Cost Accounting Report: Analysis of Costs and Revenues for M&S

VerifiedAdded on 2020/10/22

|20

|3755

|313

Report

AI Summary

This report provides a detailed analysis of costs and revenues, focusing on Marks and Spencer. It covers internal reporting, costing systems (historical, direct, absorption, and marginal), and cost classifications (fixed, variable, semi-variable). The report presents a cost sheet and analyzes cost information, including raw materials, direct labor, and overheads. It discusses inventory valuation methods (FIFO, batch, unit, process, and service costing) and cost behaviors. Furthermore, the report addresses overhead allocation and apportionment, calculating overhead absorption rates, and calculating over and under absorption of labor and wages. It also compares budgeted and actual costs, analyzes variances, and prepares a management report. Finally, the report examines the effects of changes in activity levels on unit costs and identifies factors affecting short and long-term decision-making.

Costs and Revenues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 The purpose of internal reporting and provision of precise information..............................1

1.2 Relationship between a number of costing systems within Marks and Spencer...................1

1.3 Identification of Cost, responsibility, profit, and investment centres...................................1

1.4 Cost classifications and their uses.........................................................................................2

1.5 The differences between absorption and marginal costing...................................................2

TASK 2............................................................................................................................................3

2.1 Presenting cost sheet.............................................................................................................3

2.2 Analysing cost information...................................................................................................3

2.3 Various stages of inventory...................................................................................................4

2.4 Valuation of inventory using various methods....................................................................4

2.5 Behaviours of costs...............................................................................................................6

2.6 Cost information and the costing systems............................................................................6

TASK 3............................................................................................................................................8

3.1 Allocation and apportionment of overhead cost .................................................................8

3.2 Calculating overhead absorption rates for ABC Ltd:............................................................9

3.3 Calculation of over and under absorption of labour and wages..........................................10

3.4 Methods of allocation, appropriation and absorption.........................................................11

3.5 Solving overhead data queries............................................................................................11

TASK 4..........................................................................................................................................12

4.1 Comparison of budgeted and actual cost .........................................................................12

4.2 Analysis of variance...........................................................................................................12

4.3 Information of significant variance.....................................................................................12

4.4 Preparation of management report......................................................................................12

TASK 5 .........................................................................................................................................14

5.1 Estimates of future incomes and cost for decision making.................................................14

5.2 Effect of change in activity level on unit cost.....................................................................14

5.3 Calculation of Effect of change in activity level on unit cost.............................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 The purpose of internal reporting and provision of precise information..............................1

1.2 Relationship between a number of costing systems within Marks and Spencer...................1

1.3 Identification of Cost, responsibility, profit, and investment centres...................................1

1.4 Cost classifications and their uses.........................................................................................2

1.5 The differences between absorption and marginal costing...................................................2

TASK 2............................................................................................................................................3

2.1 Presenting cost sheet.............................................................................................................3

2.2 Analysing cost information...................................................................................................3

2.3 Various stages of inventory...................................................................................................4

2.4 Valuation of inventory using various methods....................................................................4

2.5 Behaviours of costs...............................................................................................................6

2.6 Cost information and the costing systems............................................................................6

TASK 3............................................................................................................................................8

3.1 Allocation and apportionment of overhead cost .................................................................8

3.2 Calculating overhead absorption rates for ABC Ltd:............................................................9

3.3 Calculation of over and under absorption of labour and wages..........................................10

3.4 Methods of allocation, appropriation and absorption.........................................................11

3.5 Solving overhead data queries............................................................................................11

TASK 4..........................................................................................................................................12

4.1 Comparison of budgeted and actual cost .........................................................................12

4.2 Analysis of variance...........................................................................................................12

4.3 Information of significant variance.....................................................................................12

4.4 Preparation of management report......................................................................................12

TASK 5 .........................................................................................................................................14

5.1 Estimates of future incomes and cost for decision making.................................................14

5.2 Effect of change in activity level on unit cost.....................................................................14

5.3 Calculation of Effect of change in activity level on unit cost.............................................15

5.4 Identification of factors affecting short and long term decision making............................15

REFERENCES..............................................................................................................................16

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

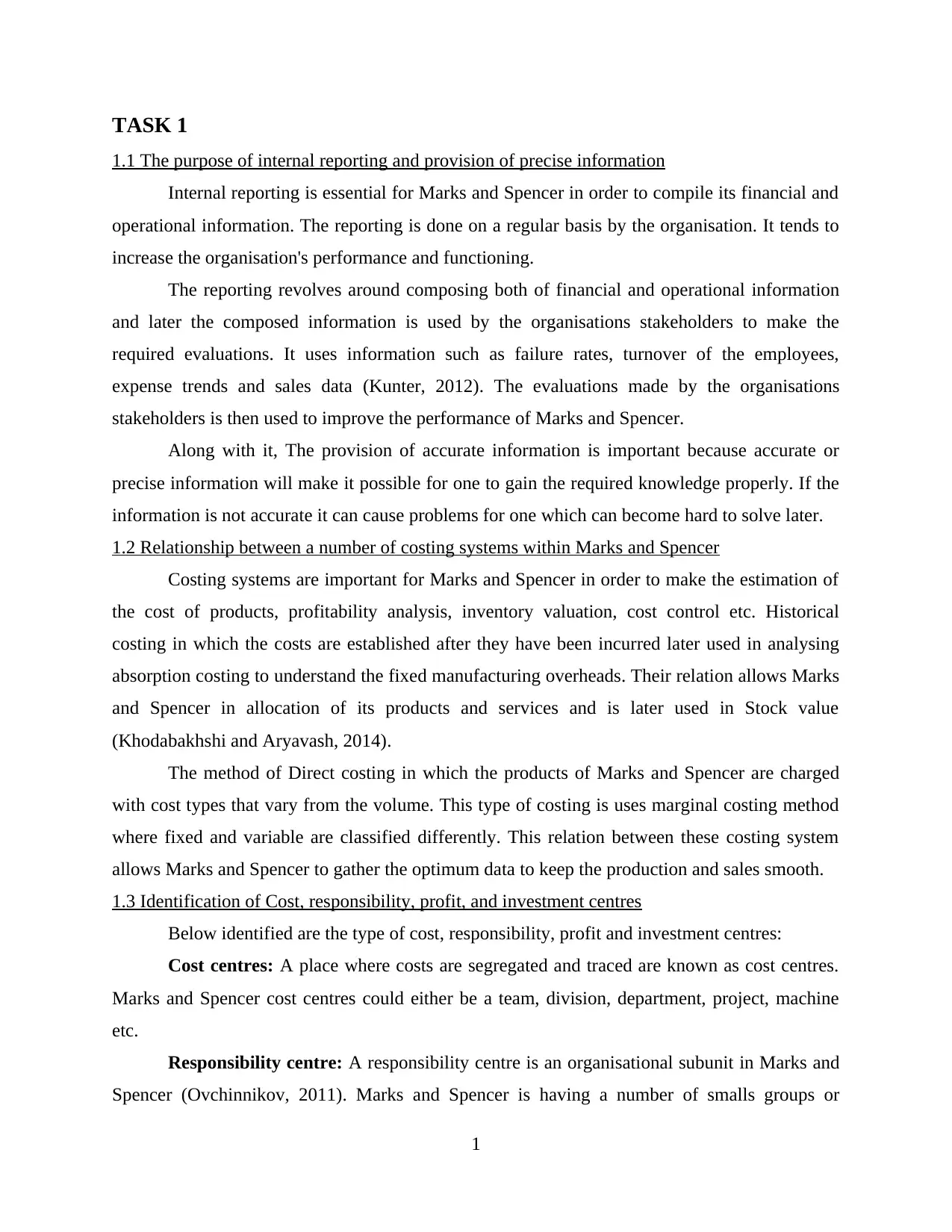

TASK 1

1.1 The purpose of internal reporting and provision of precise information

Internal reporting is essential for Marks and Spencer in order to compile its financial and

operational information. The reporting is done on a regular basis by the organisation. It tends to

increase the organisation's performance and functioning.

