs. These costs would be measure for

evaluating total costs of final units as overall outcomes. This would be considered more

effectively for making crucial decision-making in near future.

NET INCOME AS PER ABSORPTION COSTING: January February

Sales (35per units) 315000 402500

less:

Cost of Production (12+8+5+1.82) 295020 254790

Gross Profit 19980 147710

LESS:

Fixed and variable cost:

variable sales overheads (1 per unit) 9000 11500

Fixed selling cost 2000 2000

Total costs 11000 13500

NET INCOME AS PER ABSORPTION COSTING: 8980 134210

Computing net profit by using marginal costing

PARTICULARS January February

Sales (35 per unit) 315000 402500

less:

Cost of Production (12+8+5) 275000 237500

variable selling overheads (1 per unit) 11000 9500

variable cost 286000 247000

Contribution 29000 155500

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

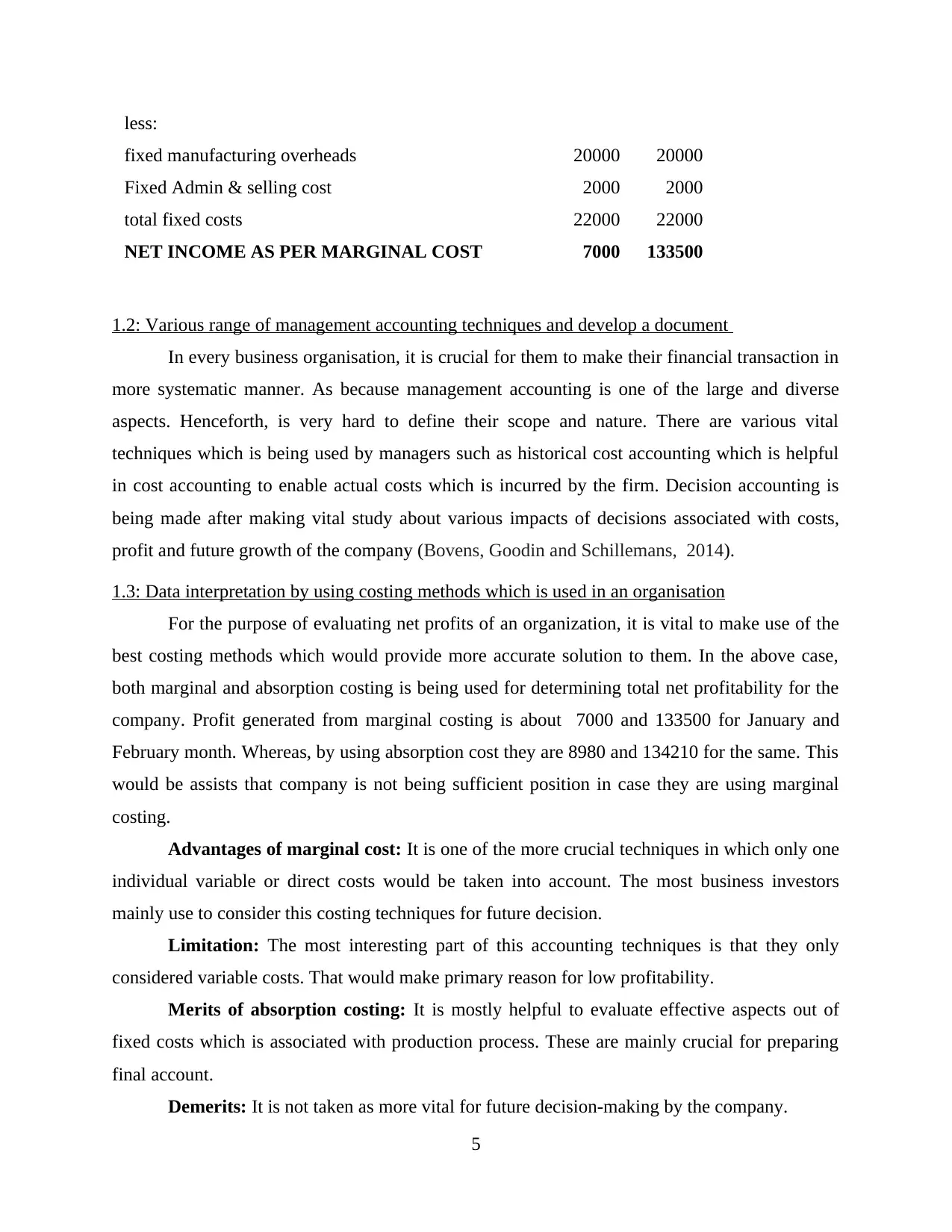

less:

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

1.2: Various range of management accounting techniques and develop a document

In every business organisation, it is crucial for them to make their financial transaction in

more systematic manner. As because management accounting is one of the large and diverse

aspects. Henceforth, is very hard to define their scope and nature. There are various vital

techniques which is being used by managers such as historical cost accounting which is helpful

in cost accounting to enable actual costs which is incurred by the firm. Decision accounting is

being made after making vital study about various impacts of decisions associated with costs,

profit and future growth of the company (Bovens, Goodin and Schillemans, 2014).

1.3: Data interpretation by using costing methods which is used in an organisation

For the purpose of evaluating net profits of an organization, it is vital to make use of the

best costing methods which would provide more accurate solution to them. In the above case,

both marginal and absorption costing is being used for determining total net profitability for the

company. Profit generated from marginal costing is about 7000 and 133500 for January and

February month. Whereas, by using absorption cost they are 8980 and 134210 for the same. This

would be assists that company is not being sufficient position in case they are using marginal

costing.

Advantages of marginal cost: It is one of the more crucial techniques in which only one

individual variable or direct costs would be taken into account. The most business investors

mainly use to consider this costing techniques for future decision.

Limitation: The most interesting part of this accounting techniques is that they only

considered variable costs. That would make primary reason for low profitability.

Merits of absorption costing: It is mostly helpful to evaluate effective aspects out of

fixed costs which is associated with production process. These are mainly crucial for preparing

final account.

Demerits: It is not taken as more vital for future decision-making by the company.

5

fixed manufacturing overheads 20000 20000

Fixed Admin & selling cost 2000 2000

total fixed costs 22000 22000

NET INCOME AS PER MARGINAL COST 7000 133500

1.2: Various range of management accounting techniques and develop a document

In every business organisation, it is crucial for them to make their financial transaction in

more systematic manner. As because management accounting is one of the large and diverse

aspects. Henceforth, is very hard to define their scope and nature. There are various vital

techniques which is being used by managers such as historical cost accounting which is helpful

in cost accounting to enable actual costs which is incurred by the firm. Decision accounting is

being made after making vital study about various impacts of decisions associated with costs,

profit and future growth of the company (Bovens, Goodin and Schillemans, 2014).

1.3: Data interpretation by using costing methods which is used in an organisation

For the purpose of evaluating net profits of an organization, it is vital to make use of the

best costing methods which would provide more accurate solution to them. In the above case,

both marginal and absorption costing is being used for determining total net profitability for the

company. Profit generated from marginal costing is about 7000 and 133500 for January and

February month. Whereas, by using absorption cost they are 8980 and 134210 for the same. This

would be assists that company is not being sufficient position in case they are using marginal

costing.

Advantages of marginal cost: It is one of the more crucial techniques in which only one

individual variable or direct costs would be taken into account. The most business investors

mainly use to consider this costing techniques for future decision.

Limitation: The most interesting part of this accounting techniques is that they only

considered variable costs. That would make primary reason for low profitability.

Merits of absorption costing: It is mostly helpful to evaluate effective aspects out of

fixed costs which is associated with production process. These are mainly crucial for preparing

final account.

Demerits: It is not taken as more vital for future decision-making by the company.

5

TASK 2

2.1: Advantages and disadvantages of using planning tools in budgetary control

Planning is utmost important part of every manufacturing business enterprises. They need

to perform certain types of business activities in order to generate maximum benefits. Every

activity must concluded with expense and incomes of UCK group of company. The primary aim

of the company is always help to make sure that the expenses does not reverse its revenue and

for that UCK group always tried to make appropriate budgets that will control their everyday

transactions. The process of budgetary control is utilise by the company in order to manage their

future estimation about total costs and expenses. In accordance with this, various kinds of

expenses prevailing in UCK group company such as cash flow expenses, capital and revenue

expenditure or so on. Some crucial budgets are sales, production and raw material budgets. An

effective budget would also assists the company to keep regular overlook of total workforce and

examine whether work is going right direction. In order to make budgets for the company

various planning tools are taken into consideration by the accounts managers. These techniques

are helpful in forecasting future growth and financial stability for the company. Some of them

are discuss underneath:

Forecasting tools: It is mostly seen in an organisation that they always plan to make

forecasted in order to attain efficiency in internal department performance. A company can

accurately held responsible for estimating better results in terms of total sales and revenue. This

will lead to create better image in front of various competitors (Hansen, 2011).

