Internal Reporting, Costing Systems, and Revenue Analysis Report

VerifiedAdded on 2020/12/09

|20

|4174

|114

Report

AI Summary

This report provides a comprehensive analysis of costs and revenues within the context of J.P. Morgon. It begins by outlining the purpose of internal reporting and its significance in providing accurate information to management. The report then explores the relationships between various costing systems, including marginal and absorption costing, and identifies different responsibility centers within an organization. It delves into cost classification, inventory valuation methods (FIFO), and the behavior of costs. Furthermore, the report examines overhead costs, absorption rates, and variance analysis, including methods of allocation and apportionment. It also addresses the estimation of future income and costs for decision-making, the impact of changing activity levels on unit costs, and factors affecting short-term and long-term decision-making processes. The report concludes with a detailed cost sheet, and relevant calculations, providing insights into the financial performance and cost management strategies of the company.

COSTS AND REVENUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1........................................................................................................................................................1

1.1 Purpose of internal reporting and providing accurate information to management..............1

1.2 Relationship between various costing system.......................................................................1

1.3 Identifying responsibility centre, cost centre, profit centre and investment centre within

the organisation...........................................................................................................................2

1.4 Characteristics of various types of cost classification and their use in costing.....................2

1.5 Difference between marginal and absorption costing...........................................................3

2........................................................................................................................................................4

2.1 Recording Cost information of the organisation...................................................................4

2.2 Analysing cost information of the organisation....................................................................5

2.3 Define the various stages of inventory..................................................................................6

2.4 Value inventory using various method.................................................................................6

2.5 Behaviour of these costs........................................................................................................8

2.6 Recording cost information using these costing system.......................................................9

3........................................................................................................................................................9

3.1 Overhead costs to production and services cost centres.......................................................9

3.2 Calculation of overhead absorption rate...............................................................................9

3.3 Adjustment for under and over recovered overhead costs..................................................10

3.4 Methods of allocation, apportionment and absorption........................................................10

3.5 Communicate with relevant staff to resolve queries related to overhead cost data............11

4......................................................................................................................................................11

4.1 Compare budget cost with actual coast ..............................................................................11

4.2 Analyse variances for report...............................................................................................12

4.3 information for budget holder of significance variance .....................................................12

4.4 Management report.............................................................................................................12

5......................................................................................................................................................13

5.1 An estimation of future income and costs for decision making process.............................13

5.2 Effect of changing activities levels on unit cost .................................................................14

INTRODUCTION...........................................................................................................................1

1........................................................................................................................................................1

1.1 Purpose of internal reporting and providing accurate information to management..............1

1.2 Relationship between various costing system.......................................................................1

1.3 Identifying responsibility centre, cost centre, profit centre and investment centre within

the organisation...........................................................................................................................2

1.4 Characteristics of various types of cost classification and their use in costing.....................2

1.5 Difference between marginal and absorption costing...........................................................3

2........................................................................................................................................................4

2.1 Recording Cost information of the organisation...................................................................4

2.2 Analysing cost information of the organisation....................................................................5

2.3 Define the various stages of inventory..................................................................................6

2.4 Value inventory using various method.................................................................................6

2.5 Behaviour of these costs........................................................................................................8

2.6 Recording cost information using these costing system.......................................................9

3........................................................................................................................................................9

3.1 Overhead costs to production and services cost centres.......................................................9

3.2 Calculation of overhead absorption rate...............................................................................9

3.3 Adjustment for under and over recovered overhead costs..................................................10

3.4 Methods of allocation, apportionment and absorption........................................................10

3.5 Communicate with relevant staff to resolve queries related to overhead cost data............11

4......................................................................................................................................................11

4.1 Compare budget cost with actual coast ..............................................................................11

4.2 Analyse variances for report...............................................................................................12

4.3 information for budget holder of significance variance .....................................................12

4.4 Management report.............................................................................................................12

5......................................................................................................................................................13

5.1 An estimation of future income and costs for decision making process.............................13

5.2 Effect of changing activities levels on unit cost .................................................................14

5.3 Effect of changing activity levels on unit cost....................................................................14

5.4 factor affecting short term and long term decision making ...............................................14

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................16

5.4 factor affecting short term and long term decision making ...............................................14

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Cost and revenue are the major part of any organisation where cost refer to actual amount

on which the good is sale by the organisation and revenue refer to the actual income that has in

the business activity and unit. Purpose of this study is based on J.P. Morgon which is one of the

leading organisation in UK and it is aim to understand the nature of costs and revenues. The

study will record and analyse cost information as well as it will utilise the information collect

from costing system.

1

1.1 Purpose of internal reporting and providing accurate information to management

Internal reporting include the compilation of operational and financial information, that is

distributed to individuals within an organisation to improve their performance ((Arzbächer

Holtgrewe and Kerst, 2017)). The purpose of internal reporting of financial and operational

information is:

Internal reporting give the holistic view of enterprise performance and on which post the

potential new employees are needed that help management to hire accordingly and

manage the employees.

The purpose of internal reporting is to manage data that can be financial or operational

that help management to utilise the financial resources effectively as well as non-

financial resources that improve the work performance of the organisation.

1.2 Relationship between various costing system

J.P. Morgon Co. design costing system to monitor the cost and the system control and

report to management about costs, profitability and revenues. There are various costing system:

Marginal costing- The marginal costing implies the additional cost that involved in

producing an extra unit of output. Marginal cost = Direct labour+ Direct material+Variable

overhead+ Direct expenses.

Standard Costing- Standard costing is a costing method that implemented by J.P.

Morgon Co. to compare standard revenues and standard costs with actual result, this system

include cost layering system such as; FIFO and LIFO method.

Absorption costing- This costing method absorb all the manufacturing cost including

fixed and variable cost.

