Internal Reporting, Costing Systems, and Variance Analysis at M&S

VerifiedAdded on 2020/10/05

|18

|3247

|253

Report

AI Summary

This report provides a comprehensive analysis of costs and revenues, focusing on the case of Marks and Spencer (M&S). It begins with an introduction to revenue, cost of goods sold, and their relationship, setting the stage for an examination of M&S's internal reporting practices. The report delves into the purpose of internal reporting, the relationship between different costing systems (job, process, and activity-based costing), and the roles of responsibility, cost, profit, and investment centers within a firm. It then explores various cost classifications (fixed, variable, marginal, and distribution channel costs) and their applications. The report includes detailed cost information recording and analysis, covering material, labor, and expenses, and the different stages of inventory (raw materials, work-in-progress, and finished goods). It also examines overhead cost allocation and absorption rates, variance analysis, and the preparation of management reports. The report also covers the impact of changing activity levels on unit costs and factors influencing short and long-term decision-making. The report concludes with a summary of findings and references used.

Costs and Revenues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose of internal reporting and providing the accurate information ................................1

1.2 Relationship between different costing systems ..................................................................1

1.3 Responsibility, cost, profits and investment centres within firm .........................................2

1.4 Different types of cost classifications and its use in costing ................................................2

1.5 Differences between marginal and absorption costing ........................................................2

TASK 2............................................................................................................................................3

2.1 Record cost information for material, labour and expenses in costing procedures ..............3

2.2 Analysis cost information for material, labour and expenses in costing procedures ...........4

2.3 Various stage of inventory ...................................................................................................4

2.4 Using the method in value inventory ...................................................................................4

2.5 Behaviour of costs ................................................................................................................6

2.6 Using costing system for record information .......................................................................6

TASK 3............................................................................................................................................7

3.1 Attribute overhead costs to production and service cost centres in accordance with agreed

.....................................................................................................................................................7

3.2 Calculating overhead absorption rates in accordance with suitable bases. ..........................7

3.Prime cost.................................................................................................................................7

3.3 Adjustment for under or over recovered overhead cost........................................................8

3.4 Method of allocation, apportionments and absorption at regular intervals...........................8

3.5 Communicate with relevant staff to resolve in overhead cost data.......................................9

TASK 4 ...........................................................................................................................................9

4.1 Compare budget with actual costs ........................................................................................9

4.2 Analysis of variance for management reports ......................................................................9

4.3 Information for budget holders of any significant variance ...............................................10

4.4 Prepare management reports ..............................................................................................10

5.1 Estimate of future income and costs ..................................................................................10

5.2 Effect of changing activity level of unit costs ....................................................................11

5.3 Calculate effects of changing activity level on unit costs ..................................................11

5.4 Factors affecting short and long term decision making .....................................................13

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose of internal reporting and providing the accurate information ................................1

1.2 Relationship between different costing systems ..................................................................1

1.3 Responsibility, cost, profits and investment centres within firm .........................................2

1.4 Different types of cost classifications and its use in costing ................................................2

1.5 Differences between marginal and absorption costing ........................................................2

TASK 2............................................................................................................................................3

2.1 Record cost information for material, labour and expenses in costing procedures ..............3

2.2 Analysis cost information for material, labour and expenses in costing procedures ...........4

2.3 Various stage of inventory ...................................................................................................4

2.4 Using the method in value inventory ...................................................................................4

2.5 Behaviour of costs ................................................................................................................6

2.6 Using costing system for record information .......................................................................6

TASK 3............................................................................................................................................7

3.1 Attribute overhead costs to production and service cost centres in accordance with agreed

.....................................................................................................................................................7

3.2 Calculating overhead absorption rates in accordance with suitable bases. ..........................7

3.Prime cost.................................................................................................................................7

3.3 Adjustment for under or over recovered overhead cost........................................................8

3.4 Method of allocation, apportionments and absorption at regular intervals...........................8

3.5 Communicate with relevant staff to resolve in overhead cost data.......................................9

TASK 4 ...........................................................................................................................................9

4.1 Compare budget with actual costs ........................................................................................9

4.2 Analysis of variance for management reports ......................................................................9

4.3 Information for budget holders of any significant variance ...............................................10

4.4 Prepare management reports ..............................................................................................10

5.1 Estimate of future income and costs ..................................................................................10

5.2 Effect of changing activity level of unit costs ....................................................................11

5.3 Calculate effects of changing activity level on unit costs ..................................................11

5.4 Factors affecting short and long term decision making .....................................................13

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Revenue is the sum of money received by the organization through selling goods and

provided services during the particular time period. Cost of good sold are the direct costs

referable to the manufacturer of good sold by firm. The relationship between revenue, profits

and total cost which help in increasing proficiencies of organization (Lohri Camenzind and

Zurbrügg, 2014). This case study is based on Marks and Spencer (M&S). It is major British

multinational retailers that operates in selling clothing, home appliances and luxury food

products. This report will explain nature and role of costing system within the organization. It

will also record and analysis cost information and explain apportion cost according requirement

of company.

TASK 1

1.1 Purpose of internal reporting and providing the accurate information

The purpose of internal reporting is to make strategic decisions and monitor financial

health of M&S. Through it, the accurate information such as detailed sales info, employee turn

over and so on. The accurate internal information help to achieve purpose of internal reporting as

well as improve performance of M&S. This reports involve cash, variance analysis, budget etc.

Internal reporting includes collection of financial and operational information on regular basis.

The another purpose of internal reporting is planning and controlling of different level of

management within M&S (Mishan, 2015). Therefore, all level of manager should make sure that

giving the accurate information, so that, it helps to achieve the purpose of internal reporting in

the organization. This report are prepared by management accountant.

1.2 Relationship between different costing systems

Job costing System: Labour, material and overhead costs are accumulated for individual

job. The cost collection process is highly elaborated and labour intensive.

Process costing system: It is an accounting system that traces and combines direct costs

and allocates indirect costs of production process.

Activity based costing system: It was evolved in response to concern that overhead

costs are often assigned in proper manner.

