Management Accounting: Evaluating Costing Methods and Profitability

VerifiedAdded on 2023/06/11

|11

|2600

|325

Report

AI Summary

This management accounting report provides a comparative analysis of traditional costing and activity-based costing (ABC) systems. It evaluates the impact of different costing methods on product costs and profitability, using Sewing Easy Ltd as a case study. The report includes calculations for overhead allocation, product costing under both systems, and profit and loss statements. It discusses the advantages and limitations of ABC, highlighting its potential for more accurate cost allocation and improved decision-making. The analysis shows how ABC can provide a more realistic view of product costs, especially for advanced models with specific activity requirements, ultimately affecting pricing strategies and market competitiveness. Desklib offers this document as a valuable resource for students studying management accounting.

Management Accounting- Questions

and Answers

1 | P a g e

and Answers

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Answer to Question No. 1...........................................................................................................................3

Answer to question No.2.............................................................................................................................3

Answer to Question no. 3............................................................................................................................5

Answer to Question No. 4...........................................................................................................................7

Answer to Question No. 5...........................................................................................................................8

References:................................................................................................................................................11

2 | P a g e

Answer to Question No. 1...........................................................................................................................3

Answer to question No.2.............................................................................................................................3

Answer to Question no. 3............................................................................................................................5

Answer to Question No. 4...........................................................................................................................7

Answer to Question No. 5...........................................................................................................................8

References:................................................................................................................................................11

