Financial Analysis: Costs, Revenues, Costing Systems, and Budgeting

VerifiedAdded on 2020/10/22

|18

|3789

|465

Report

AI Summary

This report provides a comprehensive analysis of costs and revenues within a manufacturing (Automotive) company context. It explores the purpose and importance of internal reporting, including the interrelation of various costing systems like job and process costing. The report identifies the responsibilities of cost, profit, and investment centers. It classifies different types of costs (direct, indirect, variable, fixed) and their applications in costing. It also differentiates between marginal and absorption costing, discussing their implications on product costing and inventory valuation. The report delves into inventory valuation methods such as FIFO and LIFO. Furthermore, it examines overhead cost allocation to production and service centers, calculating overhead absorption rates and addressing under/over recovered overheads. The report includes a comparison of budget costs with actual costs, variance analysis for managerial information, and the preparation of managerial reports. Finally, it presents estimated future income and costs for decision-making, exploring the impact of changing activity levels on unit costs, and identifying factors influencing short-term and long-term decisions.

COSTS

AND

REVENUES

AND

REVENUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose of internal reporting and its importance for the management............................1

1.2 Interrelation of various costing systems .........................................................................1

1.3 Identification of the responsibility of costs centre, profit centre, investment centre within

organisation............................................................................................................................2

1.4 Classification of different types of costs and their uses in costing...................................2

1.5 Differences between marginal costing and absorption costing........................................3

TASK 2 ...........................................................................................................................................3

2.1 Cost information for material, labour and expenses in accordance with the organisation’s

costing procedure....................................................................................................................3

2.2 Analysation of cost information for material, labour and expenses in accordance with the.4

Organisation...........................................................................................................................4

2.3 Several stages of Inventory valuation...............................................................................4

2.4 Valuation of inventory by using First In First Out(FIFO) and Last In First Out Method 4

2.5 Nature of Fixed, variable and Semi variable costs...........................................................6

2.6 Analysing the costs information by costing system ........................................................7

TASK 3............................................................................................................................................7

3.1 Abstraction of overhead costs to production and service cost centres in accordance with

agreed bases............................................................................................................................7

3.2 Calculation of overhead absorption rates in accordance with suitable bases of absorption. 7

3.3 Make adjustments for under or over recovered overhead costs in accordance with

established procedures............................................................................................................9

3.4 Implementation of changes to methods at regular intervals in absorption ...................10

3.5 Communicate with relevant staff to resolve any queries in overhead cost data ..........11

TASK 4..........................................................................................................................................11

4.1 Comparison of the budget costs with actual costs, finding of variances........................11

4.2 Analysing variances for managerial information...........................................................12

4.3 Information for budget holders for the potential variances ..........................................12

INTRODUCTION ........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose of internal reporting and its importance for the management............................1

1.2 Interrelation of various costing systems .........................................................................1

1.3 Identification of the responsibility of costs centre, profit centre, investment centre within

organisation............................................................................................................................2

1.4 Classification of different types of costs and their uses in costing...................................2

1.5 Differences between marginal costing and absorption costing........................................3

TASK 2 ...........................................................................................................................................3

2.1 Cost information for material, labour and expenses in accordance with the organisation’s

costing procedure....................................................................................................................3

2.2 Analysation of cost information for material, labour and expenses in accordance with the.4

Organisation...........................................................................................................................4

2.3 Several stages of Inventory valuation...............................................................................4

2.4 Valuation of inventory by using First In First Out(FIFO) and Last In First Out Method 4

2.5 Nature of Fixed, variable and Semi variable costs...........................................................6

2.6 Analysing the costs information by costing system ........................................................7

TASK 3............................................................................................................................................7

3.1 Abstraction of overhead costs to production and service cost centres in accordance with

agreed bases............................................................................................................................7

3.2 Calculation of overhead absorption rates in accordance with suitable bases of absorption. 7

3.3 Make adjustments for under or over recovered overhead costs in accordance with

established procedures............................................................................................................9

3.4 Implementation of changes to methods at regular intervals in absorption ...................10

3.5 Communicate with relevant staff to resolve any queries in overhead cost data ..........11

TASK 4..........................................................................................................................................11

4.1 Comparison of the budget costs with actual costs, finding of variances........................11

4.2 Analysing variances for managerial information...........................................................12

4.3 Information for budget holders for the potential variances ..........................................12

4.4Preparation of managerial reports.................................................................................12

Work backwards from there and create customs fields and filters in system of accounting ........12

TASK 5..........................................................................................................................................12

5.1 Presentation of estimated future income and costs for decision making:.....................12

5.2 Examining the effect of changing activity levels on unit costs......................................13

5.3 Evaluation of both the effect of changing activity levels on unit costs. ........................13

5.4 Identifying factors that influences short-term and long term decision making..............14

CONCLUSION..............................................................................................................................14

..............................................................................................................................................14

REFERENCES .............................................................................................................................15

Work backwards from there and create customs fields and filters in system of accounting ........12

TASK 5..........................................................................................................................................12

5.1 Presentation of estimated future income and costs for decision making:.....................12

5.2 Examining the effect of changing activity levels on unit costs......................................13

5.3 Evaluation of both the effect of changing activity levels on unit costs. ........................13

5.4 Identifying factors that influences short-term and long term decision making..............14

CONCLUSION..............................................................................................................................14

..............................................................................................................................................14

REFERENCES .............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1INTRODUCTION

The terms cost and revenues are associated with manufacturing (Automotive) company,

the costs refers to the expense incurred in order to manufacture goods and services with the

motive to generate the profit and revenues for the business organisation. Under manufacturing

process the goods or services are produced, the manufacturer sells them in the market to several

retailers and consumers. The consumers pays prices for buying goods or services to the producer

or retailer (Burchell and Listokin, 2012). This becomes the income source of the producer. So in

order to, the producer incurred the expenditure while the process of manufacturing (purchase of

raw material, labour, machinery cost etc.) to purchase factors of production and then receives

money from the consumers by selling those goods and services to them.