Merits: It would assist managers to make forecasting for future through making right

direction in the way company can attain their aims and objectives. As, demand of customers kept

changing which would help the company to make their creative products to an organisation.

Demerits: As forecasting is done through estimation and henceforth it cannot be accurate

and reliable in every case.

Scenario tools: The another planning tools is scenario strategies which tries to make

focus on the outlook for the future estimation. It is more vital tools by which UCK group of

company can form a positive idea for predicting future situations.

Advantages: It is one of the most creative planning which is more suits as per the given

situation in an organisation. It would deal with all those crucial aspects that remain uncertain.

6

2.1: Advantages and disadvantages of using planning tools in budgetary control

Planning is utmost important part of every manufacturing business enterprises. They need

to perform certain types of business activities in order to generate maximum benefits. Every

activity must concluded with expense and incomes of UCK group of company. The primary aim

of the company is always help to make sure that the expenses does not reverse its revenue and

for that UCK group always tried to make appropriate budgets that will control their everyday

transactions. The process of budgetary control is utilise by the company in order to manage their

future estimation about total costs and expenses. In accordance with this, various kinds of

expenses prevailing in UCK group company such as cash flow expenses, capital and revenue

expenditure or so on. Some crucial budgets are sales, production and raw material budgets. An

effective budget would also assists the company to keep regular overlook of total workforce and

examine whether work is going right direction. In order to make budgets for the company

various planning tools are taken into consideration by the accounts managers. These techniques

are helpful in forecasting future growth and financial stability for the company. Some of them

are discuss underneath:

Forecasting tools: It is mostly seen in an organisation that they always plan to make

forecasted in order to attain efficiency in internal department performance. A company can

accurately held responsible for estimating better results in terms of total sales and revenue. This

will lead to create better image in front of various competitors (Hansen, 2011).

Merits: It would assist managers to make forecasting for future through making right

direction in the way company can attain their aims and objectives. As, demand of customers kept

changing which would help the company to make their creative products to an organisation.

Demerits: As forecasting is done through estimation and henceforth it cannot be accurate

and reliable in every case.

Scenario tools: The another planning tools is scenario strategies which tries to make

focus on the outlook for the future estimation. It is more vital tools by which UCK group of

company can form a positive idea for predicting future situations.

Advantages: It is one of the most creative planning which is more suits as per the given

situation in an organisation. It would deal with all those crucial aspects that remain uncertain.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Demerits: As per this planning techniques cannot accurately predict their future because

it is based on assumptions. It is too costly to implement this types of planning tool.

Contingency tools: An organisation always faces certain types of risks which are

associated with uncertain activities. These activities can be arise from external as well as internal

contingencies such as fire occurred at the factory and some other aspects.

Merits: By the help of proper plan which would be applicable in contingency situations

in best suitable manner. Because risk are uncertain and cannot be resolve early. The role of

managers are well assigned in perfect manner before any contingencies arises.

Demerits: It is reactive methods of business management (Kihn and Ihantola, 2015).

2.2: Evaluation of expenses for July and August

In order to calculate variable cost per units in order to determine high and low activity

stage.

(Total expenditure of high activity – Expenditure from low activity)

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total expenditure (Per units): (9820-7410) / 795-505)=8.31

Total expenses for July:

= 650*8.31= 5401.5

For August:

= 750*8.31= 6232.5

2.3: Cash budget

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Less:

Purchase -16800

7

it is based on assumptions. It is too costly to implement this types of planning tool.

Contingency tools: An organisation always faces certain types of risks which are

associated with uncertain activities. These activities can be arise from external as well as internal

contingencies such as fire occurred at the factory and some other aspects.

Merits: By the help of proper plan which would be applicable in contingency situations

in best suitable manner. Because risk are uncertain and cannot be resolve early. The role of

managers are well assigned in perfect manner before any contingencies arises.

