Evaluating Job Costing and Process Costing in Milk Production

VerifiedAdded on 2023/06/05

|10

|2193

|255

Report

AI Summary

This report provides a detailed analysis of job costing and process costing methods, with a specific focus on their application in the Australian dairy industry. It explores how Australian dairy producers, such as Norco Co-operative, can utilize these costing systems to optimize their production processes. The report includes a step-by-step product cost outline using the process costing system, illustrated with hypothetical data. Furthermore, it identifies key factors that can increase profitability in the production industry, such as preventing wastage, client retention, market segmentation, velocity, focusing on high-margin products, managing competition, considering the state of the economy, price discrimination, exchange rates, employee skills, and infrastructure.

STUDENT NAME

STUDENT I.D

YEAR/SEMESTER

COURSE

SUBJECT NAME

LECTURER

STUDENT I.D

YEAR/SEMESTER

COURSE

SUBJECT NAME

LECTURER

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

There are two costing methods or systems commonly used in production, and these include Job

costing and Process costing systems.

Job costing method involves the accumulation of data about the costs identified with a specific

production or service. This cost data is useful in determining correct and accurate price quote

that enable the company to make a reasonable profit (Vanderbeck,2012). The cost data is also

helpful for assigning inventorial costs to the manufactured goods. Job costing focus on the three

types of data;

Direct material cost – Job costing should track total material cost used during the job.

Please note, the consideration here must be the only materials using during the task.

Direct labor – the process must track the cost of associated work used. Only direct labor

associated with the job can be recorded

Overheads- This system assigns overheads cost to cost pools, and at the end of the

accounting period, amounts in each cost pool are attached to the different job based on

some allocation methodology. Job costing tailored to the requirements of the customer or

consumer.

Note, Job costing is preferred when a batch is significantly different from the other quantities

(Drury, 2013)

On the other hand, process costing method is preferably used where there is mass production of

the similar products, that is, individual unit cost of output cannot be separated or differentiated

from each other for instance, oil refining, food production, chemical processing among others.

Under this system, the cost data is recorded over the fixed period for each department, summed

together and then allocated to the number of units produced during that time on consistent basis

contrast Job costing where cost is assigned to specific product unit (Turner, 2014).

Note, where the process is costing is associated with the mass production and customized

element, and then the hybrid costing method is used. Process costing is categorized into three;

Weighted average cost – This assumes the total value whether from the preceding period and the

current period are summed together and assigned to the product unit.

There are two costing methods or systems commonly used in production, and these include Job

costing and Process costing systems.

Job costing method involves the accumulation of data about the costs identified with a specific

production or service. This cost data is useful in determining correct and accurate price quote

that enable the company to make a reasonable profit (Vanderbeck,2012). The cost data is also

helpful for assigning inventorial costs to the manufactured goods. Job costing focus on the three

types of data;

Direct material cost – Job costing should track total material cost used during the job.

Please note, the consideration here must be the only materials using during the task.

Direct labor – the process must track the cost of associated work used. Only direct labor

associated with the job can be recorded

Overheads- This system assigns overheads cost to cost pools, and at the end of the

accounting period, amounts in each cost pool are attached to the different job based on

some allocation methodology. Job costing tailored to the requirements of the customer or

consumer.

Note, Job costing is preferred when a batch is significantly different from the other quantities

(Drury, 2013)

On the other hand, process costing method is preferably used where there is mass production of

the similar products, that is, individual unit cost of output cannot be separated or differentiated

from each other for instance, oil refining, food production, chemical processing among others.

Under this system, the cost data is recorded over the fixed period for each department, summed

together and then allocated to the number of units produced during that time on consistent basis

contrast Job costing where cost is assigned to specific product unit (Turner, 2014).

Note, where the process is costing is associated with the mass production and customized

element, and then the hybrid costing method is used. Process costing is categorized into three;

Weighted average cost – This assumes the total value whether from the preceding period and the

current period are summed together and assigned to the product unit.

Standard cost – is calculated similar to weighted average price but the standard value is assigned

to unit products rather than actual cost, then the actual cost is compared to the standard cost, and

the difference is reported as variance in a variance account.

First –In– First – Out (FIFO) –This system creates a layer of cost, that is, the previous layer and

the current layer. Its valuation is based on the assumption that goods are used or sold in

chronological order.

a) Costing Method used by Australian Dairy Producers

In our case of Australian dairy producers, the costing system may depend on the stages of milk

production, for instance where the production is primary then, the producer can use job costing

method, but where the milk production involves a lot of stages, then the producer can employ

process costing method.

