Economic Effects of COVID-19 Pandemic and Inflation in India

VerifiedAdded on 2021/09/18

|14

|3503

|166

Report

AI Summary

This report, prepared by a SYBA student, examines the economic effects of the COVID-19 pandemic on India, with a specific focus on whether the pandemic caused inflation. It begins with an introduction to the global health and economic shocks caused by the pandemic, followed by an overview of the Indian economy before the outbreak, highlighting slowing GDP growth and rising unemployment. The report then delves into the impact of the pandemic on inflation, macroeconomic effects such as demand and supply disruptions, and the long-run consequences of the economic disturbance, including disruptions in the accumulation of physical and human capital. The analysis covers various aspects like the decline in private consumption, investment, international trade, and manufacturing, providing a comprehensive view of the pandemic's impact on different sectors of the Indian economy. The report also considers the role of government and the Reserve Bank of India (RBI) in mitigating the crisis.

1

NAME – Shllok Porwal

CLASS – SYBA(2020-21)

DIVISION – B

ROLL NO. – 2352

SUBJECT – MACROECONOMICS - ll

SEMESTER – IV

TITLE – ECONOMIC EFFECTS OF COVID 19 PANDEMIC- DID

IT CAUSE INFLATION IN INDIA- A STUDY

DEPT. – DEPARTMENT OF ECONOMICS

EMAIL ID – sp.writes1@gmail.com

CONTACT – 8779660391

NAME – Shllok Porwal

CLASS – SYBA(2020-21)

DIVISION – B

ROLL NO. – 2352

SUBJECT – MACROECONOMICS - ll

SEMESTER – IV

TITLE – ECONOMIC EFFECTS OF COVID 19 PANDEMIC- DID

IT CAUSE INFLATION IN INDIA- A STUDY

DEPT. – DEPARTMENT OF ECONOMICS

EMAIL ID – sp.writes1@gmail.com

CONTACT – 8779660391

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

INDEX

SR. NO. TOPIC PAGE NO.

1 INTRODUCTION 3

2 THE STATE OF THE INDIAN ECONOMY ON THE EVE OF

COVID-19 OUTBREAK

5

3 INFLATION IN INDIA AND COVID 19 8

4 MACROECONOMIC EFFECTS 9

5 ECONOMIC EFFECTS OF THE PANDEMIC IN THE LONG RUN 11

6 CONCLUSION 13

7 REFERNECES 14

INDEX

SR. NO. TOPIC PAGE NO.

1 INTRODUCTION 3

2 THE STATE OF THE INDIAN ECONOMY ON THE EVE OF

COVID-19 OUTBREAK

5

3 INFLATION IN INDIA AND COVID 19 8

4 MACROECONOMIC EFFECTS 9

5 ECONOMIC EFFECTS OF THE PANDEMIC IN THE LONG RUN 11

6 CONCLUSION 13

7 REFERNECES 14

3

INTRODUCTION

We are in the middle of a global Covid-19 pandemic, which is inflicting two kinds of shocks on

countries: a health shock and an economic shock. Given the nature of the disease which is

highly contagious, the ways to contain the spread include policy actions such as imposition of

social distancing, self-isolation at home, closure of institutions, and public facilities, restrictions

on mobility and even lock-down of an entire country. These actions can potentially lead to dire

consequences for economies around the world. In other words, effective containment of the

disease requires the economy of a country to stop its normal functioning. This has triggered

fears of a deep and prolonged global recession. On April 9, the chief of International Monetary

Fund, Kristalina Georgieva said that the year 2020 could see the worst global economic fallout

since the Great Depression in the 1930s, with over 170 countries likely to experience negative

per capita GDP growth due to the raging coronavirus pandemic.34

The world has witnessed several epidemics such as the Spanish Flu of 1918, outbreak of

HIV/AIDS, SARS (Severe Acute Respiratory Syndrome), MERS (Middle East Respiratory

Syndrome) and Ebola. In the past, India has had to deal with diseases such as the small pox,

plague and polio. All of these individually have been pretty severe episodes. However the

Covid-19 which originated in China in December 2019 and over the next few months rapidly

spread to almost all countries of the world can potentially turn out to be the biggest health crisis

in our history. Many experts have already called this a Black Swan event for the global economy

The overall magnitude of the impact of the pandemic will depend upon the duration and severity

of the health crisis, the extent to which intermittent lock-downs are required in different regions

of the country and the manner in which the situation unfolds as and when the nationwide lock-

down is finally lifted and normal economic activity is permitted. The loss to the economy has

already been substantial.

This crisis comes at a time when India's GDP growth was slowing down, and unemployment

was on the rise owing to poor economic performance over the last several years. The

precarious situation that the economy was in before getting hit by this shock will potentially

worsen the effect of the shock. This is especially because the financial sector which is the brain

of the economy has not been functioning properly and the macroeconomic policy space to

respond to such a crisis is severely limited.

