BI Norwegian Business School: Credit Check Report - SFU 2999

VerifiedAdded on 2022/12/30

|12

|2917

|64

Report

AI Summary

This report provides a detailed analysis of a credit check assignment, addressing key aspects of financial assessment and risk management. It begins by examining the interpretation of the Norwegian Accounting Act's requirement for a true and fair view in financial statements and its relevance to credit evaluation. The report then delves into the assessment of a company's liquidity, outlining crucial ratios and techniques. Furthermore, it explores business and operational risks, using a case study of a sports shop chain to illustrate these concepts, including loan assessment and collateral considerations. Finally, the report analyzes the information needed for loan acceptance, evaluating the borrower's credit history, repayment capacity, and the overall economic situation to determine the viability of a loan offer.

Running head: CREDIT CHECK

CREDIT CHECK

Name of the student:

Name of the university:

Author Note:

CREDIT CHECK

Name of the student:

Name of the university:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CREDIT CHECK

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................3

Answer to Task 1...................................................................................................................3

Answer to Task 2...................................................................................................................4

Answer to Task 3...................................................................................................................5

Answer to Task 4...................................................................................................................7

Conclusion................................................................................................................................10

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................3

Answer to Task 1...................................................................................................................3

Answer to Task 2...................................................................................................................4

Answer to Task 3...................................................................................................................5

Answer to Task 4...................................................................................................................7

Conclusion................................................................................................................................10

2CREDIT CHECK

Introduction:

The aim of the assignment deals with the various types of risks which are associated

with the business of the company and the key fundamentals which are the policies and the

produces. The credit check is significant for the bank and company in order to make sure that

the company is free from the material misstatement and the company poses enough liquid

cash to meet its due obligations. Further analysis of the company’s credit payable capacity is

conducted in the study in order to ensure that the company has enough working capital to

meet the long term loans of the business.

Introduction:

The aim of the assignment deals with the various types of risks which are associated

with the business of the company and the key fundamentals which are the policies and the

produces. The credit check is significant for the bank and company in order to make sure that

the company is free from the material misstatement and the company poses enough liquid

cash to meet its due obligations. Further analysis of the company’s credit payable capacity is

conducted in the study in order to ensure that the company has enough working capital to

meet the long term loans of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CREDIT CHECK

Discussion:

Answer to Task 1

Norwegian entities with securities which are listed on a regulated market needs to

prepare the consolidated financial statements which is further based on the rules related to the

IFRS. The financial statement does not necessarily needs to be based on the aspects or rather

the principles of the IFRS. The regulation on financial services and insurance also falls under

the norms of the IFRS which may further be based on the Norwegian GAAP which is also a

simplified version of the IFRS which also involves the requirement’s and also involves

certain exemptions from the evaluation of the transactions which rather related to the

intragroup. The financial statement of the companies are prepared as per the rules or the

standard mentioned in the IFRS. The accounting standard followed by the Norwegian

accountant is the generally accepted accounting principles or the Norwegian GAAP. It is

significant to follow the rules associated with the accounting information’s and the necessary

measures are needed to be undertaken as per the principles attached to it.

The accounting information’s of the company must show true and fair view of the

business according to the financial statements which are provided to the company. This is

significant to show the true and fair view which further means that the financial statements of

the company is free from the material misstatement. The guidelines and the principles

attached to the Norwegian GAAP must be adhered to the true and the fair view of the

business in that case. The growth of the company depends upon the true and fair view of the

business in that case and the stakeholders of the company will further invest in the business

of the company which such current or future facts and figures.

Discussion:

Answer to Task 1

Norwegian entities with securities which are listed on a regulated market needs to

prepare the consolidated financial statements which is further based on the rules related to the

IFRS. The financial statement does not necessarily needs to be based on the aspects or rather

the principles of the IFRS. The regulation on financial services and insurance also falls under

the norms of the IFRS which may further be based on the Norwegian GAAP which is also a

simplified version of the IFRS which also involves the requirement’s and also involves

certain exemptions from the evaluation of the transactions which rather related to the

intragroup. The financial statement of the companies are prepared as per the rules or the

standard mentioned in the IFRS. The accounting standard followed by the Norwegian

accountant is the generally accepted accounting principles or the Norwegian GAAP. It is

significant to follow the rules associated with the accounting information’s and the necessary

measures are needed to be undertaken as per the principles attached to it.

