Unit 13: Costs and Revenues Report - Marks and Spencer Analysis

VerifiedAdded on 2021/01/01

|19

|3336

|51

Report

AI Summary

This report provides a comprehensive analysis of costs and revenues, focusing on the context of Marks and Spencer. It begins by exploring the purpose of internal reporting and the relationship between various costing systems, including historical, absorption, and direct costing. The report then delves into responsibility centers, cost classifications, and the differences between marginal and absorption costing. The core of the report includes detailed cost information for materials, labor, and expenses, along with an examination of inventory valuation methods (FIFO, LIFO, weighted average) and cost behavior. It also covers costing systems like job, batch, unit, process, and service costing. The report further addresses overhead allocation, absorption rates, and variance analysis, including budget versus actual costs. Finally, it touches on the preparation of future income and cost estimates for decision-making and factors affecting short-term and long-term decision making.

Unit 13 Costs and revenues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

1.1 Purpose of internal reporting and providing accurate information to management..............1

1.2 Relationship between various costing systems ....................................................................1

1.3 Responsibility centres, cost centres, profit centres and investment centre...........................2

1.4 Characteristics in different types of cost classifications and their use in costing.................2

1.5 Difference between marginal and absorption costing...........................................................3

LO 2.................................................................................................................................................3

2.1 Cost information for material, labour and expenses in accordance with organisation's

costing procedures.......................................................................................................................3

2.2 Cost information for material, labour and expenses in accordance with organisation's

costing procedures.......................................................................................................................4

2.3 Various stages of inventory...................................................................................................4

2.4 Value inventory with FIFO, LIFO and weighted average ...................................................5

2.5 Describe behaviour of different costs such as fixed, variable, semi-variable and stepped...8

2.6 Record cost information with using job, batch, unit, process and service costing systems..8

LO 3.................................................................................................................................................9

3.1 Attribute overhead costs to production and service cost centres in accordance with agreed

bases............................................................................................................................................9

3.2 Calculate overhead absorption rates in accordance with suitable bases of absorption such

as machine hours and labour hours.............................................................................................9

3.Prime cost.................................................................................................................................9

3.3 Make adjustment for under and over recovered overhead costs in accordance with

established procedures..............................................................................................................10

3.4 Review methods of allocation, apportionment and absorption at regular intervals with

implement agreed changes to methods.....................................................................................11

3.5 Communicate with relevant staff to resolve queries...........................................................11

LO 4...............................................................................................................................................12

4.1 Compare budget costs with actual costs and noting any variances.....................................12

4.2 Analyse variance for management reports..........................................................................12

4.3 Provide information for budget holders of any significant variance, making valid

suggestions for remedial actions...............................................................................................12

4.4 Prepare management reports in appropriate format with required timescales....................13

LO 5...............................................................................................................................................13

5.1 Prepare estimates of future income and costs for decision making....................................13

5.2 Effect of changing activities levels on unit costs................................................................13

5.3 Calculate effect of changing activity levels on unit costs...................................................14

5.4 Factors affecting short term and long term decision making..............................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

1.1 Purpose of internal reporting and providing accurate information to management..............1

1.2 Relationship between various costing systems ....................................................................1

1.3 Responsibility centres, cost centres, profit centres and investment centre...........................2

1.4 Characteristics in different types of cost classifications and their use in costing.................2

1.5 Difference between marginal and absorption costing...........................................................3

LO 2.................................................................................................................................................3

2.1 Cost information for material, labour and expenses in accordance with organisation's

costing procedures.......................................................................................................................3

2.2 Cost information for material, labour and expenses in accordance with organisation's

costing procedures.......................................................................................................................4

2.3 Various stages of inventory...................................................................................................4

2.4 Value inventory with FIFO, LIFO and weighted average ...................................................5

2.5 Describe behaviour of different costs such as fixed, variable, semi-variable and stepped...8

2.6 Record cost information with using job, batch, unit, process and service costing systems..8

LO 3.................................................................................................................................................9

3.1 Attribute overhead costs to production and service cost centres in accordance with agreed

bases............................................................................................................................................9

3.2 Calculate overhead absorption rates in accordance with suitable bases of absorption such

as machine hours and labour hours.............................................................................................9

3.Prime cost.................................................................................................................................9

3.3 Make adjustment for under and over recovered overhead costs in accordance with

established procedures..............................................................................................................10

3.4 Review methods of allocation, apportionment and absorption at regular intervals with

implement agreed changes to methods.....................................................................................11

3.5 Communicate with relevant staff to resolve queries...........................................................11

LO 4...............................................................................................................................................12

4.1 Compare budget costs with actual costs and noting any variances.....................................12

4.2 Analyse variance for management reports..........................................................................12

4.3 Provide information for budget holders of any significant variance, making valid

suggestions for remedial actions...............................................................................................12

4.4 Prepare management reports in appropriate format with required timescales....................13

LO 5...............................................................................................................................................13

5.1 Prepare estimates of future income and costs for decision making....................................13

5.2 Effect of changing activities levels on unit costs................................................................13

5.3 Calculate effect of changing activity levels on unit costs...................................................14

5.4 Factors affecting short term and long term decision making..............................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

In every business, revenue generated with generated product equals to the costs which

incurred in producing, selling and delivering products to ultimate customers. Break even analysis

blends with cost and revenue analysis that assists to determine new product or services to solve

financial sense (Ghiyasi, 2017). Present study based on Marks and Spencer which deals in retail

sector business. It is British multinational retailer which specialise products in selling of

clothing, home products and luxury food.

For gaining insight information of the present study, it covers relationship between

different costing systems. Furthermore, Value inventory also measure with LIFO, FIFO and

weighted average method. Moreover, it provides description of allocation, apportionment and

absorption at regular intervals with implement agreed changes to methods. At last, factors

identifying that affect short and long term decision making.

LO 1

1.1 Purpose of internal reporting and providing accurate information to management

In the Marks and Spencer, internal reporting consider important role which involves

compilation of financial and operational information on frequent basis. It is distributed in the

business to improve performances. It helps to provide accurate information to management

which includes expense trends, failure rates, detailed sales data, etc. (Shepherd, 2015). Objective

of financial reporting has been analysed and accomplish purpose to examine resources to manage

enterprise. It is also important to provide information regarding financial position, performance

and changes in enterprise. Economic decisions also taken to management to accomplish goals

and objectives.

1.2 Relationship between various costing systems

There are different types of costing systems that accumulate information based on

effective approach that mixes and matches to meet with needs. Following are different costing

systems: Historical costing: In this type of costing system, costs ascertained after it is incurred.

