Capital Budgeting Analysis: CQU Printers' Printer Investment Project

VerifiedAdded on 2020/05/16

|21

|3472

|44

Project

AI Summary

This project report analyzes a financial decision-making scenario for CQU Printers, focusing on whether to invest in new printers. The report begins with an introduction and case overview, explaining the need to replace old printers. Part A calculates initial investments, operating cash inflows, and terminal cash flows for two new printer options (Printer A and Printer B). Part B calculates relevant cash flow streams, and Part C assesses each printer using payback period, net present value (NPV), and internal rate of return (IRR). The analysis includes detailed calculations and working notes. Part D involves drawing graphs, and Part E discusses conflicting project rankings and recommendations based on the financial metrics. The report concludes with final recommendations in Part F and references. The analysis reveals that Printer B has a shorter payback period and a higher IRR compared to Printer A, suggesting it is the more financially attractive investment for CQU Printers. The report utilizes financial concepts such as capital budgeting and cash flow analysis to provide recommendations to the company.

Running Head: Finance

1

Project Report: Finance

1

Project Report: Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

2

Contents

Introduction.......................................................................................................................3

Case Overview..................................................................................................................3

Part A................................................................................................................................4

Initial investment..........................................................................................................4

Operating cash inflows.................................................................................................5

Terminal cash flow.......................................................................................................7

Part B................................................................................................................................8

Relevant cash flow stream:...........................................................................................8

Part C..............................................................................................................................11

Payback period............................................................................................................11

Net present value........................................................................................................12

Internal rate of return..................................................................................................12

Past D..............................................................................................................................15

Draw the graph...........................................................................................................15

Part E..............................................................................................................................16

Conflicting ranking of projects...................................................................................16

Recommendation........................................................................................................16

Part F...............................................................................................................................17

Recommendation........................................................................................................17

References.......................................................................................................................18

2

Contents

Introduction.......................................................................................................................3

Case Overview..................................................................................................................3

Part A................................................................................................................................4

Initial investment..........................................................................................................4

Operating cash inflows.................................................................................................5

Terminal cash flow.......................................................................................................7

Part B................................................................................................................................8

Relevant cash flow stream:...........................................................................................8

Part C..............................................................................................................................11

Payback period............................................................................................................11

Net present value........................................................................................................12

Internal rate of return..................................................................................................12

Past D..............................................................................................................................15

Draw the graph...........................................................................................................15

Part E..............................................................................................................................16

Conflicting ranking of projects...................................................................................16

Recommendation........................................................................................................16

Part F...............................................................................................................................17

Recommendation........................................................................................................17

References.......................................................................................................................18

Finance

3

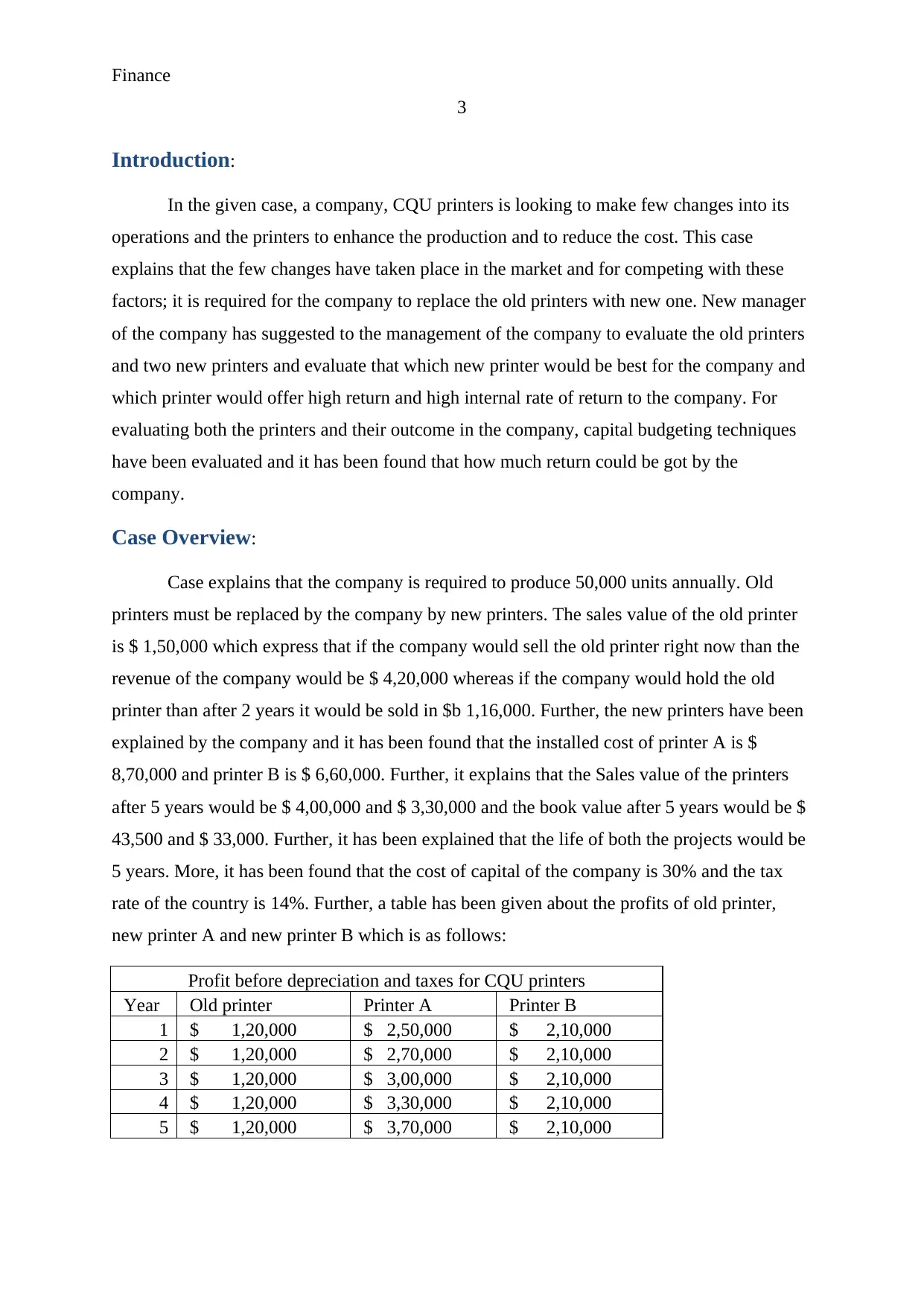

Introduction:

In the given case, a company, CQU printers is looking to make few changes into its

operations and the printers to enhance the production and to reduce the cost. This case

explains that the few changes have taken place in the market and for competing with these

factors; it is required for the company to replace the old printers with new one. New manager

of the company has suggested to the management of the company to evaluate the old printers

and two new printers and evaluate that which new printer would be best for the company and

which printer would offer high return and high internal rate of return to the company. For

evaluating both the printers and their outcome in the company, capital budgeting techniques

have been evaluated and it has been found that how much return could be got by the

company.

Case Overview:

Case explains that the company is required to produce 50,000 units annually. Old

printers must be replaced by the company by new printers. The sales value of the old printer

is $ 1,50,000 which express that if the company would sell the old printer right now than the

revenue of the company would be $ 4,20,000 whereas if the company would hold the old

printer than after 2 years it would be sold in $b 1,16,000. Further, the new printers have been

explained by the company and it has been found that the installed cost of printer A is $

8,70,000 and printer B is $ 6,60,000. Further, it explains that the Sales value of the printers

after 5 years would be $ 4,00,000 and $ 3,30,000 and the book value after 5 years would be $

43,500 and $ 33,000. Further, it has been explained that the life of both the projects would be

5 years. More, it has been found that the cost of capital of the company is 30% and the tax

rate of the country is 14%. Further, a table has been given about the profits of old printer,

new printer A and new printer B which is as follows:

Profit before depreciation and taxes for CQU printers

Year Old printer Printer A Printer B

1 $ 1,20,000 $ 2,50,000 $ 2,10,000

2 $ 1,20,000 $ 2,70,000 $ 2,10,000

3 $ 1,20,000 $ 3,00,000 $ 2,10,000

4 $ 1,20,000 $ 3,30,000 $ 2,10,000

5 $ 1,20,000 $ 3,70,000 $ 2,10,000

3

Introduction:

In the given case, a company, CQU printers is looking to make few changes into its

operations and the printers to enhance the production and to reduce the cost. This case

explains that the few changes have taken place in the market and for competing with these

factors; it is required for the company to replace the old printers with new one. New manager

of the company has suggested to the management of the company to evaluate the old printers

and two new printers and evaluate that which new printer would be best for the company and

which printer would offer high return and high internal rate of return to the company. For

evaluating both the printers and their outcome in the company, capital budgeting techniques

have been evaluated and it has been found that how much return could be got by the

company.

