Establish and Manage Trust Accounts: CPPDSM4006A Assessment 1

VerifiedAdded on 2023/01/03

|7

|2030

|78

Homework Assignment

AI Summary

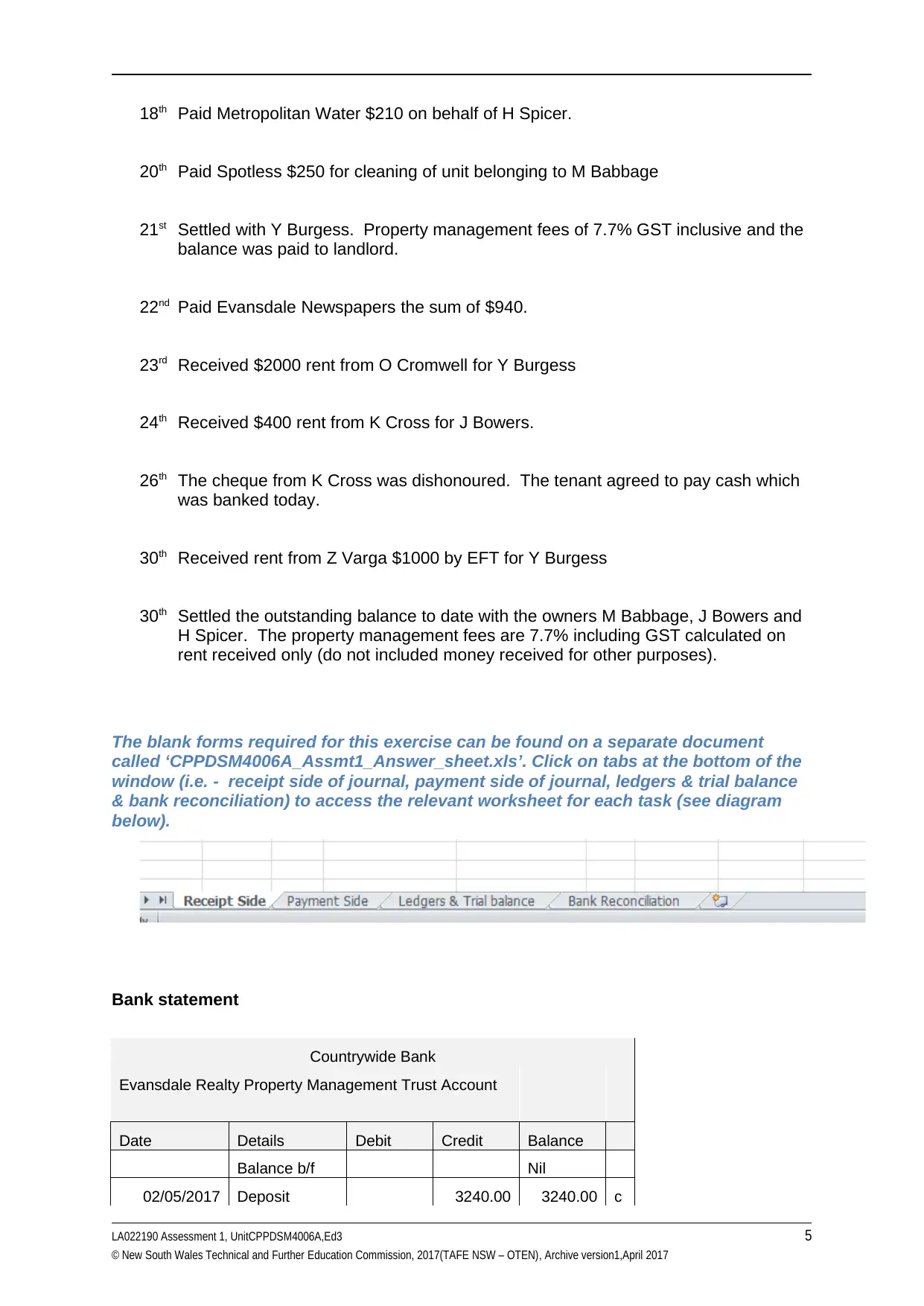

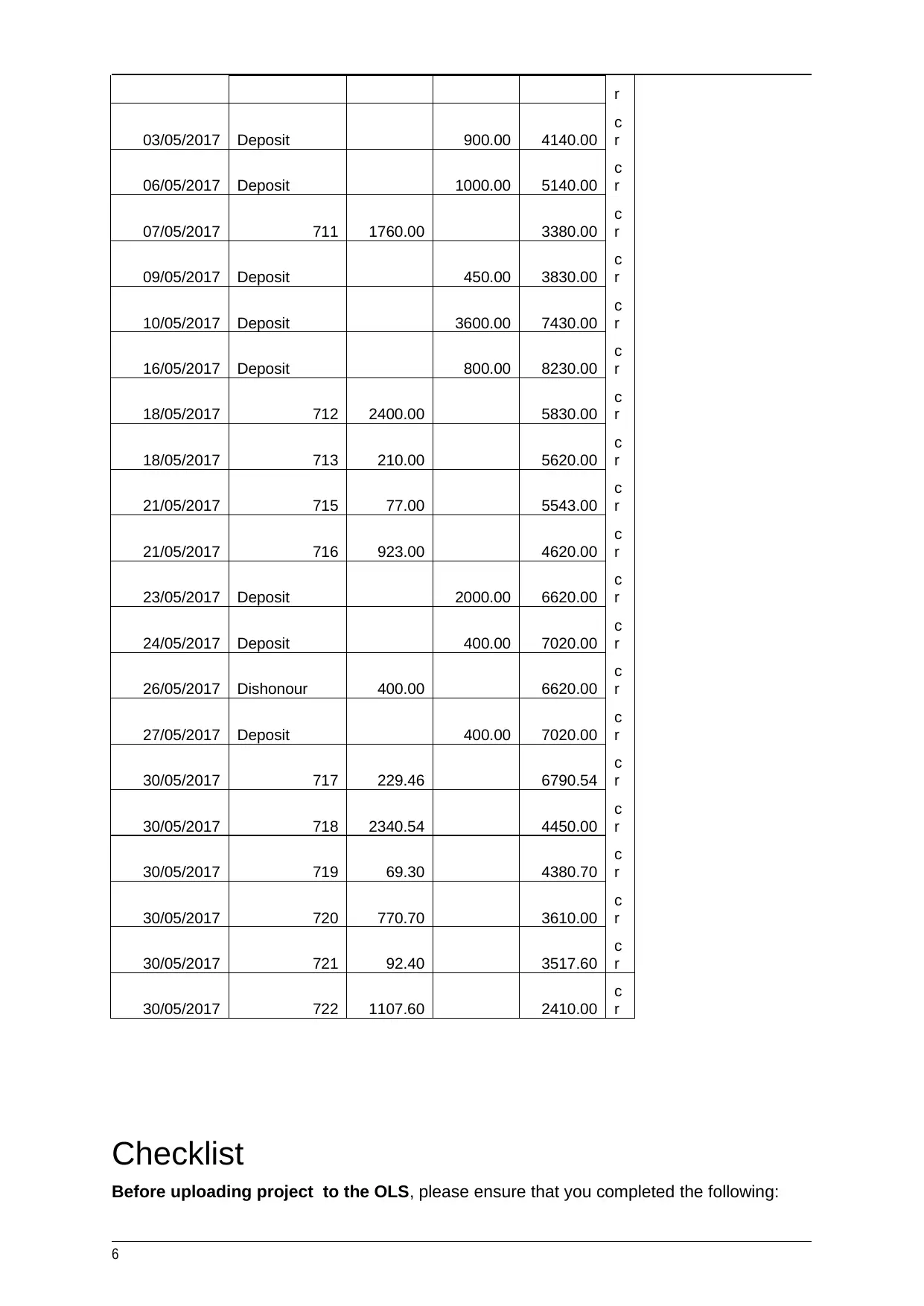

This assignment solution addresses the requirements of CPPDSM4006A, focusing on establishing and managing trust accounts within a property management context. Part A covers knowledge-based questions related to legislative requirements, internal controls, and audit procedures. It explores topics such as identifying relevant legislation, ensuring compliance, implementing security measures, and understanding the roles of auditors. Part B presents a practical activity where the student, acting as the property manager for Evansdale Realty, completes trust accounting records. This includes completing a Trust Receipt and Payment Journal, Trust Ledger, Trust Trial Balance, and a Trust Bank Reconciliation based on a provided scenario and bank statement. The solution demonstrates the ability to apply theoretical knowledge to real-world scenarios, ensuring accurate record-keeping and compliance with regulations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.