Main objective to ascertain cost which occur in the past. In Marks and Spencer,

accumulation of cost incurred in systematic manner. Hence, actual figures compared

when standards develop (Nguyen, 2018).

1

In every business, revenue generated with generated product equals to the costs which

incurred in producing, selling and delivering products to ultimate customers. Break even analysis

blends with cost and revenue analysis that assists to determine new product or services to solve

financial sense (Ghiyasi, 2017). Present study based on Marks and Spencer which deals in retail

sector business. It is British multinational retailer which specialise products in selling of

clothing, home products and luxury food.

For gaining insight information of the present study, it covers relationship between

different costing systems. Furthermore, Value inventory also measure with LIFO, FIFO and

weighted average method. Moreover, it provides description of allocation, apportionment and

absorption at regular intervals with implement agreed changes to methods. At last, factors

identifying that affect short and long term decision making.

LO 1

1.1 Purpose of internal reporting and providing accurate information to management

In the Marks and Spencer, internal reporting consider important role which involves

compilation of financial and operational information on frequent basis. It is distributed in the

business to improve performances. It helps to provide accurate information to management

which includes expense trends, failure rates, detailed sales data, etc. (Shepherd, 2015). Objective

of financial reporting has been analysed and accomplish purpose to examine resources to manage

enterprise. It is also important to provide information regarding financial position, performance

and changes in enterprise. Economic decisions also taken to management to accomplish goals

and objectives.

1.2 Relationship between various costing systems

There are different types of costing systems that accumulate information based on

effective approach that mixes and matches to meet with needs. Following are different costing

systems: Historical costing: In this type of costing system, costs ascertained after it is incurred.

Main objective to ascertain cost which occur in the past. In Marks and Spencer,

accumulation of cost incurred in systematic manner. Hence, actual figures compared

when standards develop (Nguyen, 2018).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption costing: Under this costing, all fixed and variable costs allotted with cost unit

and total overheads that absorbed as per activity level. In this system, Marks and Spencer

consider fixed manufacturing overhead that are allocated in stock valuation.

Direct costing: In this aspect, method of costing included in which product is charged

with cost which vary with volume. In Marks and Spencer, variable and direct costs

included such as direct material, direct labour and variable manufacturing expenses

(Weisbach, Heme and Nou, 2018).

In respect to consider relationship between these costing, it can be stated that main

objectives of all costing is to set future price of product. Furthermore, it is also used for stock

valuation that helps to charge price to gain revenue and ascertained traditional form of cost

ascertainment.

1.3 Responsibility centres, cost centres, profit centres and investment centre

Following are different centres in Marks and Spencer: Responsibility centre: Responsibility centre is organisational unit that headed by manager

and responsible for different activities and results. In this aspect, Marks and Spencer must

take responsibility accounting which included revenues and cost information that are

collected and reported by responsibility centres. Cost centre: Cost centre is a part of an organisation in which costs may be charged for

accomplish accounting purposes (Yang and Chen, 2018). Profit centre: Profit centre is a part of an organisation with assignable revenues and cost

for ascertainable profitability.

Investment centre: Investment centre is a classification which used in the enterprise and

essential element to measure its use of capital in term of raw costs or profits.

1.4 Characteristics in different types of cost classifications and their use in costing

In different types of cost classification, costing considered arriving at a company's

contribution. These types of information have been used for break even analysis. Fixed and variable costs: In Marks and Spencer, expenses separated into different

aspects such as variable and fixed cost. Revenue can be contributes as margin with

information that is used for break even analysis (Bai, Chen and Xu, 2017). Departmental costs: Expenses are assigned to Marks and Spencer which is responsible

for staff. This information, trend to examine ability.

2

and total overheads that absorbed as per activity level. In this system, Marks and Spencer

consider fixed manufacturing overhead that are allocated in stock valuation.

Direct costing: In this aspect, method of costing included in which product is charged

with cost which vary with volume. In Marks and Spencer, variable and direct costs

included such as direct material, direct labour and variable manufacturing expenses

(Weisbach, Heme and Nou, 2018).

In respect to consider relationship between these costing, it can be stated that main

objectives of all costing is to set future price of product. Furthermore, it is also used for stock

valuation that helps to charge price to gain revenue and ascertained traditional form of cost

ascertainment.

1.3 Responsibility centres, cost centres, profit centres and investment centre

Following are different centres in Marks and Spencer: Responsibility centre: Responsibility centre is organisational unit that headed by manager

and responsible for different activities and results. In this aspect, Marks and Spencer must

take responsibility accounting which included revenues and cost information that are

collected and reported by responsibility centres. Cost centre: Cost centre is a part of an organisation in which costs may be charged for

accomplish accounting purposes (Yang and Chen, 2018). Profit centre: Profit centre is a part of an organisation with assignable revenues and cost

for ascertainable profitability.

Investment centre: Investment centre is a classification which used in the enterprise and

essential element to measure its use of capital in term of raw costs or profits.

1.4 Characteristics in different types of cost classifications and their use in costing

In different types of cost classification, costing considered arriving at a company's

contribution. These types of information have been used for break even analysis. Fixed and variable costs: In Marks and Spencer, expenses separated into different

aspects such as variable and fixed cost. Revenue can be contributes as margin with

information that is used for break even analysis (Bai, Chen and Xu, 2017). Departmental costs: Expenses are assigned to Marks and Spencer which is responsible

for staff. This information, trend to examine ability.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

