Credit Risk Assessment and Management: A Financial Report

VerifiedAdded on 2022/12/28

|17

|4122

|1

Report

AI Summary

This report provides a comprehensive analysis of credit risk, encompassing assessment methodologies, management strategies, and real-world applications. It begins by defining credit risk and its implications, followed by a detailed examination of various assessment methods, including financial ratio analysis, cash flow analysis, and credit scoring models. The report explores how different entities and financial institutions evaluate credit risk, with examples from Fitch Ratings and Barclays Bank. It also covers the implementation of Basel II framework and credit risk management strategies. The report further analyzes the credit risk management practices within Wood Green Timber. It discusses management and governance structures, bad debt provisions, collateralization, and securities. Finally, it concludes with strategies for managing and reducing credit risks, such as risk-based pricing. Overall, the report offers valuable insights into the complexities of credit risk and its significance in the financial sector.

TASK 2

Introduction

Credit risk is regarded as the probability of loss which results from the failure of the borrower

in repaying the borrowed amount or meeting contractual covenants. Traditionally it is

regarded as the risk that the lender of money might not get the owed interest amount or

principal amount, whose ultimate outcome would be the interrupted cash flows and the cost of

collection would be enhanced. Defaults in payments can be in form of number of

circumstance like a consumer failing to repay mortgage loan or line of credit or a company

fails to repay asset-secured fixed or floating charge debt (Andrews, Gentzkow and Shapiro,

2020).

In addition to that, the credit risks can be assessed or determined with respect to the

basic ability of the borrowers for the repayment of loan as per the original terms of the

contracts. In order to make an assessment of the credit risks on loans by the consumers, the

lenders consider five Cs which includes capability to repay, credit history, the conditions of

the loan, capital and the collateral attached. Numerous companies and institutions have

different ways of assessing the credit risk which allows the entity to reach a decision about

whether to provide a loan to such entity or not.

How the Credit Risk can be assessed

Different entities and financial institutions utilise different modes of assessing the credit risks

some of the commonly utilised ways of assessing the credit risks includes financial ratios

analysis, Du Point Modelling, Cash flow statement analysis, modelling default, credit scoring,

credit risks equations, reports of the directors, audit report, customer profiling, credit policy,

credit history, stress testing, scorecards, risk rating, credit appraisal, KPI and risk memo. The

organisations all over the world utilises few of these options in order to analyse the credit risk

with respect to a particular loan to a specific lender (Erbuga, 2016). Credit rating agencies

develop their customised models for assessing risks. For example, in order to assess default

risk in credit portfolios backing collateralised debt obligations (CDOs) of asset backed

securities of corporates, Fitch Ratings has developed The Fitch Portfolio Credit Model. It is a

Monte Carlo simulation model which takes into account default probability, recovery rates,

and correlation between assets in portfolios to evaluate risk level. Fitch Model simulates the

default behaviour of individual assets in credit portfolio. It then draws a structural form

methodology which holds that a firm defaults if the value of its assets fall below value of

liabilities. It is not a cash flow model and also disregards payment waterfalls or excess spread

Introduction

Credit risk is regarded as the probability of loss which results from the failure of the borrower

in repaying the borrowed amount or meeting contractual covenants. Traditionally it is

regarded as the risk that the lender of money might not get the owed interest amount or

principal amount, whose ultimate outcome would be the interrupted cash flows and the cost of

collection would be enhanced. Defaults in payments can be in form of number of

circumstance like a consumer failing to repay mortgage loan or line of credit or a company

fails to repay asset-secured fixed or floating charge debt (Andrews, Gentzkow and Shapiro,

2020).

In addition to that, the credit risks can be assessed or determined with respect to the

basic ability of the borrowers for the repayment of loan as per the original terms of the

contracts. In order to make an assessment of the credit risks on loans by the consumers, the

lenders consider five Cs which includes capability to repay, credit history, the conditions of

the loan, capital and the collateral attached. Numerous companies and institutions have

different ways of assessing the credit risk which allows the entity to reach a decision about

whether to provide a loan to such entity or not.

