Evolution of Costing Models: Traditional, ABC, TDABC, and PFABC

VerifiedAdded on 2023/05/27

|12

|7264

|191

Report

AI Summary

This report examines the evolution of costing models, beginning with traditional costing and progressing to Activity Based Costing (ABC), Time Driven Activity Based Costing (TDABC), and Performance Focused Activity Based Costing (PFABC). It highlights the shortcomings of traditional costing, such as the use of a single cost driver and the allocation of overhead costs, which often leads to inaccurate cost prices. The report then introduces ABC, developed to address these issues by allocating costs based on activities. However, it acknowledges the challenges of ABC, including high implementation costs and complexities in data collection. TDABC is then presented as a simplified version of ABC, using time as a cost driver. Finally, the report discusses PFABC, which offers more flexibility in cost allocation by integrating aspects of both ABC and TDABC. The report emphasizes the importance of accurate cost information for managerial decision-making and highlights the ongoing need for costing systems to adapt to changes in technology and business environments.

European Online Journal of Natural and Social Sciences 2013; www.european-science.com

Vol.2, No.3 Special Issue on Accounting and Management.

ISSN 1805-3602

2497

Changing in Costing Models from Traditional to Performance Focused

Activity Based Costing (PFABC)

Fatemeh Kowsari

M.A Student in Industrial Management of Fars Research Science Branch, Islamic Azad

University, Shiraz, Iran

Email: Elham_kowsari1990@yahoo.com

Abstract

This article is aimed at studying changes in models and discussing and comparing the states

of these changes and their advantages. Today, industry and occupation need a costing system to

meet their own needs. Costing experts believe that designing a costing system is only possible by

fulfilling all its needs. On this basis, they developed different costing models for different industries

according to their structures and natures. The most fundamental method used for costing was

traditional costing which utilizes only one cost driver for allocating overhead and caused the

obtained cost price to have a great difference with the real cost price. The costing system based on

Activity Based Costing (ABC1) was designed by Cooper and Kaplan to remove the shortcomings of

traditional costing system and to allocate a cost driver suitable to any activity comparing with

traditional system and to calculate the cost price according to it. However, Activity Based Costing

model is problematic to some extent for organizations because of high costs of interviewing people,

using subjective and expensive approaches for evaluating time allocations and protection difficulties

and updating. Then, Time Driven Activity Based Costing (TDABC2) was introduced which

calculates the costs based on time driver and is simpler and less expensive than Activity Based

Costing model. In addition to solving some of the difficulties of ABC, this model can measure

unused capacity and help managers evaluate the function of different departments. However,

because of great emphasis that this system puts on "time" and due to some limitations, Namazi

introduced Performance Focused Activity Based Costing system (PFABC 3) which has caused more

flexibility in allocating costs to activities by selecting different cost drivers. This model which is an

integration of Activity Based Costing and Time Driven Activity Based Costing undertakes costing

during 8 stages, but the ambiguity and uncertainty in costing systems create some problems for

Performance Focused Activity Based Costing.

Keywords: Activity Based Costing (ABC), Time Driven Activity Based Costing (TDABC),

Performance Focused Activity Based Costing (PFABC).

Introduction

In recent decades, the development of information technology has caused a remarkable

progress in gathering and interchanging cost information in organizations. Along with these

changes, accounting as an important part of an information system has encountered similar changes.

In fact, cost information and cost price by accounting information system are used as an instrument

by managers for planning, controlling and evaluating the operations. These systems can help

managers in performing their duties when they provide them with reliable and correct information.

1 Activity Based Costing

2 Time Driven Activity Based Costing

3 Performance Focused Activity Based Costing

Vol.2, No.3 Special Issue on Accounting and Management.

ISSN 1805-3602

2497

Changing in Costing Models from Traditional to Performance Focused

Activity Based Costing (PFABC)

Fatemeh Kowsari

M.A Student in Industrial Management of Fars Research Science Branch, Islamic Azad

University, Shiraz, Iran

Email: Elham_kowsari1990@yahoo.com

Abstract

This article is aimed at studying changes in models and discussing and comparing the states

of these changes and their advantages. Today, industry and occupation need a costing system to

meet their own needs. Costing experts believe that designing a costing system is only possible by

fulfilling all its needs. On this basis, they developed different costing models for different industries

according to their structures and natures. The most fundamental method used for costing was

traditional costing which utilizes only one cost driver for allocating overhead and caused the

obtained cost price to have a great difference with the real cost price. The costing system based on

Activity Based Costing (ABC1) was designed by Cooper and Kaplan to remove the shortcomings of

traditional costing system and to allocate a cost driver suitable to any activity comparing with

traditional system and to calculate the cost price according to it. However, Activity Based Costing

model is problematic to some extent for organizations because of high costs of interviewing people,

using subjective and expensive approaches for evaluating time allocations and protection difficulties

and updating. Then, Time Driven Activity Based Costing (TDABC2) was introduced which

calculates the costs based on time driver and is simpler and less expensive than Activity Based

Costing model. In addition to solving some of the difficulties of ABC, this model can measure

unused capacity and help managers evaluate the function of different departments. However,

because of great emphasis that this system puts on "time" and due to some limitations, Namazi

introduced Performance Focused Activity Based Costing system (PFABC 3) which has caused more

flexibility in allocating costs to activities by selecting different cost drivers. This model which is an

integration of Activity Based Costing and Time Driven Activity Based Costing undertakes costing

during 8 stages, but the ambiguity and uncertainty in costing systems create some problems for

Performance Focused Activity Based Costing.

Keywords: Activity Based Costing (ABC), Time Driven Activity Based Costing (TDABC),

Performance Focused Activity Based Costing (PFABC).

Introduction

In recent decades, the development of information technology has caused a remarkable

progress in gathering and interchanging cost information in organizations. Along with these

changes, accounting as an important part of an information system has encountered similar changes.

In fact, cost information and cost price by accounting information system are used as an instrument

by managers for planning, controlling and evaluating the operations. These systems can help

managers in performing their duties when they provide them with reliable and correct information.

1 Activity Based Costing

2 Time Driven Activity Based Costing

3 Performance Focused Activity Based Costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fatemeh Kowsari

Openly accessible at http://www.european-science.com 2498

Therefore, in selecting costing systems for calculating the cost price of products and services,

managers should pay special attention. The existence of changes in trade environment has caused

some problems in costing system and has evolved and updated them according to the present needs.

Based on these changes, traditional costing system was replaced by Activity Based Costing system

so that this system could remove the existing faults in traditional costing system. this system has

improved traditional system to a great extent, but because of the high costs of interview,

performance, and updating it made researchers think of creating a new system to remove the above

faults and the obtained information become more exact and correct and help managerial decisions

more than before and made Time Driven Activity Based Costing come to existence which used time

driver to allocate costs to activities. In spite of advantages, this system has some disadvantages the

most important of which was the great emphasis on "time" and this caused the introduction of

Performance Focused Activity Based Costing.

Traditional Costing System

In this system, the costs of direct material and direct payment are directly allocated to the

production. Productive and non-productive overheads have also been considered as direct cost and

allocated to production by using the pre-assigned overhead rate. In traditional costing system, based

on the volume of cost price, each product consists of the sum of the costs of direct material, direct

labor, and the allocated construction overhead.(Shabahang.r, 2012).

