Costing, Variance Analysis, Budgeting and Sensitivity Analysis

VerifiedAdded on 2022/12/28

|10

|2301

|32

Homework Assignment

AI Summary

This assignment solution addresses key concepts in costing and budgeting, providing detailed calculations and analyses. Question 1 explores overhead absorption and activity-based costing, comparing their impacts on product profitability, including calculations for overhead absorption rates, cost per unit, and profit margins. Question 2 delves into variance analysis, calculating material usage, mix, and yield variances, and discussing issues with current variance reporting systems. Finally, Question 3 examines zero-based budgeting (ZBB) and incremental budgeting (IB), comparing their roles in planning and coordination, and discussing the strengths and weaknesses of each approach, offering a comprehensive overview of financial planning and control techniques.

Online Exam

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................6

Question 3...................................................................................................................................................8

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................6

Question 3...................................................................................................................................................8

Question 1

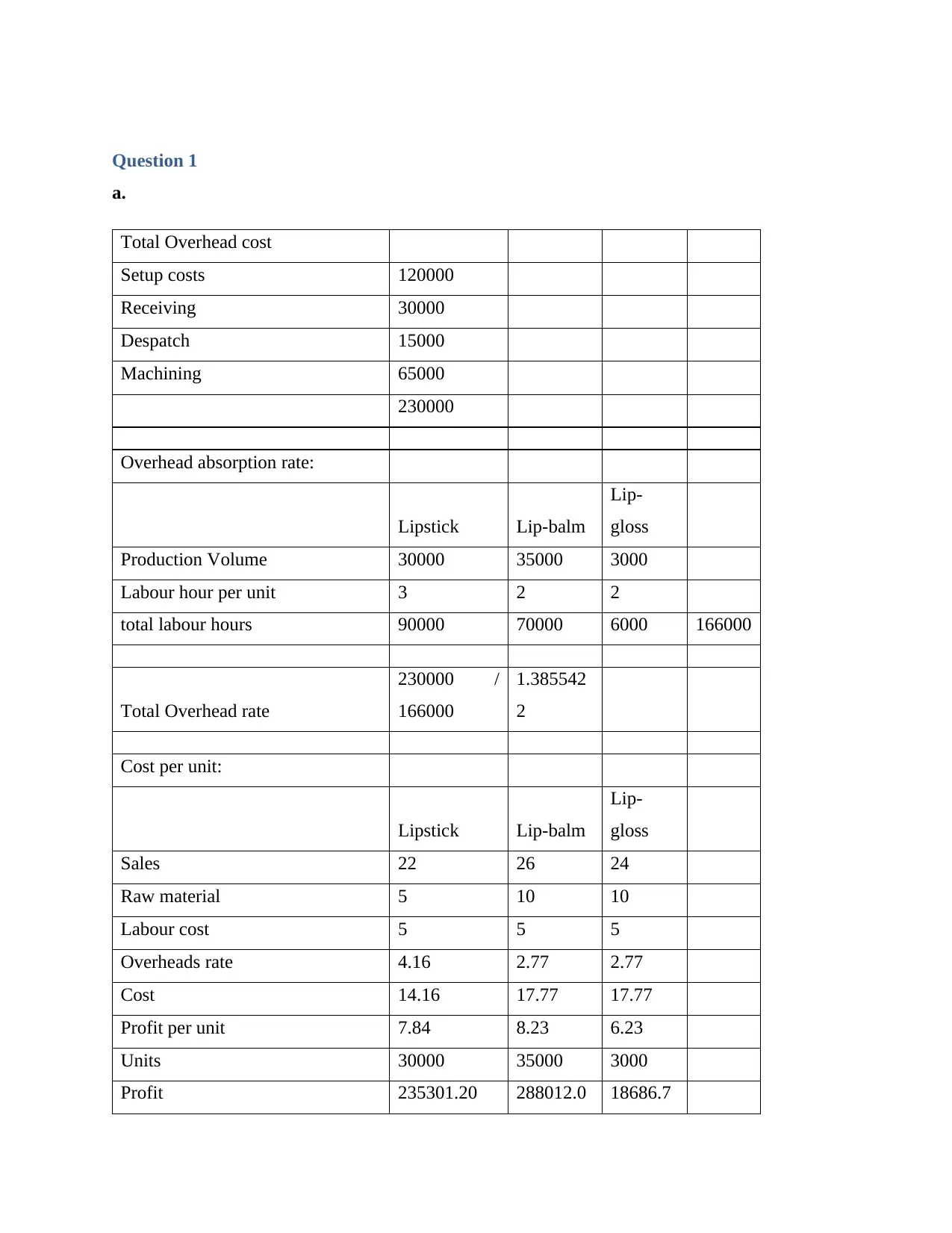

a.

