Costing Systems, Variance Analysis, and Budgeting Report

VerifiedAdded on 2020/10/22

|21

|4172

|171

Report

AI Summary

This report comprehensively examines costing systems within an organization, focusing on internal reporting and providing accurate information to management. It explores the relationships between various costing systems, including job order costing, process costing, and contract costing, and identifies different responsibility centers like cost centers, profit centers, and investment centers. The report details characteristics of cost classifications, such as fixed, variable, direct, indirect, and opportunity costs, and highlights the differences between marginal and absorption costing. It analyzes cost information for materials, labor, and expenses, including inventory valuation using FIFO, and explains cost behavior. The report then delves into overhead cost attribution, calculating overhead absorption rates, and addressing over or under-absorbed costs. Furthermore, it covers variance analysis through budgeting, providing information to budget holders and producing management reports. Finally, the report discusses estimating future income and costs for decision-making, considering the effects of changing activity levels, and factors affecting short-term and long-term decision-making processes.

COST AND REVENUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 purpose of internal reporting and providing accurate information to management..............4

1.2 Relationship between various costing system in the organisation........................................5

1.3 Identifying the responsibility centres ,cost centres , profit centres and investment centres in

organisation.................................................................................................................................5

1.4 Characteristics of different types of cost classification and their use in costing .................6

1.5 Difference between marginal and absorption costing ..........................................................6

TASK 2.................................................................................................................................................7

2.1 Cost information for material, labour and expenses in relation to organisation costing

procedures...................................................................................................................................7

2.2 Analyse the cost information for material, labour and expense............................................7

2.4 Valuation of inventory ..........................................................................................................8

Last in First out ( LIFO).......................................................................................................................9

2.5 Behaviour of the cost..........................................................................................................12

2.6 Record cost information using the costing system .............................................................12

Job costing .........................................................................................................................................12

TASK 3...............................................................................................................................................14

3.1 Attribution of overhead cost of production and service cost centres in accordance with agreed

bases of allocation and apportionment......................................................................................14

3.2 Calculation of Overhead absorption rate.............................................................................14

3.3 Adjustment for over or under recorded absorption cost .....................................................15

INTRODUCTION................................................................................................................................4

TASK 1.................................................................................................................................................4

1.1 purpose of internal reporting and providing accurate information to management..............4

1.2 Relationship between various costing system in the organisation........................................5

1.3 Identifying the responsibility centres ,cost centres , profit centres and investment centres in

organisation.................................................................................................................................5

1.4 Characteristics of different types of cost classification and their use in costing .................6

1.5 Difference between marginal and absorption costing ..........................................................6

TASK 2.................................................................................................................................................7

2.1 Cost information for material, labour and expenses in relation to organisation costing

procedures...................................................................................................................................7

2.2 Analyse the cost information for material, labour and expense............................................7

2.4 Valuation of inventory ..........................................................................................................8

Last in First out ( LIFO).......................................................................................................................9

2.5 Behaviour of the cost..........................................................................................................12

2.6 Record cost information using the costing system .............................................................12

Job costing .........................................................................................................................................12

TASK 3...............................................................................................................................................14

3.1 Attribution of overhead cost of production and service cost centres in accordance with agreed

bases of allocation and apportionment......................................................................................14

3.2 Calculation of Overhead absorption rate.............................................................................14

3.3 Adjustment for over or under recorded absorption cost .....................................................15

3.4 Methods of allocation, apportionment and absorption ......................................................15

3.5 Communicate with staff to resolve queries in overhead cost data......................................16

TASK 4......................................................................................................................................16

4.1 Cost budget to identify variances........................................................................................16

4.2 Analysing the variance........................................................................................................16

4.3 Information for budget holders of any significant variances .............................................16

4.4 Management report in appropriate format.........................................................................17

TASK 5...............................................................................................................................................18

5.1 Estimates of future income and cost for decision – making ..............................................18

5.2 Effect of changing activity level in unit cost......................................................................18

5.3 Calculation of Effecting of changing level of activity .......................................................19

5.4 factors affecting short term and long term decision making ..............................................19

CONCLUSION..................................................................................................................................19

REFERENCES...................................................................................................................................20

3.5 Communicate with staff to resolve queries in overhead cost data......................................16

TASK 4......................................................................................................................................16

4.1 Cost budget to identify variances........................................................................................16

4.2 Analysing the variance........................................................................................................16

4.3 Information for budget holders of any significant variances .............................................16

4.4 Management report in appropriate format.........................................................................17

TASK 5...............................................................................................................................................18

5.1 Estimates of future income and cost for decision – making ..............................................18

5.2 Effect of changing activity level in unit cost......................................................................18

5.3 Calculation of Effecting of changing level of activity .......................................................19

5.4 factors affecting short term and long term decision making ..............................................19

CONCLUSION..................................................................................................................................19

REFERENCES...................................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Costing refers to the process in which the organisation use the costing system to estimate the

cost of the product. This system assist in allocating the cost to the business operation on the basis of

which the selling price is determined. This study will include the nature and the role of costing

system within an organisation. Moreover, It will contain the information relating to recording of the

cost information. Furthermore, this study will provide understanding of apportion of the cost

according to the organisational requirement. Also, This will provide analysis of deviation from

budget and the use of information gathered form costing system to assist in decision- making.

TASK 1

1.1 purpose of internal reporting and providing accurate information to management

Internal reporting system are the reports which are prepared by management for improving

the performance of the company by analysing the information recorded in the reports. The internal

reporting support the organisation in providing the accurate information which assist management

in making effective decision for the organisation profitability (Bai, Chen and Xu, 2017). This

reporting provides the management with the information relating to the expenses, sales, employee

turnover etc. Management by using this information is able to improve its effectiveness which

support the firm in increasing its effectiveness. Moreover, It provides the management with insight

relating to the various issues which the firm is going through support in making decision which will

resolve the problems (Ghiyasi, 2017). Management requires the internal reporting for analysing

the trend and identifying the profitability. Internal reporting provide the management in identifying

the areas which require development and need to be improve for increasing the performance of

firm.