2 | P a g e

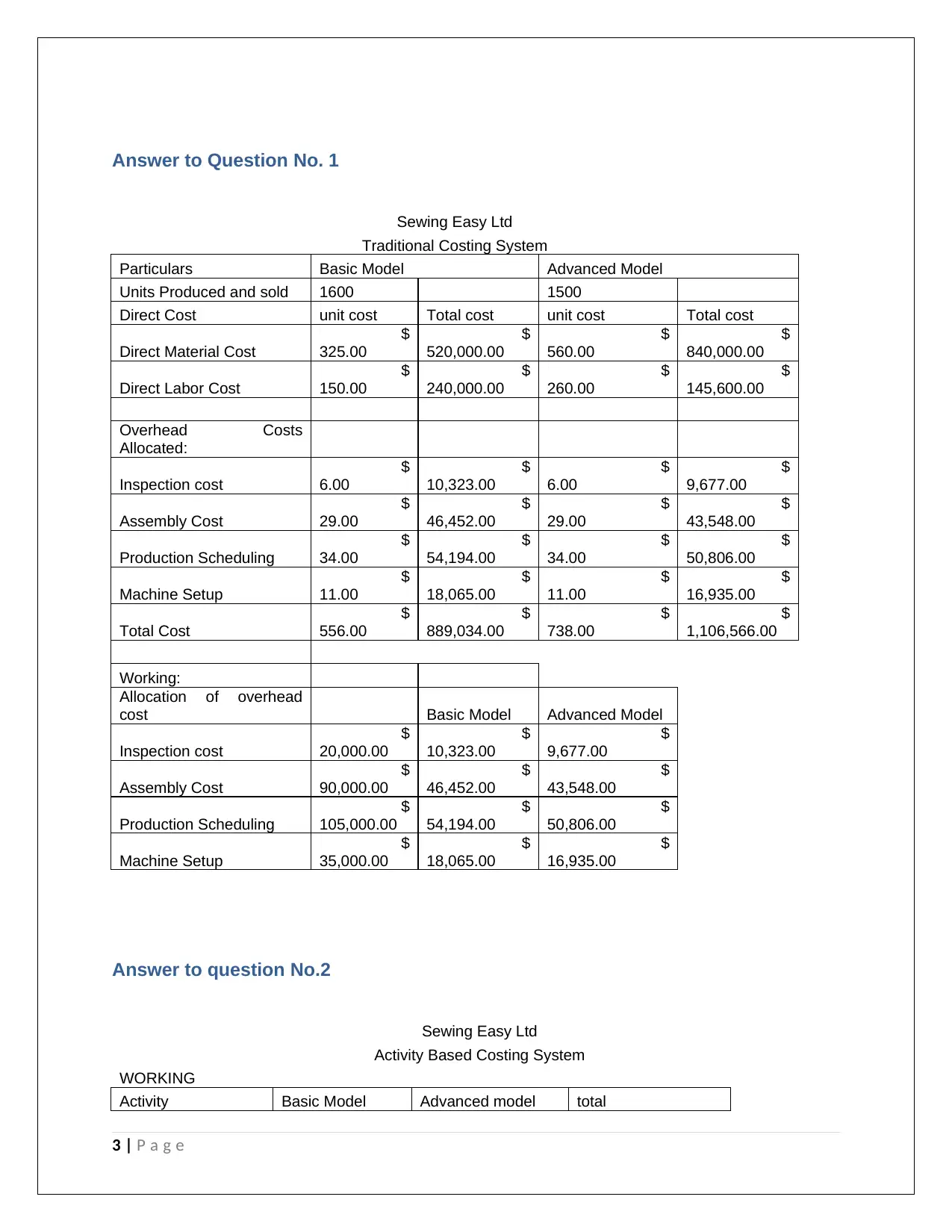

Answer to Question No. 1

Sewing Easy Ltd

Traditional Costing System

Particulars Basic Model Advanced Model

Units Produced and sold 1600 1500

Direct Cost unit cost Total cost unit cost Total cost

Direct Material Cost

$

325.00

$

520,000.00

$

560.00

$

840,000.00

Direct Labor Cost

$

150.00

$

240,000.00

$

260.00

$

145,600.00

Overhead Costs

Allocated:

Inspection cost

$

6.00

$

10,323.00

$

6.00

$

9,677.00

Assembly Cost

$

29.00

$

46,452.00

$

29.00

$

43,548.00

Production Scheduling

$

34.00

$

54,194.00

$

34.00

$

50,806.00

Machine Setup

$

11.00

$

18,065.00

$

11.00

$

16,935.00

Total Cost

$

556.00

$

889,034.00

$

738.00

$

1,106,566.00

Working:

Allocation of overhead

cost Basic Model Advanced Model

Inspection cost

$

20,000.00

$

10,323.00

$

9,677.00

Assembly Cost

$

90,000.00

$

46,452.00

$

43,548.00

Production Scheduling

$

105,000.00

$

54,194.00

$

50,806.00

Machine Setup

$

35,000.00

$

18,065.00

$

16,935.00

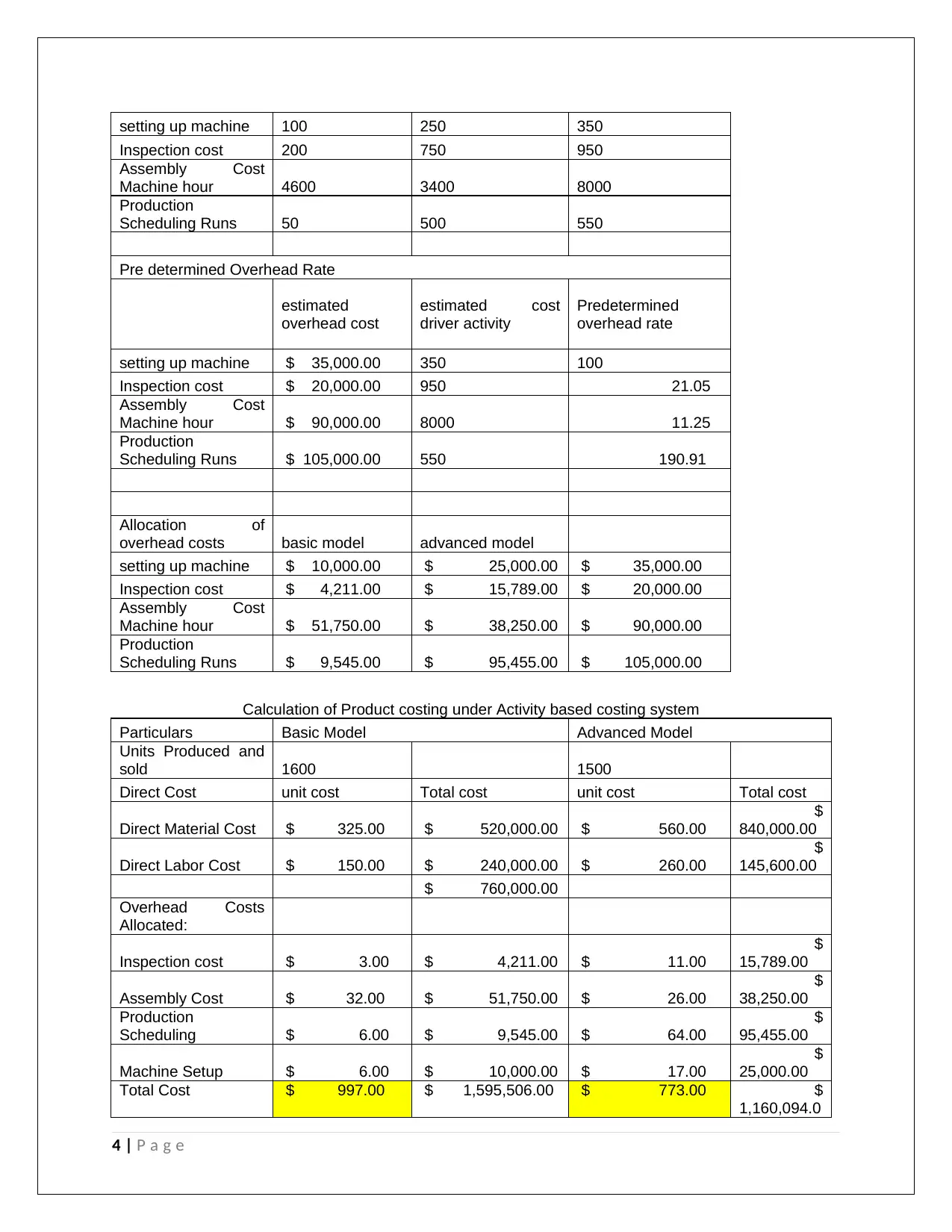

Answer to question No.2

Sewing Easy Ltd

Activity Based Costing System

WORKING

Activity Basic Model Advanced model total

3 | P a g e

Sewing Easy Ltd

Traditional Costing System

Particulars Basic Model Advanced Model

Units Produced and sold 1600 1500

Direct Cost unit cost Total cost unit cost Total cost

Direct Material Cost

$

325.00

$

520,000.00

$

560.00

$

840,000.00

Direct Labor Cost

$

150.00

$

240,000.00

$

260.00

$

145,600.00

Overhead Costs

Allocated:

Inspection cost

$

6.00

$

10,323.00

$

6.00

$

9,677.00

Assembly Cost

$

29.00

$

46,452.00

$

29.00

$

43,548.00

Production Scheduling

$

34.00

$

54,194.00

$

34.00

$

50,806.00

Machine Setup

$

11.00

$

18,065.00

$

11.00

$

16,935.00

Total Cost

$

556.00

$

889,034.00

$

738.00

$

1,106,566.00

Working:

Allocation of overhead

cost Basic Model Advanced Model

Inspection cost

$

20,000.00

$

10,323.00

$

9,677.00

Assembly Cost

$

90,000.00

$

46,452.00

$

43,548.00

Production Scheduling

$

105,000.00

$

54,194.00

$

50,806.00

Machine Setup

$

35,000.00

$

18,065.00

$

16,935.00

Answer to question No.2

Sewing Easy Ltd

Activity Based Costing System

WORKING

Activity Basic Model Advanced model total

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

setting up machine 100 250 350

Inspection cost 200 750 950

Assembly Cost

Machine hour 4600 3400 8000

Production

Scheduling Runs 50 500 550

Pre determined Overhead Rate

estimated

overhead cost

estimated cost

driver activity

Predetermined

overhead rate

setting up machine $ 35,000.00 350 100

Inspection cost $ 20,000.00 950 21.05

Assembly Cost

Machine hour $ 90,000.00 8000 11.25

Production

Scheduling Runs $ 105,000.00 550 190.91

Allocation of

overhead costs basic model advanced model

setting up machine $ 10,000.00 $ 25,000.00 $ 35,000.00

Inspection cost $ 4,211.00 $ 15,789.00 $ 20,000.00

Assembly Cost

Machine hour $ 51,750.00 $ 38,250.00 $ 90,000.00

Production

Scheduling Runs $ 9,545.00 $ 95,455.00 $ 105,000.00

Calculation of Product costing under Activity based costing system

Particulars Basic Model Advanced Model

Units Produced and

sold 1600 1500

Direct Cost unit cost Total cost unit cost Total cost

Direct Material Cost $ 325.00 $ 520,000.00 $ 560.00

$

840,000.00

Direct Labor Cost $ 150.00 $ 240,000.00 $ 260.00

$

145,600.00

$ 760,000.00

Overhead Costs

Allocated:

Inspection cost $ 3.00 $ 4,211.00 $ 11.00

$

15,789.00

Assembly Cost $ 32.00 $ 51,750.00 $ 26.00

$

38,250.00

Production

Scheduling $ 6.00 $ 9,545.00 $ 64.00

$

95,455.00

Machine Setup $ 6.00 $ 10,000.00 $ 17.00

$

25,000.00

Total Cost $ 997.00 $ 1,595,506.00 $ 773.00 $

1,160,094.0

4 | P a g e

Inspection cost 200 750 950

Assembly Cost

Machine hour 4600 3400 8000

Production

Scheduling Runs 50 500 550

Pre determined Overhead Rate

estimated

overhead cost

estimated cost

driver activity

Predetermined

overhead rate

setting up machine $ 35,000.00 350 100

Inspection cost $ 20,000.00 950 21.05

Assembly Cost

Machine hour $ 90,000.00 8000 11.25

Production

Scheduling Runs $ 105,000.00 550 190.91

Allocation of

overhead costs basic model advanced model

setting up machine $ 10,000.00 $ 25,000.00 $ 35,000.00

Inspection cost $ 4,211.00 $ 15,789.00 $ 20,000.00

Assembly Cost

Machine hour $ 51,750.00 $ 38,250.00 $ 90,000.00

Production

Scheduling Runs $ 9,545.00 $ 95,455.00 $ 105,000.00

Calculation of Product costing under Activity based costing system

Particulars Basic Model Advanced Model

Units Produced and

sold 1600 1500

Direct Cost unit cost Total cost unit cost Total cost

Direct Material Cost $ 325.00 $ 520,000.00 $ 560.00

$

840,000.00

Direct Labor Cost $ 150.00 $ 240,000.00 $ 260.00

$

145,600.00

$ 760,000.00

Overhead Costs

Allocated:

Inspection cost $ 3.00 $ 4,211.00 $ 11.00

$

15,789.00

Assembly Cost $ 32.00 $ 51,750.00 $ 26.00

$

38,250.00

Production

Scheduling $ 6.00 $ 9,545.00 $ 64.00

$

95,455.00

Machine Setup $ 6.00 $ 10,000.00 $ 17.00

$

25,000.00

Total Cost $ 997.00 $ 1,595,506.00 $ 773.00 $

1,160,094.0

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0

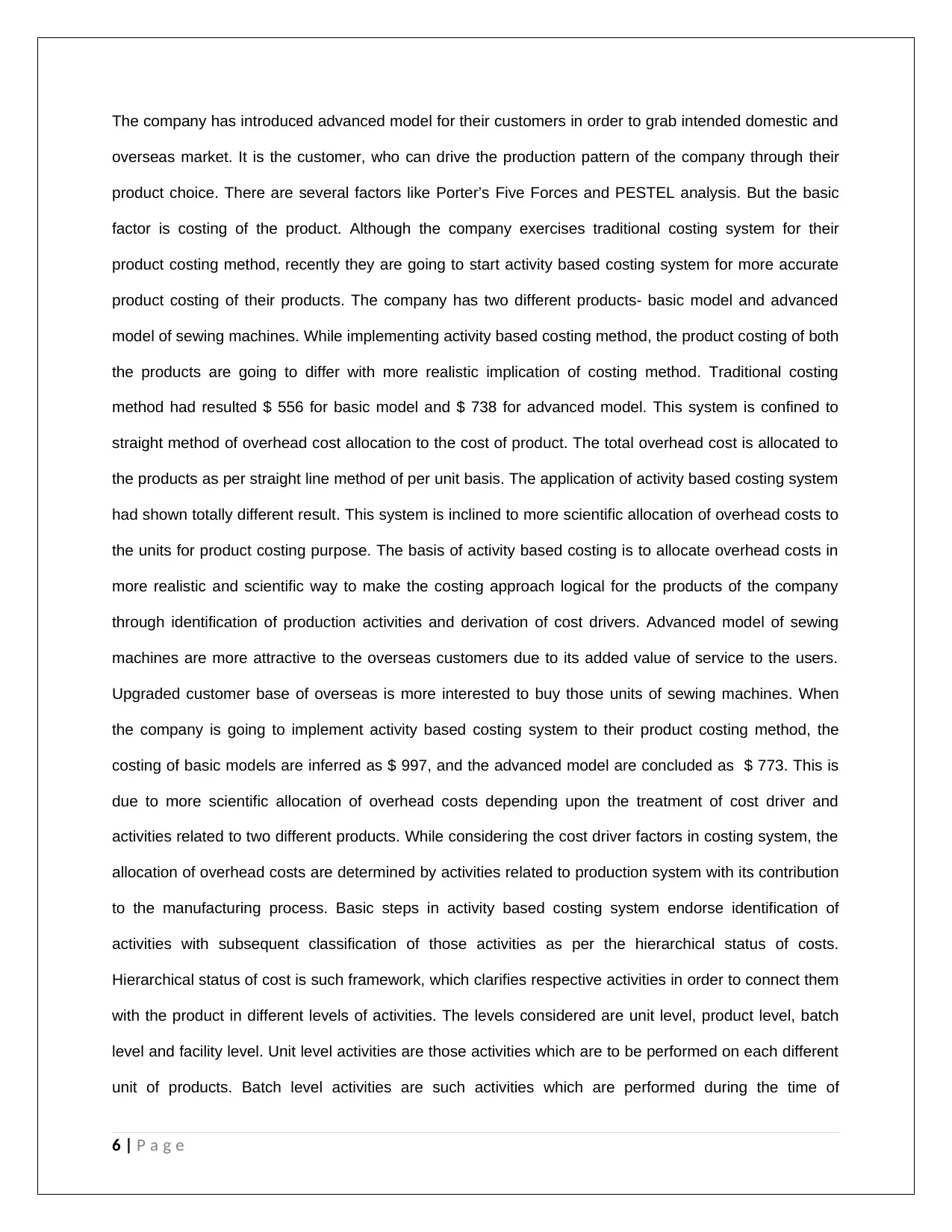

Answer to Question no. 3

Profit and Loss Account- sewing Easy Ltd

Advanced Model

Traditional Costing system Activity based Costing System

Particulars

product

cost Profit Amount Amount

product

cost Profit Amount' Amount'

Revenue

$

1,106,5

66.00

$

221,313.