The most popular used basis for allocating overhead in determining the type of costing is

direct labor hours. To calculate the overhead rate, the sum of the budgeted construction overhead is

divided by the sum of the direct labor hours or any other basis such as machine labor hours. The

basic difficulty of this system is that it doesn’t give exact information about the cost price of

products and services to decision makers and even by giving wrong information it causes managers

to make mistakes in their decisions and this system cannot be used as a reference for managerial

decisions. Also, in this system the costs of overhead between productions are common. Therefore,

some of the products, according to their production cost, have a greater share in allocating the

overhead. For example, if the construction overhead is allocated according to the direct labor hours,

the products to which have been allocated more direct labor hours will attract more overhead costs

(Tadbir Periodical). In the whole, irrelevant costs of the product unit and the variety of products are

two important factors which have not been considered in traditional costing system. This costing

system is focused more on production cost whereas for marketing and sale costs and other costs no

shares are allocated to production. Traditional systems consider the obtained advantages of changing

the processes and improving the methods as saving money in labor force. Therefore, they do not

show the improvement of functions in operational processes. Using a common basis and unit for

allocating costs such as direct labor hours of human force is considered as another shortcoming of

this type of costing. Because by developing the technology, the rate of human force engaging in

labor process has decreased to a great extent. These shortcomings caused the experts to think of

designing a new costing system that can remove the shortcomings of traditional system.

In traditional system, the cost price of product is calculated as follow:

1- Tracing: allocating direct material and direct payment to products and services.

2- Allocating overhead costs to products or services based on a definite attraction rate.

3- Calculating the cost price of products.(Gahramani, 2008)

In an economically stable time, little attention is paid to effectiveness, but in hard time, it

become essential. Therefore, reassessment of activities and reform, caused by the recent financial

crises, aim to save money and improve work performance in the public, as well as in the private

sector. Public sector organizations may have less incentive for efficiency, and this is related to the

Openly accessible at http://www.european-science.com 2498

Therefore, in selecting costing systems for calculating the cost price of products and services,

managers should pay special attention. The existence of changes in trade environment has caused

some problems in costing system and has evolved and updated them according to the present needs.

Based on these changes, traditional costing system was replaced by Activity Based Costing system

so that this system could remove the existing faults in traditional costing system. this system has

improved traditional system to a great extent, but because of the high costs of interview,

performance, and updating it made researchers think of creating a new system to remove the above

faults and the obtained information become more exact and correct and help managerial decisions

more than before and made Time Driven Activity Based Costing come to existence which used time

driver to allocate costs to activities. In spite of advantages, this system has some disadvantages the

most important of which was the great emphasis on "time" and this caused the introduction of

Performance Focused Activity Based Costing.

Traditional Costing System

In this system, the costs of direct material and direct payment are directly allocated to the

production. Productive and non-productive overheads have also been considered as direct cost and

allocated to production by using the pre-assigned overhead rate. In traditional costing system, based

on the volume of cost price, each product consists of the sum of the costs of direct material, direct

labor, and the allocated construction overhead.(Shabahang.r, 2012).

The most popular used basis for allocating overhead in determining the type of costing is

direct labor hours. To calculate the overhead rate, the sum of the budgeted construction overhead is

divided by the sum of the direct labor hours or any other basis such as machine labor hours. The

basic difficulty of this system is that it doesn’t give exact information about the cost price of

products and services to decision makers and even by giving wrong information it causes managers

to make mistakes in their decisions and this system cannot be used as a reference for managerial

decisions. Also, in this system the costs of overhead between productions are common. Therefore,

some of the products, according to their production cost, have a greater share in allocating the

overhead. For example, if the construction overhead is allocated according to the direct labor hours,

the products to which have been allocated more direct labor hours will attract more overhead costs

(Tadbir Periodical). In the whole, irrelevant costs of the product unit and the variety of products are

two important factors which have not been considered in traditional costing system. This costing

system is focused more on production cost whereas for marketing and sale costs and other costs no

shares are allocated to production. Traditional systems consider the obtained advantages of changing

the processes and improving the methods as saving money in labor force. Therefore, they do not

show the improvement of functions in operational processes. Using a common basis and unit for

allocating costs such as direct labor hours of human force is considered as another shortcoming of

this type of costing. Because by developing the technology, the rate of human force engaging in

labor process has decreased to a great extent. These shortcomings caused the experts to think of

designing a new costing system that can remove the shortcomings of traditional system.

In traditional system, the cost price of product is calculated as follow:

1- Tracing: allocating direct material and direct payment to products and services.

2- Allocating overhead costs to products or services based on a definite attraction rate.

3- Calculating the cost price of products.(Gahramani, 2008)

In an economically stable time, little attention is paid to effectiveness, but in hard time, it

become essential. Therefore, reassessment of activities and reform, caused by the recent financial

crises, aim to save money and improve work performance in the public, as well as in the private

sector. Public sector organizations may have less incentive for efficiency, and this is related to the

Special Issue on Accounting and Management

Openly accessible at http://www.european-science.com 2499

principle of budgetary control. Indeed, a public organization’s budget does not depend on the

efficiency and performance of the organization.

Because of this lack of control, public sector organizations were seldom interested in saving

their budgetary funds. If financially effective and economized, this may well have resulted a lower

budget for the next year (Riinkont.K, Jantson.S, 2011).

Today, in the present social and economic industry, paying attention to productivity and

efficiency is considered as a necessity. Taking in to consideration the great change in technology

and presenting new methods in the early 1980s, organizations found out that they should increase

the quality while decreasing the costs to survive. This subject and the existing shortcomings in

traditional costing system made them revise their accounting and managerial methods. Because of

the shortcomings of traditional system, a new system called Activity Based Costing system came to

existence. In the whole, the most important reasons for the shortcoming of traditional system are as

follows.

1- The lack of ability in presenting information about cost price especially in

organizations which give various services to their customers. Since the traditional system does not

consider the special features of each service in distributing the costs, the allocated costs and the

costs price will be considered wrongly.

2- The lack of separating different cost domains – In traditional system, they use

common cost centers to gather cost payments and overheads. This problem causes the allocation of

unreal costs to the given services.

3- Using common basis and unit for allocating costs – These systems usually used a

division basis to allocate different costs. One of these bases is direct human force labor hours. To

consider the fact with the complexity and quick technology changes, the engaging rate of human

force in labor force has decreased a lot, therefore, by using this basis, the division of cost is not

really done.

4- The lack of preparation exact information about cost price and other necessary

information for decision making. Traditional systems mainly divide the existing costs in

organizations into two groups – Direct costs and periodic costs – and they only consider the direct

costs in calculating the cost price. But in making decision they need to use both of them, direct and

periodic costs. Therefore, based on traditional methods, analysis of the improvement of activities

and methods for decreasing the costs won’t be possible.

5- Traditional systems consider the advantages obtained from changing the processes

and the improvement of methods as saving money in labor force. Therefore, they don’t show the

improvement of functions in operational processes.

6- Traditional costing systems do not show the real information about operational

process and costs. These systems only consider the costs which are easily identifiable in calculating

the costs price, and indirect costs don’t play any roles in calculating cost price (Tadbir).

In addition to shortcomings of traditional system, the growth of competition and the

complexity of technology have intensified the necessity of using new costing systems. Since the

organizations need to access correct information about costs to price products and services, It is

obvious that traditional systems are not efficient enough because of their nature.

The history of Activity Based Costing

In the late 1960s and early 1970s, accounting writers pointed to the relationship between

activity and cost. But in 1980s, because of the reflection of weaknesses and shortcomings of

common accounting systems in giving exact cost information, this relationship was focused on more

by university and occupational centers. This consideration was mainly on the basis of three basic

Openly accessible at http://www.european-science.com 2499

principle of budgetary control. Indeed, a public organization’s budget does not depend on the

efficiency and performance of the organization.

Because of this lack of control, public sector organizations were seldom interested in saving

their budgetary funds. If financially effective and economized, this may well have resulted a lower

budget for the next year (Riinkont.K, Jantson.S, 2011).

Today, in the present social and economic industry, paying attention to productivity and

efficiency is considered as a necessity. Taking in to consideration the great change in technology

and presenting new methods in the early 1980s, organizations found out that they should increase

the quality while decreasing the costs to survive. This subject and the existing shortcomings in

traditional costing system made them revise their accounting and managerial methods. Because of

the shortcomings of traditional system, a new system called Activity Based Costing system came to

existence. In the whole, the most important reasons for the shortcoming of traditional system are as

follows.

