Analysis of Management Accounting Systems at Covent Garden Hotel

VerifiedAdded on 2020/01/23

|19

|4565

|65

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within the Covent Garden Hotel, a small firm operating in London's hospitality industry. The report begins by outlining various management accounting systems, including throughput accounting, cost accounting, process costing, transfer pricing, inventory accounting, and lean accounting, detailing their specific requirements and applications within the hotel. It then examines different management accounting reporting methods such as budget reports, payroll reports, sales reports, job cost reports, manufacturing reports, and cost accounting reports, explaining how each method contributes to understanding the hotel's financial performance. Furthermore, the report delves into the calculation of net income using both marginal and absorption costing techniques, comparing the outcomes and highlighting the differences in their approaches to cost allocation. The document also differentiates between marginal and absorption costing methods, including the expenses considered in each, and how they affect profit measurement. The report concludes with a discussion of planning tools and methods for addressing financial challenges in the business environment, providing valuable insights for managing the financial aspects of the hotel.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the corporate world, management accounting plays a vital role to manage and run an

enterprise in a proper and smooth manner. There are various kinds of accounting tools and

techniques that are helpful for the entrepreneur up to a great extent. Without process of

management accounting, a businessman is unable to manage the firm and generate higher and

effective sales along with revenues at the end of a particular period of time. The present case is

based on Covent Garden Hotel (CGH) which is a small firm and operates in the hospitality

industry of London. The report describes about numerous kinds of accounting systems for

managing the business process. In addition to this, it provides information related to different

accounting reports to analyse and know financial performance of Covent Garden Hotel. Besides

this, it shows the difference between marginal costing and absorption technique to calculate net

income. Further, current study analyses about various planning tools and techniques as well as

methods to combat the financial obstacles and problems that occur in business environment.

TASK 1

P1 Explanation of requirements of different types of management accounting systems in Covent

Garden Hotel

To,

General Manager and Board of Directors,

Covent Garden Hotel,

Date: 28th June 2017.

In the accounting and financial world there are different types of methods and systems

are used by the company. Here the Covent Garden Hotel uses some management accounting

systems for various requirements are purposes. These all systems are enumerated below: Throughput accounting: The management accounting system is basically related with

the raw material rather than costing or any other aspects. It helps to identify constraints

or problems related to required raw material, turnover of employees or labour as well as

wastage occurs in firm by which capacity of plant hampers (Kaplan and Atkinson,

2015). The basic requirement for the Covent Garden Hotel of throughput accounting

system is to reduce problems as well as constraints related to such mentioned aspects in

1

In the corporate world, management accounting plays a vital role to manage and run an

enterprise in a proper and smooth manner. There are various kinds of accounting tools and

techniques that are helpful for the entrepreneur up to a great extent. Without process of

management accounting, a businessman is unable to manage the firm and generate higher and

effective sales along with revenues at the end of a particular period of time. The present case is

based on Covent Garden Hotel (CGH) which is a small firm and operates in the hospitality

industry of London. The report describes about numerous kinds of accounting systems for

managing the business process. In addition to this, it provides information related to different

accounting reports to analyse and know financial performance of Covent Garden Hotel. Besides

this, it shows the difference between marginal costing and absorption technique to calculate net

income. Further, current study analyses about various planning tools and techniques as well as

methods to combat the financial obstacles and problems that occur in business environment.

TASK 1

P1 Explanation of requirements of different types of management accounting systems in Covent

Garden Hotel

To,

General Manager and Board of Directors,

Covent Garden Hotel,

Date: 28th June 2017.

In the accounting and financial world there are different types of methods and systems

are used by the company. Here the Covent Garden Hotel uses some management accounting

systems for various requirements are purposes. These all systems are enumerated below: Throughput accounting: The management accounting system is basically related with

the raw material rather than costing or any other aspects. It helps to identify constraints

or problems related to required raw material, turnover of employees or labour as well as

wastage occurs in firm by which capacity of plant hampers (Kaplan and Atkinson,

2015). The basic requirement for the Covent Garden Hotel of throughput accounting

system is to reduce problems as well as constraints related to such mentioned aspects in