How the Credit Risk can be assessed

Different entities and financial institutions utilise different modes of assessing the credit risks

some of the commonly utilised ways of assessing the credit risks includes financial ratios

analysis, Du Point Modelling, Cash flow statement analysis, modelling default, credit scoring,

credit risks equations, reports of the directors, audit report, customer profiling, credit policy,

credit history, stress testing, scorecards, risk rating, credit appraisal, KPI and risk memo. The

organisations all over the world utilises few of these options in order to analyse the credit risk

with respect to a particular loan to a specific lender (Erbuga, 2016). Credit rating agencies

develop their customised models for assessing risks. For example, in order to assess default

risk in credit portfolios backing collateralised debt obligations (CDOs) of asset backed

securities of corporates, Fitch Ratings has developed The Fitch Portfolio Credit Model. It is a

Monte Carlo simulation model which takes into account default probability, recovery rates,

and correlation between assets in portfolios to evaluate risk level. Fitch Model simulates the

default behaviour of individual assets in credit portfolio. It then draws a structural form

methodology which holds that a firm defaults if the value of its assets fall below value of

liabilities. It is not a cash flow model and also disregards payment waterfalls or excess spread

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Kumar, 2019). It gives output in the form of rating default rate, rating loss rate and rating

recovery rate.

The banks and financial institutions utilises the cash flow statement and consider the

cash generated by the business through their operating cash flows, if the operating cash flows

of the entity suggests a consistent growth over the period, or the entity have managed to

reduce the overall cost or both the targets are being achieved. In addition to that, the banks

and lending institutions also utilises the financial ratios to analyse the credit risk in any

investment or lending being made to the consumer. Credit analysis ratios are regarded as the

tools which assists the process of credit analysis. There are numerous sets of financial ratios

which allows the lending institution or the credit rating agency to determine the credit risk

involved in the particular transaction. The liquidity ratios like the current ratios and the quick

ratios help analyse the capability of the entity to pay off its current liabilities which are due in

the next 12 months. Moreover, the coverage credit ratios like interest coverage ratio, cash

coverage ratio, debt service coverage ratio and asset coverage ratio as these ratios measures

the overall coverage cash, income, or assets provides for interest expense or debt. If the

borrowing entity has a higher coverage ratio then it suggests that the entity has a greater

capacity to meet the financial obligations (Polato, 2019).

In addition to that, the lending institutions also utilises the Key Performance Indicators (KPIs)

which is regarded as a value which can be measured that demonstrate how the entities

efficiently achieving major business targets. This actually allows the lending institutions to

determine the success rate of the business entity and whether they would be able to pay off the

principle amount and the interest amount or not. Moreover, it is a common practice on behalf

of the lending institutions to assess the credit risk of the individual business entity or the

individual by looking at its credit profile which shows its credit rating by the banks and other

financial institutions based on the past trends and their capacity as a business entity to pay off

the loan amount and the interest payment. In addition to that, the lending institution also look

at the credit history of the individual consumer or the business entity as it a complete record

of the borrower’s debt repayment in the past in a responsible manner from various sources

including credit card companies, banks, governments and collection agencies as it provides

recovery rate.

The banks and financial institutions utilises the cash flow statement and consider the

cash generated by the business through their operating cash flows, if the operating cash flows

of the entity suggests a consistent growth over the period, or the entity have managed to

reduce the overall cost or both the targets are being achieved. In addition to that, the banks

and lending institutions also utilises the financial ratios to analyse the credit risk in any

investment or lending being made to the consumer. Credit analysis ratios are regarded as the

tools which assists the process of credit analysis. There are numerous sets of financial ratios

which allows the lending institution or the credit rating agency to determine the credit risk

involved in the particular transaction. The liquidity ratios like the current ratios and the quick

ratios help analyse the capability of the entity to pay off its current liabilities which are due in

the next 12 months. Moreover, the coverage credit ratios like interest coverage ratio, cash

coverage ratio, debt service coverage ratio and asset coverage ratio as these ratios measures

the overall coverage cash, income, or assets provides for interest expense or debt. If the

borrowing entity has a higher coverage ratio then it suggests that the entity has a greater

capacity to meet the financial obligations (Polato, 2019).