20

$

1,327,87

9.20

$

1,160,0

94.00

$

232,01

8.80

$

1,392,11

2.80

Less cost of

goods sold

$

840,000.

00

$

840,000.

00

Less: Direct

Labor Cost

$

145,600.

00

$

145,600.

00

Less Production

overhead cost

$

120,966.

00

$

174,494.

00

$

1,106,56

6.00

$

1,160,09

4.00

Gross Profit

$

221,313.

20

$

232,018.

80

Less

Operational

Expenses:

Selling and

Administration

$

140,000.

00

$

140,000.

00

Interest

Expense

$

25,200.0

0

$

25,200.0

0

Office rent

$

35,900.0

0

$

35,900.0

0

Total Expenses

$

201,100.

00

$

201,100.

00

Net Profit

$

20,213.2

0

$

30,918.8

0

5 | P a g e

Answer to Question no. 3

Profit and Loss Account- sewing Easy Ltd

Advanced Model

Traditional Costing system Activity based Costing System

Particulars

product

cost Profit Amount Amount

product

cost Profit Amount' Amount'

Revenue

$

1,106,5

66.00

$

221,313.

20

$

1,327,87

9.20

$

1,160,0

94.00

$

232,01

8.80

$

1,392,11

2.80

Less cost of

goods sold

$

840,000.

00

$

840,000.

00

Less: Direct

Labor Cost

$

145,600.

00

$

145,600.

00

Less Production

overhead cost

$

120,966.

00

$

174,494.

00

$

1,106,56

6.00

$

1,160,09

4.00

Gross Profit

$

221,313.

20

$

232,018.

80

Less

Operational

Expenses:

Selling and

Administration

$

140,000.

00

$

140,000.

00

Interest

Expense

$

25,200.0

0

$

25,200.0

0

Office rent

$

35,900.0

0

$

35,900.0

0

Total Expenses

$

201,100.

00

$

201,100.

00

Net Profit

$

20,213.2

0

$

30,918.8

0

5 | P a g e

The company has introduced advanced model for their customers in order to grab intended domestic and

overseas market. It is the customer, who can drive the production pattern of the company through their

product choice. There are several factors like Porter’s Five Forces and PESTEL analysis. But the basic

factor is costing of the product. Although the company exercises traditional costing system for their

product costing method, recently they are going to start activity based costing system for more accurate

product costing of their products. The company has two different products- basic model and advanced

model of sewing machines. While implementing activity based costing method, the product costing of both

the products are going to differ with more realistic implication of costing method. Traditional costing

method had resulted $ 556 for basic model and $ 738 for advanced model. This system is confined to

straight method of overhead cost allocation to the cost of product. The total overhead cost is allocated to

the products as per straight line method of per unit basis. The application of activity based costing system

had shown totally different result. This system is inclined to more scientific allocation of overhead costs to

the units for product costing purpose. The basis of activity based costing is to allocate overhead costs in

more realistic and scientific way to make the costing approach logical for the products of the company

through identification of production activities and derivation of cost drivers. Advanced model of sewing

machines are more attractive to the overseas customers due to its added value of service to the users.

Upgraded customer base of overseas is more interested to buy those units of sewing machines. When

the company is going to implement activity based costing system to their product costing method, the

costing of basic models are inferred as $ 997, and the advanced model are concluded as $ 773. This is

due to more scientific allocation of overhead costs depending upon the treatment of cost driver and

activities related to two different products. While considering the cost driver factors in costing system, the

allocation of overhead costs are determined by activities related to production system with its contribution

to the manufacturing process. Basic steps in activity based costing system endorse identification of

activities with subsequent classification of those activities as per the hierarchical status of costs.

Hierarchical status of cost is such framework, which clarifies respective activities in order to connect them

with the product in different levels of activities. The levels considered are unit level, product level, batch

level and facility level. Unit level activities are those activities which are to be performed on each different

unit of products. Batch level activities are such activities which are performed during the time of

6 | P a g e

overseas market. It is the customer, who can drive the production pattern of the company through their

product choice. There are several factors like Porter’s Five Forces and PESTEL analysis. But the basic

factor is costing of the product. Although the company exercises traditional costing system for their

product costing method, recently they are going to start activity based costing system for more accurate

product costing of their products. The company has two different products- basic model and advanced

model of sewing machines. While implementing activity based costing method, the product costing of both

the products are going to differ with more realistic implication of costing method. Traditional costing

method had resulted $ 556 for basic model and $ 738 for advanced model. This system is confined to

straight method of overhead cost allocation to the cost of product. The total overhead cost is allocated to

the products as per straight line method of per unit basis. The application of activity based costing system

had shown totally different result. This system is inclined to more scientific allocation of overhead costs to

the units for product costing purpose. The basis of activity based costing is to allocate overhead costs in

more realistic and scientific way to make the costing approach logical for the products of the company

through identification of production activities and derivation of cost drivers. Advanced model of sewing

machines are more attractive to the overseas customers due to its added value of service to the users.

