Costing System in Management Accounting: A Comprehensive Analysis

VerifiedAdded on 2022/08/22

|17

|4179

|29

Report

AI Summary

This report delves into the intricacies of costing systems within managerial accounting, focusing on standard and target costing methods. It begins by defining cost management and the importance of standard costing as a tool for controlling and planning business operations, including its features, objectives, and limitations. The report then examines a case study on standard costing within a telecommunication industry in Nigeria, highlighting its role in cost control and managerial decision-making. It further contrasts standard costing with target costing, explaining the latter's application in product life-cycle stages and strategic planning. The report includes a case study on target costing in the insurance industry, analyzing the factors affecting its implementation. The comparison between the two costing systems provides a holistic view. The report concludes by emphasizing the strategic importance of both costing methods for contemporary organizations, facilitating efficiency, cost control, and informed decision-making.

Running Head: COSTING SYSTEM IN MANAGEMENT ACCOUNTING

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Name of the Student

Name of the University

Author Note

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Executive Summary

The purpose of this report is to understand the cost accounting system and its usefulness in

managerial decisions. This study was supported by analysing a case study on standard costing

and target costing in various industry. It was found that, target costing can be adopted by

contemporary organisation for strategic planning and standard costing can be used for

controlling the cost of business operations.

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Executive Summary

The purpose of this report is to understand the cost accounting system and its usefulness in

managerial decisions. This study was supported by analysing a case study on standard costing

and target costing in various industry. It was found that, target costing can be adopted by

contemporary organisation for strategic planning and standard costing can be used for

controlling the cost of business operations.

2

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Table of Contents

Introduction................................................................................................................................2

Discussions.................................................................................................................................2

The various features of Standard Costing..............................................................................2

Standard Costing relative to the case-study...........................................................................4

The comparison of standard costing and target costing.........................................................6

Target Costing relative to the case study...............................................................................8

Recommendations for contemporary organisations.............................................................10

Conclusion................................................................................................................................10

References................................................................................................................................12

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Table of Contents

Introduction................................................................................................................................2

Discussions.................................................................................................................................2

The various features of Standard Costing..............................................................................2

Standard Costing relative to the case-study...........................................................................4

The comparison of standard costing and target costing.........................................................6

Target Costing relative to the case study...............................................................................8

Recommendations for contemporary organisations.............................................................10

Conclusion................................................................................................................................10

References................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Introduction

Cost management is an efficient process of planning and controlling the cost of the

business operations. It deals with budgeting the business operations and accordingly reduce

the cost. This paper will focus on the importance of standard costing and target costing in the

cost management process. The article is related to a case study on standard costing in a

telecommunication industry of Nigeria and the application of target costing in the Hospitality

industry. The main objective of this report is to understand the cost accounting system and its

usefulness in managerial decisions.

Discussions

The various features of Standard Costing

Standard costing is a very important tool for the management accounting system.

Standard costing is the cost management tool that is sued to find the predetermine cost of a

goods or service or the predetermined cost of the business operations. This cost is used to

compare the predetermine cost with the actual cost of goods or service. Standard costing

system is developed from the historical data. Standard cost of the goods and services mostly

vary from the actual costs because the estimation cost is generally unpredictable. This is a

traditional cost system. This costing system is simple as compared to other costing system

like LIFO & FIIFO. Standard costing system is simple and has several applications to the

business operations. This system is used to estimate the efficiency of the performance related

to cost (ChunSooKim 2017). The predetermine cost is estimated by analysing the change in

variance of the estimated cost with the actual costs. This cost system sets a standard to

exercise the overall costs. The main aim of this costing system is to prefix the cost of the

goods or operation under certain conditions. On the basis of efficiency, variances of the

business operations, the required corrective measurement are done (academia.edu 2020). In

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Introduction

Cost management is an efficient process of planning and controlling the cost of the

business operations. It deals with budgeting the business operations and accordingly reduce

the cost. This paper will focus on the importance of standard costing and target costing in the

cost management process. The article is related to a case study on standard costing in a

telecommunication industry of Nigeria and the application of target costing in the Hospitality

industry. The main objective of this report is to understand the cost accounting system and its

usefulness in managerial decisions.

Discussions

The various features of Standard Costing

Standard costing is a very important tool for the management accounting system.