Case Overview:

Case explains that the company is required to produce 50,000 units annually. Old

printers must be replaced by the company by new printers. The sales value of the old printer

is $ 1,50,000 which express that if the company would sell the old printer right now than the

revenue of the company would be $ 4,20,000 whereas if the company would hold the old

printer than after 2 years it would be sold in $b 1,16,000. Further, the new printers have been

explained by the company and it has been found that the installed cost of printer A is $

8,70,000 and printer B is $ 6,60,000. Further, it explains that the Sales value of the printers

after 5 years would be $ 4,00,000 and $ 3,30,000 and the book value after 5 years would be $

43,500 and $ 33,000. Further, it has been explained that the life of both the projects would be

5 years. More, it has been found that the cost of capital of the company is 30% and the tax

rate of the country is 14%. Further, a table has been given about the profits of old printer,

new printer A and new printer B which is as follows:

Profit before depreciation and taxes for CQU printers

Year Old printer Printer A Printer B

1 $ 1,20,000 $ 2,50,000 $ 2,10,000

2 $ 1,20,000 $ 2,70,000 $ 2,10,000

3 $ 1,20,000 $ 3,00,000 $ 2,10,000

4 $ 1,20,000 $ 3,30,000 $ 2,10,000

5 $ 1,20,000 $ 3,70,000 $ 2,10,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

4

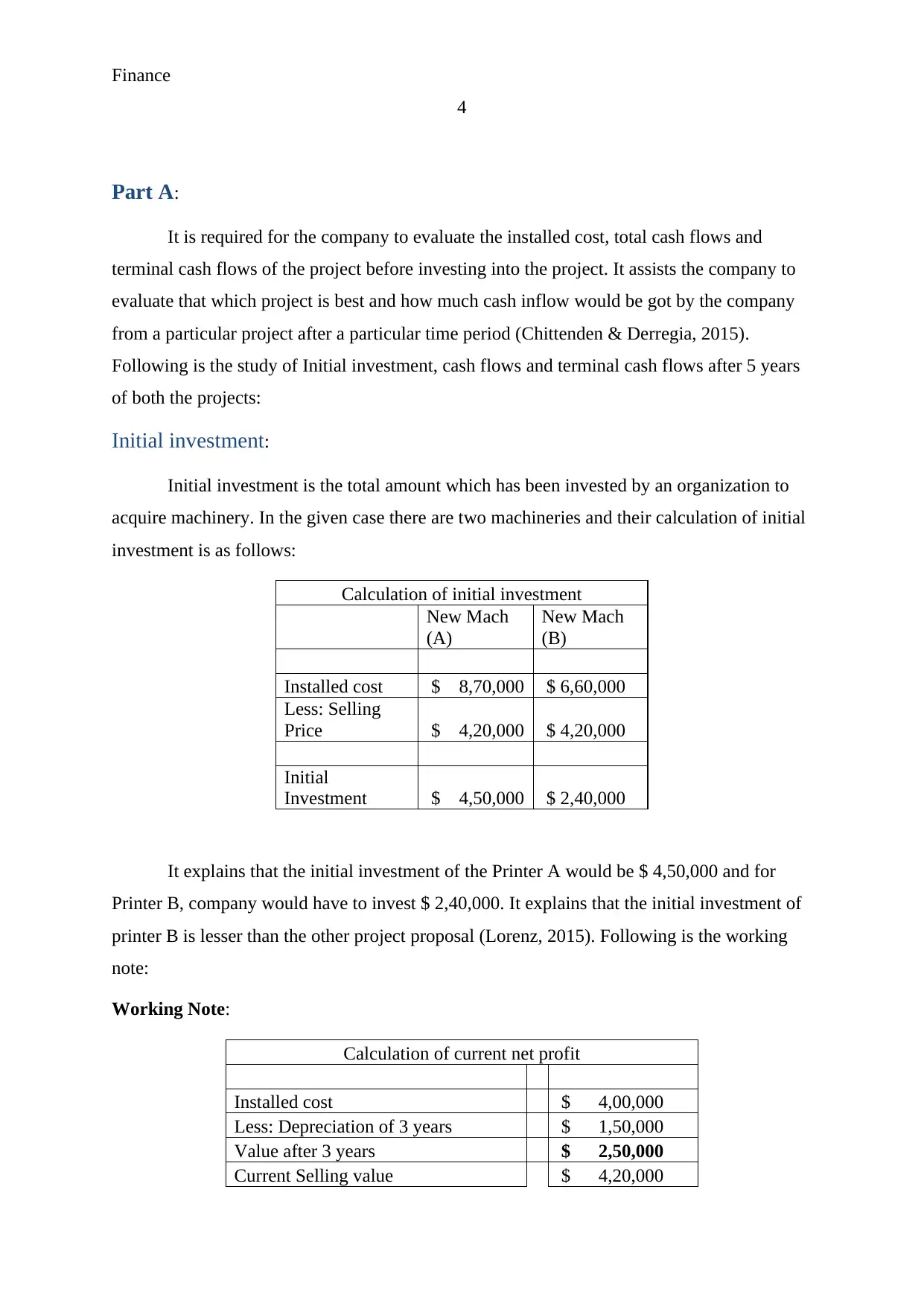

Part A:

It is required for the company to evaluate the installed cost, total cash flows and

terminal cash flows of the project before investing into the project. It assists the company to

evaluate that which project is best and how much cash inflow would be got by the company

from a particular project after a particular time period (Chittenden & Derregia, 2015).

Following is the study of Initial investment, cash flows and terminal cash flows after 5 years

of both the projects:

Initial investment:

Initial investment is the total amount which has been invested by an organization to

acquire machinery. In the given case there are two machineries and their calculation of initial

investment is as follows:

Calculation of initial investment

New Mach

(A)

New Mach

(B)

Installed cost $ 8,70,000 $ 6,60,000

Less: Selling

Price $ 4,20,000 $ 4,20,000

Initial

Investment $ 4,50,000 $ 2,40,000

It explains that the initial investment of the Printer A would be $ 4,50,000 and for

Printer B, company would have to invest $ 2,40,000. It explains that the initial investment of

printer B is lesser than the other project proposal (Lorenz, 2015). Following is the working

note:

Working Note:

Calculation of current net profit

Installed cost $ 4,00,000

Less: Depreciation of 3 years $ 1,50,000

Value after 3 years $ 2,50,000

Current Selling value $ 4,20,000

4

Part A:

It is required for the company to evaluate the installed cost, total cash flows and

terminal cash flows of the project before investing into the project. It assists the company to

evaluate that which project is best and how much cash inflow would be got by the company

from a particular project after a particular time period (Chittenden & Derregia, 2015).

