Data Science Project: Predicting Credit Card Default Rates - PR1

VerifiedAdded on 2021/08/16

|8

|2100

|64

Project

AI Summary

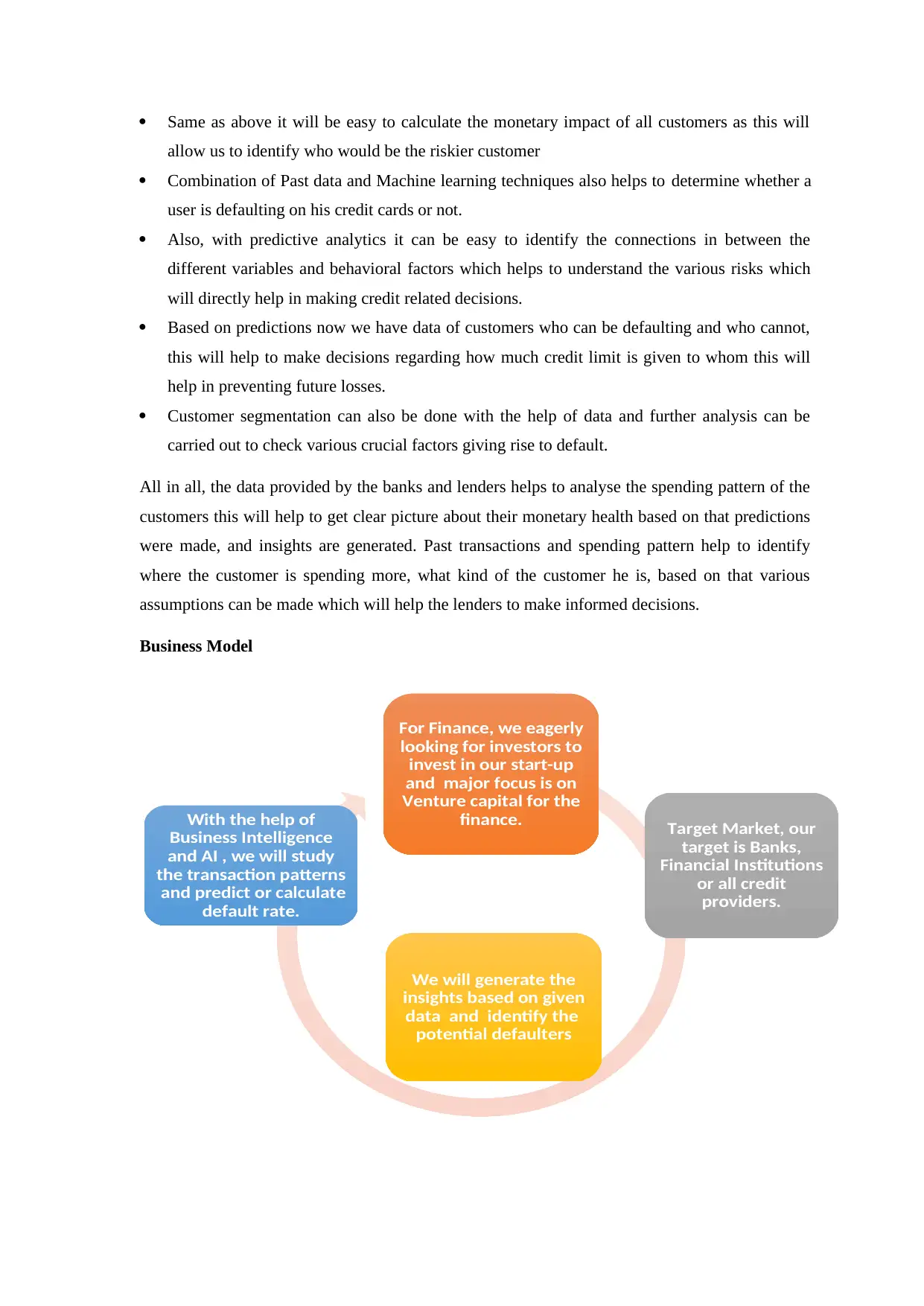

This project, submitted by Ruhi Miglani, focuses on predicting credit card defaults using data science and financial technology. The project identifies the increasing issue of credit card defaults, exacerbated by factors like the COVID-19 pandemic, and proposes a startup, 'Default Prevention Pro Services,' to assist financial institutions. The methodology involves collecting and analyzing customer data, employing business intelligence, predictive analytics, R language, and SAS Enterprise Miner to generate insights and reports. The proposed business model includes revenue generation through service contracts and aims to offer valuable predictions to prevent financial losses for lenders. The project also emphasizes data ethics and governance, ensuring compliance with relevant laws and ethical standards to protect data and promote transparency. The budget outlines costs for IT infrastructure, office setup, and staffing, highlighting the financial aspects of the venture.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.