INTRODUCTION

We are in the middle of a global Covid-19 pandemic, which is inflicting two kinds of shocks on

countries: a health shock and an economic shock. Given the nature of the disease which is

highly contagious, the ways to contain the spread include policy actions such as imposition of

social distancing, self-isolation at home, closure of institutions, and public facilities, restrictions

on mobility and even lock-down of an entire country. These actions can potentially lead to dire

consequences for economies around the world. In other words, effective containment of the

disease requires the economy of a country to stop its normal functioning. This has triggered

fears of a deep and prolonged global recession. On April 9, the chief of International Monetary

Fund, Kristalina Georgieva said that the year 2020 could see the worst global economic fallout

since the Great Depression in the 1930s, with over 170 countries likely to experience negative

per capita GDP growth due to the raging coronavirus pandemic.34

The world has witnessed several epidemics such as the Spanish Flu of 1918, outbreak of

HIV/AIDS, SARS (Severe Acute Respiratory Syndrome), MERS (Middle East Respiratory

Syndrome) and Ebola. In the past, India has had to deal with diseases such as the small pox,

plague and polio. All of these individually have been pretty severe episodes. However the

Covid-19 which originated in China in December 2019 and over the next few months rapidly

spread to almost all countries of the world can potentially turn out to be the biggest health crisis

in our history. Many experts have already called this a Black Swan event for the global economy

The overall magnitude of the impact of the pandemic will depend upon the duration and severity

of the health crisis, the extent to which intermittent lock-downs are required in different regions

of the country and the manner in which the situation unfolds as and when the nationwide lock-

down is finally lifted and normal economic activity is permitted. The loss to the economy has

already been substantial.

This crisis comes at a time when India's GDP growth was slowing down, and unemployment

was on the rise owing to poor economic performance over the last several years. The

precarious situation that the economy was in before getting hit by this shock will potentially

worsen the effect of the shock. This is especially because the financial sector which is the brain

of the economy has not been functioning properly and the macroeconomic policy space to

respond to such a crisis is severely limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Earlier, Indian economy was primarily experiencing a demand slowdown whereas now both

demand and supply have been disrupted. There are four channels through which the impact is

getting transmitted to output growth. These are: external supply and demand constraints due to

global recession and disruption of global supply chains, domestic supply disruptions, and

decline in domestic demand. The economic shock is impacting both formal and informal sectors.

It may take a long time for the economy to recover from this shock even if the lock-down is fully

lifted by August or September, 2020. To a large extent the recovery will depend on the policy

responses of the 5 government and the Reserve Bank of India (RBI) during the crisis period.

The policymakers have already announced an initial round of actions. Much more needs to be

done to minimize the impact of the shock on the economy.

Earlier, Indian economy was primarily experiencing a demand slowdown whereas now both

demand and supply have been disrupted. There are four channels through which the impact is

getting transmitted to output growth. These are: external supply and demand constraints due to

global recession and disruption of global supply chains, domestic supply disruptions, and

decline in domestic demand. The economic shock is impacting both formal and informal sectors.

It may take a long time for the economy to recover from this shock even if the lock-down is fully

lifted by August or September, 2020. To a large extent the recovery will depend on the policy

responses of the 5 government and the Reserve Bank of India (RBI) during the crisis period.

The policymakers have already announced an initial round of actions. Much more needs to be

done to minimize the impact of the shock on the economy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