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

appropriate way. Further, it leads to increase number of finished goods in same

resources and improve effectively and productivity of hotel in the overall hospitality

industry of London. Accounting of cost: In this type of system the hotel is able to know cost and expenses

which are incurred while making services for customers. Further, very basic requirement

of the cost accounting is to determine total cost of services offered by the firm. On the

basis of determining cost selling prices of each service or each room is to be calculated

by the management and able to sell in the market. Process costing: It is a method which shows cost of production occurs in each and every

manufacturing activity or process. With help of this the hotel can produce better

accommodation services for the tourists and customers as well. With this management

able to identify lack of cost in every business process further can take corrective actions

and make strategies against it (Fullerton, Kennedy and Widener, 2013). Hence, it

requires for reducing cost of every business activity and make them more efficient with

same quantity of raw materials. Transfer pricing: As per the respective system of management accounting raw material

and goods are transfer from parent company to subsidiary firm and reverse as well.

When subsidiary firm purchases services from main or parent entity then prices are less

in comparison to purchase from outsiders. Further, it leads to reduce total cost of

services and prices as well. Ultimately more number of tourists or consumers ready to

consume Covent Garden Hotel's accommodation services. Hence, requirement of attract

more number of users and enhance revenue at the end of specific period is to be

achieved by the company. Inventory accounting: Moreover, another used management accounting system by

Covent Garden Hotel is inventory accounting which helps to measure and control over

the stock at the end of financial period. Apart from this, by such system management

able to utilize its inventory in proper manner to generate more sales and revenue (Tools

and techniques of Management Accounting, 2017). Further, it can be said that the hotel

uses inventory management for making firm more efficient and achieve goals and

2

resources and improve effectively and productivity of hotel in the overall hospitality

industry of London. Accounting of cost: In this type of system the hotel is able to know cost and expenses

which are incurred while making services for customers. Further, very basic requirement

of the cost accounting is to determine total cost of services offered by the firm. On the

basis of determining cost selling prices of each service or each room is to be calculated

by the management and able to sell in the market. Process costing: It is a method which shows cost of production occurs in each and every

manufacturing activity or process. With help of this the hotel can produce better

accommodation services for the tourists and customers as well. With this management

able to identify lack of cost in every business process further can take corrective actions

and make strategies against it (Fullerton, Kennedy and Widener, 2013). Hence, it

requires for reducing cost of every business activity and make them more efficient with

same quantity of raw materials. Transfer pricing: As per the respective system of management accounting raw material

and goods are transfer from parent company to subsidiary firm and reverse as well.

When subsidiary firm purchases services from main or parent entity then prices are less

in comparison to purchase from outsiders. Further, it leads to reduce total cost of

services and prices as well. Ultimately more number of tourists or consumers ready to

consume Covent Garden Hotel's accommodation services. Hence, requirement of attract

more number of users and enhance revenue at the end of specific period is to be

achieved by the company. Inventory accounting: Moreover, another used management accounting system by

Covent Garden Hotel is inventory accounting which helps to measure and control over

the stock at the end of financial period. Apart from this, by such system management

able to utilize its inventory in proper manner to generate more sales and revenue (Tools

and techniques of Management Accounting, 2017). Further, it can be said that the hotel

uses inventory management for making firm more efficient and achieve goals and

2

targets of the firm in hospitality sector of London.

Lean accounting: According to lean accounting method the managers of Covent Garden

Hotel able to reduce cost of production by eliminate wastage services which occurs in

the firm. Apart from this, it provides various information as well as data which are

related to earning profit as well as making effective decisions for business. The

company uses the system for reducing various kinds of wastage products and obstacles

related to manufacturing process. Further, improve quality of accommodation and other

services as well in the hospitality segment.

Regards: Management Accounting Officer

P2 Various methods of management accounting reporting for Covent Garden Hotel

To,

General Manager and Board of Directors,

Covent Garden Hotel,

Date: 28th June 2017.

In an organisation, it necessary to make appropriate reports related to financial

transactions to know business performance in the industry. There are different kinds of methods

or report are used by the Covent Garden Hotel in order to management accounting reporting.

The methods are described below: Budget report: On the basis of respective report the Covent Garden Hotel able to know

that how much fund to be require for next month or year to produce particular number of

units. It shows various reports and informations such as related to cash, production units,

raw material required, revenue needs to generate etc (Schaltegger, Gibassier and

Zvezdov, 2013). These report are helps to the Covent Garden Hotel in order to manage

the company and make strategies according to it as well. Payroll report: The respective report is related to salary and wages which are provided

to the labours and employees of hotel. Amount of this report is recorded on daily and

3

Lean accounting: According to lean accounting method the managers of Covent Garden

Hotel able to reduce cost of production by eliminate wastage services which occurs in

the firm. Apart from this, it provides various information as well as data which are

related to earning profit as well as making effective decisions for business. The

company uses the system for reducing various kinds of wastage products and obstacles

related to manufacturing process. Further, improve quality of accommodation and other

services as well in the hospitality segment.