I can boldly comment Australian dairy producers use both costing systems in producing milk

because it involves various stages and some independently like raring dairy cows, logistics and

labor among others. Refer to Norco Co-operative Society, our company of reference, the expense

data and the cash flow information shows different activities with some consolidated, and with

no clear insight departmental relevant cost (Norco annual report, 2010).

Where final milk product is to process, it will have to undergo various stages such as storage,

cleaning and screaming, homogenization, fat standardization, heat treatment, chilling,

intermediate storage and finally filling and packaging. Since all this, is done by different

department, then the best costing system is the process costing.

Additionally, at the initial stages of the production specifically from the farmers, they can use job

costing system since the production methods are very dependent.

b) Product cost outline – step by step in the production of a Batch – using process

costing system

Please note, the data provided below is hypothetical, and not real data for the purposes of our

calculation. The financial data of the most production companies in Australia, including Norco

to unit products rather than actual cost, then the actual cost is compared to the standard cost, and

the difference is reported as variance in a variance account.

First –In– First – Out (FIFO) –This system creates a layer of cost, that is, the previous layer and

the current layer. Its valuation is based on the assumption that goods are used or sold in

chronological order.

a) Costing Method used by Australian Dairy Producers

In our case of Australian dairy producers, the costing system may depend on the stages of milk

production, for instance where the production is primary then, the producer can use job costing

method, but where the milk production involves a lot of stages, then the producer can employ

process costing method.

I can boldly comment Australian dairy producers use both costing systems in producing milk

because it involves various stages and some independently like raring dairy cows, logistics and

labor among others. Refer to Norco Co-operative Society, our company of reference, the expense

data and the cash flow information shows different activities with some consolidated, and with

no clear insight departmental relevant cost (Norco annual report, 2010).

Where final milk product is to process, it will have to undergo various stages such as storage,

cleaning and screaming, homogenization, fat standardization, heat treatment, chilling,

intermediate storage and finally filling and packaging. Since all this, is done by different

department, then the best costing system is the process costing.

Additionally, at the initial stages of the production specifically from the farmers, they can use job

costing system since the production methods are very dependent.

b) Product cost outline – step by step in the production of a Batch – using process

costing system

Please note, the data provided below is hypothetical, and not real data for the purposes of our

calculation. The financial data of the most production companies in Australia, including Norco