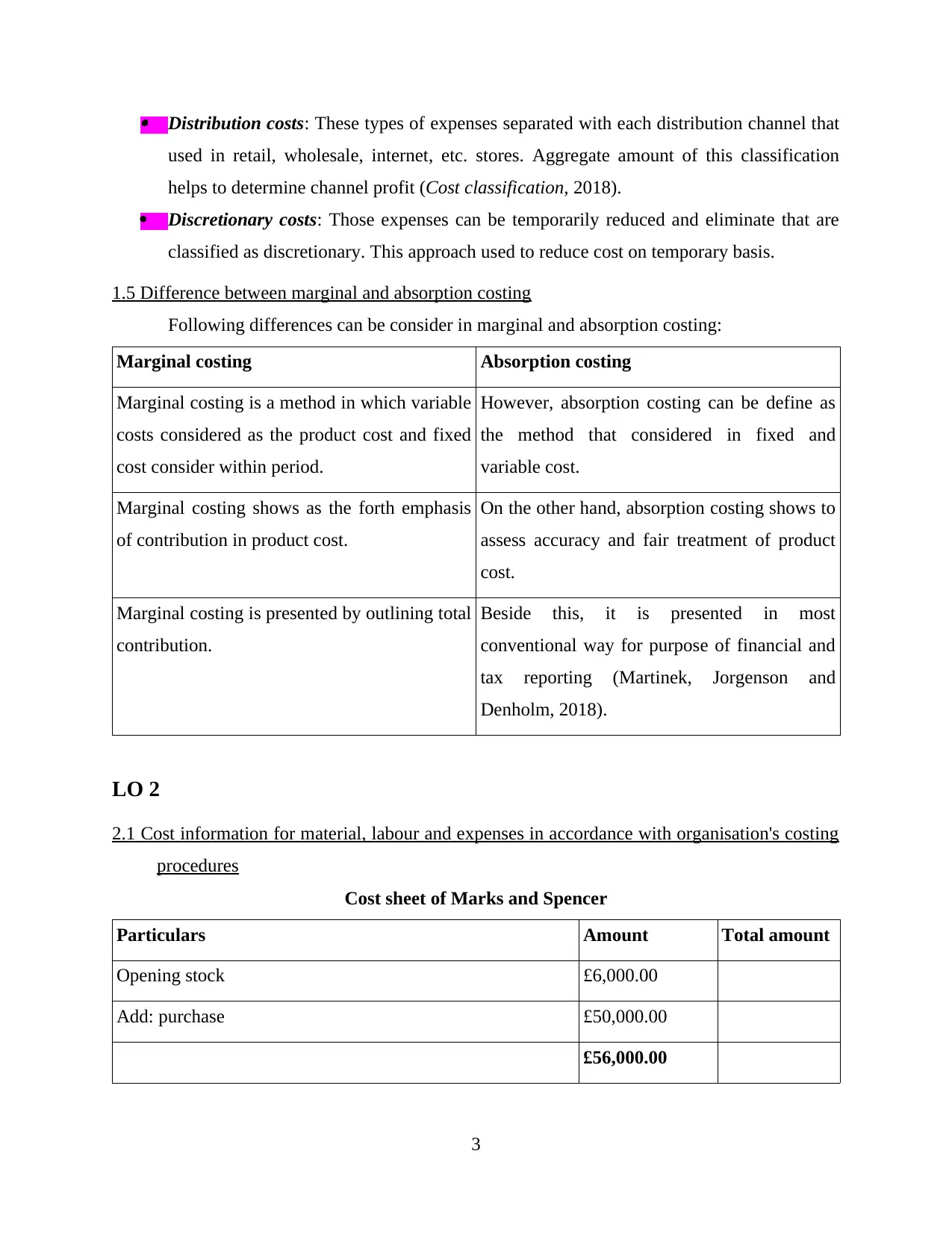

Distribution costs: These types of expenses separated with each distribution channel that

used in retail, wholesale, internet, etc. stores. Aggregate amount of this classification

helps to determine channel profit (Cost classification, 2018).

Discretionary costs: Those expenses can be temporarily reduced and eliminate that are

classified as discretionary. This approach used to reduce cost on temporary basis.

1.5 Difference between marginal and absorption costing

Following differences can be consider in marginal and absorption costing:

Marginal costing Absorption costing

Marginal costing is a method in which variable

costs considered as the product cost and fixed

cost consider within period.

However, absorption costing can be define as

the method that considered in fixed and

variable cost.

Marginal costing shows as the forth emphasis

of contribution in product cost.

On the other hand, absorption costing shows to

assess accuracy and fair treatment of product

cost.

Marginal costing is presented by outlining total

contribution.

Beside this, it is presented in most

conventional way for purpose of financial and

tax reporting (Martinek, Jorgenson and

Denholm, 2018).