This report pertain the knowledge about the costs and revenues, methods of managing

the inventory, costing techniques as well as the budgeting methods. This report helps in better

understanding of the cost and revenues concepts of the business organisation.

2TASK 1

1.1 Purpose of internal reporting and its importance for the management

Internal reporting means the consolidate financial statements that are prepared to know

the business performance of the organisation and these information pertain costs, revenues,

profits are concluded in profit and loss statement and the final statement of balance sheet, which

shows the overall performance of the business and the important thing is that preparation of these

consolidate statements are called internal report of business and it reporting to managers, Board

of directors, CEO and other internal users in order to make decisions regrading future business

operations. The management needs this annual report because these information pertains the

useful information regarding the tax, gross profit, profit after tax etc. and these are the material

facts that are essential to disclose as the mandatory requirement by IFRS, as these material are

base of future planning and future decision makings.

1.2 Interrelation of various costing systems

The costing system is used to calculate the cost incurred in performing the business

operations in order to generate profits for the organisations. Costing system are intended for

internal use and not for reporting requirements but are essential to find-out the outcomes from

the business operations which are to be shown in internal reports. The costing system pertains

1

The terms cost and revenues are associated with manufacturing (Automotive) company,

the costs refers to the expense incurred in order to manufacture goods and services with the

motive to generate the profit and revenues for the business organisation. Under manufacturing

process the goods or services are produced, the manufacturer sells them in the market to several

retailers and consumers. The consumers pays prices for buying goods or services to the producer

or retailer (Burchell and Listokin, 2012). This becomes the income source of the producer. So in

order to, the producer incurred the expenditure while the process of manufacturing (purchase of

raw material, labour, machinery cost etc.) to purchase factors of production and then receives

money from the consumers by selling those goods and services to them.

This report pertain the knowledge about the costs and revenues, methods of managing

the inventory, costing techniques as well as the budgeting methods. This report helps in better

understanding of the cost and revenues concepts of the business organisation.

2TASK 1

1.1 Purpose of internal reporting and its importance for the management

Internal reporting means the consolidate financial statements that are prepared to know

the business performance of the organisation and these information pertain costs, revenues,

profits are concluded in profit and loss statement and the final statement of balance sheet, which

shows the overall performance of the business and the important thing is that preparation of these

consolidate statements are called internal report of business and it reporting to managers, Board

of directors, CEO and other internal users in order to make decisions regrading future business

operations. The management needs this annual report because these information pertains the

useful information regarding the tax, gross profit, profit after tax etc. and these are the material

facts that are essential to disclose as the mandatory requirement by IFRS, as these material are

base of future planning and future decision makings.

1.2 Interrelation of various costing systems

The costing system is used to calculate the cost incurred in performing the business

operations in order to generate profits for the organisations. Costing system are intended for

internal use and not for reporting requirements but are essential to find-out the outcomes from

the business operations which are to be shown in internal reports. The costing system pertains

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

two systems namely. Job costing system(used for individual job purpose) and process costing

system(used for entire process of production). The main relation between them is that the costing

systems are used to calculate the costs incurred by the business but the process costing is used to

calculate the costs incurred in entire process of production and the job costing system is used to

calculate the costs incurred in performing the particular task or job (Sen and et. al., 2012).

1.3 Identification of the responsibility of costs centre, profit centre, investment centre within

organisation

The organisation delegates the whole responsibilities to different centres according to

their workings and nature. In an organisation, there are several centres like cost centre, profit

centre and investment centre ad these centres have their own responsibilities according to their

nature.

Cost centre: It is that business unit which records or incurs only costs and expenses of

business organisation but does not generate revenues. Costs centre preforms this function

of recording expenses and costs among several departments of the organisation like

accounting, human resource and IT departments (Gudeman, 2013).

Profit centre: It is that business unit which records and incurs profits or revenues, earns

by the selling of goods and services to customers.

Investment centre: it requires the amount for the investment in order to generate some

inflow of the cash or to earn some interests or revenues.

1.4 Classification of different types of costs and their uses in costing

There are several types of costs involved in costing which are as follows.

Direct costs: These are the costs which are directly related to the production process and

these costs have direct affect on the production. For example: cost of material, direct

labour etc.

Indirect costs: these are the costs which are not related to the production and they are also

known as common costs and joint costs. For example, factory overhead, rent , telephone

expenses.