1

Cost and revenue are the major part of any organisation where cost refer to actual amount

on which the good is sale by the organisation and revenue refer to the actual income that has in

the business activity and unit. Purpose of this study is based on J.P. Morgon which is one of the

leading organisation in UK and it is aim to understand the nature of costs and revenues. The

study will record and analyse cost information as well as it will utilise the information collect

from costing system.

1

1.1 Purpose of internal reporting and providing accurate information to management

Internal reporting include the compilation of operational and financial information, that is

distributed to individuals within an organisation to improve their performance ((Arzbächer

Holtgrewe and Kerst, 2017)). The purpose of internal reporting of financial and operational

information is:

Internal reporting give the holistic view of enterprise performance and on which post the

potential new employees are needed that help management to hire accordingly and

manage the employees.

The purpose of internal reporting is to manage data that can be financial or operational

that help management to utilise the financial resources effectively as well as non-

financial resources that improve the work performance of the organisation.

1.2 Relationship between various costing system

J.P. Morgon Co. design costing system to monitor the cost and the system control and

report to management about costs, profitability and revenues. There are various costing system:

Marginal costing- The marginal costing implies the additional cost that involved in

producing an extra unit of output. Marginal cost = Direct labour+ Direct material+Variable

overhead+ Direct expenses.

Standard Costing- Standard costing is a costing method that implemented by J.P.

Morgon Co. to compare standard revenues and standard costs with actual result, this system

include cost layering system such as; FIFO and LIFO method.

Absorption costing- This costing method absorb all the manufacturing cost including

fixed and variable cost.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Historical costing- In this system the cost are determined in actual cost and not

predetermined standard cost (Bayer, 2018).

Relation between these costing system

In perfect competition market AR = MR.

In imperfect competition market AR> MR.

1.3 Identifying responsibility centre, cost centre, profit centre and investment centre within the

organisation

Responsibility centre- This centre is headed by a manager in the J.P. Morgon Co. that is

responsible for all its activities and performance. All the information about cost and revenue are

gathered and reported in responsibility accounting by responsibility centre. There are three types

of responsibility centre; Cost, Profit and Investment centre.

Cost Centre- The cost centre is a department in J.P. Morgon Co. that is responsible for

allocating cost and contributes profitability of industry indirectly. It includes two type of

cost centre; production cost centre and Service cost centre. The department include in this

centre are; marketing department, HR, R&D department, etc.

Profit Centre- Profit centre is responsible for both cost and revenue. Aim of profit centre

is to earn profit and mangers of profit centre aim at marketing and production of the

product both (Dudin and et.al., 2015). It includes production and sales/marketing

department.

Investment Centre- This centre is responsible for profit and investment both. Manager

of investment centre formulates the credit policies that drive debt collection and has

control over expenditures, revenues and invested amount in the centre's assets.

Investment centre of the J.P. Morgon Co. have more responsibility and authority than

cost or profit centre.

1.4 Characteristics of various types of cost classification and their use in costing

Cost can be classified as follows and each type of cost have different characteristics and

their use in costing are different:

Classification on the basis of management function

Manufacturing Cost

This cost incurred in the organisation to convert raw material into finished goods. It

includes raw material cost, direct labour cost and factory cost. Manufacturing cost can be either

2

predetermined standard cost (Bayer, 2018).

Relation between these costing system

In perfect competition market AR = MR.

In imperfect competition market AR> MR.

1.3 Identifying responsibility centre, cost centre, profit centre and investment centre within the

organisation

Responsibility centre- This centre is headed by a manager in the J.P. Morgon Co. that is

responsible for all its activities and performance. All the information about cost and revenue are

gathered and reported in responsibility accounting by responsibility centre. There are three types

of responsibility centre; Cost, Profit and Investment centre.

Cost Centre- The cost centre is a department in J.P. Morgon Co. that is responsible for

allocating cost and contributes profitability of industry indirectly. It includes two type of

cost centre; production cost centre and Service cost centre. The department include in this

centre are; marketing department, HR, R&D department, etc.

Profit Centre- Profit centre is responsible for both cost and revenue. Aim of profit centre

is to earn profit and mangers of profit centre aim at marketing and production of the

product both (Dudin and et.al., 2015). It includes production and sales/marketing

department.

Investment Centre- This centre is responsible for profit and investment both. Manager

of investment centre formulates the credit policies that drive debt collection and has

control over expenditures, revenues and invested amount in the centre's assets.

Investment centre of the J.P. Morgon Co. have more responsibility and authority than

cost or profit centre.

1.4 Characteristics of various types of cost classification and their use in costing

Cost can be classified as follows and each type of cost have different characteristics and

their use in costing are different:

Classification on the basis of management function

Manufacturing Cost

This cost incurred in the organisation to convert raw material into finished goods. It

includes raw material cost, direct labour cost and factory cost. Manufacturing cost can be either

2

fixed or variable (Gallemore and Labro, 2015). In costing, this cost include depreciation, indirect

material and labour cost.

Non-Manufacturing Cost

Non-manufacturing cost are not calculated into cost of good sold. This cost include in

costing to analysing selling expenses, administrative expenses that incurred after the final

production.

Classification of cost by behaviour

Variable Cost

Variable cost varies as a result of change in production level, the variability of total

amount in direct portion to volume. Variable cost use in costing as by dividing sale per unit and

add up direct material and direct labour to it.

Fixed Cost

Fixed cost are those cost that remain same and constant and do not change at any level of

activity and output. They have control in many cases within the organisation with executive

management rather than operating supervisor.

Semi-Variable Cost

This type of cost has characteristics of both fixed and variable cost.

Classification of cost by nature

Direct Cost

This type of cost are direct accountable to particular object of costing such as; department

or product (Netten and Beecham, eds., 2018). It can be easily traced and computed and it is used

in costing to evaluate all the cost that are direct attached to the organisation such as; direct

labour, direct material, etc.

Indirect Cost

This type of cost are those that are not directly accountable to a cost object; it can be

either fixed or variable. It cannot be traced and identified easily. Indirect cost use in costing as

calculating office and administrative expenses, etc.