Standard costing is the cost management tool that is sued to find the predetermine cost of a

goods or service or the predetermined cost of the business operations. This cost is used to

compare the predetermine cost with the actual cost of goods or service. Standard costing

system is developed from the historical data. Standard cost of the goods and services mostly

vary from the actual costs because the estimation cost is generally unpredictable. This is a

traditional cost system. This costing system is simple as compared to other costing system

like LIFO & FIIFO. Standard costing system is simple and has several applications to the

business operations. This system is used to estimate the efficiency of the performance related

to cost (ChunSooKim 2017). The predetermine cost is estimated by analysing the change in

variance of the estimated cost with the actual costs. This cost system sets a standard to

exercise the overall costs. The main aim of this costing system is to prefix the cost of the

goods or operation under certain conditions. On the basis of efficiency, variances of the

business operations, the required corrective measurement are done (academia.edu 2020). In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

this method various statistic methods are used to prepare the difference between the

predetermine cost with the actual costs.

The various objectives of standard costing are:

To increase the efficiency of business operations.

To control the overall cost of the product and operations.

To supplement towards budget control

To provide sufficient information to management for managing the business

activities.

To drive the managerial activities.

Characteristics of standard costing:

1. This is a type of cost determination system that is designed to know the required

output on the basis of future and historical trend.

2. This costing system compare the estimated cost and revenues of the product.

3. This is a type of reporting and reviewing system.

4. Standard cost analyse the variance in the cost of the product.

5. The variance stimulated the business performance.

6. The standard cost determines the cost of labour, overhead cost and direct cost

associated with the business operations.

7. This cost is also known as ideal cost for controlling the cost of operations.

Standard costing system is based on the stock valuation of a company, hence, it can

help the investors in evaluating the company stock. It also motivates the employees by

increasing the efficiency of the operations. Standard costing also facilitates the use of

information & technology in the organisation. By understanding the variance in the cost, the

employees and management will be more responsible towards their work. It can help the

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

this method various statistic methods are used to prepare the difference between the

predetermine cost with the actual costs.

The various objectives of standard costing are:

To increase the efficiency of business operations.

To control the overall cost of the product and operations.

To supplement towards budget control

To provide sufficient information to management for managing the business

activities.

To drive the managerial activities.

Characteristics of standard costing:

1. This is a type of cost determination system that is designed to know the required

output on the basis of future and historical trend.

2. This costing system compare the estimated cost and revenues of the product.

3. This is a type of reporting and reviewing system.

4. Standard cost analyse the variance in the cost of the product.

5. The variance stimulated the business performance.

6. The standard cost determines the cost of labour, overhead cost and direct cost

associated with the business operations.

7. This cost is also known as ideal cost for controlling the cost of operations.

Standard costing system is based on the stock valuation of a company, hence, it can

help the investors in evaluating the company stock. It also motivates the employees by

increasing the efficiency of the operations. Standard costing also facilitates the use of

information & technology in the organisation. By understanding the variance in the cost, the

employees and management will be more responsible towards their work. It can help the

5

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

management in budget planning and according do the business operations. The management

can analyse the variations and find the solutions for the cost control & accordingly prepare

the budget. This costing system also has various limitations. It is not suitable for all type of

firms. Standard costing is not suitable in case of changing environment of business. It gives a

feeling of dissatisfaction among the workforce and employees. It is very difficult to set the

exact standard. One of the main disadvantage is that, this system makes assumptions that, the

cost associated with the business operations doesnot change. But, the business environment is

continuously changing and the cost may also change.

Standard Costing relative to the case-study

This case study is on the impact of standard costing system in the profit of the

manufacturing companies. The article has explored the relationship of standard costing

system with the manufacturing companies. This identifies the various techniques that have

been practiced by Nigerian manufacturing companies. The name of the company that has

been selected is ASL. The company has its operations in various parts of the country. The

main mission of this companies is to provide a high class network of customer loyalty and

quality product. Profit making is the first objective of this company. But, managers in trying

to maximize the profits face various challenges in meeting the technical and globalisation

challenge. There are certain cases in which many of the investments may not be suitable in

making profits. Therefore, the managers are facing various issues in related to cost reduction

for making this profits. They will have to focus on reducing the costs related to marketing

activities, efficient debt management. The article will focus on the various issues in the

company related to cost management that have affected the assets and liabilities of the

company. Standard costing helps the management of this organisation to determine the

predetermine cost of the materials, overheads that is required for manufacturing the services

& products that is supplied. The predetermined cost under the current working conditions is

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

management in budget planning and according do the business operations. The management

can analyse the variations and find the solutions for the cost control & accordingly prepare

the budget. This costing system also has various limitations. It is not suitable for all type of

firms. Standard costing is not suitable in case of changing environment of business. It gives a

feeling of dissatisfaction among the workforce and employees. It is very difficult to set the

exact standard. One of the main disadvantage is that, this system makes assumptions that, the

cost associated with the business operations doesnot change. But, the business environment is

continuously changing and the cost may also change.