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

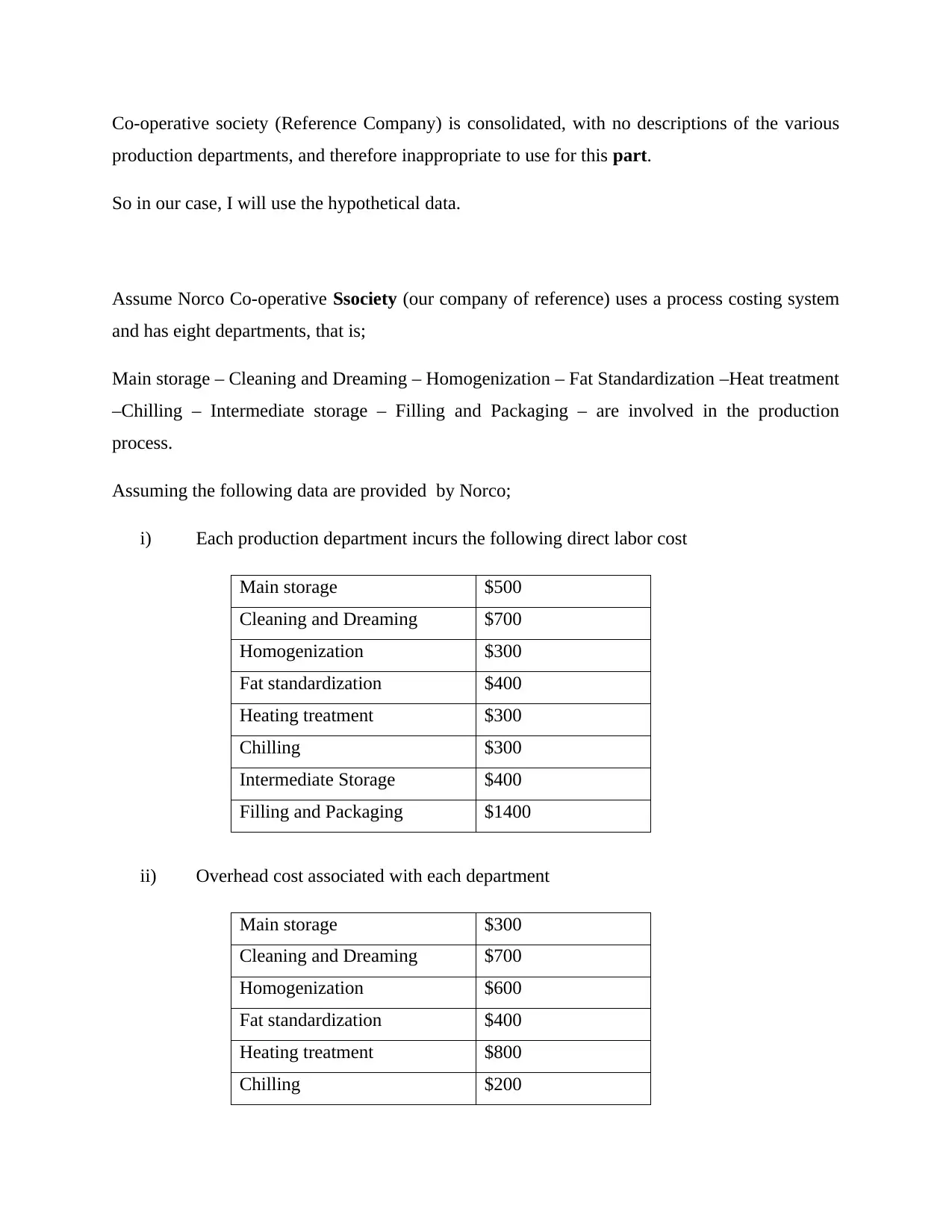

Co-operative society (Reference Company) is consolidated, with no descriptions of the various

production departments, and therefore inappropriate to use for this part.

So in our case, I will use the hypothetical data.

Assume Norco Co-operative Ssociety (our company of reference) uses a process costing system

and has eight departments, that is;

Main storage – Cleaning and Dreaming – Homogenization – Fat Standardization –Heat treatment

–Chilling – Intermediate storage – Filling and Packaging – are involved in the production

process.

Assuming the following data are provided by Norco;