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

230000

Overhead absorption rate:

Lipstick Lip-balm

Lip-

gloss

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000 166000

Total Overhead rate

230000 /

166000

1.385542

2

Cost per unit:

Lipstick Lip-balm

Lip-

gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

Units 30000 35000 3000

Profit 235301.20 288012.0 18686.7

a.

Total Overhead cost

Setup costs 120000

Receiving 30000

Despatch 15000

Machining 65000

230000

Overhead absorption rate:

Lipstick Lip-balm

Lip-

gloss

Production Volume 30000 35000 3000

Labour hour per unit 3 2 2

total labour hours 90000 70000 6000 166000

Total Overhead rate

230000 /

166000

1.385542

2

Cost per unit:

Lipstick Lip-balm

Lip-

gloss

Sales 22 26 24

Raw material 5 10 10

Labour cost 5 5 5

Overheads rate 4.16 2.77 2.77

Cost 14.16 17.77 17.77

Profit per unit 7.84 8.23 6.23

Units 30000 35000 3000

Profit 235301.20 288012.0 18686.7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 5

b.

Cost

Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12

machinin

g

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20 20 10

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22

1363.636

4

Cost per despatch

15000 /

50 300

Cost per machining activity

65000 /

12

5416.666

7

Allocation of overheads to each

product

Lipstick Lip-balm Lip-gloss

Setup costs 48000 67200 4800

12000

0

b.

Cost

Driver

Setup costs 120000 25 setups

Receiving 30000 22 deliveries

Despatch 15000 50 despatched

Machining 65000 12

machinin

g

Cost driver data:

Machine hours per unit 4 4 4

Number of setups 10 14 1

Number of deliveries received 10 10 2

Number of orders despatched 20 20 10

Cost per setup

120000/2

5 4800

Cost per receiving activity

30000 /

22

1363.636

4

Cost per despatch

15000 /

50 300

Cost per machining activity

65000 /

12

5416.666

7

Allocation of overheads to each

product

Lipstick Lip-balm Lip-gloss

Setup costs 48000 67200 4800

12000

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

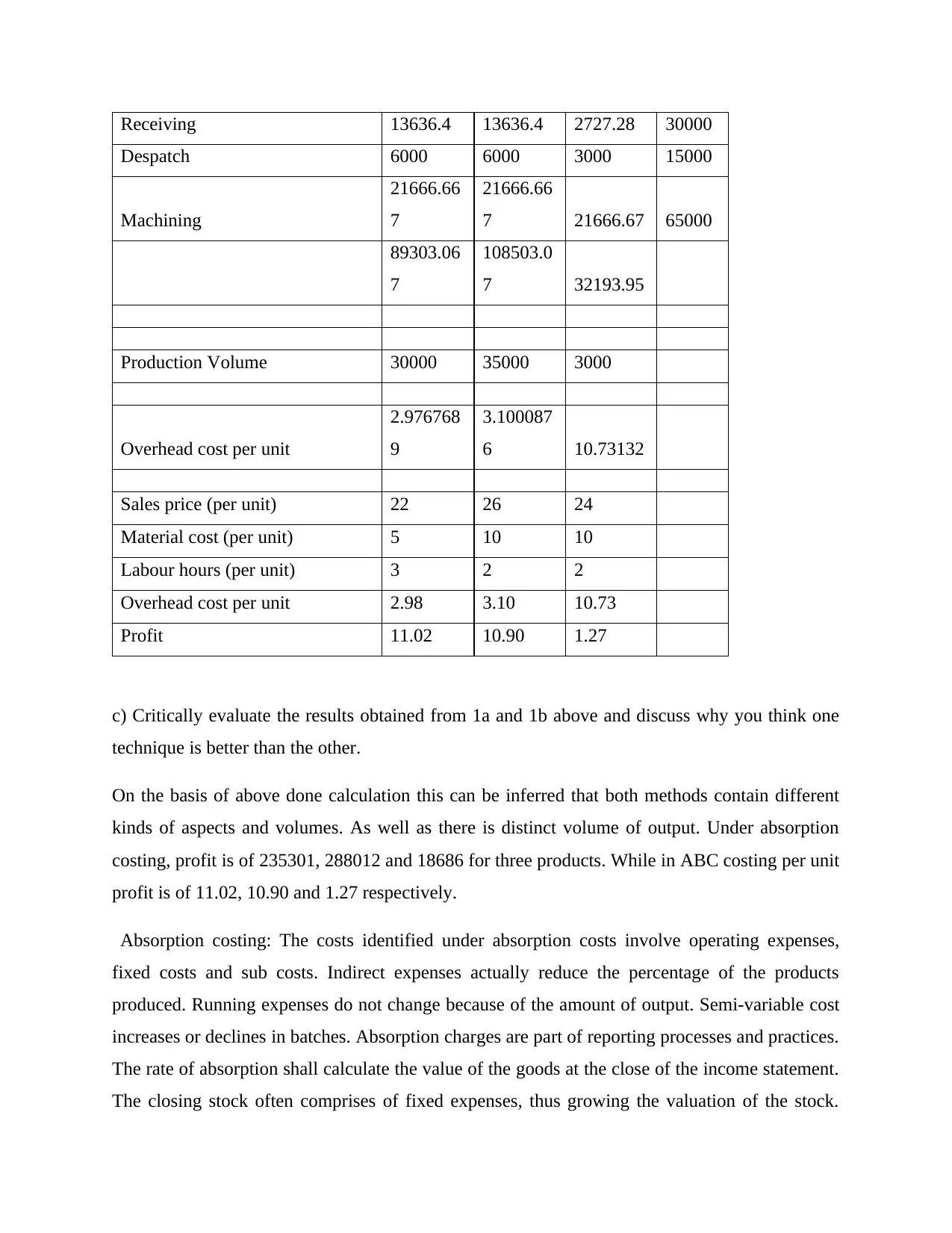

Receiving 13636.4 13636.4 2727.28 30000

Despatch 6000 6000 3000 15000

Machining

21666.66

7

21666.66

7 21666.67 65000

89303.06

7

108503.0

7 32193.95

Production Volume 30000 35000 3000

Overhead cost per unit

2.976768

9

3.100087

6 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Profit 11.02 10.90 1.27

c) Critically evaluate the results obtained from 1a and 1b above and discuss why you think one

technique is better than the other.

On the basis of above done calculation this can be inferred that both methods contain different

kinds of aspects and volumes. As well as there is distinct volume of output. Under absorption

costing, profit is of 235301, 288012 and 18686 for three products. While in ABC costing per unit

profit is of 11.02, 10.90 and 1.27 respectively.

Absorption costing: The costs identified under absorption costs involve operating expenses,

fixed costs and sub costs. Indirect expenses actually reduce the percentage of the products

produced. Running expenses do not change because of the amount of output. Semi-variable cost

increases or declines in batches. Absorption charges are part of reporting processes and practices.

The rate of absorption shall calculate the value of the goods at the close of the income statement.

The closing stock often comprises of fixed expenses, thus growing the valuation of the stock.

Despatch 6000 6000 3000 15000

Machining

21666.66

7

21666.66

7 21666.67 65000

89303.06

7

108503.0

7 32193.95

Production Volume 30000 35000 3000

Overhead cost per unit

2.976768

9

3.100087

6 10.73132

Sales price (per unit) 22 26 24

Material cost (per unit) 5 10 10

Labour hours (per unit) 3 2 2

Overhead cost per unit 2.98 3.10 10.73

Profit 11.02 10.90 1.27

c) Critically evaluate the results obtained from 1a and 1b above and discuss why you think one

technique is better than the other.

On the basis of above done calculation this can be inferred that both methods contain different

kinds of aspects and volumes. As well as there is distinct volume of output. Under absorption

costing, profit is of 235301, 288012 and 18686 for three products. While in ABC costing per unit

profit is of 11.02, 10.90 and 1.27 respectively.

Absorption costing: The costs identified under absorption costs involve operating expenses,

fixed costs and sub costs. Indirect expenses actually reduce the percentage of the products

produced. Running expenses do not change because of the amount of output. Semi-variable cost

increases or declines in batches. Absorption charges are part of reporting processes and practices.

The rate of absorption shall calculate the value of the goods at the close of the income statement.

The closing stock often comprises of fixed expenses, thus growing the valuation of the stock.

This form of inventory assessment increases the company's earnings. The system of absorption

costing is set down in the Commonly Agreed Accounting Principles (GAAP) for the recording of

reports under various laws. In this process, the fixed cost refers to the cost of output declines

with economic rates. This is opposed to variable pricing, where incremental production carries

the same constant production costs. In comparison, the variable costing approach does not offer a

correct image of financial gains and losses.

