Comprehensive Statistical Analysis Report: Credit Card Data

VerifiedAdded on 2020/01/28

|28

|1931

|243

Report

AI Summary

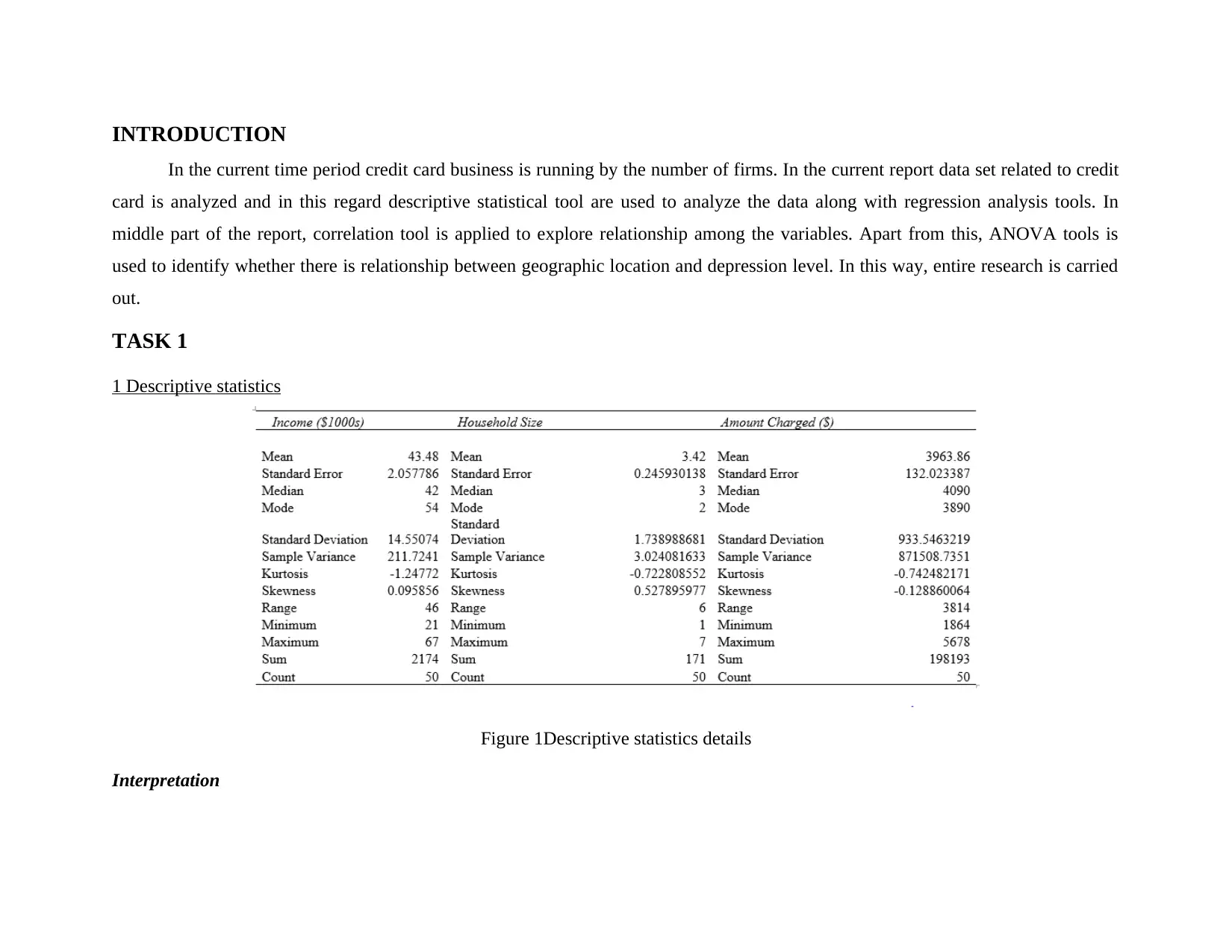