Relationship: Both costing system are related with other. Job costing and process costing

system used by M&S to meet business needs, generation revenue and increase profitability of

1

Revenue is the sum of money received by the organization through selling goods and

provided services during the particular time period. Cost of good sold are the direct costs

referable to the manufacturer of good sold by firm. The relationship between revenue, profits

and total cost which help in increasing proficiencies of organization (Lohri Camenzind and

Zurbrügg, 2014). This case study is based on Marks and Spencer (M&S). It is major British

multinational retailers that operates in selling clothing, home appliances and luxury food

products. This report will explain nature and role of costing system within the organization. It

will also record and analysis cost information and explain apportion cost according requirement

of company.

TASK 1

1.1 Purpose of internal reporting and providing the accurate information

The purpose of internal reporting is to make strategic decisions and monitor financial

health of M&S. Through it, the accurate information such as detailed sales info, employee turn

over and so on. The accurate internal information help to achieve purpose of internal reporting as

well as improve performance of M&S. This reports involve cash, variance analysis, budget etc.

Internal reporting includes collection of financial and operational information on regular basis.

The another purpose of internal reporting is planning and controlling of different level of

management within M&S (Mishan, 2015). Therefore, all level of manager should make sure that

giving the accurate information, so that, it helps to achieve the purpose of internal reporting in

the organization. This report are prepared by management accountant.

1.2 Relationship between different costing systems

Job costing System: Labour, material and overhead costs are accumulated for individual

job. The cost collection process is highly elaborated and labour intensive.

Process costing system: It is an accounting system that traces and combines direct costs

and allocates indirect costs of production process.

Activity based costing system: It was evolved in response to concern that overhead

costs are often assigned in proper manner.

Relationship: Both costing system are related with other. Job costing and process costing

system used by M&S to meet business needs, generation revenue and increase profitability of

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company. Overhead costs are involved in job, process and activity based costing system which

used by M&S.

1.3 Responsibility, cost, profits and investment centres within firm

Responsibility Centres:

It is the part of firm for which manager has authority and responsibility. The manager of

responsibility centre can handle only costs that is referred to as cost centre in the M&S.

Cost Centres:

The costs can be traced and separated that is place of cost centre within organization. The

head of cost centre is responsible for costs only not for revenue or profits (Green and Léautier,

2014)

Profits Centres:

The costs and revenues are determined that is place of profits centres. The head of profits

centre responsible for revenues.

Investment Centres:

It is the place where determine the costs, revenues and capital investment within in the

company. The head of this centre responsible for revenues costs and capital expenses.

1.4 Different types of cost classifications and its use in costing

Fixed and Variable Cost:

Fixed cost is the cost of fixed inputs utilized in process of manufacturing within in the

company. These costs do not vary with change in volume of production. On other side, variable

cost is the cost of variable inputs in manufacturing process within M&S.

Distribution Channel Cost:

Expenditure are segregated into each of distribution channels utilised such as retail and

internet stores like M&S. The aggregate amount of each these categorizations ate then deducted

from related channel revenues to define channel profits.

Marginal Cost:

It means to cost of producing one additional unit of product in process of manufacture

within company. This cost utilises to take managerial decisions by management within M&S.

1.5 Differences between marginal and absorption costing

Criteria Marginal Costing Absorption Costing

Meaning The ascertaining total cost of As opposed to, allocation of total

2

used by M&S.

1.3 Responsibility, cost, profits and investment centres within firm

Responsibility Centres:

It is the part of firm for which manager has authority and responsibility. The manager of

responsibility centre can handle only costs that is referred to as cost centre in the M&S.

Cost Centres:

The costs can be traced and separated that is place of cost centre within organization. The

head of cost centre is responsible for costs only not for revenue or profits (Green and Léautier,

2014)

Profits Centres:

The costs and revenues are determined that is place of profits centres. The head of profits

centre responsible for revenues.

Investment Centres:

It is the place where determine the costs, revenues and capital investment within in the

company. The head of this centre responsible for revenues costs and capital expenses.

1.4 Different types of cost classifications and its use in costing

Fixed and Variable Cost:

Fixed cost is the cost of fixed inputs utilized in process of manufacturing within in the

company. These costs do not vary with change in volume of production. On other side, variable

cost is the cost of variable inputs in manufacturing process within M&S.

Distribution Channel Cost:

Expenditure are segregated into each of distribution channels utilised such as retail and

internet stores like M&S. The aggregate amount of each these categorizations ate then deducted

from related channel revenues to define channel profits.

Marginal Cost:

It means to cost of producing one additional unit of product in process of manufacture

within company. This cost utilises to take managerial decisions by management within M&S.

1.5 Differences between marginal and absorption costing

Criteria Marginal Costing Absorption Costing

Meaning The ascertaining total cost of As opposed to, allocation of total

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production is called as marginal

costing.

costs to centres cost in relation to

find total cost of production is

called as absorption costing.

Cost Identification It is method where variable cost are

considered as product cost and fixed

costs are regarded ad costs of the

period (Terpstra and Verbeeten, 2014).

As compared to, it is technique

where fixed and variable cost as

product cost.

Profitability The profit volume ration used to

measure the profitability.

Profitability gets affected, due to

situations of fixed cost.

Highlights Contribution per unit involve in

marginal cost that used in M&S.

Net profit per unit includes in

absorption cost.

