Impact of Income and Household Size on Credit Card Spending Analysis

VerifiedAdded on 2019/12/28

|23

|3601

|428

Report

AI Summary

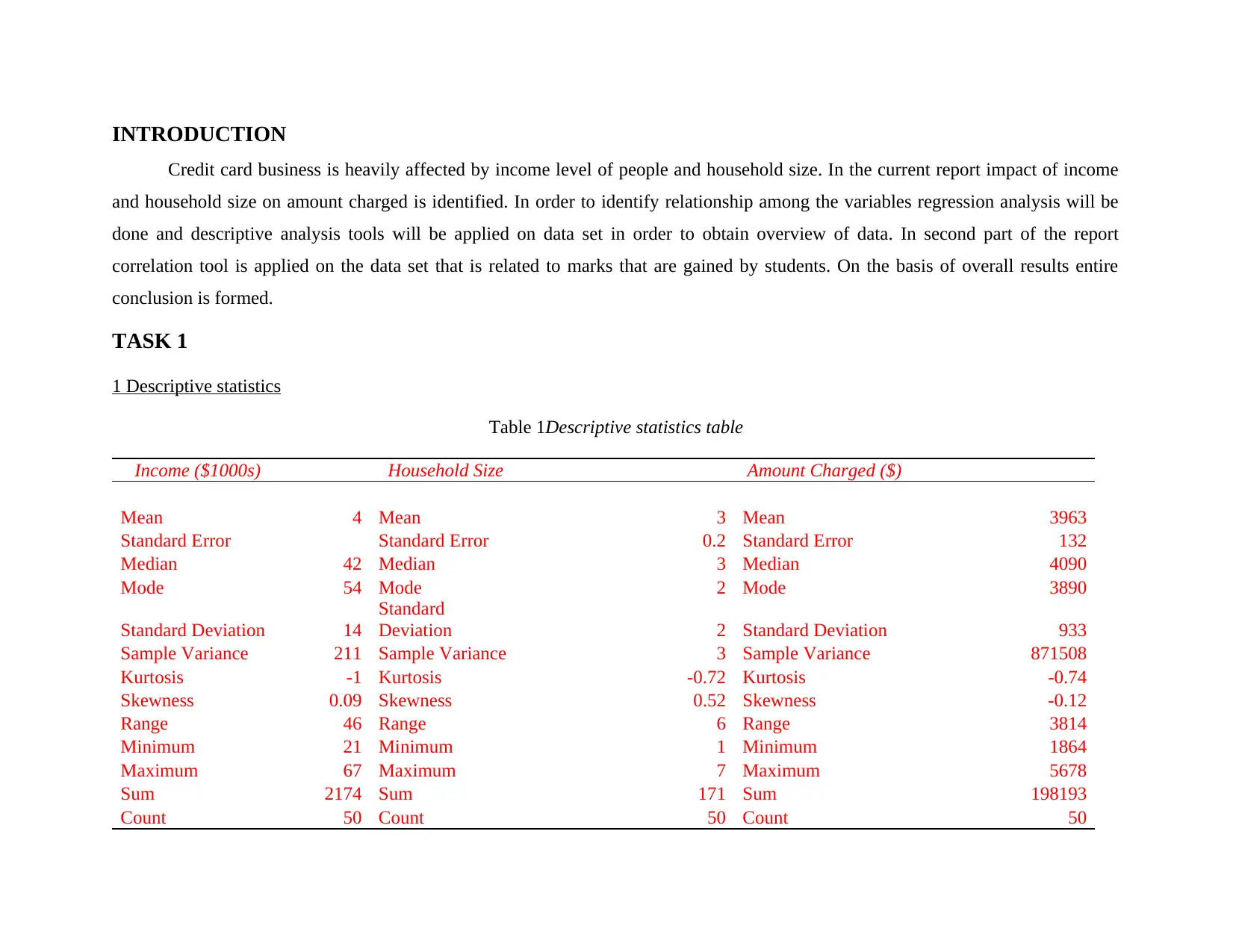

