Comprehensive Report: Costs, Revenues, and Decision Making

VerifiedAdded on 2020/12/09

|23

|4695

|486

Report

AI Summary

This report delves into the critical aspects of costs and revenues within an organization, exploring the significance of internal reporting in providing accurate information to management. It examines various costing systems, including marginal and absorption costing, and identifies cost centers, responsibility centers, profit centers, and investment centers. The report further details cost classification, inventory valuation methods (FIFO), and the behavior of different costs. It also covers overhead cost attribution, absorption rates, and variance analysis for management reporting. The analysis extends to decision-making processes, including estimating future income and costs, and identifying factors that influence short and long-term decisions. The report provides a comprehensive understanding of how costs and revenues are managed and analyzed to support effective business decisions, with detailed examples of cost sheets and inventory calculations.

COSTS AND REVENUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

1.1 Explaining purpose of internal reporting and providing accurate information to

management................................................................................................................................1

1.2 Relationship between various costing systems within an organisation...............................1

1.3 Identifying cost centres, responsibility centres, profit and investment centres in an

organisation.................................................................................................................................2

1.4 Characteristics of different kinds of cost classification and their use in costing.................3

1.5 Difference between marginal and absorption costing ..........................................................3

TASK 2 ...........................................................................................................................................4

2.1 Recording cost information for labour, material and expenses ............................................4

2.2 Analysing cost information for labour, material and expenses according to organisation's

procedure.....................................................................................................................................4

2.3 Defining different stages of inventory .................................................................................5

2.4 Inventory valuation using different methods .......................................................................5

Closing inventory: 50 unit @ (£)15 = (£)750.............................................................................7

2.5 Describing behaviour of different cost..................................................................................8

2.6 Recording cost information by using different costing systems ..........................................9

TASK 3 ...........................................................................................................................................9

3.1 Attributing overhead costs ...................................................................................................9

3.2 Calculating overhead absorption rate .................................................................................10

3.3 Adjustments for over or under overheads...........................................................................11

3.4 Methods of allocation, absorption and apportionment .......................................................12

3.5 Communicating cost related data .......................................................................................12

TASK 4 .........................................................................................................................................12

4.1 Comparing budget cost with actual cost with variances.....................................................12

4.2 Analysing variance for management report........................................................................12

4.3 Providing information to budget holders and making suggestions...................................13

4.4 Preparing management report ............................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1 ...........................................................................................................................................1

1.1 Explaining purpose of internal reporting and providing accurate information to

management................................................................................................................................1

1.2 Relationship between various costing systems within an organisation...............................1

1.3 Identifying cost centres, responsibility centres, profit and investment centres in an

organisation.................................................................................................................................2

1.4 Characteristics of different kinds of cost classification and their use in costing.................3

1.5 Difference between marginal and absorption costing ..........................................................3

TASK 2 ...........................................................................................................................................4

2.1 Recording cost information for labour, material and expenses ............................................4

2.2 Analysing cost information for labour, material and expenses according to organisation's

procedure.....................................................................................................................................4

2.3 Defining different stages of inventory .................................................................................5

2.4 Inventory valuation using different methods .......................................................................5

Closing inventory: 50 unit @ (£)15 = (£)750.............................................................................7

2.5 Describing behaviour of different cost..................................................................................8

2.6 Recording cost information by using different costing systems ..........................................9

TASK 3 ...........................................................................................................................................9

3.1 Attributing overhead costs ...................................................................................................9

3.2 Calculating overhead absorption rate .................................................................................10

3.3 Adjustments for over or under overheads...........................................................................11

3.4 Methods of allocation, absorption and apportionment .......................................................12

3.5 Communicating cost related data .......................................................................................12

TASK 4 .........................................................................................................................................12

4.1 Comparing budget cost with actual cost with variances.....................................................12

4.2 Analysing variance for management report........................................................................12

4.3 Providing information to budget holders and making suggestions...................................13

4.4 Preparing management report ............................................................................................13

TASK 5 .........................................................................................................................................15

5.1 Preparing estimates of future income and cost of decision making ...................................15

5.2 Explaining effect of changing activity level on unit costs..................................................17

5.3 Calculating effect of changing activity level on unit costs ...............................................17

5.4 Identifying factors that affect short and long term decision making .................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

5.1 Preparing estimates of future income and cost of decision making ...................................15

5.2 Explaining effect of changing activity level on unit costs..................................................17

5.3 Calculating effect of changing activity level on unit costs ...............................................17

5.4 Identifying factors that affect short and long term decision making .................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Cost and revenue are the two aspects of an organisation around which all the activities

revolves (Abel and Le Roux, 2016). The present report is going to discuss purpose of internal

reporting, classification of cost and their behaviours, different costing system and how material,

labour and expenses are recorded in these systems. A segment will discuss the importance of

management reports and factors affecting decision making of managers in an organisation.

TASK 1

1.1 Explaining purpose of internal reporting and providing accurate information to management

Internal reporting to management is a well defined system of providing business

information of all levels to management. This enables managers to measure effectiveness of

different responsibility centres.

The main purpose of internal reporting is:

To facilitate the managers in their decision making process.

Communicating vital information about the company's performance to interested

stakeholders.

Providing accurate and reliable information in the form of reports helps the management

in analysing different trends.

For examining financial health of the company such as analysis of utilisation of different

resources, cash flow etc.

To improve the efficiency and effectiveness of senior management of company.

To control the business operations. Cost control and cost reduction is efficiently done by

analysing the reports of each level in an organisation.

1.2 Relationship between various costing systems within an organisation

There are various types of costing systems such as marginal, absorption, standard,

historical which a company adopts for allocating the cost to different expenditure overheads.