1.2 Relationship between various costing system in the organisation

There are different costing system that includes job order costing, process costing , contract

costing etc. Job costing system is used in organisation to identity the cost attributable to each job. It

determines the cost incurred for completing the particular job (Jacobson And et.al., 2015). Process

costing is relating to identify the cost of product in it's each process. In this system the output of one

process is the input of the other. Under contract costing the cost of each contract but the period of

the contract is more than one year. There is a close relationship between these costing system as this

assist in determining the cost of the product by using different methods. For example, job costing is

related to the contract costing as they both identify the cost relating to the completion of the job or

contract (Jayarani and Prakash, 2018). The costing system are interdependent as the process costing

Costing refers to the process in which the organisation use the costing system to estimate the

cost of the product. This system assist in allocating the cost to the business operation on the basis of

which the selling price is determined. This study will include the nature and the role of costing

system within an organisation. Moreover, It will contain the information relating to recording of the

cost information. Furthermore, this study will provide understanding of apportion of the cost

according to the organisational requirement. Also, This will provide analysis of deviation from

budget and the use of information gathered form costing system to assist in decision- making.

TASK 1

1.1 purpose of internal reporting and providing accurate information to management

Internal reporting system are the reports which are prepared by management for improving

the performance of the company by analysing the information recorded in the reports. The internal

reporting support the organisation in providing the accurate information which assist management

in making effective decision for the organisation profitability (Bai, Chen and Xu, 2017). This

reporting provides the management with the information relating to the expenses, sales, employee

turnover etc. Management by using this information is able to improve its effectiveness which

support the firm in increasing its effectiveness. Moreover, It provides the management with insight

relating to the various issues which the firm is going through support in making decision which will

resolve the problems (Ghiyasi, 2017). Management requires the internal reporting for analysing

the trend and identifying the profitability. Internal reporting provide the management in identifying

the areas which require development and need to be improve for increasing the performance of

firm.

1.2 Relationship between various costing system in the organisation

There are different costing system that includes job order costing, process costing , contract

costing etc. Job costing system is used in organisation to identity the cost attributable to each job. It

determines the cost incurred for completing the particular job (Jacobson And et.al., 2015). Process

costing is relating to identify the cost of product in it's each process. In this system the output of one

process is the input of the other. Under contract costing the cost of each contract but the period of

the contract is more than one year. There is a close relationship between these costing system as this

assist in determining the cost of the product by using different methods. For example, job costing is

related to the contract costing as they both identify the cost relating to the completion of the job or

contract (Jayarani and Prakash, 2018). The costing system are interdependent as the process costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is finished then only the job costing is undertaken.

1.3 Identifying the responsibility centres ,cost centres , profit centres and investment centres in

organisation.

Responsibility centres are the part of the organisation for which the management hold the

responsibility. The most common responsibility centres are the departments of the company. When

the manager of the responsibility centre can only control the cost then it is known as cost centre.

The different responsibility centres in the organisation consist of cost centres, revenue centres,

profit centre, investment centre (Malfertheiner and et.al., 2017). If the manager can control both

cost and profit and then the responsibility centre is known as profit centre. Manager of investment

centre is having more authority and responsibility that the cost and profit centres.

The organisational chart shows the sub- task which will be performed by different

departments of the organisation. The cost centres the managers is held responsible for the cost

incurred in that segment and not for revenues. The organisation have production and service

departments which are classified as the cost centres. Also, marketing department, sales department

are the cost centres (Nguyen, 2018). Profit centre is responsible for both cost and revenues. The

profit centre of the organisation includes the marketing manager of product and individual sales

representative. The profit centre include the accounting, auditing etc. there are separate division in

the organisation which are made as profit centre and they focus on earning profit. Investment centre

includes department that is responsible for earning return of investment.

1.4 Characteristics of different types of cost classification and their use in costing

There are various types of cost which are used in costing for determine the cost of the

product in the organisation. There are different cost used in costing which includes the following :

Fixed cost : It includes the cost which does not change with the change in the output. This

cost is fixed and the organisation have to incur this cost whether it produces output or not. It

includes rent, interest payment, property tax, wages to the labour.

Variable cost : It changes with the change in output of the product. It includes cost of

material , labour etc.

Total cost : It is defined as the sum total of the fixed and variable cost (Preuß, Andreff, and

Weitzmann, 2018).

Direct and indirect cost : Direct cost includes the major components of the production of the

product such as direct labour, direct material. This cost is also refereed to as prime cost.

1.3 Identifying the responsibility centres ,cost centres , profit centres and investment centres in

organisation.

Responsibility centres are the part of the organisation for which the management hold the

responsibility. The most common responsibility centres are the departments of the company. When

the manager of the responsibility centre can only control the cost then it is known as cost centre.

The different responsibility centres in the organisation consist of cost centres, revenue centres,

profit centre, investment centre (Malfertheiner and et.al., 2017). If the manager can control both

cost and profit and then the responsibility centre is known as profit centre. Manager of investment

centre is having more authority and responsibility that the cost and profit centres.

The organisational chart shows the sub- task which will be performed by different

departments of the organisation. The cost centres the managers is held responsible for the cost

incurred in that segment and not for revenues. The organisation have production and service

departments which are classified as the cost centres. Also, marketing department, sales department

are the cost centres (Nguyen, 2018). Profit centre is responsible for both cost and revenues. The

profit centre of the organisation includes the marketing manager of product and individual sales

representative. The profit centre include the accounting, auditing etc. there are separate division in

the organisation which are made as profit centre and they focus on earning profit. Investment centre

includes department that is responsible for earning return of investment.

1.4 Characteristics of different types of cost classification and their use in costing

There are various types of cost which are used in costing for determine the cost of the

product in the organisation. There are different cost used in costing which includes the following :

Fixed cost : It includes the cost which does not change with the change in the output. This

cost is fixed and the organisation have to incur this cost whether it produces output or not. It

includes rent, interest payment, property tax, wages to the labour.