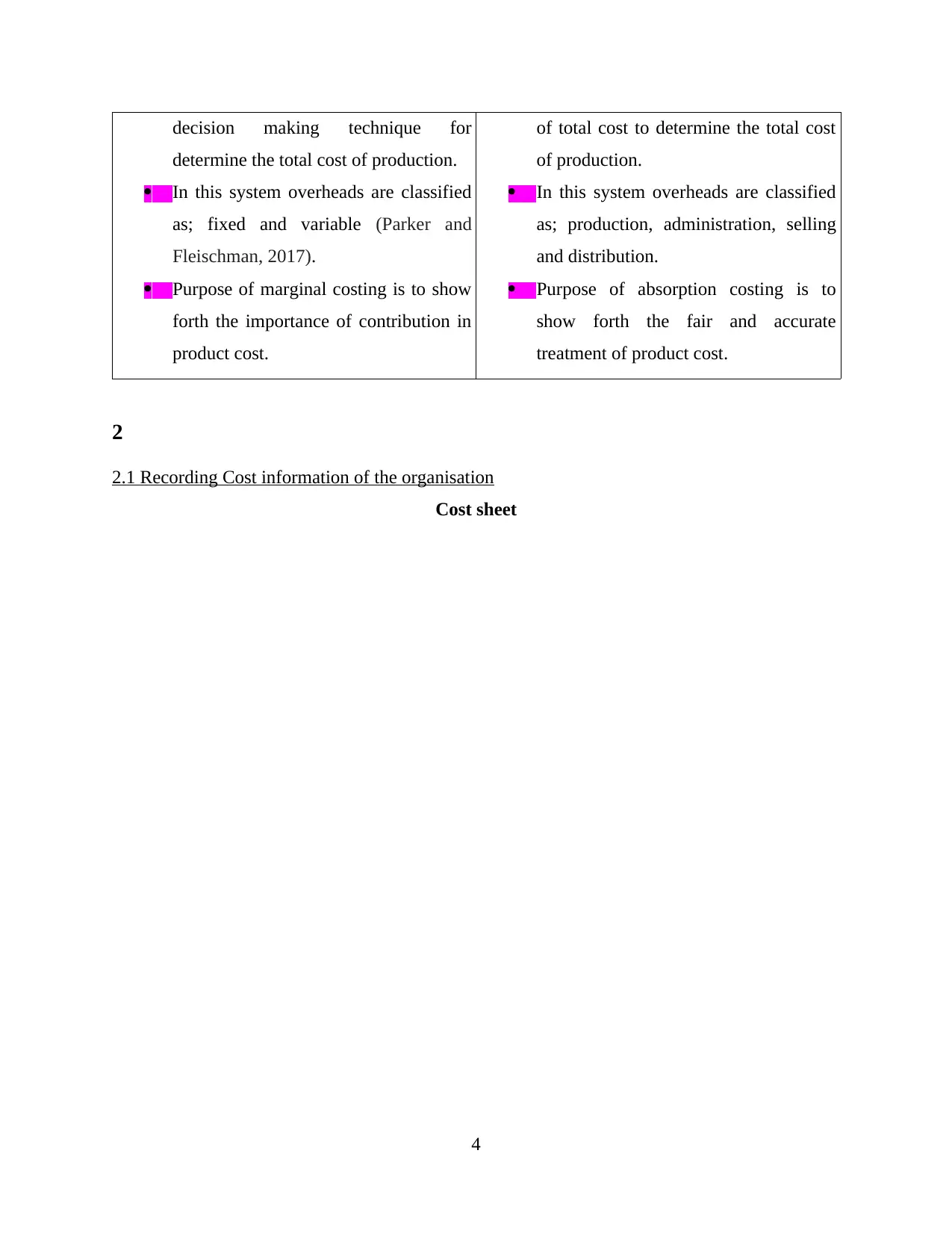

1.5 Difference between marginal and absorption costing

Marginal costing Absorption costing

Marginal costing is defined as a Absorption costing defined as allotment

3

material and labour cost.

Non-Manufacturing Cost

Non-manufacturing cost are not calculated into cost of good sold. This cost include in

costing to analysing selling expenses, administrative expenses that incurred after the final

production.

Classification of cost by behaviour

Variable Cost

Variable cost varies as a result of change in production level, the variability of total

amount in direct portion to volume. Variable cost use in costing as by dividing sale per unit and

add up direct material and direct labour to it.

Fixed Cost

Fixed cost are those cost that remain same and constant and do not change at any level of

activity and output. They have control in many cases within the organisation with executive

management rather than operating supervisor.

Semi-Variable Cost

This type of cost has characteristics of both fixed and variable cost.

Classification of cost by nature

Direct Cost

This type of cost are direct accountable to particular object of costing such as; department

or product (Netten and Beecham, eds., 2018). It can be easily traced and computed and it is used

in costing to evaluate all the cost that are direct attached to the organisation such as; direct

labour, direct material, etc.

Indirect Cost

This type of cost are those that are not directly accountable to a cost object; it can be

either fixed or variable. It cannot be traced and identified easily. Indirect cost use in costing as

calculating office and administrative expenses, etc.

1.5 Difference between marginal and absorption costing

Marginal costing Absorption costing

Marginal costing is defined as a Absorption costing defined as allotment

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision making technique for

determine the total cost of production.

In this system overheads are classified

as; fixed and variable (Parker and

Fleischman, 2017).

Purpose of marginal costing is to show

forth the importance of contribution in

product cost.

of total cost to determine the total cost

of production.

In this system overheads are classified

as; production, administration, selling

and distribution.

Purpose of absorption costing is to

show forth the fair and accurate

treatment of product cost.