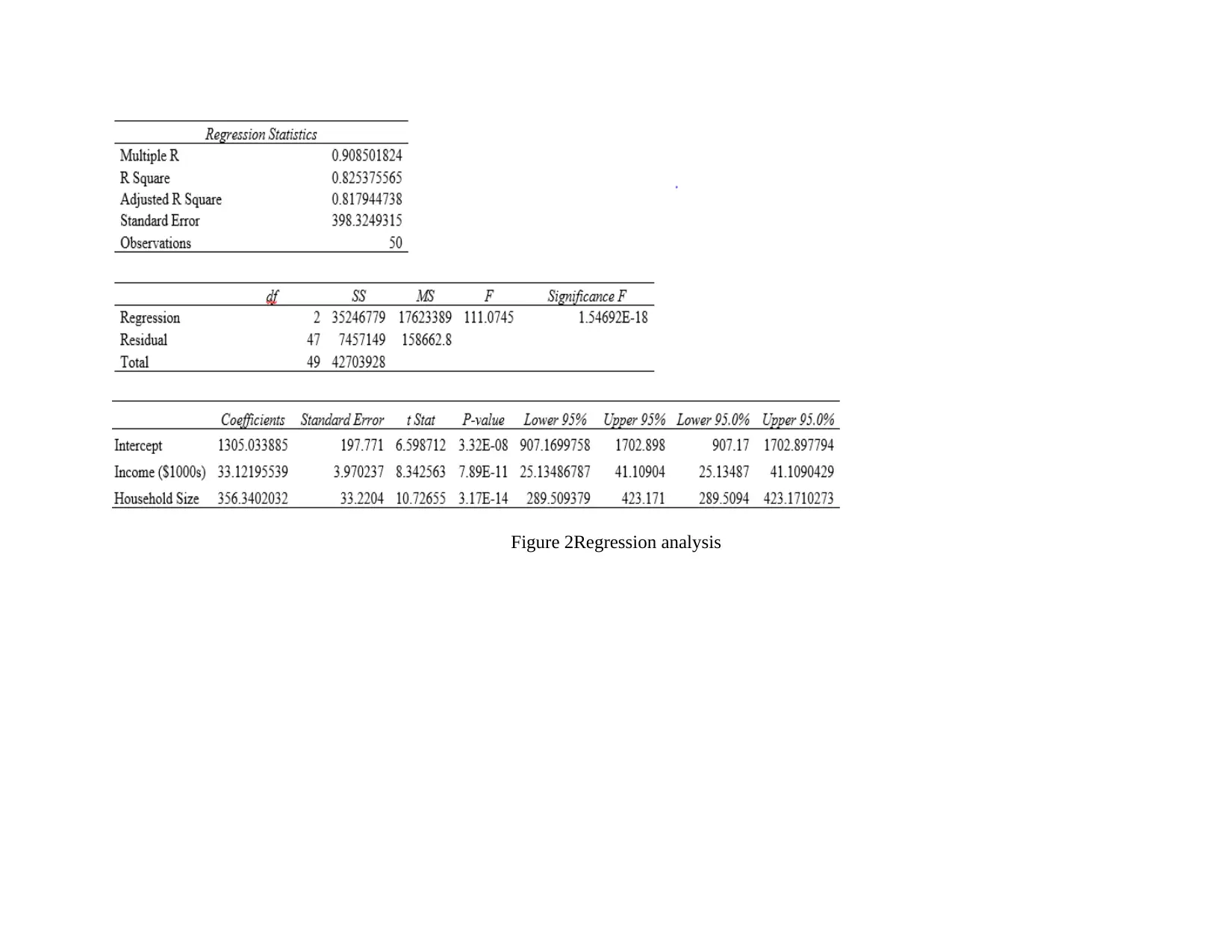

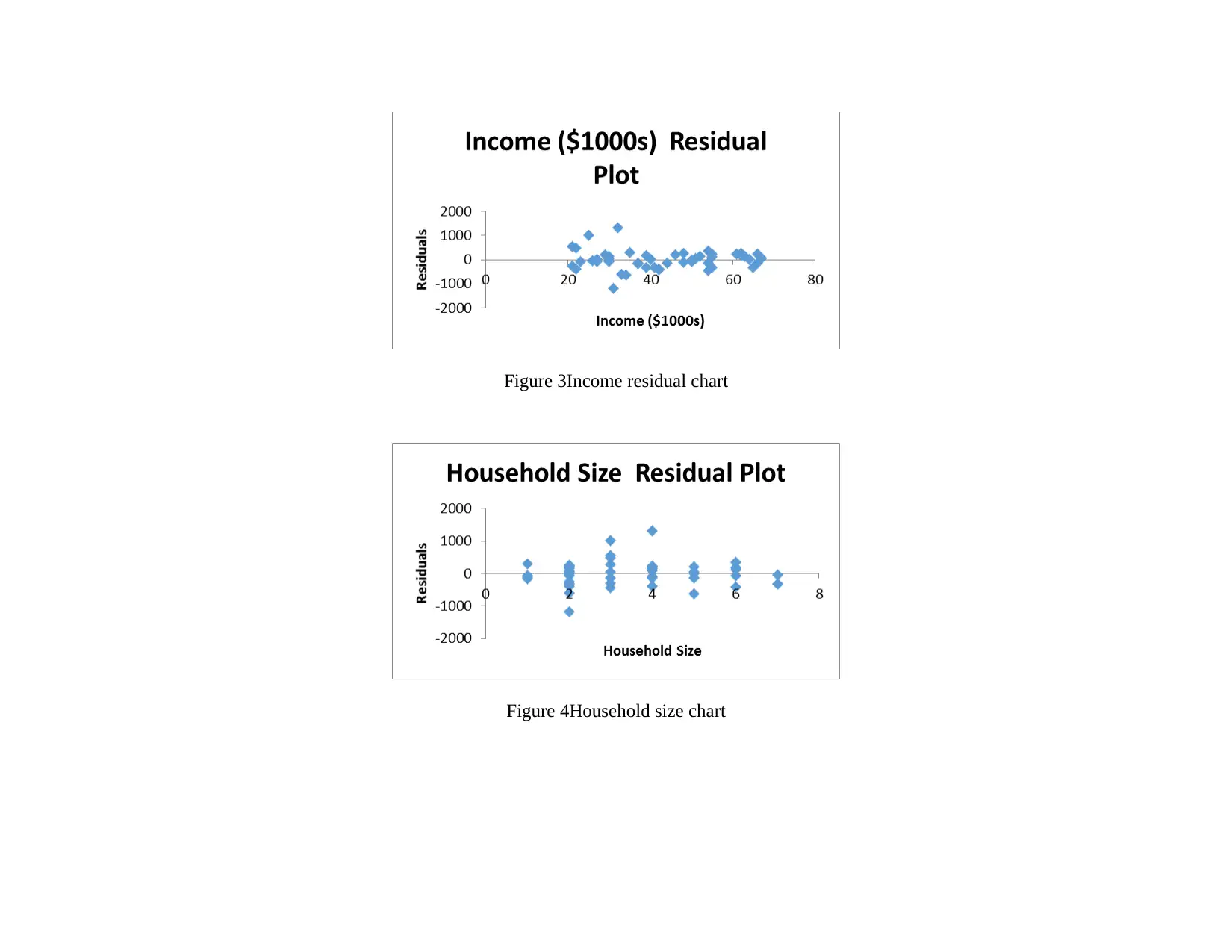

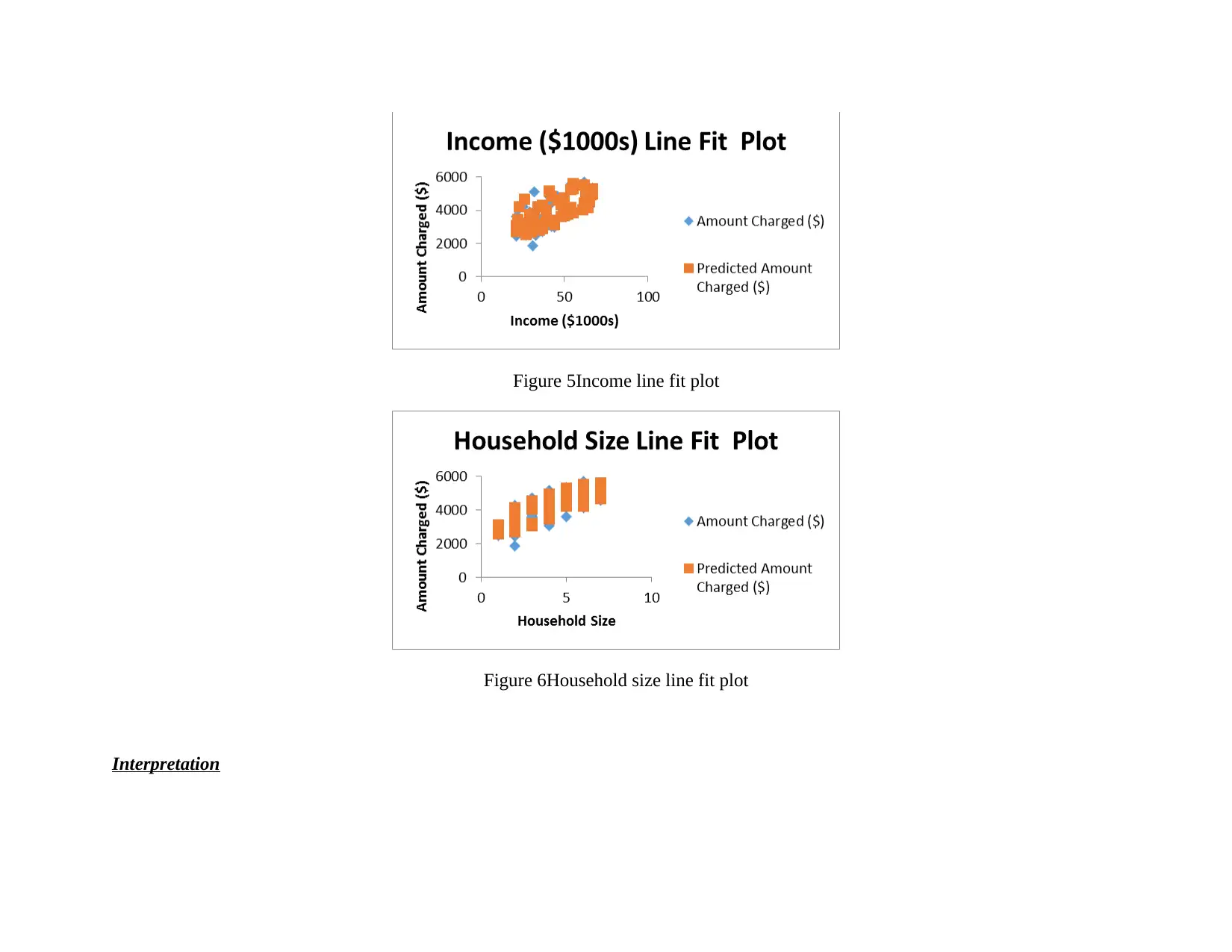

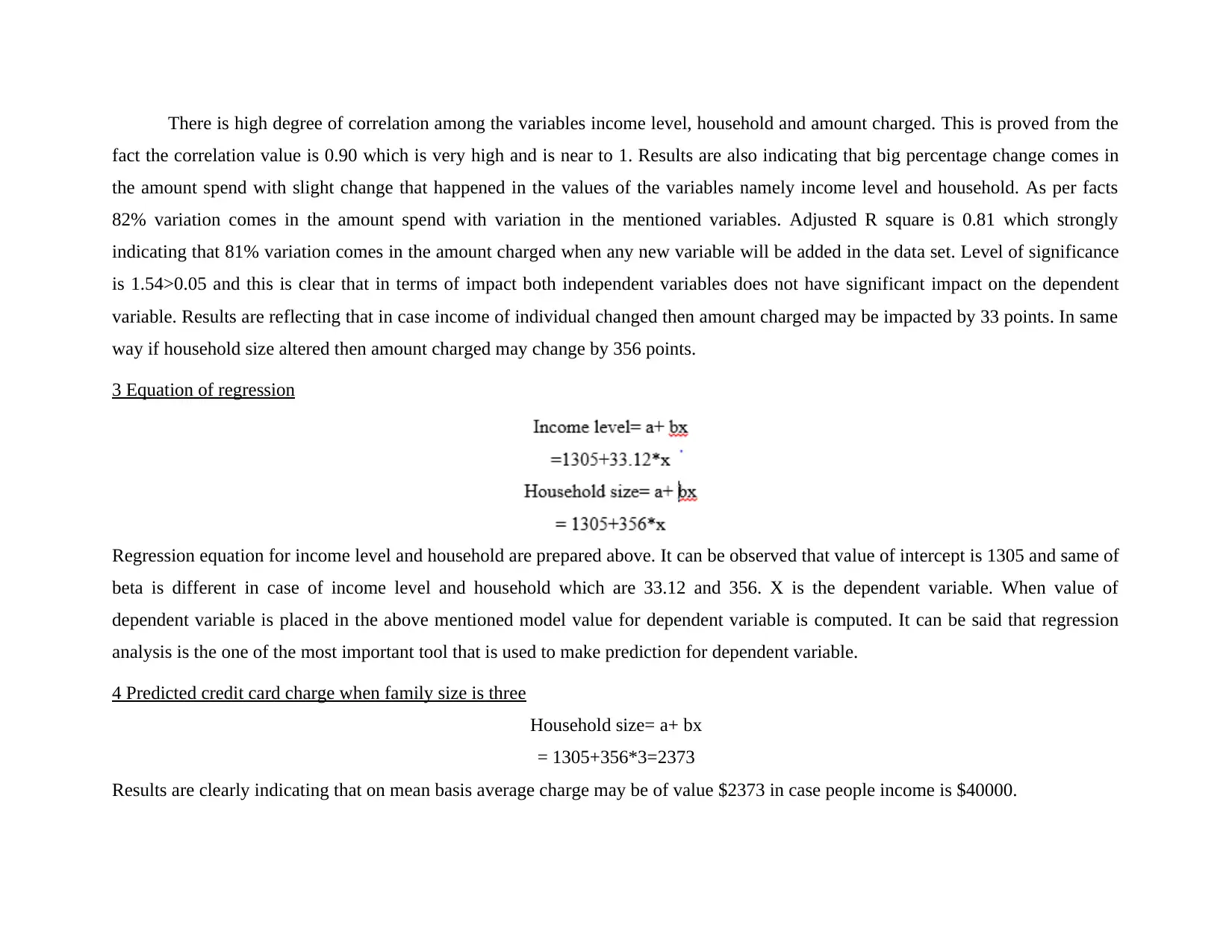

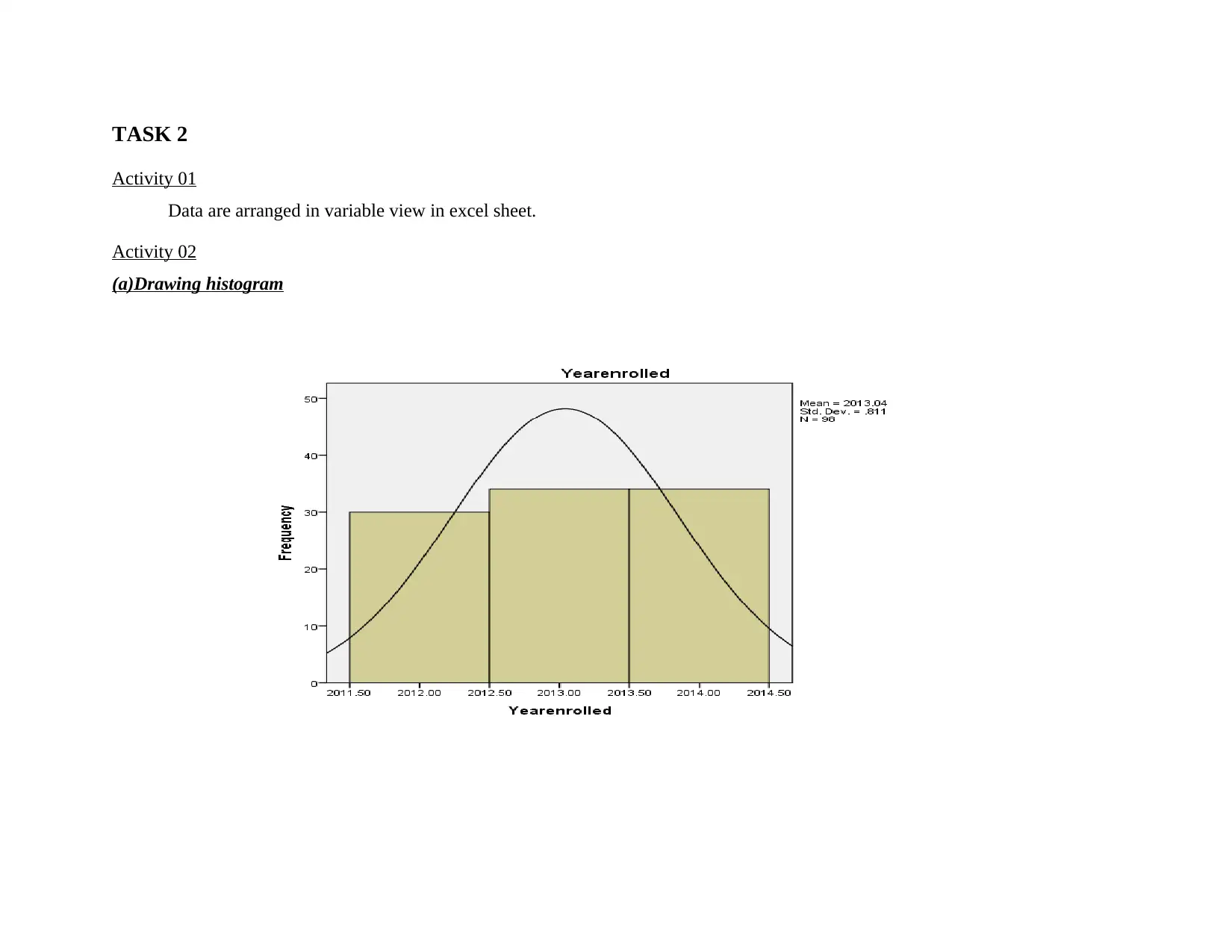