Variable cost : It changes with the change in output of the product. It includes cost of

material , labour etc.

Total cost : It is defined as the sum total of the fixed and variable cost (Preuß, Andreff, and

Weitzmann, 2018).

Direct and indirect cost : Direct cost includes the major components of the production of the

product such as direct labour, direct material. This cost is also refereed to as prime cost.

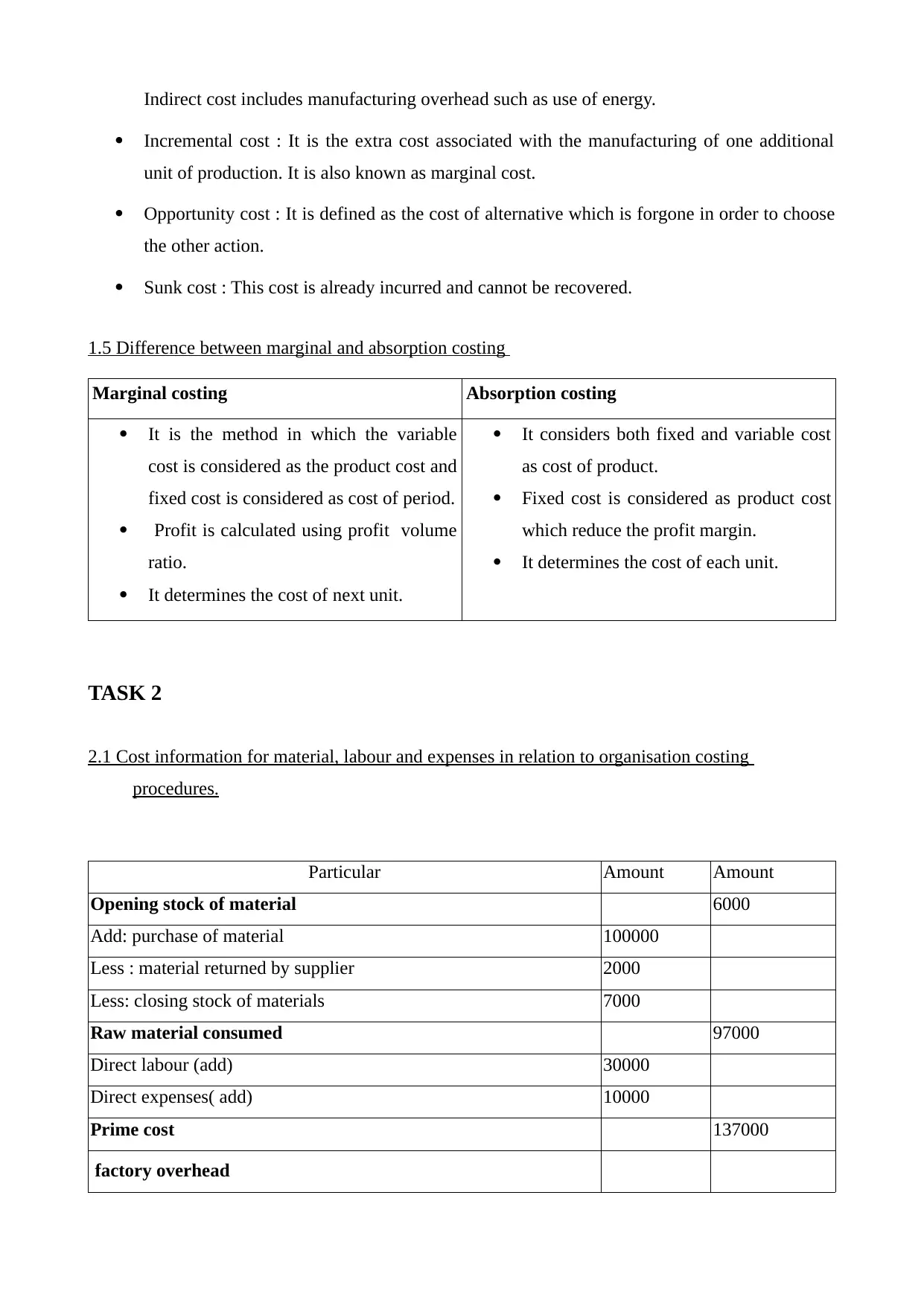

Indirect cost includes manufacturing overhead such as use of energy.

Incremental cost : It is the extra cost associated with the manufacturing of one additional

unit of production. It is also known as marginal cost.

Opportunity cost : It is defined as the cost of alternative which is forgone in order to choose

the other action.

Sunk cost : This cost is already incurred and cannot be recovered.

1.5 Difference between marginal and absorption costing

Marginal costing Absorption costing

It is the method in which the variable

cost is considered as the product cost and

fixed cost is considered as cost of period.

Profit is calculated using profit volume

ratio.

It determines the cost of next unit.

It considers both fixed and variable cost

as cost of product.

Fixed cost is considered as product cost

which reduce the profit margin.

It determines the cost of each unit.