Standard Costing relative to the case-study

This case study is on the impact of standard costing system in the profit of the

manufacturing companies. The article has explored the relationship of standard costing

system with the manufacturing companies. This identifies the various techniques that have

been practiced by Nigerian manufacturing companies. The name of the company that has

been selected is ASL. The company has its operations in various parts of the country. The

main mission of this companies is to provide a high class network of customer loyalty and

quality product. Profit making is the first objective of this company. But, managers in trying

to maximize the profits face various challenges in meeting the technical and globalisation

challenge. There are certain cases in which many of the investments may not be suitable in

making profits. Therefore, the managers are facing various issues in related to cost reduction

for making this profits. They will have to focus on reducing the costs related to marketing

activities, efficient debt management. The article will focus on the various issues in the

company related to cost management that have affected the assets and liabilities of the

company. Standard costing helps the management of this organisation to determine the

predetermine cost of the materials, overheads that is required for manufacturing the services

& products that is supplied. The predetermined cost under the current working conditions is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

determined. Accordingly, the expected cost related to quantification of raw materials, cost to

labor, wages cost and cost related to other technical specifications are identified. This cost

will help in increasing the efficiency of the business operations. It facilitates the infrastructure

development and organisational commitment in controlling the cost. It is found that, various

type of standard costing system are adopted by this company. It is recommended that,

standard costing should be executed by the company. Standard costing will help in measuring

the performance through variance analytical method. It can analyse the areas needed for

improvement. The cost can be control and measured accordingly. It also helps in formulating

the price of services. It helps the ASL group to forecast their budget. The management of

ASL group continuously assesses the efficiency of the business with related to profit or

earnings of the company. Profit includes, the management is derived towards maximising the

profit by meeting the demands of the customers, suppliers, employees and their stakeholders

(Abdullahj, Oni and Ahmed 2015). This telecommunication industry has contributed more in

the GDP economy. The company has done more investments in their infrastructure, logistics

and other equipments for improving the quality of the products or services to the customers.

This is only done by controlling the cost of the operations. The cost of the operations are

controlled by proper budgeting of the operations. The management of ASL group is engaged

in employee motivation by setting a standard target, to create a realistic environment for the

employees to reach towards the goal. This enhance the managerial decisions according to the

business strategy. Therefore, it is concluded that, various principles and techniques of

standard costing will help the ASL group to improve their business profit. This system

enhances the planning and decision-making process of the company. (Effect of Standard

Costing on Profitability of Manufacturing Companies: Study of Edo State Nigeria, 2019)

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

determined. Accordingly, the expected cost related to quantification of raw materials, cost to

labor, wages cost and cost related to other technical specifications are identified. This cost

will help in increasing the efficiency of the business operations. It facilitates the infrastructure

development and organisational commitment in controlling the cost. It is found that, various

type of standard costing system are adopted by this company. It is recommended that,

standard costing should be executed by the company. Standard costing will help in measuring

the performance through variance analytical method. It can analyse the areas needed for

improvement. The cost can be control and measured accordingly. It also helps in formulating

the price of services. It helps the ASL group to forecast their budget. The management of

ASL group continuously assesses the efficiency of the business with related to profit or

earnings of the company. Profit includes, the management is derived towards maximising the

profit by meeting the demands of the customers, suppliers, employees and their stakeholders

(Abdullahj, Oni and Ahmed 2015). This telecommunication industry has contributed more in

the GDP economy. The company has done more investments in their infrastructure, logistics

and other equipments for improving the quality of the products or services to the customers.