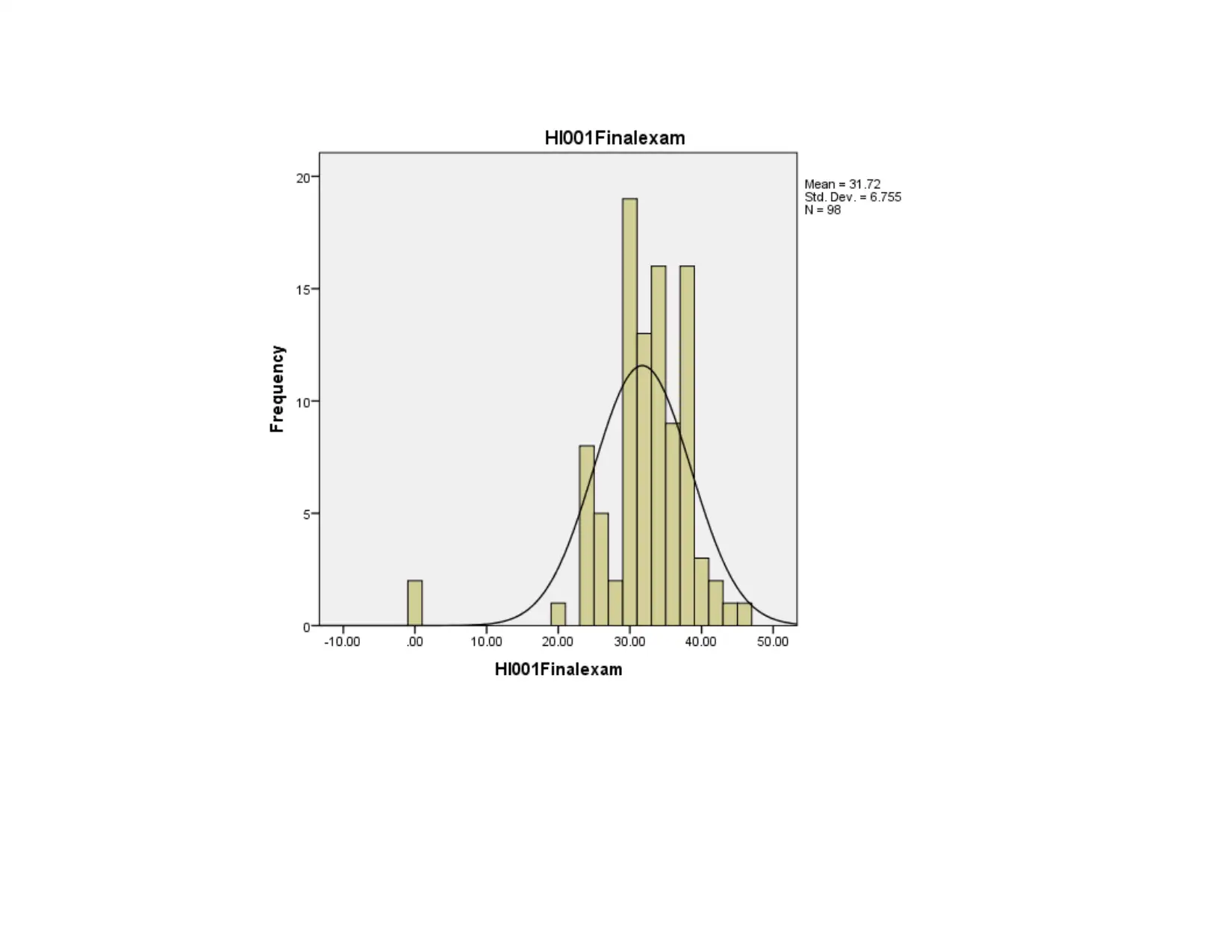

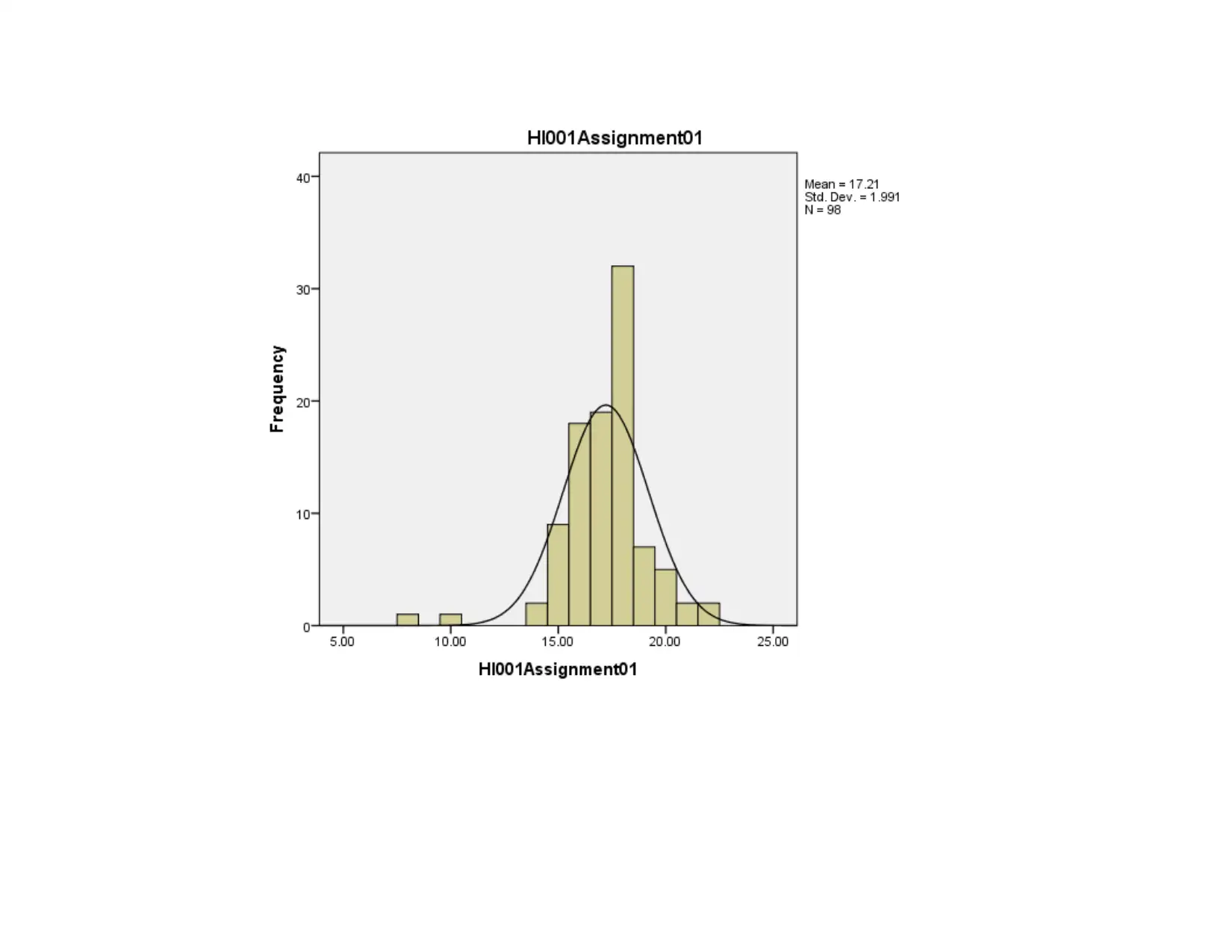

This report presents a statistical analysis of credit card data, employing descriptive statistics and regression analysis to explore relationships between variables such as income, household size, and credit card charges. The analysis includes regression equations, predicted credit card charges, and model modifications. Task 2 focuses on exam and assignment scores, utilizing histograms, descriptive statistics, and correlation analysis to identify relationships between different assessments. Task 3 delves into depression levels across different cities, employing descriptive statistics and ANOVA to assess the impact of health status on depression. The report concludes with key findings and implications derived from the statistical analyses.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.