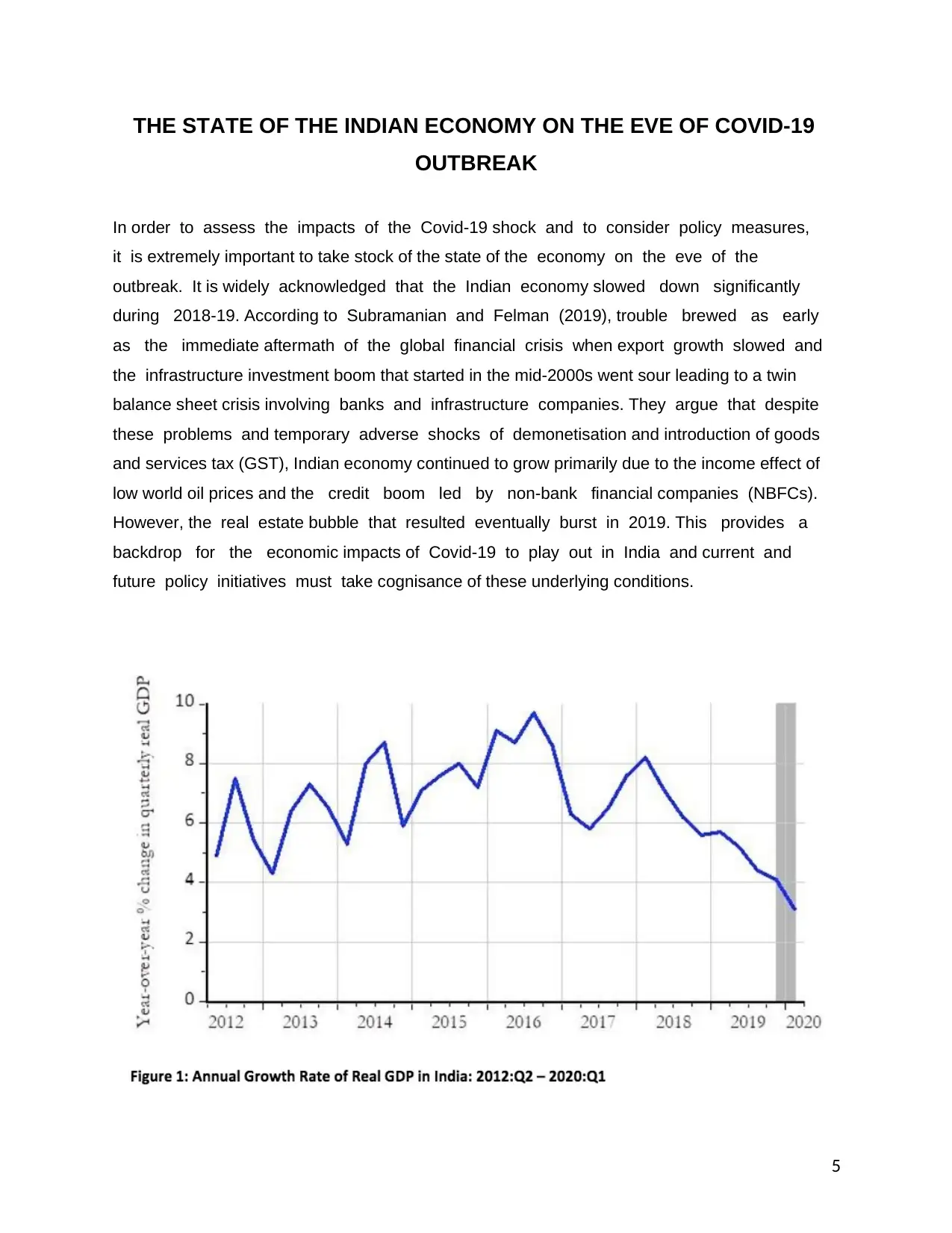

THE STATE OF THE INDIAN ECONOMY ON THE EVE OF COVID-19

OUTBREAK

In order to assess the impacts of the Covid-19 shock and to consider policy measures,

it is extremely important to take stock of the state of the economy on the eve of the

outbreak. It is widely acknowledged that the Indian economy slowed down significantly

during 2018-19. According to Subramanian and Felman (2019), trouble brewed as early

as the immediate aftermath of the global financial crisis when export growth slowed and

the infrastructure investment boom that started in the mid-2000s went sour leading to a twin

balance sheet crisis involving banks and infrastructure companies. They argue that despite

these problems and temporary adverse shocks of demonetisation and introduction of goods

and services tax (GST), Indian economy continued to grow primarily due to the income effect of

low world oil prices and the credit boom led by non-bank financial companies (NBFCs).

However, the real estate bubble that resulted eventually burst in 2019. This provides a

backdrop for the economic impacts of Covid-19 to play out in India and current and

future policy initiatives must take cognisance of these underlying conditions.

THE STATE OF THE INDIAN ECONOMY ON THE EVE OF COVID-19

OUTBREAK

In order to assess the impacts of the Covid-19 shock and to consider policy measures,

it is extremely important to take stock of the state of the economy on the eve of the

outbreak. It is widely acknowledged that the Indian economy slowed down significantly

during 2018-19. According to Subramanian and Felman (2019), trouble brewed as early

as the immediate aftermath of the global financial crisis when export growth slowed and

the infrastructure investment boom that started in the mid-2000s went sour leading to a twin

balance sheet crisis involving banks and infrastructure companies. They argue that despite

these problems and temporary adverse shocks of demonetisation and introduction of goods

and services tax (GST), Indian economy continued to grow primarily due to the income effect of

low world oil prices and the credit boom led by non-bank financial companies (NBFCs).

However, the real estate bubble that resulted eventually burst in 2019. This provides a

backdrop for the economic impacts of Covid-19 to play out in India and current and

future policy initiatives must take cognisance of these underlying conditions.