The reporting revolves around composing both of financial and operational information

and later the composed information is used by the organisations stakeholders to make the

required evaluations. It uses information such as failure rates, turnover of the employees,

expense trends and sales data (Kunter, 2012). The evaluations made by the organisations

stakeholders is then used to improve the performance of Marks and Spencer.

Along with it, The provision of accurate information is important because accurate or

precise information will make it possible for one to gain the required knowledge properly. If the

information is not accurate it can cause problems for one which can become hard to solve later.

1.2 Relationship between a number of costing systems within Marks and Spencer

Costing systems are important for Marks and Spencer in order to make the estimation of

the cost of products, profitability analysis, inventory valuation, cost control etc. Historical

costing in which the costs are established after they have been incurred later used in analysing

absorption costing to understand the fixed manufacturing overheads. Their relation allows Marks

and Spencer in allocation of its products and services and is later used in Stock value

(Khodabakhshi and Aryavash, 2014).

The method of Direct costing in which the products of Marks and Spencer are charged

with cost types that vary from the volume. This type of costing is uses marginal costing method

where fixed and variable are classified differently. This relation between these costing system

allows Marks and Spencer to gather the optimum data to keep the production and sales smooth.

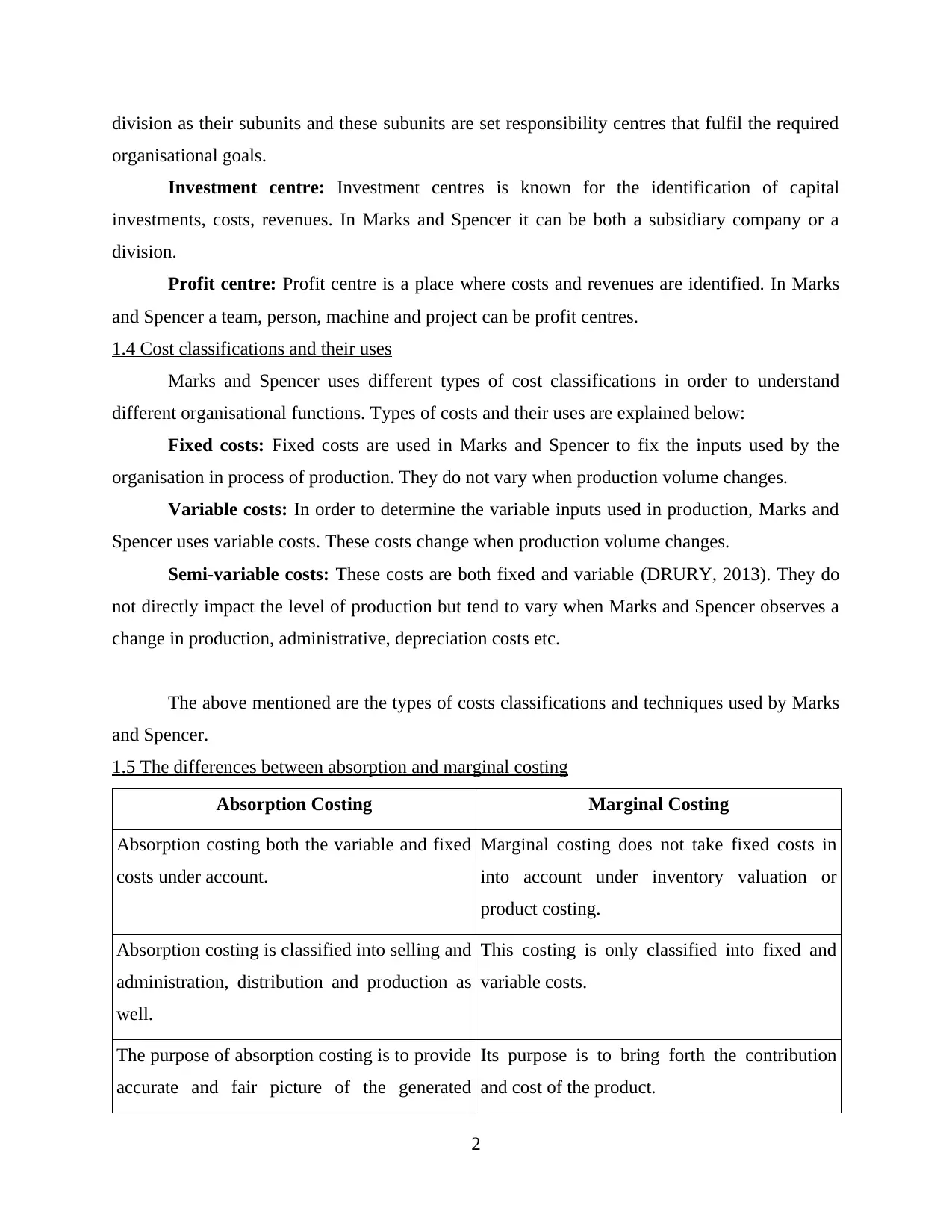

1.3 Identification of Cost, responsibility, profit, and investment centres

Below identified are the type of cost, responsibility, profit and investment centres:

Cost centres: A place where costs are segregated and traced are known as cost centres.

Marks and Spencer cost centres could either be a team, division, department, project, machine

etc.

Responsibility centre: A responsibility centre is an organisational subunit in Marks and

Spencer (Ovchinnikov, 2011). Marks and Spencer is having a number of smalls groups or

1

1.1 The purpose of internal reporting and provision of precise information

Internal reporting is essential for Marks and Spencer in order to compile its financial and

operational information. The reporting is done on a regular basis by the organisation. It tends to

increase the organisation's performance and functioning.

The reporting revolves around composing both of financial and operational information

and later the composed information is used by the organisations stakeholders to make the

required evaluations. It uses information such as failure rates, turnover of the employees,

expense trends and sales data (Kunter, 2012). The evaluations made by the organisations

stakeholders is then used to improve the performance of Marks and Spencer.

Along with it, The provision of accurate information is important because accurate or

precise information will make it possible for one to gain the required knowledge properly. If the

information is not accurate it can cause problems for one which can become hard to solve later.

1.2 Relationship between a number of costing systems within Marks and Spencer

Costing systems are important for Marks and Spencer in order to make the estimation of

the cost of products, profitability analysis, inventory valuation, cost control etc. Historical

costing in which the costs are established after they have been incurred later used in analysing

absorption costing to understand the fixed manufacturing overheads. Their relation allows Marks

and Spencer in allocation of its products and services and is later used in Stock value

(Khodabakhshi and Aryavash, 2014).