Regards: Management Accounting Officer

P2 Various methods of management accounting reporting for Covent Garden Hotel

To,

General Manager and Board of Directors,

Covent Garden Hotel,

Date: 28th June 2017.

In an organisation, it necessary to make appropriate reports related to financial

transactions to know business performance in the industry. There are different kinds of methods

or report are used by the Covent Garden Hotel in order to management accounting reporting.

The methods are described below: Budget report: On the basis of respective report the Covent Garden Hotel able to know

that how much fund to be require for next month or year to produce particular number of

units. It shows various reports and informations such as related to cash, production units,

raw material required, revenue needs to generate etc (Schaltegger, Gibassier and

Zvezdov, 2013). These report are helps to the Covent Garden Hotel in order to manage

the company and make strategies according to it as well. Payroll report: The respective report is related to salary and wages which are provided

to the labours and employees of hotel. Amount of this report is recorded on daily and

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

monthly basis when Covent Garden Hotel pays wages and salary respectively. Further,

total amount of the payroll report treated as a salary expense in the profit and loss

account of the hotel. Sales report: As per the respective management accounting reporting method the

Covent Garden Hotel record sales and revenue generated by the hotel in specific period

of time. It includes total revenue which is earns by selling services to the customers.

Here any kind of costs are not deducted and the total amount of sales report is treated in

the income statement as a revenue or sales. With this Covent Garden Hotel can know

that firm is up to which extent able to generate revenue at the end of particular time

(Aksoylu and Aykan, 2013). Job cost report: In this type of report of management accounting cost of every business

process is supposed to transacted or recorded. Here expenses of each and every batch or

process are determined which helps to the Covent Garden Hotel in order to know

expenses of every job or batch in the company. This report is submitted to management

and checked by them, in this if it identifies problems then take corrective actions to

overcome such problems of Covent Garden Hotel. Manufacturing report: The system or report shows about the units or items which are

produced in the operation process. Higher number of finished goods and services and

lower the raw material shows that Covent Garden Hotel is efficient to produce services.

Further, in this report cost of raw material, expenses which are occurred in

manufacturing process etc. includes. The total amount of production is to be recorded at

here and helps to the Covent Garden Hotel in order to make report properly. In the

accounting report the amount is to be treated as production costs in the profit and loss

account of Covent Garden Hotel (Ng, Harrison and Akroyd, 2013).

Cost accounting: At the last cost accounting report shows summation of all kinds of

expenses which comes into consideration in the business. Here expenditures of the

above mentioned all reports are included and derive cost of services which are the

Covent Garden Hotel going to offer its customers. On the basis of such costs

management of Covent Garden Hotel take effectual pricing decisions for sale such

4

total amount of the payroll report treated as a salary expense in the profit and loss

account of the hotel. Sales report: As per the respective management accounting reporting method the

Covent Garden Hotel record sales and revenue generated by the hotel in specific period

of time. It includes total revenue which is earns by selling services to the customers.

Here any kind of costs are not deducted and the total amount of sales report is treated in

the income statement as a revenue or sales. With this Covent Garden Hotel can know

that firm is up to which extent able to generate revenue at the end of particular time

(Aksoylu and Aykan, 2013). Job cost report: In this type of report of management accounting cost of every business

process is supposed to transacted or recorded. Here expenses of each and every batch or

process are determined which helps to the Covent Garden Hotel in order to know

expenses of every job or batch in the company. This report is submitted to management

and checked by them, in this if it identifies problems then take corrective actions to

overcome such problems of Covent Garden Hotel. Manufacturing report: The system or report shows about the units or items which are

produced in the operation process. Higher number of finished goods and services and

lower the raw material shows that Covent Garden Hotel is efficient to produce services.

Further, in this report cost of raw material, expenses which are occurred in

manufacturing process etc. includes. The total amount of production is to be recorded at

here and helps to the Covent Garden Hotel in order to make report properly. In the

accounting report the amount is to be treated as production costs in the profit and loss

account of Covent Garden Hotel (Ng, Harrison and Akroyd, 2013).