6

Let us take a look at some of the common measures used to evaluate the overall health of

an economy. The annual growth rate of real GDP continuously declined since its peak in

the first quarter of 2018. The real GDP increased by only 3.1 per cent in the first

quarter of 2020 over the corresponding quarter of 2019. While the outbreak and the

measures to prevent it in the month of March may have been partially responsible for

this significant dip in the growth rate, the declining trend that started much earlier indicates

serious problems elsewhere that had already been weakening the economy. This

performance of the economy can be further evaluated by looking at the changes in various

components on the expenditure side as well as on the production side (that is, the demand and

the supply side). On the expenditure side, private consumption spending increased only by 2.7

per cent over the first quarter of 2019 and this growth is substantially lower than the

growth rate of 6.6 per cent in the fourth quarter of 2019. Inventories were

growing at half of a percentage as compared to a growth rate of 1.1 per cent in the previous

quarter. This also indicates that firms were downsizing production in expectation of low future

demand. The gross fixed capital formation fell by 6.5 per cent over 2019:Q1. This suggests a

larger decline in business investment than a decline of 5.2% in 2019:Q4. India also

experienced significant decline in international trade: exports fell by 8.5 percent and imports by

7 per cent (MOSPI 2020).

Let us take a look at some of the common measures used to evaluate the overall health of

an economy. The annual growth rate of real GDP continuously declined since its peak in

the first quarter of 2018. The real GDP increased by only 3.1 per cent in the first

quarter of 2020 over the corresponding quarter of 2019. While the outbreak and the

measures to prevent it in the month of March may have been partially responsible for

this significant dip in the growth rate, the declining trend that started much earlier indicates

serious problems elsewhere that had already been weakening the economy. This

performance of the economy can be further evaluated by looking at the changes in various

components on the expenditure side as well as on the production side (that is, the demand and

the supply side). On the expenditure side, private consumption spending increased only by 2.7

per cent over the first quarter of 2019 and this growth is substantially lower than the

growth rate of 6.6 per cent in the fourth quarter of 2019. Inventories were

growing at half of a percentage as compared to a growth rate of 1.1 per cent in the previous

quarter. This also indicates that firms were downsizing production in expectation of low future

demand. The gross fixed capital formation fell by 6.5 per cent over 2019:Q1. This suggests a

larger decline in business investment than a decline of 5.2% in 2019:Q4. India also

experienced significant decline in international trade: exports fell by 8.5 percent and imports by