TASK 2

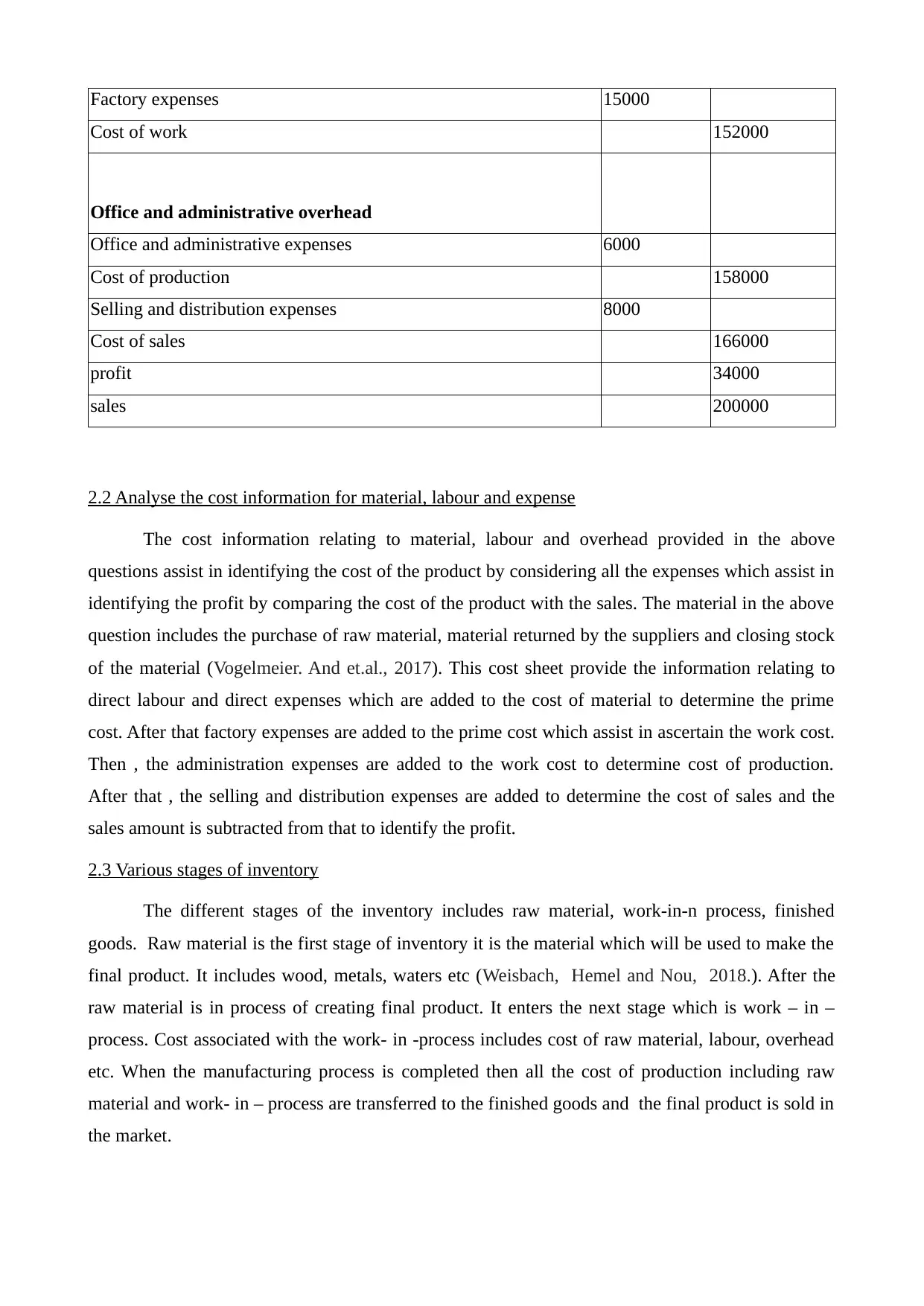

2.1 Cost information for material, labour and expenses in relation to organisation costing

procedures.

Particular Amount Amount

Opening stock of material 6000

Add: purchase of material 100000

Less : material returned by supplier 2000

Less: closing stock of materials 7000

Raw material consumed 97000

Direct labour (add) 30000

Direct expenses( add) 10000

Prime cost 137000

factory overhead

Incremental cost : It is the extra cost associated with the manufacturing of one additional

unit of production. It is also known as marginal cost.

Opportunity cost : It is defined as the cost of alternative which is forgone in order to choose

the other action.

Sunk cost : This cost is already incurred and cannot be recovered.

1.5 Difference between marginal and absorption costing

Marginal costing Absorption costing

It is the method in which the variable

cost is considered as the product cost and

fixed cost is considered as cost of period.

Profit is calculated using profit volume

ratio.

It determines the cost of next unit.

It considers both fixed and variable cost

as cost of product.

Fixed cost is considered as product cost

which reduce the profit margin.

It determines the cost of each unit.

TASK 2

2.1 Cost information for material, labour and expenses in relation to organisation costing

procedures.

Particular Amount Amount

Opening stock of material 6000

Add: purchase of material 100000

Less : material returned by supplier 2000

Less: closing stock of materials 7000

Raw material consumed 97000

Direct labour (add) 30000

Direct expenses( add) 10000

Prime cost 137000

factory overhead

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Factory expenses 15000

Cost of work 152000

Office and administrative overhead

Office and administrative expenses 6000

Cost of production 158000

Selling and distribution expenses 8000

Cost of sales 166000

profit 34000

sales 200000

2.2 Analyse the cost information for material, labour and expense

The cost information relating to material, labour and overhead provided in the above

questions assist in identifying the cost of the product by considering all the expenses which assist in

identifying the profit by comparing the cost of the product with the sales. The material in the above

question includes the purchase of raw material, material returned by the suppliers and closing stock

of the material (Vogelmeier. And et.al., 2017). This cost sheet provide the information relating to

direct labour and direct expenses which are added to the cost of material to determine the prime

cost. After that factory expenses are added to the prime cost which assist in ascertain the work cost.

Then , the administration expenses are added to the work cost to determine cost of production.

After that , the selling and distribution expenses are added to determine the cost of sales and the

sales amount is subtracted from that to identify the profit.

2.3 Various stages of inventory

The different stages of the inventory includes raw material, work-in-n process, finished

goods. Raw material is the first stage of inventory it is the material which will be used to make the

final product. It includes wood, metals, waters etc (Weisbach, Hemel and Nou, 2018.). After the

raw material is in process of creating final product. It enters the next stage which is work – in –

process. Cost associated with the work- in -process includes cost of raw material, labour, overhead

etc. When the manufacturing process is completed then all the cost of production including raw

material and work- in – process are transferred to the finished goods and the final product is sold in

the market.

