A Report on the Challenges of Internal Risk Rating Systems in Banking

VerifiedAdded on 2022/08/24

|13

|2768

|29

Report

AI Summary

This report provides an analysis of the challenges faced by internal risk rating systems within banks, focusing on credit and lending practices. It examines the credit risk management process, highlighting issues related to the Basel Committee of Banking Supervision regulations and the difficulties banks encounter in adapting to evolving credit-risk profiles. The report identifies challenges such as data requirements, regulatory compliance, and the need for robust risk assessment methodologies. It recommends that banks prioritize long-term strategic planning, improve data acquisition and maintenance, and enhance their techniques for managing credit risk. The report suggests that banks should use tools such as FICO scores and debt-to-income ratios to assess customer creditworthiness. The analysis covers the components of credit risk, the risk rating system, and the importance of internal risk-rating systems in controlling credit risks. The report concludes that banks should focus on enhancing their techniques and adapting to the changing credit risk environment to effectively manage and mitigate risks.

Running Head: CREDIT AND LENDING

CREDIT AND LENDING

Name of the Student

Name of the University

Author Note

CREDIT AND LENDING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CREDIT AND LENDING

Executive Summary

The primary purpose of this report is to analyse the various issues faced by the

internal risk rating systems of a bank. The study is supported by studying the credit risk

management process through an internal rating system. It is found that the developed bank

faces various challenges in implementing the various difficulties in following the regulations

of Basel Committee of Banking Supervision. The banks should focus on improving the

techniques more meeting with the various changes related to credit- risk profiles. Bank can

also use FICO score, and debt-to-income ratio to estimate credit extend of the customers.

CREDIT AND LENDING

Executive Summary

The primary purpose of this report is to analyse the various issues faced by the

internal risk rating systems of a bank. The study is supported by studying the credit risk

management process through an internal rating system. It is found that the developed bank

faces various challenges in implementing the various difficulties in following the regulations

of Basel Committee of Banking Supervision. The banks should focus on improving the

techniques more meeting with the various changes related to credit- risk profiles. Bank can

also use FICO score, and debt-to-income ratio to estimate credit extend of the customers.

2

CREDIT AND LENDING

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................3

Conclusion..................................................................................................................................9

References................................................................................................................................10

CREDIT AND LENDING

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................3

Conclusion..................................................................................................................................9

References................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CREDIT AND LENDING

Introduction

Internal Risk Rating System is a system that helps the financial institutions and other

banks, to control the risks that have incurred during the lending process. It also helps to

manage the creditworthiness of the borrower. The first part has discussed on the Credit Risk-

rating management process and the Risk-rating system. The next part has addressed the

various issues related to internal rating systems of the bank, and the last section has provided

specific recommendations to banks on how to execute the risk rating system. The intense of

this paper is to analyze the various issues, that bank has faces in implementing the internal

risk rating systems.

Discussions

Credit Risk Management

Credit Risk management is the process of quantifying the various risks associated

with the bank's capital reserves. Credit risks is that probability of bank loss due to the failure

in making payments to any type of debts. Credit Risk management process will help the bank

to mitigate against these type of bank losses at the given period (Bulbul, Hakenes and

Lambert 2019). Banks and other financial institutions have to follow specific steps to lend

credibility to the borrower. The following are the steps for credit risks management:

1. Adequately understand the overall credit risks by viewing the credit risks of the

customers or individual or to a company portfolio.

2. Implement an appropriate method of quantitative credit solution in the risk assessment

process.

3. A proper model should be implemented for monitoring and controlling the entire

management process.

CREDIT AND LENDING

Introduction

Internal Risk Rating System is a system that helps the financial institutions and other

banks, to control the risks that have incurred during the lending process. It also helps to

manage the creditworthiness of the borrower. The first part has discussed on the Credit Risk-

rating management process and the Risk-rating system. The next part has addressed the

various issues related to internal rating systems of the bank, and the last section has provided

specific recommendations to banks on how to execute the risk rating system. The intense of

this paper is to analyze the various issues, that bank has faces in implementing the internal

risk rating systems.