7 per cent (MOSPI 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

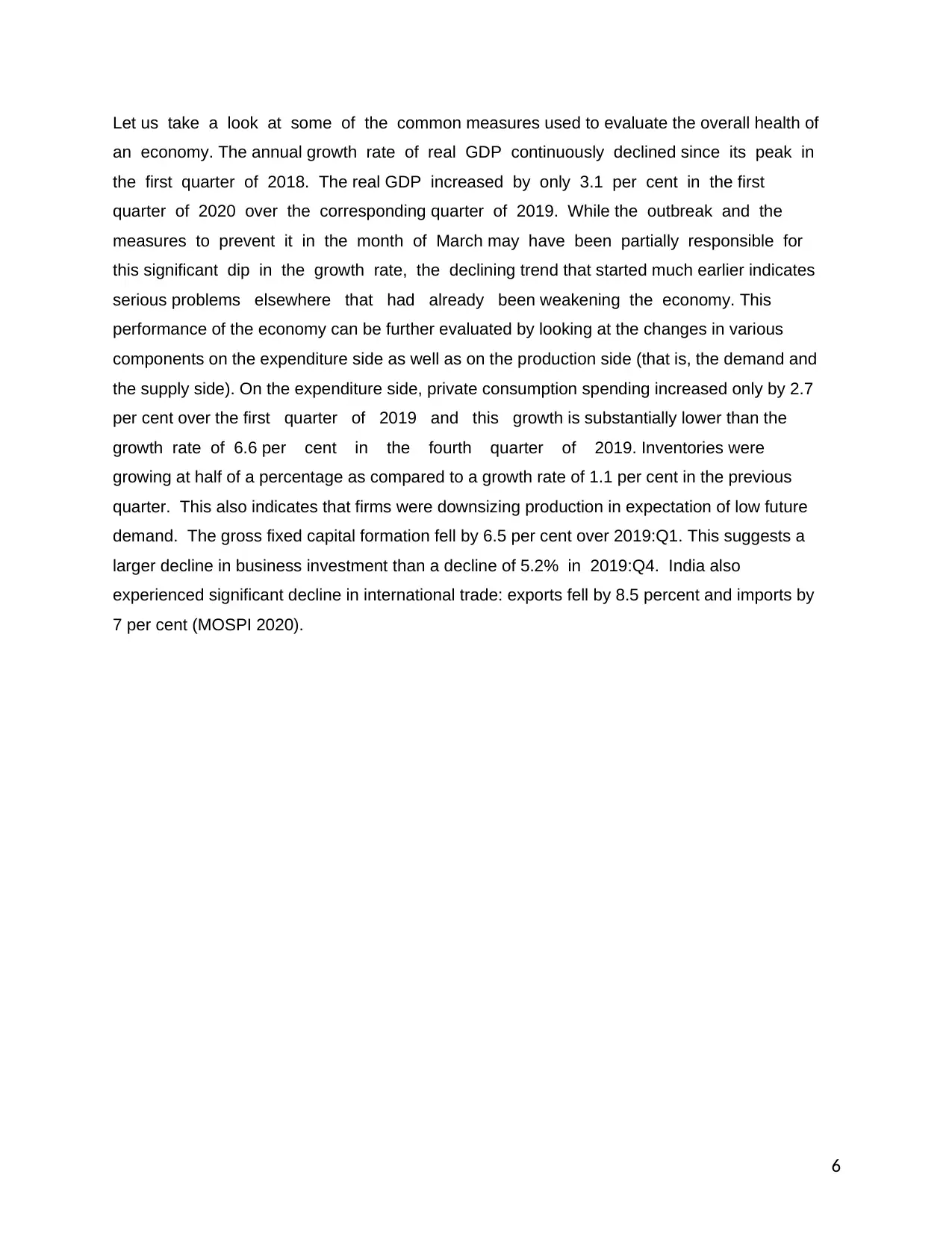

On the production side, both manufacturing and construction experienced decline:

manufacturing value-added fell by 1.4 percent over 2019:Q1 and construction by 2.2 per cent.

Note that during the fourth quarter of 2019, manufacturing declined by less than one per

cent and construction did not grow at all. Among the sectors that experienced growth,

agriculture, forestry, and fishing grew by 5.9 per cent, and mining and quarrying grew by 5.2 per

cent. Both sectors experienced some acceleration in growth. Utility services grew at 4.5 per

cent compared to its decline of 0.7 per cent in the previous quarter. Among other

services, trade, hotels, and transportation grew by 2.6 per cent, a decline from 4.3 per cent

during 2019:Q4, and finance and real estate grew by 2.4 per cent as against its growth of

3.3 per cent during the previous quarter. Of course, public administration and defence in

the government sector grew the most, by 10.1 per cent, which is slightly lower than the

growth of 10.9 per cent in the previous quarter (MOSPI 2020). Obviously, manufacturing

and construction were the trouble spots that are related to the problems we discussed at

the beginning of this section.

On the production side, both manufacturing and construction experienced decline:

manufacturing value-added fell by 1.4 percent over 2019:Q1 and construction by 2.2 per cent.

Note that during the fourth quarter of 2019, manufacturing declined by less than one per

cent and construction did not grow at all. Among the sectors that experienced growth,

agriculture, forestry, and fishing grew by 5.9 per cent, and mining and quarrying grew by 5.2 per

cent. Both sectors experienced some acceleration in growth. Utility services grew at 4.5 per

cent compared to its decline of 0.7 per cent in the previous quarter. Among other

services, trade, hotels, and transportation grew by 2.6 per cent, a decline from 4.3 per cent

during 2019:Q4, and finance and real estate grew by 2.4 per cent as against its growth of

3.3 per cent during the previous quarter. Of course, public administration and defence in

the government sector grew the most, by 10.1 per cent, which is slightly lower than the

growth of 10.9 per cent in the previous quarter (MOSPI 2020). Obviously, manufacturing

and construction were the trouble spots that are related to the problems we discussed at

the beginning of this section.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

