ACC200: Cost Allocation Methods & Beztec Limited Analysis

VerifiedAdded on 2023/06/07

|17

|2970

|219

Report

AI Summary

This report provides a detailed analysis of cost allocation methods, specifically focusing on Beztec Limited and its two printer models, Lexon and Protox. The report contrasts traditional costing methods with activity-based costing (ABC) and evaluates the impact of each on product profitability. It examines the company's initial decision to phase out the Lexon model based on traditional costing data, revealing that ABC presents a different perspective, suggesting Lexon is more profitable than initially assessed. The report includes a recalculation of operating income using ABC, a gross profit margin analysis, and a discussion on the treatment of under- or over-recovery of overheads. Furthermore, it offers recommendations for the accountant, Sue Smith, emphasizing the ethical responsibilities in ensuring accurate financial reporting and decision-making within the company. The analysis highlights the importance of selecting the correct costing method to avoid flawed business decisions.

Introduction to Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The following study contains a detailed analysis on the various types of cost allocation

method. It also contains information on importance of choosing the collection costing method

for an organisation. There are recommendations made in order to help an accountant with the

decisions making function.

2

The following study contains a detailed analysis on the various types of cost allocation

method. It also contains information on importance of choosing the collection costing method

for an organisation. There are recommendations made in order to help an accountant with the

decisions making function.

2

Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Traditional system of costing and its disadvantages..................................................................5

Activity based costing................................................................................................................6

Importance of using correct costing method..............................................................................7

Analysis of cost data of Beztec Limited....................................................................................8

Recommendation for Sue Smith..............................................................................................11

Analysis of gross profit margin of the company......................................................................12

Treatment of under-over recovery of overheads......................................................................13

Recommendation and conclusion............................................................................................14

Bibliography.............................................................................................................................15

3

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Traditional system of costing and its disadvantages..................................................................5

Activity based costing................................................................................................................6

Importance of using correct costing method..............................................................................7

Analysis of cost data of Beztec Limited....................................................................................8

Recommendation for Sue Smith..............................................................................................11

Analysis of gross profit margin of the company......................................................................12

Treatment of under-over recovery of overheads......................................................................13

Recommendation and conclusion............................................................................................14

Bibliography.............................................................................................................................15

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The management of an organisation is entrusted with the one of the most important parts of

decision making which is product costing. Determining the cost of a product is one of the

most complicated tasks. It is important that decision be taken taking into considerations all

the factors. Taking a wrong step might end up affecting the financial viability of the whole

organisation. (Atkinson, 2012)

The company, Beztec limited produce two models of printers, Lexon and Protox. The

management of the company is looking forward to phase out the older model, Lexon, based

on the fact that it has lower operating returns. The accountant Sue Smith is of the view that,

use of inappropriate costing methods has lead to these results. If the company will opt for

change in cost allocation methods, then it would help the management take correct measures.

In the following report we have discussed about two methods of cost allocation, and why it is

important to have proper allocation method. Also, we have laid down facts which will help

the management to take correct decisions.

4

The management of an organisation is entrusted with the one of the most important parts of

decision making which is product costing. Determining the cost of a product is one of the

most complicated tasks. It is important that decision be taken taking into considerations all

the factors. Taking a wrong step might end up affecting the financial viability of the whole

organisation. (Atkinson, 2012)

The company, Beztec limited produce two models of printers, Lexon and Protox. The

management of the company is looking forward to phase out the older model, Lexon, based

on the fact that it has lower operating returns. The accountant Sue Smith is of the view that,

use of inappropriate costing methods has lead to these results. If the company will opt for

change in cost allocation methods, then it would help the management take correct measures.

In the following report we have discussed about two methods of cost allocation, and why it is

important to have proper allocation method. Also, we have laid down facts which will help

the management to take correct decisions.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional system of costing and its disadvantages

The traditional system of costing is the method of cost allocation amongst the products, in

which a pre determined cost rate is allocated in between the various products based on a

certain factor such as machine hours or labour hours (Berry, 2009). The joint costs which are

incurred for various products are required to be allocated so that unit cost of different

products can be identified.