1- The lack of ability in presenting information about cost price especially in

organizations which give various services to their customers. Since the traditional system does not

consider the special features of each service in distributing the costs, the allocated costs and the

costs price will be considered wrongly.

2- The lack of separating different cost domains – In traditional system, they use

common cost centers to gather cost payments and overheads. This problem causes the allocation of

unreal costs to the given services.

3- Using common basis and unit for allocating costs – These systems usually used a

division basis to allocate different costs. One of these bases is direct human force labor hours. To

consider the fact with the complexity and quick technology changes, the engaging rate of human

force in labor force has decreased a lot, therefore, by using this basis, the division of cost is not

really done.

4- The lack of preparation exact information about cost price and other necessary

information for decision making. Traditional systems mainly divide the existing costs in

organizations into two groups – Direct costs and periodic costs – and they only consider the direct

costs in calculating the cost price. But in making decision they need to use both of them, direct and

periodic costs. Therefore, based on traditional methods, analysis of the improvement of activities

and methods for decreasing the costs won’t be possible.

5- Traditional systems consider the advantages obtained from changing the processes

and the improvement of methods as saving money in labor force. Therefore, they don’t show the

improvement of functions in operational processes.

6- Traditional costing systems do not show the real information about operational

process and costs. These systems only consider the costs which are easily identifiable in calculating

the costs price, and indirect costs don’t play any roles in calculating cost price (Tadbir).

In addition to shortcomings of traditional system, the growth of competition and the

complexity of technology have intensified the necessity of using new costing systems. Since the

organizations need to access correct information about costs to price products and services, It is

obvious that traditional systems are not efficient enough because of their nature.

The history of Activity Based Costing

In the late 1960s and early 1970s, accounting writers pointed to the relationship between

activity and cost. But in 1980s, because of the reflection of weaknesses and shortcomings of

common accounting systems in giving exact cost information, this relationship was focused on more

by university and occupational centers. This consideration was mainly on the basis of three basic

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fatemeh Kowsari

Openly accessible at http://www.european-science.com 2500

structures. The first structure was a new change in the world which occurred in different countries

especially Japan to introduce modern technology and new productive mechanisms. The second

structure was that in 1980s, the conceptual philosophy of many company managers changed a lot

and in addition to productivity, competition in the world level, and the growth of customers'

satisfaction, the basic goal of managers was to emphasize the quality control of products and to

decrease the costs. The third structure was that some of the accounting writers explained new

product situation, various technology roles, and new viewpoints to manager. They claimed that

traditional systems of industrial accounting and managers are not only responsible for managers'

needs but also their obtained information causes the managers to make wrong decisions. As a result,

the writers tried to introduce a new system called Activity Based Costing (Carol Fia).

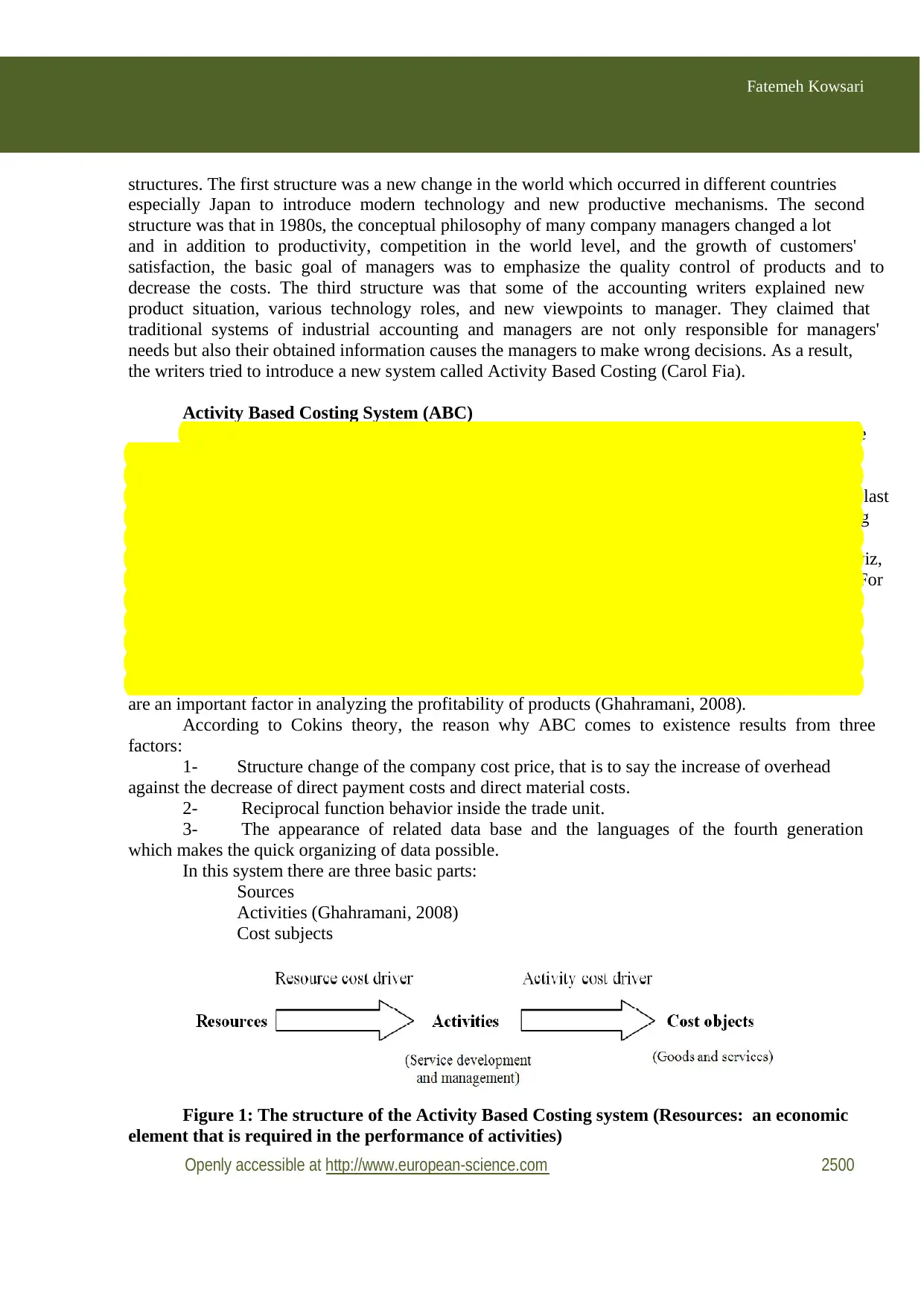

Activity Based Costing System (ABC)

Cooper and Kaplan along with Johnson (1980) have an important role in reflecting the

shortcomings of management accounting system in giving exact cost information. In 1980s, Cooper

and Kaplan suggested Activity Based Costing for the first time and it was used as a creative

invention. ABC is used as the best known method in management accounting during several last

years. In fact, in response to the need of production sector to face the dissatisfaction of using

traditional costing system, this approach depends on allocating overhead to products. In the whole, it

is not logical to use traditional approach in modern production environment (Alinezhad & Saviz,

2013). Today, most of remarkable costs in producing an item are not related to its volume. For

instance, the costs of engineering, order processing, planning, and quality controlling, or the costs of

delivering the products in time don’t relate to the production volume (Riinkont & Jantson,

2011).Activity Based Costing consist of the ability of measuring real sources used by daily activities

of a company that the obtained information of this kind of costing is considered as supporting the

management decision making. Activities done on the basis of costs related to each of the products

are an important factor in analyzing the profitability of products (Ghahramani, 2008).

According to Cokins theory, the reason why ABC comes to existence results from three

factors:

1- Structure change of the company cost price, that is to say the increase of overhead

against the decrease of direct payment costs and direct material costs.