The accounting information’s of the company must show true and fair view of the

business according to the financial statements which are provided to the company. This is

significant to show the true and fair view which further means that the financial statements of

the company is free from the material misstatement. The guidelines and the principles

attached to the Norwegian GAAP must be adhered to the true and the fair view of the

business in that case. The growth of the company depends upon the true and fair view of the

business in that case and the stakeholders of the company will further invest in the business

of the company which such current or future facts and figures.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CREDIT CHECK

Credit assessment is a type of assessment which an investor or bond portfolio

manager performs some of the significant policies on companies or other debt issuing

organization. It is order to evaluate the ability or rather the potential of an investor to meet the

obligation related to debts. The credit assessment requires some of the significant accounting

information’s in order to understand the default risks which are associated with the

investment in a particular organization. The significance of the rule is to understand and

implement the accounting policies which must represent the true and fair view of the

financial statement which is required for providing the credit assessment. The approval for

the term loan is only possible when the financial statement of the company is free from the

material misstatement.

Answer to Task 2

There are significant accounting tools and techniques which are required in order to

evaluate the liquidity position of the business. The evaluation of the company’s most liquid

asset is conducted and duly analyzed in order to understand the financial position of the

business. The evaluation of the short term liabilities and the long term liabilities of the

business in that case. The liquidity of the business must be ascertained by the organization in

order to understand the current flow of cash in the business. Some of the significant common

ratios of the firms are duly evaluated and analyzed. Then the upper level management of the

company understand the difference or the variance in the financial position and takes

necessary rules or measures in order to enhance the position of the current business policies

by making changes to the norms of the company. Evaluating the ratios would rather help to

understand the financial health of the business along with the necessary measures which are

needed to be undertaken according to the estimates if needed. Effective utilization of the

liquid asset must be undertaken in order to generate huge return out of the utilized assets

(Smales 2016).

Credit assessment is a type of assessment which an investor or bond portfolio

manager performs some of the significant policies on companies or other debt issuing

organization. It is order to evaluate the ability or rather the potential of an investor to meet the

obligation related to debts. The credit assessment requires some of the significant accounting

information’s in order to understand the default risks which are associated with the

investment in a particular organization. The significance of the rule is to understand and

implement the accounting policies which must represent the true and fair view of the

financial statement which is required for providing the credit assessment. The approval for

the term loan is only possible when the financial statement of the company is free from the

material misstatement.

Answer to Task 2

There are significant accounting tools and techniques which are required in order to

evaluate the liquidity position of the business. The evaluation of the company’s most liquid

asset is conducted and duly analyzed in order to understand the financial position of the

business. The evaluation of the short term liabilities and the long term liabilities of the

business in that case. The liquidity of the business must be ascertained by the organization in

order to understand the current flow of cash in the business. Some of the significant common

ratios of the firms are duly evaluated and analyzed. Then the upper level management of the

company understand the difference or the variance in the financial position and takes

necessary rules or measures in order to enhance the position of the current business policies

by making changes to the norms of the company. Evaluating the ratios would rather help to

understand the financial health of the business along with the necessary measures which are

needed to be undertaken according to the estimates if needed. Effective utilization of the

liquid asset must be undertaken in order to generate huge return out of the utilized assets

(Smales 2016).

5CREDIT CHECK

The things which must be considered as per the necessary conditions is that it's

important to keep in mind the asset's liquidity levels as it would take certain time to convert it

into cash. Further the cash can be obtained by selling the assets of the company in that case

by borrowing against an asset. It is significant for the company to pay the amount of loan

along with the interest to the bank which is only possible when the working capital of the

company is effective. Analyzing the ratio as per the financial statement of the company is

duly conducted as the risk of the company can be ascertained along with the liquidity position

of the company (Härle, Havas and Samandari 2016).