The method of Direct costing in which the products of Marks and Spencer are charged

with cost types that vary from the volume. This type of costing is uses marginal costing method

where fixed and variable are classified differently. This relation between these costing system

allows Marks and Spencer to gather the optimum data to keep the production and sales smooth.

1.3 Identification of Cost, responsibility, profit, and investment centres

Below identified are the type of cost, responsibility, profit and investment centres:

Cost centres: A place where costs are segregated and traced are known as cost centres.

Marks and Spencer cost centres could either be a team, division, department, project, machine

etc.

Responsibility centre: A responsibility centre is an organisational subunit in Marks and

Spencer (Ovchinnikov, 2011). Marks and Spencer is having a number of smalls groups or

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

division as their subunits and these subunits are set responsibility centres that fulfil the required

organisational goals.

Investment centre: Investment centres is known for the identification of capital

investments, costs, revenues. In Marks and Spencer it can be both a subsidiary company or a

division.

Profit centre: Profit centre is a place where costs and revenues are identified. In Marks

and Spencer a team, person, machine and project can be profit centres.

1.4 Cost classifications and their uses

Marks and Spencer uses different types of cost classifications in order to understand

different organisational functions. Types of costs and their uses are explained below:

Fixed costs: Fixed costs are used in Marks and Spencer to fix the inputs used by the

organisation in process of production. They do not vary when production volume changes.

Variable costs: In order to determine the variable inputs used in production, Marks and

Spencer uses variable costs. These costs change when production volume changes.

Semi-variable costs: These costs are both fixed and variable (DRURY, 2013). They do

not directly impact the level of production but tend to vary when Marks and Spencer observes a

change in production, administrative, depreciation costs etc.

The above mentioned are the types of costs classifications and techniques used by Marks

and Spencer.

1.5 The differences between absorption and marginal costing

Absorption Costing Marginal Costing

Absorption costing both the variable and fixed

costs under account.

Marginal costing does not take fixed costs in

into account under inventory valuation or

product costing.

Absorption costing is classified into selling and

administration, distribution and production as

well.

This costing is only classified into fixed and

variable costs.

The purpose of absorption costing is to provide

accurate and fair picture of the generated

Its purpose is to bring forth the contribution

and cost of the product.

2

organisational goals.

Investment centre: Investment centres is known for the identification of capital

investments, costs, revenues. In Marks and Spencer it can be both a subsidiary company or a

division.

Profit centre: Profit centre is a place where costs and revenues are identified. In Marks

and Spencer a team, person, machine and project can be profit centres.

1.4 Cost classifications and their uses

Marks and Spencer uses different types of cost classifications in order to understand

different organisational functions. Types of costs and their uses are explained below:

Fixed costs: Fixed costs are used in Marks and Spencer to fix the inputs used by the

organisation in process of production. They do not vary when production volume changes.

Variable costs: In order to determine the variable inputs used in production, Marks and

Spencer uses variable costs. These costs change when production volume changes.

Semi-variable costs: These costs are both fixed and variable (DRURY, 2013). They do

not directly impact the level of production but tend to vary when Marks and Spencer observes a

change in production, administrative, depreciation costs etc.

The above mentioned are the types of costs classifications and techniques used by Marks

and Spencer.

1.5 The differences between absorption and marginal costing

Absorption Costing Marginal Costing

Absorption costing both the variable and fixed

costs under account.

Marginal costing does not take fixed costs in

into account under inventory valuation or

product costing.

Absorption costing is classified into selling and

administration, distribution and production as

well.

This costing is only classified into fixed and

variable costs.

The purpose of absorption costing is to provide

accurate and fair picture of the generated

Its purpose is to bring forth the contribution

and cost of the product.

2

profits.

The method is one of the most conventional

methods of costing and of is used for tax

reporting of financial purposes in Marks and

Spencer (Dahlby and Ferede, 2011).

This method is not really conventional as it is a

costing method that involves a lot of data

analysing.

TASK 2

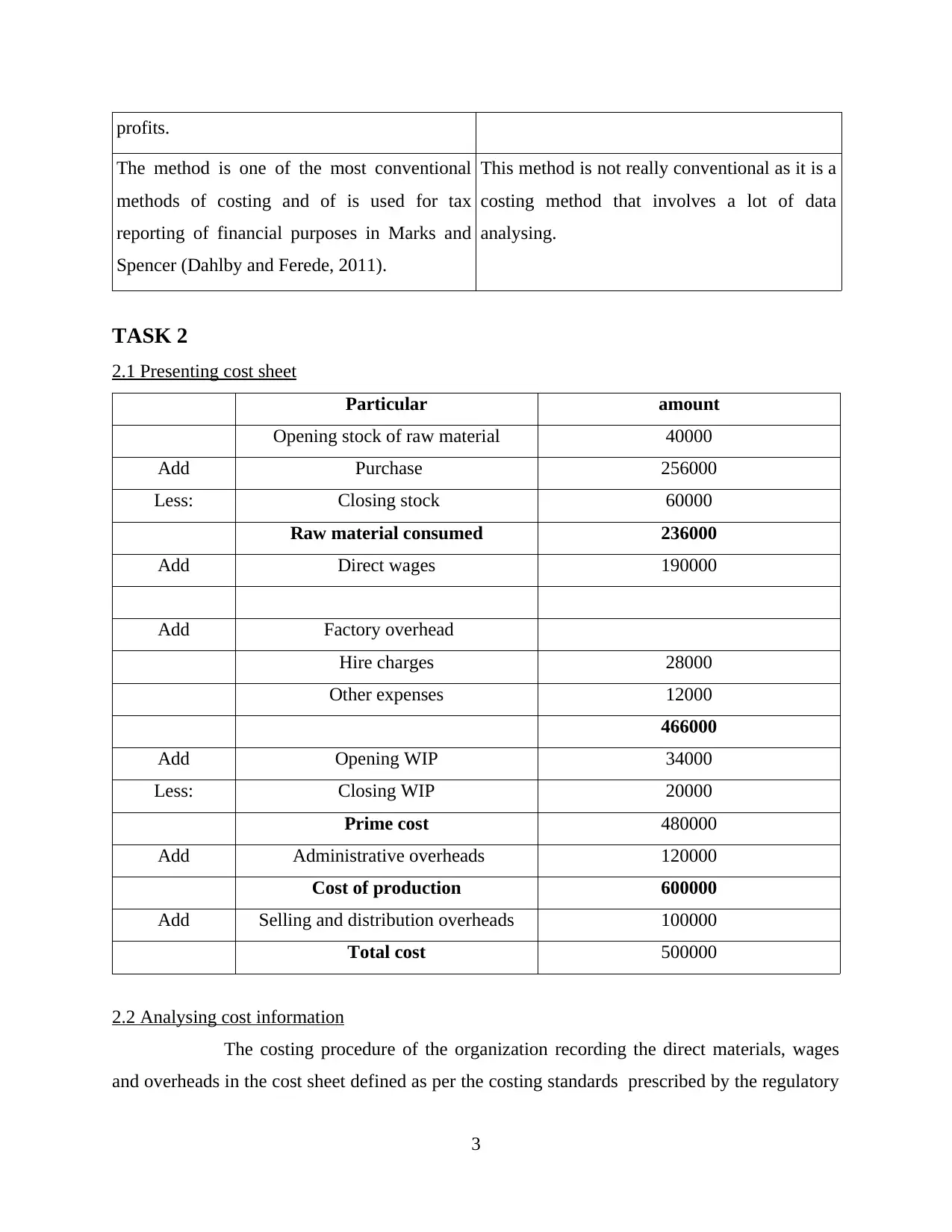

2.1 Presenting cost sheet

Particular amount

Opening stock of raw material 40000

Add Purchase 256000

Less: Closing stock 60000

Raw material consumed 236000

Add Direct wages 190000

Add Factory overhead

Hire charges 28000

Other expenses 12000

466000

Add Opening WIP 34000

Less: Closing WIP 20000

Prime cost 480000

Add Administrative overheads 120000

Cost of production 600000

Add Selling and distribution overheads 100000

Total cost 500000

2.2 Analysing cost information

The costing procedure of the organization recording the direct materials, wages

and overheads in the cost sheet defined as per the costing standards prescribed by the regulatory