i) Each production department incurs the following direct labor cost

Main storage $500

Cleaning and Dreaming $700

Homogenization $300

Fat standardization $400

Heating treatment $300

Chilling $300

Intermediate Storage $400

Filling and Packaging $1400

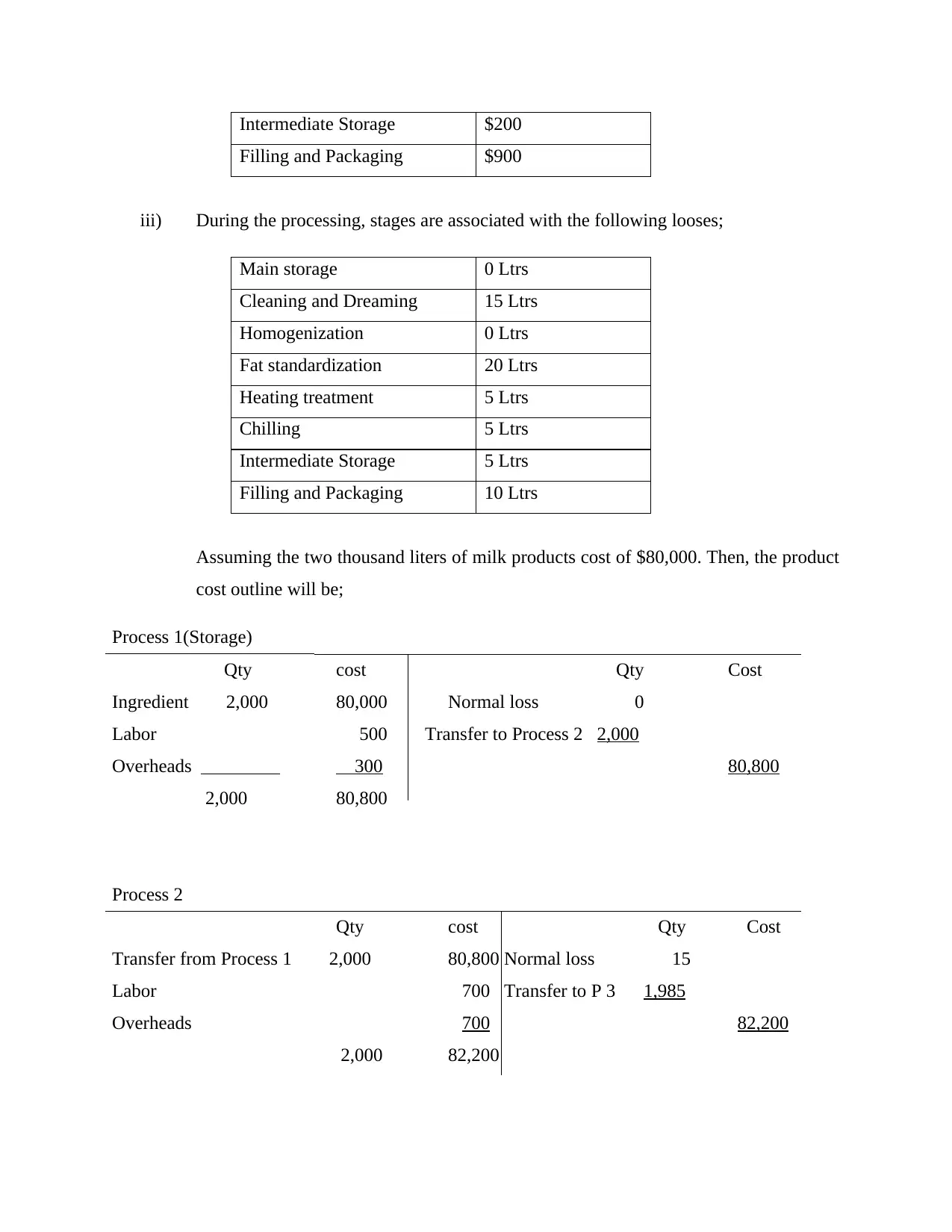

ii) Overhead cost associated with each department

Main storage $300

Cleaning and Dreaming $700

Homogenization $600

Fat standardization $400

Heating treatment $800

Chilling $200

production departments, and therefore inappropriate to use for this part.

So in our case, I will use the hypothetical data.

Assume Norco Co-operative Ssociety (our company of reference) uses a process costing system

and has eight departments, that is;

Main storage – Cleaning and Dreaming – Homogenization – Fat Standardization –Heat treatment

–Chilling – Intermediate storage – Filling and Packaging – are involved in the production

process.

Assuming the following data are provided by Norco;

i) Each production department incurs the following direct labor cost

Main storage $500

Cleaning and Dreaming $700

Homogenization $300

Fat standardization $400

Heating treatment $300

Chilling $300

Intermediate Storage $400

Filling and Packaging $1400

ii) Overhead cost associated with each department

Main storage $300

Cleaning and Dreaming $700

Homogenization $600

Fat standardization $400

Heating treatment $800

Chilling $200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Intermediate Storage $200

Filling and Packaging $900

iii) During the processing, stages are associated with the following looses;

Main storage 0 Ltrs

Cleaning and Dreaming 15 Ltrs

Homogenization 0 Ltrs

Fat standardization 20 Ltrs

Heating treatment 5 Ltrs

Chilling 5 Ltrs

Intermediate Storage 5 Ltrs

Filling and Packaging 10 Ltrs

Assuming the two thousand liters of milk products cost of $80,000. Then, the product

cost outline will be;

Process 1(Storage)

Qty cost Qty Cost

Ingredient 2,000 80,000 Normal loss 0

Labor 500 Transfer to Process 2 2,000

Overheads 300 80,800

2,000 80,800

Process 2

Qty cost Qty Cost

Transfer from Process 1 2,000 80,800 Normal loss 15

Labor 700 Transfer to P 3 1,985

Overheads 700 82,200

2,000 82,200

Filling and Packaging $900

iii) During the processing, stages are associated with the following looses;

Main storage 0 Ltrs

Cleaning and Dreaming 15 Ltrs

Homogenization 0 Ltrs

Fat standardization 20 Ltrs

Heating treatment 5 Ltrs

Chilling 5 Ltrs

Intermediate Storage 5 Ltrs

Filling and Packaging 10 Ltrs

Assuming the two thousand liters of milk products cost of $80,000. Then, the product

cost outline will be;

Process 1(Storage)