This system is old and classified as traditional, as this system fails to incorporate importance

of actual use of resources. The traditional system of cost allocation is more appropriate in

firms which have one product and simplified production process with few activities (Boyd,

2013). The modern production processes involve complex process, more products and

various activities. Due to the complexities of the nature of production it is important that the

cost is allocated properly in order to ensure correct costing of the product.

This system of cost allocation shifts the burden of overhead costs from one product to another

(Dash, 2016). The distribution of cost cannot be done evenly amongst the entire product as

they use different amount of resources. This leads to improper cost allocation and costing of

the product. This underpriceds some product and over prices the other (Datar M. S., 2015).

Due to these disadvantages the modern production facilities opt for modern, activity based

costing. Since Beztec Ltd has two products which involve use of common activities, it is

important that cost of these activities is allocated as per actual consumption in order to

calculate the correct cost of the products.

5

The traditional system of costing is the method of cost allocation amongst the products, in

which a pre determined cost rate is allocated in between the various products based on a

certain factor such as machine hours or labour hours (Berry, 2009). The joint costs which are

incurred for various products are required to be allocated so that unit cost of different

products can be identified.

This system is old and classified as traditional, as this system fails to incorporate importance

of actual use of resources. The traditional system of cost allocation is more appropriate in

firms which have one product and simplified production process with few activities (Boyd,

2013). The modern production processes involve complex process, more products and

various activities. Due to the complexities of the nature of production it is important that the

cost is allocated properly in order to ensure correct costing of the product.

This system of cost allocation shifts the burden of overhead costs from one product to another

(Dash, 2016). The distribution of cost cannot be done evenly amongst the entire product as

they use different amount of resources. This leads to improper cost allocation and costing of

the product. This underpriceds some product and over prices the other (Datar M. S., 2015).

Due to these disadvantages the modern production facilities opt for modern, activity based

costing. Since Beztec Ltd has two products which involve use of common activities, it is

important that cost of these activities is allocated as per actual consumption in order to

calculate the correct cost of the products.

5

Activity based costing

Activity based costing is the modern form of cost allocation, which has been made keeping in

mind the problems generated by the old traditional costing system (Datar S. , 2016). Under

this system of cost allocation, thorough collection and analysis of cost data is done. Amounts

incurred on various activities are recorded along with the units of these activities consumed

by each different type of product. Using this data collected, cost per each unit of activity

consumed is calculated. Based on this rate per activity, the cost is allocated amongst various

products (Holtzman, 2013).

This system of cost allocation ensures that the cost is allocated to the product only is it has

utilised that function and only to the extent till it has been consumed (Horngren, 2012).

Therefore, this leads to correct costing of the product. The management can totally rely on

the cost calculated based on activity based costing.

6

Activity based costing is the modern form of cost allocation, which has been made keeping in

mind the problems generated by the old traditional costing system (Datar S. , 2016). Under

this system of cost allocation, thorough collection and analysis of cost data is done. Amounts

incurred on various activities are recorded along with the units of these activities consumed

by each different type of product. Using this data collected, cost per each unit of activity

consumed is calculated. Based on this rate per activity, the cost is allocated amongst various

products (Holtzman, 2013).

This system of cost allocation ensures that the cost is allocated to the product only is it has

utilised that function and only to the extent till it has been consumed (Horngren, 2012).

Therefore, this leads to correct costing of the product. The management can totally rely on

the cost calculated based on activity based costing.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Importance of using correct costing method

It is important that the companies choose correct cost allocation method in order to ensure

correct decision making (Seal, 2012). Let us take the current case for example. In the given

scenario the management wants to phase out one line of product, as it thinks that it generates

mow operating income. But if we look at the data and use it appropriately we will have

opposite results.