Cost of work 152000

Office and administrative overhead

Office and administrative expenses 6000

Cost of production 158000

Selling and distribution expenses 8000

Cost of sales 166000

profit 34000

sales 200000

2.2 Analyse the cost information for material, labour and expense

The cost information relating to material, labour and overhead provided in the above

questions assist in identifying the cost of the product by considering all the expenses which assist in

identifying the profit by comparing the cost of the product with the sales. The material in the above

question includes the purchase of raw material, material returned by the suppliers and closing stock

of the material (Vogelmeier. And et.al., 2017). This cost sheet provide the information relating to

direct labour and direct expenses which are added to the cost of material to determine the prime

cost. After that factory expenses are added to the prime cost which assist in ascertain the work cost.

Then , the administration expenses are added to the work cost to determine cost of production.

After that , the selling and distribution expenses are added to determine the cost of sales and the

sales amount is subtracted from that to identify the profit.

2.3 Various stages of inventory

The different stages of the inventory includes raw material, work-in-n process, finished

goods. Raw material is the first stage of inventory it is the material which will be used to make the

final product. It includes wood, metals, waters etc (Weisbach, Hemel and Nou, 2018.). After the

raw material is in process of creating final product. It enters the next stage which is work – in –

process. Cost associated with the work- in -process includes cost of raw material, labour, overhead

etc. When the manufacturing process is completed then all the cost of production including raw

material and work- in – process are transferred to the finished goods and the final product is sold in

the market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

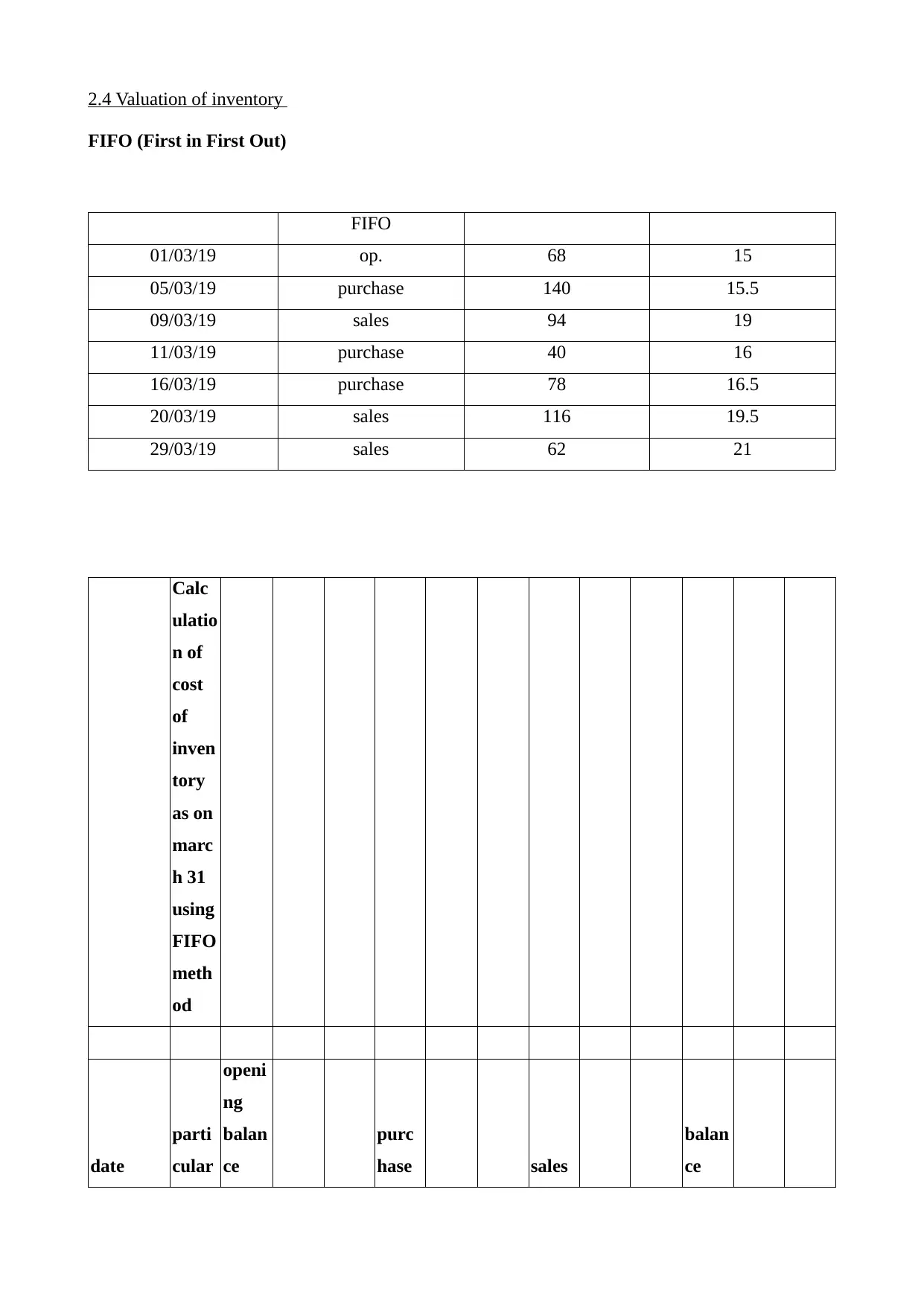

2.4 Valuation of inventory

FIFO (First in First Out)

FIFO

01/03/19 op. 68 15

05/03/19 purchase 140 15.5

09/03/19 sales 94 19

11/03/19 purchase 40 16

16/03/19 purchase 78 16.5

20/03/19 sales 116 19.5

29/03/19 sales 62 21

Calc

ulatio

n of

cost

of

inven

tory

as on

marc

h 31

using

FIFO

meth

od

date

parti

cular

openi

ng

balan

ce

purc

hase sales

balan

ce

FIFO (First in First Out)