Discussions

Credit Risk Management

Credit Risk management is the process of quantifying the various risks associated

with the bank's capital reserves. Credit risks is that probability of bank loss due to the failure

in making payments to any type of debts. Credit Risk management process will help the bank

to mitigate against these type of bank losses at the given period (Bulbul, Hakenes and

Lambert 2019). Banks and other financial institutions have to follow specific steps to lend

credibility to the borrower. The following are the steps for credit risks management:

1. Adequately understand the overall credit risks by viewing the credit risks of the

customers or individual or to a company portfolio.

2. Implement an appropriate method of quantitative credit solution in the risk assessment

process.

3. A proper model should be implemented for monitoring and controlling the entire

management process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CREDIT AND LENDING

4. Use of various business intelligence tools to collect essential data for the risk

management process.

The credit risks of a borrower are calculated by identifying their ability to pay the

loan with respect to its original amount. The banks look at the borrower's capacity, capital,

loan conditions and other associated collateral to repay the loans.

Components of Credit Risks Analysis

The various components of credit risks are determined by five C’s:

Capacity- The bank assesses the borrower's capability to pay back the loan. The

lender looks into the monthly income of the borrower in the form of salary or any

profit from the business (Belas et al. 2017). It also looks after other sources of

payment like home, gold and many more.

Capital- The bank also investigates if the borrower has any source of capital to invest

in purchasing the assets. In this case, the bank especially looks after a company or

business capital.

Collateral- Collateral is an asset in the form of mortgage, car or property, the

borrower pledges for the repayment of the loan to the banks.

Conditions- Different loans have different conditions for the loan applicants before

the loan has been approved. Both the lender and the borrower must full fill these

conditions.

Risk rating system

There is various credit risk rating system that is used to identify the credit risk rating

related to a loan. This risk rating system helps the banks and other credit unions to assess the

quality of the credit, identify the various problems associated with the loans, examine &

CREDIT AND LENDING

4. Use of various business intelligence tools to collect essential data for the risk

management process.

The credit risks of a borrower are calculated by identifying their ability to pay the

loan with respect to its original amount. The banks look at the borrower's capacity, capital,

loan conditions and other associated collateral to repay the loans.

Components of Credit Risks Analysis

The various components of credit risks are determined by five C’s:

Capacity- The bank assesses the borrower's capability to pay back the loan. The

lender looks into the monthly income of the borrower in the form of salary or any

profit from the business (Belas et al. 2017). It also looks after other sources of

payment like home, gold and many more.

Capital- The bank also investigates if the borrower has any source of capital to invest

in purchasing the assets. In this case, the bank especially looks after a company or

business capital.

Collateral- Collateral is an asset in the form of mortgage, car or property, the

borrower pledges for the repayment of the loan to the banks.

Conditions- Different loans have different conditions for the loan applicants before

the loan has been approved. Both the lender and the borrower must full fill these

conditions.

Risk rating system

There is various credit risk rating system that is used to identify the credit risk rating

related to a loan. This risk rating system helps the banks and other credit unions to assess the

quality of the credit, identify the various problems associated with the loans, examine &