2- Reciprocal function behavior inside the trade unit.

3- The appearance of related data base and the languages of the fourth generation

which makes the quick organizing of data possible.

In this system there are three basic parts:

Sources

Activities (Ghahramani, 2008)

Cost subjects

Figure 1: The structure of the Activity Based Costing system (Resources: an economic

element that is required in the performance of activities)

Openly accessible at http://www.european-science.com 2500

structures. The first structure was a new change in the world which occurred in different countries

especially Japan to introduce modern technology and new productive mechanisms. The second

structure was that in 1980s, the conceptual philosophy of many company managers changed a lot

and in addition to productivity, competition in the world level, and the growth of customers'

satisfaction, the basic goal of managers was to emphasize the quality control of products and to

decrease the costs. The third structure was that some of the accounting writers explained new

product situation, various technology roles, and new viewpoints to manager. They claimed that

traditional systems of industrial accounting and managers are not only responsible for managers'

needs but also their obtained information causes the managers to make wrong decisions. As a result,

the writers tried to introduce a new system called Activity Based Costing (Carol Fia).

Activity Based Costing System (ABC)

Cooper and Kaplan along with Johnson (1980) have an important role in reflecting the

shortcomings of management accounting system in giving exact cost information. In 1980s, Cooper

and Kaplan suggested Activity Based Costing for the first time and it was used as a creative

invention. ABC is used as the best known method in management accounting during several last

years. In fact, in response to the need of production sector to face the dissatisfaction of using

traditional costing system, this approach depends on allocating overhead to products. In the whole, it

is not logical to use traditional approach in modern production environment (Alinezhad & Saviz,

2013). Today, most of remarkable costs in producing an item are not related to its volume. For

instance, the costs of engineering, order processing, planning, and quality controlling, or the costs of

delivering the products in time don’t relate to the production volume (Riinkont & Jantson,

2011).Activity Based Costing consist of the ability of measuring real sources used by daily activities

of a company that the obtained information of this kind of costing is considered as supporting the

management decision making. Activities done on the basis of costs related to each of the products

are an important factor in analyzing the profitability of products (Ghahramani, 2008).

According to Cokins theory, the reason why ABC comes to existence results from three

factors:

1- Structure change of the company cost price, that is to say the increase of overhead

against the decrease of direct payment costs and direct material costs.

2- Reciprocal function behavior inside the trade unit.

3- The appearance of related data base and the languages of the fourth generation

which makes the quick organizing of data possible.

In this system there are three basic parts:

Sources

Activities (Ghahramani, 2008)

Cost subjects

Figure 1: The structure of the Activity Based Costing system (Resources: an economic

element that is required in the performance of activities)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Special Issue on Accounting and Management

Openly accessible at http://www.european-science.com 2501

Cost: the monetary value of resources used or sacrificed or liabilities incurred to achieve an

objective, such as to acquire or produce goods or to perform an activity or service.

Cost driver: factors that cause changes in the cost of an activity.

Resource cost driver: an indicator that helps to associate the costs of resources to

corresponding activities and to distribute the costs of different resources between activities.

Activity: what we do in an organization.

Activity cost driver: a measure of the consumption of an activity by products, customers or

services. Used as a basis of assigning activities to cost objects.

Cost object : an activity, output, or item, of which cost is to be measured. In a broad sense,

the cost object can be an organizational division, a function, task, product, service, or a customer

(Riinkont.K, Jantson.S, 2011).

Adopted approaches in this system are two staged which result in allocating over-head cost

to products or production services.

First stage

1- Identify the main activities and resources which are used in each activity.

2- Allocating the overhead cost to the identified activity which is identified as

accumulated cost.

3- Recognizing the cost drivers relate to each activity after allocating overhead cost to

accumulated cost of the activity.

Second stage

The cost of construction overhead to each activity as to the degree of these of cost drivers in

every production line is allocated (Shabahang, 2012). Activity-Based Costing is an accounting

method used to trace costs to a product or process of an organization. Rather than assigning costs

directly to the products, they are assigned to the activities performed by the company. Then, the

costs of the products are calculated by determining how much each product uses each activity(Jurek

& Bars, 2012).

One of the ABC features which distinguish it from traditional system is paying attention to

the new operational phenomena and the effect of dominant technology on the existing situation.

Furthermore, the kinds of price drivers and the number of price storages distinguish ABC from

traditional system. Cost drivers are an agent that has a direct effect on the function of activities. In

traditional system, price drivers related to the volume such as the amount of production, direct labor

hours, and direct machinery hours are known as the only agent that causes the occurrence of price,

but in ABC approach drivers related to activity are of great importance (Osmani & Ghasemzadeh,

2009).

Activity Based Costing system does not improve tracing the direct costs such as direct

material and payment conceptually, but increases caring in allocating indirect costs that is to say

overhead cost. In another word, ABC can be used to identify and remove the activities which cause

the increase of the costs without making any increased value for the customers (Mehdinezhad &

Seyed Alipoor, 2008). Furthermore, this system consists of product quality and costs related to

flexible productions in addition to direct material and payment costs. This system uses special and

various features in calculating the cost price (Moheb Alipoor & Panjomi Mahmmmodi, 2009).

These method, in calculating the cost price, apply complex, various, and specific features. A

distinct feature of this method is the non-financial information to improve the performance and

efficiency of activities. In addition by applying ABC method, organizational unused capacity

resources can be diagnosed and decreased (Rajabi & Darabi, 2012).

It seems that in spite of a lot of advantages, ABC has two shortcomings:

Openly accessible at http://www.european-science.com 2501

Cost: the monetary value of resources used or sacrificed or liabilities incurred to achieve an

objective, such as to acquire or produce goods or to perform an activity or service.

Cost driver: factors that cause changes in the cost of an activity.

Resource cost driver: an indicator that helps to associate the costs of resources to

corresponding activities and to distribute the costs of different resources between activities.

Activity: what we do in an organization.

Activity cost driver: a measure of the consumption of an activity by products, customers or

services. Used as a basis of assigning activities to cost objects.

Cost object : an activity, output, or item, of which cost is to be measured. In a broad sense,

the cost object can be an organizational division, a function, task, product, service, or a customer

(Riinkont.K, Jantson.S, 2011).

Adopted approaches in this system are two staged which result in allocating over-head cost

to products or production services.

First stage

1- Identify the main activities and resources which are used in each activity.

2- Allocating the overhead cost to the identified activity which is identified as

accumulated cost.

3- Recognizing the cost drivers relate to each activity after allocating overhead cost to

accumulated cost of the activity.

Second stage

The cost of construction overhead to each activity as to the degree of these of cost drivers in

every production line is allocated (Shabahang, 2012). Activity-Based Costing is an accounting

method used to trace costs to a product or process of an organization. Rather than assigning costs

directly to the products, they are assigned to the activities performed by the company. Then, the

costs of the products are calculated by determining how much each product uses each activity(Jurek

& Bars, 2012).

One of the ABC features which distinguish it from traditional system is paying attention to

the new operational phenomena and the effect of dominant technology on the existing situation.

Furthermore, the kinds of price drivers and the number of price storages distinguish ABC from

traditional system. Cost drivers are an agent that has a direct effect on the function of activities. In

traditional system, price drivers related to the volume such as the amount of production, direct labor

hours, and direct machinery hours are known as the only agent that causes the occurrence of price,

but in ABC approach drivers related to activity are of great importance (Osmani & Ghasemzadeh,

2009).

Activity Based Costing system does not improve tracing the direct costs such as direct

material and payment conceptually, but increases caring in allocating indirect costs that is to say

overhead cost. In another word, ABC can be used to identify and remove the activities which cause

the increase of the costs without making any increased value for the customers (Mehdinezhad &

Seyed Alipoor, 2008). Furthermore, this system consists of product quality and costs related to

flexible productions in addition to direct material and payment costs. This system uses special and

various features in calculating the cost price (Moheb Alipoor & Panjomi Mahmmmodi, 2009).