Variable costs: Variable costs are those which are not fixed in nature and also these costs

are varies or fluctuates rapidly. Example of these costs are direct labour, sales

commission based on sales (Bazaraa, Sherali and Shetty, 2013). variable costs are used to

2

system(used for entire process of production). The main relation between them is that the costing

systems are used to calculate the costs incurred by the business but the process costing is used to

calculate the costs incurred in entire process of production and the job costing system is used to

calculate the costs incurred in performing the particular task or job (Sen and et. al., 2012).

1.3 Identification of the responsibility of costs centre, profit centre, investment centre within

organisation

The organisation delegates the whole responsibilities to different centres according to

their workings and nature. In an organisation, there are several centres like cost centre, profit

centre and investment centre ad these centres have their own responsibilities according to their

nature.

Cost centre: It is that business unit which records or incurs only costs and expenses of

business organisation but does not generate revenues. Costs centre preforms this function

of recording expenses and costs among several departments of the organisation like

accounting, human resource and IT departments (Gudeman, 2013).

Profit centre: It is that business unit which records and incurs profits or revenues, earns

by the selling of goods and services to customers.

Investment centre: it requires the amount for the investment in order to generate some

inflow of the cash or to earn some interests or revenues.

1.4 Classification of different types of costs and their uses in costing

There are several types of costs involved in costing which are as follows.

Direct costs: These are the costs which are directly related to the production process and

these costs have direct affect on the production. For example: cost of material, direct

labour etc.

Indirect costs: these are the costs which are not related to the production and they are also

known as common costs and joint costs. For example, factory overhead, rent , telephone

expenses.

Variable costs: Variable costs are those which are not fixed in nature and also these costs

are varies or fluctuates rapidly. Example of these costs are direct labour, sales

commission based on sales (Bazaraa, Sherali and Shetty, 2013). variable costs are used to

2

show the costs incurred by the business, that costs are not fixed costs changes according

to the activity levels.

Fixed costs: the fixed costs are that costs which remains constant throughout the

particular period of production regardless of the level of activity. For example, rent,

insurance, depreciation etc. fixed costs are used to show the cost that does not change

even if the production stopped. Such costs are Rent of building etc.

1.5 Differences between marginal costing and absorption costing

There are some differences between the marginal costing and absorption costing, are as

follows.

Marginal costing Absorption costing

Under marginal costing only variable costs are

considered for product costing and inventory

valuation.

Under the absorption costing both fixed and

variable costs are considered for product

costing and inventory valuation.

Fixed costs are concerned for as periodic costs

and therefore the profitability of different

products is evaluated by their P/V ratio.

Fixed costs are charged to the cost of

production, as every produced product involves

some share of fixed costs and thus profitability

of the products is influenced by apportioning of

fixed costs.

Cost data presented a summary of total

contribution of each product.

Cost data are presented in stodgy pattern, as net

profit from each product after the deduction of

the fixed costs.

3TASK 2

2.1 Cost information for material, labour and expenses in accordance with the organisation’s

costing procedure

Under the costing procedure first of all, the prime costs or direct costs are calculated to

quantify the cost of gross margin, as the prime or direct costs includes the costs of material, costs

of labour and all those costs which are related to the production of the organisation.

3

to the activity levels.

Fixed costs: the fixed costs are that costs which remains constant throughout the

particular period of production regardless of the level of activity. For example, rent,

insurance, depreciation etc. fixed costs are used to show the cost that does not change

even if the production stopped. Such costs are Rent of building etc.

1.5 Differences between marginal costing and absorption costing

There are some differences between the marginal costing and absorption costing, are as

follows.

Marginal costing Absorption costing

Under marginal costing only variable costs are

considered for product costing and inventory

valuation.

Under the absorption costing both fixed and

variable costs are considered for product

costing and inventory valuation.

Fixed costs are concerned for as periodic costs

and therefore the profitability of different

products is evaluated by their P/V ratio.

Fixed costs are charged to the cost of

production, as every produced product involves

some share of fixed costs and thus profitability

of the products is influenced by apportioning of

fixed costs.

Cost data presented a summary of total

contribution of each product.

Cost data are presented in stodgy pattern, as net

profit from each product after the deduction of

the fixed costs.

3TASK 2

2.1 Cost information for material, labour and expenses in accordance with the organisation’s

costing procedure

Under the costing procedure first of all, the prime costs or direct costs are calculated to

quantify the cost of gross margin, as the prime or direct costs includes the costs of material, costs

of labour and all those costs which are related to the production of the organisation.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

After the calculation of prime costs or gross margin the next requirement is to quantify

the overall revenues and expenses from the business operation. Therefore, the calculation of

indirect expense or costs are need to be calculated as for quantifying the profit of the

organisation. As for the calculation of operating revenues or contribution the prime or direct

costs are calculated first which includes material and labour costs and then other costs which are

not related to the production are to calculated direct costs calculations.

2.2 Analysation of cost information for material, labour and expenses in accordance with the

Organisation

The cost incurred in raw material cost incurred is $11000 and direct labour is $9000 and

the overhead expenditure $15000, it shows the production overheads of the organisation

increases and affecting the revenues of the business it depicts that the management is unable to

manage the production process properly.

2.3 Several stages of Inventory valuation

There are the three stages of inventory stocks and these three stages are as follows.

Begins with raw materials:it is the form of the raw material which are used to prepare

the finished goods. These raw material are used as input to produce the out put.

Intermediate goods or stock: these are the goods of half manufactured goods and are

used to manufacture as the intermediate goods or unfinished goods to produce the

finished goods.