TASK 2

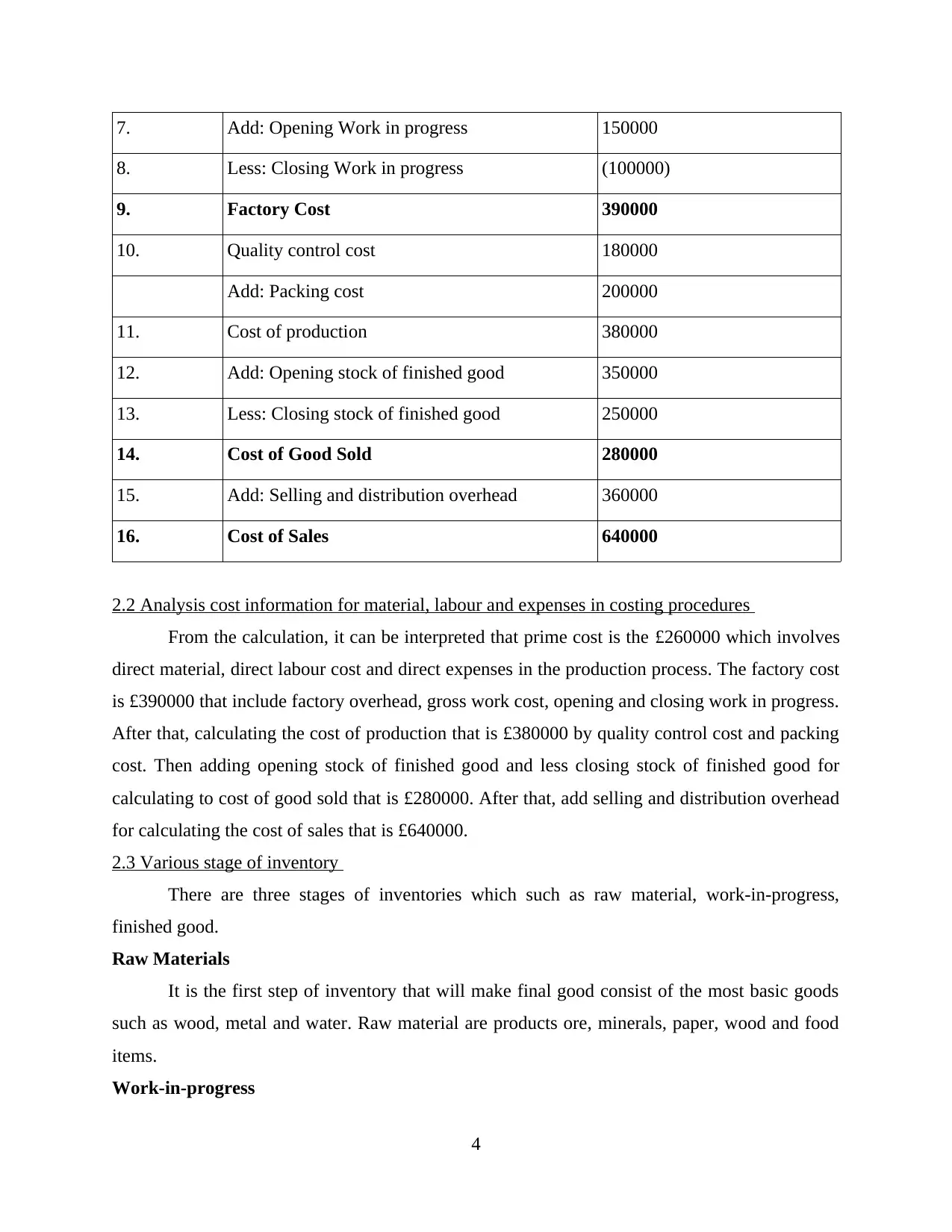

2.1 Record cost information for material, labour and expenses in costing procedures

Cost Sheet is the statement which is used by company for recording cost information for

material, labour and expenses in costing procedure which is used by M&S.

Cost Sheet

S. No. Particular Total Cost (£)

1. Opening stock material 300000

Add: Purchases 200000

Less: Closing Stock of Material (150000)

100000

2. Direct labour cost 90000

3. Direct Expenses 70000

4. Prime Cost 260000

5. Factory Overhead 80000

6. Gross Work cost 340000

3

costing.

costs to centres cost in relation to

find total cost of production is

called as absorption costing.

Cost Identification It is method where variable cost are

considered as product cost and fixed

costs are regarded ad costs of the

period (Terpstra and Verbeeten, 2014).

As compared to, it is technique

where fixed and variable cost as

product cost.

Profitability The profit volume ration used to

measure the profitability.

Profitability gets affected, due to

situations of fixed cost.

Highlights Contribution per unit involve in

marginal cost that used in M&S.

Net profit per unit includes in

absorption cost.

TASK 2

2.1 Record cost information for material, labour and expenses in costing procedures

Cost Sheet is the statement which is used by company for recording cost information for

material, labour and expenses in costing procedure which is used by M&S.

Cost Sheet

S. No. Particular Total Cost (£)

1. Opening stock material 300000

Add: Purchases 200000

Less: Closing Stock of Material (150000)

100000

2. Direct labour cost 90000

3. Direct Expenses 70000

4. Prime Cost 260000

5. Factory Overhead 80000

6. Gross Work cost 340000

3

7. Add: Opening Work in progress 150000

8. Less: Closing Work in progress (100000)

9. Factory Cost 390000

10. Quality control cost 180000

Add: Packing cost 200000

11. Cost of production 380000

12. Add: Opening stock of finished good 350000

13. Less: Closing stock of finished good 250000

14. Cost of Good Sold 280000

15. Add: Selling and distribution overhead 360000

16. Cost of Sales 640000

2.2 Analysis cost information for material, labour and expenses in costing procedures

From the calculation, it can be interpreted that prime cost is the £260000 which involves

direct material, direct labour cost and direct expenses in the production process. The factory cost

is £390000 that include factory overhead, gross work cost, opening and closing work in progress.

After that, calculating the cost of production that is £380000 by quality control cost and packing

cost. Then adding opening stock of finished good and less closing stock of finished good for

calculating to cost of good sold that is £280000. After that, add selling and distribution overhead

for calculating the cost of sales that is £640000.

2.3 Various stage of inventory

There are three stages of inventories which such as raw material, work-in-progress,

finished good.

Raw Materials

It is the first step of inventory that will make final good consist of the most basic goods

such as wood, metal and water. Raw material are products ore, minerals, paper, wood and food

items.

Work-in-progress

4

8. Less: Closing Work in progress (100000)

9. Factory Cost 390000

10. Quality control cost 180000

Add: Packing cost 200000

11. Cost of production 380000

12. Add: Opening stock of finished good 350000

13. Less: Closing stock of finished good 250000

14. Cost of Good Sold 280000

15. Add: Selling and distribution overhead 360000

16. Cost of Sales 640000

2.2 Analysis cost information for material, labour and expenses in costing procedures

From the calculation, it can be interpreted that prime cost is the £260000 which involves

direct material, direct labour cost and direct expenses in the production process. The factory cost

is £390000 that include factory overhead, gross work cost, opening and closing work in progress.