3

The method is one of the most conventional

methods of costing and of is used for tax

reporting of financial purposes in Marks and

Spencer (Dahlby and Ferede, 2011).

This method is not really conventional as it is a

costing method that involves a lot of data

analysing.

TASK 2

2.1 Presenting cost sheet

Particular amount

Opening stock of raw material 40000

Add Purchase 256000

Less: Closing stock 60000

Raw material consumed 236000

Add Direct wages 190000

Add Factory overhead

Hire charges 28000

Other expenses 12000

466000

Add Opening WIP 34000

Less: Closing WIP 20000

Prime cost 480000

Add Administrative overheads 120000

Cost of production 600000

Add Selling and distribution overheads 100000

Total cost 500000

2.2 Analysing cost information

The costing procedure of the organization recording the direct materials, wages

and overheads in the cost sheet defined as per the costing standards prescribed by the regulatory

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

authorities and institutions (Gren, Turner and Wulff, 2017). Raw material actually consumed

labour incurred on production and manufacturing expenses along with other expenses incurred

and adjustments related with opening and closing stock are made to reach prime cost.

Administrative and S& cost are added to determined the cost of sales.

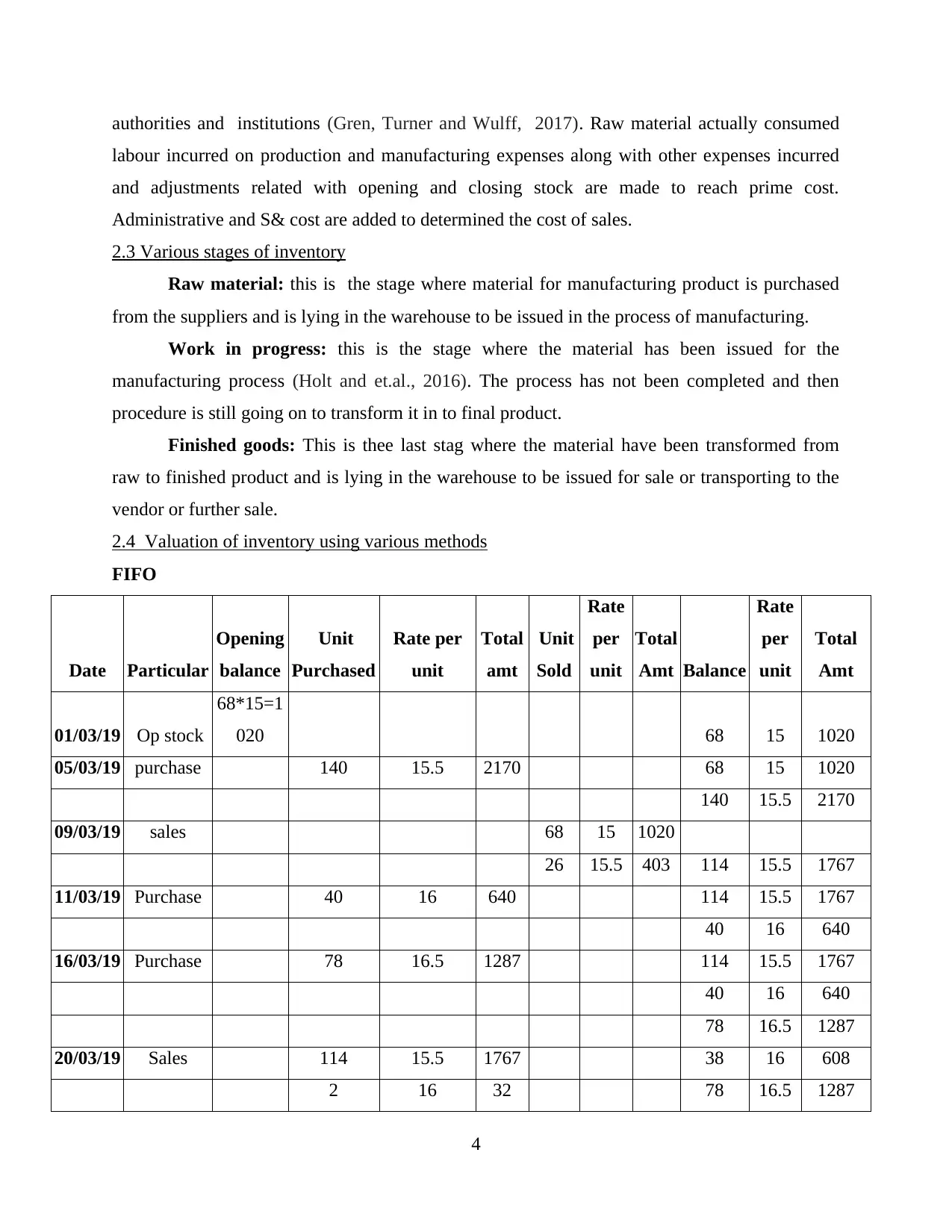

2.3 Various stages of inventory

Raw material: this is the stage where material for manufacturing product is purchased

from the suppliers and is lying in the warehouse to be issued in the process of manufacturing.

Work in progress: this is the stage where the material has been issued for the

manufacturing process (Holt and et.al., 2016). The process has not been completed and then

procedure is still going on to transform it in to final product.

Finished goods: This is thee last stag where the material have been transformed from

raw to finished product and is lying in the warehouse to be issued for sale or transporting to the

vendor or further sale.

2.4 Valuation of inventory using various methods

FIFO

Date Particular

Opening

balance

Unit

Purchased

Rate per

unit

Total

amt

Unit

Sold

Rate

per

unit

Total

Amt Balance

Rate

per

unit

Total

Amt

01/03/19 Op stock

68*15=1

020 68 15 1020

05/03/19 purchase 140 15.5 2170 68 15 1020

140 15.5 2170

09/03/19 sales 68 15 1020

26 15.5 403 114 15.5 1767

11/03/19 Purchase 40 16 640 114 15.5 1767

40 16 640

16/03/19 Purchase 78 16.5 1287 114 15.5 1767

40 16 640

78 16.5 1287

20/03/19 Sales 114 15.5 1767 38 16 608

2 16 32 78 16.5 1287

4

labour incurred on production and manufacturing expenses along with other expenses incurred

and adjustments related with opening and closing stock are made to reach prime cost.