Implementation of correct cost allocation method is very important. The decision made by the

management is based on the financial data. If this data is not properly arranged, then

management might end up taking improper decisions which will affect the future of the

company (Siciliano, 2015). Taking wrong decision might also lead to collapse of company in

near future.

7

It is important that the companies choose correct cost allocation method in order to ensure

correct decision making (Seal, 2012). Let us take the current case for example. In the given

scenario the management wants to phase out one line of product, as it thinks that it generates

mow operating income. But if we look at the data and use it appropriately we will have

opposite results.

Implementation of correct cost allocation method is very important. The decision made by the

management is based on the financial data. If this data is not properly arranged, then

management might end up taking improper decisions which will affect the future of the

company (Siciliano, 2015). Taking wrong decision might also lead to collapse of company in

near future.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

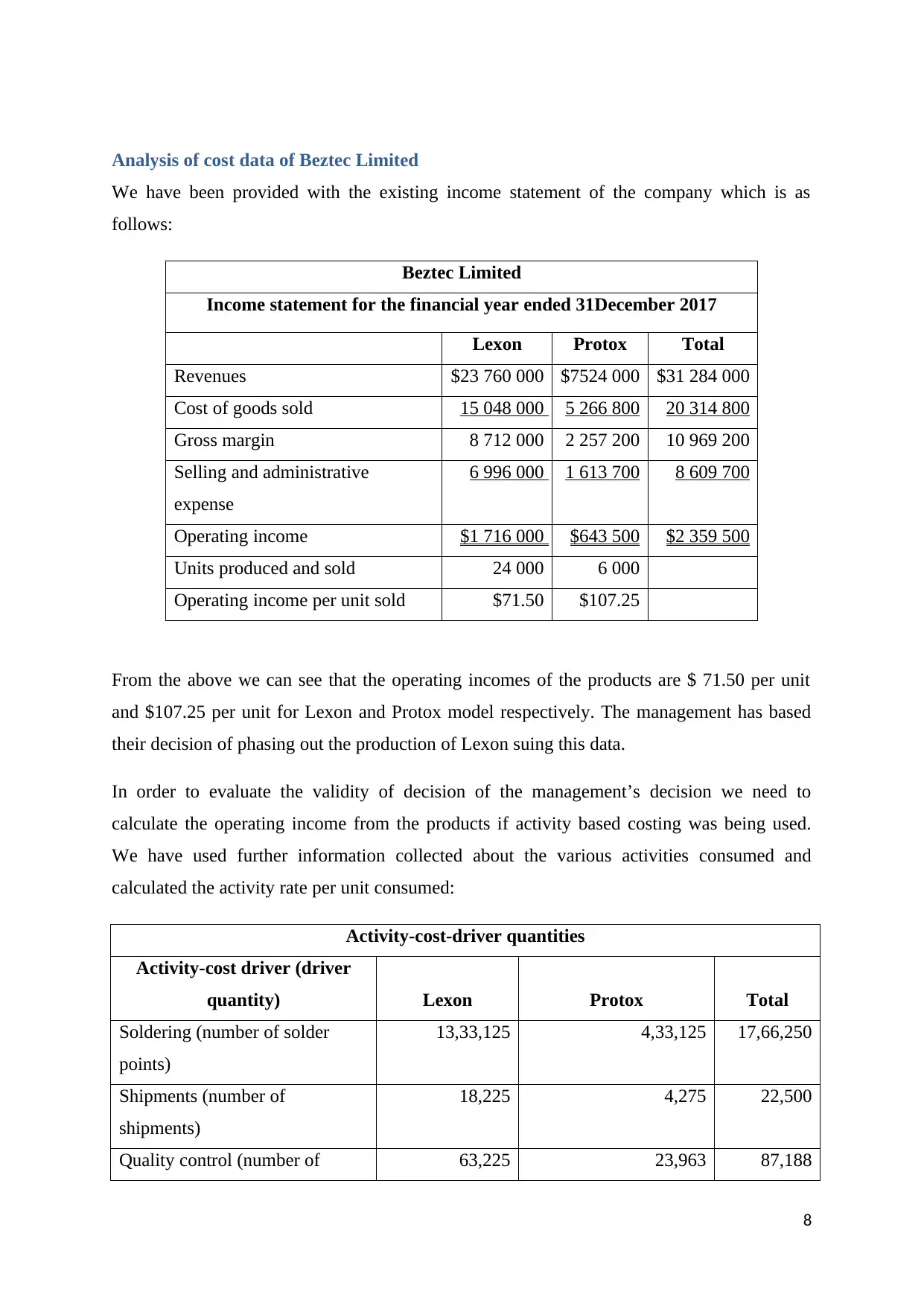

Analysis of cost data of Beztec Limited

We have been provided with the existing income statement of the company which is as

follows:

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues $23 760 000 $7524 000 $31 284 000

Cost of goods sold 15 048 000 5 266 800 20 314 800

Gross margin 8 712 000 2 257 200 10 969 200

Selling and administrative

expense

6 996 000 1 613 700 8 609 700

Operating income $1 716 000 $643 500 $2 359 500

Units produced and sold 24 000 6 000

Operating income per unit sold $71.50 $107.25

From the above we can see that the operating incomes of the products are $ 71.50 per unit

and $107.25 per unit for Lexon and Protox model respectively. The management has based