Qty cost Qty Cost

Ingredient 2,000 80,000 Normal loss 0

Labor 500 Transfer to Process 2 2,000

Overheads 300 80,800

2,000 80,800

Process 2

Qty cost Qty Cost

Transfer from Process 1 2,000 80,800 Normal loss 15

Labor 700 Transfer to P 3 1,985

Overheads 700 82,200

2,000 82,200

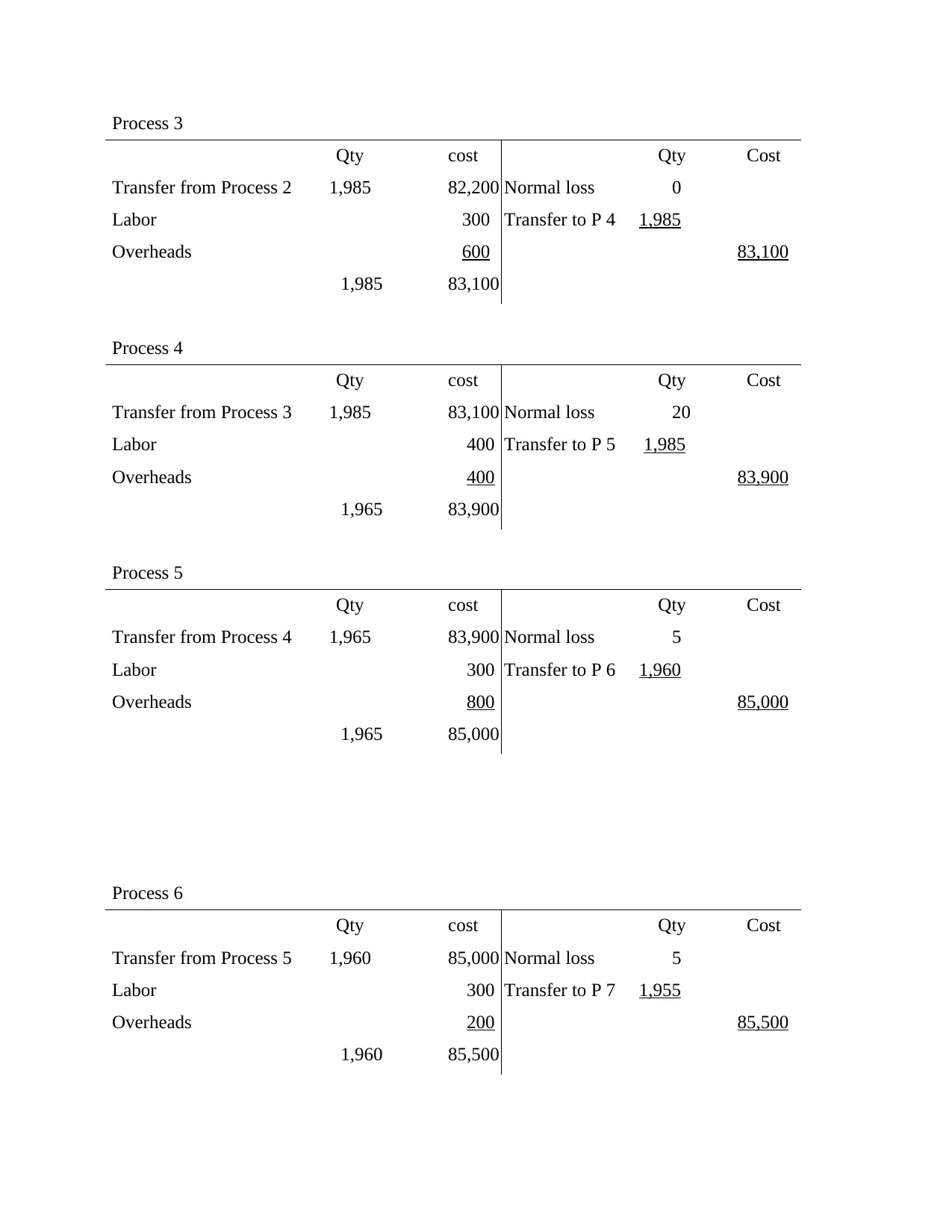

Process 3

Qty cost Qty Cost

Transfer from Process 2 1,985 82,200 Normal loss 0

Labor 300 Transfer to P 4 1,985

Overheads 600 83,100

1,985 83,100

Process 4

Qty cost Qty Cost

Transfer from Process 3 1,985 83,100 Normal loss 20

Labor 400 Transfer to P 5 1,985

Overheads 400 83,900

1,965 83,900

Process 5

Qty cost Qty Cost

Transfer from Process 4 1,965 83,900 Normal loss 5

Labor 300 Transfer to P 6 1,960

Overheads 800 85,000

1,965 85,000

Process 6

Qty cost Qty Cost

Transfer from Process 5 1,960 85,000 Normal loss 5

Labor 300 Transfer to P 7 1,955

Overheads 200 85,500

1,960 85,500

Qty cost Qty Cost

Transfer from Process 2 1,985 82,200 Normal loss 0

Labor 300 Transfer to P 4 1,985

Overheads 600 83,100

1,985 83,100

Process 4

Qty cost Qty Cost

Transfer from Process 3 1,985 83,100 Normal loss 20

Labor 400 Transfer to P 5 1,985

Overheads 400 83,900

1,965 83,900

Process 5

Qty cost Qty Cost

Transfer from Process 4 1,965 83,900 Normal loss 5

Labor 300 Transfer to P 6 1,960

Overheads 800 85,000

1,965 85,000

Process 6

Qty cost Qty Cost

Transfer from Process 5 1,960 85,000 Normal loss 5

Labor 300 Transfer to P 7 1,955

Overheads 200 85,500

1,960 85,500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

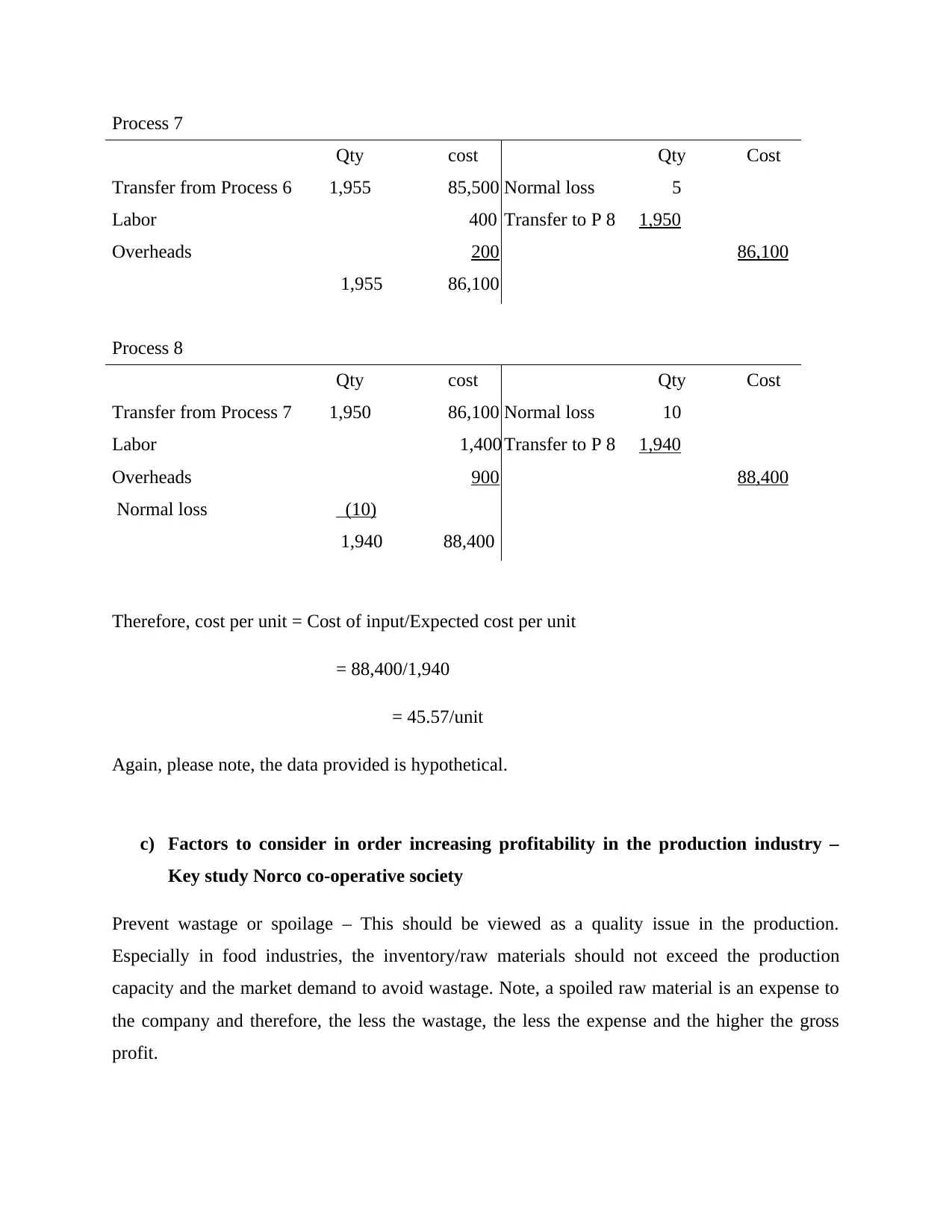

Process 7

Qty cost Qty Cost

Transfer from Process 6 1,955 85,500 Normal loss 5

Labor 400 Transfer to P 8 1,950

Overheads 200 86,100

1,955 86,100

Process 8

Qty cost Qty Cost

Transfer from Process 7 1,950 86,100 Normal loss 10

Labor 1,400 Transfer to P 8 1,940

Overheads 900 88,400

Normal loss (10)

1,940 88,400

Therefore, cost per unit = Cost of input/Expected cost per unit

= 88,400/1,940

= 45.57/unit

Again, please note, the data provided is hypothetical.

c) Factors to consider in order increasing profitability in the production industry –

Key study Norco co-operative society

Prevent wastage or spoilage – This should be viewed as a quality issue in the production.