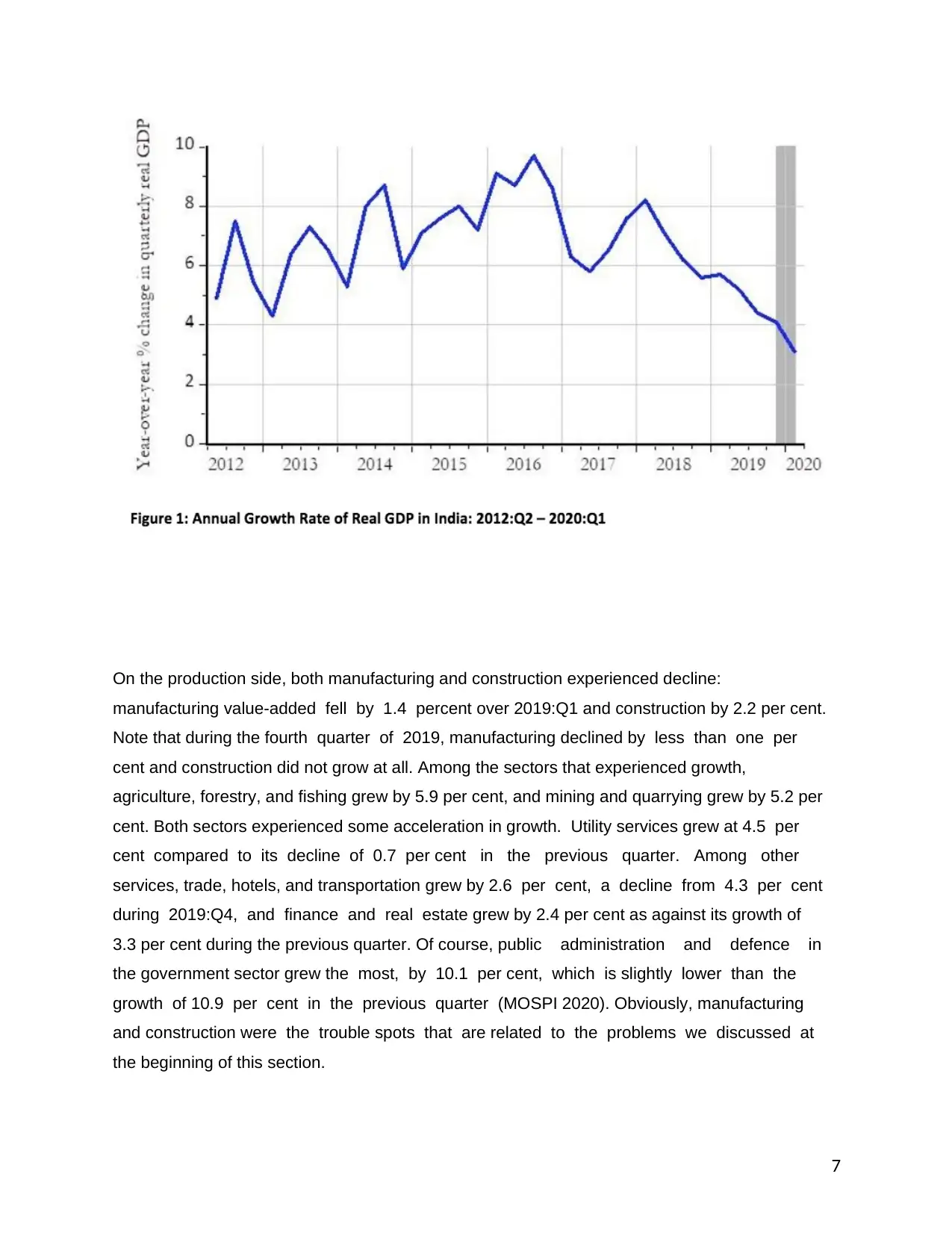

INFLATION IN INDIA AND COVID 19

Among the many ways in which Covid-19 has affected the economy, the most tangible

outcome, the one that affects each and every person, is the impact on inflation.

Even before the pandemic struck, consumer inflation had crossed the upper tolerance level of

six per cent in December 2019. India was in a tight situation with inflation higher than the

mandate, but economic growth falling fast to levels of three per cent, a rare low.

But even into the pandemic, when inflation numbers in most countries eased, Indians did not

see it going below six per cent, apart from the two months of April and May when the consumer

price index was imputed from limited data

INFLATION IN INDIA AND COVID 19

Among the many ways in which Covid-19 has affected the economy, the most tangible

outcome, the one that affects each and every person, is the impact on inflation.

Even before the pandemic struck, consumer inflation had crossed the upper tolerance level of

six per cent in December 2019. India was in a tight situation with inflation higher than the

mandate, but economic growth falling fast to levels of three per cent, a rare low.

But even into the pandemic, when inflation numbers in most countries eased, Indians did not

see it going below six per cent, apart from the two months of April and May when the consumer

price index was imputed from limited data

9

MACROECONOMIC EFFECTS

The countrywide lockdown has brought nearly all economic activities to an abrupt halt. The

disruption of demand and supply forces are likely to continue even after the lockdown is lifted. It

will take time for the economy to return to a normal state and even then social distancing

measures will continue for as long as the health shock plays out. Hence demand is unlikely to

get restored in the next several months, especially demand for non-essential goods and

services. Three major components of aggregate demand- consumption, investment, and

exports are likely to stay subdued for a prolonged period of time. In addition to the

unprecedented collapse in demand, widespread supply chain disruptions will continue for a

while due to the unavailability of raw materials, exodus of millions of migrant workers from urban

areas, slowing global trade, and shipment and travel related restrictions imposed by nearly all

affected countries. The supply chains are unlikely to normalise for some time to come. Already

several industries are struggling owing to complete disruption of supply chains from China. The

longer the crisis lasts, the more difficult it will be for firms to stay afloat. This will negatively affect

production in almost all domestic industries. This in turn will have further spill over effects on

investment, employment, income and consumption, pulling down the aggregate growth rate of

the economy.