Cost accounting: At the last cost accounting report shows summation of all kinds of

expenses which comes into consideration in the business. Here expenditures of the

above mentioned all reports are included and derive cost of services which are the

Covent Garden Hotel going to offer its customers. On the basis of such costs

management of Covent Garden Hotel take effectual pricing decisions for sale such

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

services in the market.

Regards: Management Accounting Officer

TASK 2

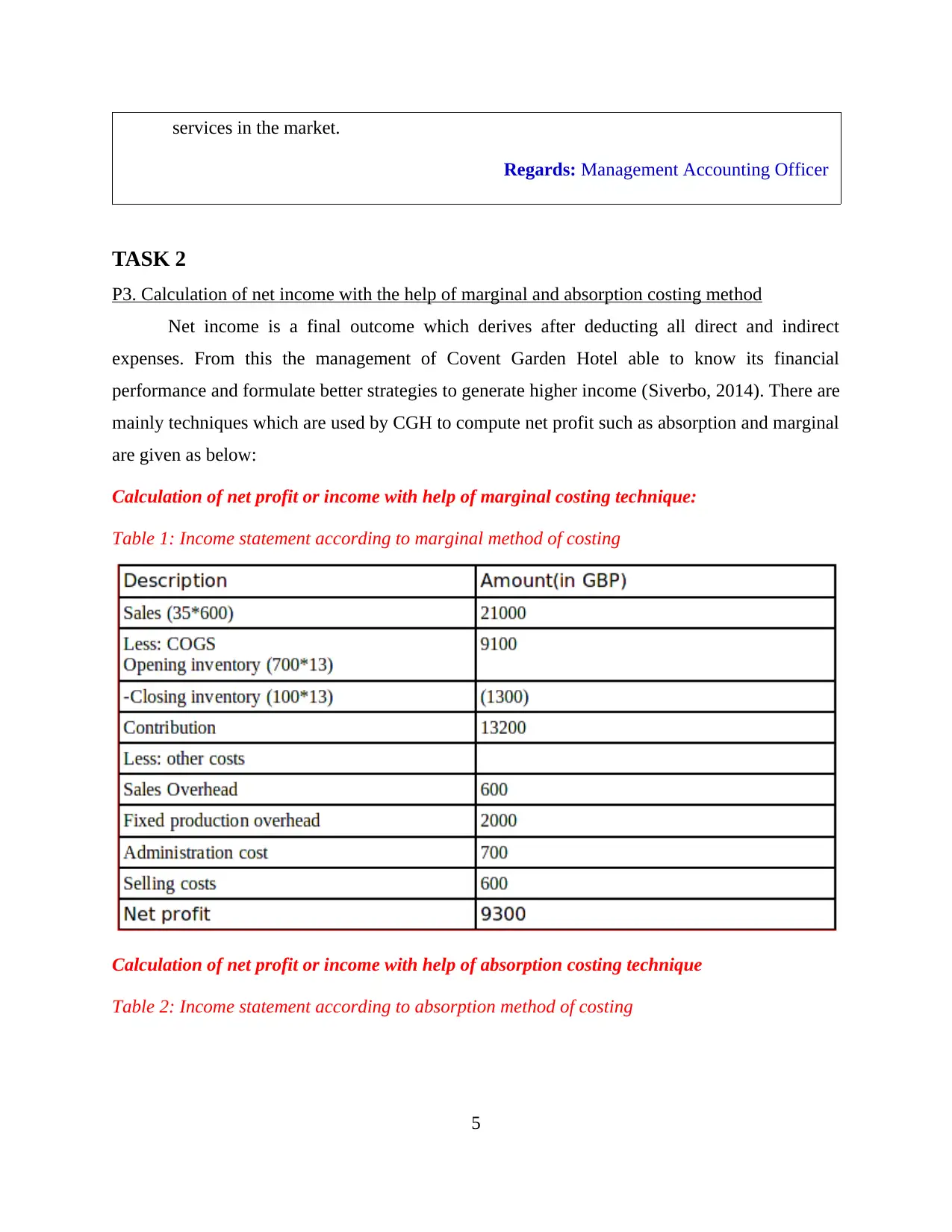

P3. Calculation of net income with the help of marginal and absorption costing method