Finished goods or final inventory: these are the finished goods which are manufactured

by using input and intermediate goods. These are termed as the out of the company.

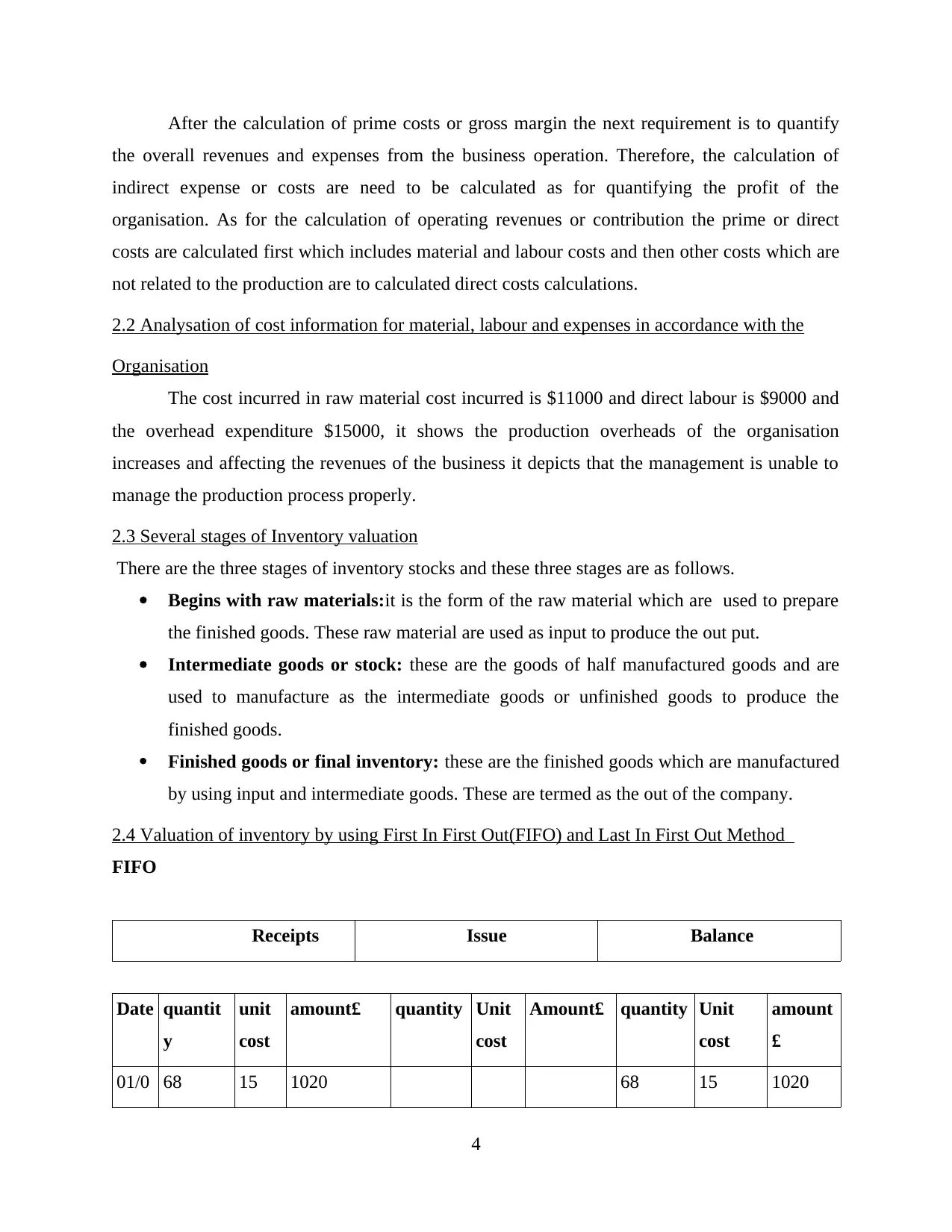

2.4 Valuation of inventory by using First In First Out(FIFO) and Last In First Out Method

FIFO

Receipts Issue Balance

Date quantit

y

unit

cost

amount£ quantity Unit

cost

Amount£ quantity Unit

cost

amount

£

01/0 68 15 1020 68 15 1020

4

the overall revenues and expenses from the business operation. Therefore, the calculation of

indirect expense or costs are need to be calculated as for quantifying the profit of the

organisation. As for the calculation of operating revenues or contribution the prime or direct

costs are calculated first which includes material and labour costs and then other costs which are

not related to the production are to calculated direct costs calculations.

2.2 Analysation of cost information for material, labour and expenses in accordance with the

Organisation

The cost incurred in raw material cost incurred is $11000 and direct labour is $9000 and

the overhead expenditure $15000, it shows the production overheads of the organisation

increases and affecting the revenues of the business it depicts that the management is unable to

manage the production process properly.

2.3 Several stages of Inventory valuation

There are the three stages of inventory stocks and these three stages are as follows.

Begins with raw materials:it is the form of the raw material which are used to prepare

the finished goods. These raw material are used as input to produce the out put.

Intermediate goods or stock: these are the goods of half manufactured goods and are

used to manufacture as the intermediate goods or unfinished goods to produce the

finished goods.

Finished goods or final inventory: these are the finished goods which are manufactured

by using input and intermediate goods. These are termed as the out of the company.