Activity based costing- Activity-based costing (ABC) applies overhead processing costs to goods

in a more rational way than the conventional method of merely allocating costing is the process

of system hours. First, activity-based cost attributes costs to operations that are the true source of

expenses. It then allocates the expense of those operations only to the goods that are currently

requesting the activities. Activity-based costing acknowledges that special technology, special

testing, system setups, and the others are costs-inducing the organization to use money. Under

ABC, the organization will measure the cost of the equipment used by both of these operations.

Next, the cost of any of these operations will be allocated only to the items that are needed to

carry out the activities.

d) Discuss how sensitivity analysis helps managers to cope with uncertainties.

Sensitivity analysis obtains as to how various values of an unregulated variable can have an

effect on such restricted response variable under the specified set of factors. Simply stated, the

sensitivity study would analyze how many causes of heterogeneity in graphical model relate to

the overall ambiguity of interpretation. This approach is used within such parameters that rely on

one or even more outputs that may differ. Sensitivity measurement is used both in the corporate

world and in sociology. It is commonly used by analysts and financial experts. Sensitivity study

is typically referred to as an analysis of what-if. Sensitivity analysis may be considered as a

funding plan or interpretation that specifies how the target factors are influenced by differences

in other associated variables. This are called input variables. This approach is one of the

approaches to forecast the outcome of a decision when given a number of complex variables.

When a decision is taken using a number of factors, economists and financial analysts can be

able to predict how adjustments to a particular variable will influence the final result. Sensitivity

analysis is an analytical technique that helps to assess how differing views of a variable can

influence a certain dependent variable. It can be useful in a variety of subjects other than

costing is set down in the Commonly Agreed Accounting Principles (GAAP) for the recording of

reports under various laws. In this process, the fixed cost refers to the cost of output declines

with economic rates. This is opposed to variable pricing, where incremental production carries

the same constant production costs. In comparison, the variable costing approach does not offer a

correct image of financial gains and losses.

Activity based costing- Activity-based costing (ABC) applies overhead processing costs to goods

in a more rational way than the conventional method of merely allocating costing is the process

of system hours. First, activity-based cost attributes costs to operations that are the true source of

expenses. It then allocates the expense of those operations only to the goods that are currently

requesting the activities. Activity-based costing acknowledges that special technology, special

testing, system setups, and the others are costs-inducing the organization to use money. Under

ABC, the organization will measure the cost of the equipment used by both of these operations.

Next, the cost of any of these operations will be allocated only to the items that are needed to

carry out the activities.

d) Discuss how sensitivity analysis helps managers to cope with uncertainties.

Sensitivity analysis obtains as to how various values of an unregulated variable can have an

effect on such restricted response variable under the specified set of factors. Simply stated, the

sensitivity study would analyze how many causes of heterogeneity in graphical model relate to

the overall ambiguity of interpretation. This approach is used within such parameters that rely on

one or even more outputs that may differ. Sensitivity measurement is used both in the corporate

world and in sociology. It is commonly used by analysts and financial experts. Sensitivity study

is typically referred to as an analysis of what-if. Sensitivity analysis may be considered as a

funding plan or interpretation that specifies how the target factors are influenced by differences

in other associated variables. This are called input variables. This approach is one of the

approaches to forecast the outcome of a decision when given a number of complex variables.

When a decision is taken using a number of factors, economists and financial analysts can be

able to predict how adjustments to a particular variable will influence the final result. Sensitivity

analysis is an analytical technique that helps to assess how differing views of a variable can

influence a certain dependent variable. It can be useful in a variety of subjects other than

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

economics, such as chemistry, history, genetics, etc. Sensitivity analysis helps the management

to realize which factors have a high effect on the performance or loss of the venture. For

instance, in the Sensitivity Study of Company A, the leadership learned that the advertising of

their product had a sales effect of up to 20%. Management should also rely on offering the

highest product packaging in order to maximize sales. Sensitivity analysis results in the

prediction assisted data. When all the factors are weighed and all the findings are analysed, it is

easier for management to make decisions regarding invested capital and decisions regarding

investments in the markets. It is also an incredibly valuable method for future planning.