5

CREDIT AND LENDING

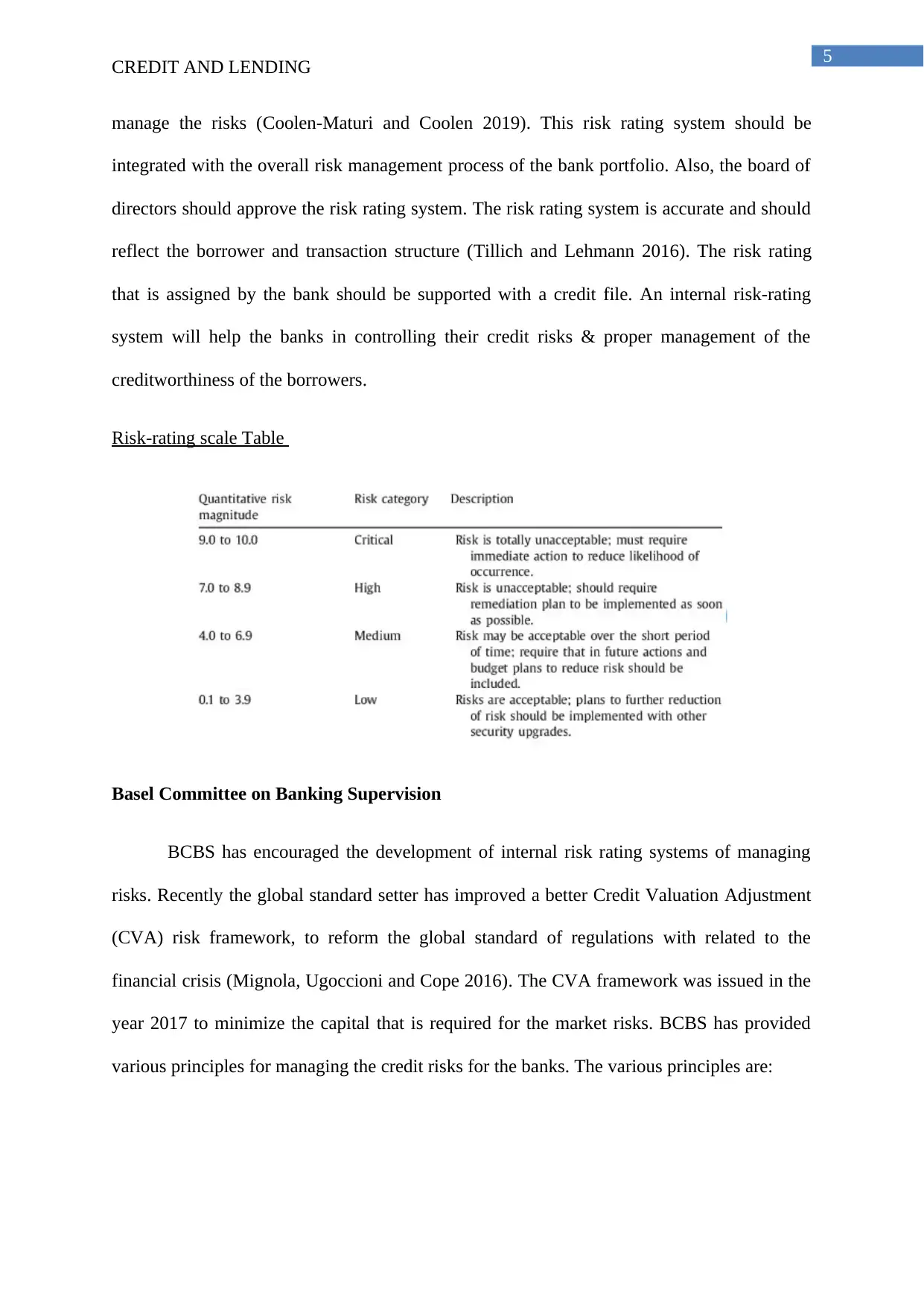

manage the risks (Coolen‐Maturi and Coolen 2019). This risk rating system should be

integrated with the overall risk management process of the bank portfolio. Also, the board of

directors should approve the risk rating system. The risk rating system is accurate and should

reflect the borrower and transaction structure (Tillich and Lehmann 2016). The risk rating

that is assigned by the bank should be supported with a credit file. An internal risk-rating

system will help the banks in controlling their credit risks & proper management of the

creditworthiness of the borrowers.