LO 2

2.1 Cost information for material, labour and expenses in accordance with organisation's costing

procedures

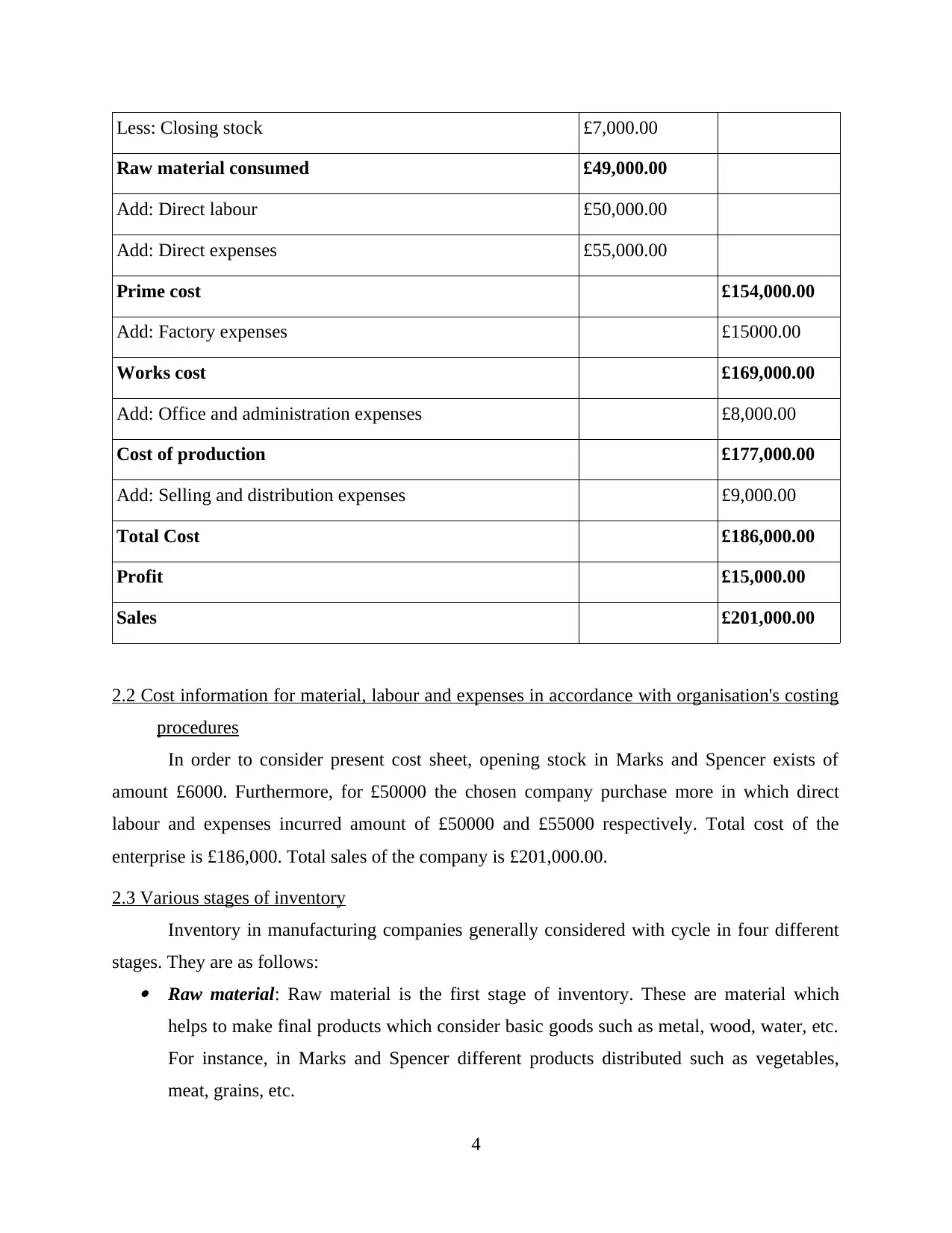

Cost sheet of Marks and Spencer

Particulars Amount Total amount

Opening stock £6,000.00

Add: purchase £50,000.00

£56,000.00

3

used in retail, wholesale, internet, etc. stores. Aggregate amount of this classification

helps to determine channel profit (Cost classification, 2018).

Discretionary costs: Those expenses can be temporarily reduced and eliminate that are

classified as discretionary. This approach used to reduce cost on temporary basis.

1.5 Difference between marginal and absorption costing

Following differences can be consider in marginal and absorption costing:

Marginal costing Absorption costing

Marginal costing is a method in which variable

costs considered as the product cost and fixed

cost consider within period.

However, absorption costing can be define as

the method that considered in fixed and

variable cost.

Marginal costing shows as the forth emphasis

of contribution in product cost.

On the other hand, absorption costing shows to

assess accuracy and fair treatment of product

cost.

Marginal costing is presented by outlining total

contribution.

Beside this, it is presented in most

conventional way for purpose of financial and

tax reporting (Martinek, Jorgenson and

Denholm, 2018).

LO 2

2.1 Cost information for material, labour and expenses in accordance with organisation's costing

procedures

Cost sheet of Marks and Spencer

Particulars Amount Total amount

Opening stock £6,000.00

Add: purchase £50,000.00

£56,000.00

3

Less: Closing stock £7,000.00

Raw material consumed £49,000.00

Add: Direct labour £50,000.00

Add: Direct expenses £55,000.00

Prime cost £154,000.00

Add: Factory expenses £15000.00

Works cost £169,000.00

Add: Office and administration expenses £8,000.00

Cost of production £177,000.00

Add: Selling and distribution expenses £9,000.00

Total Cost £186,000.00

Profit £15,000.00

Sales £201,000.00

2.2 Cost information for material, labour and expenses in accordance with organisation's costing

procedures

In order to consider present cost sheet, opening stock in Marks and Spencer exists of

amount £6000. Furthermore, for £50000 the chosen company purchase more in which direct

labour and expenses incurred amount of £50000 and £55000 respectively. Total cost of the

enterprise is £186,000. Total sales of the company is £201,000.00.

2.3 Various stages of inventory

Inventory in manufacturing companies generally considered with cycle in four different

stages. They are as follows: Raw material: Raw material is the first stage of inventory. These are material which

helps to make final products which consider basic goods such as metal, wood, water, etc.

For instance, in Marks and Spencer different products distributed such as vegetables,

meat, grains, etc.

4

Raw material consumed £49,000.00

Add: Direct labour £50,000.00

Add: Direct expenses £55,000.00

Prime cost £154,000.00

Add: Factory expenses £15000.00

Works cost £169,000.00

Add: Office and administration expenses £8,000.00

Cost of production £177,000.00

Add: Selling and distribution expenses £9,000.00

Total Cost £186,000.00

Profit £15,000.00

Sales £201,000.00

2.2 Cost information for material, labour and expenses in accordance with organisation's costing

procedures

In order to consider present cost sheet, opening stock in Marks and Spencer exists of

amount £6000. Furthermore, for £50000 the chosen company purchase more in which direct

labour and expenses incurred amount of £50000 and £55000 respectively. Total cost of the

enterprise is £186,000. Total sales of the company is £201,000.00.

2.3 Various stages of inventory

Inventory in manufacturing companies generally considered with cycle in four different

stages. They are as follows: Raw material: Raw material is the first stage of inventory. These are material which

helps to make final products which consider basic goods such as metal, wood, water, etc.

For instance, in Marks and Spencer different products distributed such as vegetables,