Question 2

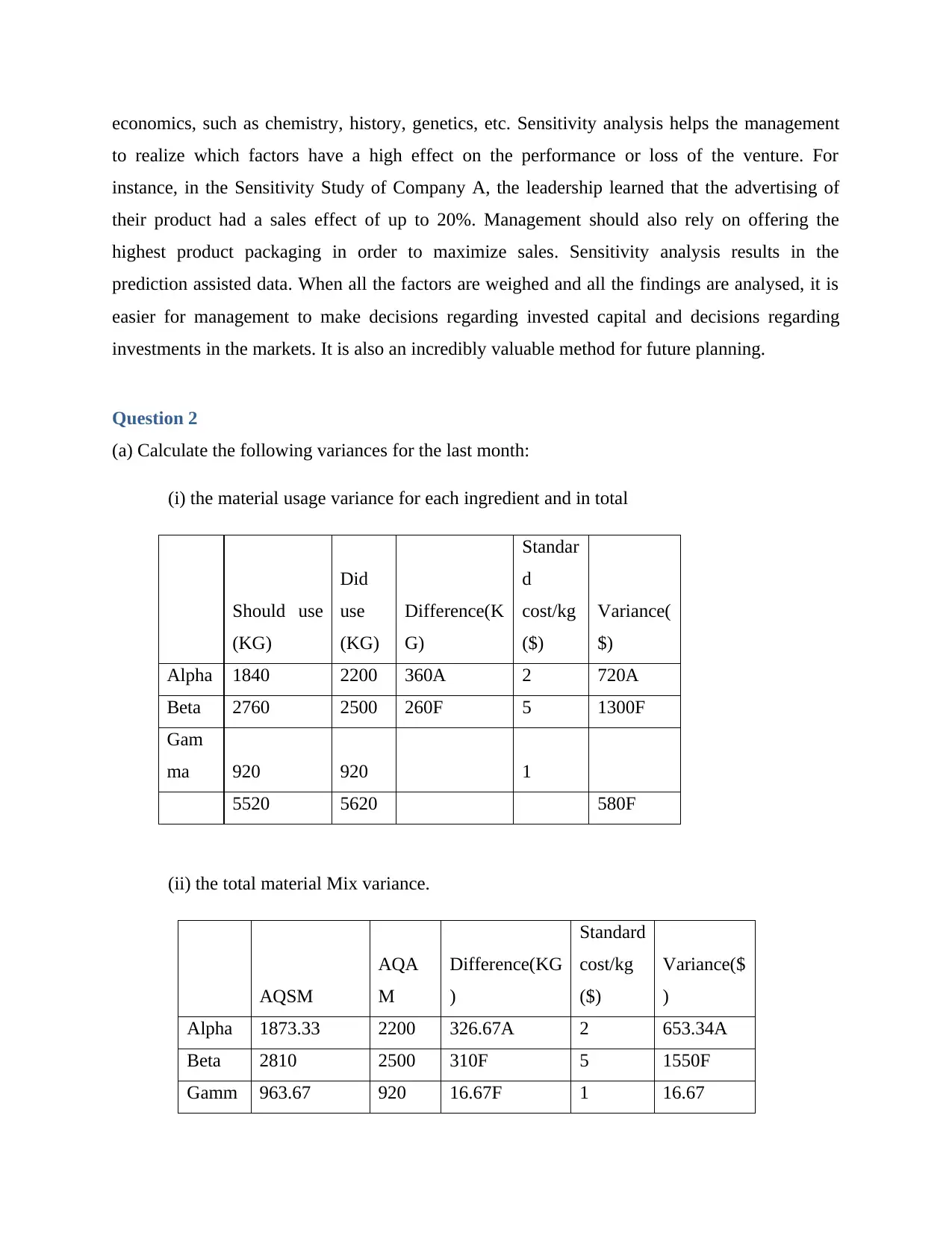

(a) Calculate the following variances for the last month:

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did

use

(KG)

Difference(K

G)

Standar

d

cost/kg

($)

Variance(

$)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gam

ma 920 920 1

5520 5620 580F

(ii) the total material Mix variance.

AQSM

AQA

M

Difference(KG

)

Standard

cost/kg

($)

Variance($

)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamm 963.67 920 16.67F 1 16.67

to realize which factors have a high effect on the performance or loss of the venture. For

instance, in the Sensitivity Study of Company A, the leadership learned that the advertising of

their product had a sales effect of up to 20%. Management should also rely on offering the

highest product packaging in order to maximize sales. Sensitivity analysis results in the

prediction assisted data. When all the factors are weighed and all the findings are analysed, it is

easier for management to make decisions regarding invested capital and decisions regarding

investments in the markets. It is also an incredibly valuable method for future planning.

Question 2

(a) Calculate the following variances for the last month:

(i) the material usage variance for each ingredient and in total

Should use

(KG)

Did

use

(KG)

Difference(K

G)

Standar

d

cost/kg

($)

Variance(

$)

Alpha 1840 2200 360A 2 720A

Beta 2760 2500 260F 5 1300F

Gam

ma 920 920 1

5520 5620 580F

(ii) the total material Mix variance.