Risk-rating scale Table

Basel Committee on Banking Supervision

BCBS has encouraged the development of internal risk rating systems of managing

risks. Recently the global standard setter has improved a better Credit Valuation Adjustment

(CVA) risk framework, to reform the global standard of regulations with related to the

financial crisis (Mignola, Ugoccioni and Cope 2016). The CVA framework was issued in the

year 2017 to minimize the capital that is required for the market risks. BCBS has provided

various principles for managing the credit risks for the banks. The various principles are:

CREDIT AND LENDING

manage the risks (Coolen‐Maturi and Coolen 2019). This risk rating system should be

integrated with the overall risk management process of the bank portfolio. Also, the board of

directors should approve the risk rating system. The risk rating system is accurate and should

reflect the borrower and transaction structure (Tillich and Lehmann 2016). The risk rating

that is assigned by the bank should be supported with a credit file. An internal risk-rating

system will help the banks in controlling their credit risks & proper management of the

creditworthiness of the borrowers.

Risk-rating scale Table

Basel Committee on Banking Supervision

BCBS has encouraged the development of internal risk rating systems of managing

risks. Recently the global standard setter has improved a better Credit Valuation Adjustment

(CVA) risk framework, to reform the global standard of regulations with related to the

financial crisis (Mignola, Ugoccioni and Cope 2016). The CVA framework was issued in the

year 2017 to minimize the capital that is required for the market risks. BCBS has provided

various principles for managing the credit risks for the banks. The various principles are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CREDIT AND LENDING

To establish a proper credit risk environment in the business. The board of directors

are responsible for revising the credit risks policies and strategy of the banks. The

management is responsible for implementing the risks according to the policies.

Operating a sound credit process-Banks should have proper criteria for establishing

the credit limits for the borrowers and the other groups. They should have a clear

business process for allowing a new credit in the banks.

Should have a proper monitoring process in the bank for examining the on-going

credit risk-bearing portfolios. A proper internal risk rating system should be

developed to manage credit risks. The monitoring process should have a proper

analytical technique and information system to measure their inherent credit portfolios

and identify the concentration of risk (Alber and Ramadan 2017). Banks should also

consider future economic changes while assessing credit portfolios.

The banks must ensure adequate control over the bank risks. They should implement a

system that can easily communicate the results of credit risk assessment to their board

of directors. Banks should guarantee that the credit exposures are within the internal

limits and standards of the banks. The banks must have a system of managing the

problems related to credits during the process.

The supervisors of the bank should consider the bank policies, strategies, procedures

and practices to properly conduct the credit risk management process.

Banks internal risk-rating systems

The banks are permitted to use their risk parameters for estimating their capital

requirements for credit risks. Bank uses the risk-rating system to rate their customers based

on their creditworthiness. Risk-rating systems provide greater support to the top management

in managing their credit risks. Therefore, establishing an efficient internal risk-rating

framework is very much important for maintaining the losses from loans. This process

CREDIT AND LENDING

To establish a proper credit risk environment in the business. The board of directors

are responsible for revising the credit risks policies and strategy of the banks. The

management is responsible for implementing the risks according to the policies.

Operating a sound credit process-Banks should have proper criteria for establishing

the credit limits for the borrowers and the other groups. They should have a clear

business process for allowing a new credit in the banks.

Should have a proper monitoring process in the bank for examining the on-going

credit risk-bearing portfolios. A proper internal risk rating system should be

developed to manage credit risks. The monitoring process should have a proper

analytical technique and information system to measure their inherent credit portfolios

and identify the concentration of risk (Alber and Ramadan 2017). Banks should also

consider future economic changes while assessing credit portfolios.

The banks must ensure adequate control over the bank risks. They should implement a

system that can easily communicate the results of credit risk assessment to their board

of directors. Banks should guarantee that the credit exposures are within the internal

limits and standards of the banks. The banks must have a system of managing the

problems related to credits during the process.

The supervisors of the bank should consider the bank policies, strategies, procedures

and practices to properly conduct the credit risk management process.