In addition to that, the lending institutions also utilises the Key Performance Indicators (KPIs)

which is regarded as a value which can be measured that demonstrate how the entities

efficiently achieving major business targets. This actually allows the lending institutions to

determine the success rate of the business entity and whether they would be able to pay off the

principle amount and the interest amount or not. Moreover, it is a common practice on behalf

of the lending institutions to assess the credit risk of the individual business entity or the

individual by looking at its credit profile which shows its credit rating by the banks and other

financial institutions based on the past trends and their capacity as a business entity to pay off

the loan amount and the interest payment. In addition to that, the lending institution also look

at the credit history of the individual consumer or the business entity as it a complete record

of the borrower’s debt repayment in the past in a responsible manner from various sources

including credit card companies, banks, governments and collection agencies as it provides

the capital history of the individual or an entity. For example, HSBC Bank has a separate

committee for credit risk evaluation which is known as Credit Risk Analytics Oversight

Committee which checks the overall risk portfolio of the company and further guides

subordinate teams on the guidelines to be followed for assessing credit worthiness and the

underlying risk analysis. It uses 5C model and checks capacity, collateral, capital, character

and condition of the applicant. Credit score given by credit rating agencies like Fitch Ratings

play a very important role followed by the detailed assessment of the historical payments by

the applicant (Orna, 2017).

Considering the practical application of the Barclays Bank of the United Kingdom, as

it is evident from their annual report that the entity utilises the framework provide in Basel 2

as part of the strategy of capital management. As per this particular framework which is

developed of three basic pillars, under the first pillar the entity calculates the risk weighted

assets for credit risks, under the pillar 2 the entity consider a view on whether the bank

requires to hold an additional capital for dealing with the credit risks, whereas, the third pillar

covers the overall communication with respect to the credits risks of the consumers and the

credit risk face by the entity. Barclays bank also carry-out a test on a regular basis under

which the comparison of the credit exposure is being made with the other banks of the

industry. This would allow the entity to manage their respective credit risk and maintain the

capital requirement. The Bank of England have also stated a certain amount of minimum

capital requirement which is also been followed by the Barclays Bank. As per the

standardised approach method requirement for credit risk is monitored by the entity on a

regular basis and the credit exposure of the entity is managed based on the credit risk capital

requirement as per the internal SOPs of the entity and the regulations provided by the Bank of

England.

Conclusion

committee for credit risk evaluation which is known as Credit Risk Analytics Oversight

Committee which checks the overall risk portfolio of the company and further guides

subordinate teams on the guidelines to be followed for assessing credit worthiness and the

underlying risk analysis. It uses 5C model and checks capacity, collateral, capital, character

and condition of the applicant. Credit score given by credit rating agencies like Fitch Ratings

play a very important role followed by the detailed assessment of the historical payments by

the applicant (Orna, 2017).

Considering the practical application of the Barclays Bank of the United Kingdom, as

it is evident from their annual report that the entity utilises the framework provide in Basel 2

as part of the strategy of capital management. As per this particular framework which is

developed of three basic pillars, under the first pillar the entity calculates the risk weighted

assets for credit risks, under the pillar 2 the entity consider a view on whether the bank

requires to hold an additional capital for dealing with the credit risks, whereas, the third pillar

covers the overall communication with respect to the credits risks of the consumers and the

credit risk face by the entity. Barclays bank also carry-out a test on a regular basis under

which the comparison of the credit exposure is being made with the other banks of the

industry. This would allow the entity to manage their respective credit risk and maintain the

capital requirement. The Bank of England have also stated a certain amount of minimum

capital requirement which is also been followed by the Barclays Bank. As per the

standardised approach method requirement for credit risk is monitored by the entity on a

regular basis and the credit exposure of the entity is managed based on the credit risk capital

requirement as per the internal SOPs of the entity and the regulations provided by the Bank of

England.

Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the end it can be concluded that there are numerous options available to the entities,

financial institutions and non-financial institutions to assess the credit risk which are being

discussed already. It is evident that the entities utilised more than one option for assessing the

credit risk some of the basic options include the relevant financial ratios, cash flow statement

especially the net cash flows from operating activities, Du Point analysis and there are

numerous credit rating agencies which maintains the credit profile of an individual or an

entity and helps in determining their capacity of principal repayment and interest payments.

Same is the case with Barclays Bank who has maintained its minimum capital requirement in

order to deal with the exposure and credit risk.

TASK 3

Name of organisation:

Wood Green Timber

Main objectives:

The main objective of the credit risk management of the particular financial is to minimize

the losses generated from the loans provided to the consumer while enhancing the overall

income of the entity.

Management and governance:

financial institutions and non-financial institutions to assess the credit risk which are being

discussed already. It is evident that the entities utilised more than one option for assessing the

credit risk some of the basic options include the relevant financial ratios, cash flow statement

especially the net cash flows from operating activities, Du Point analysis and there are

numerous credit rating agencies which maintains the credit profile of an individual or an

entity and helps in determining their capacity of principal repayment and interest payments.

Same is the case with Barclays Bank who has maintained its minimum capital requirement in

order to deal with the exposure and credit risk.

TASK 3

Name of organisation:

Wood Green Timber

Main objectives:

The main objective of the credit risk management of the particular financial is to minimize

the losses generated from the loans provided to the consumer while enhancing the overall

income of the entity.

Management and governance:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The entity has developed a particular management and governance structure within an

organization and a specific department which is solely developed for the purpose of the

managing the credit risk of the organization and helps the entity in achieving its overall

objective of enhancing the overall income and the reducing the loan losses. In my chosen

organization there is a comprehensive governance committee and under this particular

committee, there is a sub-department of credit risk management which directly reports to the

board of directors after consulting the governance committee of the Board of Directors.

Credit Risk Management is regarded as one of the major issue with respect to banking

industry.

Regulation and responsibility for credit risk

Sox throughout the nation, it impacts all public corporations by forcing them to comply with

the terms of the 11 parts of the Act. In contrast to publicly listed entities, Sarbanes-Oxley

often controls financial firms which conduct audits for each and every U.S. public

corporation, alongside their subsidiaries including international companies which are wholly

owned while doing business in this Country (Lemieux, 2017). In an attempt to enable visitors

to stay forward to expose alleged illegal activity in wood green timber company, Sarbanes-

Oxley provides security for squeal. Experts also said that the stringent sanctions for officers,

major shareholders, and accountants for losing company records are clearly illegal and will

extend to non-profit entities and also law-targeted market capitalisation firms.

Bad debt provision for company

The provision for bad debts may apply to the set of accounts, also referred to this as

the Bad Debts Payment, Questionable Liabilities Income, or Unpayable Account Exemption

(Sharma, Kanchan and Krishan, 2018). So then, a contra asset fund is the account Allowance

for Doubtful Debt (an asset account with a credit balance). In addition, for the capital

structure of company for the credit risk it is to disclose the valuation adjustments valuation of

the deferred revenue records of the business, it has been used together with the payroll

Consumer Receives. The entry in such contrary transactions to raise the monthly payment is a

deduction to the Bad Debts Cost balance sheet report. In the context of wood green timber, it

is also stated that to record the credit losses corresponding to the duration of the balance sheet,

organization and a specific department which is solely developed for the purpose of the

managing the credit risk of the organization and helps the entity in achieving its overall

objective of enhancing the overall income and the reducing the loan losses. In my chosen

organization there is a comprehensive governance committee and under this particular

committee, there is a sub-department of credit risk management which directly reports to the

board of directors after consulting the governance committee of the Board of Directors.