2

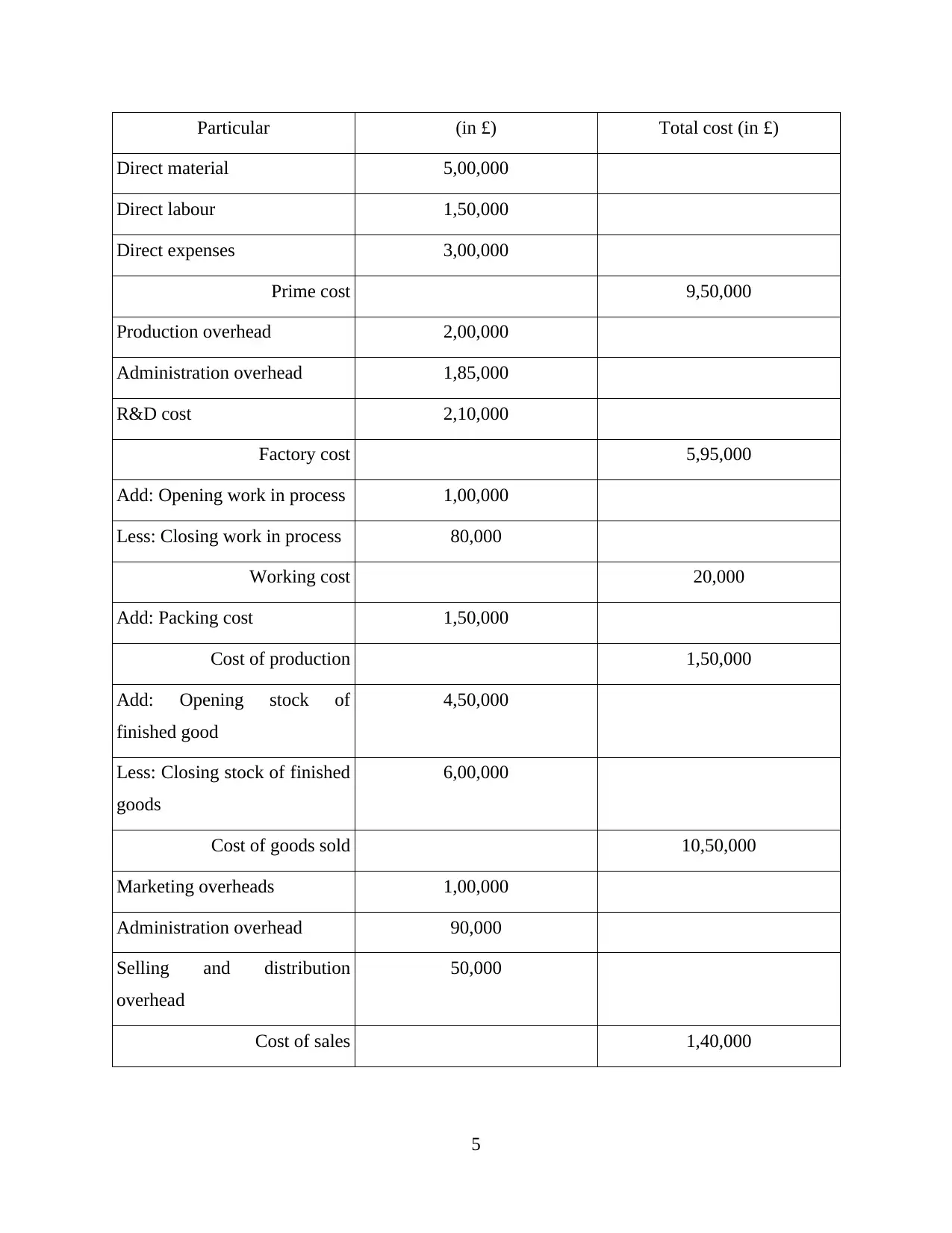

2.1 Recording Cost information of the organisation

Cost sheet

4

determine the total cost of production.

In this system overheads are classified

as; fixed and variable (Parker and

Fleischman, 2017).

Purpose of marginal costing is to show

forth the importance of contribution in

product cost.

of total cost to determine the total cost

of production.

In this system overheads are classified

as; production, administration, selling

and distribution.

Purpose of absorption costing is to

show forth the fair and accurate

treatment of product cost.

2

2.1 Recording Cost information of the organisation

Cost sheet

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particular (in £) Total cost (in £)

Direct material 5,00,000

Direct labour 1,50,000

Direct expenses 3,00,000

Prime cost 9,50,000

Production overhead 2,00,000

Administration overhead 1,85,000

R&D cost 2,10,000

Factory cost 5,95,000

Add: Opening work in process 1,00,000

Less: Closing work in process 80,000

Working cost 20,000

Add: Packing cost 1,50,000

Cost of production 1,50,000

Add: Opening stock of

finished good

4,50,000

Less: Closing stock of finished

goods

6,00,000

Cost of goods sold 10,50,000

Marketing overheads 1,00,000

Administration overhead 90,000

Selling and distribution

overhead

50,000

Cost of sales 1,40,000

5

Direct material 5,00,000

Direct labour 1,50,000

Direct expenses 3,00,000

Prime cost 9,50,000

Production overhead 2,00,000

Administration overhead 1,85,000

R&D cost 2,10,000

Factory cost 5,95,000

Add: Opening work in process 1,00,000

Less: Closing work in process 80,000

Working cost 20,000

Add: Packing cost 1,50,000

Cost of production 1,50,000

Add: Opening stock of

finished good

4,50,000

Less: Closing stock of finished

goods

6,00,000

Cost of goods sold 10,50,000

Marketing overheads 1,00,000

Administration overhead 90,000

Selling and distribution

overhead

50,000

Cost of sales 1,40,000

5

2.2 Analysing cost information of the organisation

From the above cost sheet it has been analysed that there are various cost such as; direct

and indirect that adding up in the total cost of the organisation and decreasing the total margin

(Rahim, 2017). Prime cost is the total amount of direct labour, direct material and direct

expenses. Production cost include administration, R&D cost, etc. in the cost sheet, all the

products are not made for sale that state that they are not known as goods for sold.