These method, in calculating the cost price, apply complex, various, and specific features. A

distinct feature of this method is the non-financial information to improve the performance and

efficiency of activities. In addition by applying ABC method, organizational unused capacity

resources can be diagnosed and decreased (Rajabi & Darabi, 2012).

It seems that in spite of a lot of advantages, ABC has two shortcomings:

Fatemeh Kowsari

Openly accessible at http://www.european-science.com 2502

The costs of interviewing and analyzing people viewpoints for the early models of

ABC.

High costs of subjective time allocations and the difficulties of updating.

We can point to other ABC shortcoming such as high costs of the number of activity centers

and costing factors and also the necessity of allocating some costs on the basis of volume-based

contract norms.

Simplifying Activity Based Costing

In spite of the simplicity of ABC concept, it is complex and costing to be used by

organizations. In order to solve the problems of using the Activity Based Costing model, researchers

have tried to simplify it in the last two decades. According to simplified model presented by Babad

and Balachandran (1993), at first an optimum upset of drivers of Activity Based Costing complete

model is selected to make a balance between the costs of gathering, maintaining, and data

processing and the benefit resulted from correct information. This model makes it possible for

decision makers to be able to specify and limit most of the drivers in the simplified system. In this

procedure, we should specify an integrated cost storage. In order to create more integrated cost

centers, all of the activities related to selected cost drivers has been omitted and moved into the cost

storage of selected cost drivers. Humborg developed Babad and Balachandran model. According to

Hamborg model, the cost of activities related to the omitted drivers is allocated to several selected

cost drivers instead of allocating to one drivers of selected cost. In this model, the subset of optimum

drivers are selected in a way that their information costs do not increase up to a definite level and the

loss of lack of accuracy resulting from information limitation decreases. The cost storage of selected

drivers consists of the cost of activity related to selected drivers and a share of the costs of activities

related to the omitted drivers. Humborg model is a simplified model which has the same complex

level in comparison with Babad and Balachandran model. Bet in comparing with it, it fives more

correct product costs. Considering the fact that Humborg model presents a more correct system with

less information cost, it is obvious that the simplified model of Babad and Balachandran is not an

optimum one. However, in both models, it is supposed that the simplification should not result in the

cost of losing the information correctness. In both models the act of simplification focuses on the

decrease of the number of activities and drivers so that the cost of the information correctness

resulting from the decrease of activities and incentives will reach a minimum. However, all these

activities required that ABC would be done completely before being simplified. That is to say that

all activities and drivers should be identified before being simplified. This kind of simplification is

called the simplification after the occurrence. It is necessary for the system to be completely done

before being simplified. The simplification will be of no benefit. Furthermore, when the system

needs to be updated, the model should be completely updated first and then simplified which this

procedure need more time and cost. Therefore, having considered the limitation of performing

Activity Based Costing, researchers of accounting thought of replacing a new costing system which

has an easier updating and performing and covers the Activity Based Costing shortcomings. As a

result, the Time Driven Activity Based Costing (TDABC) was introduced (Soltani & Kalani, 2010).

The history of Time Driven Activity Based Costing (TDABC)

The origin of TDABC dates back to 1997. This model was used by Steven Anderson and his

company as Acron Systems. Before 2001, the company of Acron Systems introduced this model

with the name of Activity Based on Transactions. In 2001, Kaplan joined the board of directors of

Acron Company and cooperated in developing this procedure. The result of this cooperation was to

Openly accessible at http://www.european-science.com 2502

The costs of interviewing and analyzing people viewpoints for the early models of

ABC.

High costs of subjective time allocations and the difficulties of updating.

We can point to other ABC shortcoming such as high costs of the number of activity centers

and costing factors and also the necessity of allocating some costs on the basis of volume-based

contract norms.

Simplifying Activity Based Costing

In spite of the simplicity of ABC concept, it is complex and costing to be used by

organizations. In order to solve the problems of using the Activity Based Costing model, researchers

have tried to simplify it in the last two decades. According to simplified model presented by Babad

and Balachandran (1993), at first an optimum upset of drivers of Activity Based Costing complete

model is selected to make a balance between the costs of gathering, maintaining, and data

processing and the benefit resulted from correct information. This model makes it possible for

decision makers to be able to specify and limit most of the drivers in the simplified system. In this

procedure, we should specify an integrated cost storage. In order to create more integrated cost

centers, all of the activities related to selected cost drivers has been omitted and moved into the cost

storage of selected cost drivers. Humborg developed Babad and Balachandran model. According to

Hamborg model, the cost of activities related to the omitted drivers is allocated to several selected

cost drivers instead of allocating to one drivers of selected cost. In this model, the subset of optimum

drivers are selected in a way that their information costs do not increase up to a definite level and the

loss of lack of accuracy resulting from information limitation decreases. The cost storage of selected

drivers consists of the cost of activity related to selected drivers and a share of the costs of activities

related to the omitted drivers. Humborg model is a simplified model which has the same complex

level in comparison with Babad and Balachandran model. Bet in comparing with it, it fives more

correct product costs. Considering the fact that Humborg model presents a more correct system with

less information cost, it is obvious that the simplified model of Babad and Balachandran is not an

optimum one. However, in both models, it is supposed that the simplification should not result in the

cost of losing the information correctness. In both models the act of simplification focuses on the

decrease of the number of activities and drivers so that the cost of the information correctness

resulting from the decrease of activities and incentives will reach a minimum. However, all these

activities required that ABC would be done completely before being simplified. That is to say that

all activities and drivers should be identified before being simplified. This kind of simplification is

called the simplification after the occurrence. It is necessary for the system to be completely done

before being simplified. The simplification will be of no benefit. Furthermore, when the system

needs to be updated, the model should be completely updated first and then simplified which this

procedure need more time and cost. Therefore, having considered the limitation of performing

Activity Based Costing, researchers of accounting thought of replacing a new costing system which

has an easier updating and performing and covers the Activity Based Costing shortcomings. As a

result, the Time Driven Activity Based Costing (TDABC) was introduced (Soltani & Kalani, 2010).

The history of Time Driven Activity Based Costing (TDABC)

The origin of TDABC dates back to 1997. This model was used by Steven Anderson and his

company as Acron Systems. Before 2001, the company of Acron Systems introduced this model

with the name of Activity Based on Transactions. In 2001, Kaplan joined the board of directors of

Acron Company and cooperated in developing this procedure. The result of this cooperation was to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Special Issue on Accounting and Management

Openly accessible at http://www.european-science.com 2503

present the theory of Time Driven Activity Based Costing which simplifies costing process by

omitting staff interview stages and allocation the source cost to activities (Soltani & Kalani, 2010 ).

Time Driven Activity Based Costing (TDABC)

This approach is mainly based on using time driver and its performing method is very

different from performing stages of common method of Activity Based Costing (ABC). Time

Driven Activity Based Costing contrary to ABC system does not identify the activities and allocates

related costs to activities first, but in this approach, the management anticipates the necessary

sources for each cost subject (goods, services, customers) directly. Instead of specifying the time of

presenting questionnaire to them, they determine the cost resources based on time equation and

allocate them to activities and operations performed directly and automatically. This model specifies

the first stage of Activity Based Costing to allocate costs of resources to activities and introduces

time equation to avoid complex and various transactions and summarize the time equations which

an activity is done in a process. Therefore the focus of this approach (TDABC) is on processes

rather than activities and this matter makes the system more controllable (Jurek & Bars, 2012).

This method identifies the capacity of each department or process and allocates the cost of

this capacity of resource groups over the cost object based on the time required to perform an

activity. If the demand for work in these departments or processes declines, TDABC can estimate

the quantity of resources released. TDABC captures the different characteristic of an activity by

time equations in which the time consumed by an activity is a function of different characteristics.