After that, calculating the cost of production that is £380000 by quality control cost and packing

cost. Then adding opening stock of finished good and less closing stock of finished good for

calculating to cost of good sold that is £280000. After that, add selling and distribution overhead

for calculating the cost of sales that is £640000.

2.3 Various stage of inventory

There are three stages of inventories which such as raw material, work-in-progress,

finished good.

Raw Materials

It is the first step of inventory that will make final good consist of the most basic goods

such as wood, metal and water. Raw material are products ore, minerals, paper, wood and food

items.

Work-in-progress

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is second stage of inventory that are pulled into process of creating final product which

is known work-in-progress. The costs linked with this stage such as cost of raw material, labour

and manufacturing cost involving overhead (Stubbs and Higgins, 2014).

Finished Goods

All the cost associated with productions involving raw material and work-in-progress

costs are transferred to third step of inventory which is called as finished goods.

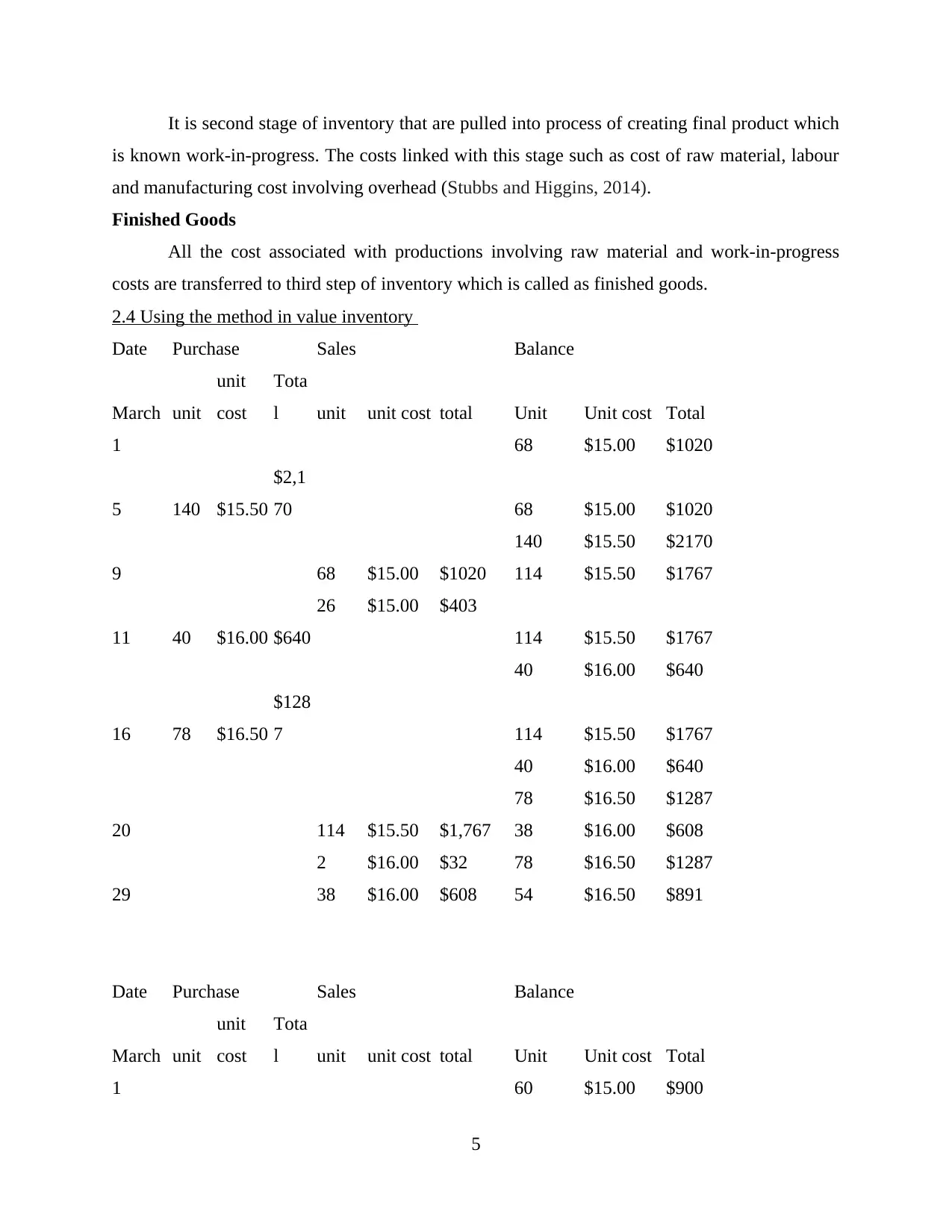

2.4 Using the method in value inventory

Date Purchase Sales Balance

March unit

unit

cost

Tota

l unit unit cost total Unit Unit cost Total

1 68 $15.00 $1020

5 140 $15.50

$2,1

70 68 $15.00 $1020

140 $15.50 $2170

9 68 $15.00 $1020 114 $15.50 $1767

26 $15.00 $403

11 40 $16.00 $640 114 $15.50 $1767

40 $16.00 $640

16 78 $16.50

$128

7 114 $15.50 $1767

40 $16.00 $640

78 $16.50 $1287

20 114 $15.50 $1,767 38 $16.00 $608

2 $16.00 $32 78 $16.50 $1287

29 38 $16.00 $608 54 $16.50 $891

Date Purchase Sales Balance

March unit

unit

cost

Tota

l unit unit cost total Unit Unit cost Total

1 60 $15.00 $900

5

is known work-in-progress. The costs linked with this stage such as cost of raw material, labour

and manufacturing cost involving overhead (Stubbs and Higgins, 2014).

Finished Goods

All the cost associated with productions involving raw material and work-in-progress

costs are transferred to third step of inventory which is called as finished goods.