Answer to Task 3

Ascertaining the business risks and the operational risk is mainly conducted by the

business analyst and the risk associated with the business strategies must be evaluated and

duly analyzed. The operational risks of an organization is the process of the internal decision

making and the practices associated. Business risks involves the risk associated with the

products and the strategic decisions associated with company. Operational risks associated by

implementing the internal controls which further manages the internal risks which are

associated with the perspective of the company. It is important to understand the major risks

which are associated with the business of the company and hence some of the major

decisions in that case are needed to be taken. Business risks are those risks which rather help

to manage the risks according to some parameters or degree (Bruno and Shin 2015).

The loans associated with the two family-owned holding companies have necessary

collateral the inventories and hence the risks associated with the business is less. The possible

risks which are associated with the bank is that the chance of NPA which is low here which

means that the chance of default on loan will be less as there are enough collateral associated

with the business of the company (Li and Zhang 2019). The potential risks which are

associated with the long term loan is significantly high as the amount on the default on loan is

The things which must be considered as per the necessary conditions is that it's

important to keep in mind the asset's liquidity levels as it would take certain time to convert it

into cash. Further the cash can be obtained by selling the assets of the company in that case

by borrowing against an asset. It is significant for the company to pay the amount of loan

along with the interest to the bank which is only possible when the working capital of the

company is effective. Analyzing the ratio as per the financial statement of the company is

duly conducted as the risk of the company can be ascertained along with the liquidity position

of the company (Härle, Havas and Samandari 2016).

Answer to Task 3

Ascertaining the business risks and the operational risk is mainly conducted by the

business analyst and the risk associated with the business strategies must be evaluated and

duly analyzed. The operational risks of an organization is the process of the internal decision

making and the practices associated. Business risks involves the risk associated with the

products and the strategic decisions associated with company. Operational risks associated by

implementing the internal controls which further manages the internal risks which are

associated with the perspective of the company. It is important to understand the major risks

which are associated with the business of the company and hence some of the major

decisions in that case are needed to be taken. Business risks are those risks which rather help

to manage the risks according to some parameters or degree (Bruno and Shin 2015).

The loans associated with the two family-owned holding companies have necessary

collateral the inventories and hence the risks associated with the business is less. The possible

risks which are associated with the bank is that the chance of NPA which is low here which

means that the chance of default on loan will be less as there are enough collateral associated

with the business of the company (Li and Zhang 2019). The potential risks which are

associated with the long term loan is significantly high as the amount on the default on loan is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CREDIT CHECK

similarly high in that case. The limit of the overdraft facility provided by the bank will be up

to NOK 5 and hence such facility will be exercised within the limit of both the companies.

The profit margin and the return of the company is 2% and 6% respectively which means that

the profitability position of the companies must be enhanced in order to accompany the

necessary changes for further enhancing the profitability position of the company in that case.

The operating revenue of the company were NOK 160 million which further means that the

company have enough reserves as profit. The company has the necessary potential to

eliminate the risk associated as the profit margin of the company is pretty good. The amount

of loan opted by the company from the bank is pretty low compared to the amount of profit

the company is making. As the business of the company has the necessary collateral attached

to the loans which further eliminates the risk associated with the bank. The net incomes of the

bank is higher after considering the tax and the company will easily able to meet the

obligations of the business in that case. The reputation of the business will further enhance

the growth of the financial aspects of the firm.

In order to minimize the business risk of the firm, there are certain parameters which

are needed to be considered in that case. The conditions which are it is needed to develop an

effective plan, perform quality control test from various aspects of the firm. Then it is needed

to keep standard or good records of the firm which matters regarding the application of loan.

It is essential to diversify the loan amount of the company so that the return which is

generated from the business is enough the payoff the long term loans and obligations. It is

needed to keep in reserve the return which is generated from the utilization of the investment.

The invested value of the firm must be effective so that the company is able to generate the

profit or return in order to make the business of the company much more effective.