Upgraded customer base of overseas is more interested to buy those units of sewing machines. When

the company is going to implement activity based costing system to their product costing method, the

costing of basic models are inferred as $ 997, and the advanced model are concluded as $ 773. This is

due to more scientific allocation of overhead costs depending upon the treatment of cost driver and

activities related to two different products. While considering the cost driver factors in costing system, the

allocation of overhead costs are determined by activities related to production system with its contribution

to the manufacturing process. Basic steps in activity based costing system endorse identification of

activities with subsequent classification of those activities as per the hierarchical status of costs.

Hierarchical status of cost is such framework, which clarifies respective activities in order to connect them

with the product in different levels of activities. The levels considered are unit level, product level, batch

level and facility level. Unit level activities are those activities which are to be performed on each different

unit of products. Batch level activities are such activities which are performed during the time of

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

production of a single batch. Product level activities are those activities, which are identified to be carried

out on separate note for each output. The types of facility level activities are those activities, which are

taken care of at the plant level. The most easily identifiable activities are unit level activities while facility

level activates are really tough to be traced. (Schmitz, 2012)

With the above discussion, it is easily identifiable that Sewing easy Ltd is more concentrated on product

level activities. The implementation of activity based costing system is easily allocated to this production

method and the identification of cost driver is easy to be identified for overhead cost allocation. For this

purpose, the advanced model product with activity based costing proves to be economic with the required

level of service from those sewing machines, as asked for by the overseas customers. (Explained, 2017)

Answer to Question No. 4

Overhead normally relates to indirect nature of manufacturing costs in accounting. There are other

expenses or costs take part in manufacturing process other than direct material and direct labor costs.

Actual overhead is referred as those indirect manufacturing costs which normally occurs and recorded in

the books of accounts. These segments of actual overhead costs include different provisions like water,

gas, electricity, production supervisors, property tax, repair and maintenance, depreciation and several

other head of costs.

Applied costs are those indirect manufacturing costs, which are assigned to the products manufactured.

In this context, application, assignment and allocation of manufacturing overheads are exercised by

assessment of predetermined periodical overhead rate. Example for this concept is an estimation of $

3,000,000 as manufacturing costs with the total machine hour as 60,000. The resultant predetermined

annual overhead rate is arrived at $50 per machine hour.

When historical costing system is followed on the basis of actual costs, the derivation of recovery rate is

instrumental to match actual and applied overhead through the system of predetermined recovery rate.

This situation prevents occurrence of over or under applied costs. (Focus, 2017)

7 | P a g e

out on separate note for each output. The types of facility level activities are those activities, which are

taken care of at the plant level. The most easily identifiable activities are unit level activities while facility

level activates are really tough to be traced. (Schmitz, 2012)

With the above discussion, it is easily identifiable that Sewing easy Ltd is more concentrated on product

level activities. The implementation of activity based costing system is easily allocated to this production

method and the identification of cost driver is easy to be identified for overhead cost allocation. For this

purpose, the advanced model product with activity based costing proves to be economic with the required

level of service from those sewing machines, as asked for by the overseas customers. (Explained, 2017)

Answer to Question No. 4

Overhead normally relates to indirect nature of manufacturing costs in accounting. There are other

expenses or costs take part in manufacturing process other than direct material and direct labor costs.

Actual overhead is referred as those indirect manufacturing costs which normally occurs and recorded in

the books of accounts. These segments of actual overhead costs include different provisions like water,

gas, electricity, production supervisors, property tax, repair and maintenance, depreciation and several

other head of costs.

Applied costs are those indirect manufacturing costs, which are assigned to the products manufactured.

In this context, application, assignment and allocation of manufacturing overheads are exercised by

assessment of predetermined periodical overhead rate. Example for this concept is an estimation of $

3,000,000 as manufacturing costs with the total machine hour as 60,000. The resultant predetermined

annual overhead rate is arrived at $50 per machine hour.

When historical costing system is followed on the basis of actual costs, the derivation of recovery rate is

instrumental to match actual and applied overhead through the system of predetermined recovery rate.

This situation prevents occurrence of over or under applied costs. (Focus, 2017)

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The situation of over or under applied costs arises for these two instances:

a) The cost of actual overhead exceeds or is lesser than the estimated overhead;

b) The base of actual absorption amount under different heads differs from the basis of estimated

absorption.

This situation of over or under absorbed overheads can be managed in three ways:

1) The amount may be carried forward to next financial period accounting;

2) The amount may be written off through exercise of costing profit and loss account;

3) A supplementary rate of absorption may be worked out with subsequent application to the

manufacturing process. (Net, 2014)

These above three steps can be useful to manage over or under absorbed overheads for any

organization with logical foundation.