their decision of phasing out the production of Lexon suing this data.

In order to evaluate the validity of decision of the management’s decision we need to

calculate the operating income from the products if activity based costing was being used.

We have used further information collected about the various activities consumed and

calculated the activity rate per unit consumed:

Activity-cost-driver quantities

Activity-cost driver (driver

quantity) Lexon Protox Total

Soldering (number of solder

points)

13,33,125 4,33,125 17,66,250

Shipments (number of

shipments)

18,225 4,275 22,500

Quality control (number of 63,225 23,963 87,188

8

We have been provided with the existing income statement of the company which is as

follows:

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues $23 760 000 $7524 000 $31 284 000

Cost of goods sold 15 048 000 5 266 800 20 314 800

Gross margin 8 712 000 2 257 200 10 969 200

Selling and administrative

expense

6 996 000 1 613 700 8 609 700

Operating income $1 716 000 $643 500 $2 359 500

Units produced and sold 24 000 6 000

Operating income per unit sold $71.50 $107.25

From the above we can see that the operating incomes of the products are $ 71.50 per unit

and $107.25 per unit for Lexon and Protox model respectively. The management has based

their decision of phasing out the production of Lexon suing this data.

In order to evaluate the validity of decision of the management’s decision we need to

calculate the operating income from the products if activity based costing was being used.

We have used further information collected about the various activities consumed and

calculated the activity rate per unit consumed:

Activity-cost-driver quantities

Activity-cost driver (driver

quantity) Lexon Protox Total

Soldering (number of solder

points)

13,33,125 4,33,125 17,66,250

Shipments (number of

shipments)