Especially in food industries, the inventory/raw materials should not exceed the production

capacity and the market demand to avoid wastage. Note, a spoiled raw material is an expense to

the company and therefore, the less the wastage, the less the expense and the higher the gross

profit.

Qty cost Qty Cost

Transfer from Process 6 1,955 85,500 Normal loss 5

Labor 400 Transfer to P 8 1,950

Overheads 200 86,100

1,955 86,100

Process 8

Qty cost Qty Cost

Transfer from Process 7 1,950 86,100 Normal loss 10

Labor 1,400 Transfer to P 8 1,940

Overheads 900 88,400

Normal loss (10)

1,940 88,400

Therefore, cost per unit = Cost of input/Expected cost per unit

= 88,400/1,940

= 45.57/unit

Again, please note, the data provided is hypothetical.

c) Factors to consider in order increasing profitability in the production industry –

Key study Norco co-operative society

Prevent wastage or spoilage – This should be viewed as a quality issue in the production.

Especially in food industries, the inventory/raw materials should not exceed the production

capacity and the market demand to avoid wastage. Note, a spoiled raw material is an expense to

the company and therefore, the less the wastage, the less the expense and the higher the gross

profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Client retention – Retention is associated with attrition costs. Retaining the customers reduces

the cost associated with acquiring new ones. The production industry should focus on the "drop

point" in clients purchase history to keep them actively. Remember, courting your current clients

significantly reduces the acquisition or marketing cost even in the later date.

Creating the market segmentation- This will be able to devise customers according to their

needs. It will also increase the sales per unit and consequently the profit margin since every

customer is valued. Market segmentation will also assist the sales and marketing department to

aggressively work towards reaching the customers fast where the demand is high and therefore

increasing purchase velocity.

Velocity matters – This is the difference between the order and delivery time. The less the time,

the lower the overhead cost per product unit and this mean higher the profit margin. Please note,