AQSM

AQA

M

Difference(KG

)

Standard

cost/kg

($)

Variance($

)

Alpha 1873.33 2200 326.67A 2 653.34A

Beta 2810 2500 310F 5 1550F

Gamm 963.67 920 16.67F 1 16.67

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

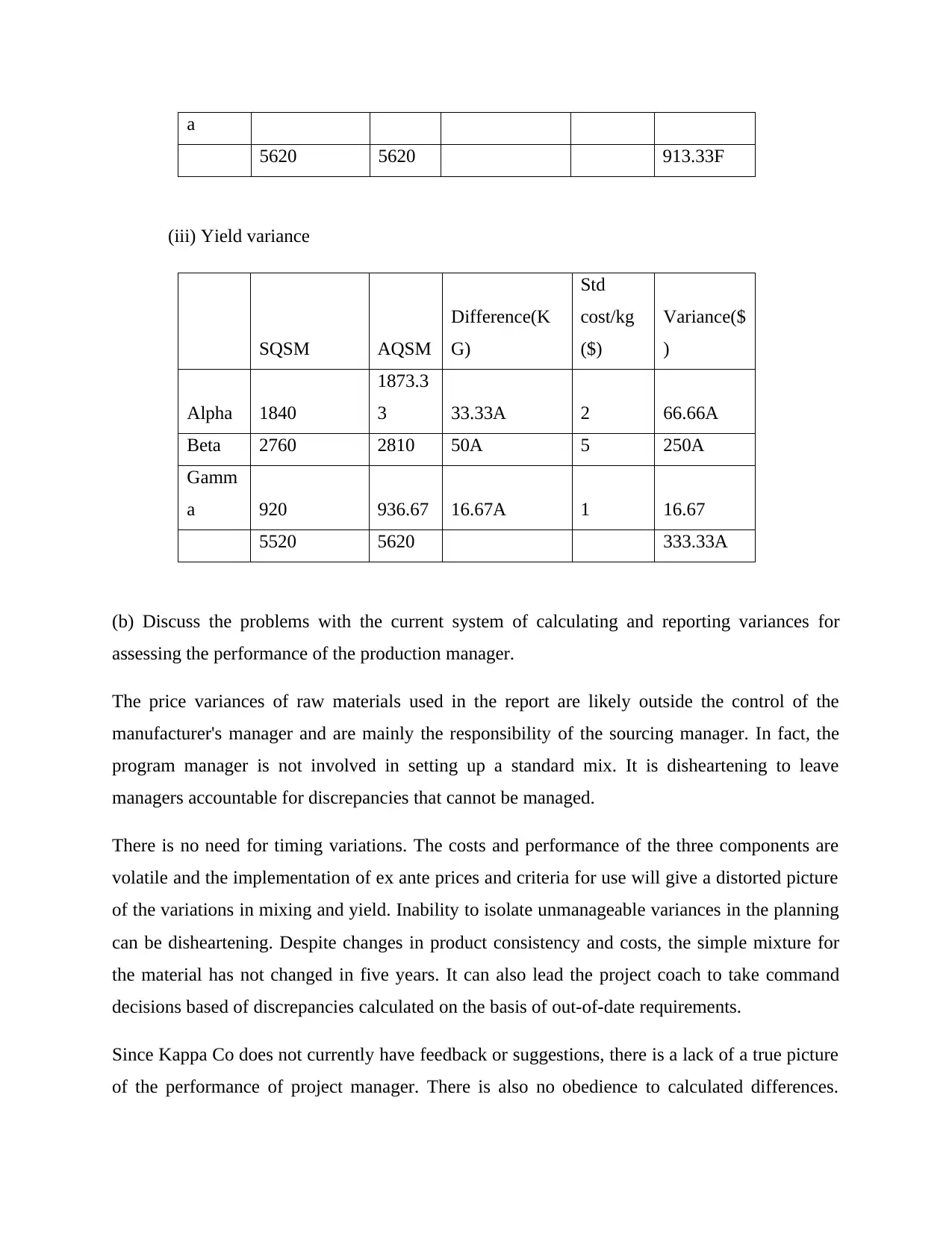

a

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM

Difference(K

G)

Std

cost/kg

($)

Variance($

)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamm

a 920 936.67 16.67A 1 16.67

5520 5620 333.33A

(b) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager.