2.4 Valuation of inventory by using First In First Out(FIFO) and Last In First Out Method

FIFO

Receipts Issue Balance

Date quantit

y

unit

cost

amount£ quantity Unit

cost

Amount£ quantity Unit

cost

amount

£

01/0 68 15 1020 68 15 1020

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3/01

05/0

3/18

140 15.5 2170 140 15.5 2170

09/0

3/18

68 15 1020

26 15.5 430

11/0

3/18

40 16 640 114 15.5 1767

40 16 640

16/0

3/18

78 16.5 1287 114 15.5 1767

40 16 640

78 16.5 1287

20/0

3/18

114 15.5 1767 38 16 608

2 16 32 78 16.5 1287

29/0

3/18

38 16 608

31/0

3/18

24 16.5 396 54 16.5 891

The closing inventory from the FIFO method is 54 units of (16.5) of 891£

Last In First Out (LIFO)

Receipts issued Balance

5

05/0

3/18

140 15.5 2170 140 15.5 2170

09/0

3/18

68 15 1020

26 15.5 430

11/0

3/18

40 16 640 114 15.5 1767

40 16 640

16/0

3/18

78 16.5 1287 114 15.5 1767

40 16 640

78 16.5 1287

20/0

3/18

114 15.5 1767 38 16 608

2 16 32 78 16.5 1287

29/0

3/18

38 16 608

31/0

3/18

24 16.5 396 54 16.5 891

The closing inventory from the FIFO method is 54 units of (16.5) of 891£

Last In First Out (LIFO)