Administrative and S& cost are added to determined the cost of sales.

2.3 Various stages of inventory

Raw material: this is the stage where material for manufacturing product is purchased

from the suppliers and is lying in the warehouse to be issued in the process of manufacturing.

Work in progress: this is the stage where the material has been issued for the

manufacturing process (Holt and et.al., 2016). The process has not been completed and then

procedure is still going on to transform it in to final product.

Finished goods: This is thee last stag where the material have been transformed from

raw to finished product and is lying in the warehouse to be issued for sale or transporting to the

vendor or further sale.

2.4 Valuation of inventory using various methods

FIFO

Date Particular

Opening

balance

Unit

Purchased

Rate per

unit

Total

amt

Unit

Sold

Rate

per

unit

Total

Amt Balance

Rate

per

unit

Total

Amt

01/03/19 Op stock

68*15=1

020 68 15 1020

05/03/19 purchase 140 15.5 2170 68 15 1020

140 15.5 2170

09/03/19 sales 68 15 1020

26 15.5 403 114 15.5 1767

11/03/19 Purchase 40 16 640 114 15.5 1767

40 16 640

16/03/19 Purchase 78 16.5 1287 114 15.5 1767

40 16 640

78 16.5 1287

20/03/19 Sales 114 15.5 1767 38 16 608

2 16 32 78 16.5 1287

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

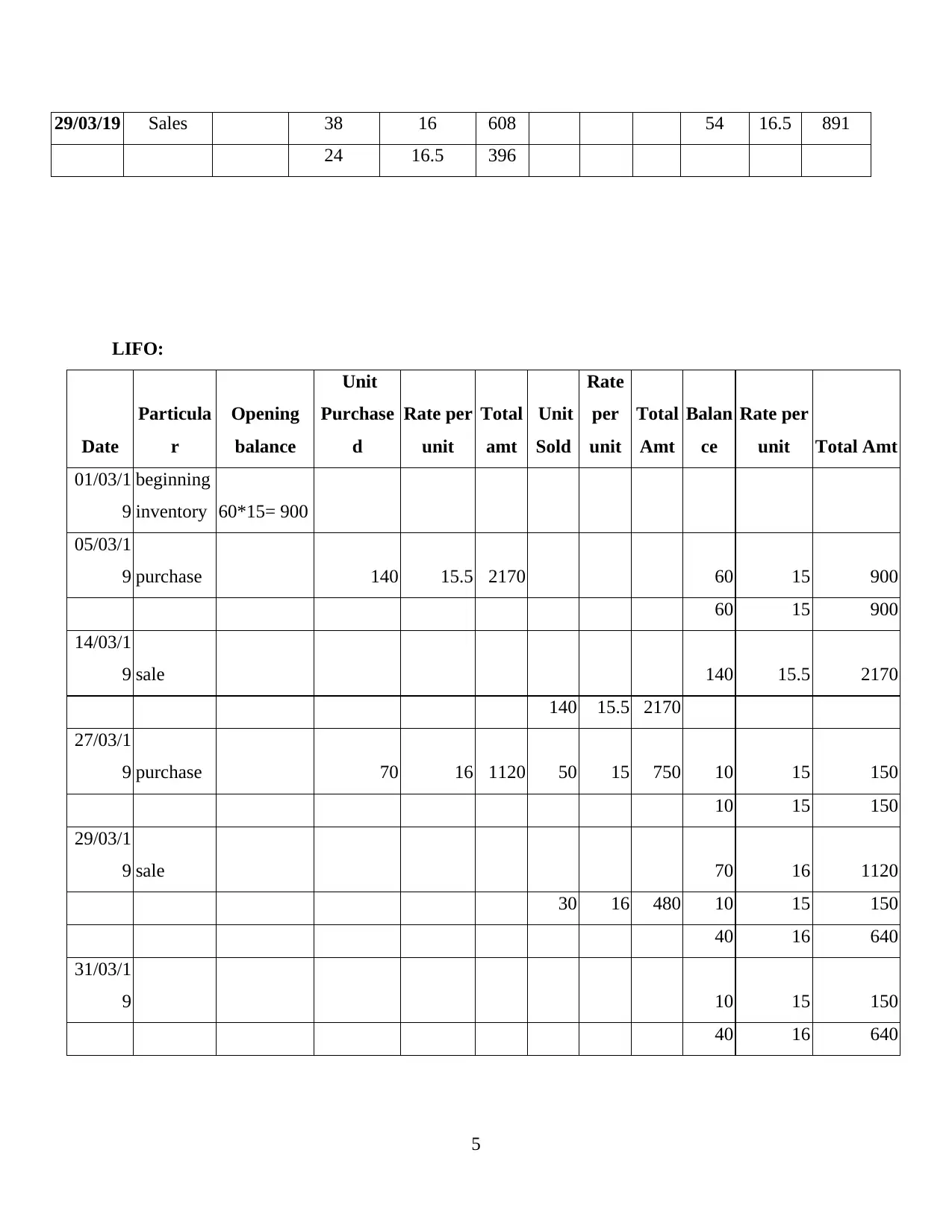

29/03/19 Sales 38 16 608 54 16.5 891

24 16.5 396

LIFO:

Date

Particula

r

Opening

balance

Unit

Purchase

d

Rate per

unit

Total

amt

Unit

Sold

Rate

per

unit

Total

Amt

Balan

ce

Rate per

unit Total Amt

01/03/1

9

beginning

inventory 60*15= 900

05/03/1

9 purchase 140 15.5 2170 60 15 900

60 15 900

14/03/1

9 sale 140 15.5 2170

140 15.5 2170

27/03/1

9 purchase 70 16 1120 50 15 750 10 15 150

10 15 150

29/03/1

9 sale 70 16 1120

30 16 480 10 15 150

40 16 640

31/03/1

9 10 15 150

40 16 640

5

24 16.5 396

LIFO:

Date

Particula

r

Opening

balance

Unit

Purchase

d

Rate per

unit

Total

amt

Unit

Sold

Rate

per

unit

Total

Amt

Balan

ce

Rate per

unit Total Amt

01/03/1

9

beginning

inventory 60*15= 900

05/03/1

9 purchase 140 15.5 2170 60 15 900

60 15 900

14/03/1

9 sale 140 15.5 2170

140 15.5 2170

27/03/1

9 purchase 70 16 1120 50 15 750 10 15 150

10 15 150

29/03/1

9 sale 70 16 1120

30 16 480 10 15 150

40 16 640

31/03/1

9 10 15 150

40 16 640

5

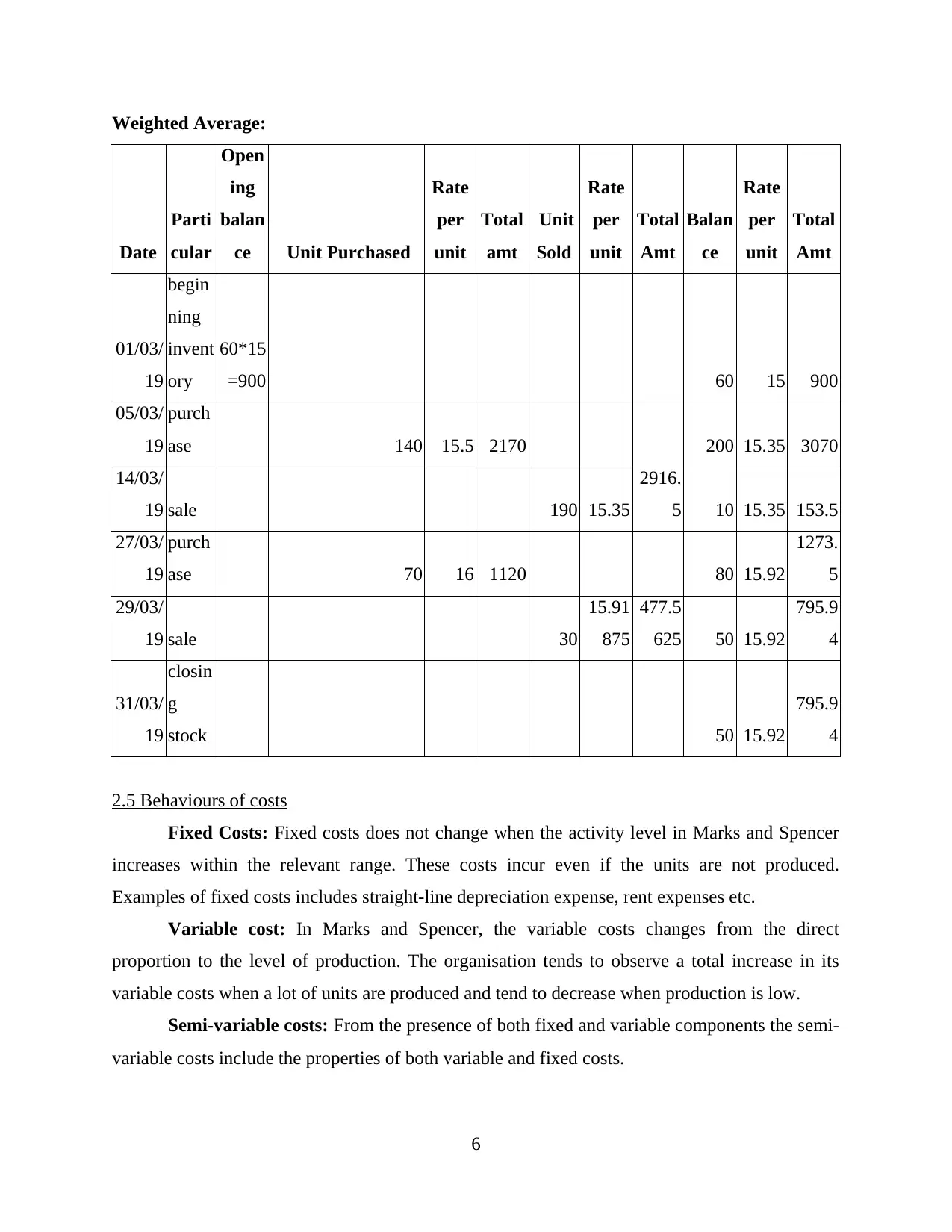

Weighted Average:

Date

Parti

cular

Open

ing

balan

ce Unit Purchased

Rate

per

unit

Total

amt

Unit

Sold

Rate

per

unit

Total

Amt

Balan

ce

Rate

per

unit

Total

Amt

01/03/

19

begin

ning

invent

ory

60*15

=900 60 15 900

05/03/

19

purch

ase 140 15.5 2170 200 15.35 3070

14/03/

19 sale 190 15.35

2916.

5 10 15.35 153.5

27/03/

19

purch

ase 70 16 1120 80 15.92

1273.

5

29/03/

19 sale 30

15.91

875

477.5

625 50 15.92

795.9

4

31/03/

19

closin

g

stock 50 15.92

795.9

4

2.5 Behaviours of costs

Fixed Costs: Fixed costs does not change when the activity level in Marks and Spencer

increases within the relevant range. These costs incur even if the units are not produced.

Examples of fixed costs includes straight-line depreciation expense, rent expenses etc.

Variable cost: In Marks and Spencer, the variable costs changes from the direct

proportion to the level of production. The organisation tends to observe a total increase in its

variable costs when a lot of units are produced and tend to decrease when production is low.

Semi-variable costs: From the presence of both fixed and variable components the semi-

variable costs include the properties of both variable and fixed costs.

6

Date

Parti

cular

Open

ing

balan

ce Unit Purchased

Rate

per

unit

Total

amt

Unit

Sold

Rate

per

unit

Total

Amt

Balan

ce

Rate

per

unit

Total

Amt

01/03/

19

begin

ning

invent

ory

60*15

=900 60 15 900

05/03/

19

purch

ase 140 15.5 2170 200 15.35 3070

14/03/

19 sale 190 15.35

2916.

5 10 15.35 153.5

27/03/

19

purch

ase 70 16 1120 80 15.92

1273.

5

29/03/

19 sale 30

15.91

875

477.5

625 50 15.92

795.9

4

31/03/

19

closin

g

stock 50 15.92

795.9

4

2.5 Behaviours of costs

Fixed Costs: Fixed costs does not change when the activity level in Marks and Spencer

increases within the relevant range. These costs incur even if the units are not produced.

Examples of fixed costs includes straight-line depreciation expense, rent expenses etc.

Variable cost: In Marks and Spencer, the variable costs changes from the direct

proportion to the level of production. The organisation tends to observe a total increase in its

variable costs when a lot of units are produced and tend to decrease when production is low.

Semi-variable costs: From the presence of both fixed and variable components the semi-

variable costs include the properties of both variable and fixed costs.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Step costs: Step costs does not change when Marks and Spencer's activity volume is

changed. It changes at discrete points.