Credit Risk Management is regarded as one of the major issue with respect to banking

industry.

Regulation and responsibility for credit risk

Sox throughout the nation, it impacts all public corporations by forcing them to comply with

the terms of the 11 parts of the Act. In contrast to publicly listed entities, Sarbanes-Oxley

often controls financial firms which conduct audits for each and every U.S. public

corporation, alongside their subsidiaries including international companies which are wholly

owned while doing business in this Country (Lemieux, 2017). In an attempt to enable visitors

to stay forward to expose alleged illegal activity in wood green timber company, Sarbanes-

Oxley provides security for squeal. Experts also said that the stringent sanctions for officers,

major shareholders, and accountants for losing company records are clearly illegal and will

extend to non-profit entities and also law-targeted market capitalisation firms.

Bad debt provision for company

The provision for bad debts may apply to the set of accounts, also referred to this as

the Bad Debts Payment, Questionable Liabilities Income, or Unpayable Account Exemption

(Sharma, Kanchan and Krishan, 2018). So then, a contra asset fund is the account Allowance

for Doubtful Debt (an asset account with a credit balance). In addition, for the capital

structure of company for the credit risk it is to disclose the valuation adjustments valuation of

the deferred revenue records of the business, it has been used together with the payroll

Consumer Receives. The entry in such contrary transactions to raise the monthly payment is a

deduction to the Bad Debts Cost balance sheet report. In the context of wood green timber, it

is also stated that to record the credit losses corresponding to the duration of the balance sheet,

use the summary clause for consumer debt on the cash flow statement. In any case, it will be a

financial statements account to provide for bad loans.

Collateralisation and securities

Usually, the principal balance required in a collateralized lending is dependent on the estate's

appraised credit quality. Around 70 percent to 90 percent of the cost of the assets would be

loaned by most insured lenders. Collateralized mortgages are intrinsically better and thus

usually have lower returns than non-collateralized mortgages. Savings accounts and consumer

lending provide non-collateralized, or unprotected, loans. Securities at other side, enable the

lender to profit both from the debt and the portfolio of securities whereas the mortgage is

already being repaid while the portfolio of securities stays underneath the ownership of the

investor. The borrower takes a higher risk, nevertheless, since the valuation of the bonds can

fluctuate dramatically (Linder and Williander, 2017).

Actions to manage and reduce credit risks

Risk based pricing: The Lender normally owes the Creditors a higher interest rate

here the, because they see a danger of defaults to see the financial situation or the Creditor's

background experience. Therefore, under this form of credit risk management framework,

regarding the risk tolerance as well as the willingness to repay the loan, varying rates would

be adapted to various creditors. For both the loan granted to beginning firms, the company

charges a higher interest rate only comparatively low the rate of interest as and then when the

economy wants to succeed. In this, any default to a lower rate better borrower is paid by the

other consumer to which the mortgage has also been granted much high rate.

Inserting covenants: Throughout the Term Loan, the Borrower may attach certain clauses or

assumable before distributing the funding to the Borrower. Capital Covenants, Organizational

Covenants, Technological Covenants & Company Level Contractual obligations may be

categorized into them. Any violation of the Covenant pursuant to the Arrangement would

cause a warning signal to the Borrower that even a failure will occur in the coming years, and

reasonable steps should be taken to protect the amount of the loan. For instance, according to

the recent amendments in the RBI Guidance, the Capital Adequacy is among the most

significant agreements for all the NBFC to retain up to 15 percent. It will be a compliance

violation for the NBFC at any point whether that ratio falls under 155 and would in fact have

significant consequences for the firm as well as its lenders to never track the very same

effectively (Menna, Agrafiotis and Georgopoulos, 2018).

financial statements account to provide for bad loans.