Receipts issued Balance

5

Date quantit

y

Unit

cost

amount quantit

y

Unit

cost

amount quantit

y

Unit

cost

amount

01/03/1

8

60 15 240 60 15 240

05/03/1

8

140 15.5 2170 140 15.5 2170

14/03/1

8

140 15.5 2170

50 15 750 10 15 150

27/03/1

8

70 16 1120 10 15 150

70 16 1120

29/03/1

8

30 16 480 10 15 150

31/03/1

8

40 16 640

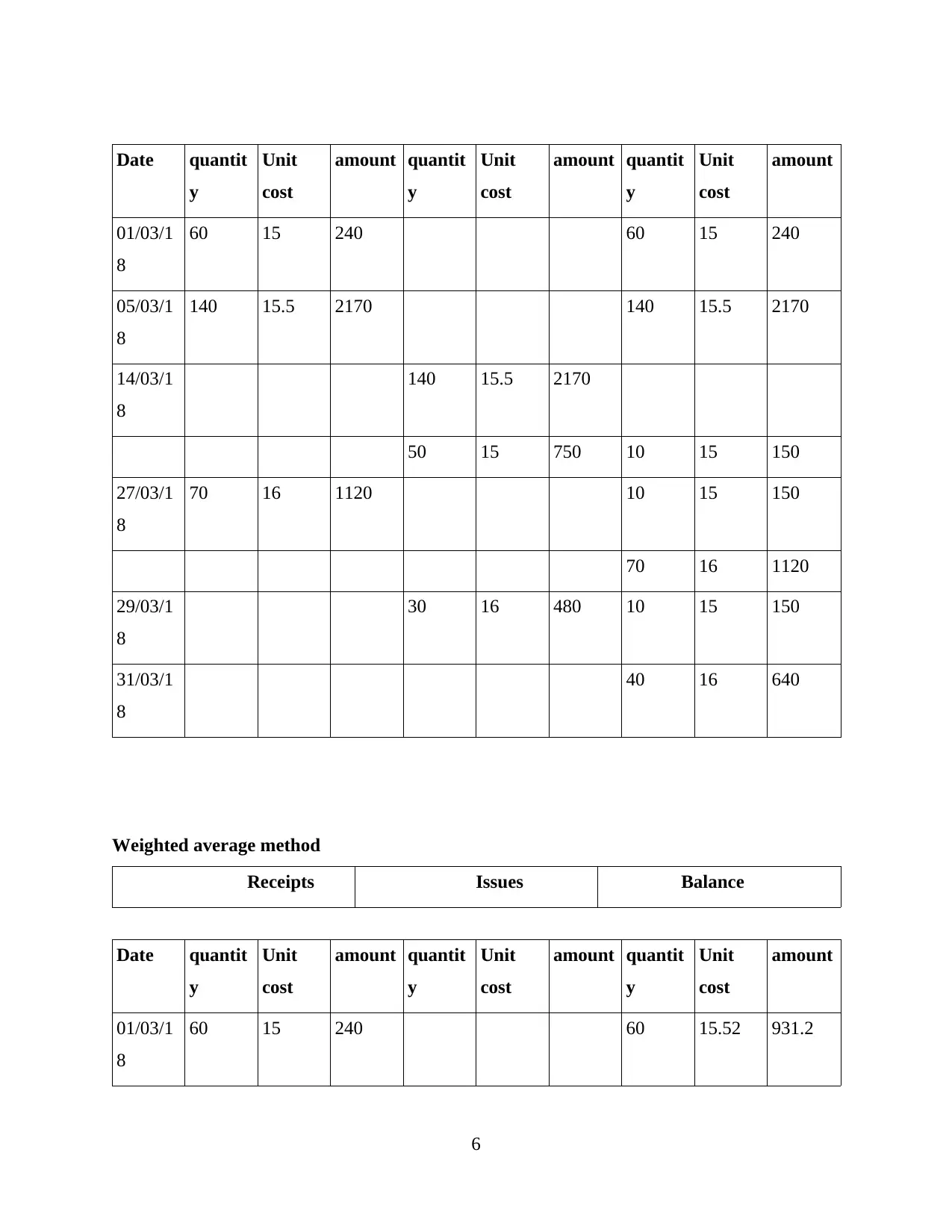

Weighted average method

Receipts Issues Balance

Date quantit

y

Unit

cost

amount quantit

y

Unit

cost

amount quantit

y

Unit

cost

amount

01/03/1

8

60 15 240 60 15.52 931.2

6

y

Unit

cost

amount quantit

y

Unit

cost

amount quantit

y

Unit

cost

amount

01/03/1

8

60 15 240 60 15 240

05/03/1

8

140 15.5 2170 140 15.5 2170

14/03/1

8

140 15.5 2170

50 15 750 10 15 150

27/03/1

8

70 16 1120 10 15 150

70 16 1120

29/03/1

8

30 16 480 10 15 150

31/03/1

8

40 16 640

Weighted average method

Receipts Issues Balance

Date quantit

y

Unit

cost

amount quantit

y

Unit

cost

amount quantit

y

Unit

cost

amount

01/03/1

8

60 15 240 60 15.52 931.2

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

05/03/1

8

140 15.5 2170 140 15.52 2172.8

14/03/1

8

190 15.52 2948.8

27/03/1

8

70 16 1120 10 15.52 155.2

70 15.52 1086.4

29/03/1

8

30 15.52 465.6 50 15.52 776

The inventory valuation by AVCO method, the closing stock remaining is 50units of (15.52)

of 776£.

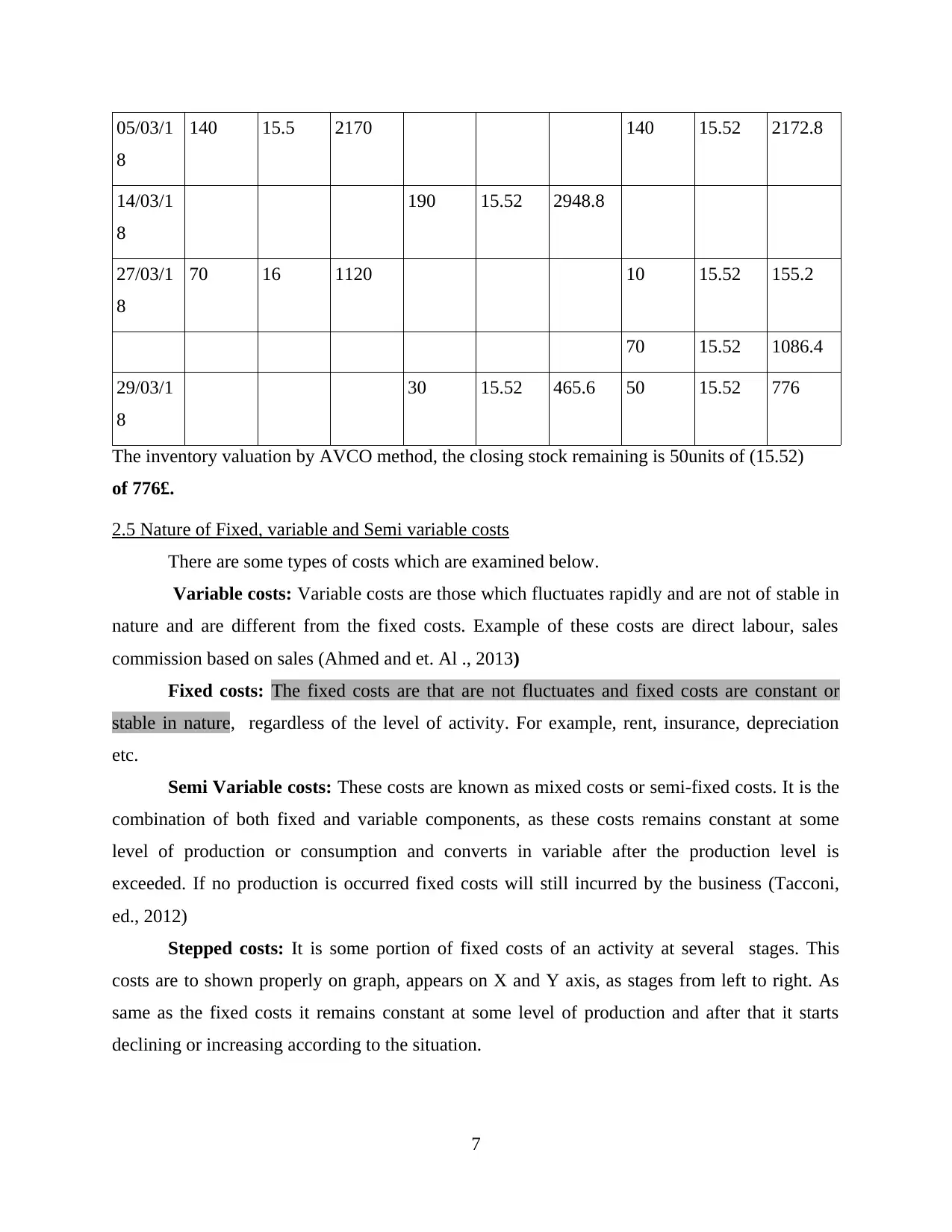

2.5 Nature of Fixed, variable and Semi variable costs

There are some types of costs which are examined below.