Net income is a final outcome which derives after deducting all direct and indirect

expenses. From this the management of Covent Garden Hotel able to know its financial

performance and formulate better strategies to generate higher income (Siverbo, 2014). There are

mainly techniques which are used by CGH to compute net profit such as absorption and marginal

are given as below:

Calculation of net profit or income with help of marginal costing technique:

Table 1: Income statement according to marginal method of costing

Calculation of net profit or income with help of absorption costing technique

Table 2: Income statement according to absorption method of costing

5

Regards: Management Accounting Officer

TASK 2

P3. Calculation of net income with the help of marginal and absorption costing method

Net income is a final outcome which derives after deducting all direct and indirect

expenses. From this the management of Covent Garden Hotel able to know its financial

performance and formulate better strategies to generate higher income (Siverbo, 2014). There are

mainly techniques which are used by CGH to compute net profit such as absorption and marginal

are given as below:

Calculation of net profit or income with help of marginal costing technique:

Table 1: Income statement according to marginal method of costing

Calculation of net profit or income with help of absorption costing technique

Table 2: Income statement according to absorption method of costing

5

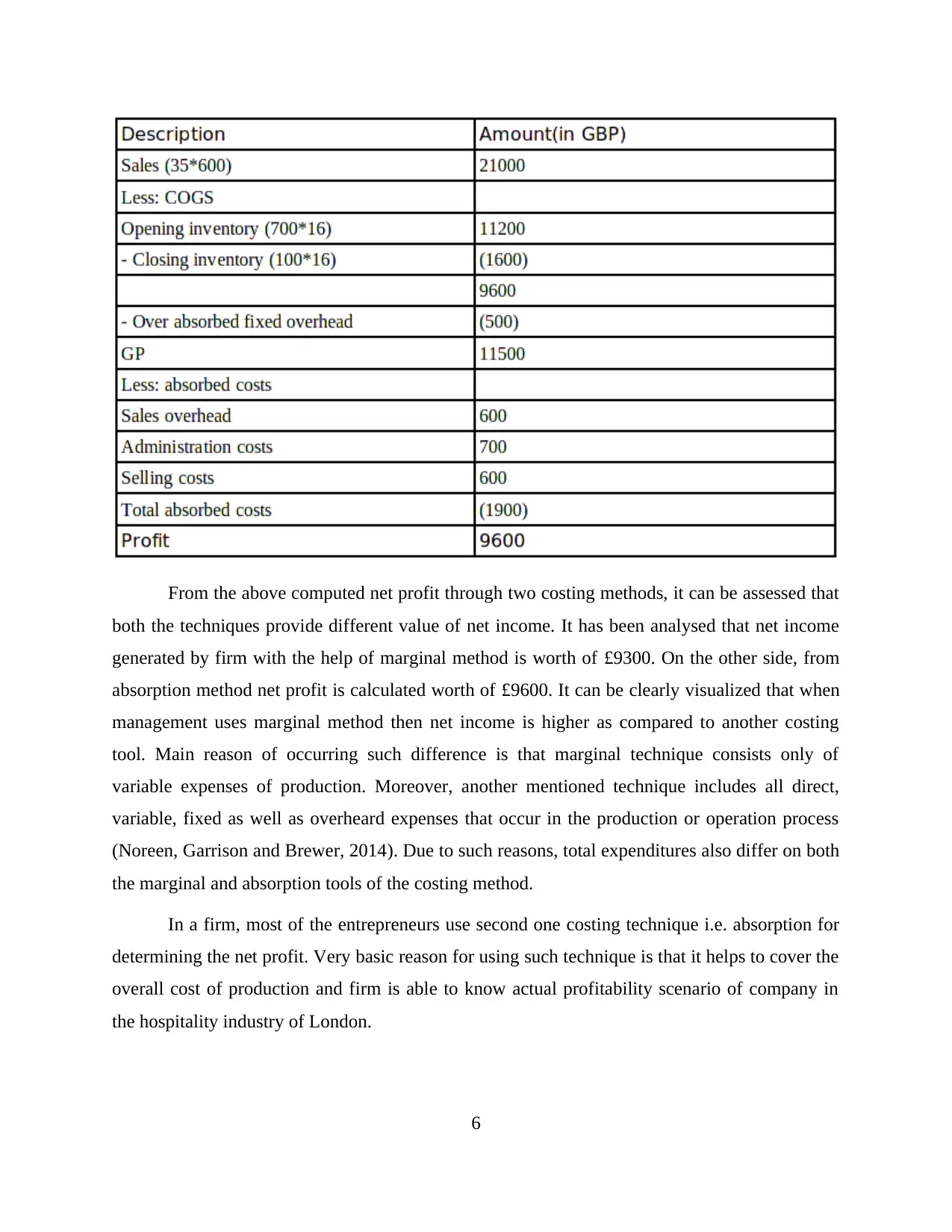

From the above computed net profit through two costing methods, it can be assessed that