This equation assigns the time and the cost of the activity to the cost object based on characteristics

of each object (Rodriguez & Nasiri, 2012).

Although TDABC is an attractive and simple approach, it is powerful in costing processes of

a commercial unit which prepares comprehensive reports of profit and loss for the most complex

organizations. This model is simpler and less expensive than ABC and its performing is faster. The

simplicity of this model results from the fact that only two parameters for every bureau should be

evaluated.

1- The cost rate of each capacity unit.

2- The using rate of the capacity (different times for each driver) by activities that the

organization does to produce and present services. The using rate of capacity by activities means the

amount of capacity that each transaction, product, or customer uses (Beshkoh & Kazemi, as cited in

Monory & Nasiri, 2012.).

a) estimating the capacity cost rate

To describe the capacity rate of each unit, two evaluations should be done. At first, supplied

capacity cost which is the whole costs of a bureau is calculated and then the practical capacity of

supplied resources will be obtained through dividing the whole costs of each bureau by practical

capacity.

Capacity cost rate=

To describe practical supplied capacity the following cases should be considered:

1 –considering the practical capacity equal to 80% to 90% of nominal capacity.

2 –Using analytic approach: in this approach nominal optimum capacity is considered and

then hours for staff relaxation are subtracted.

To estimate the supplied capacity cost some items such as the cost of indirect payment and

other indirect supporting costs should be considered.

b) determining the rate of capacity use

Openly accessible at http://www.european-science.com 2503

present the theory of Time Driven Activity Based Costing which simplifies costing process by

omitting staff interview stages and allocation the source cost to activities (Soltani & Kalani, 2010 ).

Time Driven Activity Based Costing (TDABC)

This approach is mainly based on using time driver and its performing method is very

different from performing stages of common method of Activity Based Costing (ABC). Time

Driven Activity Based Costing contrary to ABC system does not identify the activities and allocates

related costs to activities first, but in this approach, the management anticipates the necessary

sources for each cost subject (goods, services, customers) directly. Instead of specifying the time of

presenting questionnaire to them, they determine the cost resources based on time equation and

allocate them to activities and operations performed directly and automatically. This model specifies

the first stage of Activity Based Costing to allocate costs of resources to activities and introduces

time equation to avoid complex and various transactions and summarize the time equations which

an activity is done in a process. Therefore the focus of this approach (TDABC) is on processes

rather than activities and this matter makes the system more controllable (Jurek & Bars, 2012).

This method identifies the capacity of each department or process and allocates the cost of

this capacity of resource groups over the cost object based on the time required to perform an

activity. If the demand for work in these departments or processes declines, TDABC can estimate

the quantity of resources released. TDABC captures the different characteristic of an activity by

time equations in which the time consumed by an activity is a function of different characteristics.

This equation assigns the time and the cost of the activity to the cost object based on characteristics

of each object (Rodriguez & Nasiri, 2012).

Although TDABC is an attractive and simple approach, it is powerful in costing processes of

a commercial unit which prepares comprehensive reports of profit and loss for the most complex

organizations. This model is simpler and less expensive than ABC and its performing is faster. The

simplicity of this model results from the fact that only two parameters for every bureau should be

evaluated.

1- The cost rate of each capacity unit.

2- The using rate of the capacity (different times for each driver) by activities that the

organization does to produce and present services. The using rate of capacity by activities means the

amount of capacity that each transaction, product, or customer uses (Beshkoh & Kazemi, as cited in

Monory & Nasiri, 2012.).

a) estimating the capacity cost rate

To describe the capacity rate of each unit, two evaluations should be done. At first, supplied

capacity cost which is the whole costs of a bureau is calculated and then the practical capacity of

supplied resources will be obtained through dividing the whole costs of each bureau by practical

capacity.

Capacity cost rate=

To describe practical supplied capacity the following cases should be considered:

1 –considering the practical capacity equal to 80% to 90% of nominal capacity.

2 –Using analytic approach: in this approach nominal optimum capacity is considered and

then hours for staff relaxation are subtracted.

To estimate the supplied capacity cost some items such as the cost of indirect payment and

other indirect supporting costs should be considered.

b) determining the rate of capacity use

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fatemeh Kowsari

Openly accessible at http://www.european-science.com 2504

In common Activity Based Costing approach; the costs of activity based on transaction

drivers such as the number of machinery fixing times, customer orders, the number of production

times, receiving the material and delivering the products to customers are allocated to the cost

subject. However today, many systems use enterprise resource planning system. This system

presents transaction data such as order headline, customer identity, order details, material lists and

quality details, losses and other important structures related to each order along with other details

quickly and completely. Based on the above conditions and under the enterprise resource planning

system, Time Driven Activity Based Costing (TDABC) can do better than Activity Based Costing

system (ABC) (Alinezhad & Saviz, 2013). In this system after determining the rate capacity cost

rate in bureau, management should determine the rate of capacity consumption in each transaction

for each activity. In this approach the goal is not to determine the exact time but the time

approximation for predicting the model is sufficient. Therefore, in this approach, it is not necessary

to use field study related to the time percent allocated to related activities. TDABC model can be

carried out as follows:

First stage: evaluation the costs of different practiced capacity resource which every resource

provides such as:

1- Identifying the resource groups which perform the activities.

2- Evaluating the cost of each resource group.

3- Evaluating the practical capacity of each resource group.

4- Calculating the cost of each supplied capacity unit for each resource group through

dividing the total cost of each resource.

Second stage: evaluating the time necessary for different activities including:

1- Identifying the factors that affect the time of doing each activity. (time drivers)

2- Making time equations which show the dependence of the time of doing the activity

to all agents.

Third stage: multiplying the cost of each supplied capacity unit of each group of resources by

the time of doing each activity ( Soltani & Kalani, 2010).

The advantages of TDABC

1- Constructing an exact model is made quicker and easier.

2- Having a good conforming with the data which are available in enterprise resource

planning system. This (matter) makes the system more dynamic and at the same time less dependent

on human force.

3- It moves the cost to activities and order by using the characteristics of orders,

processes, suppliers, and customers.

4- It can be used monthly.

5- It creates transparency in using the capacity and proficiency of processes that is to

say it determines the extra capacity.

6- It anticipates thee demand rate of necessary resources and provides the possible

budgeting for capacity resources based the anticipated order rate for the companies.

7- It conforms to the existing model using software and technology of information

banks easily.

8- It’s possible to maintain a quick and less expensive model.

9- It provides clear information for users in identifying the difficulty originally.

10- It’s used in every industry or company with different complexity about customers,

products, units, and processes.

Openly accessible at http://www.european-science.com 2504

In common Activity Based Costing approach; the costs of activity based on transaction

drivers such as the number of machinery fixing times, customer orders, the number of production

times, receiving the material and delivering the products to customers are allocated to the cost

subject. However today, many systems use enterprise resource planning system. This system

presents transaction data such as order headline, customer identity, order details, material lists and

quality details, losses and other important structures related to each order along with other details

quickly and completely. Based on the above conditions and under the enterprise resource planning

system, Time Driven Activity Based Costing (TDABC) can do better than Activity Based Costing

system (ABC) (Alinezhad & Saviz, 2013). In this system after determining the rate capacity cost

rate in bureau, management should determine the rate of capacity consumption in each transaction

for each activity. In this approach the goal is not to determine the exact time but the time

approximation for predicting the model is sufficient. Therefore, in this approach, it is not necessary

to use field study related to the time percent allocated to related activities. TDABC model can be

carried out as follows:

First stage: evaluation the costs of different practiced capacity resource which every resource

provides such as:

1- Identifying the resource groups which perform the activities.

2- Evaluating the cost of each resource group.

3- Evaluating the practical capacity of each resource group.