Following is the study of Initial investment, cash flows and terminal cash flows after 5 years

of both the projects:

Initial investment:

Initial investment is the total amount which has been invested by an organization to

acquire machinery. In the given case there are two machineries and their calculation of initial

investment is as follows:

Calculation of initial investment

New Mach

(A)

New Mach

(B)

Installed cost $ 8,70,000 $ 6,60,000

Less: Selling

Price $ 4,20,000 $ 4,20,000

Initial

Investment $ 4,50,000 $ 2,40,000

It explains that the initial investment of the Printer A would be $ 4,50,000 and for

Printer B, company would have to invest $ 2,40,000. It explains that the initial investment of

printer B is lesser than the other project proposal (Lorenz, 2015). Following is the working

note:

Working Note:

Calculation of current net profit

Installed cost $ 4,00,000

Less: Depreciation of 3 years $ 1,50,000

Value after 3 years $ 2,50,000

Current Selling value $ 4,20,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

5

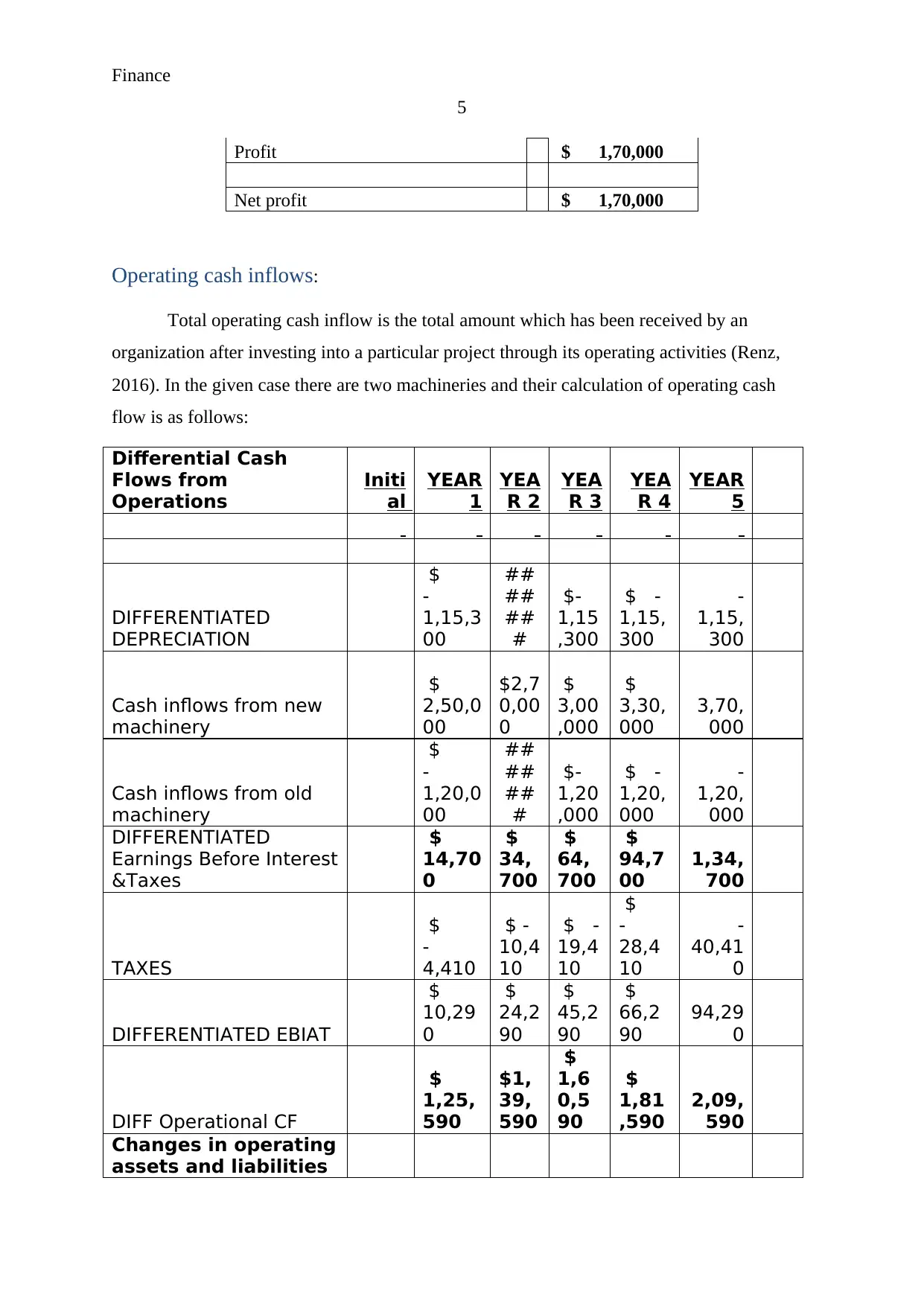

Profit $ 1,70,000

Net profit $ 1,70,000

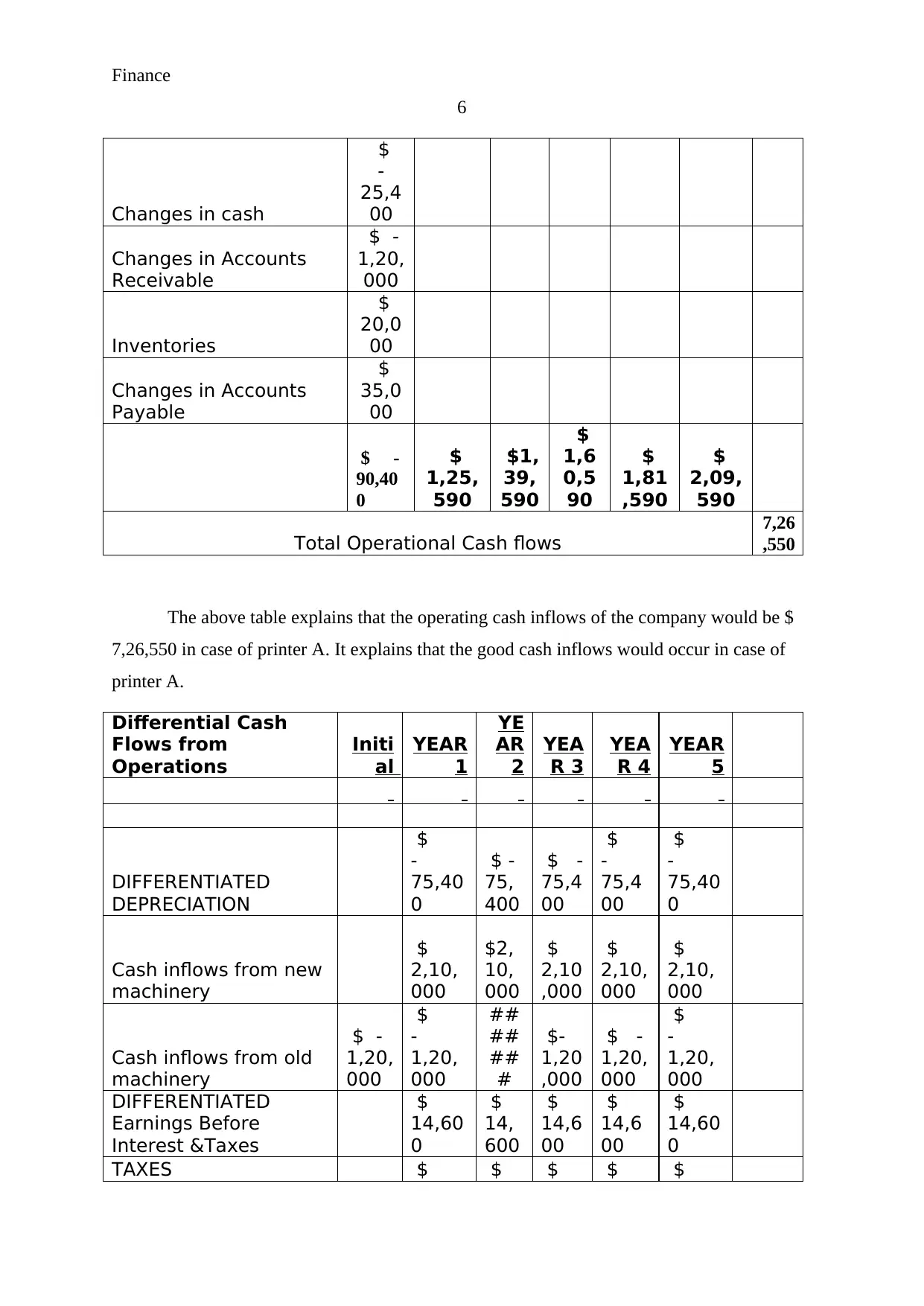

Operating cash inflows:

Total operating cash inflow is the total amount which has been received by an

organization after investing into a particular project through its operating activities (Renz,

2016). In the given case there are two machineries and their calculation of operating cash

flow is as follows:

Differential Cash

Flows from

Operations

Initi

al

YEAR

1

YEA

R 2

YEA

R 3

YEA

R 4

YEAR

5

DIFFERENTIATED

DEPRECIATION

$

-

1,15,3

00

##

##

##

#

$-

1,15

,300

$ -

1,15,

300

-

1,15,

300

Cash inflows from new

machinery

$

2,50,0

00

$2,7

0,00

0

$

3,00

,000

$

3,30,

000

3,70,

000

Cash inflows from old

machinery

$

-

1,20,0

00

##

##

##

#

$-

1,20

,000

$ -

1,20,

000

-

1,20,

000

DIFFERENTIATED

Earnings Before Interest

&Taxes

$

14,70

0

$

34,

700

$

64,

700

$

94,7

00

1,34,

700

TAXES

$

-

4,410

$ -

10,4

10

$ -

19,4

10

$

-

28,4

10

-

40,41

0

DIFFERENTIATED EBIAT

$

10,29

0

$

24,2

90

$

45,2

90

$

66,2

90

94,29

0

DIFF Operational CF

$

1,25,

590

$1,

39,

590

$

1,6

0,5

90

$

1,81

,590

2,09,

590

Changes in operating

assets and liabilities

5

Profit $ 1,70,000

Net profit $ 1,70,000

Operating cash inflows:

Total operating cash inflow is the total amount which has been received by an

organization after investing into a particular project through its operating activities (Renz,

2016). In the given case there are two machineries and their calculation of operating cash

flow is as follows:

Differential Cash

Flows from

Operations

Initi

al

YEAR

1

YEA

R 2

YEA

R 3

YEA

R 4

YEAR

5

DIFFERENTIATED

DEPRECIATION

$

-

1,15,3

00

##

##

##

#

$-

1,15

,300

$ -

1,15,

300

-

1,15,

300

Cash inflows from new

machinery

$

2,50,0

00

$2,7

0,00

0

$

3,00

,000

$

3,30,

000

3,70,

000

Cash inflows from old

machinery

$

-

1,20,0

00

##

##

##

#

$-

1,20

,000

$ -

1,20,

000

-

1,20,

000

DIFFERENTIATED

Earnings Before Interest

&Taxes

$

14,70

0

$

34,

700

$

64,

700

$

94,7

00

1,34,

700

TAXES

$

-

4,410

$ -

10,4

10

$ -

19,4

10

$

-

28,4

10

-

40,41

0

DIFFERENTIATED EBIAT

$

10,29

0

$

24,2

90

$

45,2

90

$

66,2

90

94,29

0

DIFF Operational CF

$

1,25,

590

$1,

39,

590

$

1,6

0,5

90

$

1,81

,590

2,09,

590

Changes in operating

assets and liabilities

Finance

6

Changes in cash

$

-

25,4

00

Changes in Accounts

Receivable

$ -

1,20,

000

Inventories

$

20,0

00

Changes in Accounts

Payable

$

35,0

00

$ -

90,40

0

$

1,25,

590

$1,

39,

590

$

1,6

0,5

90

$

1,81

,590

$

2,09,

590

Total Operational Cash flows

7,26

,550

The above table explains that the operating cash inflows of the company would be $

7,26,550 in case of printer A. It explains that the good cash inflows would occur in case of

printer A.

Differential Cash

Flows from

Operations

Initi

al

YEAR

1

YE

AR

2

YEA

R 3

YEA

R 4

YEAR

5

DIFFERENTIATED

DEPRECIATION

$

-

75,40

0

$ -

75,

400

$ -

75,4

00

$

-

75,4

00

$

-

75,40

0

Cash inflows from new

machinery

$

2,10,

000

$2,

10,

000

$

2,10

,000

$

2,10,

000

$

2,10,

000

Cash inflows from old

machinery

$ -

1,20,

000

$

-

1,20,

000

##

##

##

#

$-

1,20

,000

$ -

1,20,

000

$

-

1,20,

000

DIFFERENTIATED

Earnings Before

Interest &Taxes

$

14,60

0

$

14,

600

$

14,6

00

$

14,6

00

$

14,60

0

TAXES $ $ $ $ $

6

Changes in cash

$

-

25,4

00

Changes in Accounts

Receivable

$ -

1,20,

000

Inventories

$

20,0

00

Changes in Accounts

Payable

$

35,0

00

$ -

90,40

0

$

1,25,

590

$1,

39,

590

$

1,6

0,5

90

$

1,81

,590

$

2,09,

590

Total Operational Cash flows

7,26

,550

The above table explains that the operating cash inflows of the company would be $

7,26,550 in case of printer A. It explains that the good cash inflows would occur in case of

printer A.

Differential Cash

Flows from

Operations

Initi

al

YEAR

1

YE

AR

2

YEA

R 3

YEA

R 4

YEAR

5

DIFFERENTIATED

DEPRECIATION

$

-

75,40

0

$ -

75,

400

$ -

75,4

00

$

-

75,4

00

$

-

75,40

0

Cash inflows from new

machinery

$

2,10,

000

$2,

10,

000

$

2,10

,000

$

2,10,

000

$

2,10,

000

Cash inflows from old

machinery

$ -

1,20,

000

$

-

1,20,

000

##

##

##

#

$-

1,20

,000

$ -

1,20,

000

$

-

1,20,

000

DIFFERENTIATED

Earnings Before

Interest &Taxes

$

14,60

0

$

14,

600

$

14,6

00

$

14,6

00

$

14,60

0

TAXES $ $ $ $ $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

7

-

4,380

-

4,3

80

-

4,38

0

-

4,38

0

-

4,380

DIFFERENTIATED

EBIAT

$

10,22

0

$

10,

220

$

10,2

20

$

10,2

20

$

10,22

0

DIFF Operational CF

$

85,62

0

$

85,

620

$

85,6

20

$

85,6

20

$

85,62

0

Total Operational Cash flows

$

4,28,1

00

The above table explains that the operating cash inflows of the company would be $

4,28,100 in case of printer B. It explains that the good cash inflows would occur in case of

printer B. Though, in comparison of Printer A, cash inflow of printer B is quite lesser (Otley,

2016).

Working Note:

Years 1 to 5

Differential Depreciation

DEPRECIAT NEW

MACHIN

-

1,65,300

-1,25,400

DEPRECIAT OLD

MACHIN

50,000 50,000

Differential Depreciation -

1,15,300

-75,400

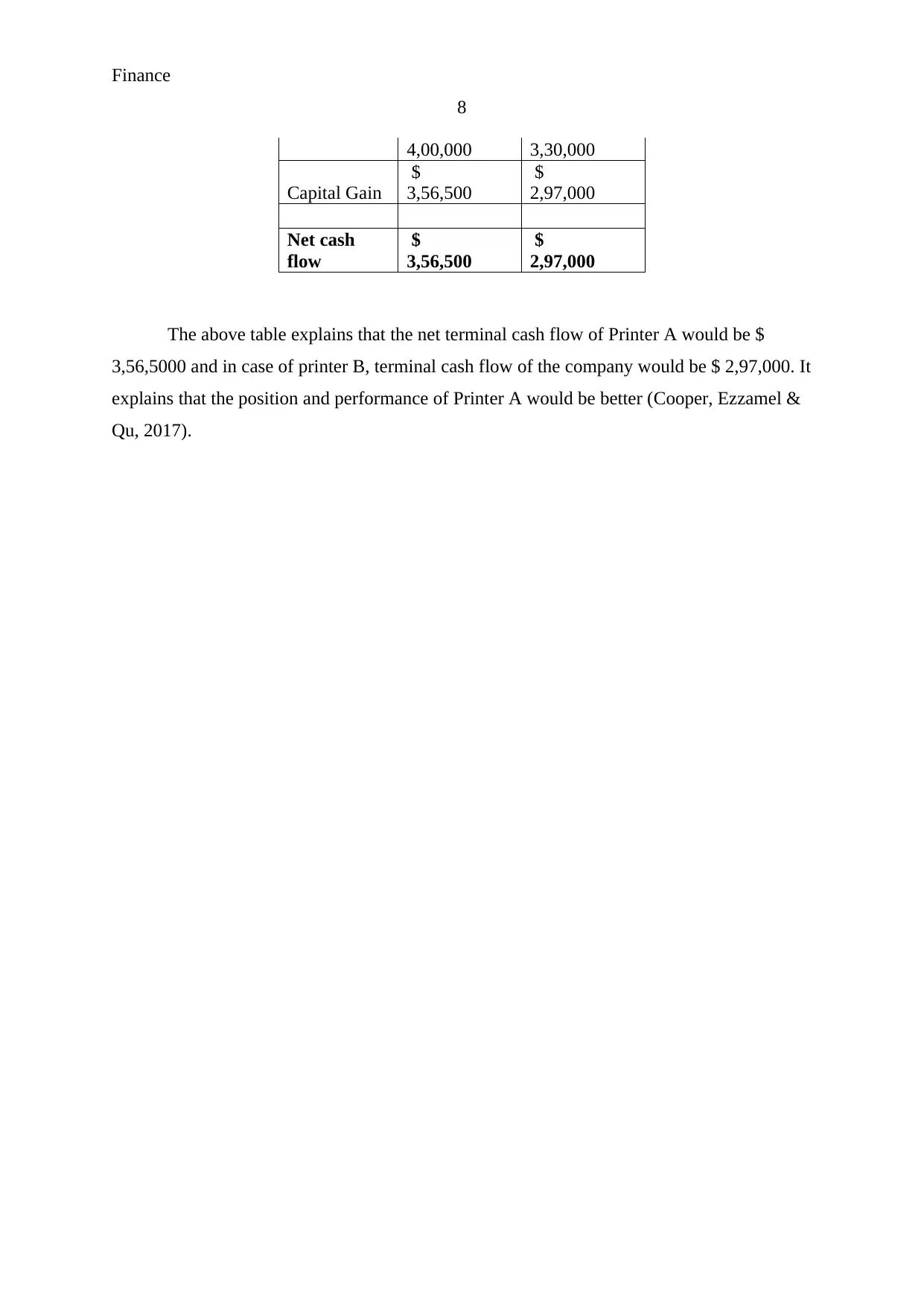

Terminal cash flow:

Terminal cash flows are the total amount which has been received by an organization

after terminating a project or machinery. This amount is calculated at the end of a project. In

the given case there are two machineries and their calculation of terminal cash flows are as

follows:

Calculation of terminal cash flows

Printer A Printer B

Salvage

Value

$

43,500

$

33,000

Book Value $ $

7

-

4,380

-

4,3

80

-

4,38

0

-

4,38

0

-

4,380

DIFFERENTIATED

EBIAT

$

10,22

0

$

10,

220

$

10,2

20

$

10,2

20

$

10,22

0

DIFF Operational CF

$

85,62

0

$

85,

620

$

85,6

20

$

85,6

20

$

85,62

0

Total Operational Cash flows

$

4,28,1

00

The above table explains that the operating cash inflows of the company would be $

4,28,100 in case of printer B. It explains that the good cash inflows would occur in case of

printer B. Though, in comparison of Printer A, cash inflow of printer B is quite lesser (Otley,

2016).

Working Note:

Years 1 to 5

Differential Depreciation

DEPRECIAT NEW

MACHIN

-

1,65,300

-1,25,400

DEPRECIAT OLD

MACHIN

50,000 50,000

Differential Depreciation -

1,15,300

-75,400

Terminal cash flow:

Terminal cash flows are the total amount which has been received by an organization

after terminating a project or machinery. This amount is calculated at the end of a project. In

the given case there are two machineries and their calculation of terminal cash flows are as

follows:

Calculation of terminal cash flows

Printer A Printer B

Salvage

Value

$

43,500

$

33,000

Book Value $ $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

8

4,00,000 3,30,000

Capital Gain

$

3,56,500

$

2,97,000

Net cash

flow

$

3,56,500

$

2,97,000

The above table explains that the net terminal cash flow of Printer A would be $

3,56,5000 and in case of printer B, terminal cash flow of the company would be $ 2,97,000. It

explains that the position and performance of Printer A would be better (Cooper, Ezzamel &

Qu, 2017).

8

4,00,000 3,30,000

Capital Gain

$

3,56,500

$

2,97,000

Net cash

flow

$

3,56,500

$

2,97,000

The above table explains that the net terminal cash flow of Printer A would be $

3,56,5000 and in case of printer B, terminal cash flow of the company would be $ 2,97,000. It

explains that the position and performance of Printer A would be better (Cooper, Ezzamel &

Qu, 2017).

Finance

9

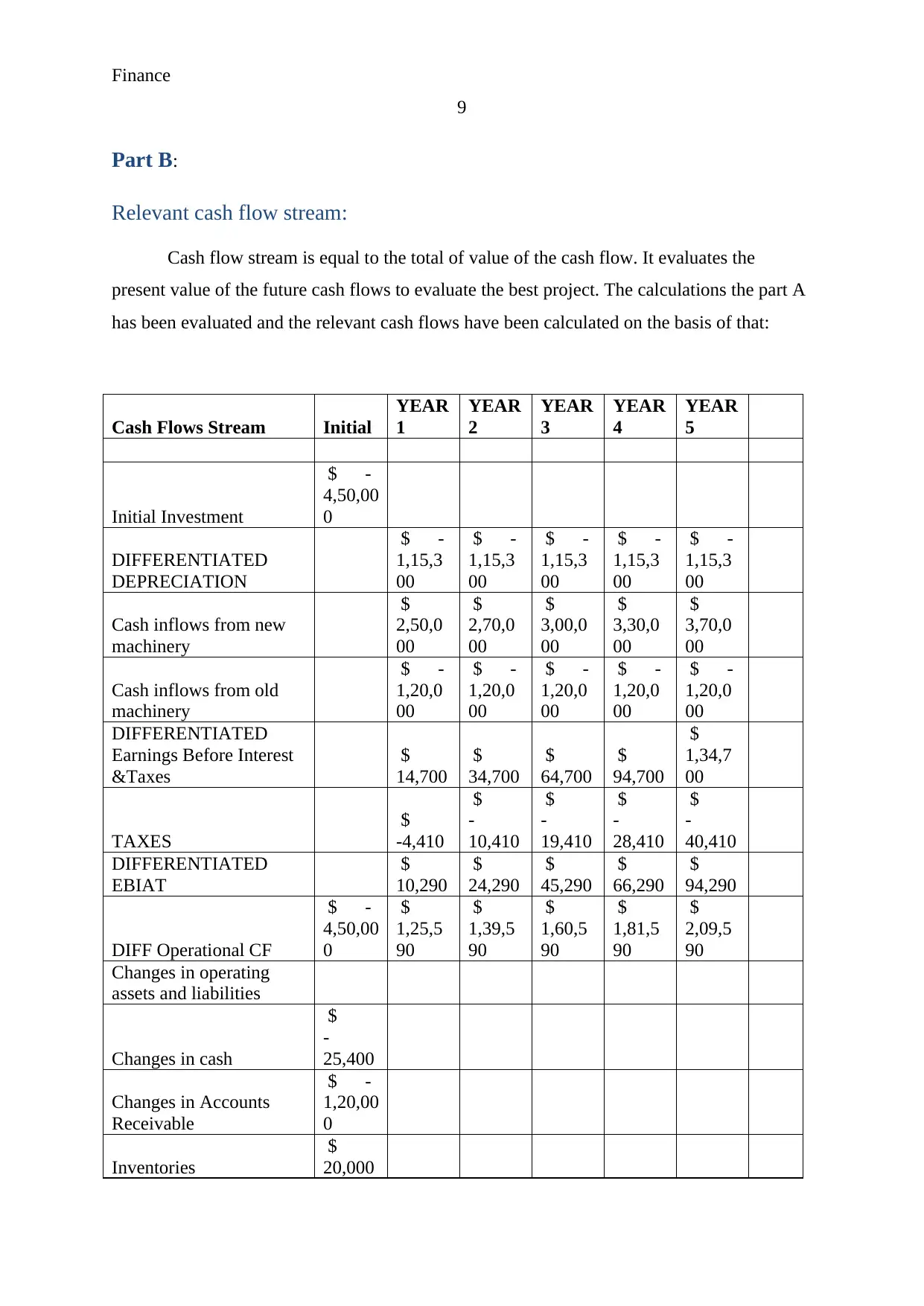

Part B:

Relevant cash flow stream:

Cash flow stream is equal to the total of value of the cash flow. It evaluates the

present value of the future cash flows to evaluate the best project. The calculations the part A

has been evaluated and the relevant cash flows have been calculated on the basis of that:

Cash Flows Stream Initial

YEAR

1

YEAR

2

YEAR

3

YEAR

4

YEAR

5

Initial Investment

$ -

4,50,00

0

DIFFERENTIATED

DEPRECIATION

$ -

1,15,3

00

$ -

1,15,3

00

$ -

1,15,3

00

$ -

1,15,3

00

$ -

1,15,3

00

Cash inflows from new

machinery

$

2,50,0

00

$

2,70,0

00

$

3,00,0

00

$

3,30,0

00

$

3,70,0

00

Cash inflows from old

machinery

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

DIFFERENTIATED

Earnings Before Interest

&Taxes

$

14,700

$

34,700

$

64,700

$

94,700

$

1,34,7

00

TAXES

$

-4,410

$

-

10,410

$

-

19,410

$

-

28,410

$

-

40,410

DIFFERENTIATED

EBIAT

$

10,290

$

24,290

$

45,290

$

66,290

$

94,290

DIFF Operational CF

$ -

4,50,00

0

$

1,25,5

90

$

1,39,5

90

$

1,60,5

90

$

1,81,5

90

$

2,09,5

90

Changes in operating

assets and liabilities

Changes in cash

$

-

25,400

Changes in Accounts

Receivable

$ -

1,20,00

0

Inventories

$

20,000

9

Part B:

Relevant cash flow stream:

Cash flow stream is equal to the total of value of the cash flow. It evaluates the

present value of the future cash flows to evaluate the best project. The calculations the part A

has been evaluated and the relevant cash flows have been calculated on the basis of that:

Cash Flows Stream Initial

YEAR

1

YEAR

2

YEAR

3

YEAR

4

YEAR

5

Initial Investment

$ -

4,50,00

0

DIFFERENTIATED

DEPRECIATION

$ -

1,15,3

00

$ -

1,15,3

00

$ -

1,15,3

00

$ -

1,15,3

00

$ -

1,15,3

00

Cash inflows from new

machinery

$

2,50,0

00

$

2,70,0

00

$

3,00,0

00

$

3,30,0

00

$

3,70,0

00

Cash inflows from old

machinery

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

DIFFERENTIATED

Earnings Before Interest

&Taxes

$

14,700

$

34,700

$

64,700

$

94,700

$

1,34,7

00

TAXES

$

-4,410

$

-

10,410

$

-

19,410

$

-

28,410

$

-

40,410

DIFFERENTIATED

EBIAT

$

10,290

$

24,290

$

45,290

$

66,290

$

94,290

DIFF Operational CF

$ -

4,50,00

0

$

1,25,5

90

$

1,39,5

90

$

1,60,5

90

$

1,81,5

90

$

2,09,5

90

Changes in operating

assets and liabilities

Changes in cash

$

-

25,400

Changes in Accounts

Receivable

$ -

1,20,00

0

Inventories

$

20,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance

10

Changes in Accounts

Payable

$

35,000

$ -

5,40,40

0

$

1,25,5

90

$

1,39,5

90

$

1,60,5

90

$

1,81,5

90

$

2,09,5

90

Salvage Value

$

43,500

Book Value

$

4,00,0

00

Capital Gain

$

3,56,5

00

Tax on capital gain

Net cash flow

$

3,56,5

00

Total Operational Cash

flows

$ -

5,40,40

0

$

1,25,5

90

$

1,39,5

90

$

1,60,5

90

$

1,81,5

90

$

5,66,0

90

$6,3

3,05

0

Present value factor 1 0.8772 0.7695 0.6750 0.5921 0.5194

Present value

-

540400

11016

6.6667

10740

9.9723

10839

3.6758

10751

5.8576

29400

9.4072

1,87,

096

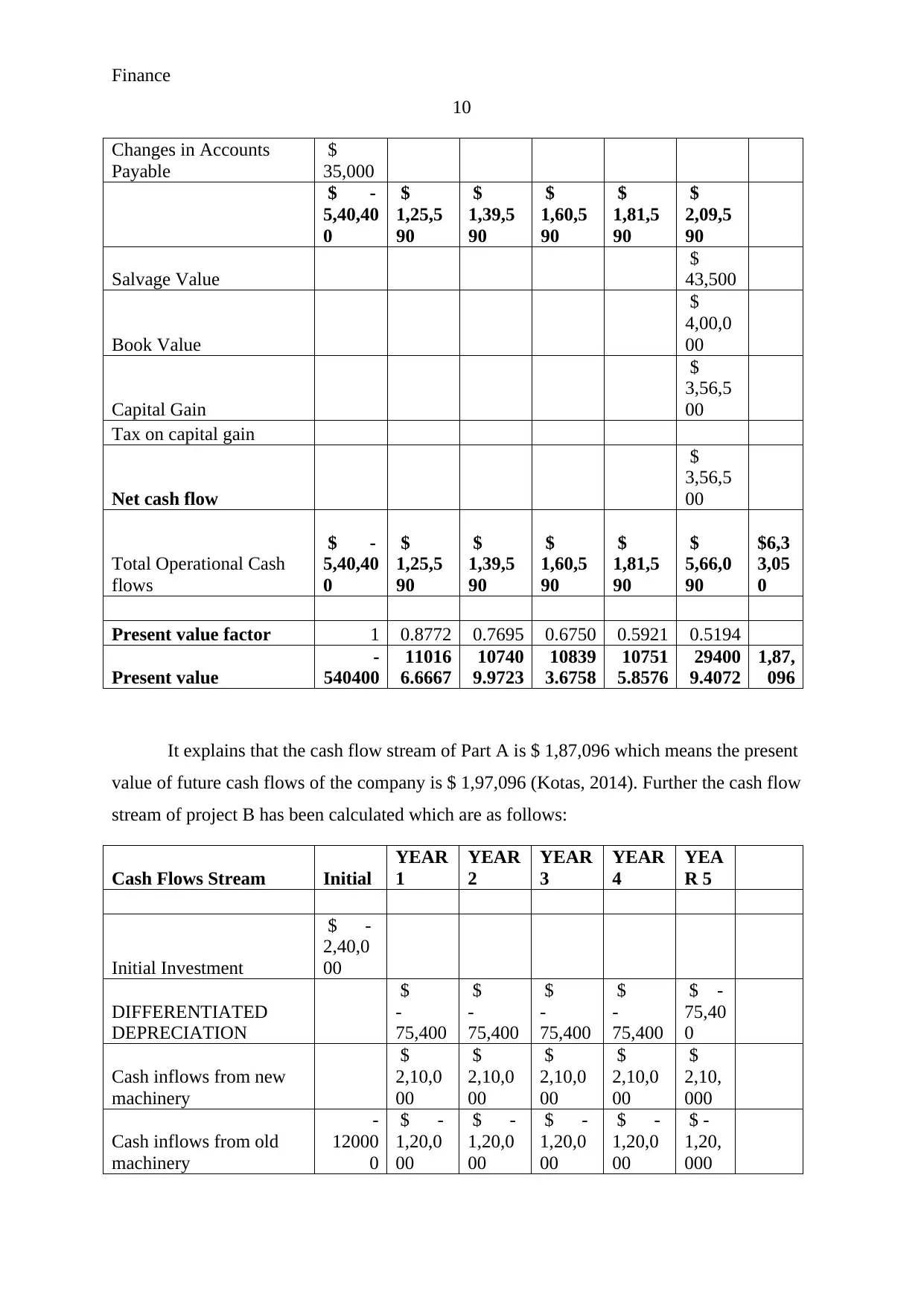

It explains that the cash flow stream of Part A is $ 1,87,096 which means the present

value of future cash flows of the company is $ 1,97,096 (Kotas, 2014). Further the cash flow

stream of project B has been calculated which are as follows:

Cash Flows Stream Initial

YEAR

1

YEAR

2

YEAR

3

YEAR

4

YEA

R 5

Initial Investment

$ -

2,40,0

00

DIFFERENTIATED

DEPRECIATION

$

-

75,400

$

-

75,400

$

-

75,400

$

-

75,400

$ -

75,40

0

Cash inflows from new

machinery

$

2,10,0

00

$

2,10,0

00

$

2,10,0

00

$

2,10,0

00

$

2,10,

000

Cash inflows from old

machinery

-

12000

0

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,

000

10

Changes in Accounts

Payable

$

35,000

$ -

5,40,40

0

$

1,25,5

90

$

1,39,5

90

$

1,60,5

90

$

1,81,5

90

$

2,09,5

90

Salvage Value

$

43,500

Book Value

$

4,00,0

00

Capital Gain

$

3,56,5

00

Tax on capital gain

Net cash flow

$

3,56,5

00

Total Operational Cash

flows

$ -

5,40,40

0

$

1,25,5

90

$

1,39,5

90

$

1,60,5

90

$

1,81,5

90

$

5,66,0

90

$6,3

3,05

0

Present value factor 1 0.8772 0.7695 0.6750 0.5921 0.5194

Present value

-

540400

11016

6.6667

10740

9.9723

10839

3.6758

10751

5.8576

29400

9.4072

1,87,

096

It explains that the cash flow stream of Part A is $ 1,87,096 which means the present

value of future cash flows of the company is $ 1,97,096 (Kotas, 2014). Further the cash flow

stream of project B has been calculated which are as follows:

Cash Flows Stream Initial

YEAR

1

YEAR

2

YEAR

3

YEAR

4

YEA

R 5

Initial Investment

$ -

2,40,0

00

DIFFERENTIATED

DEPRECIATION

$

-

75,400

$

-

75,400

$

-

75,400

$

-

75,400

$ -

75,40

0

Cash inflows from new

machinery

$

2,10,0

00

$

2,10,0

00

$

2,10,0

00

$

2,10,0

00

$

2,10,

000

Cash inflows from old

machinery

-

12000

0

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,0

00

$ -

1,20,

000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance

11

DIFFERENTIATED

Earnings Before Interest

&Taxes

$

14,600

$

14,600

$

14,600

$

14,600

$

14,60

0

TAXES

$

-4,380

$

-4,380

$

-4,380

$

-4,380

$

-

4,380

DIFFERENTIATED

EBIAT

$

10,220

$

10,220

$

10,220

$

10,220

$

10,22

0

DIFF Operational CF

$ -

2,40,0

00

$

85,620

$

85,620

$

85,620

$

85,620

$

85,62

0

Salvage Value

$

33,00

0

Book Value

$

3,30,

000

Capital Gain

$

2,97,

000

Tax on capital gain

Net cash flow

2970

00

Total Operational Cash

flows

$ -

2,40,0

00

$

85,620

$

85,620

$

85,620

$

85,620

$

3,82,

620

$

4,85,1

00

Present value factor

$

1

$

1

$

1

$

1

$

1

$

1

Present value

$ -

2,40,0

00

$

75,105

$

65,882

$

57,791

$

50,694

$

1,98,

721

$

2,08,1

93

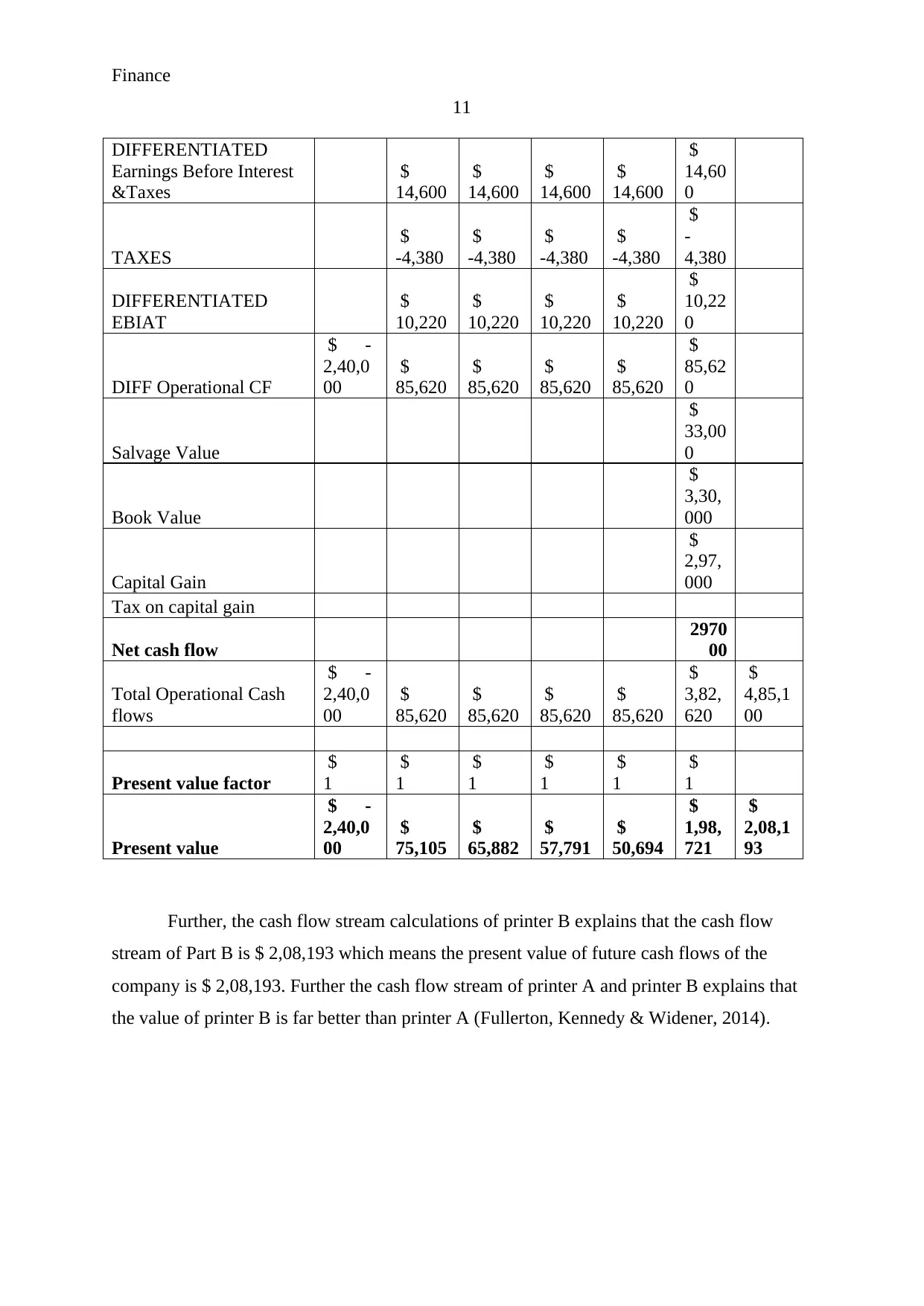

Further, the cash flow stream calculations of printer B explains that the cash flow

stream of Part B is $ 2,08,193 which means the present value of future cash flows of the

company is $ 2,08,193. Further the cash flow stream of printer A and printer B explains that

the value of printer B is far better than printer A (Fullerton, Kennedy & Widener, 2014).