2.6 Cost information and the costing systems

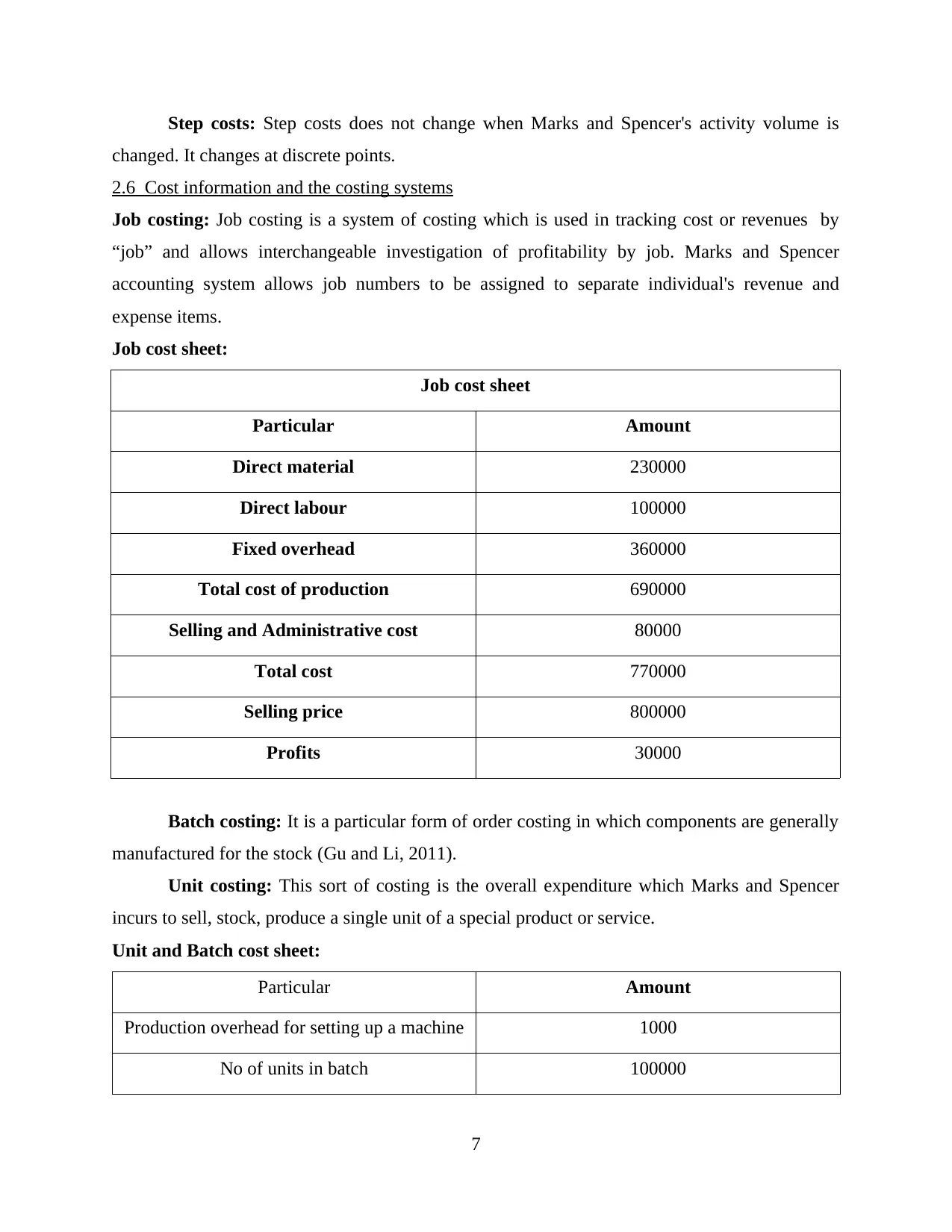

Job costing: Job costing is a system of costing which is used in tracking cost or revenues by

“job” and allows interchangeable investigation of profitability by job. Marks and Spencer

accounting system allows job numbers to be assigned to separate individual's revenue and

expense items.

Job cost sheet:

Job cost sheet

Particular Amount

Direct material 230000

Direct labour 100000

Fixed overhead 360000

Total cost of production 690000

Selling and Administrative cost 80000

Total cost 770000

Selling price 800000

Profits 30000

Batch costing: It is a particular form of order costing in which components are generally

manufactured for the stock (Gu and Li, 2011).

Unit costing: This sort of costing is the overall expenditure which Marks and Spencer

incurs to sell, stock, produce a single unit of a special product or service.

Unit and Batch cost sheet:

Particular Amount

Production overhead for setting up a machine 1000

No of units in batch 100000

7

changed. It changes at discrete points.

2.6 Cost information and the costing systems

Job costing: Job costing is a system of costing which is used in tracking cost or revenues by

“job” and allows interchangeable investigation of profitability by job. Marks and Spencer

accounting system allows job numbers to be assigned to separate individual's revenue and

expense items.

Job cost sheet:

Job cost sheet

Particular Amount

Direct material 230000

Direct labour 100000

Fixed overhead 360000

Total cost of production 690000

Selling and Administrative cost 80000

Total cost 770000

Selling price 800000

Profits 30000

Batch costing: It is a particular form of order costing in which components are generally

manufactured for the stock (Gu and Li, 2011).

Unit costing: This sort of costing is the overall expenditure which Marks and Spencer

incurs to sell, stock, produce a single unit of a special product or service.

Unit and Batch cost sheet:

Particular Amount

Production overhead for setting up a machine 1000

No of units in batch 100000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

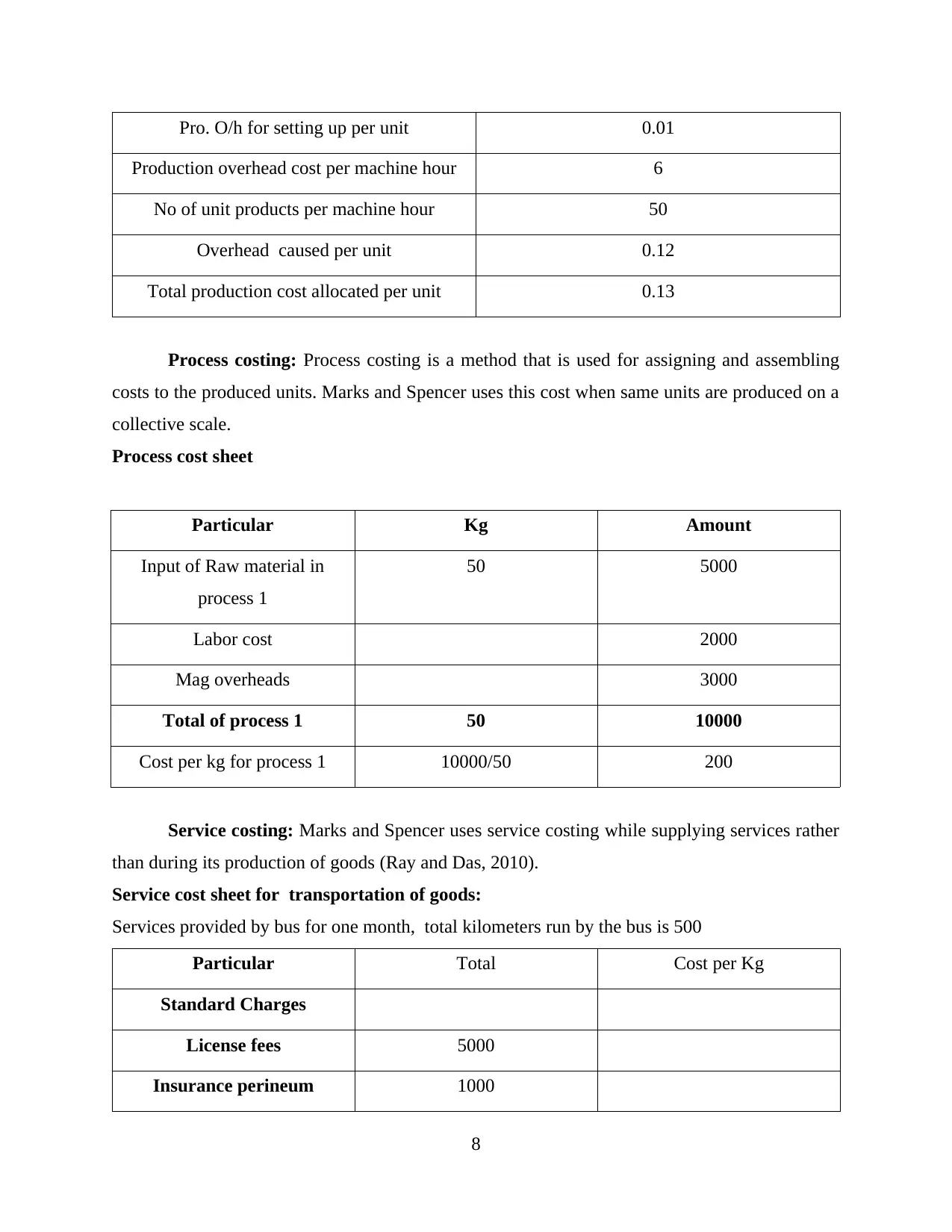

Pro. O/h for setting up per unit 0.01

Production overhead cost per machine hour 6

No of unit products per machine hour 50

Overhead caused per unit 0.12

Total production cost allocated per unit 0.13

Process costing: Process costing is a method that is used for assigning and assembling

costs to the produced units. Marks and Spencer uses this cost when same units are produced on a

collective scale.