Banks internal risk-rating systems

The banks are permitted to use their risk parameters for estimating their capital

requirements for credit risks. Bank uses the risk-rating system to rate their customers based

on their creditworthiness. Risk-rating systems provide greater support to the top management

in managing their credit risks. Therefore, establishing an efficient internal risk-rating

framework is very much important for maintaining the losses from loans. This process

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CREDIT AND LENDING

involves the initiation of the loan applications to classification of the transactions into various

credit-risks (Yaacob, Markom and Hakimah 2018). The regulators want the banks to improve

their risk-management practices to ensure safety in the entire banking system. However, the

internal risk-rating systems of developed banks face various issues during the improvement

of their internal risk rating systems. The different issues are:

Challenges due to the Basel Committee on Banking Supervision (BCBS)

The auditors dealing with the internal risk-reporting system have to monitor the entire

process continuously. They face various challenges while dealing with the risk-rating system.

The internal auditors are involved in dealing with the risk-reporting systems of the company,

are involved in a material misstatement in the company’s balance sheet. This can create an

issue in the development of a banks internal risk-rating system (Kumar and Kaur 2019).

1. The bank faces various challenges to compliance their changes with the regulatory

principles of the Basel Committee on Banking Supervisions. Implementation of these

regulations influences the finance, management, risks and regulatory reporting

practices of the banks.

2. The banks had to assess the data, upgrade the current process with new functionality.

During the data collection process, they have to face huge challenges in maintaining

cost and time.

3. The Basel standards include an enterprise-standards related to business processes. The

banks find difficulties to collect information’s related to the customers and other

organizations.

4. The banks were not able to manage the diverse range of data from multiple business

lines. They find difficulties in calculating the key risk indicators. Basel guidelines

enforce the banks to make extensive data for doing their credit-risks (Zainudin et al.

CREDIT AND LENDING

involves the initiation of the loan applications to classification of the transactions into various

credit-risks (Yaacob, Markom and Hakimah 2018). The regulators want the banks to improve

their risk-management practices to ensure safety in the entire banking system. However, the

internal risk-rating systems of developed banks face various issues during the improvement

of their internal risk rating systems. The different issues are:

Challenges due to the Basel Committee on Banking Supervision (BCBS)

The auditors dealing with the internal risk-reporting system have to monitor the entire

process continuously. They face various challenges while dealing with the risk-rating system.

The internal auditors are involved in dealing with the risk-reporting systems of the company,

are involved in a material misstatement in the company’s balance sheet. This can create an

issue in the development of a banks internal risk-rating system (Kumar and Kaur 2019).

1. The bank faces various challenges to compliance their changes with the regulatory

principles of the Basel Committee on Banking Supervisions. Implementation of these

regulations influences the finance, management, risks and regulatory reporting

practices of the banks.

2. The banks had to assess the data, upgrade the current process with new functionality.

During the data collection process, they have to face huge challenges in maintaining

cost and time.

3. The Basel standards include an enterprise-standards related to business processes. The

banks find difficulties to collect information’s related to the customers and other

organizations.

4. The banks were not able to manage the diverse range of data from multiple business

lines. They find difficulties in calculating the key risk indicators. Basel guidelines

enforce the banks to make extensive data for doing their credit-risks (Zainudin et al.

8

CREDIT AND LENDING

2019). This has led to the exposure of some sensitive exposure of credit data of the

business units.

5. The banking sector faced various complexities in following this regulatory

framework; due to continuous change of the regulatory guidelines. They are unable to

manage the uncertainties that require a strong communication system, a proper

mechanism to manage the change-management and resolve the issues and conflicts.

6. The banks had to adopt a hybrid model, which is a combination of global and

individual country initiatives (Edwards 2016).

Other challenges faced by the banks in internal-risk rating systems

The internal-risk rating system allows the credit risks to be measured on the basis of

quantitative and qualitative factors (Rahim et al., 2017). The different credit scores on

different credit intervals are arranged with a credit grade. This type of risk-rating system is

not applicable in all banking conditions. The large banks require an internal rating system,

which can allow multiple grading account procedures, according to the complex level of the

credits exposed. They require a statistical system to measure the credit risks, based on the

different credit exposures with the growth of internal risk-rating systems (Wang 2020). For

doing this, the banks will have to continuously monitor the level of creditworthiness for

measuring the credit risks. It was found that, due to converging pressure on the banks, the

banks are disclosing poor disclosure of the internal data to face credit risk management

issues. The Basel Committee did not provide any map of showing how to achieve the plans.