11

DIFFERENTIATED

Earnings Before Interest

&Taxes

$

14,600

$

14,600

$

14,600

$

14,600

$

14,60

0

TAXES

$

-4,380

$

-4,380

$

-4,380

$

-4,380

$

-

4,380

DIFFERENTIATED

EBIAT

$

10,220

$

10,220

$

10,220

$

10,220

$

10,22

0

DIFF Operational CF

$ -

2,40,0

00

$

85,620

$

85,620

$

85,620

$

85,620

$

85,62

0

Salvage Value

$

33,00

0

Book Value

$

3,30,

000

Capital Gain

$

2,97,

000

Tax on capital gain

Net cash flow

2970

00

Total Operational Cash

flows

$ -

2,40,0

00

$

85,620

$

85,620

$

85,620

$

85,620

$

3,82,

620

$

4,85,1

00

Present value factor

$

1

$

1

$

1

$

1

$

1

$

1

Present value

$ -

2,40,0

00

$

75,105

$

65,882

$

57,791

$

50,694

$

1,98,

721

$

2,08,1

93

Further, the cash flow stream calculations of printer B explains that the cash flow

stream of Part B is $ 2,08,193 which means the present value of future cash flows of the

company is $ 2,08,193. Further the cash flow stream of printer A and printer B explains that

the value of printer B is far better than printer A (Fullerton, Kennedy & Widener, 2014).

Finance

12

Part C:

After evaluating the cash flows of both the projects, the NPV, IRR and payback

period of both the printers have been calculated to evaluate the best project. Capital

budgeting techniques makes it easy for the company to measure the changes and make a

better decision:

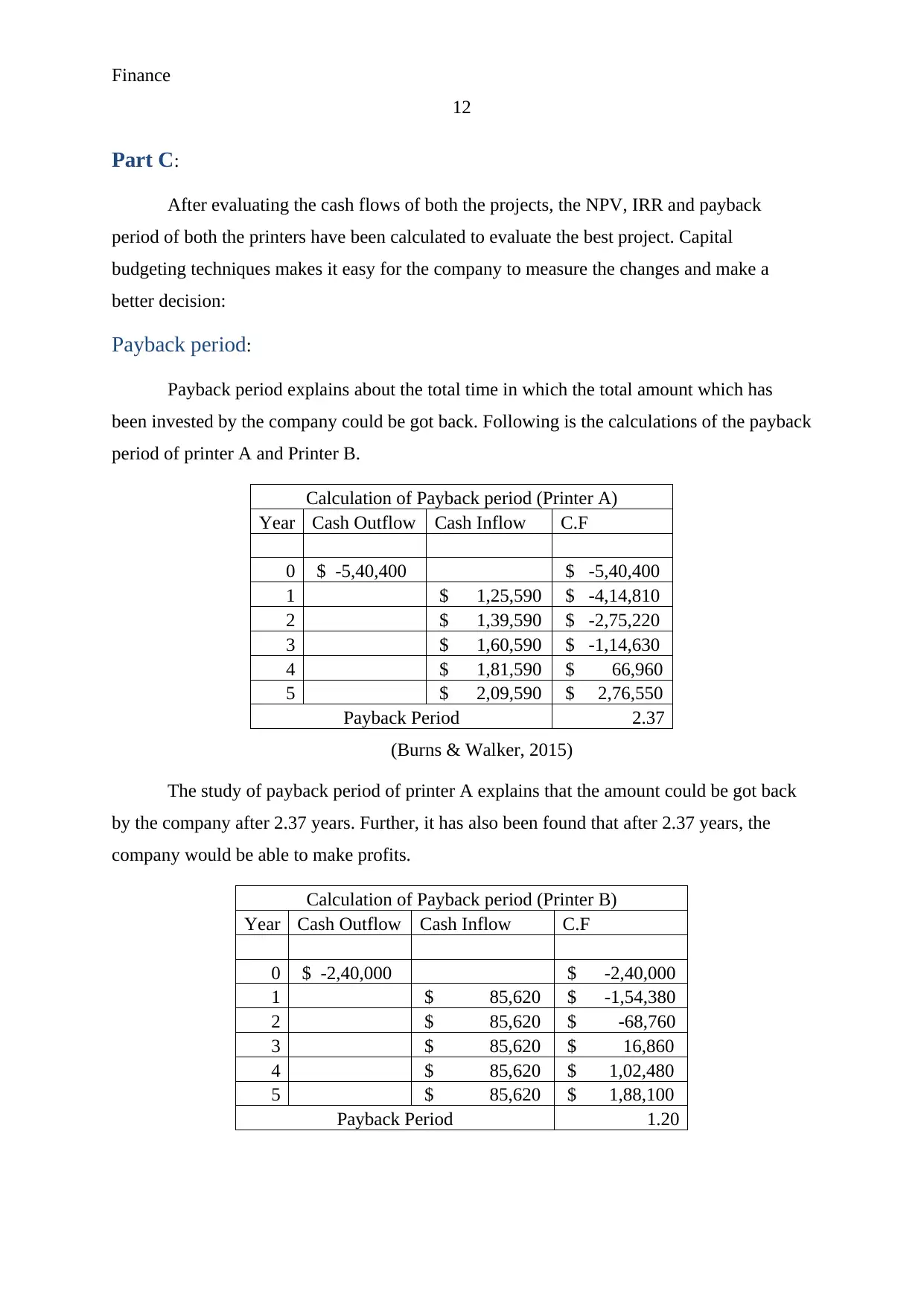

Payback period:

Payback period explains about the total time in which the total amount which has

been invested by the company could be got back. Following is the calculations of the payback

period of printer A and Printer B.

Calculation of Payback period (Printer A)

Year Cash Outflow Cash Inflow C.F

0 $ -5,40,400 $ -5,40,400

1 $ 1,25,590 $ -4,14,810

2 $ 1,39,590 $ -2,75,220

3 $ 1,60,590 $ -1,14,630

4 $ 1,81,590 $ 66,960

5 $ 2,09,590 $ 2,76,550

Payback Period 2.37

(Burns & Walker, 2015)

The study of payback period of printer A explains that the amount could be got back

by the company after 2.37 years. Further, it has also been found that after 2.37 years, the

company would be able to make profits.

Calculation of Payback period (Printer B)

Year Cash Outflow Cash Inflow C.F

0 $ -2,40,000 $ -2,40,000

1 $ 85,620 $ -1,54,380

2 $ 85,620 $ -68,760

3 $ 85,620 $ 16,860

4 $ 85,620 $ 1,02,480

5 $ 85,620 $ 1,88,100

Payback Period 1.20

12

Part C:

After evaluating the cash flows of both the projects, the NPV, IRR and payback

period of both the printers have been calculated to evaluate the best project. Capital

budgeting techniques makes it easy for the company to measure the changes and make a

better decision:

Payback period:

Payback period explains about the total time in which the total amount which has

been invested by the company could be got back. Following is the calculations of the payback

period of printer A and Printer B.

Calculation of Payback period (Printer A)

Year Cash Outflow Cash Inflow C.F

0 $ -5,40,400 $ -5,40,400

1 $ 1,25,590 $ -4,14,810

2 $ 1,39,590 $ -2,75,220

3 $ 1,60,590 $ -1,14,630

4 $ 1,81,590 $ 66,960

5 $ 2,09,590 $ 2,76,550

Payback Period 2.37

(Burns & Walker, 2015)

The study of payback period of printer A explains that the amount could be got back

by the company after 2.37 years. Further, it has also been found that after 2.37 years, the

company would be able to make profits.

Calculation of Payback period (Printer B)

Year Cash Outflow Cash Inflow C.F

0 $ -2,40,000 $ -2,40,000

1 $ 85,620 $ -1,54,380

2 $ 85,620 $ -68,760

3 $ 85,620 $ 16,860

4 $ 85,620 $ 1,02,480

5 $ 85,620 $ 1,88,100

Payback Period 1.20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.