In order to eliminate the operational risks of the business, it is further needed to

understand the internal controls of the business which means that the effectiveness or rather

similarly high in that case. The limit of the overdraft facility provided by the bank will be up

to NOK 5 and hence such facility will be exercised within the limit of both the companies.

The profit margin and the return of the company is 2% and 6% respectively which means that

the profitability position of the companies must be enhanced in order to accompany the

necessary changes for further enhancing the profitability position of the company in that case.

The operating revenue of the company were NOK 160 million which further means that the

company have enough reserves as profit. The company has the necessary potential to

eliminate the risk associated as the profit margin of the company is pretty good. The amount

of loan opted by the company from the bank is pretty low compared to the amount of profit

the company is making. As the business of the company has the necessary collateral attached

to the loans which further eliminates the risk associated with the bank. The net incomes of the

bank is higher after considering the tax and the company will easily able to meet the

obligations of the business in that case. The reputation of the business will further enhance

the growth of the financial aspects of the firm.

In order to minimize the business risk of the firm, there are certain parameters which

are needed to be considered in that case. The conditions which are it is needed to develop an

effective plan, perform quality control test from various aspects of the firm. Then it is needed

to keep standard or good records of the firm which matters regarding the application of loan.

It is essential to diversify the loan amount of the company so that the return which is

generated from the business is enough the payoff the long term loans and obligations. It is

needed to keep in reserve the return which is generated from the utilization of the investment.

The invested value of the firm must be effective so that the company is able to generate the

profit or return in order to make the business of the company much more effective.

In order to eliminate the operational risks of the business, it is further needed to

understand the internal controls of the business which means that the effectiveness or rather

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CREDIT CHECK

efficiency of the working capital of the companies. Effective flow of cash in the companies

will further help to meet the obligations of the business in that case. As per the analysis it can

be said that the company must further strengthen the effectiveness of the internal control

management (Bluhm, Overbeck and Wagner 2016). This will help the management of the

company in order to meet the obligations of the company on the perspective of the long term

loan which is availed by the company from the bank. Due to such reputation of the company,

it is significant for the upper level management of the company to take some of the major

decisions to further enhance the financial position of the business (Bruno and Shin 2015).

The risks will automatically be optimized if some of the significant changes are made like the

operational changes in the system. Further up gradation and optimization in the system of the

companies and providing training to the employees will further enhance the financial position

of the business (Huang, Shi and Zhou 2019).

Answer to Task 4

The significant information’s which are needed to be analyzed and collected in order

to make the acceptance of the loan offer which are the credit history, purpose of the loan

regarding such business, it further needed to identify the potential collateral associated with

such loan, the capacity to repay the loan, the need for the capital and finally analyzing the

overall economic situation or rather the present scenario of the company. The business plan

regarding the shopping center must be analyzed and the overall project cost of the business

200 million. The current strategy which is adopted by the company is that 70% on loan and

30% on equity which means that the company is adopting the debt financing strategy. The

building loan taken by the bank is about NOK 140 million and hence necessary collateral are

needed to be identified so that the chance of the loan default may be taken into account in that

case. In order to get more offer it is significant in order to analyze the potential of the

company regarding the past and the current financial position of the business (Alshatti 2015).

efficiency of the working capital of the companies. Effective flow of cash in the companies

will further help to meet the obligations of the business in that case. As per the analysis it can

be said that the company must further strengthen the effectiveness of the internal control

management (Bluhm, Overbeck and Wagner 2016). This will help the management of the

company in order to meet the obligations of the company on the perspective of the long term

loan which is availed by the company from the bank. Due to such reputation of the company,

it is significant for the upper level management of the company to take some of the major

decisions to further enhance the financial position of the business (Bruno and Shin 2015).

The risks will automatically be optimized if some of the significant changes are made like the

operational changes in the system. Further up gradation and optimization in the system of the

companies and providing training to the employees will further enhance the financial position

of the business (Huang, Shi and Zhou 2019).

