Analysis of Costs and Revenues: Financial Reporting and Costing

VerifiedAdded on 2020/12/26

|19

|3782

|497

Report

AI Summary

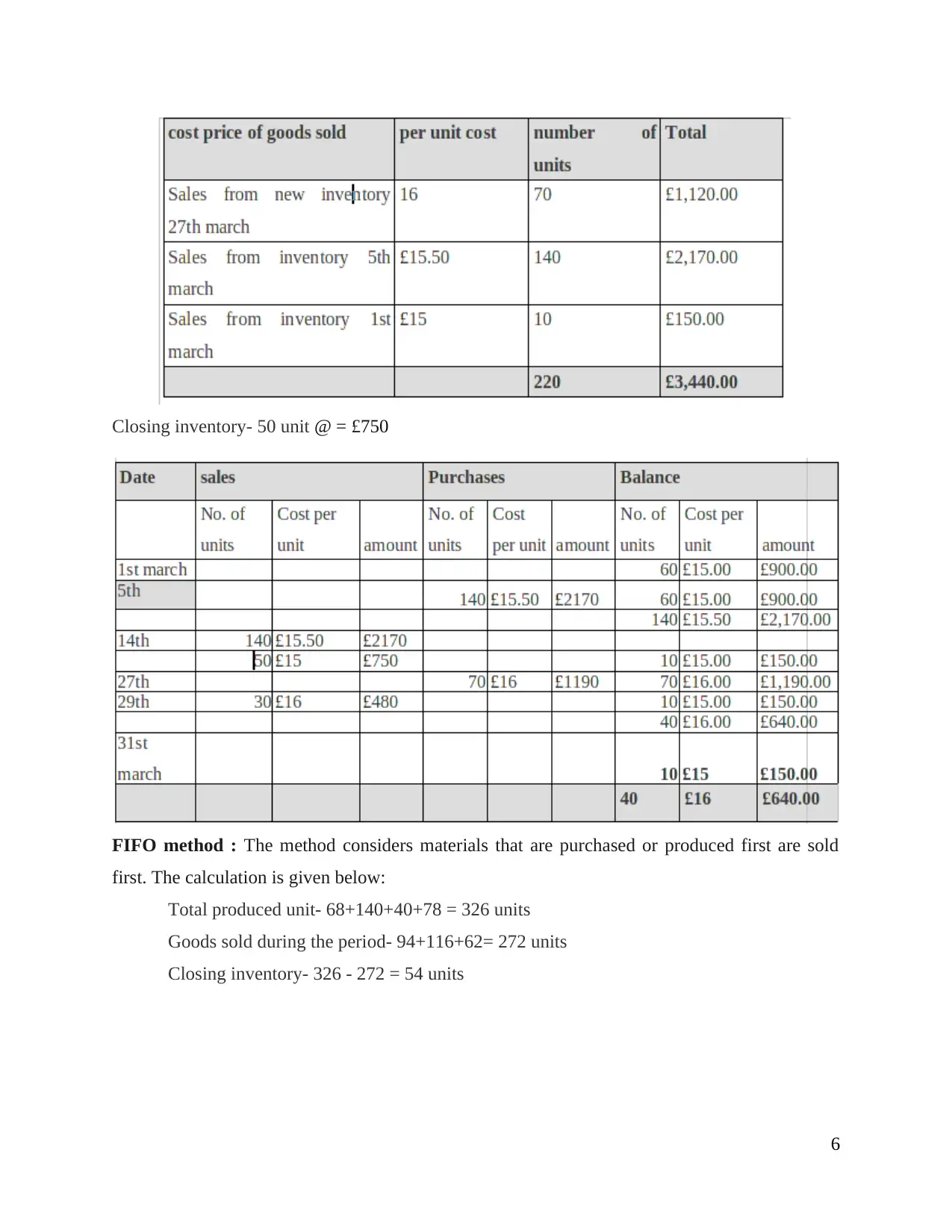

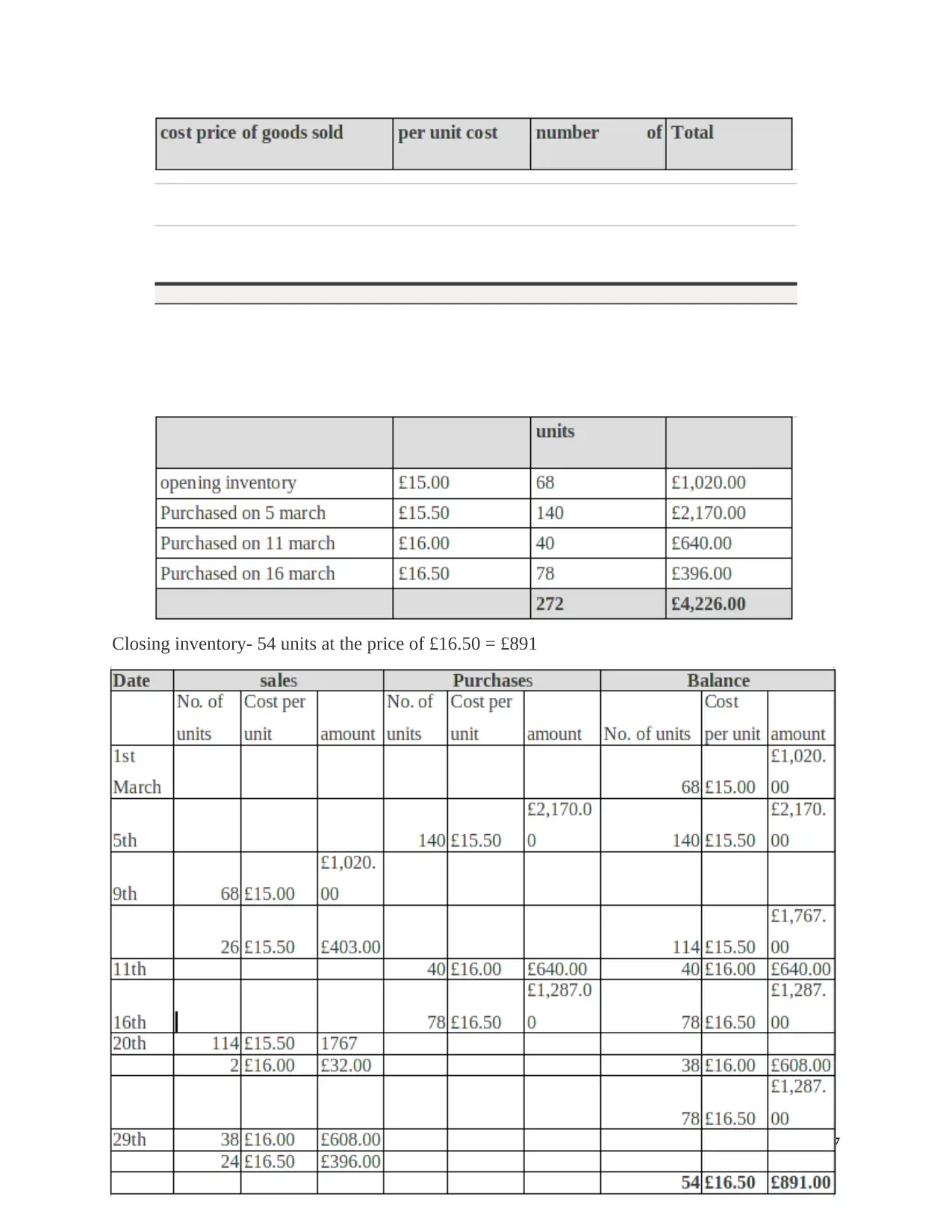

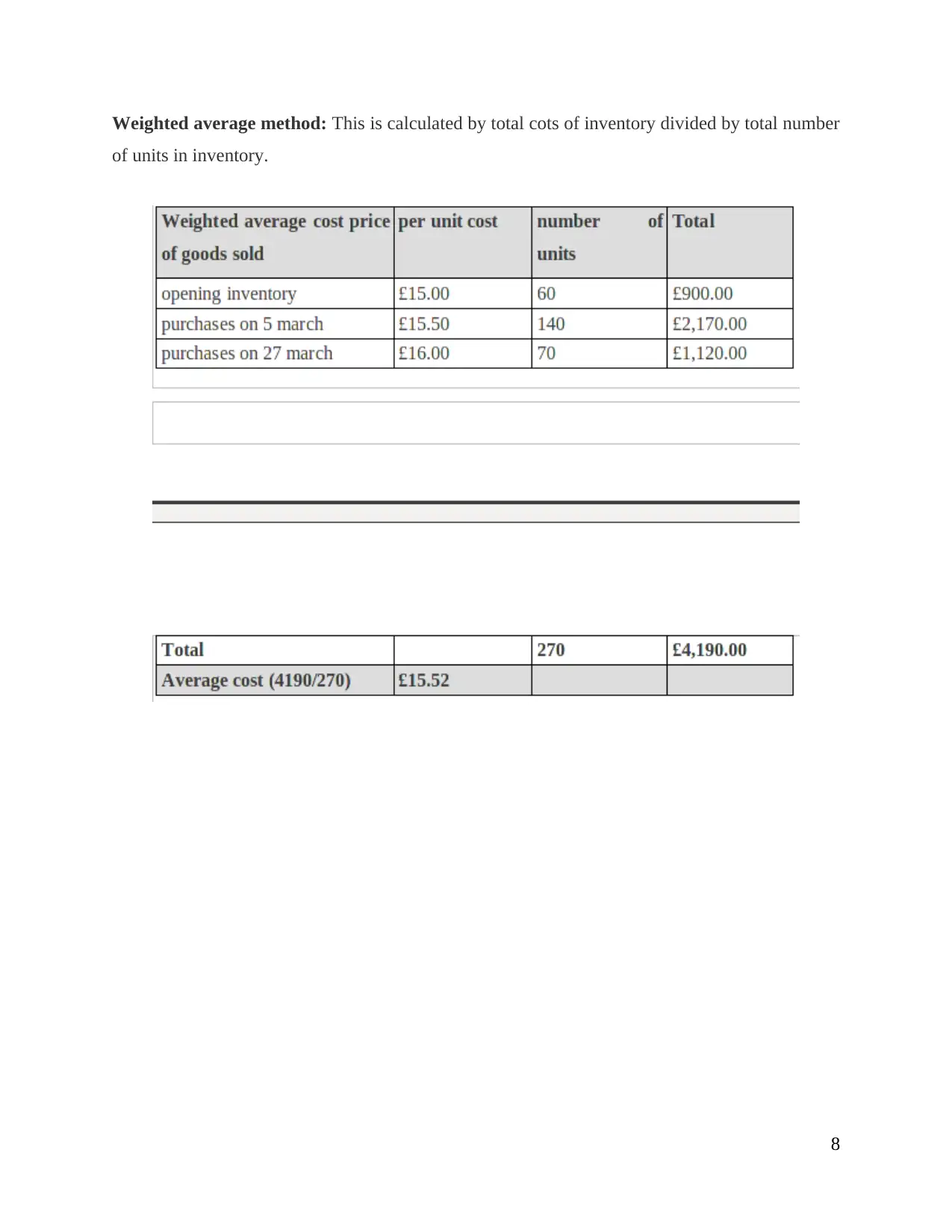

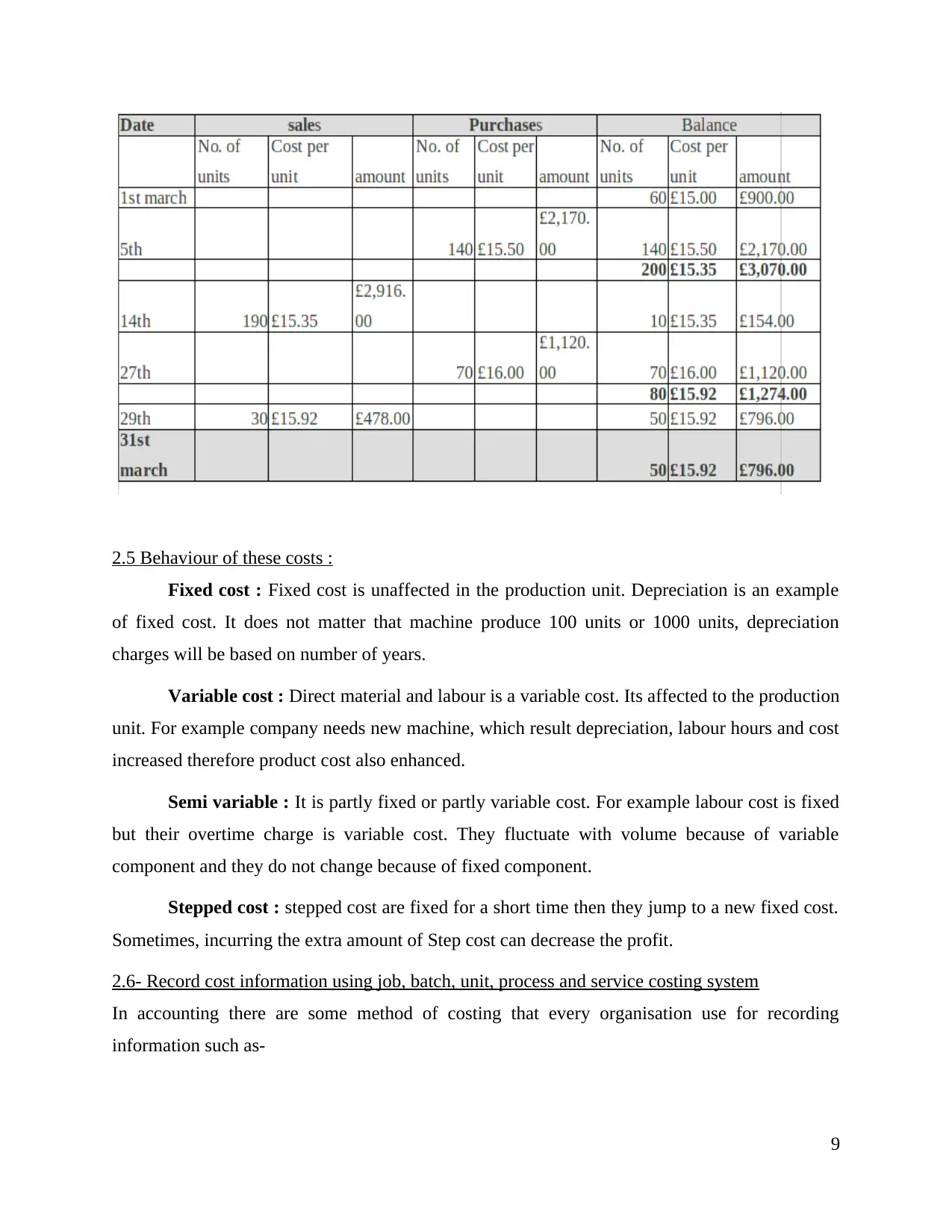

This report provides a comprehensive analysis of costs and revenues, covering various aspects of financial reporting and costing systems. The report begins by exploring the purpose of internal reporting and the relationships between different costing systems, including marginal and absorption costing. It delves into the responsibility centers within an organization, such as cost centers, profit centers, and investment centers. The report then examines different cost classifications and their uses in costing. Further, it covers recording cost information for labor, material, and expenses and analyzing this information according to organizational costing procedures. It examines the various stages of inventory, inventory valuation methods (LIFO, FIFO, and weighted average), and the behavior of different cost types. The report also discusses the recording of cost information using various costing systems (job, batch, unit, process, and service costing). It then moves on to overhead costs, including their allocation and apportionment, calculation of overhead absorption rates, and adjustments for under or over-recovered overhead costs. The report also includes variance analysis, budget comparisons, and providing information for budget holders. Finally, it explores the estimation of future incomes and costs for decision-making, the effect of changing activity levels on unit costs, and factors affecting short-term and long-term decision-making.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.