18,225 4,275 22,500

Quality control (number of 63,225 23,963 87,188

8

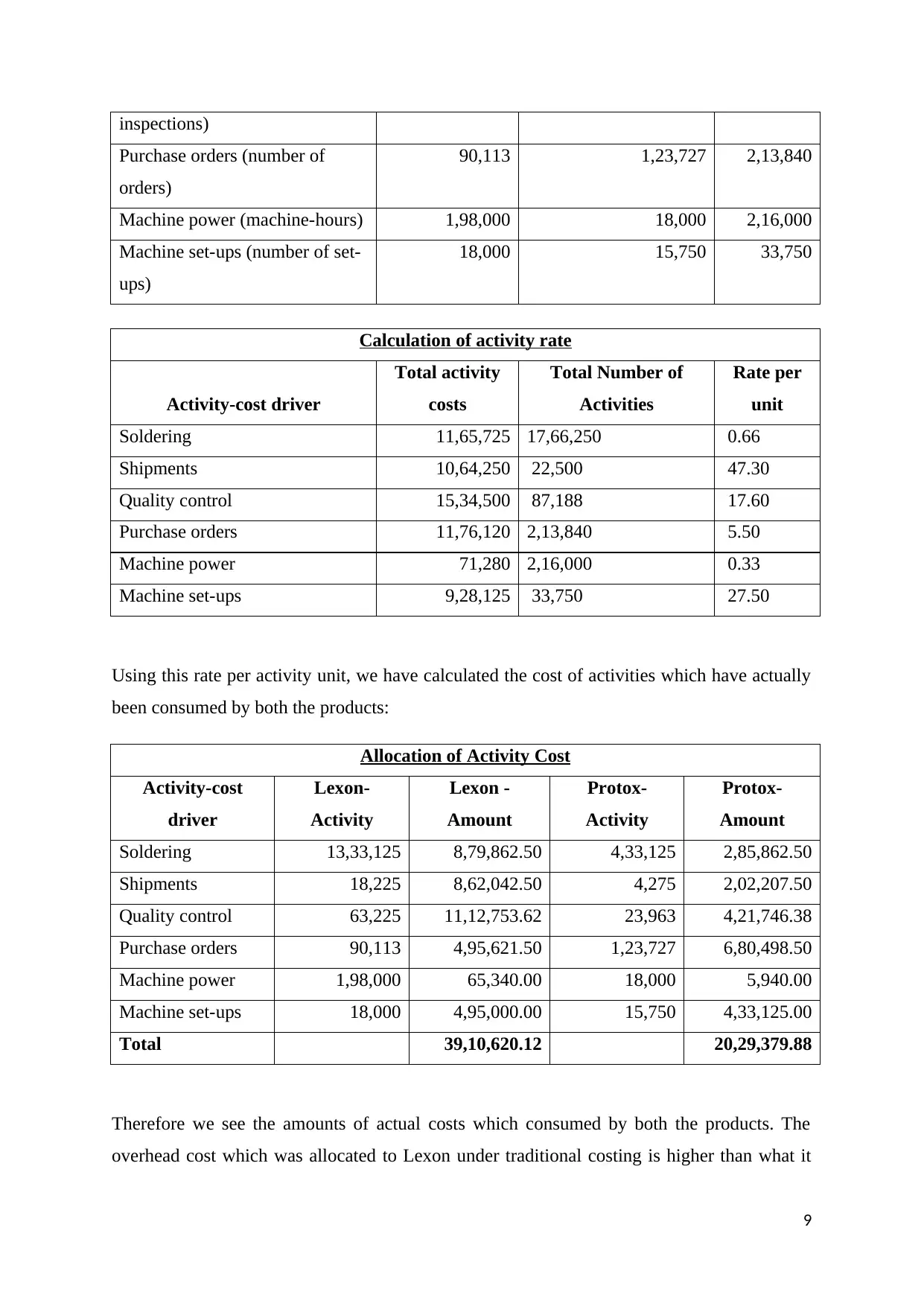

inspections)

Purchase orders (number of

orders)

90,113 1,23,727 2,13,840

Machine power (machine-hours) 1,98,000 18,000 2,16,000

Machine set-ups (number of set-

ups)

18,000 15,750 33,750

Calculation of activity rate

Activity-cost driver

Total activity

costs

Total Number of

Activities

Rate per

unit

Soldering 11,65,725 17,66,250 0.66

Shipments 10,64,250 22,500 47.30

Quality control 15,34,500 87,188 17.60

Purchase orders 11,76,120 2,13,840 5.50

Machine power 71,280 2,16,000 0.33

Machine set-ups 9,28,125 33,750 27.50

Using this rate per activity unit, we have calculated the cost of activities which have actually

been consumed by both the products:

Allocation of Activity Cost

Activity-cost

driver

Lexon-

Activity

Lexon -

Amount

Protox-

Activity

Protox-

Amount

Soldering 13,33,125 8,79,862.50 4,33,125 2,85,862.50

Shipments 18,225 8,62,042.50 4,275 2,02,207.50

Quality control 63,225 11,12,753.62 23,963 4,21,746.38

Purchase orders 90,113 4,95,621.50 1,23,727 6,80,498.50

Machine power 1,98,000 65,340.00 18,000 5,940.00

Machine set-ups 18,000 4,95,000.00 15,750 4,33,125.00

Total 39,10,620.12 20,29,379.88

Therefore we see the amounts of actual costs which consumed by both the products. The

overhead cost which was allocated to Lexon under traditional costing is higher than what it

9

Purchase orders (number of

orders)

90,113 1,23,727 2,13,840

Machine power (machine-hours) 1,98,000 18,000 2,16,000

Machine set-ups (number of set-

ups)

18,000 15,750 33,750

Calculation of activity rate

Activity-cost driver

Total activity

costs

Total Number of

Activities

Rate per

unit

Soldering 11,65,725 17,66,250 0.66

Shipments 10,64,250 22,500 47.30

Quality control 15,34,500 87,188 17.60

Purchase orders 11,76,120 2,13,840 5.50

Machine power 71,280 2,16,000 0.33

Machine set-ups 9,28,125 33,750 27.50

Using this rate per activity unit, we have calculated the cost of activities which have actually

been consumed by both the products:

Allocation of Activity Cost

Activity-cost

driver

Lexon-

Activity

Lexon -

Amount

Protox-

Activity

Protox-

Amount

Soldering 13,33,125 8,79,862.50 4,33,125 2,85,862.50

Shipments 18,225 8,62,042.50 4,275 2,02,207.50

Quality control 63,225 11,12,753.62 23,963 4,21,746.38

Purchase orders 90,113 4,95,621.50 1,23,727 6,80,498.50

Machine power 1,98,000 65,340.00 18,000 5,940.00

Machine set-ups 18,000 4,95,000.00 15,750 4,33,125.00

Total 39,10,620.12 20,29,379.88

Therefore we see the amounts of actual costs which consumed by both the products. The

overhead cost which was allocated to Lexon under traditional costing is higher than what it