The main problems are:

1. Data requirements for measuring the credit risks- Internal risk rating system allows

two approaches; foundation and methodologies. These approaches allow the banks to

use their data to determine the risk (Al-Shawabkeh and Kanungo 2017). These

CREDIT AND LENDING

2019). This has led to the exposure of some sensitive exposure of credit data of the

business units.

5. The banking sector faced various complexities in following this regulatory

framework; due to continuous change of the regulatory guidelines. They are unable to

manage the uncertainties that require a strong communication system, a proper

mechanism to manage the change-management and resolve the issues and conflicts.

6. The banks had to adopt a hybrid model, which is a combination of global and

individual country initiatives (Edwards 2016).

Other challenges faced by the banks in internal-risk rating systems

The internal-risk rating system allows the credit risks to be measured on the basis of

quantitative and qualitative factors (Rahim et al., 2017). The different credit scores on

different credit intervals are arranged with a credit grade. This type of risk-rating system is

not applicable in all banking conditions. The large banks require an internal rating system,

which can allow multiple grading account procedures, according to the complex level of the

credits exposed. They require a statistical system to measure the credit risks, based on the

different credit exposures with the growth of internal risk-rating systems (Wang 2020). For

doing this, the banks will have to continuously monitor the level of creditworthiness for

measuring the credit risks. It was found that, due to converging pressure on the banks, the

banks are disclosing poor disclosure of the internal data to face credit risk management

issues. The Basel Committee did not provide any map of showing how to achieve the plans.

The main problems are:

1. Data requirements for measuring the credit risks- Internal risk rating system allows

two approaches; foundation and methodologies. These approaches allow the banks to

use their data to determine the risk (Al-Shawabkeh and Kanungo 2017). These

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CREDIT AND LENDING

requirements are quite complex. Banks should collect more data through the risk

assessment process. But, they are collecting information on the basis of loan structure

and terms.

2. Proposed practice for meeting the new standards- The banks had to develop a long-

term strategy to solve their issues related to credit risk management (Lim et al., 2017).

The strategy includes acquisition and maintenance strategy. Banks faced challenges in

getting accurate and complete information.

Recommendations

The banks should focus on making a broad term planning, of the entire program in a

long-term perspective. A single rating system cannot solve the problems. The banks should

consider a potential solution and know how to balance the risk data. The banks should

include sound data acquisition and maintenance procedures in their rating system. This will

help the developed banks to store multiple data of the customers (Adrian 2018). Banks should

also determine the regulatory functions; they are aiming and accordingly develop their

business requirements. To advance the credit risk management process with the internal

rating systems, the banks should focus on improving the techniques, on accommodating with

the changes of the credit-risk profiles. They should adequately estimate the credit risk

components. Banks can calculate the FICO score of the customer, which was created by the

Fair Isaac Corporation (Francis 2019). FICO scores will help the bank to determine the credit

extend of customers. Banks can also calculate their debt-to-income ratio for identify their

credit risks.

Conclusion

Therefore, it can be deferred that, the developed bank faces various challenges in

implementing the various challenges in following the regulations of Basel Committee of

CREDIT AND LENDING

requirements are quite complex. Banks should collect more data through the risk

assessment process. But, they are collecting information on the basis of loan structure

and terms.

2. Proposed practice for meeting the new standards- The banks had to develop a long-

term strategy to solve their issues related to credit risk management (Lim et al., 2017).

The strategy includes acquisition and maintenance strategy. Banks faced challenges in

getting accurate and complete information.