Process cost sheet

Particular Kg Amount

Input of Raw material in

process 1

50 5000

Labor cost 2000

Mag overheads 3000

Total of process 1 50 10000

Cost per kg for process 1 10000/50 200

Service costing: Marks and Spencer uses service costing while supplying services rather

than during its production of goods (Ray and Das, 2010).

Service cost sheet for transportation of goods:

Services provided by bus for one month, total kilometers run by the bus is 500

Particular Total Cost per Kg

Standard Charges

License fees 5000

Insurance perineum 1000

8

Production overhead cost per machine hour 6

No of unit products per machine hour 50

Overhead caused per unit 0.12

Total production cost allocated per unit 0.13

Process costing: Process costing is a method that is used for assigning and assembling

costs to the produced units. Marks and Spencer uses this cost when same units are produced on a

collective scale.

Process cost sheet

Particular Kg Amount

Input of Raw material in

process 1

50 5000

Labor cost 2000

Mag overheads 3000

Total of process 1 50 10000

Cost per kg for process 1 10000/50 200

Service costing: Marks and Spencer uses service costing while supplying services rather

than during its production of goods (Ray and Das, 2010).

Service cost sheet for transportation of goods:

Services provided by bus for one month, total kilometers run by the bus is 500

Particular Total Cost per Kg

Standard Charges

License fees 5000

Insurance perineum 1000

8

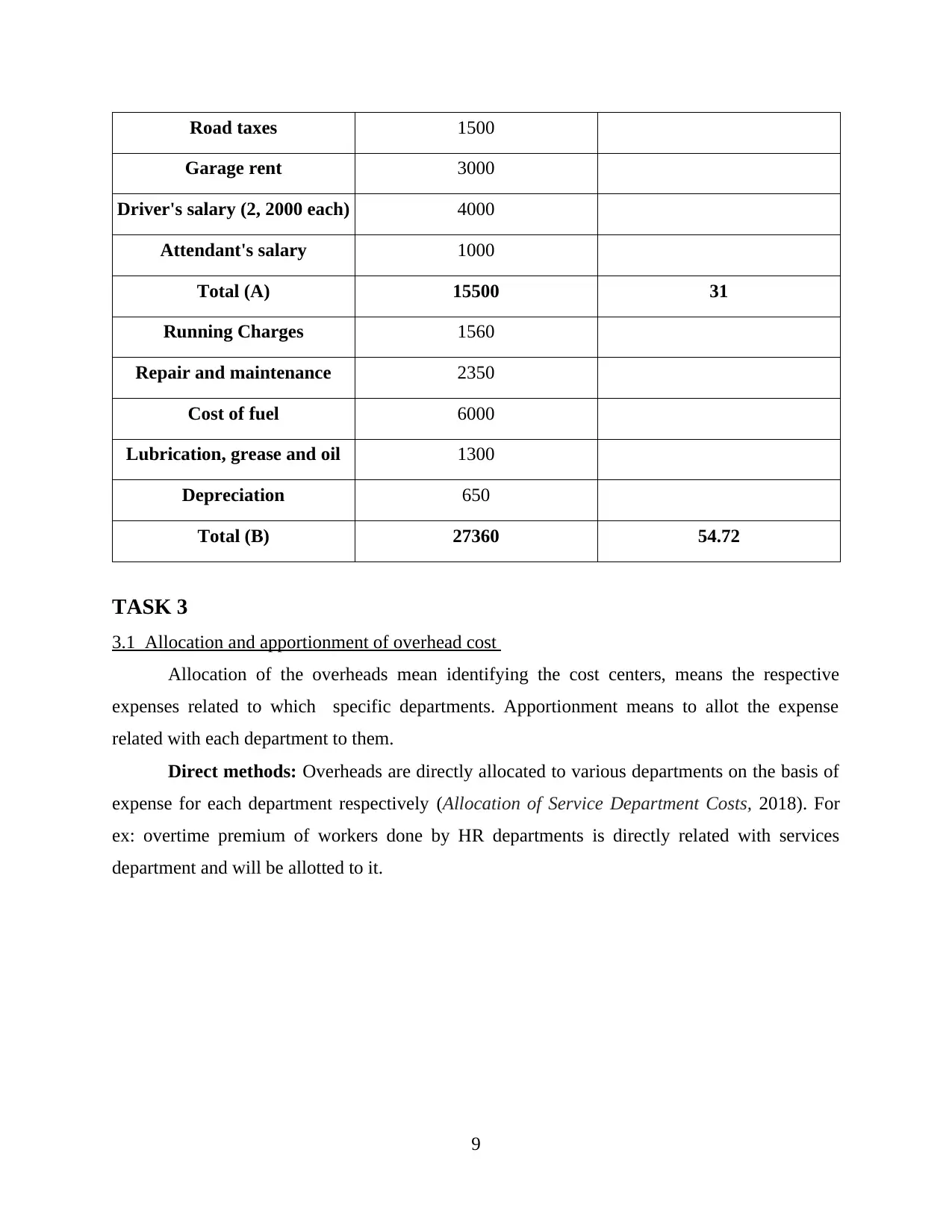

Road taxes 1500

Garage rent 3000

Driver's salary (2, 2000 each) 4000

Attendant's salary 1000

Total (A) 15500 31

Running Charges 1560

Repair and maintenance 2350

Cost of fuel 6000

Lubrication, grease and oil 1300

Depreciation 650

Total (B) 27360 54.72

TASK 3

3.1 Allocation and apportionment of overhead cost

Allocation of the overheads mean identifying the cost centers, means the respective

expenses related to which specific departments. Apportionment means to allot the expense

related with each department to them.

Direct methods: Overheads are directly allocated to various departments on the basis of

expense for each department respectively (Allocation of Service Department Costs, 2018). For

ex: overtime premium of workers done by HR departments is directly related with services

department and will be allotted to it.

9

Garage rent 3000

Driver's salary (2, 2000 each) 4000

Attendant's salary 1000

Total (A) 15500 31

Running Charges 1560

Repair and maintenance 2350

Cost of fuel 6000

Lubrication, grease and oil 1300

Depreciation 650

Total (B) 27360 54.72

TASK 3

3.1 Allocation and apportionment of overhead cost

Allocation of the overheads mean identifying the cost centers, means the respective

expenses related to which specific departments. Apportionment means to allot the expense

related with each department to them.

Direct methods: Overheads are directly allocated to various departments on the basis of

expense for each department respectively (Allocation of Service Department Costs, 2018). For

ex: overtime premium of workers done by HR departments is directly related with services

department and will be allotted to it.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.