Variable costs: Variable costs are those which fluctuates rapidly and are not of stable in

nature and are different from the fixed costs. Example of these costs are direct labour, sales

commission based on sales (Ahmed and et. Al ., 2013)

Fixed costs: The fixed costs are that are not fluctuates and fixed costs are constant or

stable in nature, regardless of the level of activity. For example, rent, insurance, depreciation

etc.

Semi Variable costs: These costs are known as mixed costs or semi-fixed costs. It is the

combination of both fixed and variable components, as these costs remains constant at some

level of production or consumption and converts in variable after the production level is

exceeded. If no production is occurred fixed costs will still incurred by the business (Tacconi,

ed., 2012)

Stepped costs: It is some portion of fixed costs of an activity at several stages. This

costs are to shown properly on graph, appears on X and Y axis, as stages from left to right. As

same as the fixed costs it remains constant at some level of production and after that it starts

declining or increasing according to the situation.

7

8

140 15.5 2170 140 15.52 2172.8

14/03/1

8

190 15.52 2948.8

27/03/1

8

70 16 1120 10 15.52 155.2

70 15.52 1086.4

29/03/1

8

30 15.52 465.6 50 15.52 776

The inventory valuation by AVCO method, the closing stock remaining is 50units of (15.52)

of 776£.

2.5 Nature of Fixed, variable and Semi variable costs

There are some types of costs which are examined below.

Variable costs: Variable costs are those which fluctuates rapidly and are not of stable in

nature and are different from the fixed costs. Example of these costs are direct labour, sales

commission based on sales (Ahmed and et. Al ., 2013)

Fixed costs: The fixed costs are that are not fluctuates and fixed costs are constant or

stable in nature, regardless of the level of activity. For example, rent, insurance, depreciation

etc.

Semi Variable costs: These costs are known as mixed costs or semi-fixed costs. It is the

combination of both fixed and variable components, as these costs remains constant at some

level of production or consumption and converts in variable after the production level is

exceeded. If no production is occurred fixed costs will still incurred by the business (Tacconi,

ed., 2012)

Stepped costs: It is some portion of fixed costs of an activity at several stages. This

costs are to shown properly on graph, appears on X and Y axis, as stages from left to right. As

same as the fixed costs it remains constant at some level of production and after that it starts

declining or increasing according to the situation.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.6 Analysing the costs information by costing system

Costs incurred by the business in different types of costs techniques and by using these

costing techniques there are several types of costs are analysed and classified. Mainly there are

two types of costing techniques namely absorption and marginal costing and these both are

similar in context of aim, but different in context of calculation of fixed costs (Subramaniam. and

Watson, 2016)

TASK 3

3.1 Abstraction of overhead costs to production and service cost centres in accordance with

agreed bases

There are various types of cost which are occurred in the production of goods and

services. It is described as follows:

Direct: It is that cost which is directly affiliated to the production of products.

Depreciation is difficult to quantify for a particular product. Example, commission paid to

suppliers.

Step down: This method assists the cost of a services departments to other operating

departments of the company.

3.2 Calculation of overhead absorption rates in accordance with suitable bases of absorption

Raw material cost basis:

Absorption rate of overhead= Estimated factory overhead/ estimated cost of material

= 150000/110000*100

= 136.6 % of direct labour

Overhead absorption based on direct material cost:

Overhead absorption rate* Material cost of job = Absorbed Overhead

136.36 % * 240 = 327

Direct labour cost basis:

Absorption of overhead rate= Cost of estimated factory overhead/ labour cost*100

= 150000/90000*100

= 166.67 %

Overhead of absorption based on direct labour cost

8

Costs incurred by the business in different types of costs techniques and by using these

costing techniques there are several types of costs are analysed and classified. Mainly there are

two types of costing techniques namely absorption and marginal costing and these both are

similar in context of aim, but different in context of calculation of fixed costs (Subramaniam. and

Watson, 2016)

TASK 3

3.1 Abstraction of overhead costs to production and service cost centres in accordance with

agreed bases

There are various types of cost which are occurred in the production of goods and

services. It is described as follows:

Direct: It is that cost which is directly affiliated to the production of products.

Depreciation is difficult to quantify for a particular product. Example, commission paid to

suppliers.

Step down: This method assists the cost of a services departments to other operating

departments of the company.