FIFO

01/03/19 op. 68 15

05/03/19 purchase 140 15.5

09/03/19 sales 94 19

11/03/19 purchase 40 16

16/03/19 purchase 78 16.5

20/03/19 sales 116 19.5

29/03/19 sales 62 21

Calc

ulatio

n of

cost

of

inven

tory

as on

marc

h 31

using

FIFO

meth

od

date

parti

cular

openi

ng

balan

ce

purc

hase sales

balan

ce

units rate

amou

nt unit rate

amou

nt unit rate

amou

nt unit rate

amou

nt

01/03/19

begin

ning

inven

tory 68 15 1020 68 15 1020

05/03/19

purch

ase 140 15.5 2170 68 15 1020

140 15.5 2170

09/03/19 sales 68 15 1020

26 15.5 403 114 15.5 1767

11/03/19 40 16 640 114 15.5 1767

40 16 640

16/03/19 78 16.5 1287 114 15.5 1767

40 16 640

78 16.5 1287

20/03/19 114 15.5 1767 38 16 608

2 16 32 78 16.5 1287

29/03/19 38 16 608 54 16.5 891

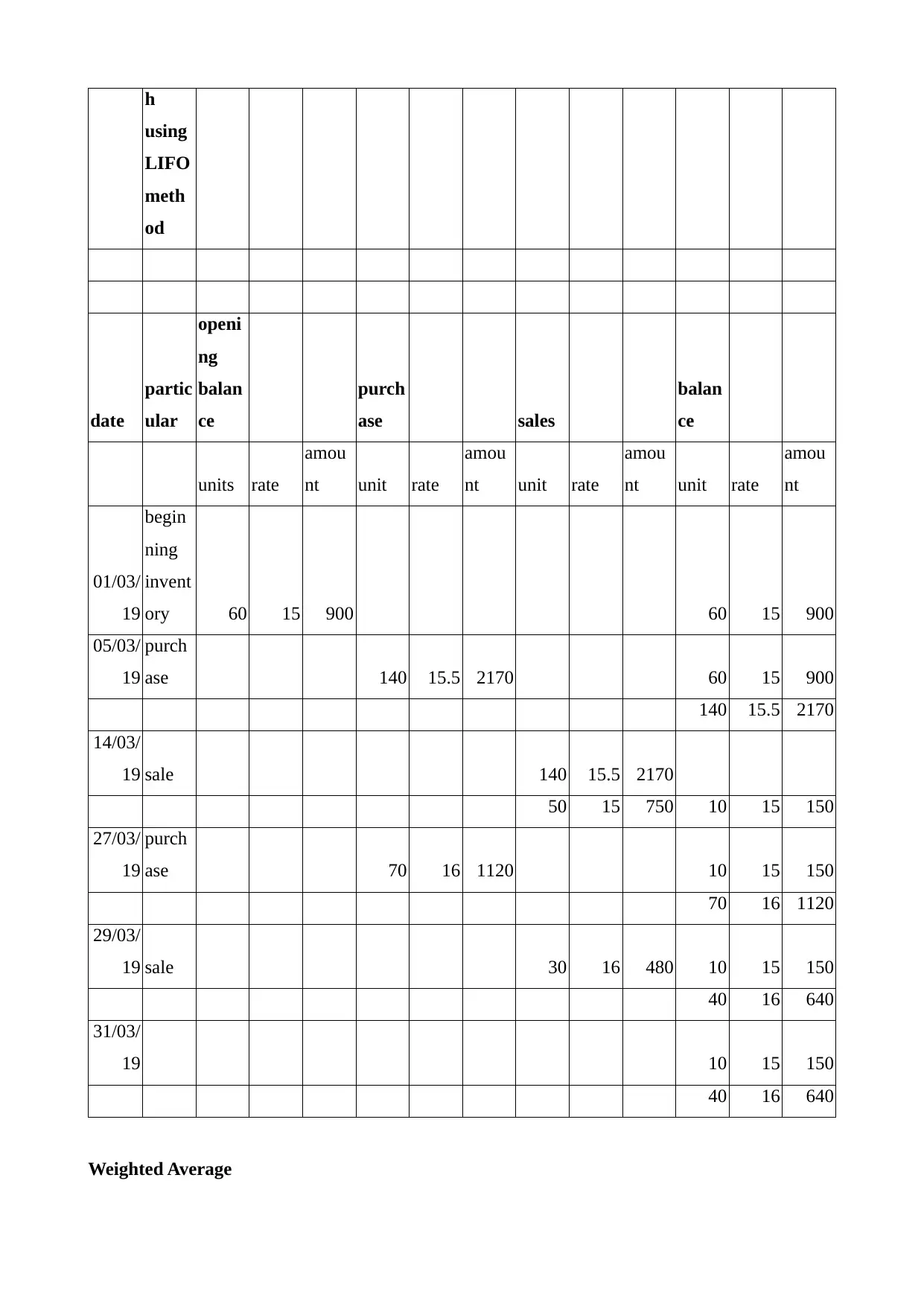

Last in First out ( LIFO)

calcul

ation

of

cost

of

inven

tory

as on

31

marc

amou

nt unit rate

amou

nt unit rate

amou

nt unit rate

amou

nt

01/03/19

begin

ning

inven

tory 68 15 1020 68 15 1020

05/03/19

purch

ase 140 15.5 2170 68 15 1020

140 15.5 2170

09/03/19 sales 68 15 1020

26 15.5 403 114 15.5 1767

11/03/19 40 16 640 114 15.5 1767

40 16 640

16/03/19 78 16.5 1287 114 15.5 1767

40 16 640

78 16.5 1287

20/03/19 114 15.5 1767 38 16 608

2 16 32 78 16.5 1287

29/03/19 38 16 608 54 16.5 891

Last in First out ( LIFO)