Answer to Task 4

The significant information’s which are needed to be analyzed and collected in order

to make the acceptance of the loan offer which are the credit history, purpose of the loan

regarding such business, it further needed to identify the potential collateral associated with

such loan, the capacity to repay the loan, the need for the capital and finally analyzing the

overall economic situation or rather the present scenario of the company. The business plan

regarding the shopping center must be analyzed and the overall project cost of the business

200 million. The current strategy which is adopted by the company is that 70% on loan and

30% on equity which means that the company is adopting the debt financing strategy. The

building loan taken by the bank is about NOK 140 million and hence necessary collateral are

needed to be identified so that the chance of the loan default may be taken into account in that

case. In order to get more offer it is significant in order to analyze the potential of the

company regarding the past and the current financial position of the business (Alshatti 2015).

8CREDIT CHECK

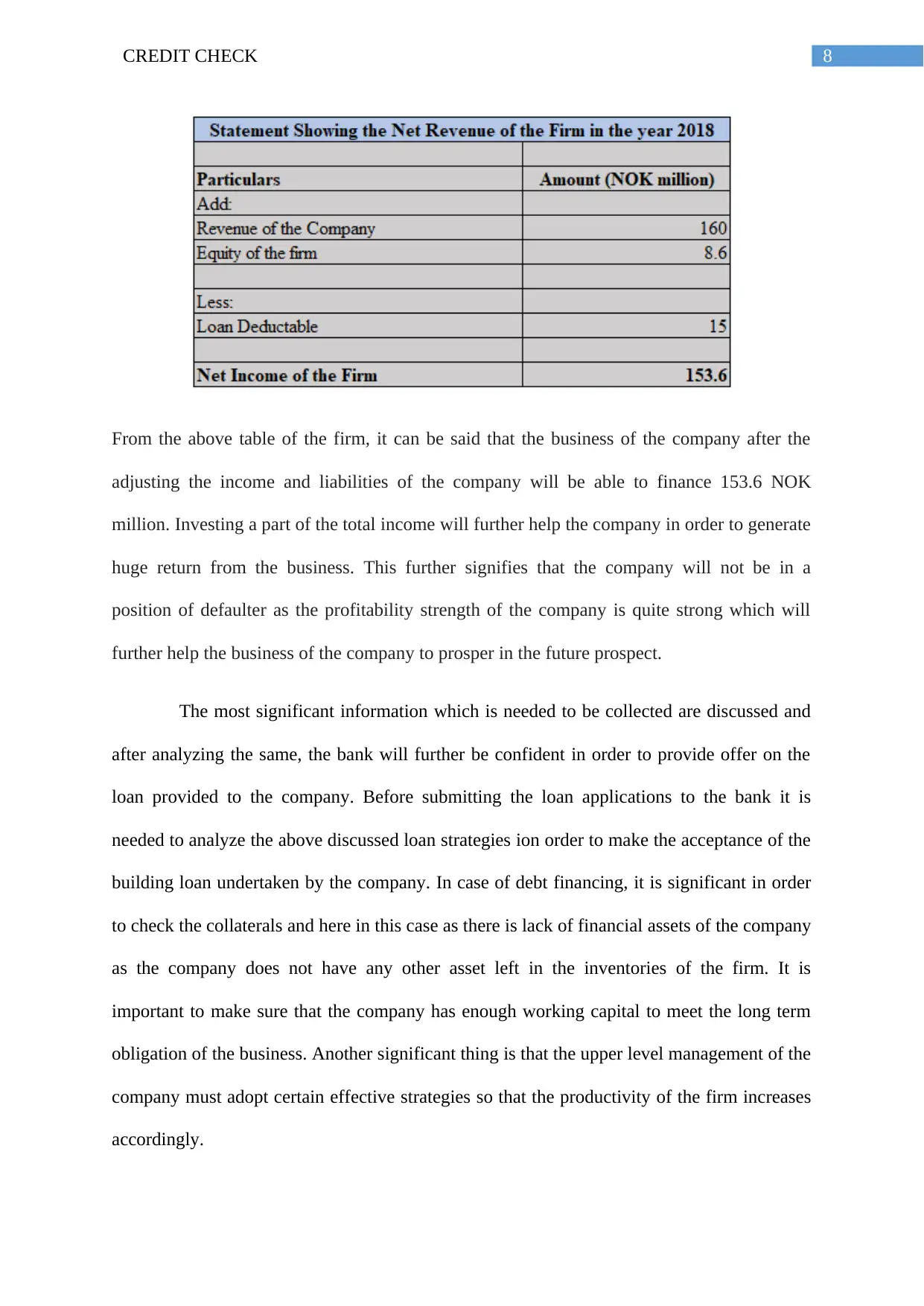

From the above table of the firm, it can be said that the business of the company after the