This is only done by controlling the cost of the operations. The cost of the operations are

controlled by proper budgeting of the operations. The management of ASL group is engaged

in employee motivation by setting a standard target, to create a realistic environment for the

employees to reach towards the goal. This enhance the managerial decisions according to the

business strategy. Therefore, it is concluded that, various principles and techniques of

standard costing will help the ASL group to improve their business profit. This system

enhances the planning and decision-making process of the company. (Effect of Standard

Costing on Profitability of Manufacturing Companies: Study of Edo State Nigeria, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

The features described in the above case study, is similar to the features of standard

costing. It estimates the business expenditures and accordingly take control measures to reach

the business goal.

The comparison of standard costing and target costing

Target costing- This type of costing system is used in determining the cost of the

product in the product life-cycle stage. This is used to determine the target profit of the

business. The main objective of type of costing system is to efficiently manage the business

profitability in the changing market place (Kaplan and Atkinson 2015). It is an effective

planning system in terms of cost reduction and cost management through the design &

development of the product. Target costing system is divided into various sections. In the first

section, it focuses on the market conditions of the product and identifies the cost require to

meet the long-term profit of the business (De Melo et al. 2016). At this stage, the long-term

profits and objectives of the sales are developed by collecting relevant information from the

marketplace, customers and customers. Product mix is also designed at this stage. In the next

section it performs various strategies for reducing the cost associated with the product design

& development. In the last stage, the targeted cost will be functioned by each and every

departments and the suppliers of the organisation (Albers, Revfi and Spadinger 2017). Target

cost will determine the maximum cost that is linked with the product. Target costing is

widely used in the manufacturing, energy and health care industry (Longdong 2016). There

are various factors that affect the target based costing system. These factors are:

Market conditions- The intensity of market conditions are continuously changing.

Competition and change in consumer demand will impact this system in a broader

way. This may also change the company’s strategy (Tommelein and Ballard 2016).

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

The features described in the above case study, is similar to the features of standard

costing. It estimates the business expenditures and accordingly take control measures to reach

the business goal.

The comparison of standard costing and target costing

Target costing- This type of costing system is used in determining the cost of the

product in the product life-cycle stage. This is used to determine the target profit of the

business. The main objective of type of costing system is to efficiently manage the business

profitability in the changing market place (Kaplan and Atkinson 2015). It is an effective

planning system in terms of cost reduction and cost management through the design &

development of the product. Target costing system is divided into various sections. In the first

section, it focuses on the market conditions of the product and identifies the cost require to

meet the long-term profit of the business (De Melo et al. 2016). At this stage, the long-term

profits and objectives of the sales are developed by collecting relevant information from the

marketplace, customers and customers. Product mix is also designed at this stage. In the next

section it performs various strategies for reducing the cost associated with the product design

& development. In the last stage, the targeted cost will be functioned by each and every

departments and the suppliers of the organisation (Albers, Revfi and Spadinger 2017). Target

cost will determine the maximum cost that is linked with the product. Target costing is

widely used in the manufacturing, energy and health care industry (Longdong 2016). There

are various factors that affect the target based costing system. These factors are:

Market conditions- The intensity of market conditions are continuously changing.

Competition and change in consumer demand will impact this system in a broader

way. This may also change the company’s strategy (Tommelein and Ballard 2016).

8

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Change in product strategy-Target costing is used in the product designing &

development stage. The change in complexity of the product in terms of product

duration, level of innovation will affect this type of costing system.

Change in supplier strategy- The nature of relations with the suppliers and the cost

pressure on the suppliers will change the strategy for the supplier. This will impact the

target cost.