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

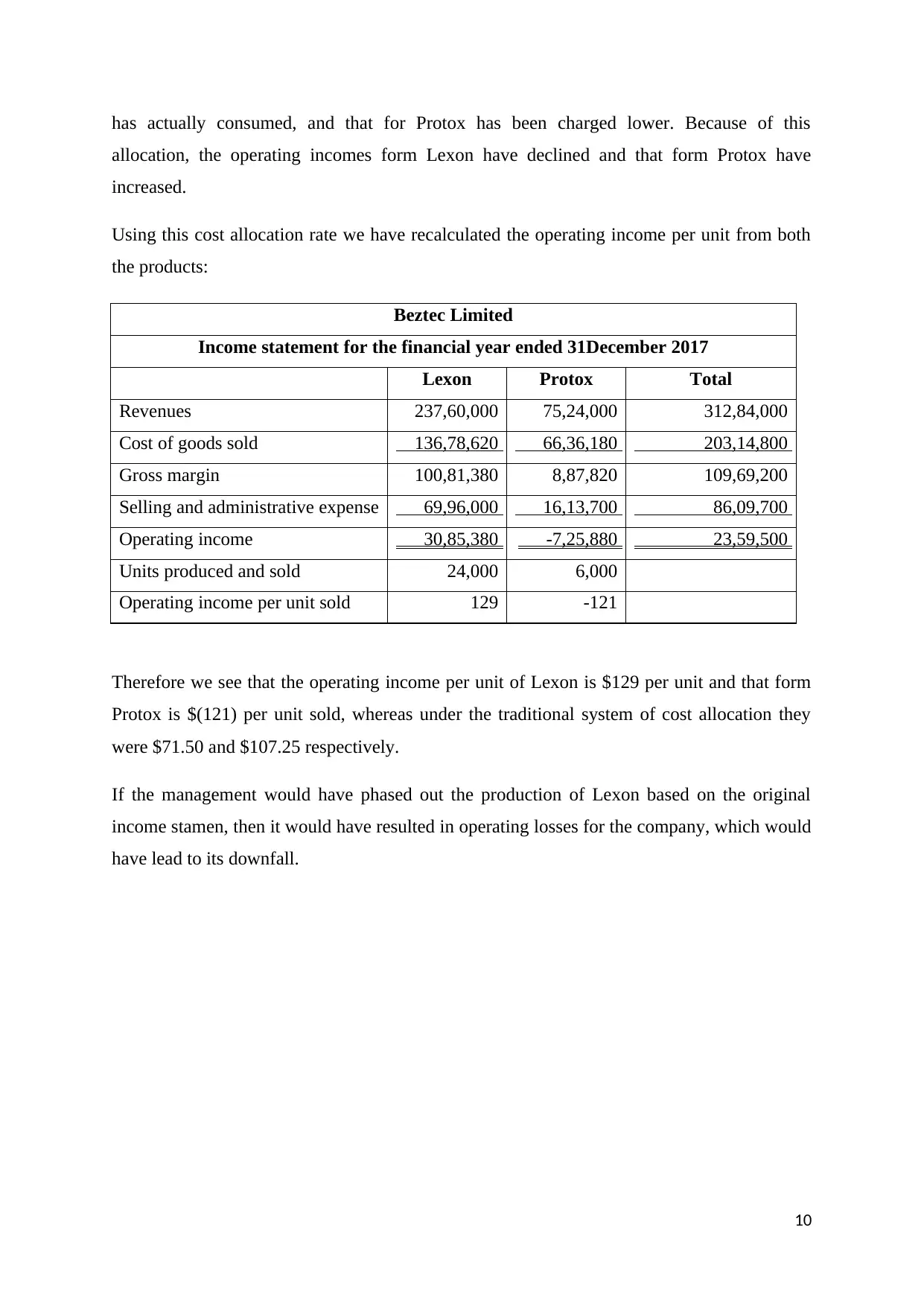

has actually consumed, and that for Protox has been charged lower. Because of this

allocation, the operating incomes form Lexon have declined and that form Protox have

increased.

Using this cost allocation rate we have recalculated the operating income per unit from both

the products:

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues 237,60,000 75,24,000 312,84,000

Cost of goods sold 136,78,620 66,36,180 203,14,800

Gross margin 100,81,380 8,87,820 109,69,200

Selling and administrative expense 69,96,000 16,13,700 86,09,700

Operating income 30,85,380 -7,25,880 23,59,500

Units produced and sold 24,000 6,000

Operating income per unit sold 129 -121

Therefore we see that the operating income per unit of Lexon is $129 per unit and that form

Protox is $(121) per unit sold, whereas under the traditional system of cost allocation they

were $71.50 and $107.25 respectively.

If the management would have phased out the production of Lexon based on the original

income stamen, then it would have resulted in operating losses for the company, which would

have lead to its downfall.

10

allocation, the operating incomes form Lexon have declined and that form Protox have

increased.

Using this cost allocation rate we have recalculated the operating income per unit from both

the products:

Beztec Limited

Income statement for the financial year ended 31December 2017

Lexon Protox Total

Revenues 237,60,000 75,24,000 312,84,000

Cost of goods sold 136,78,620 66,36,180 203,14,800

Gross margin 100,81,380 8,87,820 109,69,200

Selling and administrative expense 69,96,000 16,13,700 86,09,700

Operating income 30,85,380 -7,25,880 23,59,500

Units produced and sold 24,000 6,000

Operating income per unit sold 129 -121

Therefore we see that the operating income per unit of Lexon is $129 per unit and that form

Protox is $(121) per unit sold, whereas under the traditional system of cost allocation they

were $71.50 and $107.25 respectively.