both the techniques provide different value of net income. It has been analysed that net income

generated by firm with the help of marginal method is worth of £9300. On the other side, from

absorption method net profit is calculated worth of £9600. It can be clearly visualized that when

management uses marginal method then net income is higher as compared to another costing

tool. Main reason of occurring such difference is that marginal technique consists only of

variable expenses of production. Moreover, another mentioned technique includes all direct,

variable, fixed as well as overheard expenses that occur in the production or operation process

(Noreen, Garrison and Brewer, 2014). Due to such reasons, total expenditures also differ on both

the marginal and absorption tools of the costing method.

In a firm, most of the entrepreneurs use second one costing technique i.e. absorption for

determining the net profit. Very basic reason for using such technique is that it helps to cover the

overall cost of production and firm is able to know actual profitability scenario of company in

the hospitality industry of London.

6

both the techniques provide different value of net income. It has been analysed that net income

generated by firm with the help of marginal method is worth of £9300. On the other side, from

absorption method net profit is calculated worth of £9600. It can be clearly visualized that when

management uses marginal method then net income is higher as compared to another costing

tool. Main reason of occurring such difference is that marginal technique consists only of

variable expenses of production. Moreover, another mentioned technique includes all direct,

variable, fixed as well as overheard expenses that occur in the production or operation process

(Noreen, Garrison and Brewer, 2014). Due to such reasons, total expenditures also differ on both

the marginal and absorption tools of the costing method.

In a firm, most of the entrepreneurs use second one costing technique i.e. absorption for

determining the net profit. Very basic reason for using such technique is that it helps to cover the

overall cost of production and firm is able to know actual profitability scenario of company in

the hospitality industry of London.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