2.4 Using the method in value inventory

Date Purchase Sales Balance

March unit

unit

cost

Tota

l unit unit cost total Unit Unit cost Total

1 68 $15.00 $1020

5 140 $15.50

$2,1

70 68 $15.00 $1020

140 $15.50 $2170

9 68 $15.00 $1020 114 $15.50 $1767

26 $15.00 $403

11 40 $16.00 $640 114 $15.50 $1767

40 $16.00 $640

16 78 $16.50

$128

7 114 $15.50 $1767

40 $16.00 $640

78 $16.50 $1287

20 114 $15.50 $1,767 38 $16.00 $608

2 $16.00 $32 78 $16.50 $1287

29 38 $16.00 $608 54 $16.50 $891

Date Purchase Sales Balance

March unit

unit

cost

Tota

l unit unit cost total Unit Unit cost Total

1 60 $15.00 $900

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 140 $15.50

$2,1

70 60 $15.00 $900

140 $15.50 $2170

14 140 $15.50 $2170 10 $15.00 $150

50 $15.00 $750

27 70 $16.00

$119

0 10 $15.00 $150

70 $16.00 $1120

29 30 $16.00 $480 10 $15.00 $150

40 $16.00 $640

31 10 $15.00 $150

40 $16.00 $640

Date Purchases Sales Balance

Unit

s

Unit

Cost

Tota

l Units

Unit

Cost Total Units Unit Cost Total

31/12/

99 60 $15.00 $900

5 140 $15.50

$2,1

70 60 $15.00 $900

140 $15.00

$2,17

0

200 $15.35 $3070

14 190 $15.35 $2916 10 $15.35 $154

27 70 $16.00

$1,1

20 10 $15.35 $154

70 $16.00 $1120

80 $15.92 $1274

29 30 $15.92 $478 50 $15.92 $796

31 50 $15.92 $796

6

$2,1

70 60 $15.00 $900

140 $15.50 $2170

14 140 $15.50 $2170 10 $15.00 $150

50 $15.00 $750

27 70 $16.00

$119

0 10 $15.00 $150

70 $16.00 $1120

29 30 $16.00 $480 10 $15.00 $150

40 $16.00 $640

31 10 $15.00 $150

40 $16.00 $640

Date Purchases Sales Balance

Unit

s

Unit

Cost

Tota

l Units

Unit

Cost Total Units Unit Cost Total

31/12/

99 60 $15.00 $900

5 140 $15.50

$2,1

70 60 $15.00 $900

140 $15.00

$2,17

0

200 $15.35 $3070

14 190 $15.35 $2916 10 $15.35 $154

27 70 $16.00

$1,1

20 10 $15.35 $154

70 $16.00 $1120

80 $15.92 $1274

29 30 $15.92 $478 50 $15.92 $796

31 50 $15.92 $796

6

2.5 Behaviour of costs

Fixed cost

It is cost that tends to be uninfluenced by changes in level of activity during given time of

period. The fixed cost remain constant in total regardless change in volume up to certain level of

output.

Variable cost

It changes in direct proportion to level of production. This refers increase total variable

cost when more unit are produced and decreased when producing less unit (Stubbs and Higgins,

2014).

Semi-variable cost

The fixed cost and variable cost have properties which is called as semi-variable cost.

This concept is utilized to task financial performance at various activity levels.

Stepped cost

It is the cost that does not change steadily with modification in activity volume but rather

at separate points.

2.6 Using costing system for record information

Job: It is used to compile costs at small-unit level. The result of this is discrete buckets of

info about each job.

Batch: It is bunch of costs incurred when group of produced goods and services. It is

considered to allot batch cost to individual units within batch.

Unit: It is total expenses incurred by firm to produce, store and sell one unit of particular

good and services.

Process : It is an accounting method that hint and compile direct cost, and allocates

indirect costs of production process (Abbott and et.al., 2016).

Services: The costing system used by services organization relating to customer charges.

TASK 3

3.1 Attribute overhead costs to production and service cost centres in accordance with agreed

Direct : Direct method is the part of method were overhead costing calculating directly

such as direct labour and cost material.

7

Fixed cost

It is cost that tends to be uninfluenced by changes in level of activity during given time of

period. The fixed cost remain constant in total regardless change in volume up to certain level of

output.

Variable cost

It changes in direct proportion to level of production. This refers increase total variable

cost when more unit are produced and decreased when producing less unit (Stubbs and Higgins,

2014).

Semi-variable cost

The fixed cost and variable cost have properties which is called as semi-variable cost.

This concept is utilized to task financial performance at various activity levels.

Stepped cost

It is the cost that does not change steadily with modification in activity volume but rather

at separate points.

2.6 Using costing system for record information

Job: It is used to compile costs at small-unit level. The result of this is discrete buckets of

info about each job.

Batch: It is bunch of costs incurred when group of produced goods and services. It is

considered to allot batch cost to individual units within batch.

Unit: It is total expenses incurred by firm to produce, store and sell one unit of particular

good and services.

Process : It is an accounting method that hint and compile direct cost, and allocates

indirect costs of production process (Abbott and et.al., 2016).

Services: The costing system used by services organization relating to customer charges.

TASK 3

3.1 Attribute overhead costs to production and service cost centres in accordance with agreed

Direct : Direct method is the part of method were overhead costing calculating directly

such as direct labour and cost material.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