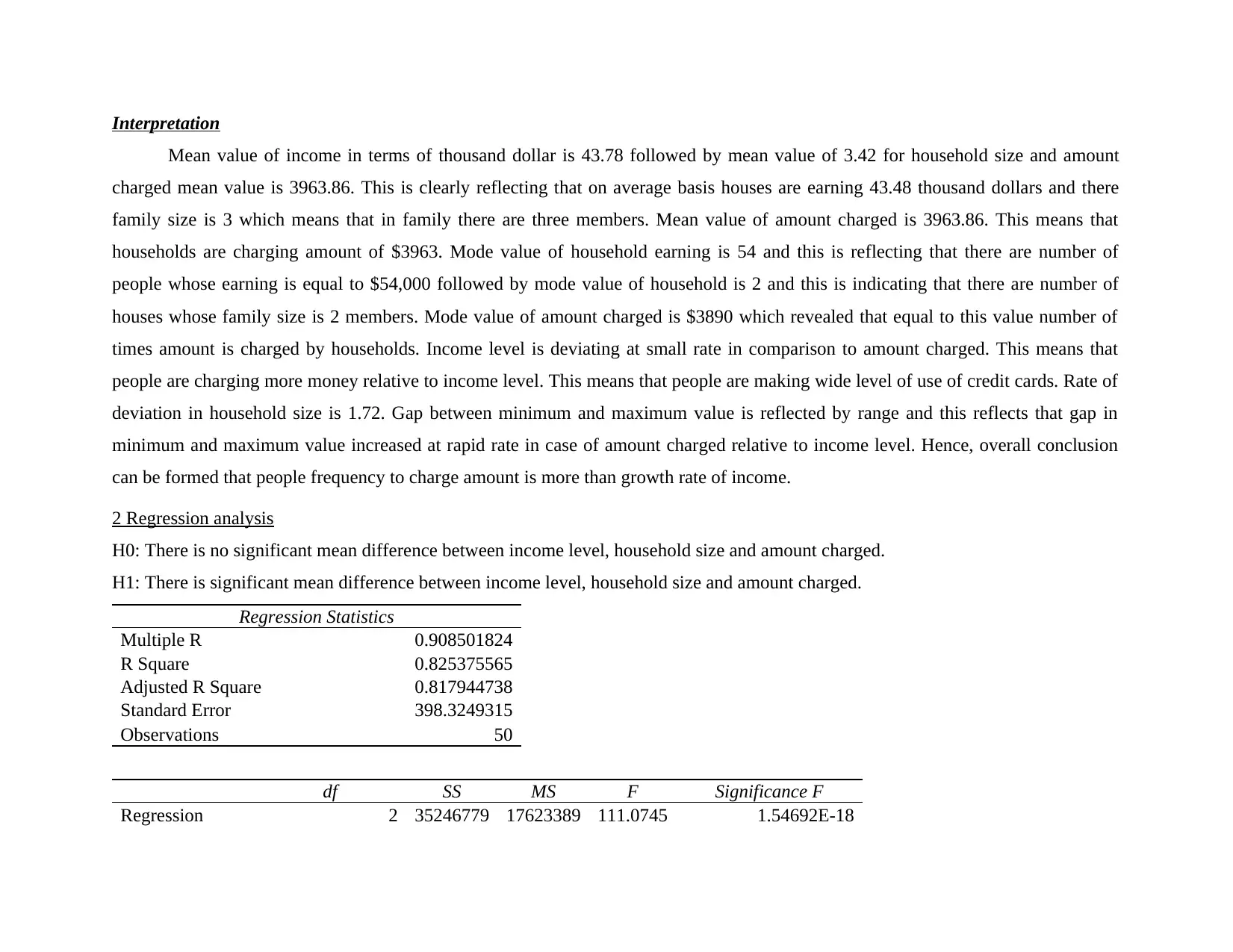

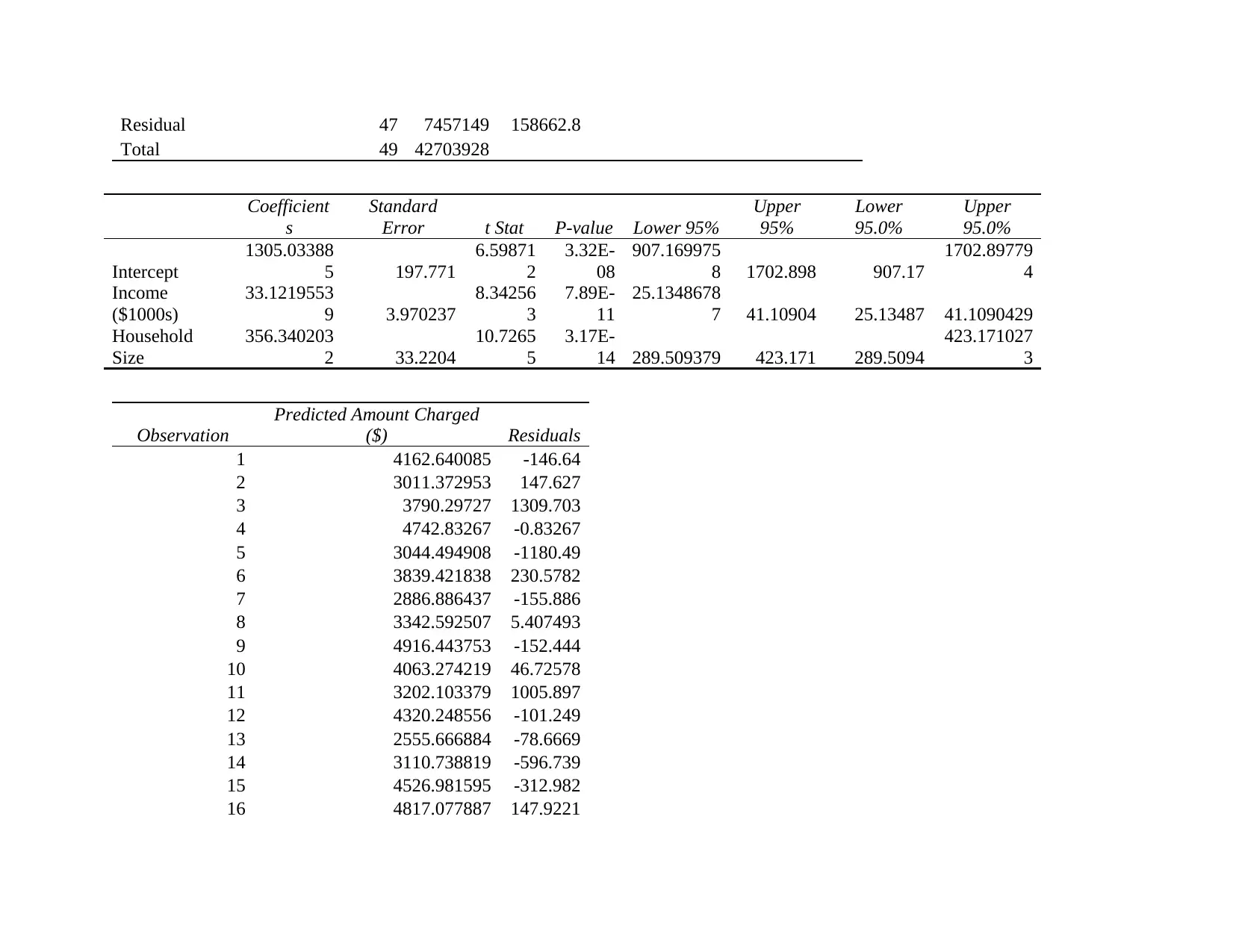

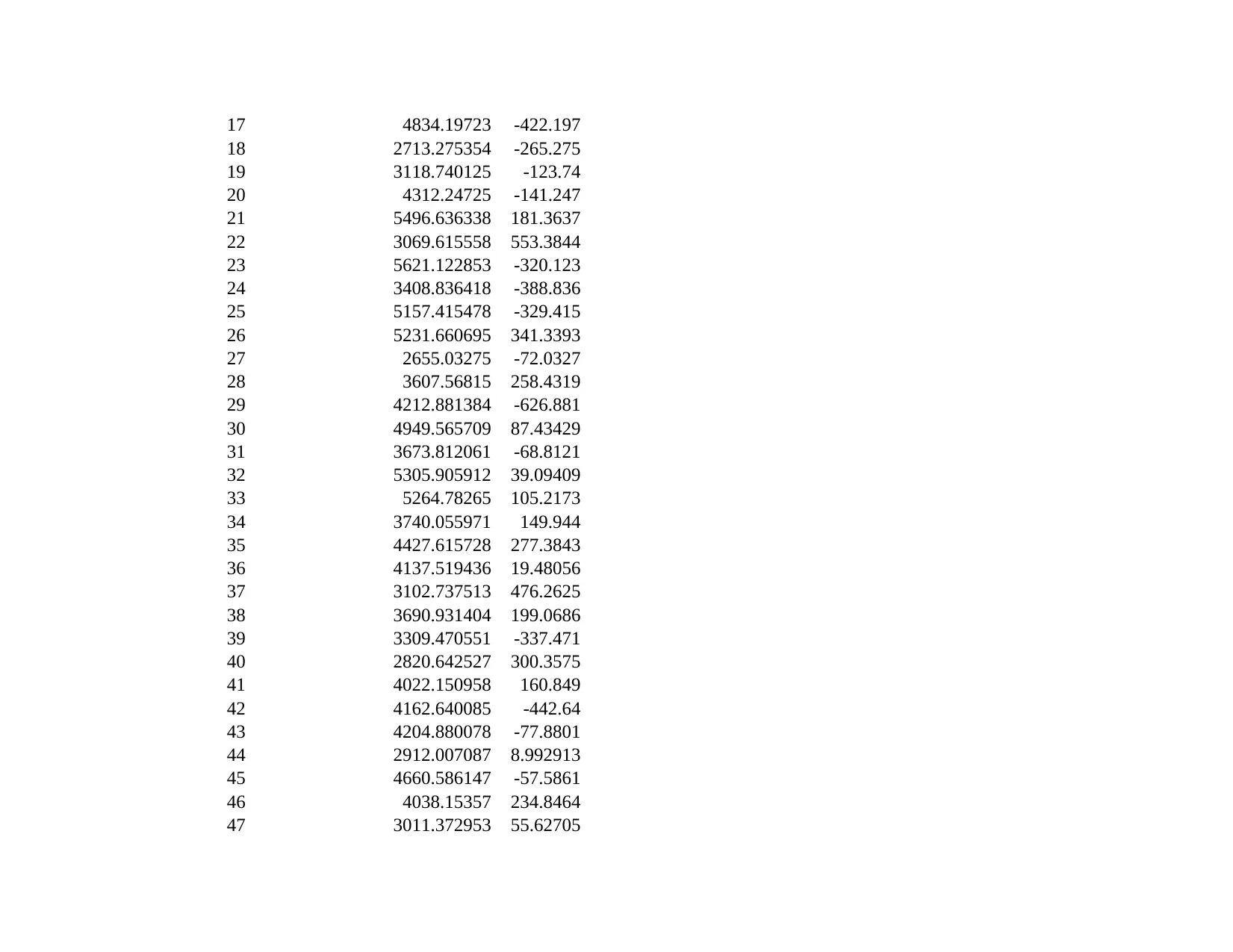

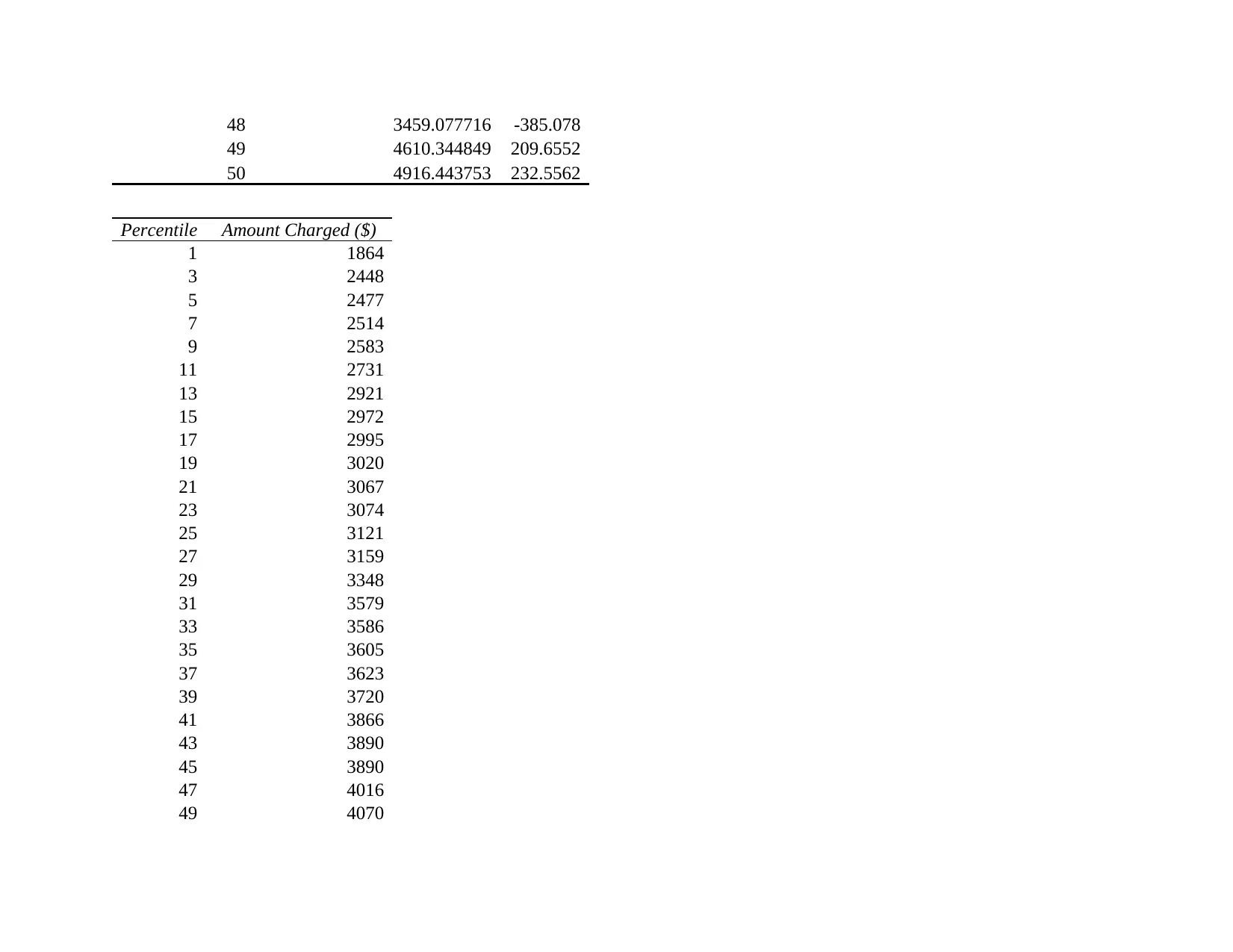

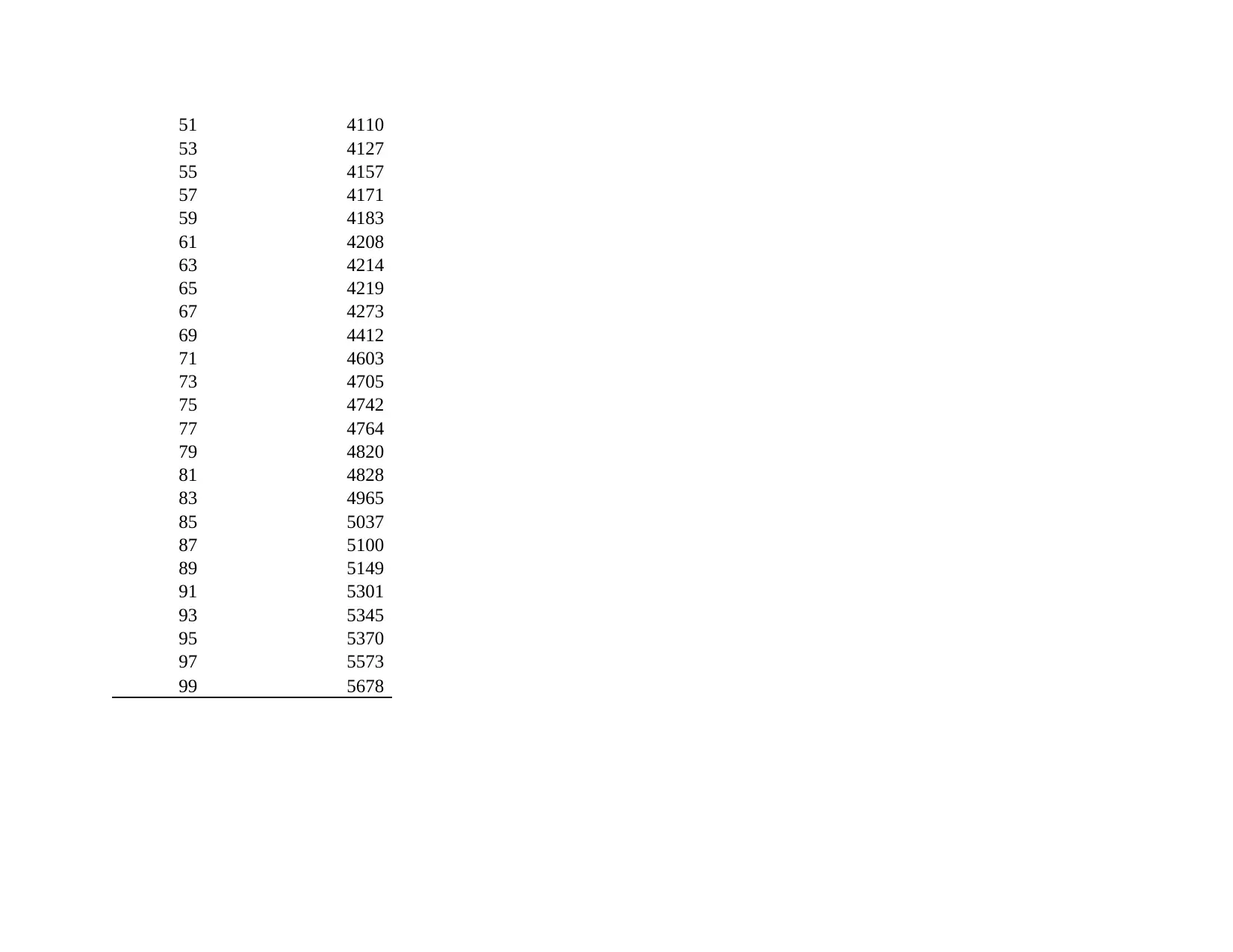