calcul

ation

of

cost

of

inven

tory

as on

31

marc

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

h

using

LIFO

meth

od

date

partic

ular

openi

ng

balan

ce

purch

ase sales

balan

ce

units rate

amou

nt unit rate

amou

nt unit rate

amou

nt unit rate

amou

nt

01/03/

19

begin

ning

invent

ory 60 15 900 60 15 900

05/03/

19

purch

ase 140 15.5 2170 60 15 900

140 15.5 2170

14/03/

19 sale 140 15.5 2170

50 15 750 10 15 150

27/03/

19

purch

ase 70 16 1120 10 15 150

70 16 1120

29/03/

19 sale 30 16 480 10 15 150

40 16 640

31/03/

19 10 15 150

40 16 640

Weighted Average

using

LIFO

meth

od

date

partic

ular

openi

ng

balan

ce

purch

ase sales

balan

ce

units rate

amou

nt unit rate

amou

nt unit rate

amou

nt unit rate

amou

nt

01/03/

19

begin

ning

invent

ory 60 15 900 60 15 900

05/03/

19

purch

ase 140 15.5 2170 60 15 900

140 15.5 2170

14/03/

19 sale 140 15.5 2170

50 15 750 10 15 150

27/03/

19

purch

ase 70 16 1120 10 15 150

70 16 1120

29/03/

19 sale 30 16 480 10 15 150

40 16 640

31/03/

19 10 15 150

40 16 640

Weighted Average

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

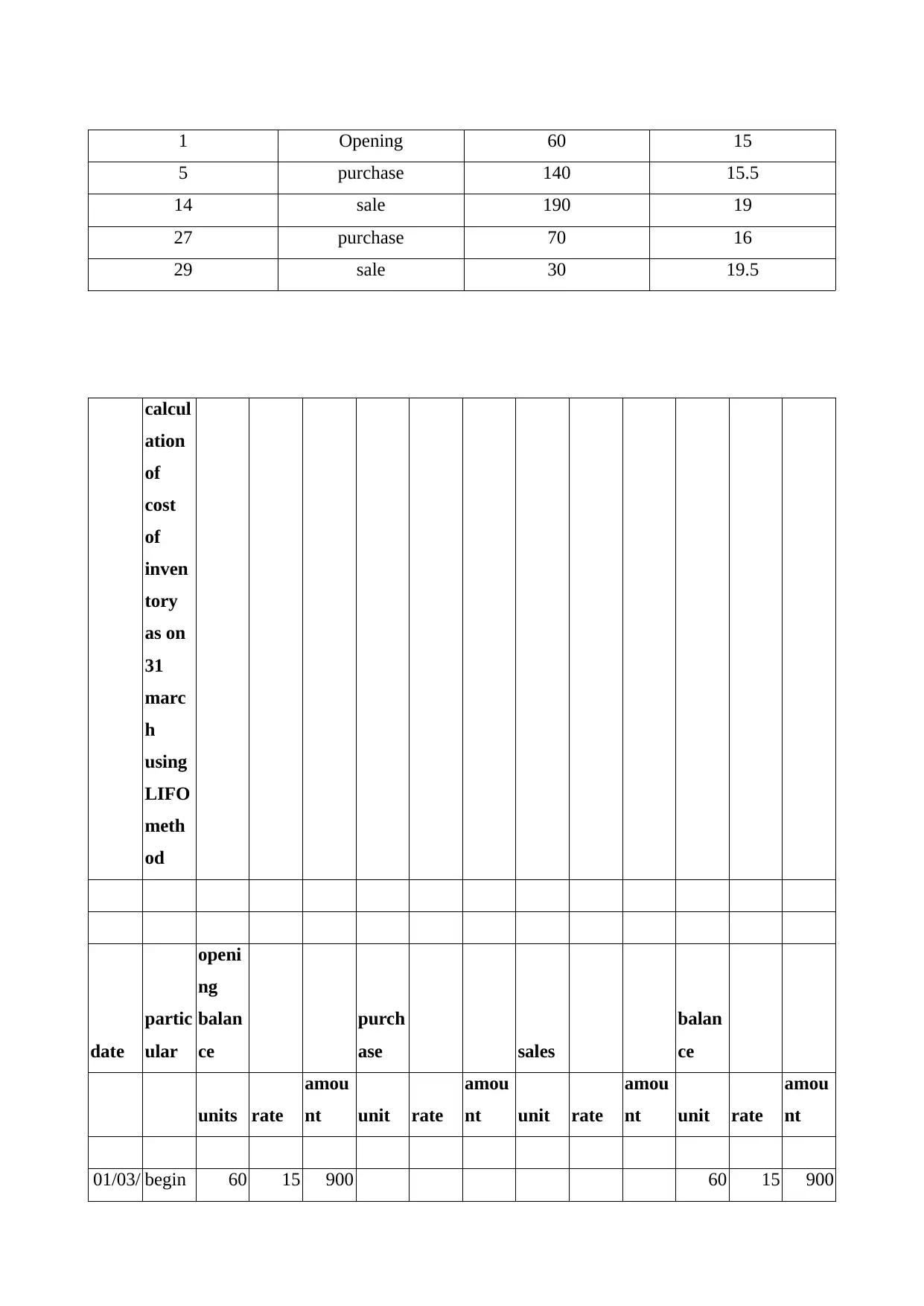

1 Opening 60 15

5 purchase 140 15.5

14 sale 190 19

27 purchase 70 16

29 sale 30 19.5

calcul

ation

of

cost

of

inven

tory

as on

31

marc

h

using

LIFO

meth

od

date

partic

ular

openi

ng

balan

ce

purch

ase sales

balan

ce

units rate

amou

nt unit rate

amou

nt unit rate

amou

nt unit rate

amou

nt

01/03/ begin 60 15 900 60 15 900

5 purchase 140 15.5

14 sale 190 19

27 purchase 70 16

29 sale 30 19.5

calcul

ation

of

cost

of

inven

tory

as on

31

marc

h

using

LIFO

meth

od

date

partic

ular

openi

ng

balan

ce

purch

ase sales

balan

ce

units rate

amou

nt unit rate

amou

nt unit rate

amou

nt unit rate

amou

nt

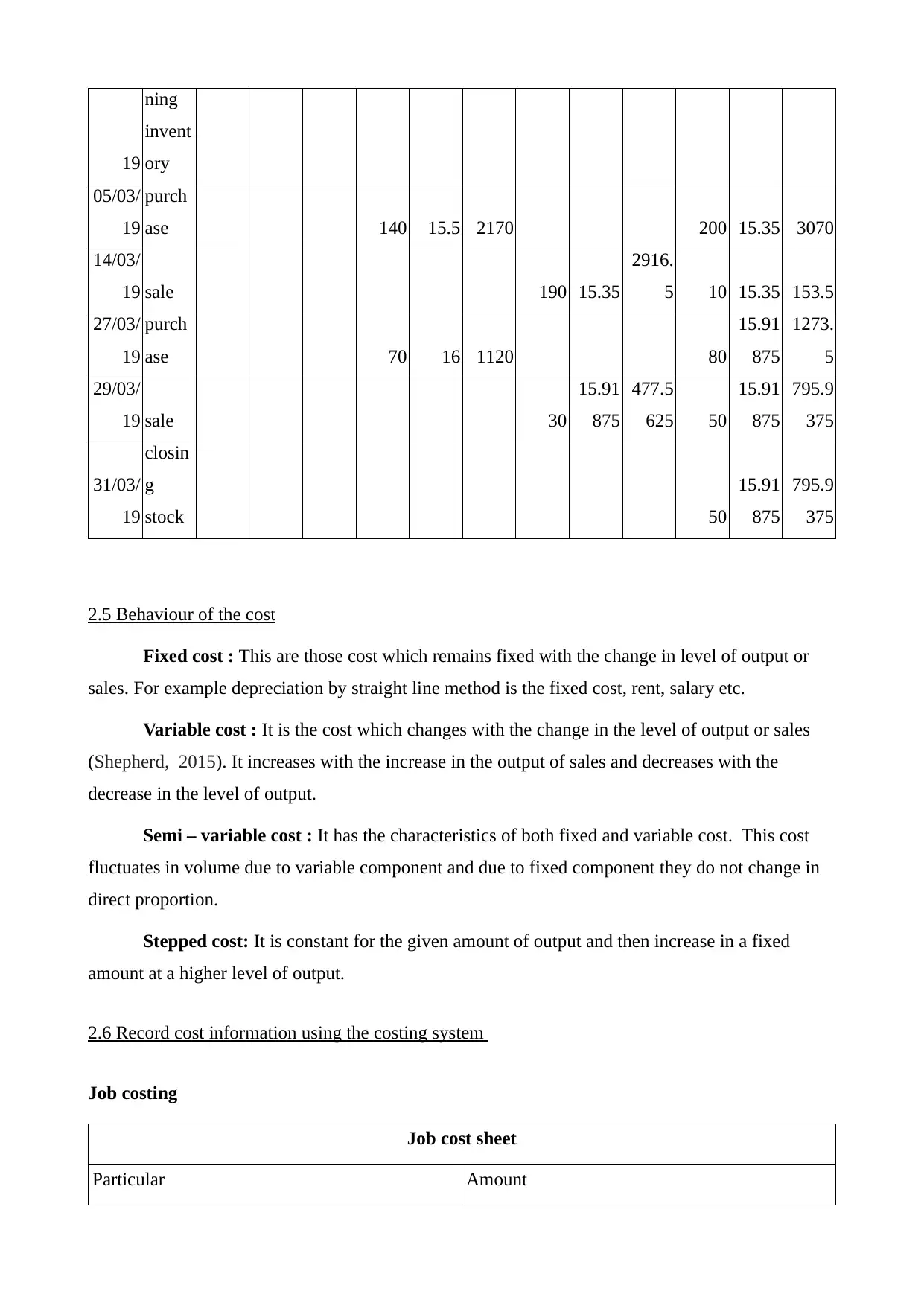

01/03/ begin 60 15 900 60 15 900

19

ning

invent

ory

05/03/

19

purch

ase 140 15.5 2170 200 15.35 3070

14/03/

19 sale 190 15.35

2916.

5 10 15.35 153.5

27/03/

19

purch

ase 70 16 1120 80

15.91

875

1273.

5

29/03/

19 sale 30

15.91

875

477.5