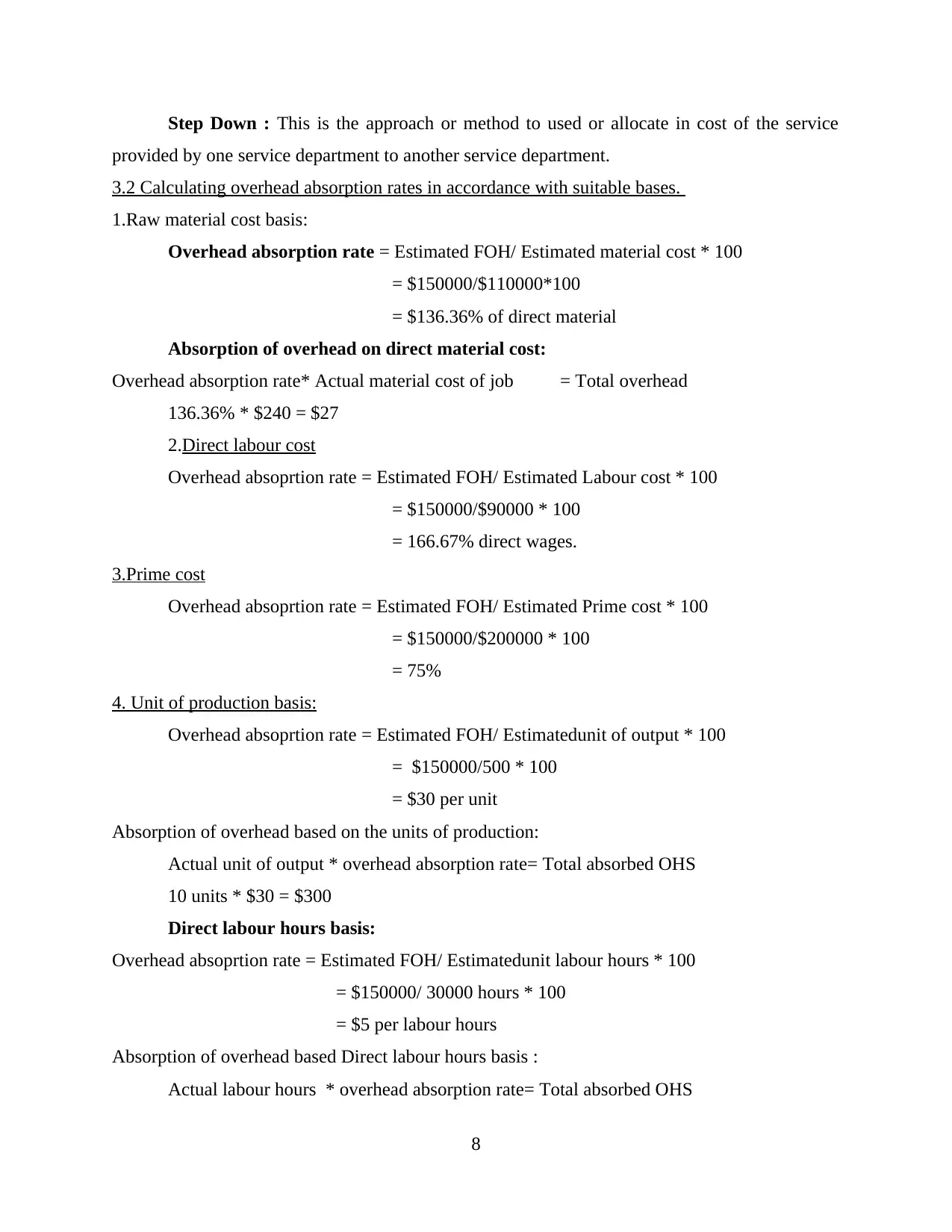

Step Down : This is the approach or method to used or allocate in cost of the service

provided by one service department to another service department.

3.2 Calculating overhead absorption rates in accordance with suitable bases.

1.Raw material cost basis:

Overhead absorption rate = Estimated FOH/ Estimated material cost * 100

= $150000/$110000*100

= $136.36% of direct material

Absorption of overhead on direct material cost:

Overhead absorption rate* Actual material cost of job = Total overhead

136.36% * $240 = $27

2.Direct labour cost

Overhead absoprtion rate = Estimated FOH/ Estimated Labour cost * 100

= $150000/$90000 * 100

= 166.67% direct wages.

3.Prime cost

Overhead absoprtion rate = Estimated FOH/ Estimated Prime cost * 100

= $150000/$200000 * 100

= 75%

4. Unit of production basis:

Overhead absoprtion rate = Estimated FOH/ Estimatedunit of output * 100

= $150000/500 * 100

= $30 per unit

Absorption of overhead based on the units of production:

Actual unit of output * overhead absorption rate= Total absorbed OHS

10 units * $30 = $300

Direct labour hours basis:

Overhead absoprtion rate = Estimated FOH/ Estimatedunit labour hours * 100

= $150000/ 30000 hours * 100

= $5 per labour hours

Absorption of overhead based Direct labour hours basis :

Actual labour hours * overhead absorption rate= Total absorbed OHS

8

provided by one service department to another service department.

3.2 Calculating overhead absorption rates in accordance with suitable bases.

1.Raw material cost basis:

Overhead absorption rate = Estimated FOH/ Estimated material cost * 100

= $150000/$110000*100

= $136.36% of direct material

Absorption of overhead on direct material cost:

Overhead absorption rate* Actual material cost of job = Total overhead

136.36% * $240 = $27

2.Direct labour cost

Overhead absoprtion rate = Estimated FOH/ Estimated Labour cost * 100

= $150000/$90000 * 100

= 166.67% direct wages.

3.Prime cost

Overhead absoprtion rate = Estimated FOH/ Estimated Prime cost * 100

= $150000/$200000 * 100

= 75%

4. Unit of production basis:

Overhead absoprtion rate = Estimated FOH/ Estimatedunit of output * 100

= $150000/500 * 100

= $30 per unit

Absorption of overhead based on the units of production:

Actual unit of output * overhead absorption rate= Total absorbed OHS

10 units * $30 = $300

Direct labour hours basis:

Overhead absoprtion rate = Estimated FOH/ Estimatedunit labour hours * 100

= $150000/ 30000 hours * 100

= $5 per labour hours

Absorption of overhead based Direct labour hours basis :

Actual labour hours * overhead absorption rate= Total absorbed OHS

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

63 hours * $5 = $315

Machine Hour basis :

Overhead absorption rate = Estimated FOH/ Estimated machine hours * 100

= $150000/ 25000 hours * 100

= $6 per machine hours

Absorption of overhead based on machine hours basis :