meat, grains, etc.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

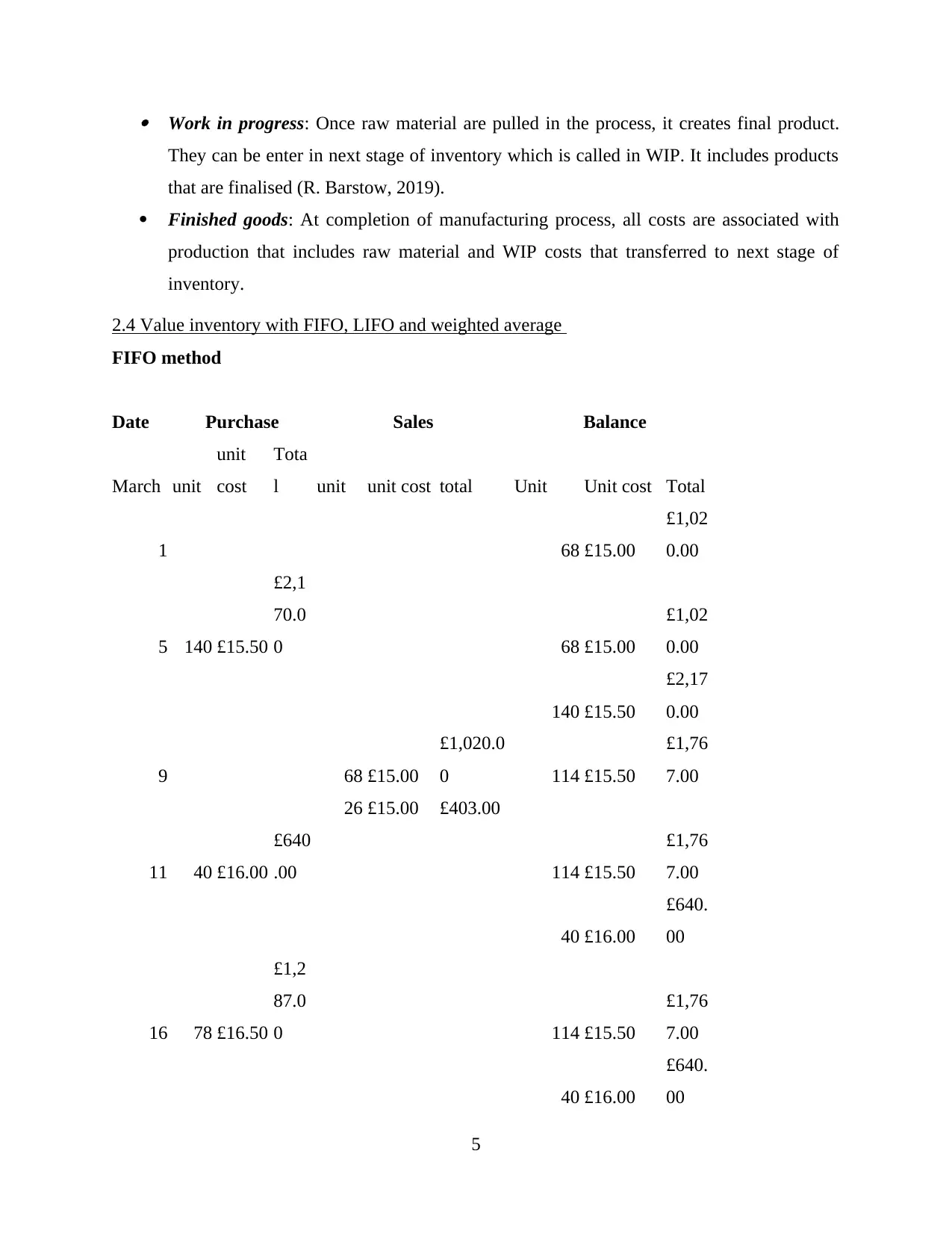

Work in progress: Once raw material are pulled in the process, it creates final product.

They can be enter in next stage of inventory which is called in WIP. It includes products

that are finalised (R. Barstow, 2019).

Finished goods: At completion of manufacturing process, all costs are associated with

production that includes raw material and WIP costs that transferred to next stage of

inventory.

2.4 Value inventory with FIFO, LIFO and weighted average

FIFO method

Date Purchase Sales Balance

March unit

unit

cost

Tota

l unit unit cost total Unit Unit cost Total

1 68 £15.00

£1,02

0.00

5 140 £15.50

£2,1

70.0

0 68 £15.00

£1,02

0.00

140 £15.50

£2,17

0.00

9 68 £15.00

£1,020.0

0 114 £15.50

£1,76

7.00

26 £15.00 £403.00

11 40 £16.00

£640

.00 114 £15.50

£1,76

7.00

40 £16.00

£640.

00

16 78 £16.50

£1,2

87.0

0 114 £15.50

£1,76

7.00

40 £16.00

£640.

00

5

They can be enter in next stage of inventory which is called in WIP. It includes products

that are finalised (R. Barstow, 2019).

Finished goods: At completion of manufacturing process, all costs are associated with

production that includes raw material and WIP costs that transferred to next stage of

inventory.

2.4 Value inventory with FIFO, LIFO and weighted average

FIFO method

Date Purchase Sales Balance

March unit

unit

cost

Tota

l unit unit cost total Unit Unit cost Total

1 68 £15.00

£1,02

0.00

5 140 £15.50

£2,1

70.0

0 68 £15.00

£1,02

0.00

140 £15.50

£2,17

0.00

9 68 £15.00

£1,020.0

0 114 £15.50

£1,76

7.00

26 £15.00 £403.00

11 40 £16.00

£640

.00 114 £15.50

£1,76

7.00

40 £16.00

£640.

00

16 78 £16.50

£1,2

87.0

0 114 £15.50

£1,76

7.00

40 £16.00

£640.

00

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

78 £16.50

£1,28

7.00

20 114 £15.50

£1,767.0

0 38 £16.00

£608.

00

2 £16.00 £32.00 78 £16.50

£1,28

7.00

29 38 £16.00 £608.00 54 £16.50

£891.

00

24 £16.50 £396.00

Working notes

Units available for sales = 68+140+40+78 = 326

Unit sold = 94+116+62 = 272

Unit in Inventory = 326-272 = 54

LIFO method

Date Purchase Sales Balance

March unit

unit

cost

Tota

l unit unit cost total Unit Unit cost Total

1 60 £15.00

£900.

00

5 140 £15.50

£2,1

70.0

0 60 £15.00

£900.

00

140 £15.50

£2,17

0.00

14 140 £15.50

£2,170.0

0 10 £15.00

£150.

00

50 £15.00 £750.00

27 70 £16.00 £1,1 10 £15.00 £150.

6

£1,28

7.00

20 114 £15.50

£1,767.0

0 38 £16.00

£608.

00

2 £16.00 £32.00 78 £16.50

£1,28

7.00

29 38 £16.00 £608.00 54 £16.50

£891.