At this stage, the possible duration of the underlying health crisis remains uncertain. In addition

there are multiple unknown factors such as the true extent of impairment suffered by the

different sectors of the economy, the magnitude of deterioration of the balance sheets of

economic agents such as firms and households, the ability of both the formal and informal

sectors to bounce back to normalcy once the lockdown is fully relaxed and most importantly, the

potential destruction of the productive capacity of the economy. Therefore, it is difficult to fully

comprehend the extent of the damage that the Indian economy is currently incurring. Some of

the statistics available now already highlight the severity and duration of the slowdown the

economy may experience going forward. After some amount of recovery in economic activity in

June, 2020 it appears that the slowdown has resumed once again in most of the sectors. The

improvement seen in most high-frequency indicators in June after the dramatic collapse in the

April-May period has begun to wane since mid June. This is presumably due to the renewed

MACROECONOMIC EFFECTS

The countrywide lockdown has brought nearly all economic activities to an abrupt halt. The

disruption of demand and supply forces are likely to continue even after the lockdown is lifted. It

will take time for the economy to return to a normal state and even then social distancing

measures will continue for as long as the health shock plays out. Hence demand is unlikely to

get restored in the next several months, especially demand for non-essential goods and

services. Three major components of aggregate demand- consumption, investment, and

exports are likely to stay subdued for a prolonged period of time. In addition to the

unprecedented collapse in demand, widespread supply chain disruptions will continue for a

while due to the unavailability of raw materials, exodus of millions of migrant workers from urban

areas, slowing global trade, and shipment and travel related restrictions imposed by nearly all

affected countries. The supply chains are unlikely to normalise for some time to come. Already

several industries are struggling owing to complete disruption of supply chains from China. The

longer the crisis lasts, the more difficult it will be for firms to stay afloat. This will negatively affect

production in almost all domestic industries. This in turn will have further spill over effects on

investment, employment, income and consumption, pulling down the aggregate growth rate of

the economy.

At this stage, the possible duration of the underlying health crisis remains uncertain. In addition

there are multiple unknown factors such as the true extent of impairment suffered by the

different sectors of the economy, the magnitude of deterioration of the balance sheets of

economic agents such as firms and households, the ability of both the formal and informal

sectors to bounce back to normalcy once the lockdown is fully relaxed and most importantly, the

potential destruction of the productive capacity of the economy. Therefore, it is difficult to fully

comprehend the extent of the damage that the Indian economy is currently incurring. Some of

the statistics available now already highlight the severity and duration of the slowdown the

economy may experience going forward. After some amount of recovery in economic activity in

June, 2020 it appears that the slowdown has resumed once again in most of the sectors. The

improvement seen in most high-frequency indicators in June after the dramatic collapse in the

April-May period has begun to wane since mid June. This is presumably due to the renewed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

lockdowns all over the country and damage to consumer sentiment and overall economic

productivity.

With all non-essential businesses closed, most industries have been witnessing a drastic

decline in sales. Revenue losses will force businesses to either close down or opt for wholesale

retrenchment of workers. Operations of a large number of companies in specific sectors will not

see business getting back to normal even after the lockdown ends, as the labour has moved

out. Even capital intensive sectors such as real estate, consumer durables, and jewellery may

not see a demand revival for several months or quarters.

lockdowns all over the country and damage to consumer sentiment and overall economic

productivity.

With all non-essential businesses closed, most industries have been witnessing a drastic

decline in sales. Revenue losses will force businesses to either close down or opt for wholesale

retrenchment of workers. Operations of a large number of companies in specific sectors will not

see business getting back to normal even after the lockdown ends, as the labour has moved

out. Even capital intensive sectors such as real estate, consumer durables, and jewellery may

not see a demand revival for several months or quarters.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

ECONOMIC EFFECTS OF THE PANDEMIC IN THE LONG RUN

The long-run impacts of this macroeconomic disturbance are primarily related to the

disruptions in accumulation of both physical and human capital. As business investment

declines, the stock of physical capital does not grow as much as it should, and it hurts long-run

growth. Similarly, as the educational institutions have been closed, there has been a disruption

in the process of human capital accumulation as well. The excessive stress on the

healthcare system due to the fight against Covid-19 may also have a negative effect on

people’s health, another component of human capital. However, because of the complex

interactions of several factors such as reduced pollution, increased hygiene, dangerous

plights of the migrant population etc., the net impact on human capital accumulation through

health outcome is nuanced and would require more careful investigation afterwards.

There are other channels through which this episode may affect the Indian economy in

the long-run. Because of reduced income, some people will be using up their savings, and

others will not be able to save as much. Overall, the total savings in the economy are

likely to drop. For the overall economy, savings are essential for financing investment.

Thus, the decrease in savings will also lead to lower capital accumulation which is

likely to slow long-run growth.

Further, various measures to fight Covid-19 at all levels, including economic recovery efforts,

will cost the governments dearly. With reduced tax earning, the government budget deficit is

going to rise. As the government borrows to finance its deficit, interest rate rises, and it

crowds out private investment –the diversion of private savings from the financing of private

investment to that of government deficit. While a larger budget deficit may be a necessity

in the short run, its persistence for a prolonged period maybe harmful to the country’s

long-run growth.