adjusting the income and liabilities of the company will be able to finance 153.6 NOK

million. Investing a part of the total income will further help the company in order to generate

huge return from the business. This further signifies that the company will not be in a

position of defaulter as the profitability strength of the company is quite strong which will

further help the business of the company to prosper in the future prospect.

The most significant information which is needed to be collected are discussed and

after analyzing the same, the bank will further be confident in order to provide offer on the

loan provided to the company. Before submitting the loan applications to the bank it is

needed to analyze the above discussed loan strategies ion order to make the acceptance of the

building loan undertaken by the company. In case of debt financing, it is significant in order

to check the collaterals and here in this case as there is lack of financial assets of the company

as the company does not have any other asset left in the inventories of the firm. It is

important to make sure that the company has enough working capital to meet the long term

obligation of the business. Another significant thing is that the upper level management of the

company must adopt certain effective strategies so that the productivity of the firm increases

accordingly.

From the above table of the firm, it can be said that the business of the company after the

adjusting the income and liabilities of the company will be able to finance 153.6 NOK

million. Investing a part of the total income will further help the company in order to generate

huge return from the business. This further signifies that the company will not be in a

position of defaulter as the profitability strength of the company is quite strong which will

further help the business of the company to prosper in the future prospect.

The most significant information which is needed to be collected are discussed and

after analyzing the same, the bank will further be confident in order to provide offer on the

loan provided to the company. Before submitting the loan applications to the bank it is

needed to analyze the above discussed loan strategies ion order to make the acceptance of the

building loan undertaken by the company. In case of debt financing, it is significant in order

to check the collaterals and here in this case as there is lack of financial assets of the company

as the company does not have any other asset left in the inventories of the firm. It is

important to make sure that the company has enough working capital to meet the long term

obligation of the business. Another significant thing is that the upper level management of the

company must adopt certain effective strategies so that the productivity of the firm increases

accordingly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CREDIT CHECK

The capacity to repay the loan must be analyzed in a detailed manner and there are

insufficient collateral as the company is running out of the fixed assets of the firm and hence

certain effective measures are needed to consider as per the other operational aspects of the

firm. The operations must be analyzed in such a way that the loopholes of the business must

be kept into account. If the company satisfies the above discussed the parameters then it will

definitely help the bank to provide certain offers to the company (Laeven, Ratnovski and

Tong 2016).

The offers of the bank will definitely help the company in order to repay the loan

faster. Enough working capital of the firm will further help the firm to meet the debt

obligations. The leverage must be effective which further means that the investment of the

debt capital becomes too much risky and hence the firm needs to adopt some of the

significant strategies to make sure that the effective investment is conducted. The liquidity

and efficiency of the company must be analyzed so that the company have enough capital to

run the business of the company in that case. The leverage risk must be optimized so that the

company must be able to meet the daily obligation otherwise such kind of leverage can result

in the debt trap of the company. In case of debt trap the company will face difficulty such as

dissolution of the company in that case. Hence, in this case the analysis of the financial ratios

in that case is certainly significant in order to make sure the current business position of the

company is effective and efficient.

The capacity to repay the loan must be analyzed in a detailed manner and there are

insufficient collateral as the company is running out of the fixed assets of the firm and hence

certain effective measures are needed to consider as per the other operational aspects of the

firm. The operations must be analyzed in such a way that the loopholes of the business must

be kept into account. If the company satisfies the above discussed the parameters then it will

definitely help the bank to provide certain offers to the company (Laeven, Ratnovski and

Tong 2016).