Marginal and absorption costing systems shares a prevalence that both the systems helps in

finding out the cost per unit and profit per unit. Both the system helps management in their

decision making regarding estimation of budgets, assessing where the resources are being over

1

Cost and revenue are the two aspects of an organisation around which all the activities

revolves (Abel and Le Roux, 2016). The present report is going to discuss purpose of internal

reporting, classification of cost and their behaviours, different costing system and how material,

labour and expenses are recorded in these systems. A segment will discuss the importance of

management reports and factors affecting decision making of managers in an organisation.

TASK 1

1.1 Explaining purpose of internal reporting and providing accurate information to management

Internal reporting to management is a well defined system of providing business

information of all levels to management. This enables managers to measure effectiveness of

different responsibility centres.

The main purpose of internal reporting is:

To facilitate the managers in their decision making process.

Communicating vital information about the company's performance to interested

stakeholders.

Providing accurate and reliable information in the form of reports helps the management

in analysing different trends.

For examining financial health of the company such as analysis of utilisation of different

resources, cash flow etc.

To improve the efficiency and effectiveness of senior management of company.

To control the business operations. Cost control and cost reduction is efficiently done by

analysing the reports of each level in an organisation.

1.2 Relationship between various costing systems within an organisation

There are various types of costing systems such as marginal, absorption, standard,

historical which a company adopts for allocating the cost to different expenditure overheads.

Marginal and absorption costing systems shares a prevalence that both the systems helps in

finding out the cost per unit and profit per unit. Both the system helps management in their

decision making regarding estimation of budgets, assessing where the resources are being over

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

utilised etc. The management gains from these systems as these methods helps in optimum

allocation of cost to different overheads. This leads to accurate determination cost of each input

that is being used in production process (Dempsey and Kelliher, 2018).

However, there is one major difference between these two system is that marginal costing

only considers variable costs as product cost and fixed cost as cost of period whereas absorption

costing considers both fixed and variable cost as product cost.

Standard and historical costing system also shares some similar characteristics such as

determining cost of each unit. These also helps management in framing out various rationale

decisions regarding the cost allocation within the different overheads. However, standard costing

considers pre-estimated standards for determining the cost of direct materials, labour, direct

overheads whereas historical costing method considers actual costs that have been incurred and

does not rely estimated standards.

1.3 Identifying cost centres, responsibility centres, profit and investment centres in an

organisation

A responsibility centre can be defined as a part of an enterprise for which a specific

individual namely as manager who is responsible for all the operations of that unit. Cost and

profit centres are some typical example of responsibility centre.

Cost centre is one of the type of the type of responsibility centre which is concerned with

a particular department in a company to which different costs are allocated. Logistics, It,

production, R&D are some departments in an organisation which incurs costs that directly or

indirectly contribute in manufacturing of the goods and services.

Profit centre is a segment of an organisation whose stand-alone profitability is analysed.

Profits and losses of this segment is computed separately. The manger responsible for profit

centre is responsible for bringing cash in to the organisation by the way of increase in sale.

Selling or sales department is profit centre which is responsible for generating higher sales and

for which profit and loss can be calculated (Hemel, Nou, and Weisbach, 2018).

Investment centre is treated as business unit in an organisation for evaluating

performance of a segment or department of company. This takes into consideration costs,

2

allocation of cost to different overheads. This leads to accurate determination cost of each input

that is being used in production process (Dempsey and Kelliher, 2018).

However, there is one major difference between these two system is that marginal costing

only considers variable costs as product cost and fixed cost as cost of period whereas absorption

costing considers both fixed and variable cost as product cost.

Standard and historical costing system also shares some similar characteristics such as

determining cost of each unit. These also helps management in framing out various rationale

decisions regarding the cost allocation within the different overheads. However, standard costing

considers pre-estimated standards for determining the cost of direct materials, labour, direct

overheads whereas historical costing method considers actual costs that have been incurred and

does not rely estimated standards.

1.3 Identifying cost centres, responsibility centres, profit and investment centres in an

organisation

A responsibility centre can be defined as a part of an enterprise for which a specific

individual namely as manager who is responsible for all the operations of that unit. Cost and

profit centres are some typical example of responsibility centre.

Cost centre is one of the type of the type of responsibility centre which is concerned with

a particular department in a company to which different costs are allocated. Logistics, It,

production, R&D are some departments in an organisation which incurs costs that directly or

indirectly contribute in manufacturing of the goods and services.

Profit centre is a segment of an organisation whose stand-alone profitability is analysed.

Profits and losses of this segment is computed separately. The manger responsible for profit

centre is responsible for bringing cash in to the organisation by the way of increase in sale.

Selling or sales department is profit centre which is responsible for generating higher sales and

for which profit and loss can be calculated (Hemel, Nou, and Weisbach, 2018).

Investment centre is treated as business unit in an organisation for evaluating

performance of a segment or department of company. This takes into consideration costs,

2

revenues, capital expenditure in the form of assets that are used in production process, ultimately

contributing to profitability of the organisation.

1.4 Characteristics of different kinds of cost classification and their use in costing

There are different types of costs that a company incurs for producing and selling its

goods and services which are given below:

Fixed cost : These are the cost that does not vary with change in production level such as

rent of premises, insurance premium, interest payment, depreciation etc. Fixed cost are used in

costing for determining the total costs incurred for producing each unit.

Variable cost : These are the costs that varies with change in production level such as

direct labour, raw materials, factory's electricity bill etc. Marginal costing considers only variable

cost in determining the cost of each additional unit of output.

Semi variable cost: These cost are mixture of fixed and variable cost. To an extent, a part

of cost remains fixed but after passing the limit, it becomes variable in nature.

Direct an Indirect cost : Direct costs are those which directly contribute to the production

cost such as direct labour, material utility. These are summed for up for finding out prime cost of

a product.

Indirect cost are those which do not directly contributes to manufacturing of a product

such as salaries, commissions, packaging etc. These are included in prime cost for finding out

total cost of production (Holzhacker, Krishnan and Mahlendorf, 2015).