There is another way the country’s physical capital accumulation and long-run growth may

be hurt. The construction of all kinds (various infrastructure projects, commercial and

residential buildings) in megacities and large urban growth centres is heavily dependent

on the labour of migrant workers. In the wake of the nation-wide lockdown, millions of those

workers were left stranded and jobless. Media reports on their plight abound. Most of these

workers returned to their home states. If a large portion of these workers decide not to go

ECONOMIC EFFECTS OF THE PANDEMIC IN THE LONG RUN

The long-run impacts of this macroeconomic disturbance are primarily related to the

disruptions in accumulation of both physical and human capital. As business investment

declines, the stock of physical capital does not grow as much as it should, and it hurts long-run

growth. Similarly, as the educational institutions have been closed, there has been a disruption

in the process of human capital accumulation as well. The excessive stress on the

healthcare system due to the fight against Covid-19 may also have a negative effect on

people’s health, another component of human capital. However, because of the complex

interactions of several factors such as reduced pollution, increased hygiene, dangerous

plights of the migrant population etc., the net impact on human capital accumulation through

health outcome is nuanced and would require more careful investigation afterwards.

There are other channels through which this episode may affect the Indian economy in

the long-run. Because of reduced income, some people will be using up their savings, and

others will not be able to save as much. Overall, the total savings in the economy are

likely to drop. For the overall economy, savings are essential for financing investment.

Thus, the decrease in savings will also lead to lower capital accumulation which is

likely to slow long-run growth.

Further, various measures to fight Covid-19 at all levels, including economic recovery efforts,

will cost the governments dearly. With reduced tax earning, the government budget deficit is

going to rise. As the government borrows to finance its deficit, interest rate rises, and it

crowds out private investment –the diversion of private savings from the financing of private

investment to that of government deficit. While a larger budget deficit may be a necessity

in the short run, its persistence for a prolonged period maybe harmful to the country’s

long-run growth.

There is another way the country’s physical capital accumulation and long-run growth may

be hurt. The construction of all kinds (various infrastructure projects, commercial and

residential buildings) in megacities and large urban growth centres is heavily dependent

on the labour of migrant workers. In the wake of the nation-wide lockdown, millions of those

workers were left stranded and jobless. Media reports on their plight abound. Most of these

workers returned to their home states. If a large portion of these workers decide not to go

12

back immediately, the construction projects may be indefinitely delayed or permanently stalled.

This will hurt long-run growth. However, a well-thought-out fiscal stimulus with

increased government spending on infrastructure projects with a focus on economically

backward states —that also send most of the migrant workers to the growth centres —

could potentially reduce the economic stress of those workers and, by improving the

infrastructure, may lead to more regionally balanced growth.

The closure of educational institutions not only disrupts human capital formation but may

also lead to economic inequality in the long-run. For many in the rural areas and

from low socioeconomic background, education provided through the public education system

–although not perfect –is the only way and opportunity for upward socioeconomic mobility. The

psychological and economic stress created by the pandemic and lockdown may draw a full stop

to the academic endeavours of a large number of such students across the country

eliminating the possibility of climbing the ladder of upward mobility.

Crises also lay bare the deficiencies in a system and create opportunities for innovative thinking

to mend those lacunas and for making permanent changes. In India, many parts of the

socioeconomic, political, and legal system operate according to and using archaic ideology,

technology, administrative and legislative procedures that are simply not appropriate for the

twenty -first century. If both public and private parties take this opportunity to change at least

a few things to improve public health, general education, the supply chain, and the social

safety net, they may have positive long-run impacts.

back immediately, the construction projects may be indefinitely delayed or permanently stalled.

This will hurt long-run growth. However, a well-thought-out fiscal stimulus with

increased government spending on infrastructure projects with a focus on economically

backward states —that also send most of the migrant workers to the growth centres —

could potentially reduce the economic stress of those workers and, by improving the

infrastructure, may lead to more regionally balanced growth.

The closure of educational institutions not only disrupts human capital formation but may

also lead to economic inequality in the long-run. For many in the rural areas and

from low socioeconomic background, education provided through the public education system

–although not perfect –is the only way and opportunity for upward socioeconomic mobility. The

psychological and economic stress created by the pandemic and lockdown may draw a full stop

to the academic endeavours of a large number of such students across the country

eliminating the possibility of climbing the ladder of upward mobility.

Crises also lay bare the deficiencies in a system and create opportunities for innovative thinking

to mend those lacunas and for making permanent changes. In India, many parts of the

socioeconomic, political, and legal system operate according to and using archaic ideology,

technology, administrative and legislative procedures that are simply not appropriate for the

twenty -first century. If both public and private parties take this opportunity to change at least

a few things to improve public health, general education, the supply chain, and the social

safety net, they may have positive long-run impacts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.