The offers of the bank will definitely help the company in order to repay the loan

faster. Enough working capital of the firm will further help the firm to meet the debt

obligations. The leverage must be effective which further means that the investment of the

debt capital becomes too much risky and hence the firm needs to adopt some of the

significant strategies to make sure that the effective investment is conducted. The liquidity

and efficiency of the company must be analyzed so that the company have enough capital to

run the business of the company in that case. The leverage risk must be optimized so that the

company must be able to meet the daily obligation otherwise such kind of leverage can result

in the debt trap of the company. In case of debt trap the company will face difficulty such as

dissolution of the company in that case. Hence, in this case the analysis of the financial ratios

in that case is certainly significant in order to make sure the current business position of the

company is effective and efficient.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CREDIT CHECK

Conclusion

From the above discussion it can be concluded that as per the above analysis of the

study regarding the risk which are associated with the business. The rules and regulation of

the business of the company is duly analyzed in that case where it is further found the

business of the company has enough collateral. This will further help the company as the

profitability position of the company is good and the company will meet its due obligation

where the chance of default will be less. The financial position of the business is analyzed

duly in the above study and further tools and techniques have been provided in that case.

Conclusion

From the above discussion it can be concluded that as per the above analysis of the

study regarding the risk which are associated with the business. The rules and regulation of

the business of the company is duly analyzed in that case where it is further found the

business of the company has enough collateral. This will further help the company as the

profitability position of the company is good and the company will meet its due obligation

where the chance of default will be less. The financial position of the business is analyzed

duly in the above study and further tools and techniques have been provided in that case.

11CREDIT CHECK

References:

Alshatti, A.S., 2015. The effect of credit risk management on financial performance of the

Jordanian commercial banks. Investment Management and Financial Innovations, 12(1),

pp.338-345.

Bluhm, C., Overbeck, L. and Wagner, C., 2016. Introduction to credit risk modeling.

Chapman and Hall/CRC.

Bruno, V. and Shin, H.S., 2015. Capital flows and the risk-taking channel of monetary policy.

Journal of Monetary Economics, 71, pp.119-132.

Härle, P., Havas, A. and Samandari, H., 2016. The future of bank risk management.

McKinsey on Risk, (1).

Huang, J.Z., Shi, Z. and Zhou, H., 2019. Specification analysis of structural credit risk

models. Available at SSRN 968020.

Laeven, L., Ratnovski, L. and Tong, H., 2016. Bank size, capital, and systemic risk: Some

international evidence. Journal of Banking & Finance, 69, pp.S25-S34.

Li, G. and Zhang, C., 2019. Counterparty credit risk and derivatives pricing. Journal of

Financial Economics.

Smales, L.A., 2016. News sentiment and bank credit risk. Journal of Empirical Finance, 38,

pp.37-61.

References:

Alshatti, A.S., 2015. The effect of credit risk management on financial performance of the

Jordanian commercial banks. Investment Management and Financial Innovations, 12(1),

pp.338-345.

Bluhm, C., Overbeck, L. and Wagner, C., 2016. Introduction to credit risk modeling.

Chapman and Hall/CRC.

Bruno, V. and Shin, H.S., 2015. Capital flows and the risk-taking channel of monetary policy.

Journal of Monetary Economics, 71, pp.119-132.

Härle, P., Havas, A. and Samandari, H., 2016. The future of bank risk management.

McKinsey on Risk, (1).

Huang, J.Z., Shi, Z. and Zhou, H., 2019. Specification analysis of structural credit risk

models. Available at SSRN 968020.

Laeven, L., Ratnovski, L. and Tong, H., 2016. Bank size, capital, and systemic risk: Some

international evidence. Journal of Banking & Finance, 69, pp.S25-S34.

Li, G. and Zhang, C., 2019. Counterparty credit risk and derivatives pricing. Journal of

Financial Economics.

Smales, L.A., 2016. News sentiment and bank credit risk. Journal of Empirical Finance, 38,

pp.37-61.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.