Actual machine hours * overhead absorption rate= Total absorbed OHS

44 hours * $6 = $ 264

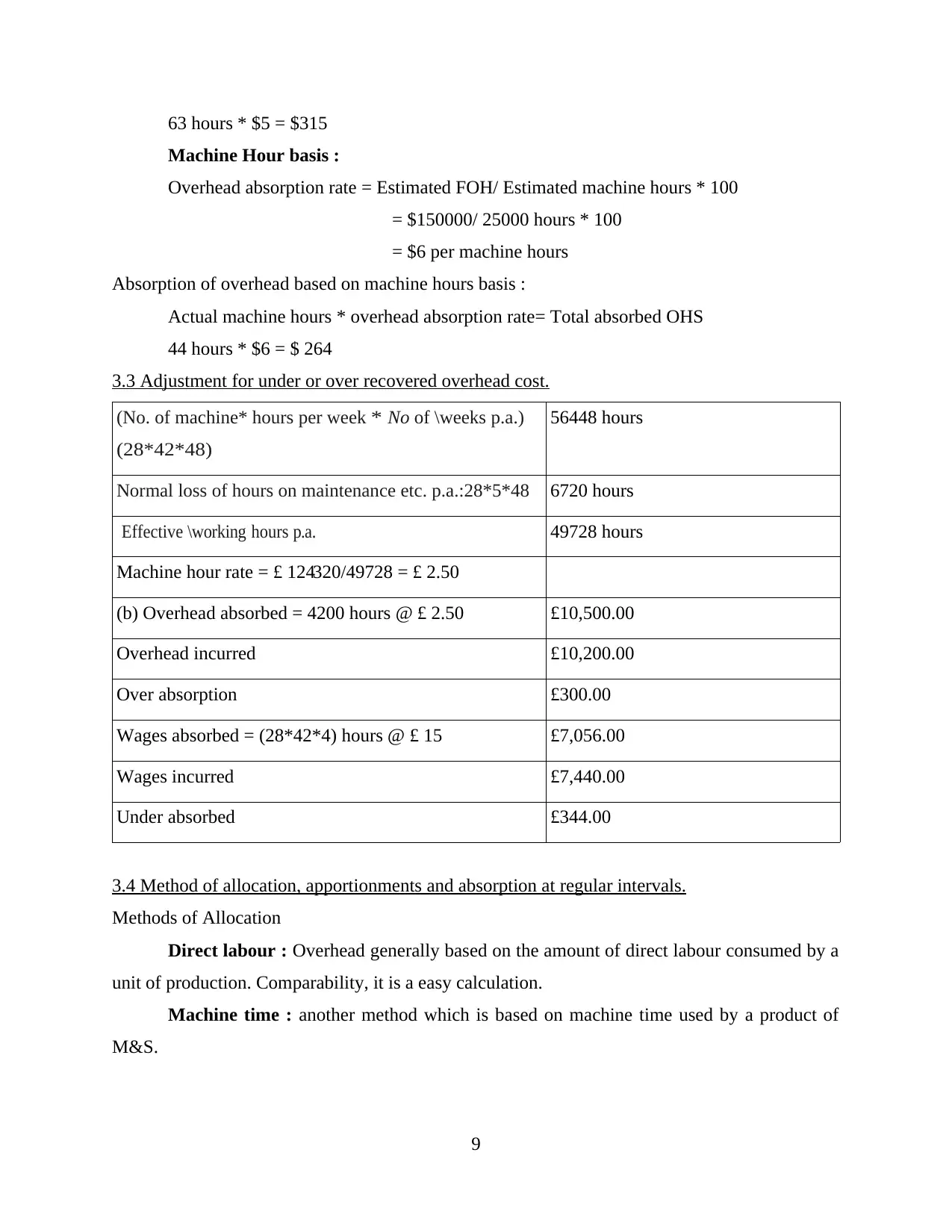

3.3 Adjustment for under or over recovered overhead cost.

(No. of machine* hours per week * No of \weeks p.a.)

(28*42*48)

56448 hours

Normal loss of hours on maintenance etc. p.a.:28*5*48 6720 hours

Effective \working hours p.a. 49728 hours

Machine hour rate = £ 124320/49728 = £ 2.50

(b) Overhead absorbed = 4200 hours @ £ 2.50 £10,500.00

Overhead incurred £10,200.00

Over absorption £300.00

Wages absorbed = (28*42*4) hours @ £ 15 £7,056.00

Wages incurred £7,440.00

Under absorbed £344.00

3.4 Method of allocation, apportionments and absorption at regular intervals.

Methods of Allocation

Direct labour : Overhead generally based on the amount of direct labour consumed by a

unit of production. Comparability, it is a easy calculation.

Machine time : another method which is based on machine time used by a product of

M&S.

9

Machine Hour basis :

Overhead absorption rate = Estimated FOH/ Estimated machine hours * 100

= $150000/ 25000 hours * 100

= $6 per machine hours

Absorption of overhead based on machine hours basis :

Actual machine hours * overhead absorption rate= Total absorbed OHS

44 hours * $6 = $ 264

3.3 Adjustment for under or over recovered overhead cost.

(No. of machine* hours per week * No of \weeks p.a.)

(28*42*48)

56448 hours

Normal loss of hours on maintenance etc. p.a.:28*5*48 6720 hours

Effective \working hours p.a. 49728 hours

Machine hour rate = £ 124320/49728 = £ 2.50

(b) Overhead absorbed = 4200 hours @ £ 2.50 £10,500.00

Overhead incurred £10,200.00

Over absorption £300.00

Wages absorbed = (28*42*4) hours @ £ 15 £7,056.00

Wages incurred £7,440.00

Under absorbed £344.00

3.4 Method of allocation, apportionments and absorption at regular intervals.

Methods of Allocation

Direct labour : Overhead generally based on the amount of direct labour consumed by a

unit of production. Comparability, it is a easy calculation.

Machine time : another method which is based on machine time used by a product of

M&S.

9

Square footage : this cost is separate cost out of those expenses related to the inventory

storage (Mio, Marco and Pauluzzo, 2016).

Methods of apportionments : Method of Apportionments is describing fair division. In

which company divides among places.

Method of Absorption : Absorption is the method which refers to charging as per the

individual products or job.

3.5 Communicate with relevant staff to resolve in overhead cost data.

In order to execute the data or project requirement, in order to control the unnecessary

expenses or cost. Manager of M&S needs to adopt indispensable tool to manage and other

participants in the construction process.