4- Calculating the cost of each supplied capacity unit for each resource group through

dividing the total cost of each resource.

Second stage: evaluating the time necessary for different activities including:

1- Identifying the factors that affect the time of doing each activity. (time drivers)

2- Making time equations which show the dependence of the time of doing the activity

to all agents.

Third stage: multiplying the cost of each supplied capacity unit of each group of resources by

the time of doing each activity ( Soltani & Kalani, 2010).

The advantages of TDABC

1- Constructing an exact model is made quicker and easier.

2- Having a good conforming with the data which are available in enterprise resource

planning system. This (matter) makes the system more dynamic and at the same time less dependent

on human force.

3- It moves the cost to activities and order by using the characteristics of orders,

processes, suppliers, and customers.

4- It can be used monthly.

5- It creates transparency in using the capacity and proficiency of processes that is to

say it determines the extra capacity.

6- It anticipates thee demand rate of necessary resources and provides the possible

budgeting for capacity resources based the anticipated order rate for the companies.

7- It conforms to the existing model using software and technology of information

banks easily.

8- It’s possible to maintain a quick and less expensive model.

9- It provides clear information for users in identifying the difficulty originally.

10- It’s used in every industry or company with different complexity about customers,

products, units, and processes.

Special Issue on Accounting and Management

Openly accessible at http://www.european-science.com 2505

The disadvantages of TDABC

1- Correct and reliable drivers are not available. If reliable, correct, and exact data are

not available, Time Driven Activity Based Costing causes more problems rather than solving

problems. If the data obtained are of a reliable system such as demand survey automatic systems and

are updated regularly, they will be infallible. But if they are out of date or based on inexact

evaluation, they will result in basic errors. Maybe the difference between the evaluation of carrying

one kilo of material to storage in four minutes or four minutes plus ten seconds won’t be

remarkable. But when it is supposed to carry 100,000 kilos of material into storage we will get a

remarkable number.

2- Differences in time drivers: when time drivers for each transaction are available,

Time Driven Activity Based Costing can be used for calculating each case separately for example,

the parts that take 8 minutes to be carried into a storage will attract costs double in comparison with

those which take four hours, but if a complete order is received and the time necessary for doing it is

calculated by an inexperienced person, the cost price allocated to activities will be unreliable and

will result in wrong decision when the necessary time for carrying goods to customer’s work place

is considered as time driver, it will result in allocating less costs for customers who are nearer and

more costs for those who are father. The cost is also dependent on the distance that is used for

delivering goods. The cited complexity of TDABC becomes greater in calculating when we use the

"origin time". Origin time is the amount of time when the goods is carried from the storage to the

first customer station. A way to treat the time between the stations is to calculate its cost and divide

it among all who are on the way of carrying the goods equally.

3- Collecting and updating data: it is said repeatedly that Time Driven Activity Based

Costing removes the need to researching and collecting data, but it is not true. Each time that the

updated model changes, the time drivers should also be updated. Even if the most repeated

processes change the important point is that if there are reliable systems for determining time

drivers, the management has to depend on staff viewpoints which are expressed based on their

comfort and in making unused capacity.

4- Data volume: activity costing will create separately and by using TDABC a great

volume of data quickly and causes the management analysis and report preparation requiring great

data station and report analyzing instruments to become very powerful (Beshkoh & Kazemi, 2010).

Performance Focused Activity Based Costing

Considering the above problems and the model emphasis on time drivers, Dr.Namazi (2009)

introduced the third generation of costing called Performance Focused Activity Based Costing

(PFABC) to accountants for removing the most important problem due to TDABC. This system can

unite with organization resource programming (ORP) and performance management system to

identify activities which is thought to be a key step in ABC and is omitted in TDABC. The principal

of this method is to use the estimations in calculating products' costs and services such as estimating

the resources needed, overcharge appropriation rate, cost drivers, etc. This needed collecting data

with high expenses and also the standard estimations needed in this system will be very difficult.

This is the greatest disadvantage of PFABC system.

Managers should permanently administer two separate accounting systems. One for

determining the products' expenses and the other is controlling and assessing performance.

Maintaining these two systems has always forced management to encounter high expenses and

problems. To remove this problem, a unified system called Performance Focused Activity Based

Costing (PFABC) was proposed. This new system is based on a nine-step process for each cost item

(Namazi, 2009).

Openly accessible at http://www.european-science.com 2505

The disadvantages of TDABC

1- Correct and reliable drivers are not available. If reliable, correct, and exact data are

not available, Time Driven Activity Based Costing causes more problems rather than solving

problems. If the data obtained are of a reliable system such as demand survey automatic systems and

are updated regularly, they will be infallible. But if they are out of date or based on inexact

evaluation, they will result in basic errors. Maybe the difference between the evaluation of carrying

one kilo of material to storage in four minutes or four minutes plus ten seconds won’t be

remarkable. But when it is supposed to carry 100,000 kilos of material into storage we will get a

remarkable number.

2- Differences in time drivers: when time drivers for each transaction are available,

Time Driven Activity Based Costing can be used for calculating each case separately for example,

the parts that take 8 minutes to be carried into a storage will attract costs double in comparison with

those which take four hours, but if a complete order is received and the time necessary for doing it is

calculated by an inexperienced person, the cost price allocated to activities will be unreliable and

will result in wrong decision when the necessary time for carrying goods to customer’s work place

is considered as time driver, it will result in allocating less costs for customers who are nearer and

more costs for those who are father. The cost is also dependent on the distance that is used for

delivering goods. The cited complexity of TDABC becomes greater in calculating when we use the

"origin time". Origin time is the amount of time when the goods is carried from the storage to the

first customer station. A way to treat the time between the stations is to calculate its cost and divide

it among all who are on the way of carrying the goods equally.

3- Collecting and updating data: it is said repeatedly that Time Driven Activity Based

Costing removes the need to researching and collecting data, but it is not true. Each time that the

updated model changes, the time drivers should also be updated. Even if the most repeated

processes change the important point is that if there are reliable systems for determining time

drivers, the management has to depend on staff viewpoints which are expressed based on their

comfort and in making unused capacity.

4- Data volume: activity costing will create separately and by using TDABC a great

volume of data quickly and causes the management analysis and report preparation requiring great

data station and report analyzing instruments to become very powerful (Beshkoh & Kazemi, 2010).

Performance Focused Activity Based Costing

Considering the above problems and the model emphasis on time drivers, Dr.Namazi (2009)

introduced the third generation of costing called Performance Focused Activity Based Costing

(PFABC) to accountants for removing the most important problem due to TDABC. This system can

unite with organization resource programming (ORP) and performance management system to

identify activities which is thought to be a key step in ABC and is omitted in TDABC. The principal

of this method is to use the estimations in calculating products' costs and services such as estimating

the resources needed, overcharge appropriation rate, cost drivers, etc. This needed collecting data

with high expenses and also the standard estimations needed in this system will be very difficult.

This is the greatest disadvantage of PFABC system.

Managers should permanently administer two separate accounting systems. One for

determining the products' expenses and the other is controlling and assessing performance.