3.2 Calculation of overhead absorption rates in accordance with suitable bases of absorption

Raw material cost basis:

Absorption rate of overhead= Estimated factory overhead/ estimated cost of material

= 150000/110000*100

= 136.6 % of direct labour

Overhead absorption based on direct material cost:

Overhead absorption rate* Material cost of job = Absorbed Overhead

136.36 % * 240 = 327

Direct labour cost basis:

Absorption of overhead rate= Cost of estimated factory overhead/ labour cost*100

= 150000/90000*100

= 166.67 %

Overhead of absorption based on direct labour cost

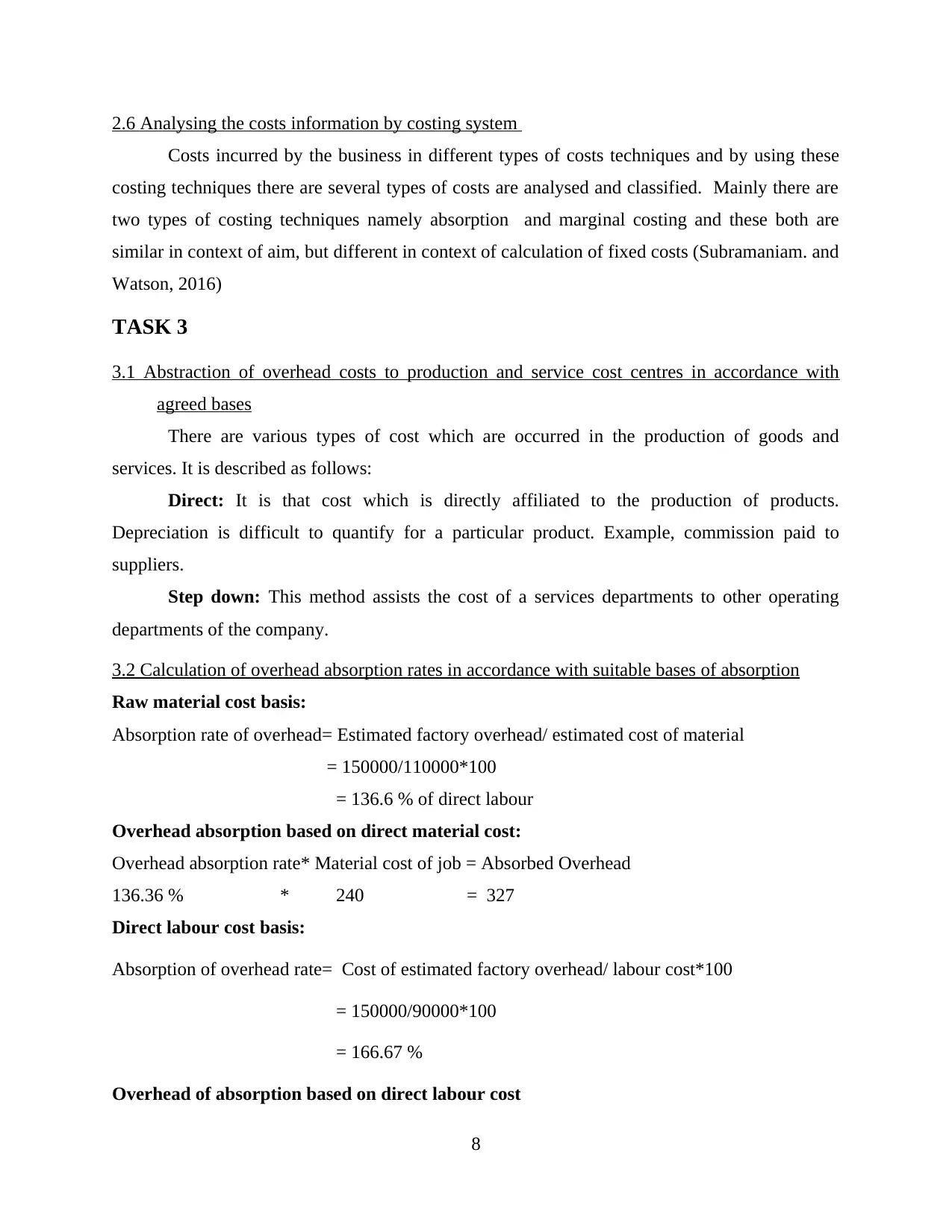

8

Labour cost of job * absorption rate of overhead= Absorption overhead

200* 166.7% = 333

Prime cost basis:

Absorption rate of overhead = Estimated Factory overhead/ estimated prime cost*100

= 150000/200000*100

75 %

Overhead of absorption based on prime cost:

Prime cost of job * absorption rate = Absorbed overhead

240+ 200+* 75% = 330

Units of production basis

Absorption rate = Estimated factory overhead/ units of output* 100

= 150000/500*100

= 30

Overhead based on units of production

Units of output * absorption rate = Absorbed overhead

10* 30 = 300

Direct labour hour basis:

Absorption rate = Estimated factory overhead/ labour rate* 100

= 150000/ 30000*100

= 5

Overhead related to direct labour hours:

Labour hours for the job * absorption rate of overhead = Absorbed overhead

63 * 5 = 315

Machine hour basis:

9

200* 166.7% = 333

Prime cost basis:

Absorption rate of overhead = Estimated Factory overhead/ estimated prime cost*100

= 150000/200000*100

75 %

Overhead of absorption based on prime cost:

Prime cost of job * absorption rate = Absorbed overhead

240+ 200+* 75% = 330

Units of production basis

Absorption rate = Estimated factory overhead/ units of output* 100

= 150000/500*100

= 30

Overhead based on units of production

Units of output * absorption rate = Absorbed overhead

10* 30 = 300

Direct labour hour basis:

Absorption rate = Estimated factory overhead/ labour rate* 100

= 150000/ 30000*100

= 5

Overhead related to direct labour hours:

Labour hours for the job * absorption rate of overhead = Absorbed overhead

63 * 5 = 315

Machine hour basis:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.