the shorter the order to delivery cycle, the more the profit.

Do away with low – margin clients and product and focus on higher producing part of your

business – This enables the production industry focus more on higher margin product and at the

same time, save time and money on production. The company will also concentrate on the high

profile customers and work towards increasing efficiency and quality and therefore increasing

profit margin.

Competition – Production Company should at all the time remain on top of their competitors.

The intensely competitive market will automatically reduce the profitability of the company

since the customer will buy from the cheapest supply. Therefore, the production company should

employ an outstanding competitive strategy to enable them to beat their competitors and remain

active in the market.

State of the economy – Production market should invest more in where the economy is growing.

If there is economic growth the demand is high and the profit margin increases and therefore I

would suggest the company to invest more where the economy is growing.

Price discrimination – charging different prices of the same product depending on the market

environment will automatically increase company sale and at the same time, increase the profit

margin.

the cost associated with acquiring new ones. The production industry should focus on the "drop

point" in clients purchase history to keep them actively. Remember, courting your current clients

significantly reduces the acquisition or marketing cost even in the later date.

Creating the market segmentation- This will be able to devise customers according to their

needs. It will also increase the sales per unit and consequently the profit margin since every

customer is valued. Market segmentation will also assist the sales and marketing department to

aggressively work towards reaching the customers fast where the demand is high and therefore

increasing purchase velocity.

Velocity matters – This is the difference between the order and delivery time. The less the time,

the lower the overhead cost per product unit and this mean higher the profit margin. Please note,

the shorter the order to delivery cycle, the more the profit.