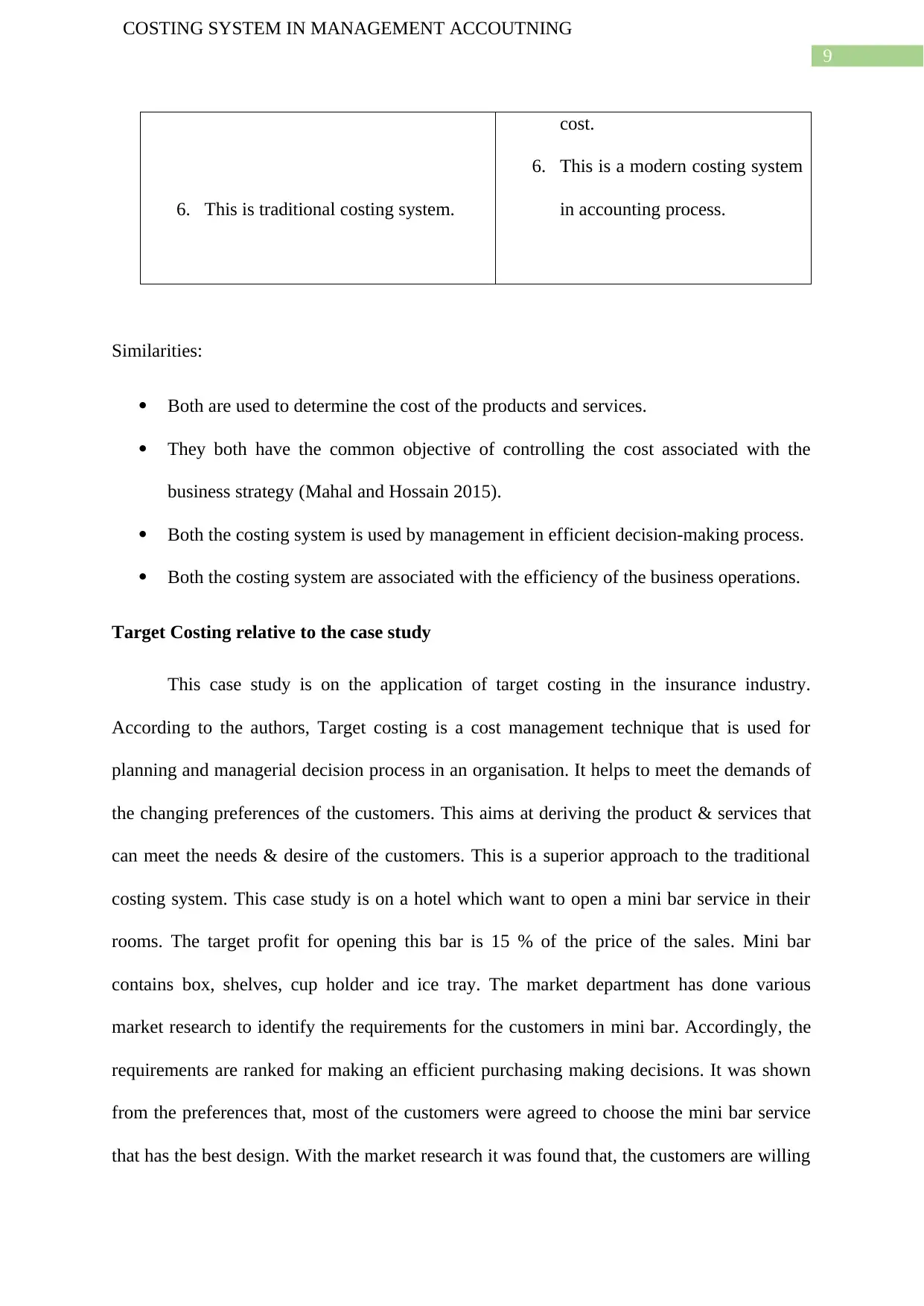

Differences

Standard costing system Target costing system

1. A standard cost is a predetermine

cost or budgeted cost of the product

or services.

2. This cost will reflect the cost of the

current working conditions of the

business (Girish and Panigrahi 2018).

3. The calculation of this system is on

the basis of inward selling.

4. Standard cost is calculated for

existing goods & services.

5. This is helpful to control the costs.

1. A target cost is the desired cost

according to the business

strategy.

2. This cost is not on the basis of

current working conditions.

3. Target costing includes external

selling process of the product. It

includes, price of the goods &

services.

4. Target costing is calculated for

planned products and services.

This is generally calculated at

the product design stage

(Cooper 2017).

5. This is helpful to attain the

targeted profit and the target

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

Change in product strategy-Target costing is used in the product designing &

development stage. The change in complexity of the product in terms of product

duration, level of innovation will affect this type of costing system.

Change in supplier strategy- The nature of relations with the suppliers and the cost

pressure on the suppliers will change the strategy for the supplier. This will impact the

target cost.

Differences

Standard costing system Target costing system

1. A standard cost is a predetermine

cost or budgeted cost of the product

or services.

2. This cost will reflect the cost of the

current working conditions of the

business (Girish and Panigrahi 2018).

3. The calculation of this system is on

the basis of inward selling.

4. Standard cost is calculated for

existing goods & services.

5. This is helpful to control the costs.

1. A target cost is the desired cost

according to the business

strategy.