Demerits: It is reactive methods of business management (Kihn and Ihantola, 2015).

2.2: Evaluation of expenses for July and August

In order to calculate variable cost per units in order to determine high and low activity

stage.

(Total expenditure of high activity – Expenditure from low activity)

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total expenditure (Per units): (9820-7410) / 795-505)=8.31

Total expenses for July:

= 650*8.31= 5401.5

For August:

= 750*8.31= 6232.5

2.3: Cash budget

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

Less:

Purchase -16800

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash at the end of

September month 6848

TASK 3

3.1: Adoption of accounting system to determine financial issues

In every business like UCK group is working in formulating various issues which will

leads to make huge implications over the ratio of an organisation.

Ratios Formula UCK furnitures UCK woodworks

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+31

930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/13000+24900*1

00

=25.03%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/23106+

31930

=0.68 times

8150/81230

=0.100 times

UCK Furnitures UCK WOODWORKDS

It is mostly related with producing only one

products which is desks.

They are held responsible for providing

valuable material to UCK furnitures.

As per the ROCE ratio, it has been seen that Under this company, just 8.56% of total return

8

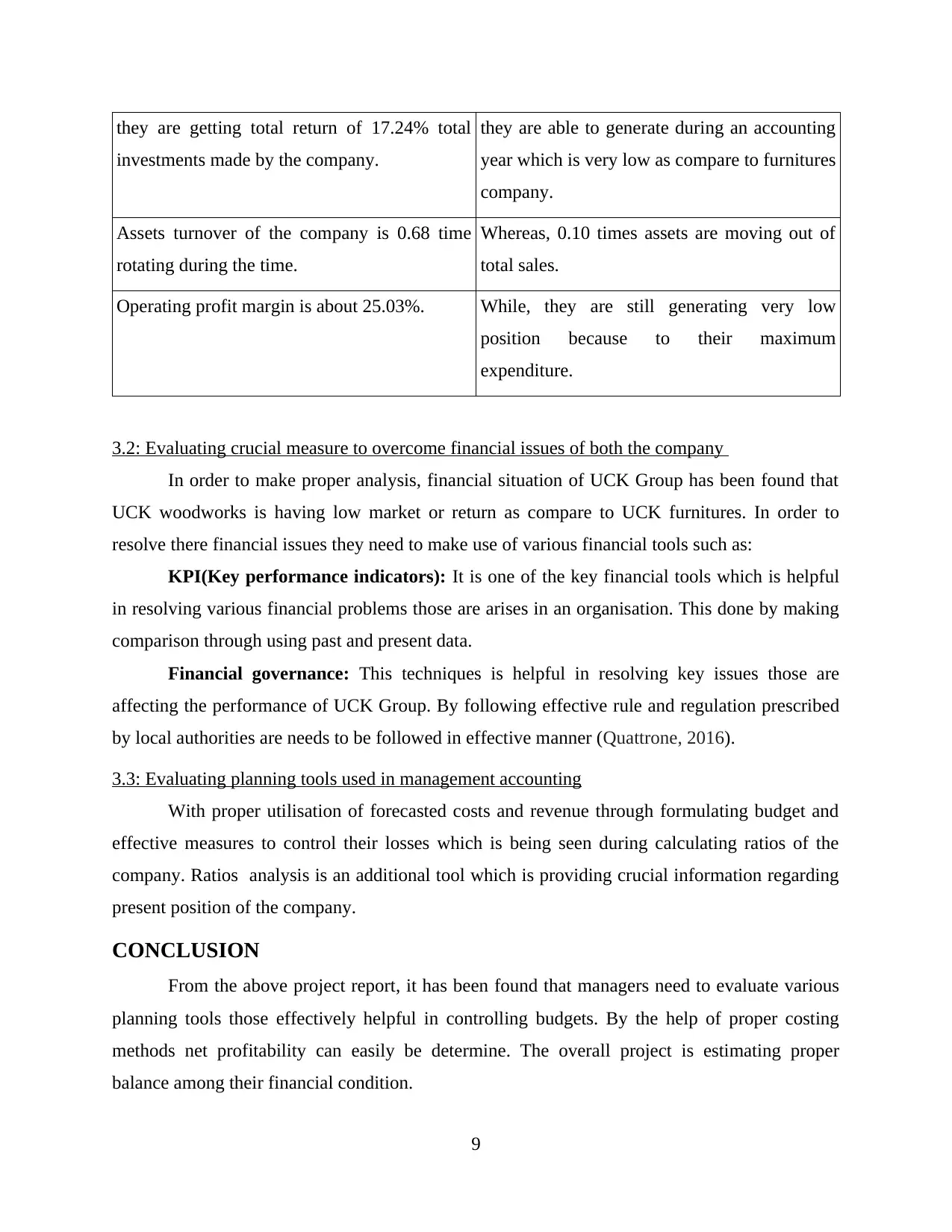

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash at the end of

September month 6848

TASK 3

3.1: Adoption of accounting system to determine financial issues

In every business like UCK group is working in formulating various issues which will

leads to make huge implications over the ratio of an organisation.

Ratios Formula UCK furnitures UCK woodworks

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+31

930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/13000+24900*1

00

=25.03%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/23106+

31930

=0.68 times

8150/81230

=0.100 times

UCK Furnitures UCK WOODWORKDS

It is mostly related with producing only one

products which is desks.

They are held responsible for providing

valuable material to UCK furnitures.

As per the ROCE ratio, it has been seen that Under this company, just 8.56% of total return

8

they are getting total return of 17.24% total

investments made by the company.

they are able to generate during an accounting

year which is very low as compare to furnitures

company.

Assets turnover of the company is 0.68 time

rotating during the time.

Whereas, 0.10 times assets are moving out of

total sales.

Operating profit margin is about 25.03%. While, they are still generating very low

position because to their maximum

expenditure.

3.2: Evaluating crucial measure to overcome financial issues of both the company

In order to make proper analysis, financial situation of UCK Group has been found that

UCK woodworks is having low market or return as compare to UCK furnitures. In order to

resolve there financial issues they need to make use of various financial tools such as:

KPI(Key performance indicators): It is one of the key financial tools which is helpful

in resolving various financial problems those are arises in an organisation. This done by making

comparison through using past and present data.

Financial governance: This techniques is helpful in resolving key issues those are

affecting the performance of UCK Group. By following effective rule and regulation prescribed

by local authorities are needs to be followed in effective manner (Quattrone, 2016).

3.3: Evaluating planning tools used in management accounting

With proper utilisation of forecasted costs and revenue through formulating budget and

effective measures to control their losses which is being seen during calculating ratios of the

company. Ratios analysis is an additional tool which is providing crucial information regarding

present position of the company.

CONCLUSION

From the above project report, it has been found that managers need to evaluate various

planning tools those effectively helpful in controlling budgets. By the help of proper costing

methods net profitability can easily be determine. The overall project is estimating proper

balance among their financial condition.

9

investments made by the company.

they are able to generate during an accounting

year which is very low as compare to furnitures

company.

Assets turnover of the company is 0.68 time

rotating during the time.

Whereas, 0.10 times assets are moving out of

total sales.

Operating profit margin is about 25.03%. While, they are still generating very low

position because to their maximum

expenditure.

3.2: Evaluating crucial measure to overcome financial issues of both the company

In order to make proper analysis, financial situation of UCK Group has been found that

UCK woodworks is having low market or return as compare to UCK furnitures. In order to

resolve there financial issues they need to make use of various financial tools such as:

KPI(Key performance indicators): It is one of the key financial tools which is helpful

in resolving various financial problems those are arises in an organisation. This done by making

comparison through using past and present data.

Financial governance: This techniques is helpful in resolving key issues those are

affecting the performance of UCK Group. By following effective rule and regulation prescribed

by local authorities are needs to be followed in effective manner (Quattrone, 2016).

3.3: Evaluating planning tools used in management accounting

With proper utilisation of forecasted costs and revenue through formulating budget and

effective measures to control their losses which is being seen during calculating ratios of the

company. Ratios analysis is an additional tool which is providing crucial information regarding

present position of the company.

CONCLUSION

From the above project report, it has been found that managers need to evaluate various

planning tools those effectively helpful in controlling budgets. By the help of proper costing

methods net profitability can easily be determine. The overall project is estimating proper

balance among their financial condition.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.