Applying Management Accounting Techniques: Cost Analysis & Budgeting

VerifiedAdded on 2023/04/19

|8

|982

|148

Report

AI Summary

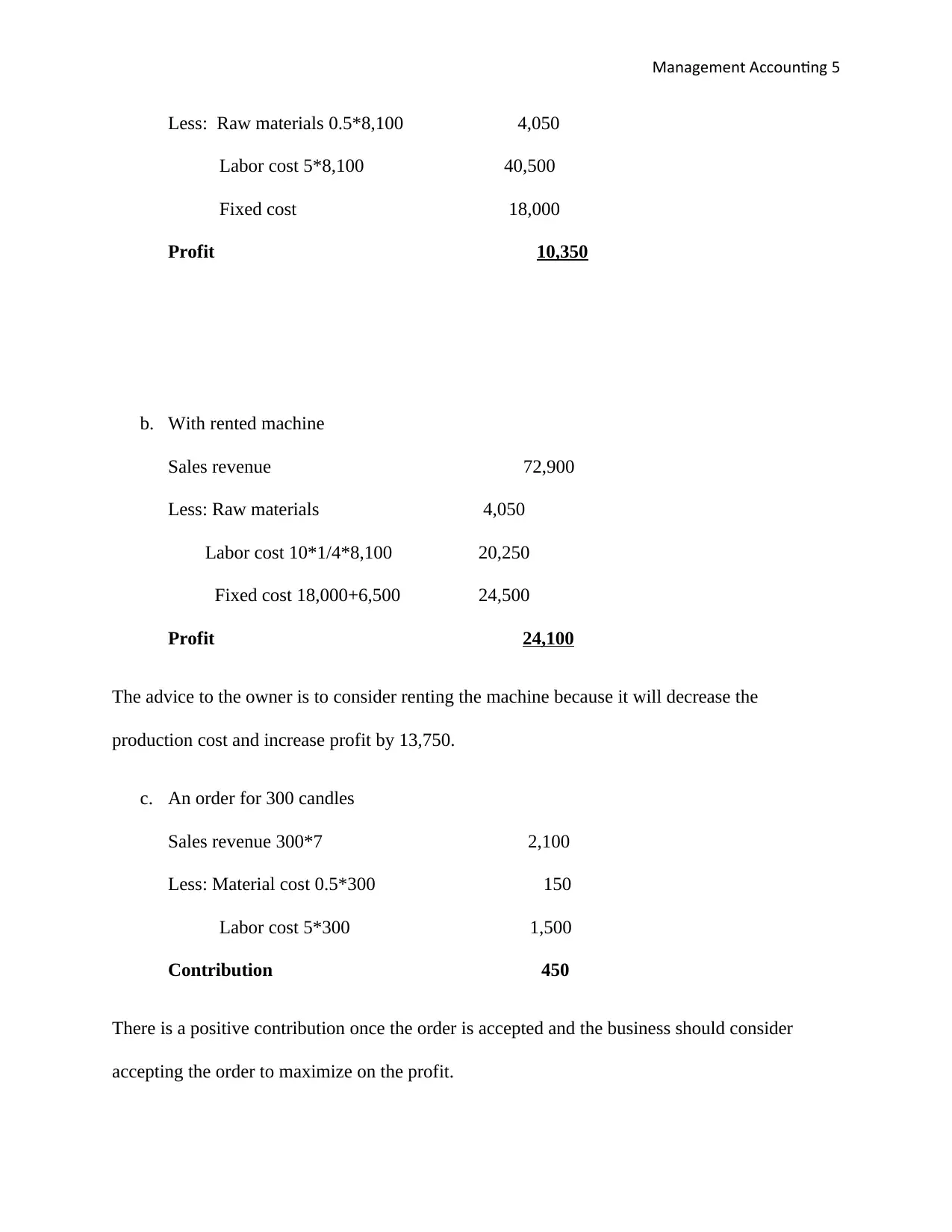

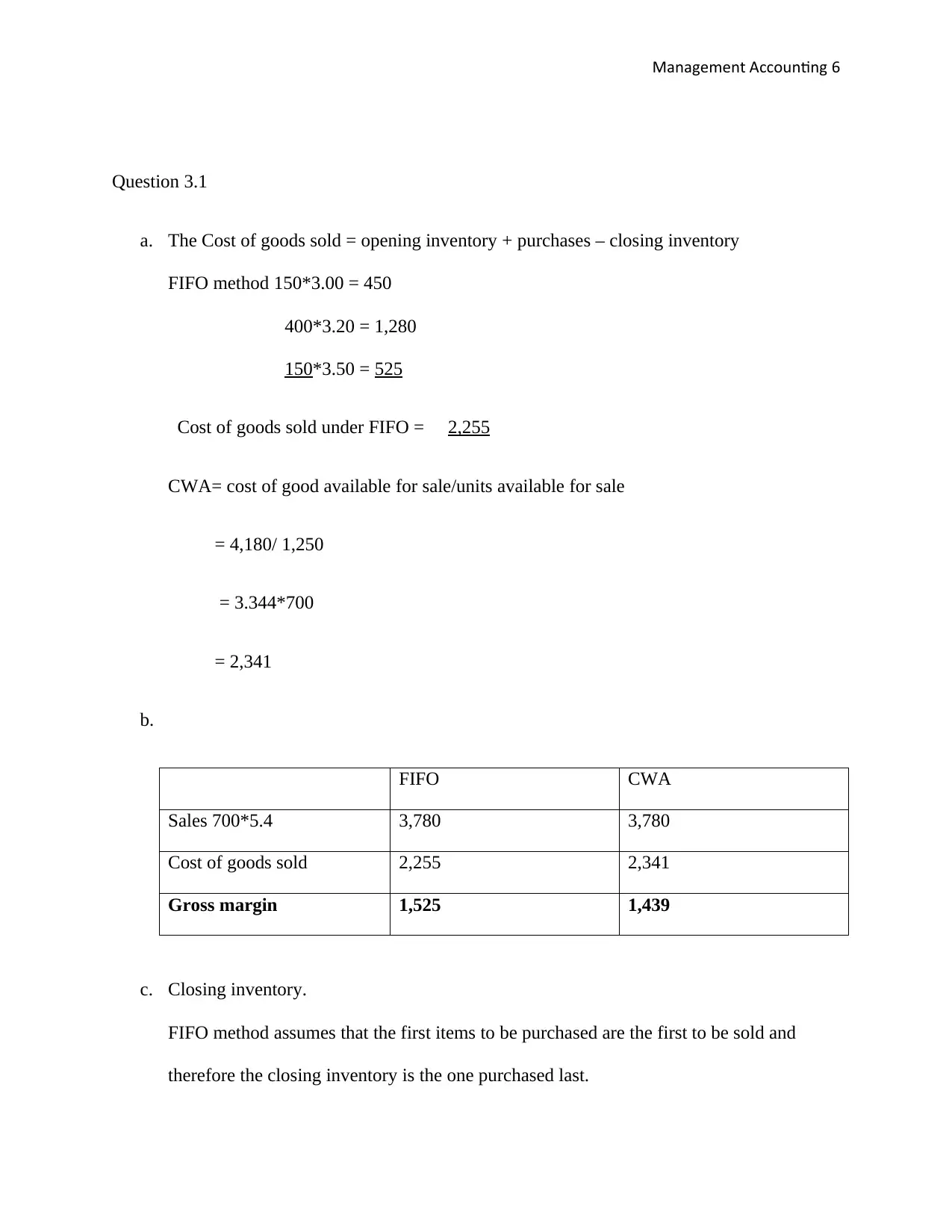

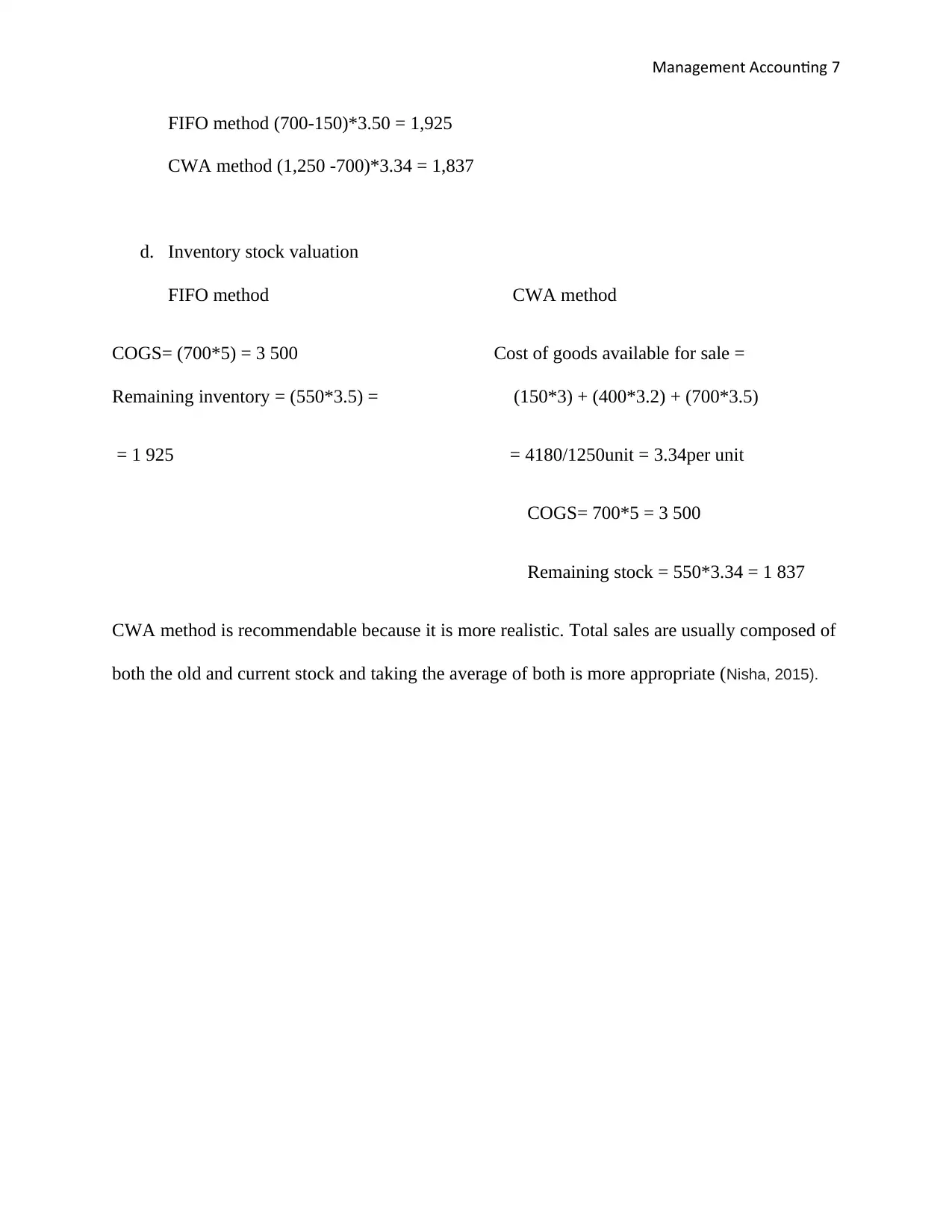

This management accounting assignment delves into cost-volume-profit analysis, flexible budgeting, and cost variances, using Lemon4U as a case study. It calculates break-even points, analyzes monthly profit, and assesses variances between budgeted and actual figures. The report also evaluates the cost-plus pricing method and explores absorption rates for dental treatments. Furthermore, it examines the impact of renting a machine on production costs and profitability, and assesses the viability of accepting a special order for candles. Finally, the assignment contrasts FIFO and CWA methods for inventory valuation, recommending the CWA method for its realism. Desklib offers a wealth of similar solved assignments and past papers for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.