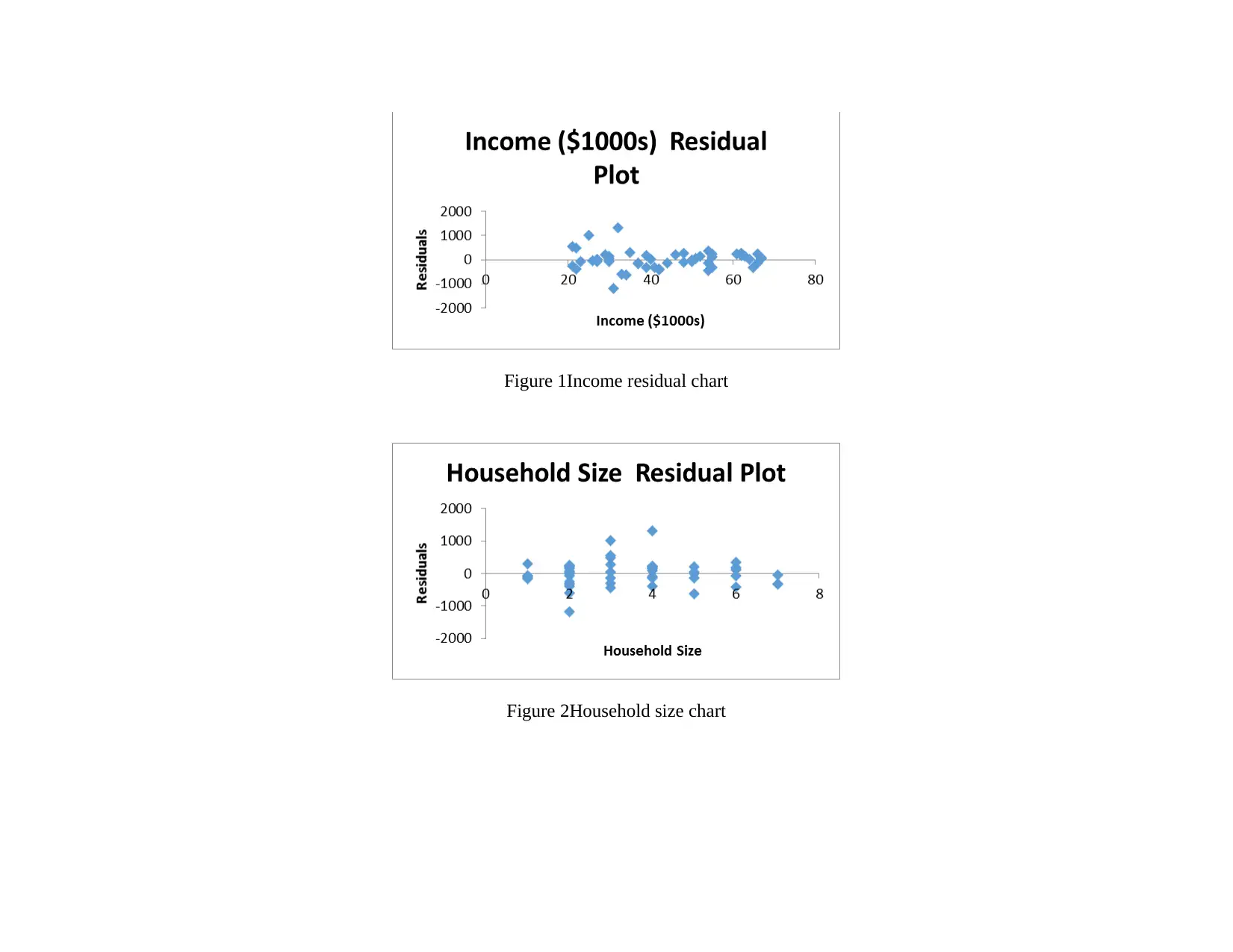

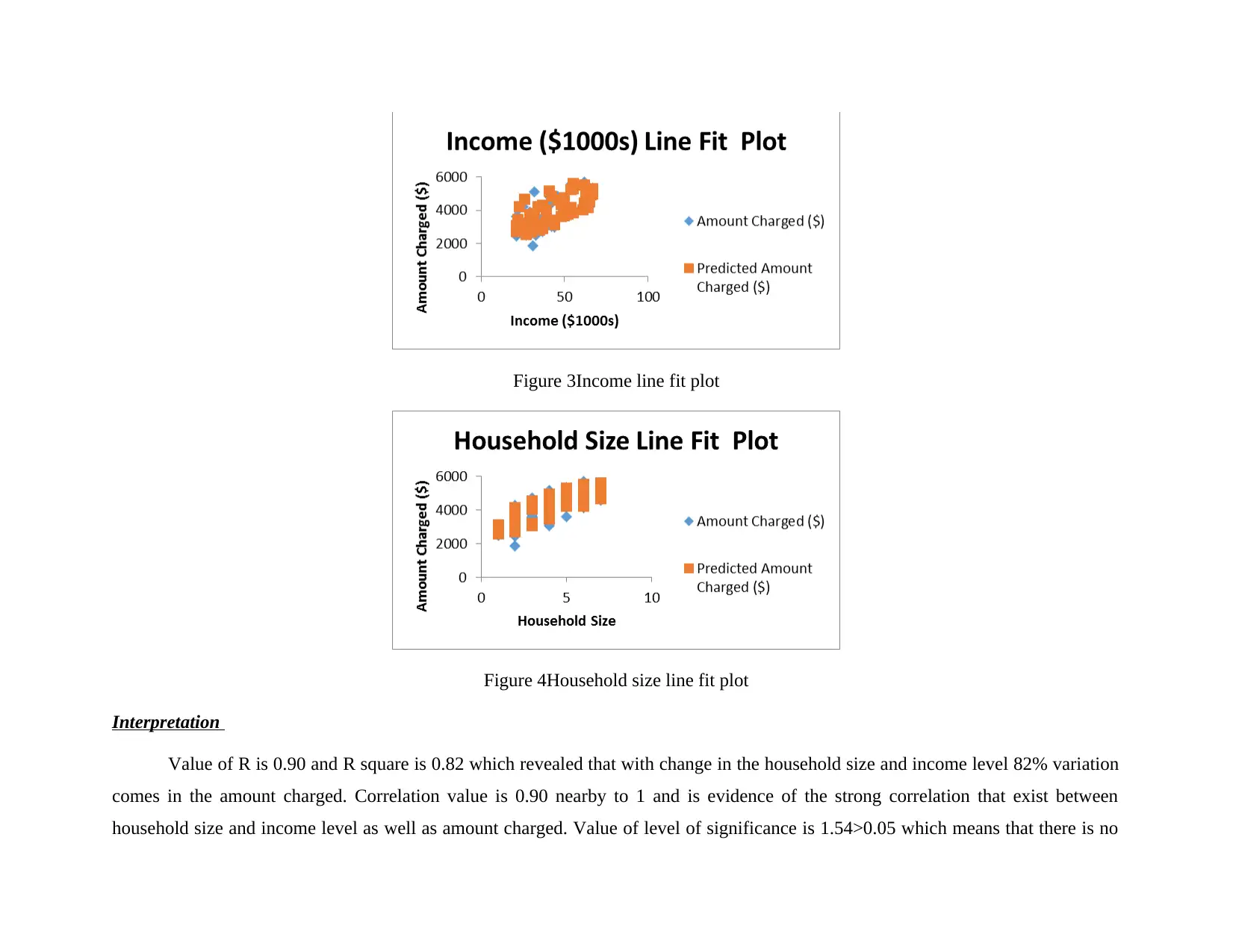

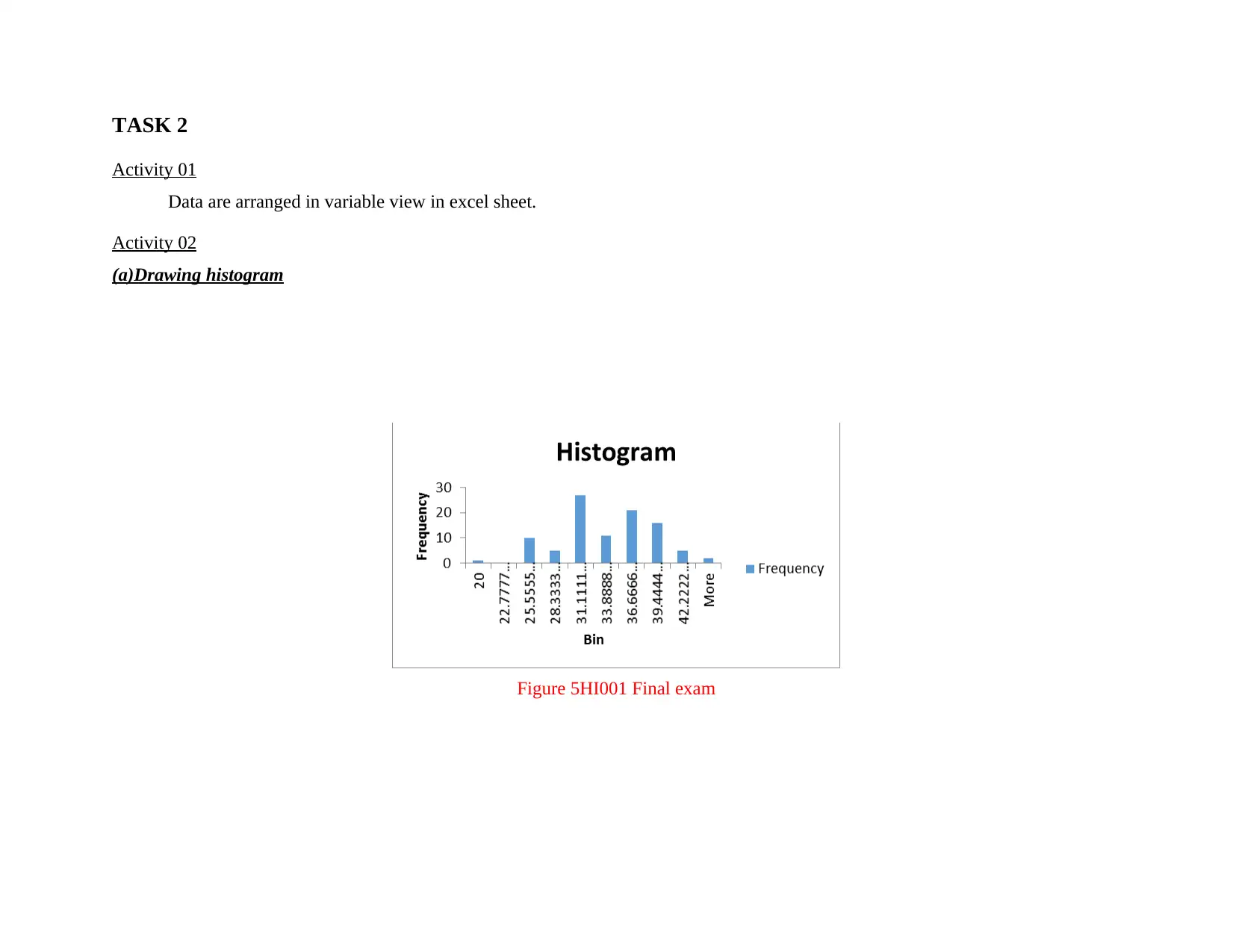

This report investigates the relationship between income, household size, and credit card spending using descriptive statistics and regression analysis. The analysis reveals a strong correlation between household size, income levels, and the amount charged on credit cards. The descriptive statistics provide an overview of the data, while the regression analysis identifies the impact of income and household size on spending. The study predicts average spending for a household size of three with an annual income of $40,000. The report also includes an analysis of student marks, applying correlation tools to assess relationships between different assessment components. The findings suggest that changes in household size have a more significant impact on credit card charges than income levels. The report concludes with an overall assessment of the variables, and suggests further analysis by introducing additional independent variables.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.