1.5 Difference between marginal and absorption costing

Basis Marginal costing Absorption costing

Treatment of fixed cost and

variable cost

It considers only variable cost

as products cost

It considers fixed and variable

both costs as product cost.

Inventory It does not take into

consideration opening and

closing stock while

determining cost.

It involves opening and closing

inventory in its calculation.

Purpose and requirement There is no such legal It is legally required to apply

3

contributing to profitability of the organisation.

1.4 Characteristics of different kinds of cost classification and their use in costing

There are different types of costs that a company incurs for producing and selling its

goods and services which are given below:

Fixed cost : These are the cost that does not vary with change in production level such as

rent of premises, insurance premium, interest payment, depreciation etc. Fixed cost are used in

costing for determining the total costs incurred for producing each unit.

Variable cost : These are the costs that varies with change in production level such as

direct labour, raw materials, factory's electricity bill etc. Marginal costing considers only variable

cost in determining the cost of each additional unit of output.

Semi variable cost: These cost are mixture of fixed and variable cost. To an extent, a part

of cost remains fixed but after passing the limit, it becomes variable in nature.

Direct an Indirect cost : Direct costs are those which directly contribute to the production

cost such as direct labour, material utility. These are summed for up for finding out prime cost of

a product.

Indirect cost are those which do not directly contributes to manufacturing of a product

such as salaries, commissions, packaging etc. These are included in prime cost for finding out

total cost of production (Holzhacker, Krishnan and Mahlendorf, 2015).

1.5 Difference between marginal and absorption costing

Basis Marginal costing Absorption costing

Treatment of fixed cost and

variable cost

It considers only variable cost

as products cost

It considers fixed and variable

both costs as product cost.

Inventory It does not take into

consideration opening and

closing stock while

determining cost.

It involves opening and closing

inventory in its calculation.

Purpose and requirement There is no such legal It is legally required to apply

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

foundation and it is generally

prepared for internal reporting

for enabling managers to make

rationale decisions.

absorption costing and its

reporting purpose is to

communicate information

externally.

TASK 2

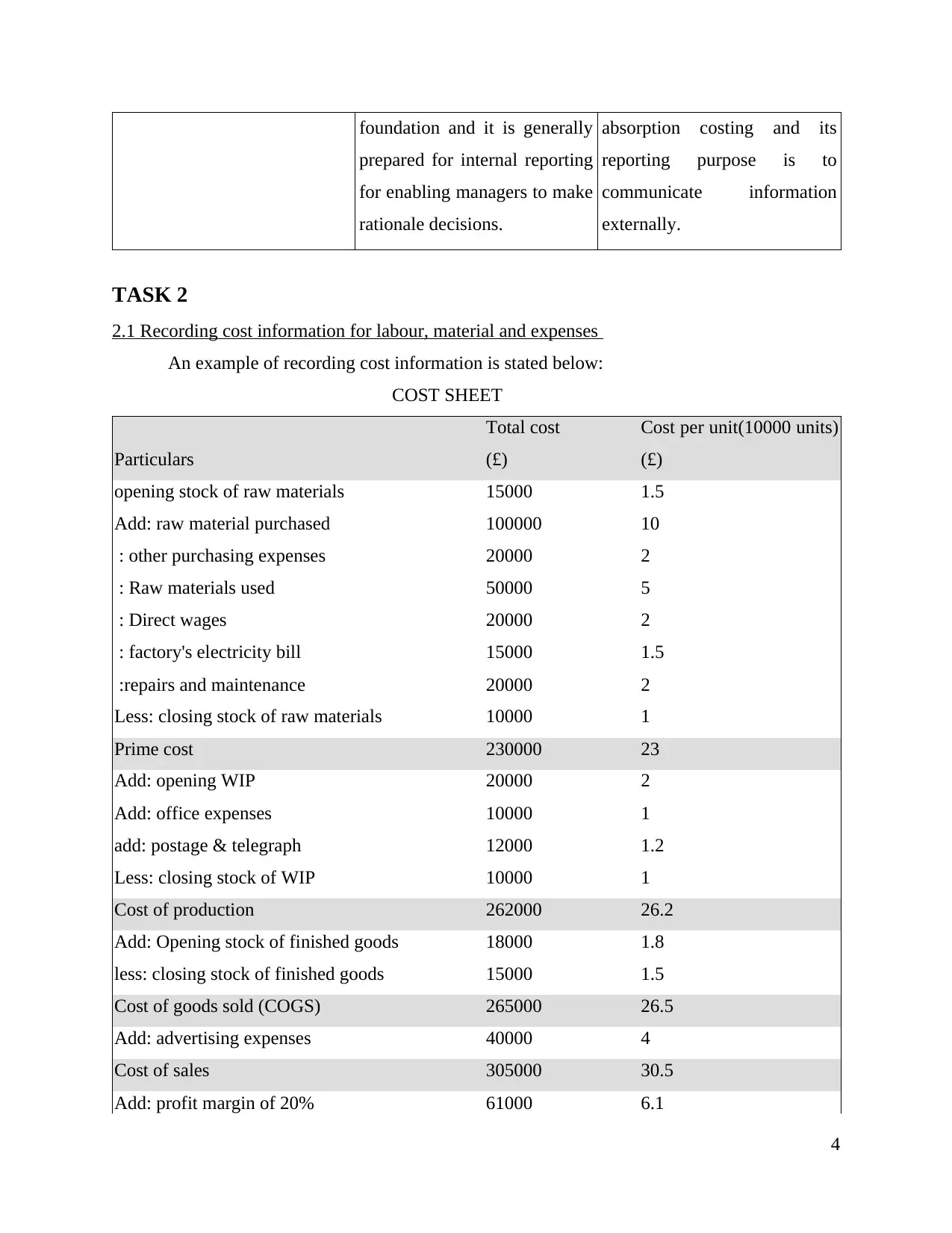

2.1 Recording cost information for labour, material and expenses

An example of recording cost information is stated below:

COST SHEET

Particulars

Total cost

(£)

Cost per unit(10000 units)

(£)

opening stock of raw materials 15000 1.5

Add: raw material purchased 100000 10

: other purchasing expenses 20000 2

: Raw materials used 50000 5

: Direct wages 20000 2

: factory's electricity bill 15000 1.5

:repairs and maintenance 20000 2

Less: closing stock of raw materials 10000 1

Prime cost 230000 23

Add: opening WIP 20000 2

Add: office expenses 10000 1

add: postage & telegraph 12000 1.2

Less: closing stock of WIP 10000 1

Cost of production 262000 26.2

Add: Opening stock of finished goods 18000 1.8

less: closing stock of finished goods 15000 1.5

Cost of goods sold (COGS) 265000 26.5

Add: advertising expenses 40000 4

Cost of sales 305000 30.5

Add: profit margin of 20% 61000 6.1

4

prepared for internal reporting

for enabling managers to make

rationale decisions.

absorption costing and its

reporting purpose is to

communicate information

externally.

TASK 2

2.1 Recording cost information for labour, material and expenses

An example of recording cost information is stated below:

COST SHEET

Particulars

Total cost

(£)

Cost per unit(10000 units)

(£)

opening stock of raw materials 15000 1.5

Add: raw material purchased 100000 10

: other purchasing expenses 20000 2

: Raw materials used 50000 5

: Direct wages 20000 2

: factory's electricity bill 15000 1.5

:repairs and maintenance 20000 2

Less: closing stock of raw materials 10000 1

Prime cost 230000 23

Add: opening WIP 20000 2

Add: office expenses 10000 1

add: postage & telegraph 12000 1.2

Less: closing stock of WIP 10000 1

Cost of production 262000 26.2

Add: Opening stock of finished goods 18000 1.8

less: closing stock of finished goods 15000 1.5

Cost of goods sold (COGS) 265000 26.5

Add: advertising expenses 40000 4

Cost of sales 305000 30.5

Add: profit margin of 20% 61000 6.1

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling price 366000 36.6

2.2 Analysing cost information for labour, material and expenses according to organisation's

procedure

Direct labour, raw material's opening stock, purchases of raw materials, expenses related

to purchasing of raw materials such as carriage expenses are added. Direct wages, manufacturing

expenses such as factory's electricity bill, repairs and maintenance are added up for finding out

the prime cost of the product. Closing stock of raw material is deducted while calculating prime

cost (Kim, 2018).

Prime cost is the cost of manufacturing a product for sale by taking into consideration

direct cost to production such as direct materials, direct wages and direct manufacturing

expenses. This cost is the basis for calculating cost of production in which opening WIP is added

along with administrative expenses such as office expenses, postage, telegraph etc. Closing stock

of WIP is deducted for finding out the Cost of goods sold (COGS). In here, opening and closing

stock of finished goods are added and subtracted respectively for calculating cost of sales.

Selling expenses such as advertising are added up for reaching at total cost. A desired profit

margin is added up in total cost for determining the selling price of the product produced. This is

the price at which an organisation sells it products to the consumers.

2.3 Defining different stages of inventory

Inventory in an organisation refers to all work that has been done or it is in process for

converting raw materials into finished goods. The inventory have 4 stages that are given below:

Raw material : These include every component that is used in conversion process of

manufacturing goods and services. Example of raw material are crude oil for producing

chemicals, fuels etc. vegetables used by restaurant company for converting into a dish

(Becker-Peth and Thonemann, 2016).

Work in progress: It includes partially processed raw materials, component, assembling

products etc. that is being transferred from stage one.

Finished goods : These are the goods that are fully processed and are ready to be used by

final consumers. Inventory of finished goods include stock of ready to use goods.

5

2.2 Analysing cost information for labour, material and expenses according to organisation's

procedure

Direct labour, raw material's opening stock, purchases of raw materials, expenses related

to purchasing of raw materials such as carriage expenses are added. Direct wages, manufacturing

expenses such as factory's electricity bill, repairs and maintenance are added up for finding out

the prime cost of the product. Closing stock of raw material is deducted while calculating prime

cost (Kim, 2018).

Prime cost is the cost of manufacturing a product for sale by taking into consideration

direct cost to production such as direct materials, direct wages and direct manufacturing

expenses. This cost is the basis for calculating cost of production in which opening WIP is added

along with administrative expenses such as office expenses, postage, telegraph etc. Closing stock

of WIP is deducted for finding out the Cost of goods sold (COGS). In here, opening and closing

stock of finished goods are added and subtracted respectively for calculating cost of sales.

Selling expenses such as advertising are added up for reaching at total cost. A desired profit

margin is added up in total cost for determining the selling price of the product produced. This is

the price at which an organisation sells it products to the consumers.

2.3 Defining different stages of inventory

Inventory in an organisation refers to all work that has been done or it is in process for

converting raw materials into finished goods. The inventory have 4 stages that are given below:

Raw material : These include every component that is used in conversion process of

manufacturing goods and services. Example of raw material are crude oil for producing

chemicals, fuels etc. vegetables used by restaurant company for converting into a dish

(Becker-Peth and Thonemann, 2016).

Work in progress: It includes partially processed raw materials, component, assembling

products etc. that is being transferred from stage one.

Finished goods : These are the goods that are fully processed and are ready to be used by

final consumers. Inventory of finished goods include stock of ready to use goods.

5

Goods for resale : Sometimes products are returned by customers that can be sell again

are included in inventories of organisation However, this element is usually not included

in inventory of a company.

