Retirement Investment Trends: A Data Analysis Report (Finance)

VerifiedAdded on 2022/12/09

|14

|2442

|97

Report

AI Summary

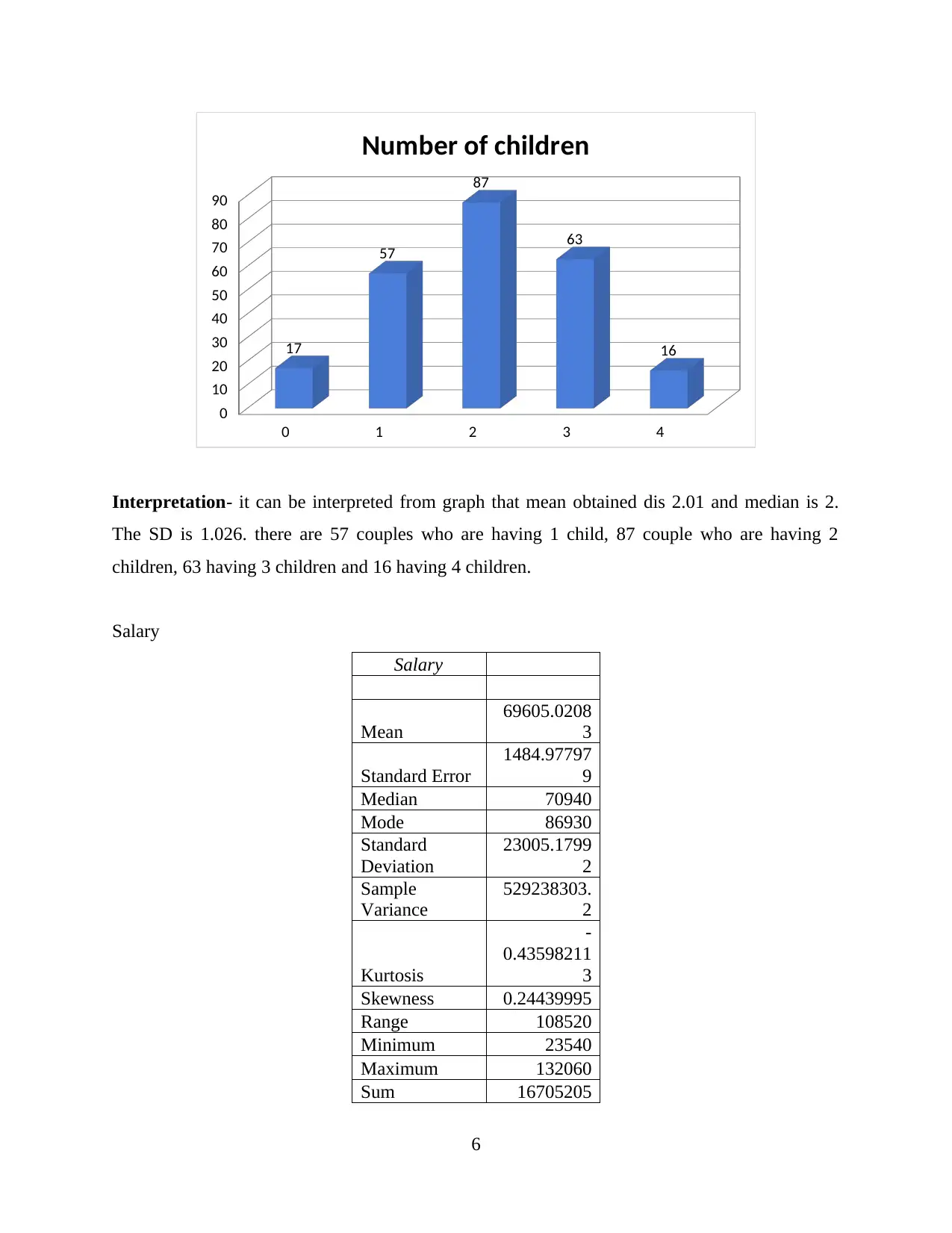

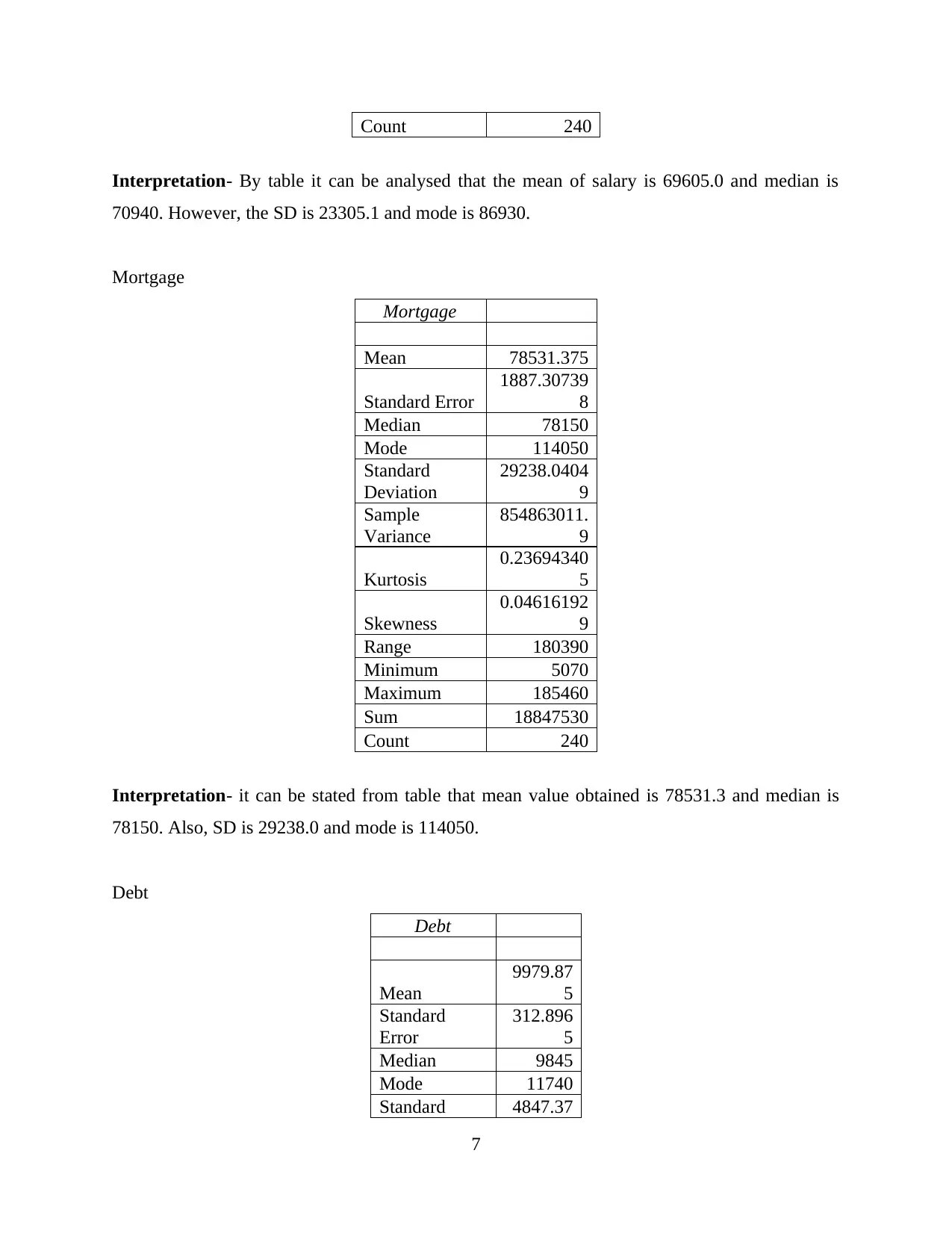