If the management would have phased out the production of Lexon based on the original

income stamen, then it would have resulted in operating losses for the company, which would

have lead to its downfall.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Recommendation for Sue Smith

Smith is the accountant for Beztec Limited and it is her responsibility to make sure that the

financial data show true and correct view. It is her responsibility to ensure that the record

show the true nature of the transactions and the true position of the financials of the company.

Smith is of the view that activity based costing will ensure correct decision making by the

management, but because of the CEO’s personal interest she was forced to implement

traditional costing.

As the accountant of the company it is her responsibility to conduct her duties wills

professionalism (Taillard, 2013). She is responsible to conduct her duties in honest way in

order to ensure heath of the company. She is to conduct her work with total integrity and

objectivity wit professional competence and due care (White, 2009). The decision made by

the CEO, Steven Kay, to still carry the cost allocation based on traditional costing involves a

personal interest. Since his bonuses are dependent on the revenue of various divisions, Kay

wants to ensure that none of the divisions are phased out. Steven has a personal interest in

continuance of the division which has made his opinion biased.

Being the employ of the company it is smith’s responsibility to do correct by the company.

Taking a step in order to secure a financial benefit for the benefit of the CEO is ethically

wrong. The principles of ethic for the accountants also lay out that it is accountant’s duty out

there work with integrity and honesty.

Therefore we would suggest Sue to lay forward the results of both the cost allocation to the

management and the CEO and explain to them about both the results.

11

Smith is the accountant for Beztec Limited and it is her responsibility to make sure that the

financial data show true and correct view. It is her responsibility to ensure that the record

show the true nature of the transactions and the true position of the financials of the company.

Smith is of the view that activity based costing will ensure correct decision making by the

management, but because of the CEO’s personal interest she was forced to implement

traditional costing.

As the accountant of the company it is her responsibility to conduct her duties wills

professionalism (Taillard, 2013). She is responsible to conduct her duties in honest way in

order to ensure heath of the company. She is to conduct her work with total integrity and

objectivity wit professional competence and due care (White, 2009). The decision made by

the CEO, Steven Kay, to still carry the cost allocation based on traditional costing involves a

personal interest. Since his bonuses are dependent on the revenue of various divisions, Kay

wants to ensure that none of the divisions are phased out. Steven has a personal interest in

continuance of the division which has made his opinion biased.

Being the employ of the company it is smith’s responsibility to do correct by the company.

Taking a step in order to secure a financial benefit for the benefit of the CEO is ethically

wrong. The principles of ethic for the accountants also lay out that it is accountant’s duty out

there work with integrity and honesty.

Therefore we would suggest Sue to lay forward the results of both the cost allocation to the

management and the CEO and explain to them about both the results.

11

Analysis of gross profit margin of the company

We have calculated the gross profit margin of the company when it was using traditional

method and when it was using activity based costing, and we have the following data:

Gross Profit analysis

Gross profit margin under traditional costing 36.67 30.00

Gross profit margin under Activity Based costing 42.43 11.80

Therefore, form the above we can see that the gross profit margin for Lexon was 36.67%

under traditional costing method, but it raised to 42.43% under the activity based costing.

Similarly, under traditional method the gross margin for Protox was 30%, but under activity

based costing it reduced to 11.80%. This change in the gross margins for both the product

was result of change in allocation of overhead costs. Therefore, we see that how cost

allocation methods can affect the decision making function of the management.

12

We have calculated the gross profit margin of the company when it was using traditional

method and when it was using activity based costing, and we have the following data:

Gross Profit analysis

Gross profit margin under traditional costing 36.67 30.00

Gross profit margin under Activity Based costing 42.43 11.80

Therefore, form the above we can see that the gross profit margin for Lexon was 36.67%

under traditional costing method, but it raised to 42.43% under the activity based costing.

Similarly, under traditional method the gross margin for Protox was 30%, but under activity

based costing it reduced to 11.80%. This change in the gross margins for both the product

was result of change in allocation of overhead costs. Therefore, we see that how cost

allocation methods can affect the decision making function of the management.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.