2.3 Define the various stages of inventory

There are various stage of inventory; raw material, finished goods, work-in-progress and

cost of goods sold.

Raw material- This is the first stage of inventory. Raw material defined as a crude or

processed material that can be transform by manufacture, processing or combination into new

and useful product. Basically these are the material that will make final good at the last stage of

production.

Work-in-progress- After raw material are pulled into the process of developing a final

product they basically enter in second stage that is work-in-progress. It is a portion of inventory

that represent that products tat are no longer saleable as a raw material and not yet saleable as

finished product. WIP also called as semi-finished good.

Finished goods- This stage of inventory are the final stage that goods completed the

manufacturing process and convert into final product but still not has been sold to customers

(Reynard and et.al., 2016).

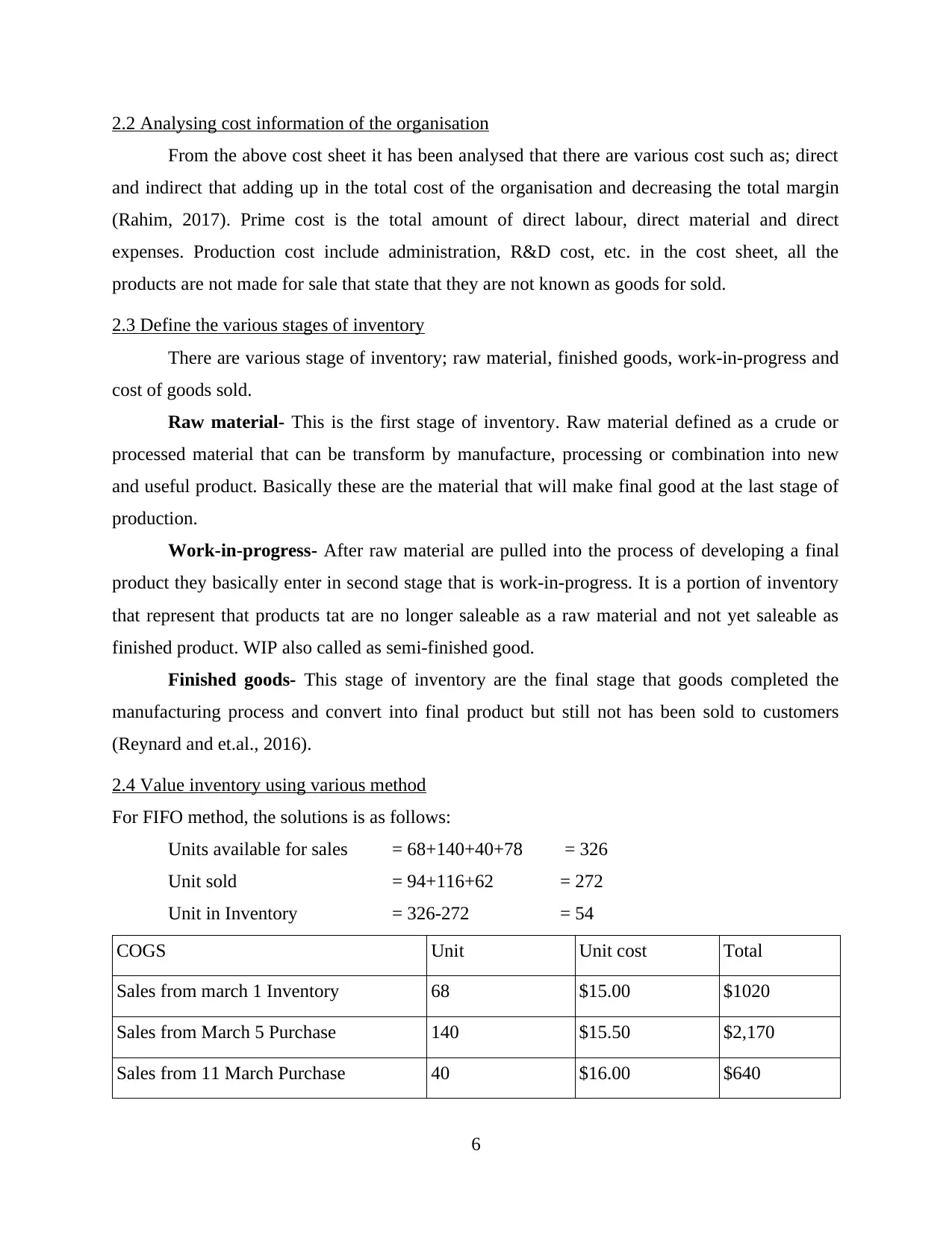

2.4 Value inventory using various method

For FIFO method, the solutions is as follows:

Units available for sales = 68+140+40+78 = 326

Unit sold = 94+116+62 = 272

Unit in Inventory = 326-272 = 54

COGS Unit Unit cost Total

Sales from march 1 Inventory 68 $15.00 $1020

Sales from March 5 Purchase 140 $15.50 $2,170

Sales from 11 March Purchase 40 $16.00 $640

6

From the above cost sheet it has been analysed that there are various cost such as; direct

and indirect that adding up in the total cost of the organisation and decreasing the total margin

(Rahim, 2017). Prime cost is the total amount of direct labour, direct material and direct

expenses. Production cost include administration, R&D cost, etc. in the cost sheet, all the

products are not made for sale that state that they are not known as goods for sold.

2.3 Define the various stages of inventory

There are various stage of inventory; raw material, finished goods, work-in-progress and

cost of goods sold.

Raw material- This is the first stage of inventory. Raw material defined as a crude or

processed material that can be transform by manufacture, processing or combination into new

and useful product. Basically these are the material that will make final good at the last stage of

production.

Work-in-progress- After raw material are pulled into the process of developing a final

product they basically enter in second stage that is work-in-progress. It is a portion of inventory

that represent that products tat are no longer saleable as a raw material and not yet saleable as

finished product. WIP also called as semi-finished good.