TASK 4

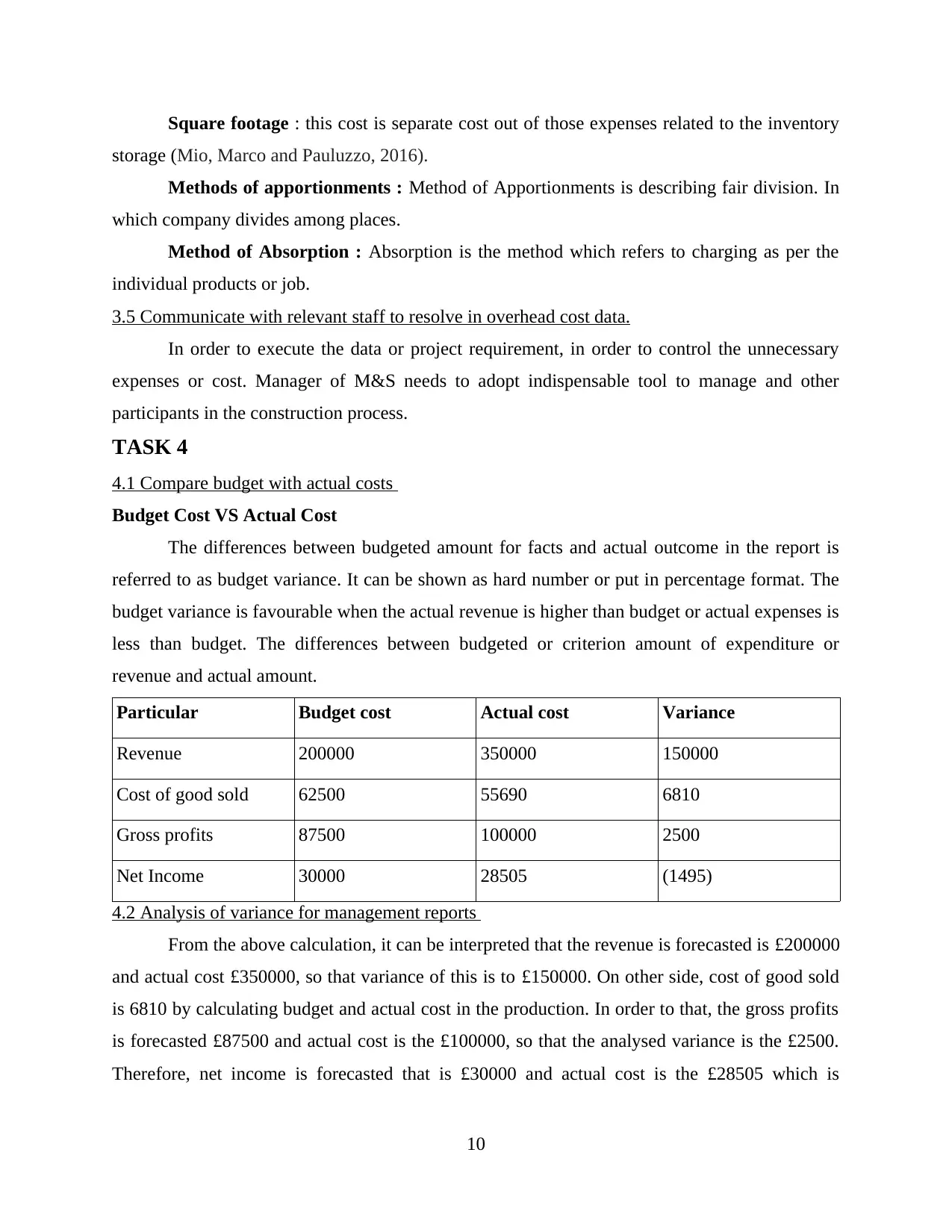

4.1 Compare budget with actual costs

Budget Cost VS Actual Cost

The differences between budgeted amount for facts and actual outcome in the report is

referred to as budget variance. It can be shown as hard number or put in percentage format. The

budget variance is favourable when the actual revenue is higher than budget or actual expenses is

less than budget. The differences between budgeted or criterion amount of expenditure or

revenue and actual amount.

Particular Budget cost Actual cost Variance

Revenue 200000 350000 150000

Cost of good sold 62500 55690 6810

Gross profits 87500 100000 2500

Net Income 30000 28505 (1495)

4.2 Analysis of variance for management reports

From the above calculation, it can be interpreted that the revenue is forecasted is £200000

and actual cost £350000, so that variance of this is to £150000. On other side, cost of good sold

is 6810 by calculating budget and actual cost in the production. In order to that, the gross profits

is forecasted £87500 and actual cost is the £100000, so that the analysed variance is the £2500.

Therefore, net income is forecasted that is £30000 and actual cost is the £28505 which is

10

storage (Mio, Marco and Pauluzzo, 2016).

Methods of apportionments : Method of Apportionments is describing fair division. In

which company divides among places.

Method of Absorption : Absorption is the method which refers to charging as per the

individual products or job.

3.5 Communicate with relevant staff to resolve in overhead cost data.

In order to execute the data or project requirement, in order to control the unnecessary

expenses or cost. Manager of M&S needs to adopt indispensable tool to manage and other

participants in the construction process.

TASK 4

4.1 Compare budget with actual costs

Budget Cost VS Actual Cost

The differences between budgeted amount for facts and actual outcome in the report is

referred to as budget variance. It can be shown as hard number or put in percentage format. The

budget variance is favourable when the actual revenue is higher than budget or actual expenses is

less than budget. The differences between budgeted or criterion amount of expenditure or

revenue and actual amount.

Particular Budget cost Actual cost Variance

Revenue 200000 350000 150000

Cost of good sold 62500 55690 6810

Gross profits 87500 100000 2500

Net Income 30000 28505 (1495)

4.2 Analysis of variance for management reports

From the above calculation, it can be interpreted that the revenue is forecasted is £200000

and actual cost £350000, so that variance of this is to £150000. On other side, cost of good sold

is 6810 by calculating budget and actual cost in the production. In order to that, the gross profits

is forecasted £87500 and actual cost is the £100000, so that the analysed variance is the £2500.

Therefore, net income is forecasted that is £30000 and actual cost is the £28505 which is

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.