Maintaining these two systems has always forced management to encounter high expenses and

problems. To remove this problem, a unified system called Performance Focused Activity Based

Costing (PFABC) was proposed. This new system is based on a nine-step process for each cost item

(Namazi, 2009).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fatemeh Kowsari

Openly accessible at http://www.european-science.com 2506

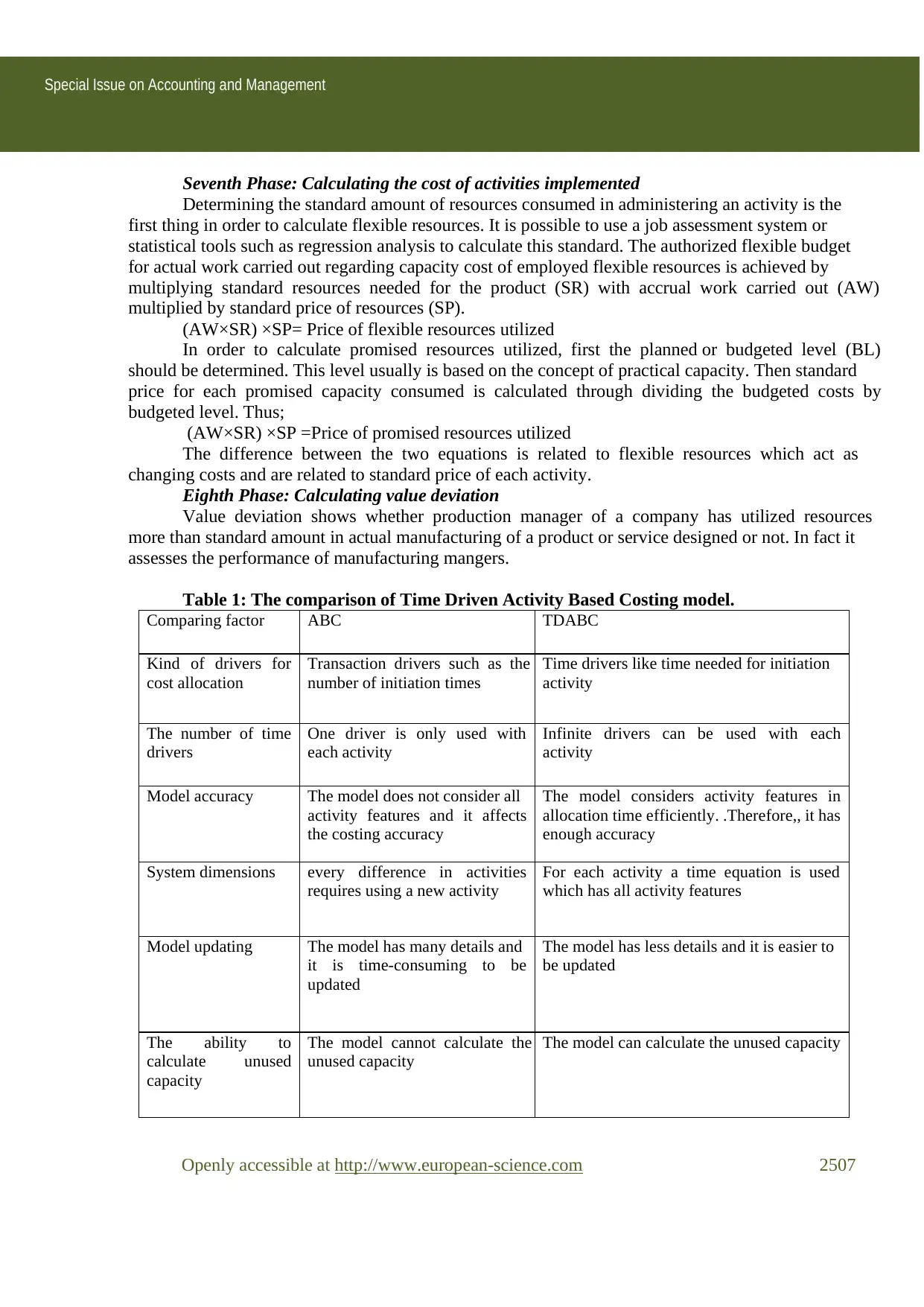

First Phase: Identifying major activities

This step is similar to the first step in traditional ABC which has been omitted in TDABC.

This phase is needed for two reasons: 1- the nature and behavior of costs for each activity is usually

different from other activities. 2- It is one of the major components of ABC which should be

maintained in order to continue the process of administrative production.

Second Phase: Identifying the actual resources needed for each activity

The staffs who administer a designed activity can recognize the type and amount of

resources needed for each activity based on the behavior or companies' data systems, especially

accounting data system. Resources may include time, the amount of direct materials, or other

suitable measures. But resource should have a definite relationship with cost. This creates a great

deal of suppleness in choosing the capacity of different effective resources. This phase includes the

determination of the actual resources' behavior resulted for the cost issue regarding two resources:

flexible resources and promised resources. Flexible resources have behaviors like variable costs and

promised resources have behaviors like fixed costs.

Third Phase: Determining the actual rate of each activity resource

The actual rate of each activity in ABC is determined regarding the time percentage of each

activity carried out by the staffs. In TDABC, only one rate of capacity cost has been determined for

all parts by dividing the cost of the whole capacity utilized to the practical capacity of the resources

used based on the time resource. In PFABC, the actual rates of costs are determined separately for

each of activities done by the company based on different drivers through present data systems

according to the actual data and regarding the resources and behaviors of its costs.

Fourth Phase: Determining the cost for each activity

PFABC determines the cost of each activity regarding the behavior of cost resource. When

the resource is a changing cost, the cost of input factors are calculated by multiplying the actual

resources used in each activity (AR) and the actual price of the resources used (AP).

The actual price of the resources used * the actual resources used = the actual activity cost

AC=AR×AP

Here flexible resources such as direct materials, direct work and production overcharge can

be identified very easily and are determined as flexible resources with changing cost behavior. Also

the promised costs are appropriated by using one of the methods of flexible costs appropriation

approach, cost driver appropriation approach, harmonized average, net retrievable value and multi-

criteria decision making models.

Fifth Phase: Calculating standard rate of activity

This stage is common in ABC and it is not seen in TDABC, but it is a key step in PFABC

process administration. In this step standard rate of each activity should be estimated. This

estimation can be achieved by different tools such as measurement and job assessment techniques,

market mechanisms and internal or external criteria. Also we can administer statistical techniques

such as regression analysis and time sequential models. This standard should be calculated

accurately because it is used as a criterion for comparison with actual rates and actual costs of

operations.

Sixth Phase: Calculating activity price deviation

This stage is not common neither in ABC nor is it present in TDABC. Cost managers gain

price deviation by calculating actual resources needed for each activity multiplied by standard price

for resources consumed and subtracting it from actual cost of each activity. Promised resources

cannot be changed because their amounts are fixed.

Openly accessible at http://www.european-science.com 2506

First Phase: Identifying major activities

This step is similar to the first step in traditional ABC which has been omitted in TDABC.

This phase is needed for two reasons: 1- the nature and behavior of costs for each activity is usually

different from other activities. 2- It is one of the major components of ABC which should be

maintained in order to continue the process of administrative production.

Second Phase: Identifying the actual resources needed for each activity

The staffs who administer a designed activity can recognize the type and amount of

resources needed for each activity based on the behavior or companies' data systems, especially

accounting data system. Resources may include time, the amount of direct materials, or other

suitable measures. But resource should have a definite relationship with cost. This creates a great

deal of suppleness in choosing the capacity of different effective resources. This phase includes the

determination of the actual resources' behavior resulted for the cost issue regarding two resources:

flexible resources and promised resources. Flexible resources have behaviors like variable costs and

promised resources have behaviors like fixed costs.

Third Phase: Determining the actual rate of each activity resource

The actual rate of each activity in ABC is determined regarding the time percentage of each

activity carried out by the staffs. In TDABC, only one rate of capacity cost has been determined for

all parts by dividing the cost of the whole capacity utilized to the practical capacity of the resources

used based on the time resource. In PFABC, the actual rates of costs are determined separately for

each of activities done by the company based on different drivers through present data systems

according to the actual data and regarding the resources and behaviors of its costs.

Fourth Phase: Determining the cost for each activity

PFABC determines the cost of each activity regarding the behavior of cost resource. When

the resource is a changing cost, the cost of input factors are calculated by multiplying the actual

resources used in each activity (AR) and the actual price of the resources used (AP).

The actual price of the resources used * the actual resources used = the actual activity cost

AC=AR×AP

Here flexible resources such as direct materials, direct work and production overcharge can