Finished goods- This stage of inventory are the final stage that goods completed the

manufacturing process and convert into final product but still not has been sold to customers

(Reynard and et.al., 2016).

2.4 Value inventory using various method

For FIFO method, the solutions is as follows:

Units available for sales = 68+140+40+78 = 326

Unit sold = 94+116+62 = 272

Unit in Inventory = 326-272 = 54

COGS Unit Unit cost Total

Sales from march 1 Inventory 68 $15.00 $1020

Sales from March 5 Purchase 140 $15.50 $2,170

Sales from 11 March Purchase 40 $16.00 $640

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

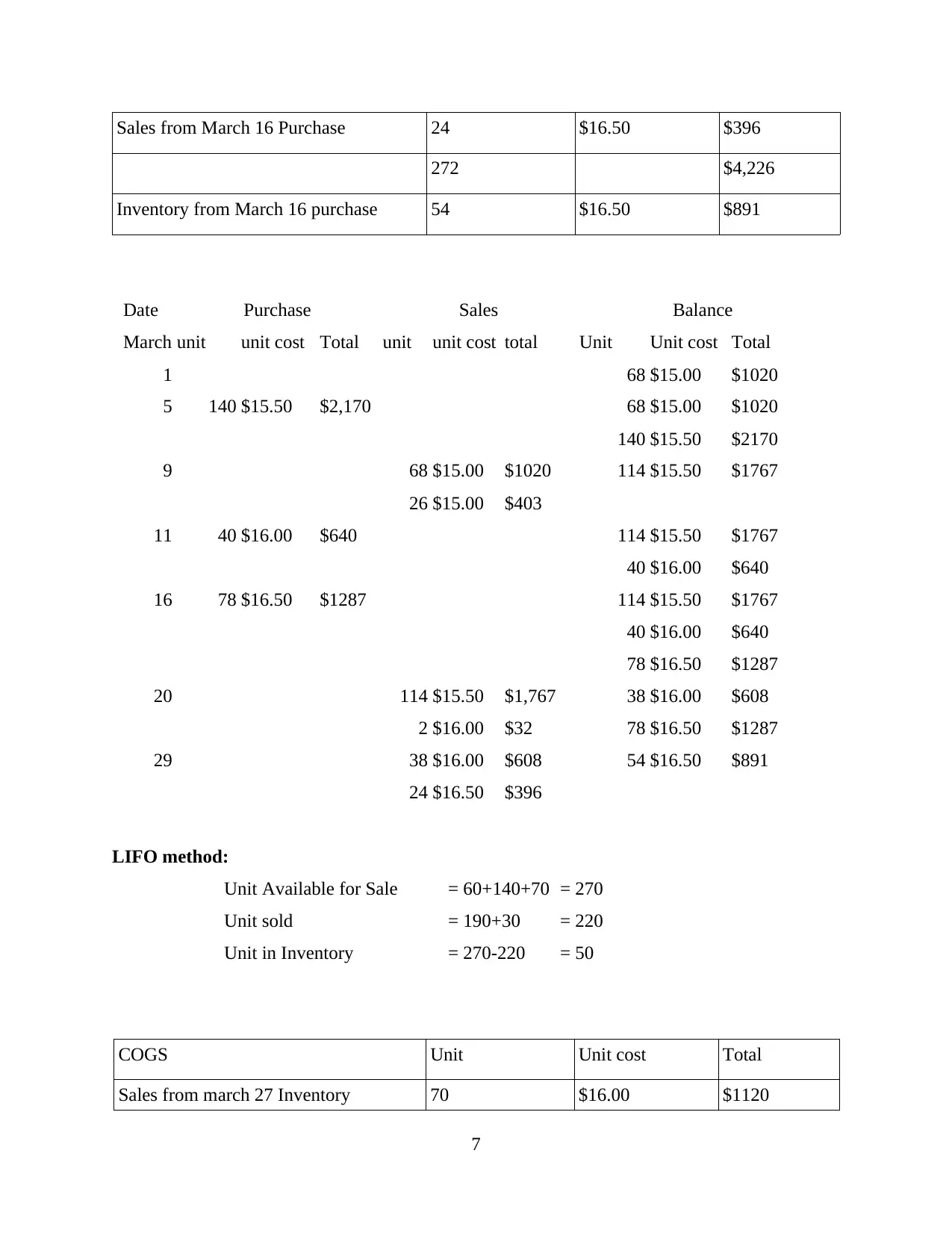

Sales from March 16 Purchase 24 $16.50 $396

272 $4,226

Inventory from March 16 purchase 54 $16.50 $891

Date Purchase Sales Balance

March unit unit cost Total unit unit cost total Unit Unit cost Total

1 68 $15.00 $1020

5 140 $15.50 $2,170 68 $15.00 $1020

140 $15.50 $2170

9 68 $15.00 $1020 114 $15.50 $1767

26 $15.00 $403

11 40 $16.00 $640 114 $15.50 $1767

40 $16.00 $640

16 78 $16.50 $1287 114 $15.50 $1767

40 $16.00 $640

78 $16.50 $1287

20 114 $15.50 $1,767 38 $16.00 $608

2 $16.00 $32 78 $16.50 $1287

29 38 $16.00 $608 54 $16.50 $891

24 $16.50 $396

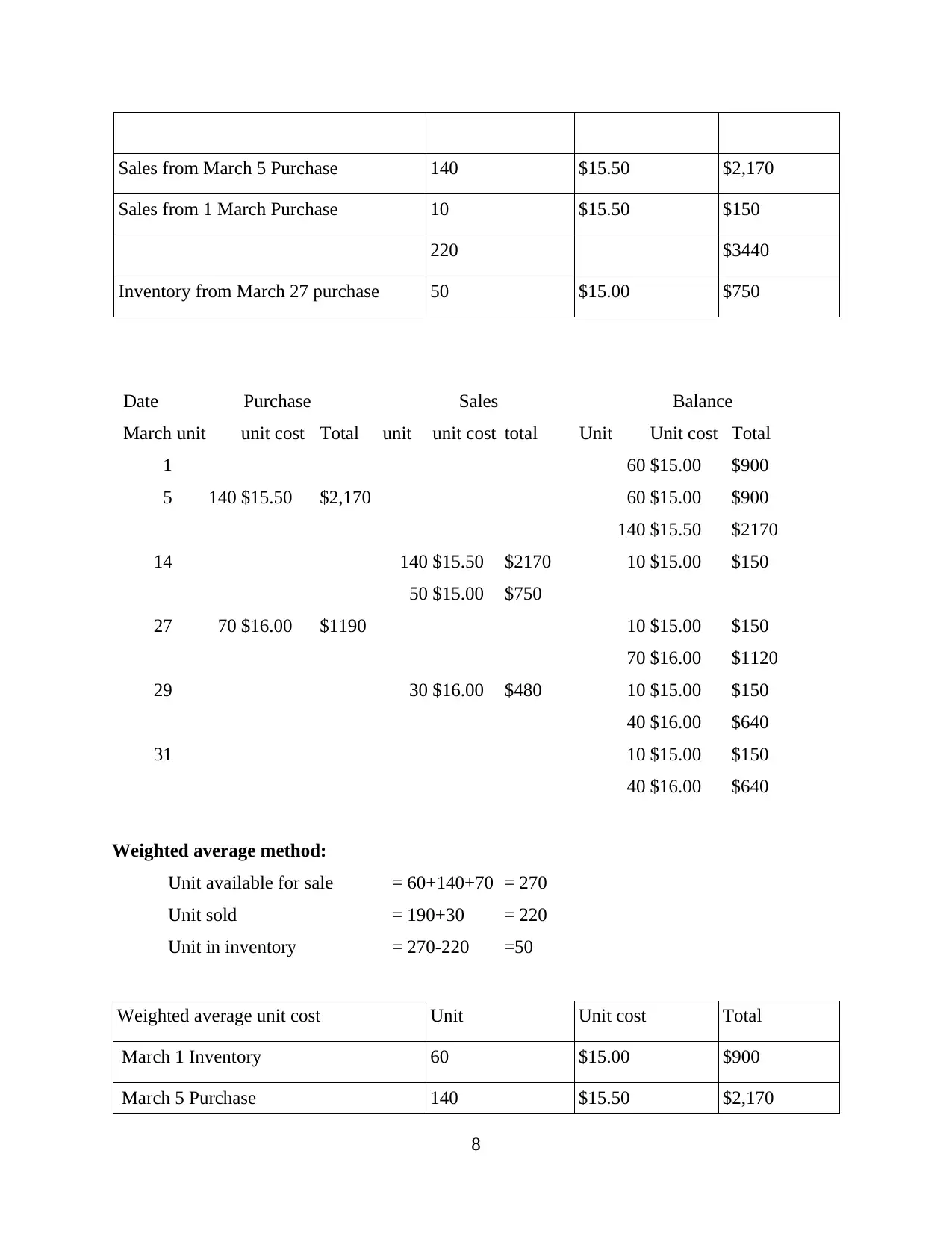

LIFO method:

Unit Available for Sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in Inventory = 270-220 = 50

COGS Unit Unit cost Total

Sales from march 27 Inventory 70 $16.00 $1120

7

272 $4,226

Inventory from March 16 purchase 54 $16.50 $891

Date Purchase Sales Balance

March unit unit cost Total unit unit cost total Unit Unit cost Total

1 68 $15.00 $1020

5 140 $15.50 $2,170 68 $15.00 $1020

140 $15.50 $2170

9 68 $15.00 $1020 114 $15.50 $1767

26 $15.00 $403

11 40 $16.00 $640 114 $15.50 $1767