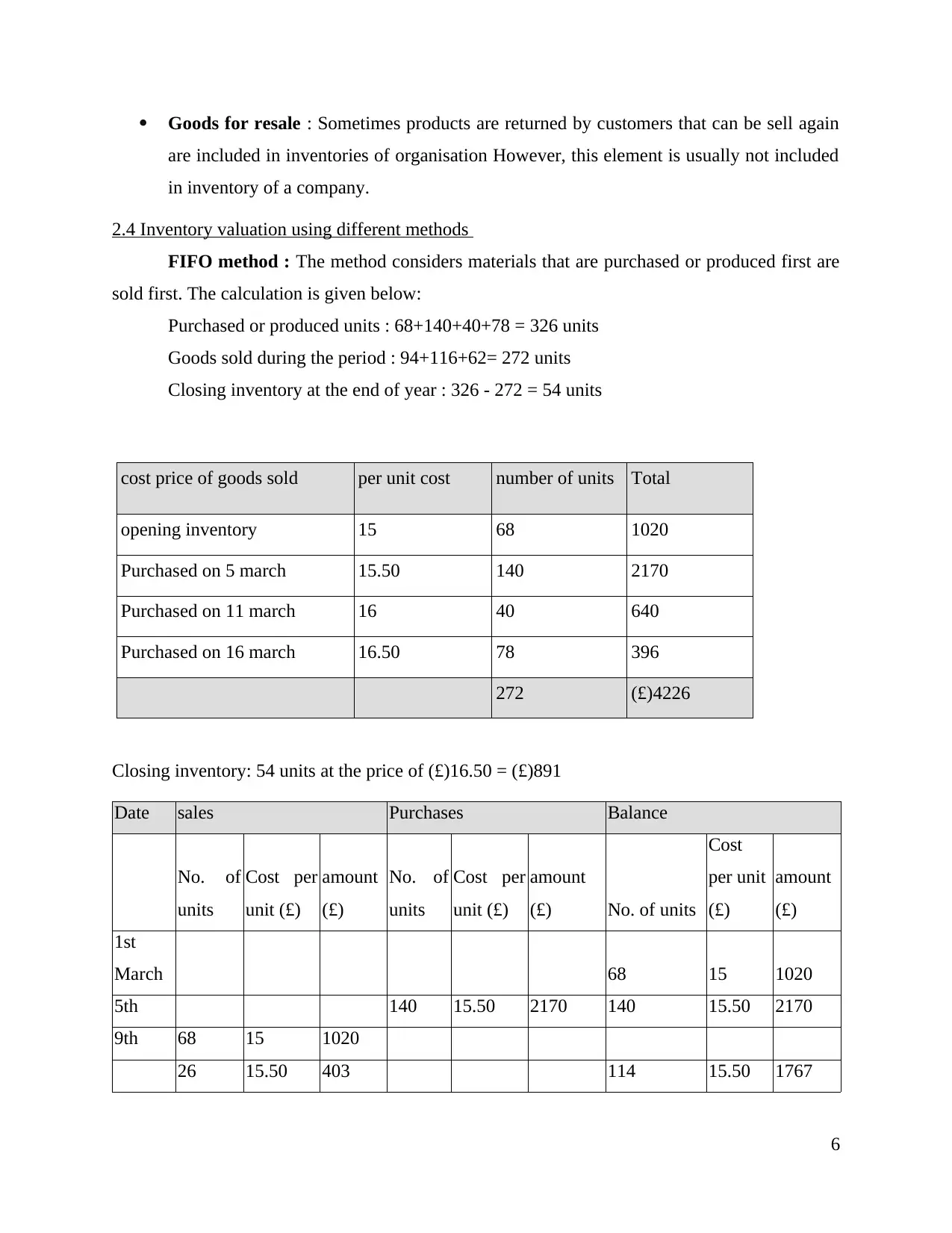

2.4 Inventory valuation using different methods

FIFO method : The method considers materials that are purchased or produced first are

sold first. The calculation is given below:

Purchased or produced units : 68+140+40+78 = 326 units

Goods sold during the period : 94+116+62= 272 units

Closing inventory at the end of year : 326 - 272 = 54 units

cost price of goods sold per unit cost number of units Total

opening inventory 15 68 1020

Purchased on 5 march 15.50 140 2170

Purchased on 11 march 16 40 640

Purchased on 16 march 16.50 78 396

272 (£)4226

Closing inventory: 54 units at the price of (£)16.50 = (£)891

Date sales Purchases Balance

No. of

units

Cost per

unit (£)

amount

(£)

No. of

units

Cost per

unit (£)

amount

(£) No. of units

Cost

per unit

(£)

amount

(£)

1st

March 68 15 1020

5th 140 15.50 2170 140 15.50 2170

9th 68 15 1020

26 15.50 403 114 15.50 1767

6

are included in inventories of organisation However, this element is usually not included

in inventory of a company.

2.4 Inventory valuation using different methods

FIFO method : The method considers materials that are purchased or produced first are

sold first. The calculation is given below:

Purchased or produced units : 68+140+40+78 = 326 units

Goods sold during the period : 94+116+62= 272 units

Closing inventory at the end of year : 326 - 272 = 54 units

cost price of goods sold per unit cost number of units Total

opening inventory 15 68 1020

Purchased on 5 march 15.50 140 2170

Purchased on 11 march 16 40 640

Purchased on 16 march 16.50 78 396

272 (£)4226

Closing inventory: 54 units at the price of (£)16.50 = (£)891

Date sales Purchases Balance

No. of

units

Cost per

unit (£)

amount

(£)

No. of

units

Cost per

unit (£)

amount

(£) No. of units

Cost

per unit

(£)

amount

(£)