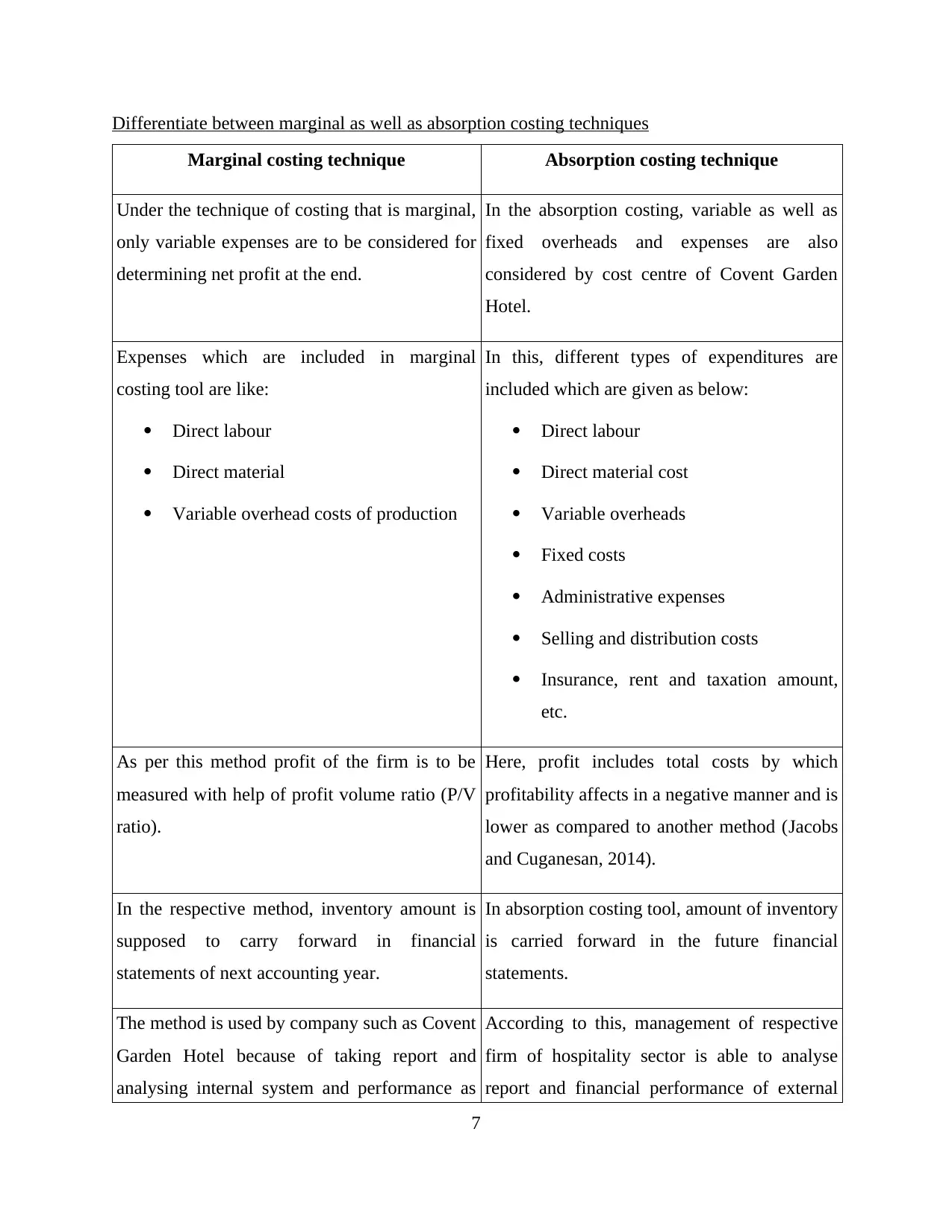

Differentiate between marginal as well as absorption costing techniques

Marginal costing technique Absorption costing technique

Under the technique of costing that is marginal,

only variable expenses are to be considered for

determining net profit at the end.

In the absorption costing, variable as well as

fixed overheads and expenses are also

considered by cost centre of Covent Garden

Hotel.

Expenses which are included in marginal

costing tool are like:

Direct labour

Direct material

Variable overhead costs of production

In this, different types of expenditures are

included which are given as below:

Direct labour

Direct material cost

Variable overheads

Fixed costs

Administrative expenses

Selling and distribution costs

Insurance, rent and taxation amount,

etc.

As per this method profit of the firm is to be

measured with help of profit volume ratio (P/V

ratio).

Here, profit includes total costs by which

profitability affects in a negative manner and is

lower as compared to another method (Jacobs

and Cuganesan, 2014).

In the respective method, inventory amount is

supposed to carry forward in financial

statements of next accounting year.

In absorption costing tool, amount of inventory

is carried forward in the future financial

statements.

The method is used by company such as Covent

Garden Hotel because of taking report and

analysing internal system and performance as

According to this, management of respective

firm of hospitality sector is able to analyse

report and financial performance of external

7

Marginal costing technique Absorption costing technique

Under the technique of costing that is marginal,

only variable expenses are to be considered for

determining net profit at the end.

In the absorption costing, variable as well as

fixed overheads and expenses are also

considered by cost centre of Covent Garden

Hotel.

Expenses which are included in marginal

costing tool are like:

Direct labour

Direct material

Variable overhead costs of production

In this, different types of expenditures are

included which are given as below:

Direct labour

Direct material cost

Variable overheads

Fixed costs

Administrative expenses

Selling and distribution costs

Insurance, rent and taxation amount,

etc.

As per this method profit of the firm is to be

measured with help of profit volume ratio (P/V

ratio).

Here, profit includes total costs by which

profitability affects in a negative manner and is

lower as compared to another method (Jacobs

and Cuganesan, 2014).

In the respective method, inventory amount is

supposed to carry forward in financial

statements of next accounting year.

In absorption costing tool, amount of inventory

is carried forward in the future financial

statements.

The method is used by company such as Covent

Garden Hotel because of taking report and

analysing internal system and performance as

According to this, management of respective

firm of hospitality sector is able to analyse

report and financial performance of external

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

well as company (Krishnan, 2015). system.