Collateralisation and securities

Usually, the principal balance required in a collateralized lending is dependent on the estate's

appraised credit quality. Around 70 percent to 90 percent of the cost of the assets would be

loaned by most insured lenders. Collateralized mortgages are intrinsically better and thus

usually have lower returns than non-collateralized mortgages. Savings accounts and consumer

lending provide non-collateralized, or unprotected, loans. Securities at other side, enable the

lender to profit both from the debt and the portfolio of securities whereas the mortgage is

already being repaid while the portfolio of securities stays underneath the ownership of the

investor. The borrower takes a higher risk, nevertheless, since the valuation of the bonds can

fluctuate dramatically (Linder and Williander, 2017).

Actions to manage and reduce credit risks

Risk based pricing: The Lender normally owes the Creditors a higher interest rate

here the, because they see a danger of defaults to see the financial situation or the Creditor's

background experience. Therefore, under this form of credit risk management framework,

regarding the risk tolerance as well as the willingness to repay the loan, varying rates would

be adapted to various creditors. For both the loan granted to beginning firms, the company

charges a higher interest rate only comparatively low the rate of interest as and then when the

economy wants to succeed. In this, any default to a lower rate better borrower is paid by the

other consumer to which the mortgage has also been granted much high rate.

Inserting covenants: Throughout the Term Loan, the Borrower may attach certain clauses or

assumable before distributing the funding to the Borrower. Capital Covenants, Organizational

Covenants, Technological Covenants & Company Level Contractual obligations may be

categorized into them. Any violation of the Covenant pursuant to the Arrangement would

cause a warning signal to the Borrower that even a failure will occur in the coming years, and

reasonable steps should be taken to protect the amount of the loan. For instance, according to

the recent amendments in the RBI Guidance, the Capital Adequacy is among the most

significant agreements for all the NBFC to retain up to 15 percent. It will be a compliance

violation for the NBFC at any point whether that ratio falls under 155 and would in fact have

significant consequences for the firm as well as its lenders to never track the very same

effectively (Menna, Agrafiotis and Georgopoulos, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Limiting sectors exposure: In this, since it would have a huge effect mostly on NPA

levels of the wood green timber, the investor will determine the industries in which he will be

involved in lending the resources to the lender. Throughout optimising its returns and retain

leverage over the potential customers instead of distributing the deposits at different stages,

the Lender can often opt to loan to a certain state or city.