00

24 £16.50 £396.00

Working notes

Units available for sales = 68+140+40+78 = 326

Unit sold = 94+116+62 = 272

Unit in Inventory = 326-272 = 54

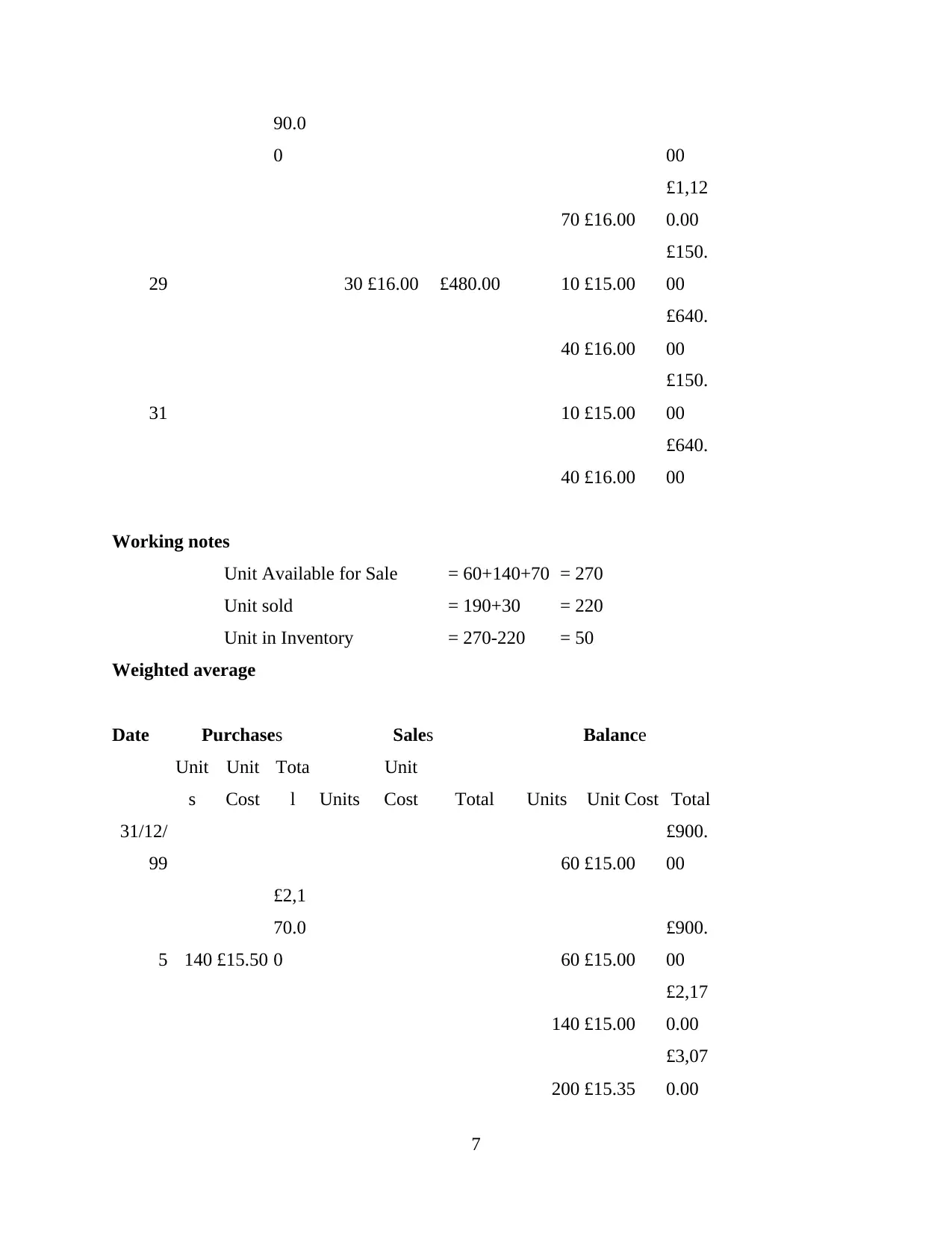

LIFO method

Date Purchase Sales Balance

March unit

unit

cost

Tota

l unit unit cost total Unit Unit cost Total

1 60 £15.00

£900.

00

5 140 £15.50

£2,1

70.0

0 60 £15.00

£900.

00

140 £15.50

£2,17

0.00

14 140 £15.50

£2,170.0

0 10 £15.00

£150.

00

50 £15.00 £750.00

27 70 £16.00 £1,1 10 £15.00 £150.

6

90.0

0 00

70 £16.00

£1,12

0.00

29 30 £16.00 £480.00 10 £15.00

£150.

00

40 £16.00

£640.

00

31 10 £15.00

£150.

00

40 £16.00

£640.

00

Working notes

Unit Available for Sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in Inventory = 270-220 = 50

Weighted average

Date Purchases Sales Balance

Unit

s

Unit

Cost

Tota

l Units

Unit

Cost Total Units Unit Cost Total

31/12/

99 60 £15.00

£900.

00

5 140 £15.50

£2,1

70.0

0 60 £15.00

£900.

00

140 £15.00

£2,17

0.00

200 £15.35

£3,07

0.00

7

0 00

70 £16.00

£1,12

0.00

29 30 £16.00 £480.00 10 £15.00

£150.

00

40 £16.00

£640.

00

31 10 £15.00

£150.

00

40 £16.00

£640.

00

Working notes

Unit Available for Sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in Inventory = 270-220 = 50

Weighted average

Date Purchases Sales Balance

Unit

s

Unit

Cost

Tota

l Units

Unit

Cost Total Units Unit Cost Total

31/12/

99 60 £15.00

£900.

00

5 140 £15.50

£2,1

70.0

0 60 £15.00

£900.