2. This cost is not on the basis of

current working conditions.

3. Target costing includes external

selling process of the product. It

includes, price of the goods &

services.

4. Target costing is calculated for

planned products and services.

This is generally calculated at

the product design stage

(Cooper 2017).

5. This is helpful to attain the

targeted profit and the target

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

6. This is traditional costing system.

cost.

6. This is a modern costing system

in accounting process.

Similarities:

Both are used to determine the cost of the products and services.

They both have the common objective of controlling the cost associated with the

business strategy (Mahal and Hossain 2015).

Both the costing system is used by management in efficient decision-making process.

Both the costing system are associated with the efficiency of the business operations.

Target Costing relative to the case study

This case study is on the application of target costing in the insurance industry.

According to the authors, Target costing is a cost management technique that is used for

planning and managerial decision process in an organisation. It helps to meet the demands of

the changing preferences of the customers. This aims at deriving the product & services that

can meet the needs & desire of the customers. This is a superior approach to the traditional

costing system. This case study is on a hotel which want to open a mini bar service in their

rooms. The target profit for opening this bar is 15 % of the price of the sales. Mini bar

contains box, shelves, cup holder and ice tray. The market department has done various

market research to identify the requirements for the customers in mini bar. Accordingly, the

requirements are ranked for making an efficient purchasing making decisions. It was shown

from the preferences that, most of the customers were agreed to choose the mini bar service

that has the best design. With the market research it was found that, the customers are willing

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

6. This is traditional costing system.

cost.

6. This is a modern costing system

in accounting process.

Similarities:

Both are used to determine the cost of the products and services.

They both have the common objective of controlling the cost associated with the

business strategy (Mahal and Hossain 2015).

Both the costing system is used by management in efficient decision-making process.

Both the costing system are associated with the efficiency of the business operations.

Target Costing relative to the case study

This case study is on the application of target costing in the insurance industry.

According to the authors, Target costing is a cost management technique that is used for

planning and managerial decision process in an organisation. It helps to meet the demands of

the changing preferences of the customers. This aims at deriving the product & services that

can meet the needs & desire of the customers. This is a superior approach to the traditional

costing system. This case study is on a hotel which want to open a mini bar service in their

rooms. The target profit for opening this bar is 15 % of the price of the sales. Mini bar

contains box, shelves, cup holder and ice tray. The market department has done various

market research to identify the requirements for the customers in mini bar. Accordingly, the

requirements are ranked for making an efficient purchasing making decisions. It was shown

from the preferences that, most of the customers were agreed to choose the mini bar service

that has the best design. With the market research it was found that, the customers are willing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

to pay 35 Euro for the mini bar service. Hence, it covers all the cost necessary for the

production & purchase purpose. The target price was on the basis of market analysis on

market competition and customer demands. The target price was easily evaluated by doing

the market analysis of the target customers. The authors gave attention to the fact that, the

overall cost in the market is drawn through various factors. The most important factor is level

of competition & the sale price of the existing products. The buyers will be willing to pay

more if the product gives more value than the existing product. Therefore, the company must

build knowledge to design the product in such a way that, it can add more value to the

customers. Value making is the key factor to analyse the target price of the production. The

next step in product pricing is identifying the target cost. Target cost should be done on the

basis of long-term strategy of the organisation. Long-term strategy is done on the basis of

market size, market competition and sales. Target costing system determines the cost of new

product or services by comparing the specifications of the existing product in the business

(Pajrok 2020). The traditional costing system will unable to analyse the today’s market

conditions of the product or services. Therefore, it is concluded in the case study that, target

costing is a managerial accounting system that is focused on efficient planning of the product

design and cost reduction. It focus on integrating the strategic variable with the product. This

costing system plays a very important role in product development. It contributes to cost

reduction in the product life cycle stage. This method requires the managerial support to

direct the business strategy in all level of organisation (Arifin 2016). Target costing system is

benefit for the hospitality industry for identifying the customer requirements. (Wakefield and

Thambar, 2019)

From the above case study, it is clear that target costing system of accounting is

relevant for meeting the demands of today’s competitive environment. This system helps in

determining the target profit by doing market analysis (Do, Ballard and Tommelein 2015).