TASK 3

P4 Benefits and drawbacks of different kinds of planning techniques

In the business environment, planning has an important role for making effective and

proper plan of the firm to make it more efficient. There are numerous kinds of techniques that are

the most helpful for Covent Garden Hotel to make successful plan up to a high extent. The tools

are explained below along with their benefits and limitations:

Budget: Key planning tool is budget which is used by the management in order to predict

about the future financial informations. With help of this the Covent Garden Hotel is able to

make effective plan in different criterias such as cash balance, production units required to

produce, revenue needs to generate, requires raw material etc. for current and next period. In

addition to this, different types of budgets are to be framed such as cash, production, material,

sales and revenue etc (Panaretou, Shackleton and Taylor, 2013).

Various benefits and limitations of the budget are as follows:

Benefits:

Budget is tool of planning orientation and helps to make highly appropriate financial plan

for current and future periods in Covent Garden Hotel (Agarwal, 2016).

It shows both sides on the firm such as income side and expense side as well.

Covent Garden Hotel is able to allocate cash as well as financial resources to each

organisational functions on the basis of available cash flow.

Further, it helps to make the plan for collecting fund from different source of finance.

It is very cost conscious method so management of Covent Garden Hotel able to control

and reduce over the cost of production. It helps to evaluate business performance with help of budgeted data as well as actual

results.

Limitations:

8

TASK 3

P4 Benefits and drawbacks of different kinds of planning techniques

In the business environment, planning has an important role for making effective and

proper plan of the firm to make it more efficient. There are numerous kinds of techniques that are

the most helpful for Covent Garden Hotel to make successful plan up to a high extent. The tools

are explained below along with their benefits and limitations:

Budget: Key planning tool is budget which is used by the management in order to predict

about the future financial informations. With help of this the Covent Garden Hotel is able to

make effective plan in different criterias such as cash balance, production units required to

produce, revenue needs to generate, requires raw material etc. for current and next period. In

addition to this, different types of budgets are to be framed such as cash, production, material,

sales and revenue etc (Panaretou, Shackleton and Taylor, 2013).

Various benefits and limitations of the budget are as follows:

Benefits:

Budget is tool of planning orientation and helps to make highly appropriate financial plan

for current and future periods in Covent Garden Hotel (Agarwal, 2016).

It shows both sides on the firm such as income side and expense side as well.

Covent Garden Hotel is able to allocate cash as well as financial resources to each

organisational functions on the basis of available cash flow.

Further, it helps to make the plan for collecting fund from different source of finance.

It is very cost conscious method so management of Covent Garden Hotel able to control

and reduce over the cost of production. It helps to evaluate business performance with help of budgeted data as well as actual

results.

Limitations:

8

It's a very time consuming method and sometimes reduce efficiency of the individuals

who are working finance department.

Highly experienced along with better skilled employee is required who charge higher

salary from Covent Garden Hotel (Ball, 2013).

On the basis of budget the manager of Covent Garden Hotel allocate financial resource to

every department but manager of particular department sometimes re quire more or less

money by which disputes can be arise. It considers as well as deal with the financial treatment, further, it ignores different

subjective problems and issues of the firm.

Cash budget

A budget statement which supports to the Covent Garden Hotel in terms of assessing

future cash position along with expenses and incomes is considered as cash budget. Generally all

the firms prepare such kind of budget because by predetermining level of liquidity, management

easily able to make decisions appropriately. Hypothetical example of the cash budget is stated

along with its benefits and drawbacks below:

Particulars Amount (in GBP)

Cash incomes

Revenue 850

Loan from bank 400

Cash collection of debtors 350

Total cash incomes (A) 1600

Cash disposals

Rental expenses 350

Premium on insurance 180

9

who are working finance department.

Highly experienced along with better skilled employee is required who charge higher

salary from Covent Garden Hotel (Ball, 2013).

On the basis of budget the manager of Covent Garden Hotel allocate financial resource to

every department but manager of particular department sometimes re quire more or less

money by which disputes can be arise. It considers as well as deal with the financial treatment, further, it ignores different

subjective problems and issues of the firm.

Cash budget

A budget statement which supports to the Covent Garden Hotel in terms of assessing

future cash position along with expenses and incomes is considered as cash budget. Generally all

the firms prepare such kind of budget because by predetermining level of liquidity, management

easily able to make decisions appropriately. Hypothetical example of the cash budget is stated

along with its benefits and drawbacks below:

Particulars Amount (in GBP)

Cash incomes

Revenue 850

Loan from bank 400

Cash collection of debtors 350

Total cash incomes (A) 1600

Cash disposals

Rental expenses 350

Premium on insurance 180

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.