1st

March 68 15 1020

5th 140 15.50 2170 140 15.50 2170

9th 68 15 1020

26 15.50 403 114 15.50 1767

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

11th 40 16 640 40 16 640

16th 78 16.50 1287 78 16.50 1287

20th 114 15.50 1767

2 16 32 38 16 608

78 16.50 1287

29th 38 16 608

24 16.50 396

54 16.50 891

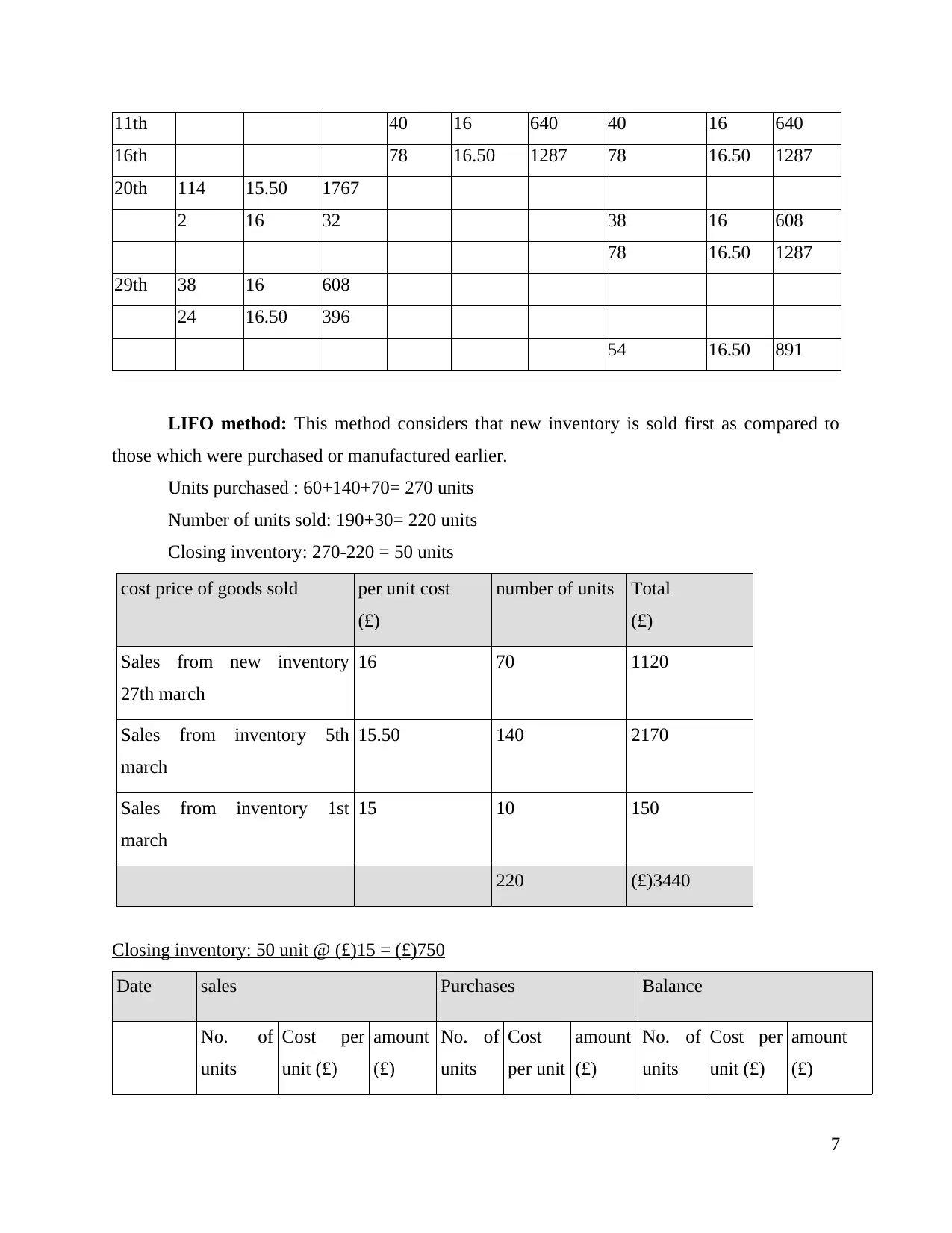

LIFO method: This method considers that new inventory is sold first as compared to

those which were purchased or manufactured earlier.

Units purchased : 60+140+70= 270 units

Number of units sold: 190+30= 220 units

Closing inventory: 270-220 = 50 units

cost price of goods sold per unit cost

(£)

number of units Total

(£)

Sales from new inventory

27th march

16 70 1120

Sales from inventory 5th

march

15.50 140 2170

Sales from inventory 1st

march

15 10 150

220 (£)3440

Closing inventory: 50 unit @ (£)15 = (£)750

Date sales Purchases Balance

No. of

units

Cost per

unit (£)

amount

(£)

No. of

units

Cost

per unit

amount

(£)

No. of

units

Cost per

unit (£)

amount

(£)

7

16th 78 16.50 1287 78 16.50 1287

20th 114 15.50 1767

2 16 32 38 16 608

78 16.50 1287

29th 38 16 608

24 16.50 396

54 16.50 891

LIFO method: This method considers that new inventory is sold first as compared to

those which were purchased or manufactured earlier.

Units purchased : 60+140+70= 270 units

Number of units sold: 190+30= 220 units

Closing inventory: 270-220 = 50 units

cost price of goods sold per unit cost

(£)

number of units Total

(£)

Sales from new inventory

27th march

16 70 1120

Sales from inventory 5th

march

15.50 140 2170

Sales from inventory 1st

march

15 10 150

220 (£)3440

Closing inventory: 50 unit @ (£)15 = (£)750

Date sales Purchases Balance

No. of

units

Cost per

unit (£)

amount

(£)

No. of

units

Cost

per unit

amount

(£)

No. of

units

Cost per

unit (£)

amount

(£)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(£)