00

140 £15.00

£2,17

0.00

200 £15.35

£3,07

0.00

7

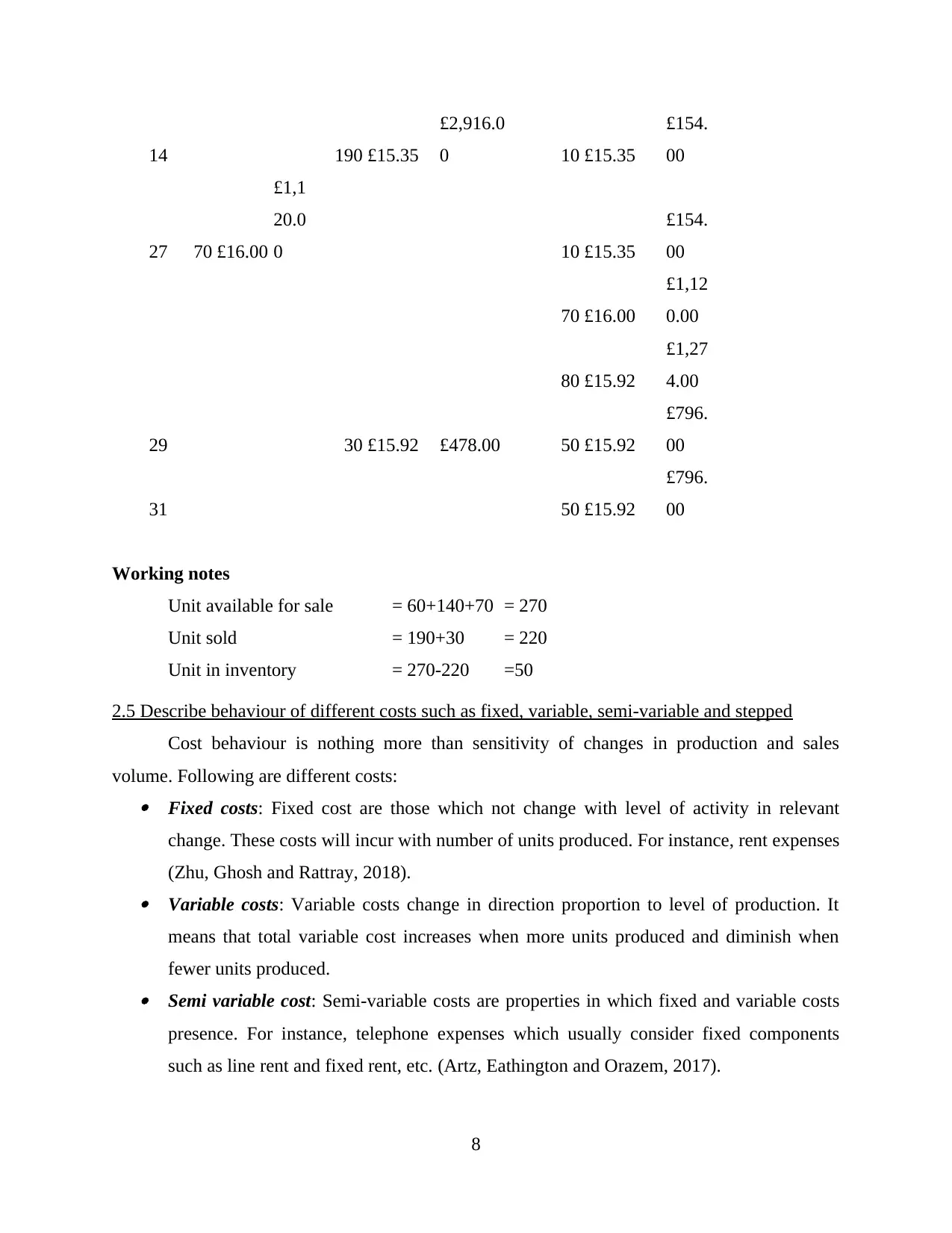

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

14 190 £15.35

£2,916.0

0 10 £15.35

£154.

00

27 70 £16.00

£1,1

20.0

0 10 £15.35

£154.

00

70 £16.00

£1,12

0.00

80 £15.92

£1,27

4.00

29 30 £15.92 £478.00 50 £15.92

£796.

00

31 50 £15.92

£796.

00

Working notes

Unit available for sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in inventory = 270-220 =50

2.5 Describe behaviour of different costs such as fixed, variable, semi-variable and stepped

Cost behaviour is nothing more than sensitivity of changes in production and sales

volume. Following are different costs: Fixed costs: Fixed cost are those which not change with level of activity in relevant

change. These costs will incur with number of units produced. For instance, rent expenses

(Zhu, Ghosh and Rattray, 2018). Variable costs: Variable costs change in direction proportion to level of production. It

means that total variable cost increases when more units produced and diminish when

fewer units produced. Semi variable cost: Semi-variable costs are properties in which fixed and variable costs

presence. For instance, telephone expenses which usually consider fixed components

such as line rent and fixed rent, etc. (Artz, Eathington and Orazem, 2017).

8

£2,916.0

0 10 £15.35

£154.

00

27 70 £16.00

£1,1

20.0

0 10 £15.35

£154.

00

70 £16.00

£1,12

0.00

80 £15.92

£1,27

4.00

29 30 £15.92 £478.00 50 £15.92

£796.

00

31 50 £15.92

£796.

00

Working notes

Unit available for sale = 60+140+70 = 270

Unit sold = 190+30 = 220

Unit in inventory = 270-220 =50

2.5 Describe behaviour of different costs such as fixed, variable, semi-variable and stepped

Cost behaviour is nothing more than sensitivity of changes in production and sales

volume. Following are different costs: Fixed costs: Fixed cost are those which not change with level of activity in relevant

change. These costs will incur with number of units produced. For instance, rent expenses

(Zhu, Ghosh and Rattray, 2018). Variable costs: Variable costs change in direction proportion to level of production. It

means that total variable cost increases when more units produced and diminish when

fewer units produced. Semi variable cost: Semi-variable costs are properties in which fixed and variable costs

presence. For instance, telephone expenses which usually consider fixed components

such as line rent and fixed rent, etc. (Artz, Eathington and Orazem, 2017).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stepped cost: Stepped costs is amount which is not change with steadily and changes in

activity volume instead of discrete points.

2.6 Record cost information with using job, batch, unit, process and service costing systems

Following are different cost information which can be used in different costing systems: Job: Job order costing is a system for assigning manufacturing costs to each individual

product and group of products. In this aspect, products manufactured that sufficient

different from each other. Batch: Batch costing is a form of specific order costing. It is similar to job costing to job

costing in each batch where number of identical units. Each batch is separately with

identifiable cost unit (Zhang, Jiao and Chen, 2017). Unit: Unit cost is the total expenditure which incurred by the enterprise to produce, store

and sell one unit of particular product and services. Process: Process costing is an accounting methodology which traces and accumulates

direct costs and indirect cost allocates in manufacturing process. It is system where large

quantities producing for homogeneous products.

Service: In cost information, cost is generally refers with amount that paid for receive

particular goods and services (Artz, Eathington and Orazem, 2017).

LO 3

3.1 Attribute overhead costs to production and service cost centres in accordance with agreed

bases

In production and service centres, there are following agreed bases of allocation and

apportionment: Direct: Direct cost can be defines as the price that can be completely attributed to the

production of specific goods and services. Some costs, such as depreciation or

administrative expenses are more difficult to assign for specific products. As a result, it is

considered to be indirect costs.

Step down: Step down allocation method is approach that used to allocate appropriate

amount of cost in services provided by one department to another. It is also allocates

other costs which can be develop in operating department.

9

activity volume instead of discrete points.

2.6 Record cost information with using job, batch, unit, process and service costing systems

Following are different cost information which can be used in different costing systems: Job: Job order costing is a system for assigning manufacturing costs to each individual

product and group of products. In this aspect, products manufactured that sufficient

different from each other. Batch: Batch costing is a form of specific order costing. It is similar to job costing to job

costing in each batch where number of identical units. Each batch is separately with

identifiable cost unit (Zhang, Jiao and Chen, 2017). Unit: Unit cost is the total expenditure which incurred by the enterprise to produce, store

and sell one unit of particular product and services. Process: Process costing is an accounting methodology which traces and accumulates

direct costs and indirect cost allocates in manufacturing process. It is system where large

quantities producing for homogeneous products.

Service: In cost information, cost is generally refers with amount that paid for receive

particular goods and services (Artz, Eathington and Orazem, 2017).

LO 3

3.1 Attribute overhead costs to production and service cost centres in accordance with agreed

bases

In production and service centres, there are following agreed bases of allocation and

apportionment: Direct: Direct cost can be defines as the price that can be completely attributed to the

production of specific goods and services. Some costs, such as depreciation or

administrative expenses are more difficult to assign for specific products. As a result, it is

considered to be indirect costs.