The price variances of raw materials used in the report are likely outside the control of the

manufacturer's manager and are mainly the responsibility of the sourcing manager. In fact, the

program manager is not involved in setting up a standard mix. It is disheartening to leave

managers accountable for discrepancies that cannot be managed.

There is no need for timing variations. The costs and performance of the three components are

volatile and the implementation of ex ante prices and criteria for use will give a distorted picture

of the variations in mixing and yield. Inability to isolate unmanageable variances in the planning

can be disheartening. Despite changes in product consistency and costs, the simple mixture for

the material has not changed in five years. It can also lead the project coach to take command

decisions based of discrepancies calculated on the basis of out-of-date requirements.

Since Kappa Co does not currently have feedback or suggestions, there is a lack of a true picture

of the performance of project manager. There is also no obedience to calculated differences.

5620 5620 913.33F

(iii) Yield variance

SQSM AQSM

Difference(K

G)

Std

cost/kg

($)

Variance($

)

Alpha 1840

1873.3

3 33.33A 2 66.66A

Beta 2760 2810 50A 5 250A

Gamm

a 920 936.67 16.67A 1 16.67

5520 5620 333.33A

(b) Discuss the problems with the current system of calculating and reporting variances for

assessing the performance of the production manager.

The price variances of raw materials used in the report are likely outside the control of the

manufacturer's manager and are mainly the responsibility of the sourcing manager. In fact, the

program manager is not involved in setting up a standard mix. It is disheartening to leave

managers accountable for discrepancies that cannot be managed.

There is no need for timing variations. The costs and performance of the three components are

volatile and the implementation of ex ante prices and criteria for use will give a distorted picture

of the variations in mixing and yield. Inability to isolate unmanageable variances in the planning

can be disheartening. Despite changes in product consistency and costs, the simple mixture for

the material has not changed in five years. It can also lead the project coach to take command

decisions based of discrepancies calculated on the basis of out-of-date requirements.

Since Kappa Co does not currently have feedback or suggestions, there is a lack of a true picture

of the performance of project manager. There is also no obedience to calculated differences.

Since Kappa Co does not appear to place any focus on discrepancies, the team leader will not be

able to control expenses that can become unmotivated, which could negatively impact Kappa Co

as whole. It can be demonstrated by checking at the maximum usage variance reported, which

suggests a favorable variance of $580, such that the project manager could anticipate good

performance. Even then, if the usage variance is perceived more closely, by means of combining

and yield calculations, it can be observed that it was driven by a change in the blend. There is a

strong link between the two of them. Materials mix heterogeneity and material yield volatility,

using a blend of products that differed from default, resulted in savings of $913.33; however, the

yield was marginally lower than would have been produced by Kappa Co if the traditional

mixture of products had been implemented. Also changing the blend can have an effect on

quality and, as a result, on sales, and there is no detail on this.

Question 3

Zero-based budgeting (ZBB) is a form of financial planning from the beginning. The plan does

not rely on past budgets. Instead, the strategy ends at empty. For zero-based financial

management, any expense must be clarified before adding it to the key function. The goal of

zero-based financial planning is to decrease expenses by emphasizing where it is possible to

eliminate spending. Zero-based budgeting (ZBB) is a technique that aims to align business

expenditures with financial goals. The strategy helps organizations to create their yearly budget

from zero every year and checks have been carried out to ensure that all elements of the yearly

budget are spending, acceptable and produce better savings.

Function of ZBB in the preparation and organization of:

ZBB enables high-level strategic priorities to be integrated into the budgeting process by relating

them to proper business regions of the business, where spending can be clustered first and then

measured against historical results and current targets. It also enhances departmental cohesion

and coordination and motivates staff by including them in decision-making. In addition, during

the preparation of the project, potential changes over the next year are also taken into

consideration, above prior experience. If there is a weakness or flaw in the previous year's plan

that has not been detected by any agency so far, it is very difficult to prepare the required budget

for both the coming years. These components are addressed in the zero-loss budgetary control.

able to control expenses that can become unmotivated, which could negatively impact Kappa Co

as whole. It can be demonstrated by checking at the maximum usage variance reported, which

suggests a favorable variance of $580, such that the project manager could anticipate good

performance. Even then, if the usage variance is perceived more closely, by means of combining

and yield calculations, it can be observed that it was driven by a change in the blend. There is a

strong link between the two of them. Materials mix heterogeneity and material yield volatility,

using a blend of products that differed from default, resulted in savings of $913.33; however, the

yield was marginally lower than would have been produced by Kappa Co if the traditional

mixture of products had been implemented. Also changing the blend can have an effect on

quality and, as a result, on sales, and there is no detail on this.