Do away with low – margin clients and product and focus on higher producing part of your

business – This enables the production industry focus more on higher margin product and at the

same time, save time and money on production. The company will also concentrate on the high

profile customers and work towards increasing efficiency and quality and therefore increasing

profit margin.

Competition – Production Company should at all the time remain on top of their competitors.

The intensely competitive market will automatically reduce the profitability of the company

since the customer will buy from the cheapest supply. Therefore, the production company should

employ an outstanding competitive strategy to enable them to beat their competitors and remain

active in the market.

State of the economy – Production market should invest more in where the economy is growing.

If there is economic growth the demand is high and the profit margin increases and therefore I

would suggest the company to invest more where the economy is growing.

Price discrimination – charging different prices of the same product depending on the market

environment will automatically increase company sale and at the same time, increase the profit

margin.

Exchange rate – If the industry relies on exports, depreciation in the exchange rate should

increase the profitability. Therefore the firm should always consider exchange rate whenever

doing the export so that can remain in the money.

Employee skills – Where the production company employee high skilled employees, the work is

done effectively and in efficient way and therefore reducing the cost associated with training and

coaching leading to high profit margin.

Infrastructure – Where the production infrastructure are in good condition, the production tends

to be high since the products are able to reach the market on time and therefore reducing any cost

associated with delay and order cancellation.

increase the profitability. Therefore the firm should always consider exchange rate whenever

doing the export so that can remain in the money.

Employee skills – Where the production company employee high skilled employees, the work is

done effectively and in efficient way and therefore reducing the cost associated with training and

coaching leading to high profit margin.

Infrastructure – Where the production infrastructure are in good condition, the production tends

to be high since the products are able to reach the market on time and therefore reducing any cost

associated with delay and order cancellation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Horngren, C. T., Bhimani, A., Datar, S. M., Foster, G., & Horngren, C. T. (2002). Management

and cost accounting. Harlow: Financial Times/Prentice Hall.

Horngren, C. T. (2009). Cost accounting: A managerial emphasis, 13/e. Pearson Education.

Hilton, R. W., & Platt, D.E.(2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Blocher, E., Chen, K.H., & Lin, W.T. (2002). Cost management: A strategic emphasis.

Garrison, R. H., Noreen, E.W., Brewer, P.C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Vanderbeck, E. J. (2012). The Principles of cost accounting. Cengage Learning.

Fisher, J.G., & Krumwiede, K.(2012). Product costing systems: Finding the right

approach. Journal of Corporate Accounting & Finance, 23(3), 43-51.

Rumble, G. (2012). The costs and economics of open and distance learning. Routledge.

Blocher, E, Chen, K. H., & Lin, W. T. (2002). Cost management: A strategic emphasis.

Drury, C. (2013). Costing: an introduction. Springer.

Laudon, K.C., & Traver, C.G. (2013). E-commerce. Pearson.

Turner, J. R. (2014). Handbook of project-based management (Vol. 92). New York, NY:

McGraw-hill.

Puterman, M. L. (2014). Markov decision processes: discrete stochastic dynamic programming.

John Wiley & Sons.

Horngren, C. T., Bhimani, A., Datar, S. M., Foster, G., & Horngren, C. T. (2002). Management

and cost accounting. Harlow: Financial Times/Prentice Hall.

Horngren, C. T. (2009). Cost accounting: A managerial emphasis, 13/e. Pearson Education.

Hilton, R. W., & Platt, D.E.(2013). Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Blocher, E., Chen, K.H., & Lin, W.T. (2002). Cost management: A strategic emphasis.

Garrison, R. H., Noreen, E.W., Brewer, P.C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Vanderbeck, E. J. (2012). The Principles of cost accounting. Cengage Learning.

Fisher, J.G., & Krumwiede, K.(2012). Product costing systems: Finding the right

approach. Journal of Corporate Accounting & Finance, 23(3), 43-51.

Rumble, G. (2012). The costs and economics of open and distance learning. Routledge.

Blocher, E, Chen, K. H., & Lin, W. T. (2002). Cost management: A strategic emphasis.

Drury, C. (2013). Costing: an introduction. Springer.

Laudon, K.C., & Traver, C.G. (2013). E-commerce. Pearson.

Turner, J. R. (2014). Handbook of project-based management (Vol. 92). New York, NY:

McGraw-hill.

Puterman, M. L. (2014). Markov decision processes: discrete stochastic dynamic programming.

John Wiley & Sons.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.