Recommendations

The banks should focus on making a broad term planning, of the entire program in a

long-term perspective. A single rating system cannot solve the problems. The banks should

consider a potential solution and know how to balance the risk data. The banks should

include sound data acquisition and maintenance procedures in their rating system. This will

help the developed banks to store multiple data of the customers (Adrian 2018). Banks should

also determine the regulatory functions; they are aiming and accordingly develop their

business requirements. To advance the credit risk management process with the internal

rating systems, the banks should focus on improving the techniques, on accommodating with

the changes of the credit-risk profiles. They should adequately estimate the credit risk

components. Banks can calculate the FICO score of the customer, which was created by the

Fair Isaac Corporation (Francis 2019). FICO scores will help the bank to determine the credit

extend of customers. Banks can also calculate their debt-to-income ratio for identify their

credit risks.

Conclusion

Therefore, it can be deferred that, the developed bank faces various challenges in

implementing the various challenges in following the regulations of Basel Committee of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CREDIT AND LENDING

Banking Supervision. It is recommended that the banks should focus on improving the

techniques more meeting with the various changes related to credit- risk profiles. Bank can

also use FICO score, and debt-to-income ratio to estimate credit extend of the customers.

References

Adrian, T., 2018. Risk management and regulation. International Monetary Fund.

Alber, N. and Ramadan, H., 2017. The Impact of Applying Basel Committee Norms on Asset

Quality of Egyptian Banks. Available at SSRN 2995456.

Al-Shawabkeh, A. and Kanungo, R., 2017. Credit risk estimate using internal explicit

knowledge. Investment Management & Financial Innovations, 14(1), p.55.

Belás, J., Mišanková, M., Schönfeld, J. and Gavurová, B., 2017. CREDIT RISK

MANAGEMENT: FINANCIAL SAFETY AND SUSTAINABILITY ASPECTS. Journal of

Security & Sustainability Issues, 7(1).

Bülbül, D., Hakenes, H. and Lambert, C., 2019. What influences banks’ choice of credit risk

management practices? Theory and evidence. Journal of Financial Stability, 40, pp.1-14.

Coolen‐Maturi, T. and Coolen, F.P.A., 2019. Non‐parametric predictive inference for the

validation of credit rating systems. Journal of the Royal Statistical Society: Series A

(Statistics in Society), 182(4), pp.1189-1204.

Edwards, G.A., 2016. Supervisors’ key roles as banks implement expected credit loss

provisioning. SEACEN Financial Stability Journal, 7(1), pp.1-25.

Francis, G., 2019. Enterprise Risk Management (ERM): Key Risks, Responses and

Applications.

CREDIT AND LENDING

Banking Supervision. It is recommended that the banks should focus on improving the

techniques more meeting with the various changes related to credit- risk profiles. Bank can

also use FICO score, and debt-to-income ratio to estimate credit extend of the customers.

References

Adrian, T., 2018. Risk management and regulation. International Monetary Fund.

Alber, N. and Ramadan, H., 2017. The Impact of Applying Basel Committee Norms on Asset

Quality of Egyptian Banks. Available at SSRN 2995456.

Al-Shawabkeh, A. and Kanungo, R., 2017. Credit risk estimate using internal explicit

knowledge. Investment Management & Financial Innovations, 14(1), p.55.

Belás, J., Mišanková, M., Schönfeld, J. and Gavurová, B., 2017. CREDIT RISK

MANAGEMENT: FINANCIAL SAFETY AND SUSTAINABILITY ASPECTS. Journal of

Security & Sustainability Issues, 7(1).

Bülbül, D., Hakenes, H. and Lambert, C., 2019. What influences banks’ choice of credit risk

management practices? Theory and evidence. Journal of Financial Stability, 40, pp.1-14.

Coolen‐Maturi, T. and Coolen, F.P.A., 2019. Non‐parametric predictive inference for the

validation of credit rating systems. Journal of the Royal Statistical Society: Series A

(Statistics in Society), 182(4), pp.1189-1204.

Edwards, G.A., 2016. Supervisors’ key roles as banks implement expected credit loss

provisioning. SEACEN Financial Stability Journal, 7(1), pp.1-25.