Question 3

Zero-based budgeting (ZBB) is a form of financial planning from the beginning. The plan does

not rely on past budgets. Instead, the strategy ends at empty. For zero-based financial

management, any expense must be clarified before adding it to the key function. The goal of

zero-based financial planning is to decrease expenses by emphasizing where it is possible to

eliminate spending. Zero-based budgeting (ZBB) is a technique that aims to align business

expenditures with financial goals. The strategy helps organizations to create their yearly budget

from zero every year and checks have been carried out to ensure that all elements of the yearly

budget are spending, acceptable and produce better savings.

Function of ZBB in the preparation and organization of:

ZBB enables high-level strategic priorities to be integrated into the budgeting process by relating

them to proper business regions of the business, where spending can be clustered first and then

measured against historical results and current targets. It also enhances departmental cohesion

and coordination and motivates staff by including them in decision-making. In addition, during

the preparation of the project, potential changes over the next year are also taken into

consideration, above prior experience. If there is a weakness or flaw in the previous year's plan

that has not been detected by any agency so far, it is very difficult to prepare the required budget

for both the coming years. These components are addressed in the zero-loss budgetary control.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incremental budgeting: Incremental budgeting is a type of budgeting process that relies on the

assumption that, by making just a few small changes to the current budget, a budget agreement

may be best defined. In other terms, the existing budget can be used for fiscal oversight on the

basis of which further changes are made or removed from the specific sums for the calculation of

spending plan sums. Incremental budgeting is commonly regarded as the most stringent method

for all forms of financial management. Incremental budgeting is the safest approach. Since the

schedule is used for the current time to predict the future plan, accurate projections are not

needed. Sometimes, only a few hypotheses are required in the budgeting process. Finally, the

simplicity of the strategy allows companies to save time in financial management.

Role of IB in planning and coordination:

Incremental budgets are necessary to illustrate the financial ramifications of the proposals, to

outline the tools required to execute such plans and to provide a means of measuring, reviewing

and tracking the results achieved as compared to the plans. The budget could also avert imminent

emergencies. Gradual budgeting is a central component of administrative preparation, focused on

the principle of making small changes to the existing budget in order to fulfill the upcoming

budget. Only incremental quantities are used to meet the most recent budgeted estimates. There

is no fixed guideline for meeting the incremental budget, but a plan is followed. The total

budgeting approach begins with the assumption that the expenses incurred in the past year will

be the baseline for the estimates for the present year. An overview into the positives and pitfalls

to gradual budgeting will help us explain the definition. The budget used by the current fiscal

year will become the basis for the next year's funds allocated. Experts predict both departments

to continue to work at their existing amount of spending, and if any new sums are expected, the

expenditure estimates for the next year will be used. Cases where expenditure should be lower

could, in the face of those expectations, result in a reduction in the budget from the current bass.

assumption that, by making just a few small changes to the current budget, a budget agreement

may be best defined. In other terms, the existing budget can be used for fiscal oversight on the

basis of which further changes are made or removed from the specific sums for the calculation of

spending plan sums. Incremental budgeting is commonly regarded as the most stringent method

for all forms of financial management. Incremental budgeting is the safest approach. Since the

schedule is used for the current time to predict the future plan, accurate projections are not

needed. Sometimes, only a few hypotheses are required in the budgeting process. Finally, the

simplicity of the strategy allows companies to save time in financial management.

Role of IB in planning and coordination:

Incremental budgets are necessary to illustrate the financial ramifications of the proposals, to

outline the tools required to execute such plans and to provide a means of measuring, reviewing

and tracking the results achieved as compared to the plans. The budget could also avert imminent

emergencies. Gradual budgeting is a central component of administrative preparation, focused on

the principle of making small changes to the existing budget in order to fulfill the upcoming

budget. Only incremental quantities are used to meet the most recent budgeted estimates. There

is no fixed guideline for meeting the incremental budget, but a plan is followed. The total

budgeting approach begins with the assumption that the expenses incurred in the past year will

be the baseline for the estimates for the present year. An overview into the positives and pitfalls

to gradual budgeting will help us explain the definition. The budget used by the current fiscal

year will become the basis for the next year's funds allocated. Experts predict both departments

to continue to work at their existing amount of spending, and if any new sums are expected, the

expenditure estimates for the next year will be used. Cases where expenditure should be lower

could, in the face of those expectations, result in a reduction in the budget from the current bass.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.