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

to pay 35 Euro for the mini bar service. Hence, it covers all the cost necessary for the

production & purchase purpose. The target price was on the basis of market analysis on

market competition and customer demands. The target price was easily evaluated by doing

the market analysis of the target customers. The authors gave attention to the fact that, the

overall cost in the market is drawn through various factors. The most important factor is level

of competition & the sale price of the existing products. The buyers will be willing to pay

more if the product gives more value than the existing product. Therefore, the company must

build knowledge to design the product in such a way that, it can add more value to the

customers. Value making is the key factor to analyse the target price of the production. The

next step in product pricing is identifying the target cost. Target cost should be done on the

basis of long-term strategy of the organisation. Long-term strategy is done on the basis of

market size, market competition and sales. Target costing system determines the cost of new

product or services by comparing the specifications of the existing product in the business

(Pajrok 2020). The traditional costing system will unable to analyse the today’s market

conditions of the product or services. Therefore, it is concluded in the case study that, target

costing is a managerial accounting system that is focused on efficient planning of the product

design and cost reduction. It focus on integrating the strategic variable with the product. This

costing system plays a very important role in product development. It contributes to cost

reduction in the product life cycle stage. This method requires the managerial support to

direct the business strategy in all level of organisation (Arifin 2016). Target costing system is

benefit for the hospitality industry for identifying the customer requirements. (Wakefield and

Thambar, 2019)

From the above case study, it is clear that target costing system of accounting is

relevant for meeting the demands of today’s competitive environment. This system helps in

determining the target profit by doing market analysis (Do, Ballard and Tommelein 2015).

11

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

The level of competition and customer’s requirement helps in identifying the target profit of a

company (Oliva et al. 2016). The case study has showed that, target costing is relevant to the

hospitality industry in doing market research and adding value to the customers.

Recommendations for contemporary organisations

From the above study on standard costing and target costing, it is recommended that,

contemporary organisation should use both the system for enhancing their cost management

process. Contemporary organisations will have to deal with the changing trends of the

customers. The managers are involved in accomplishing the business goal by cost control

process. Both the system will help the management for making decisions efficiently. Out of

the two costing system, target costing system is used for planning purpose and standard

costing system can be used for cost controlling process. Target costing is used for planning

purpose because, it sets the targeted profit of the business operations at the product

development stage. It helps to facilitate the quality of the product or services (Dale and

Plunkett 2017). This costing system will help to create value to the product or services for the

customers. But, it can only analyse the cost of existing product, it cannot predict the future

cost of the business operations. Therefore, in this case standard costing system will be helpful

for the company. Standard costing system can be used for controlling the cost because it

determines the predetermined cost of the products or services and relates the estimated cost

with the actual cost of associated with the product or services (Baral 2016). The management

can predetermine the cost and the change in variance associated with the cost, hence,

accordingly control the cost of the business operations (Navissi and Sridharan 2017).

Therefore, the management of the contemporary organistaions should adopt both the costing

system for efficiently manage their cost and making efficient decisions to reach the business

goals.

COSTING SYSTEM IN MANAGEMENT ACCOUTNING

The level of competition and customer’s requirement helps in identifying the target profit of a

company (Oliva et al. 2016). The case study has showed that, target costing is relevant to the

hospitality industry in doing market research and adding value to the customers.

Recommendations for contemporary organisations

From the above study on standard costing and target costing, it is recommended that,

contemporary organisation should use both the system for enhancing their cost management

process. Contemporary organisations will have to deal with the changing trends of the

customers. The managers are involved in accomplishing the business goal by cost control

process. Both the system will help the management for making decisions efficiently. Out of

the two costing system, target costing system is used for planning purpose and standard

costing system can be used for cost controlling process. Target costing is used for planning

purpose because, it sets the targeted profit of the business operations at the product

development stage. It helps to facilitate the quality of the product or services (Dale and

Plunkett 2017). This costing system will help to create value to the product or services for the

customers. But, it can only analyse the cost of existing product, it cannot predict the future

cost of the business operations. Therefore, in this case standard costing system will be helpful

for the company. Standard costing system can be used for controlling the cost because it

determines the predetermined cost of the products or services and relates the estimated cost

with the actual cost of associated with the product or services (Baral 2016). The management

can predetermine the cost and the change in variance associated with the cost, hence,

accordingly control the cost of the business operations (Navissi and Sridharan 2017).

Therefore, the management of the contemporary organistaions should adopt both the costing

system for efficiently manage their cost and making efficient decisions to reach the business

goals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.