625 50

15.91

875

795.9

375

31/03/

19

closin

g

stock 50

15.91

875

795.9

375

2.5 Behaviour of the cost

Fixed cost : This are those cost which remains fixed with the change in level of output or

sales. For example depreciation by straight line method is the fixed cost, rent, salary etc.

Variable cost : It is the cost which changes with the change in the level of output or sales

(Shepherd, 2015). It increases with the increase in the output of sales and decreases with the

decrease in the level of output.

Semi – variable cost : It has the characteristics of both fixed and variable cost. This cost

fluctuates in volume due to variable component and due to fixed component they do not change in

direct proportion.

Stepped cost: It is constant for the given amount of output and then increase in a fixed

amount at a higher level of output.

2.6 Record cost information using the costing system

Job costing

Job cost sheet

Particular Amount

ning

invent

ory

05/03/

19

purch

ase 140 15.5 2170 200 15.35 3070

14/03/

19 sale 190 15.35

2916.

5 10 15.35 153.5

27/03/

19

purch

ase 70 16 1120 80

15.91

875

1273.

5

29/03/

19 sale 30

15.91

875

477.5

625 50

15.91

875

795.9

375

31/03/

19

closin

g

stock 50

15.91

875

795.9

375

2.5 Behaviour of the cost

Fixed cost : This are those cost which remains fixed with the change in level of output or

sales. For example depreciation by straight line method is the fixed cost, rent, salary etc.

Variable cost : It is the cost which changes with the change in the level of output or sales

(Shepherd, 2015). It increases with the increase in the output of sales and decreases with the

decrease in the level of output.

Semi – variable cost : It has the characteristics of both fixed and variable cost. This cost

fluctuates in volume due to variable component and due to fixed component they do not change in

direct proportion.

Stepped cost: It is constant for the given amount of output and then increase in a fixed

amount at a higher level of output.

2.6 Record cost information using the costing system

Job costing

Job cost sheet

Particular Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.