Step down: Step down allocation method is approach that used to allocate appropriate

amount of cost in services provided by one department to another. It is also allocates

other costs which can be develop in operating department.

9

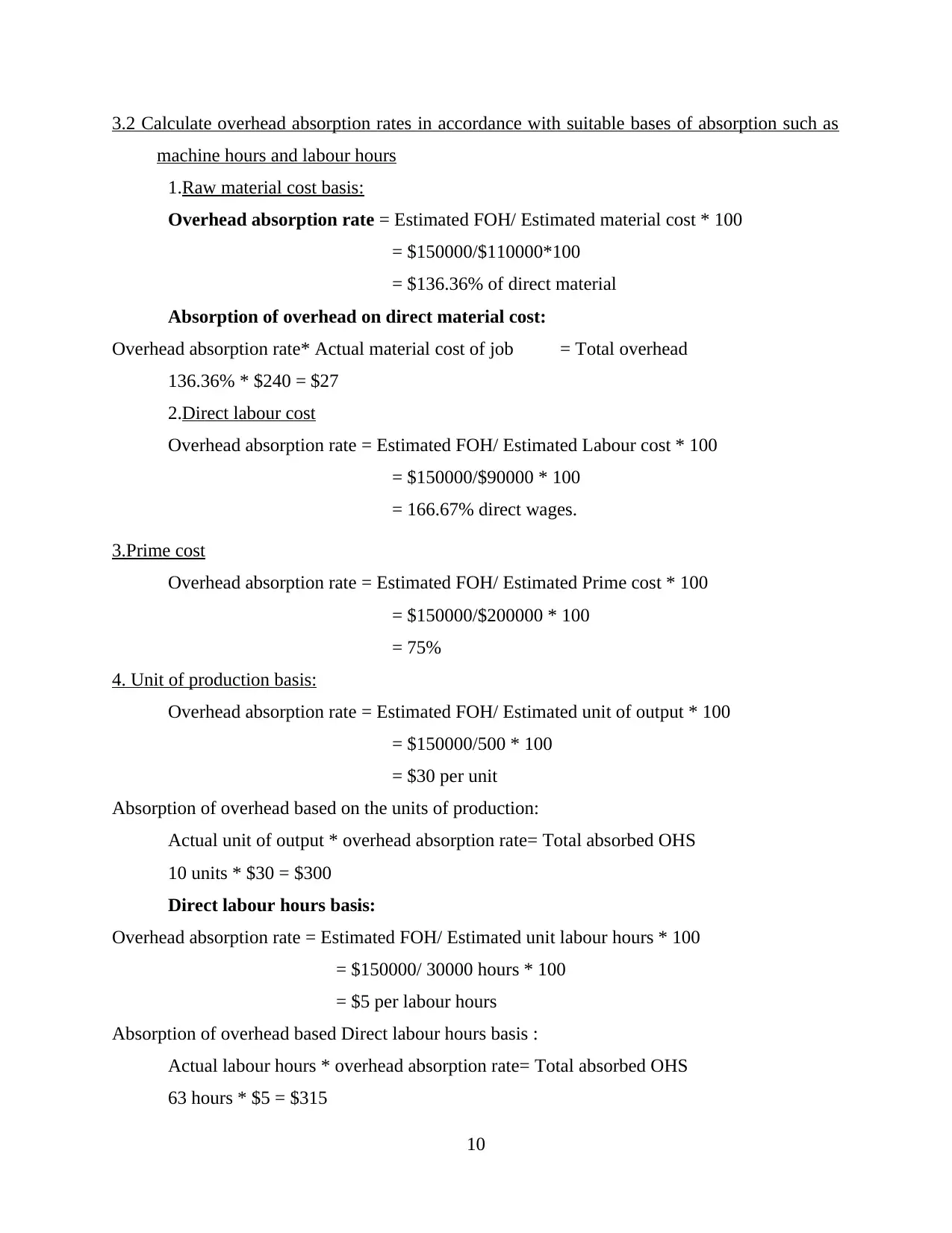

3.2 Calculate overhead absorption rates in accordance with suitable bases of absorption such as

machine hours and labour hours

1.Raw material cost basis:

Overhead absorption rate = Estimated FOH/ Estimated material cost * 100

= $150000/$110000*100

= $136.36% of direct material

Absorption of overhead on direct material cost:

Overhead absorption rate* Actual material cost of job = Total overhead

136.36% * $240 = $27

2.Direct labour cost

Overhead absorption rate = Estimated FOH/ Estimated Labour cost * 100

= $150000/$90000 * 100

= 166.67% direct wages.

3.Prime cost

Overhead absorption rate = Estimated FOH/ Estimated Prime cost * 100

= $150000/$200000 * 100

= 75%

4. Unit of production basis:

Overhead absorption rate = Estimated FOH/ Estimated unit of output * 100

= $150000/500 * 100

= $30 per unit

Absorption of overhead based on the units of production:

Actual unit of output * overhead absorption rate= Total absorbed OHS

10 units * $30 = $300

Direct labour hours basis:

Overhead absorption rate = Estimated FOH/ Estimated unit labour hours * 100

= $150000/ 30000 hours * 100

= $5 per labour hours

Absorption of overhead based Direct labour hours basis :

Actual labour hours * overhead absorption rate= Total absorbed OHS

63 hours * $5 = $315

10

machine hours and labour hours

1.Raw material cost basis:

Overhead absorption rate = Estimated FOH/ Estimated material cost * 100

= $150000/$110000*100

= $136.36% of direct material

Absorption of overhead on direct material cost:

Overhead absorption rate* Actual material cost of job = Total overhead

136.36% * $240 = $27

2.Direct labour cost

Overhead absorption rate = Estimated FOH/ Estimated Labour cost * 100

= $150000/$90000 * 100

= 166.67% direct wages.

3.Prime cost

Overhead absorption rate = Estimated FOH/ Estimated Prime cost * 100

= $150000/$200000 * 100

= 75%

4. Unit of production basis:

Overhead absorption rate = Estimated FOH/ Estimated unit of output * 100

= $150000/500 * 100

= $30 per unit

Absorption of overhead based on the units of production:

Actual unit of output * overhead absorption rate= Total absorbed OHS

10 units * $30 = $300

Direct labour hours basis:

Overhead absorption rate = Estimated FOH/ Estimated unit labour hours * 100

= $150000/ 30000 hours * 100

= $5 per labour hours

Absorption of overhead based Direct labour hours basis :

Actual labour hours * overhead absorption rate= Total absorbed OHS

63 hours * $5 = $315

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.