40 $16.00 $640

16 78 $16.50 $1287 114 $15.50 $1767

40 $16.00 $640

78 $16.50 $1287

20 114 $15.50 $1,767 38 $16.00 $608

2 $16.00 $32 78 $16.50 $1287

29 38 $16.00 $608 54 $16.50 $891

24 $16.50 $396

LIFO method:

Unit Available for Sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in Inventory = 270-220 = 50

COGS Unit Unit cost Total

Sales from march 27 Inventory 70 $16.00 $1120

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales from March 5 Purchase 140 $15.50 $2,170

Sales from 1 March Purchase 10 $15.50 $150

220 $3440

Inventory from March 27 purchase 50 $15.00 $750

Date Purchase Sales Balance

March unit unit cost Total unit unit cost total Unit Unit cost Total

1 60 $15.00 $900

5 140 $15.50 $2,170 60 $15.00 $900

140 $15.50 $2170

14 140 $15.50 $2170 10 $15.00 $150

50 $15.00 $750

27 70 $16.00 $1190 10 $15.00 $150

70 $16.00 $1120

29 30 $16.00 $480 10 $15.00 $150

40 $16.00 $640

31 10 $15.00 $150

40 $16.00 $640

Weighted average method:

Unit available for sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in inventory = 270-220 =50

Weighted average unit cost Unit Unit cost Total

March 1 Inventory 60 $15.00 $900

March 5 Purchase 140 $15.50 $2,170

8

Sales from 1 March Purchase 10 $15.50 $150

220 $3440

Inventory from March 27 purchase 50 $15.00 $750

Date Purchase Sales Balance

March unit unit cost Total unit unit cost total Unit Unit cost Total

1 60 $15.00 $900

5 140 $15.50 $2,170 60 $15.00 $900

140 $15.50 $2170

14 140 $15.50 $2170 10 $15.00 $150

50 $15.00 $750

27 70 $16.00 $1190 10 $15.00 $150

70 $16.00 $1120

29 30 $16.00 $480 10 $15.00 $150

40 $16.00 $640

31 10 $15.00 $150

40 $16.00 $640

Weighted average method:

Unit available for sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in inventory = 270-220 =50