Answer to Question No. 5

Activity based costing is defined as an approach to the aspect of costing through monitoring of different

manufacturing activities. This system is involved in tracing of resource consumption followed by making

costing analysis of final product. In this process, resources are allocated to different manufacturing

activities followed by activities to the objects of cost. Main deriving agent for this practice is determination

of cost drivers related to activities and attach those activity costs to the products. (CGMA, 2013)

Activity based Costing was first introduced by Kaplan and Bruns in 1980. It is reckoned as the latest

alternative concept of absorption costing, which allows the managers for better understanding of product

costing and net profitability of customers. This system can make the business more equipped with better

level of information flow to ensure value added proposition to enble for more effective level of decisions.

Basic difference between Activity based costing system and traditional costing system is that ABC is

8 | P a g e

a) The cost of actual overhead exceeds or is lesser than the estimated overhead;

b) The base of actual absorption amount under different heads differs from the basis of estimated

absorption.

This situation of over or under absorbed overheads can be managed in three ways:

1) The amount may be carried forward to next financial period accounting;

2) The amount may be written off through exercise of costing profit and loss account;

3) A supplementary rate of absorption may be worked out with subsequent application to the

manufacturing process. (Net, 2014)

These above three steps can be useful to manage over or under absorbed overheads for any

organization with logical foundation.

Answer to Question No. 5

Activity based costing is defined as an approach to the aspect of costing through monitoring of different

manufacturing activities. This system is involved in tracing of resource consumption followed by making

costing analysis of final product. In this process, resources are allocated to different manufacturing

activities followed by activities to the objects of cost. Main deriving agent for this practice is determination

of cost drivers related to activities and attach those activity costs to the products. (CGMA, 2013)

Activity based Costing was first introduced by Kaplan and Bruns in 1980. It is reckoned as the latest

alternative concept of absorption costing, which allows the managers for better understanding of product

costing and net profitability of customers. This system can make the business more equipped with better

level of information flow to ensure value added proposition to enble for more effective level of decisions.

Basic difference between Activity based costing system and traditional costing system is that ABC is

8 | P a g e

based on identification of driver based activities while traditional costing system is depending upon flat

system of cost allocation to the output. (efinancemanagement, 2017)

Activity based Costing is a method of 2 steps of costing. Through this method, allocations of costs are first

made to the activities identified for any business followed by the assignment of products or services

through those activities. Alternatively, the ABC system endorses the concept of costing of products or

services on the specific activities required to produce or render products or services.

There are certain advantages and limitations of this ABC system. They are defined below:

Advantages:

More perfect system of costing with accuracy related to allied products or services, to suffice the

value justification to stakeholders in the forms of customers, supply chain associates and referred

SKUs.

For better understanding of respective overheads

Easy for everyone to understand the concept

Scientific approach to consider unit cost instead of total cost

Prone to integration with latest management tools like six sigma and other development programs

Ability to visualize waste and other activities which are not able to add value

Support management of performance derivation with different parameter like Balance Score card

Confirms ability of costing to processes, value chain and supply chain ingredients

This system of costing enables projecting the path of work done

Confirms facilitation of benchmarking

Limitations of Activity based Costing System

Although the concept of Activity based Costing system proves to be helpful and conclusive for the

managers to ensure management of overhead to make clear concept of understanding profitability of

products and respective stakeholders, and proves to be stronger tools for managerial decision making;

this system has certain limitations too, which are given below:

9 | P a g e

system of cost allocation to the output. (efinancemanagement, 2017)

Activity based Costing is a method of 2 steps of costing. Through this method, allocations of costs are first

made to the activities identified for any business followed by the assignment of products or services

through those activities. Alternatively, the ABC system endorses the concept of costing of products or

services on the specific activities required to produce or render products or services.

There are certain advantages and limitations of this ABC system. They are defined below:

Advantages:

More perfect system of costing with accuracy related to allied products or services, to suffice the

value justification to stakeholders in the forms of customers, supply chain associates and referred

SKUs.

For better understanding of respective overheads

Easy for everyone to understand the concept

Scientific approach to consider unit cost instead of total cost

Prone to integration with latest management tools like six sigma and other development programs

Ability to visualize waste and other activities which are not able to add value

Support management of performance derivation with different parameter like Balance Score card

Confirms ability of costing to processes, value chain and supply chain ingredients

This system of costing enables projecting the path of work done

Confirms facilitation of benchmarking

Limitations of Activity based Costing System

Although the concept of Activity based Costing system proves to be helpful and conclusive for the

managers to ensure management of overhead to make clear concept of understanding profitability of

products and respective stakeholders, and proves to be stronger tools for managerial decision making;

this system has certain limitations too, which are given below:

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Limitations:

Transformation of costing system from traditional to activity based costing system is a major

project. This transformation need to be implemented through introduction of massive IT enabled

infrastructure. Properly qualified IT professionals are required for this purpose, who are able to

handle big data and mange them as per the requirement of the organization. This process

involves big amount of financial impact for the organization, too.