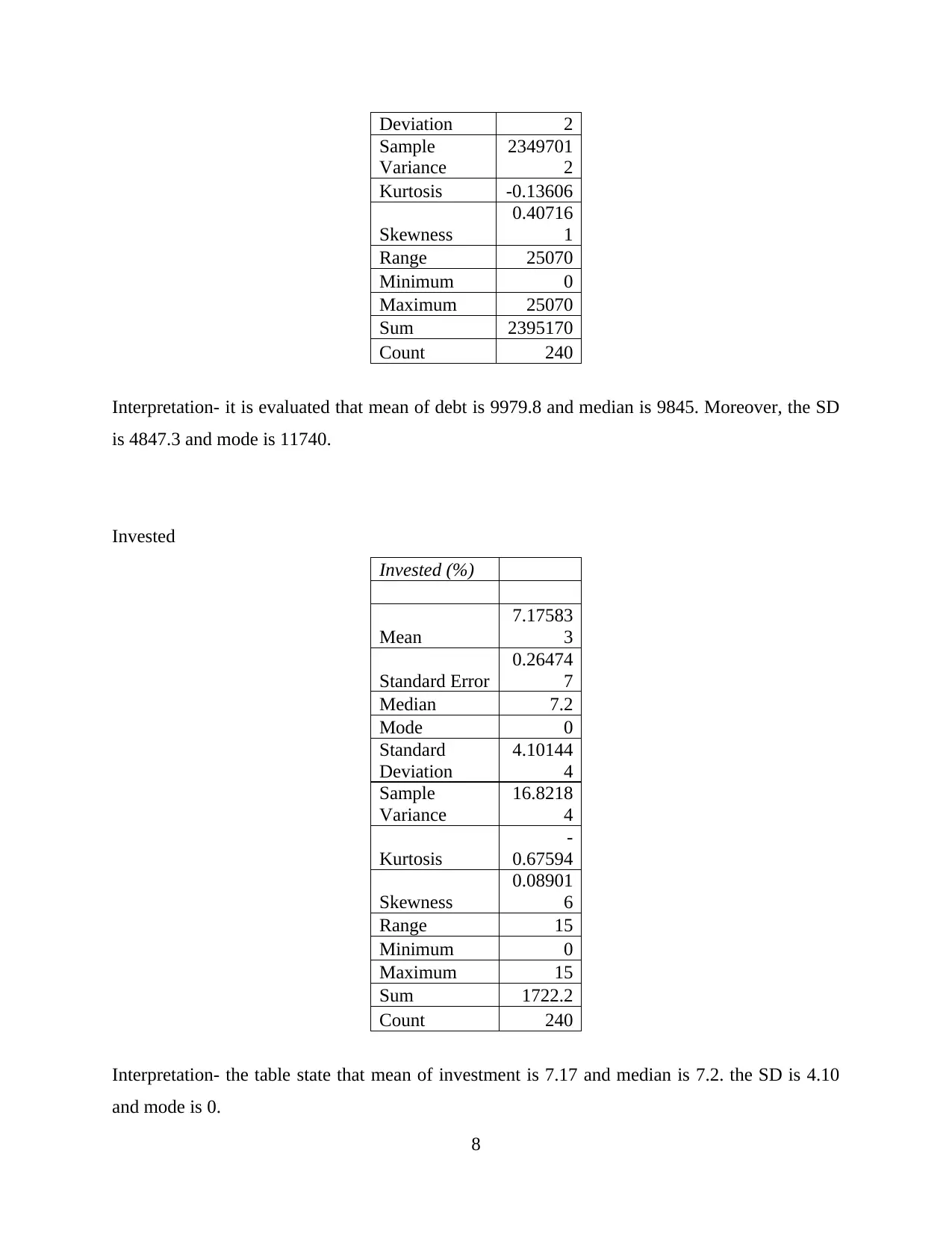

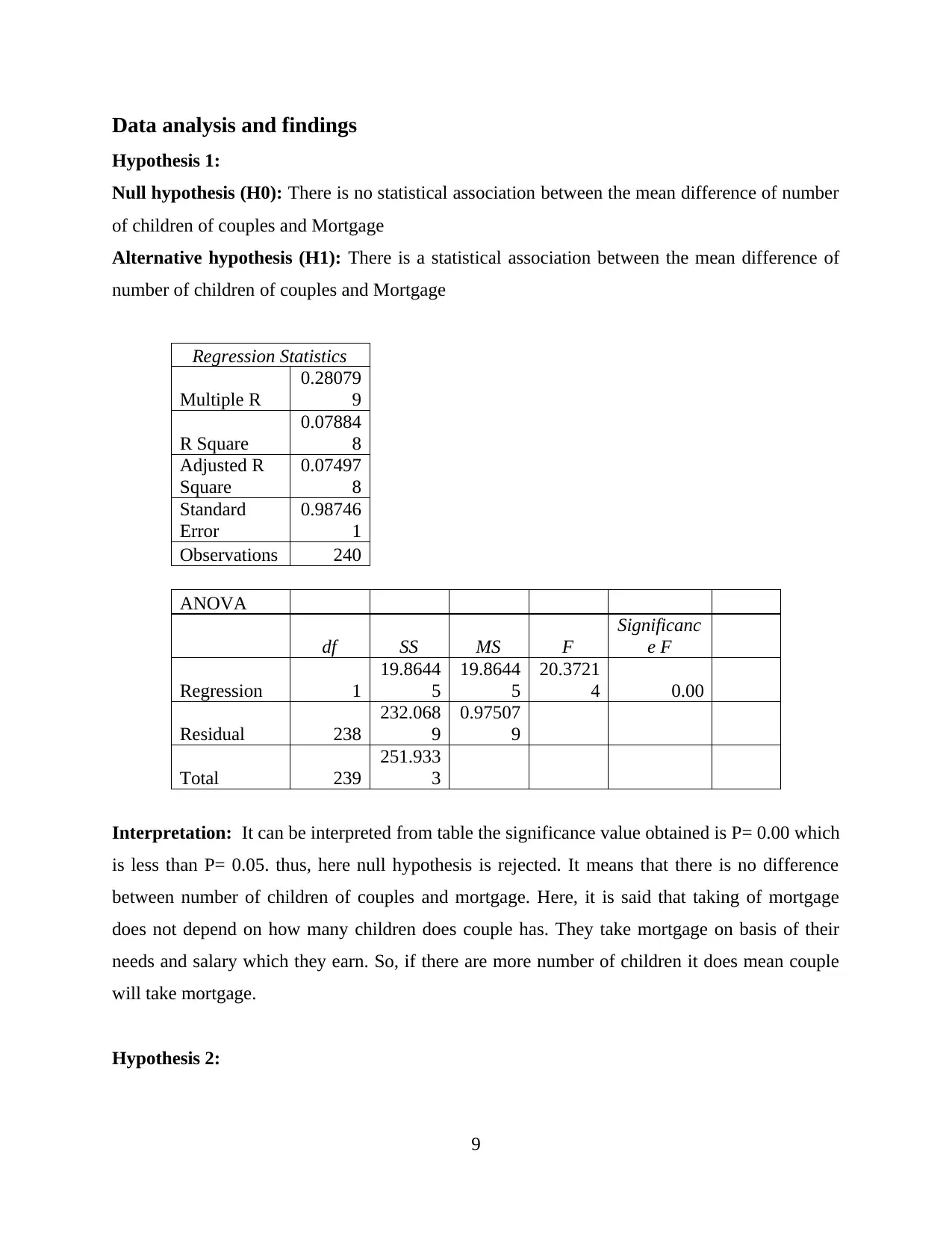

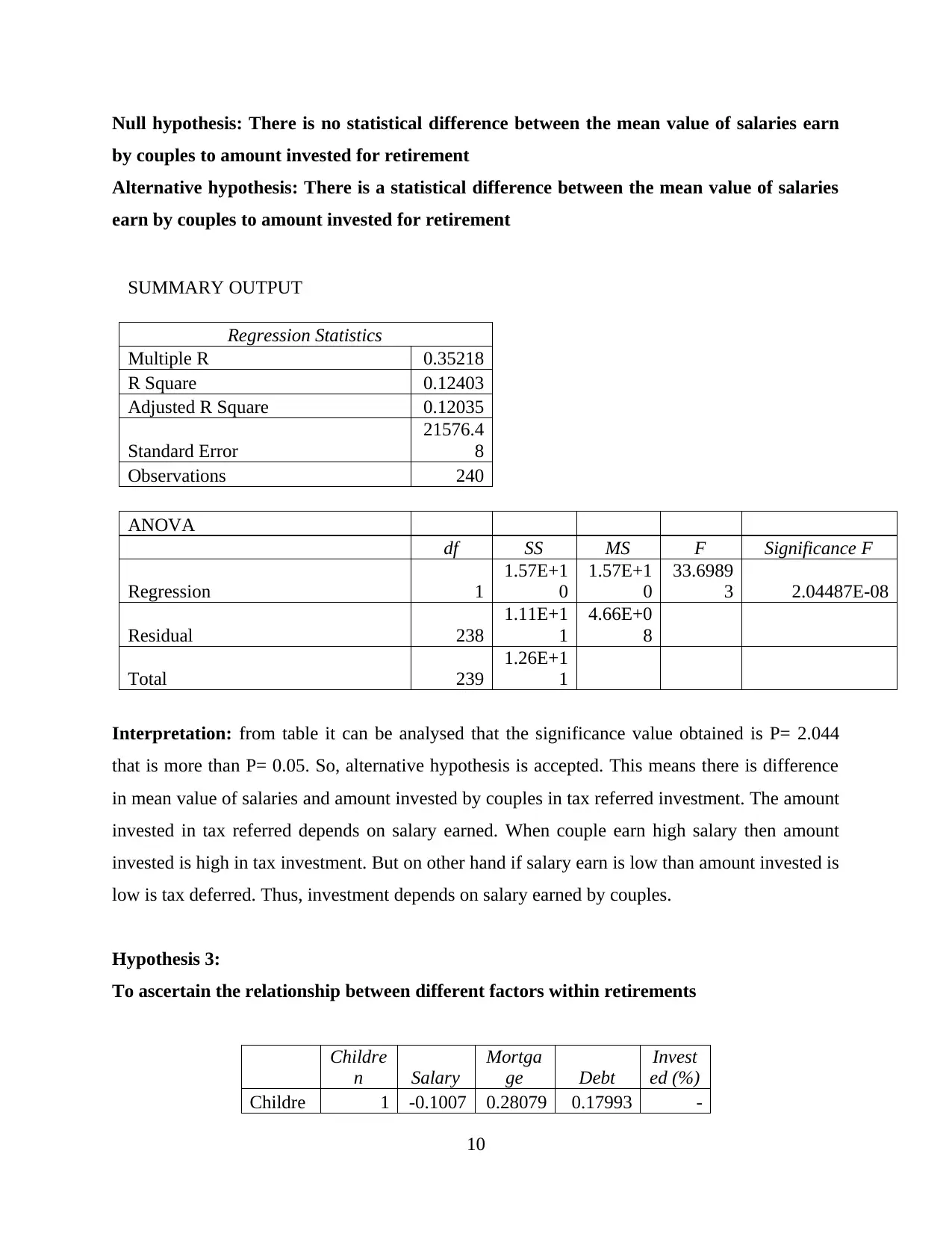

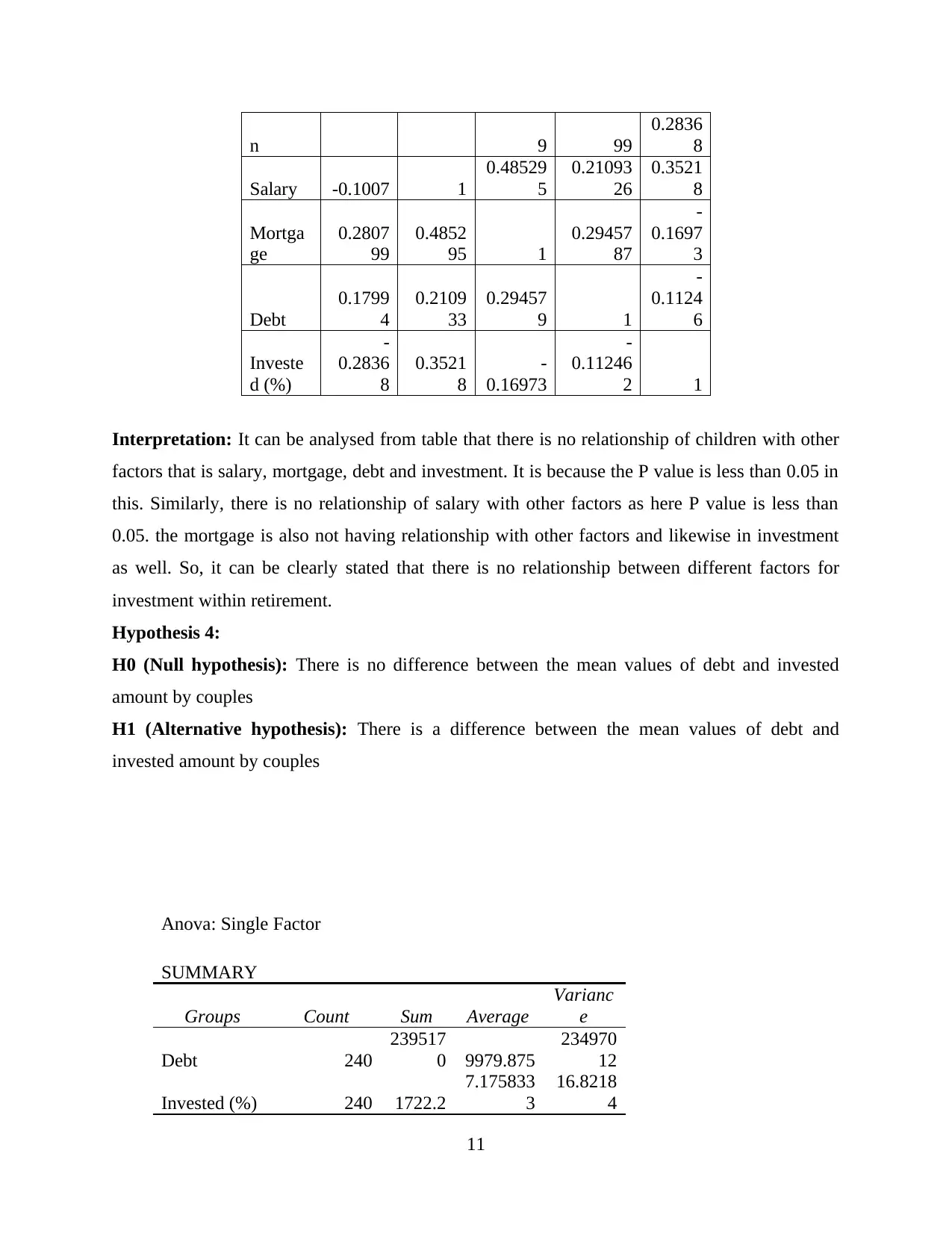

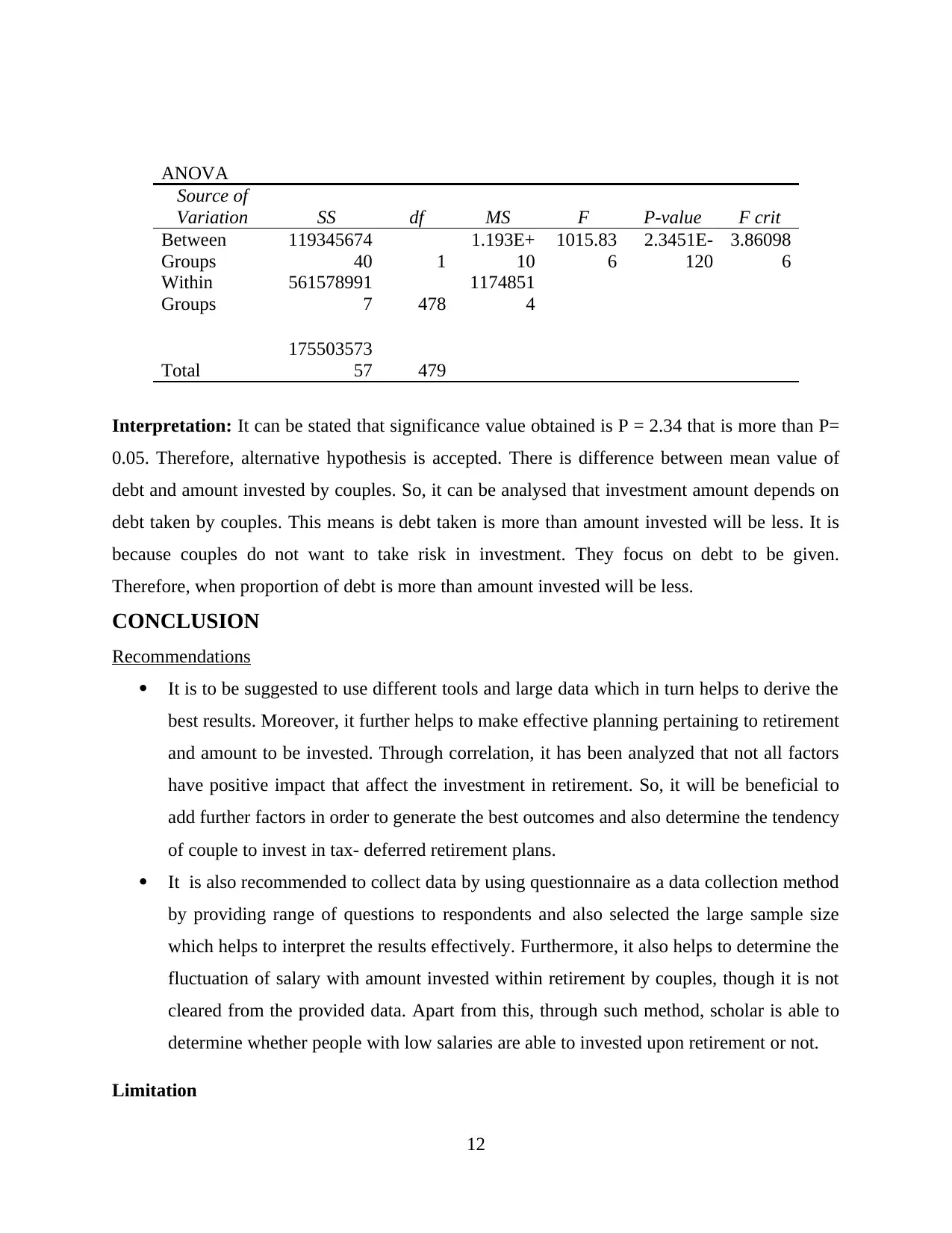

This report presents an analysis of couples' retirement investment behavior, based on a provided dataset. The study investigates the influence of various factors, including salary, mortgage, debt, and the number of children, on the amount invested in tax-deferred retirement plans. The research employs statistical methods like regression analysis, descriptive statistics, correlation, and ANOVA to test several hypotheses. The findings reveal a significant correlation between salary and investment amounts, with couples earning higher salaries tending to invest more. The analysis also indicates that mortgage and debt levels impact investment decisions, though the relationship isn't always straightforward. The report also explores how the number of children affects investment patterns. The conclusion offers recommendations for further research, suggesting the inclusion of additional factors and data collection methods to refine the understanding of couples' retirement investment strategies. The limitations of the study, such as the lack of information about the data source, are also acknowledged.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.