Weighted average unit cost Unit Unit cost Total

March 1 Inventory 60 $15.00 $900

March 5 Purchase 140 $15.50 $2,170

8

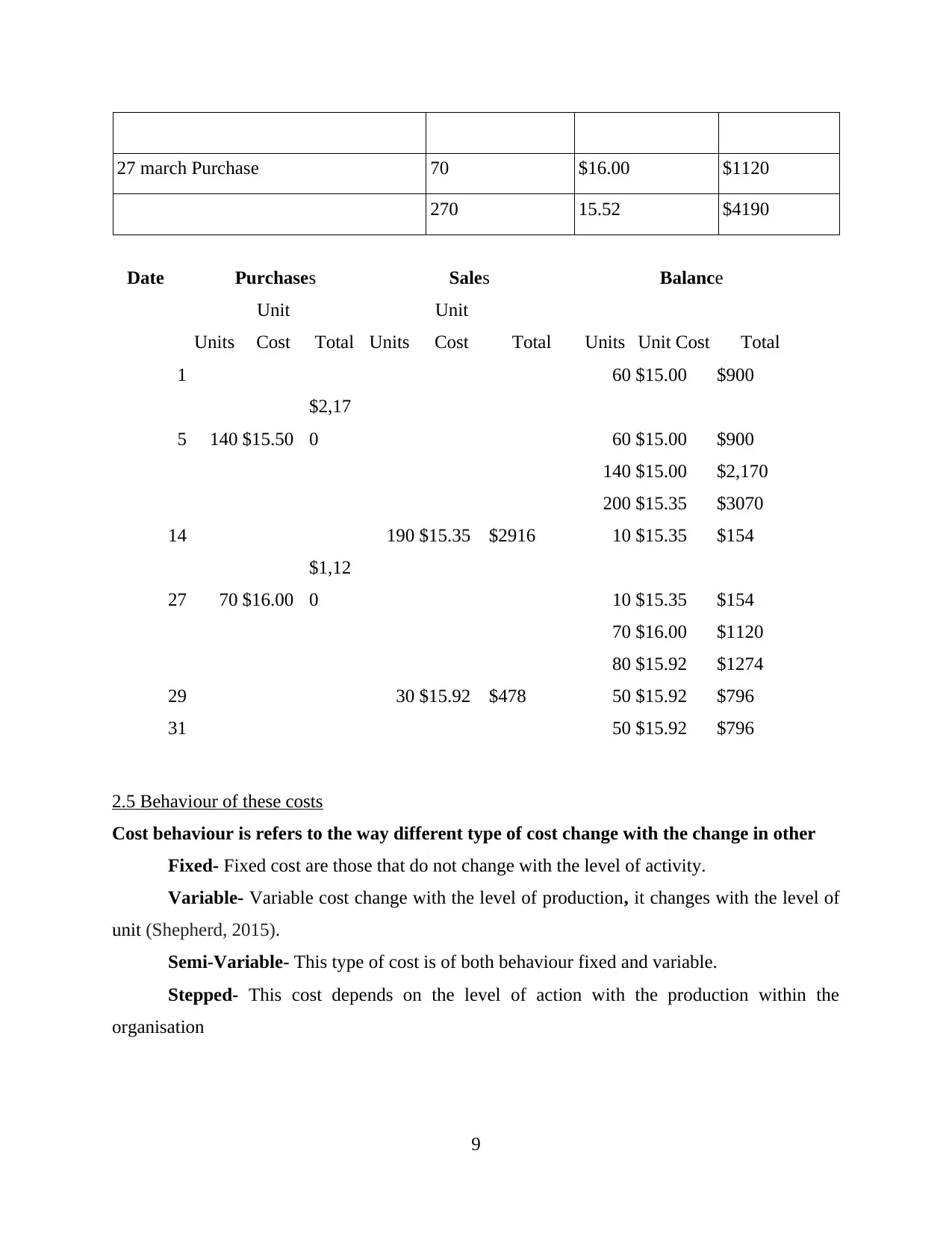

27 march Purchase 70 $16.00 $1120

270 15.52 $4190

Date Purchases Sales Balance

Units

Unit

Cost Total Units

Unit

Cost Total Units Unit Cost Total

1 60 $15.00 $900

5 140 $15.50

$2,17

0 60 $15.00 $900

140 $15.00 $2,170

200 $15.35 $3070

14 190 $15.35 $2916 10 $15.35 $154

27 70 $16.00

$1,12

0 10 $15.35 $154

70 $16.00 $1120

80 $15.92 $1274

29 30 $15.92 $478 50 $15.92 $796

31 50 $15.92 $796

2.5 Behaviour of these costs

Cost behaviour is refers to the way different type of cost change with the change in other

Fixed- Fixed cost are those that do not change with the level of activity.

Variable- Variable cost change with the level of production, it changes with the level of

unit (Shepherd, 2015).

Semi-Variable- This type of cost is of both behaviour fixed and variable.

Stepped- This cost depends on the level of action with the production within the

organisation

9

270 15.52 $4190

Date Purchases Sales Balance

Units

Unit

Cost Total Units

Unit

Cost Total Units Unit Cost Total

1 60 $15.00 $900

5 140 $15.50

$2,17

0 60 $15.00 $900

140 $15.00 $2,170

200 $15.35 $3070

14 190 $15.35 $2916 10 $15.35 $154

27 70 $16.00

$1,12

0 10 $15.35 $154

70 $16.00 $1120

80 $15.92 $1274

29 30 $15.92 $478 50 $15.92 $796

31 50 $15.92 $796

2.5 Behaviour of these costs

Cost behaviour is refers to the way different type of cost change with the change in other

Fixed- Fixed cost are those that do not change with the level of activity.

Variable- Variable cost change with the level of production, it changes with the level of

unit (Shepherd, 2015).

Semi-Variable- This type of cost is of both behaviour fixed and variable.

Stepped- This cost depends on the level of action with the production within the

organisation

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.