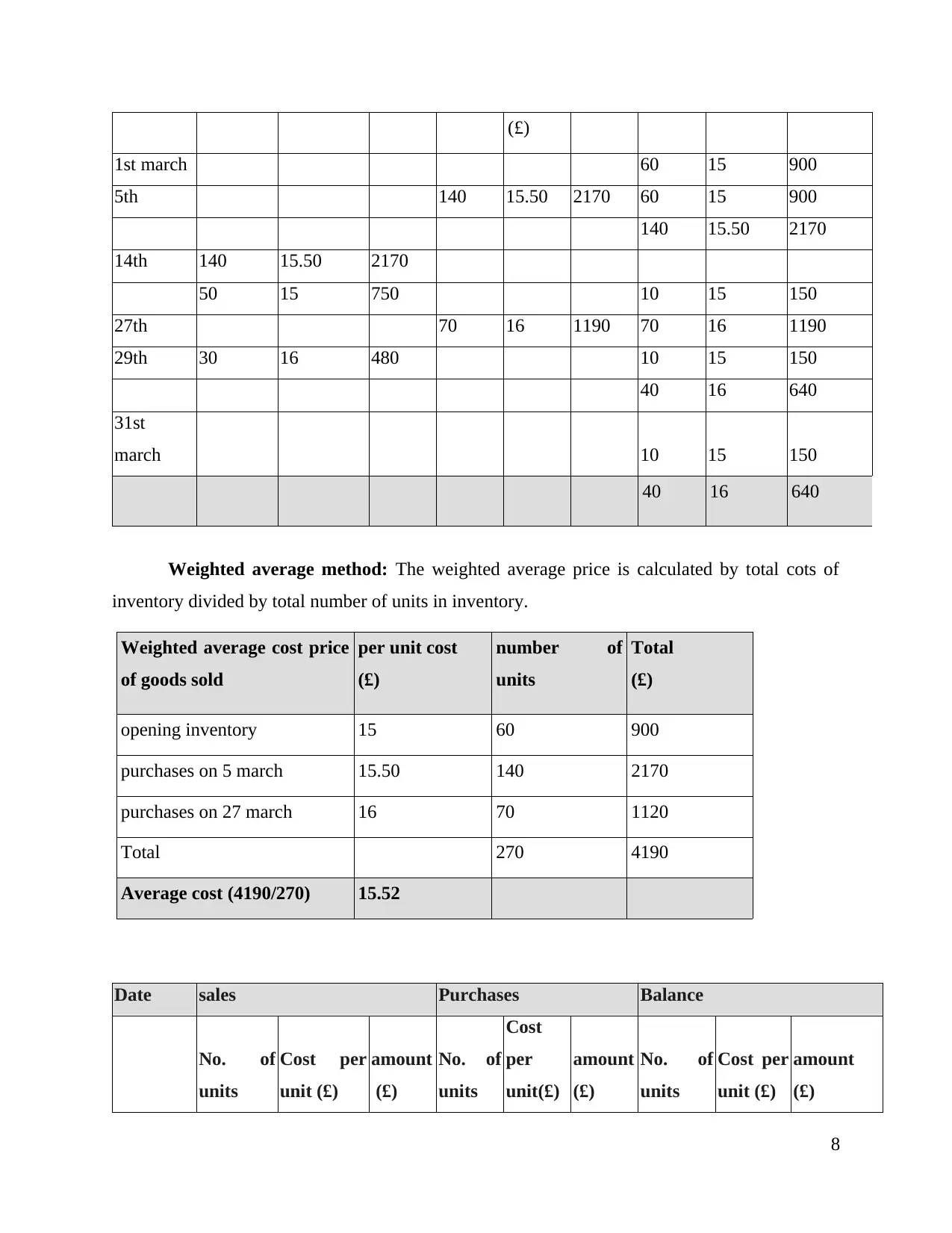

1st march 60 15 900

5th 140 15.50 2170 60 15 900

140 15.50 2170

14th 140 15.50 2170

50 15 750 10 15 150

27th 70 16 1190 70 16 1190

29th 30 16 480 10 15 150

40 16 640

31st

march 10 15 150

40 16 640

Weighted average method: The weighted average price is calculated by total cots of

inventory divided by total number of units in inventory.

Weighted average cost price

of goods sold

per unit cost

(£)

number of

units

Total

(£)

opening inventory 15 60 900

purchases on 5 march 15.50 140 2170

purchases on 27 march 16 70 1120

Total 270 4190

Average cost (4190/270) 15.52

Date sales Purchases Balance

No. of

units

Cost per

unit (£)

amount

(£)

No. of

units

Cost

per

unit(£)

amount

(£)

No. of

units

Cost per

unit (£)

amount

(£)

8

1st march 60 15 900

5th 140 15.50 2170 60 15 900

140 15.50 2170

14th 140 15.50 2170

50 15 750 10 15 150

27th 70 16 1190 70 16 1190

29th 30 16 480 10 15 150

40 16 640

31st

march 10 15 150

40 16 640

Weighted average method: The weighted average price is calculated by total cots of

inventory divided by total number of units in inventory.

Weighted average cost price

of goods sold

per unit cost

(£)

number of

units

Total

(£)

opening inventory 15 60 900

purchases on 5 march 15.50 140 2170

purchases on 27 march 16 70 1120

Total 270 4190

Average cost (4190/270) 15.52

Date sales Purchases Balance

No. of

units

Cost per

unit (£)

amount

(£)

No. of

units

Cost

per

unit(£)

amount

(£)

No. of

units

Cost per

unit (£)

amount

(£)