Francis, G., 2019. Enterprise Risk Management (ERM): Key Risks, Responses and

Applications.

11

CREDIT AND LENDING

Kumar, S. and Kaur, M., 2019. CORPORATE GOVERNANCE OF BANKS. CORPORATE

GOVERNANCE, 7(02).

Lim, C.Y., Woods, M., Humphrey, C. and Seow, J.L., 2017. The paradoxes of risk

management in the banking sector. The British Accounting Review, 49(1), pp.75-90.

Mignola, G., Ugoccioni, R. and Cope, E., 2016. Comments on the Basel Committee on

Banking Supervision proposal for a new standardized approach for operational risk. Journal

of Operational Risk, 11(3).

Rahim, N.F.A., Jaafar, A.R., Syamsuddin, J. and Sarkawi, M.N., 2017. Internal Control

System and Hazard Identification of Operational Risk in Malaysian Conventional Banking.

Int. J Sup. Chain. Mgt Vol, 6(2), p.215.

Tillich, D. and Lehmann, C., 2016. Estimation in discontinuous Bernoulli mixture models

applicable in credit rating systems with dependent data. Technische Universität, Fakultät

Wirtschaftswissenschaften.

Wang, B. and Wang, X., 2020, January. Study on the Current Development, Problems, and

Countermeasures of Shadow Banking in China. In 5th International Conference on

Economics, Management, Law and Education (EMLE 2019) (pp. 383-386). Atlantis Press.

Yaacob, H., Markom, R. and Hakimah, A., 2018. COPING WITH THE INTERNATIONAL

STANDARDS OF BASEL COMMITTEE ON CORE PRINCIPLES ON EFFECTIVE

BANKING SUPERVISION (BCBS): ANALYSIS AND REFORM FOR ISLAMIC

BANKING.

Zainudin, S.M., Rasid, A., Zaleha, S., Omar, R. and Hassan, R., 2019. The Good and Bad

News about the New Liquidity Rules of Basel III in Islamic Banking of Malaysia. Journal of

Risk and Financial Management, 12(3), p.120.

CREDIT AND LENDING

Kumar, S. and Kaur, M., 2019. CORPORATE GOVERNANCE OF BANKS. CORPORATE

GOVERNANCE, 7(02).

Lim, C.Y., Woods, M., Humphrey, C. and Seow, J.L., 2017. The paradoxes of risk

management in the banking sector. The British Accounting Review, 49(1), pp.75-90.

Mignola, G., Ugoccioni, R. and Cope, E., 2016. Comments on the Basel Committee on

Banking Supervision proposal for a new standardized approach for operational risk. Journal

of Operational Risk, 11(3).

Rahim, N.F.A., Jaafar, A.R., Syamsuddin, J. and Sarkawi, M.N., 2017. Internal Control

System and Hazard Identification of Operational Risk in Malaysian Conventional Banking.

Int. J Sup. Chain. Mgt Vol, 6(2), p.215.

Tillich, D. and Lehmann, C., 2016. Estimation in discontinuous Bernoulli mixture models

applicable in credit rating systems with dependent data. Technische Universität, Fakultät

Wirtschaftswissenschaften.

Wang, B. and Wang, X., 2020, January. Study on the Current Development, Problems, and

Countermeasures of Shadow Banking in China. In 5th International Conference on

Economics, Management, Law and Education (EMLE 2019) (pp. 383-386). Atlantis Press.

Yaacob, H., Markom, R. and Hakimah, A., 2018. COPING WITH THE INTERNATIONAL

STANDARDS OF BASEL COMMITTEE ON CORE PRINCIPLES ON EFFECTIVE

BANKING SUPERVISION (BCBS): ANALYSIS AND REFORM FOR ISLAMIC

BANKING.

Zainudin, S.M., Rasid, A., Zaleha, S., Omar, R. and Hassan, R., 2019. The Good and Bad

News about the New Liquidity Rules of Basel III in Islamic Banking of Malaysia. Journal of

Risk and Financial Management, 12(3), p.120.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.