Activity based costing system generates numerical figures like product margins. These figures

are produced in odd numerology as compared to the output of traditional costing system. As the

managers are more conversant with traditional system to perform their management duties, and

that is the parameter of their performance evaluation, ABC system is not the ideal option for this

performance evaluation in initial stage.

Understanding activity based costing output in the form of data is not easy for new users and it is

often tending towards misinterpretation. Hence referred output data must be handled with proper

knowledge base and true care to arrive at the decisive managerial decision making. Assignment

of costs to products or services along with its impact on customers and other objects of cost are

mainly relevant with potential ability. It is the preamble of using activity based costing data for the

managers to identify those costs which proves relevance for the decision to be made.

The reports generated from the Activity based costing system do not ascertain the concept of

Generally Accepted Accounting Principle or GAAP. Subsequently, the organization with Activity

based costing system should follow two types of costing system- first to use internally and second

to prepare external reports. (Explanation, 2017)

10 | P a g e

Transformation of costing system from traditional to activity based costing system is a major

project. This transformation need to be implemented through introduction of massive IT enabled

infrastructure. Properly qualified IT professionals are required for this purpose, who are able to

handle big data and mange them as per the requirement of the organization. This process

involves big amount of financial impact for the organization, too.

Activity based costing system generates numerical figures like product margins. These figures

are produced in odd numerology as compared to the output of traditional costing system. As the

managers are more conversant with traditional system to perform their management duties, and

that is the parameter of their performance evaluation, ABC system is not the ideal option for this

performance evaluation in initial stage.

Understanding activity based costing output in the form of data is not easy for new users and it is

often tending towards misinterpretation. Hence referred output data must be handled with proper

knowledge base and true care to arrive at the decisive managerial decision making. Assignment

of costs to products or services along with its impact on customers and other objects of cost are

mainly relevant with potential ability. It is the preamble of using activity based costing data for the

managers to identify those costs which proves relevance for the decision to be made.

The reports generated from the Activity based costing system do not ascertain the concept of

Generally Accepted Accounting Principle or GAAP. Subsequently, the organization with Activity

based costing system should follow two types of costing system- first to use internally and second

to prepare external reports. (Explanation, 2017)

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References:

CGMA, 2013. Activity Based Costing(ABC). [Online] Available at:

https://www.cgma.org/resources/tools/essential-tools/activity-based-costing.html [Accessed 22 May

2018].

efinancemanagement, 2017. Activity Based Costing. [Online] Available at:

https://efinancemanagement.com/costing-terms/activity-based-costing [Accessed 22 May 2018].

Explained, A., 2017. Activity Bassed Costing. [Online] Available at:

https://accountingexplained.com/managerial/cost-systems/activity-based-costing [Accessed 22 May

2018].

Explanation, A., 2017. Advantages, Disadvantages and Limitations of Activity Based Costing (ABC)

System. [Online] Available at:

http://www.accountingexplanation.com/advantages_disadvantages_and_limitations_of_activity_based_co

sting.htm [Accessed 22 May 2018].

Focus, A.i., 2017. Appled Overhead versus Actual overhead. [Online] Available at:

http://accountinginfocus.com/managerial-accounting-2/overhead-allocation/applied-overhead-versus-

actual-overhead/ [Accessed 22 May 2018].

Net, T.o., 2014. Treatment Of Over Or Under Absortion Of Overhead. [Online] Available at:

http://www.tutorsonnet.com/over-or-under-absorption-of-overhead-homework-help.php [Accessed 22 May

2018].

Schmitz, A., 2012. Accounting for Managers.

11 | P a g e

CGMA, 2013. Activity Based Costing(ABC). [Online] Available at:

https://www.cgma.org/resources/tools/essential-tools/activity-based-costing.html [Accessed 22 May

2018].

efinancemanagement, 2017. Activity Based Costing. [Online] Available at:

https://efinancemanagement.com/costing-terms/activity-based-costing [Accessed 22 May 2018].

Explained, A., 2017. Activity Bassed Costing. [Online] Available at:

https://accountingexplained.com/managerial/cost-systems/activity-based-costing [Accessed 22 May

2018].

Explanation, A., 2017. Advantages, Disadvantages and Limitations of Activity Based Costing (ABC)

System. [Online] Available at:

http://www.accountingexplanation.com/advantages_disadvantages_and_limitations_of_activity_based_co

sting.htm [Accessed 22 May 2018].

Focus, A.i., 2017. Appled Overhead versus Actual overhead. [Online] Available at:

http://accountinginfocus.com/managerial-accounting-2/overhead-allocation/applied-overhead-versus-

actual-overhead/ [Accessed 22 May 2018].

Net, T.o., 2014. Treatment Of Over Or Under Absortion Of Overhead. [Online] Available at:

http://www.tutorsonnet.com/over-or-under-absorption-of-overhead-homework-help.php [Accessed 22 May

2018].

Schmitz, A., 2012. Accounting for Managers.

11 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.