8

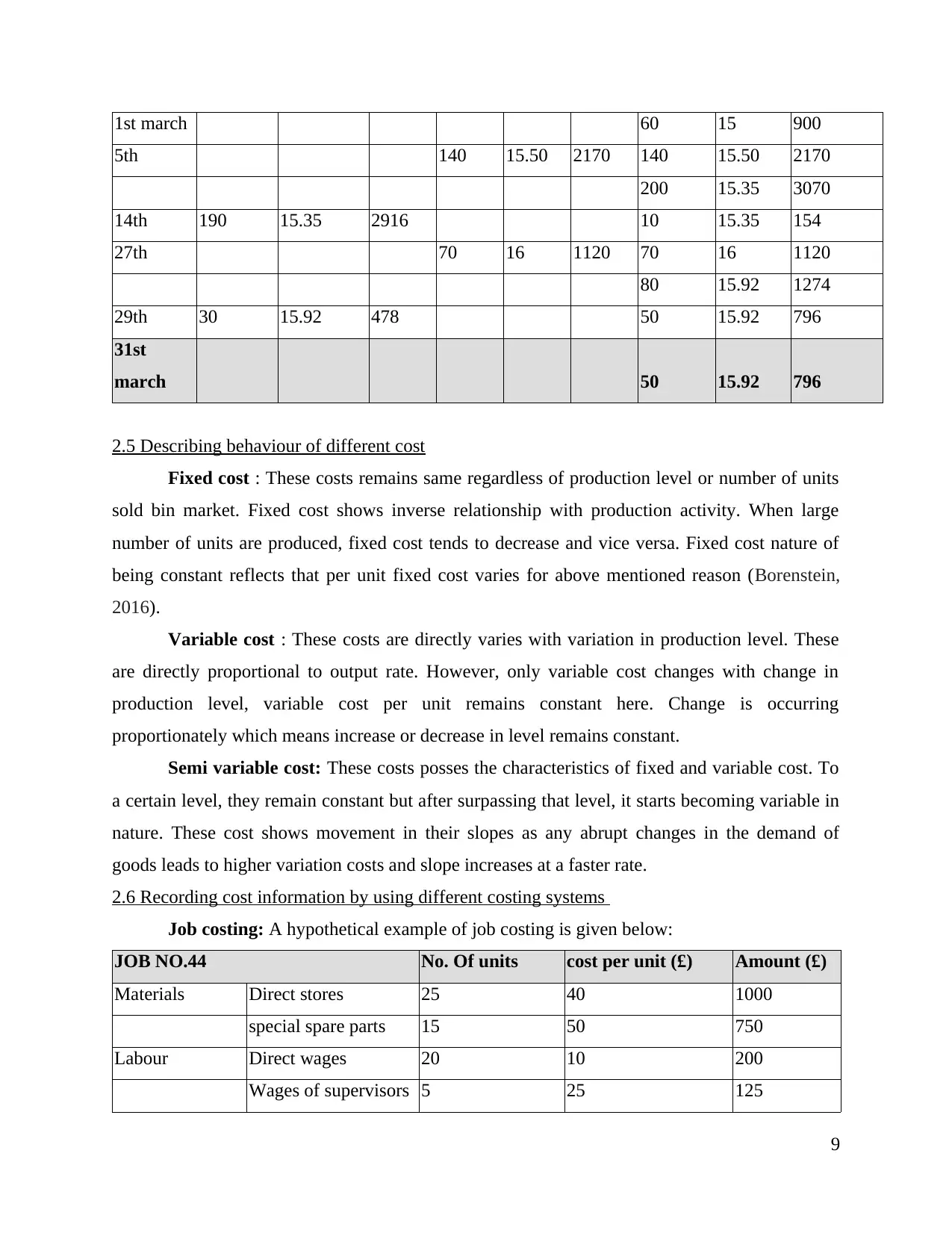

1st march 60 15 900

5th 140 15.50 2170 140 15.50 2170

200 15.35 3070

14th 190 15.35 2916 10 15.35 154

27th 70 16 1120 70 16 1120

80 15.92 1274

29th 30 15.92 478 50 15.92 796

31st

march 50 15.92 796

2.5 Describing behaviour of different cost

Fixed cost : These costs remains same regardless of production level or number of units

sold bin market. Fixed cost shows inverse relationship with production activity. When large

number of units are produced, fixed cost tends to decrease and vice versa. Fixed cost nature of

being constant reflects that per unit fixed cost varies for above mentioned reason (Borenstein,

2016).

Variable cost : These costs are directly varies with variation in production level. These

are directly proportional to output rate. However, only variable cost changes with change in

production level, variable cost per unit remains constant here. Change is occurring

proportionately which means increase or decrease in level remains constant.

Semi variable cost: These costs posses the characteristics of fixed and variable cost. To

a certain level, they remain constant but after surpassing that level, it starts becoming variable in

nature. These cost shows movement in their slopes as any abrupt changes in the demand of

goods leads to higher variation costs and slope increases at a faster rate.

2.6 Recording cost information by using different costing systems

Job costing: A hypothetical example of job costing is given below:

JOB NO.44 No. Of units cost per unit (£) Amount (£)

Materials Direct stores 25 40 1000

special spare parts 15 50 750

Labour Direct wages 20 10 200

Wages of supervisors 5 25 125

9

5th 140 15.50 2170 140 15.50 2170

200 15.35 3070

14th 190 15.35 2916 10 15.35 154

27th 70 16 1120 70 16 1120

80 15.92 1274

29th 30 15.92 478 50 15.92 796

31st

march 50 15.92 796

2.5 Describing behaviour of different cost

Fixed cost : These costs remains same regardless of production level or number of units

sold bin market. Fixed cost shows inverse relationship with production activity. When large

number of units are produced, fixed cost tends to decrease and vice versa. Fixed cost nature of

being constant reflects that per unit fixed cost varies for above mentioned reason (Borenstein,

2016).

Variable cost : These costs are directly varies with variation in production level. These

are directly proportional to output rate. However, only variable cost changes with change in

production level, variable cost per unit remains constant here. Change is occurring

proportionately which means increase or decrease in level remains constant.

Semi variable cost: These costs posses the characteristics of fixed and variable cost. To

a certain level, they remain constant but after surpassing that level, it starts becoming variable in

nature. These cost shows movement in their slopes as any abrupt changes in the demand of

goods leads to higher variation costs and slope increases at a faster rate.

2.6 Recording cost information by using different costing systems

Job costing: A hypothetical example of job costing is given below:

JOB NO.44 No. Of units cost per unit (£) Amount (£)

Materials Direct stores 25 40 1000

special spare parts 15 50 750

Labour Direct wages 20 10 200

Wages of supervisors 5 25 125

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.