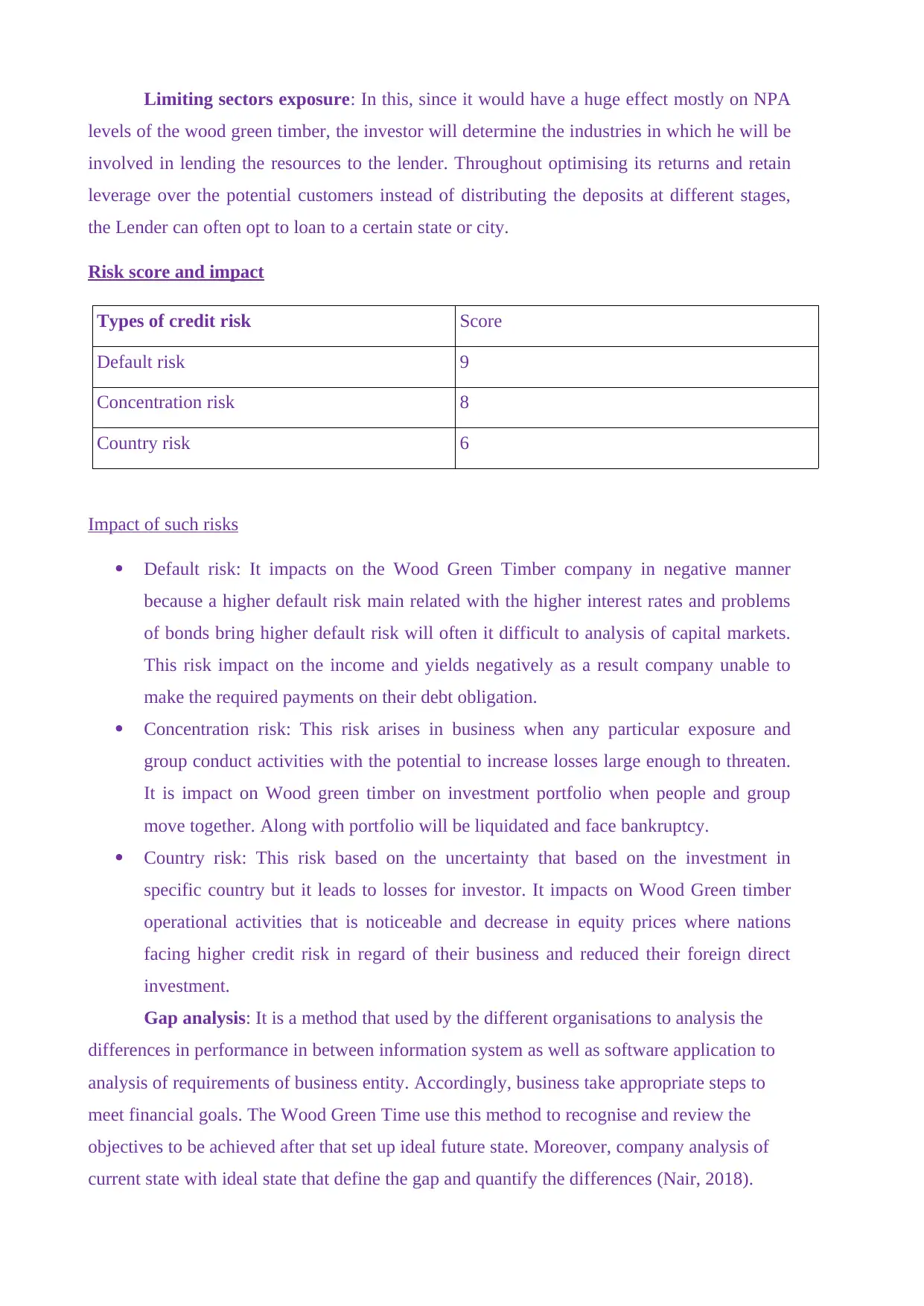

Risk score and impact

Types of credit risk Score

Default risk 9

Concentration risk 8

Country risk 6

Impact of such risks

Default risk: It impacts on the Wood Green Timber company in negative manner

because a higher default risk main related with the higher interest rates and problems

of bonds bring higher default risk will often it difficult to analysis of capital markets.

This risk impact on the income and yields negatively as a result company unable to

make the required payments on their debt obligation.

Concentration risk: This risk arises in business when any particular exposure and

group conduct activities with the potential to increase losses large enough to threaten.

It is impact on Wood green timber on investment portfolio when people and group

move together. Along with portfolio will be liquidated and face bankruptcy.

Country risk: This risk based on the uncertainty that based on the investment in

specific country but it leads to losses for investor. It impacts on Wood Green timber

operational activities that is noticeable and decrease in equity prices where nations

facing higher credit risk in regard of their business and reduced their foreign direct

investment.

Gap analysis: It is a method that used by the different organisations to analysis the

differences in performance in between information system as well as software application to

analysis of requirements of business entity. Accordingly, business take appropriate steps to

meet financial goals. The Wood Green Time use this method to recognise and review the

objectives to be achieved after that set up ideal future state. Moreover, company analysis of

current state with ideal state that define the gap and quantify the differences (Nair, 2018).

levels of the wood green timber, the investor will determine the industries in which he will be

involved in lending the resources to the lender. Throughout optimising its returns and retain

leverage over the potential customers instead of distributing the deposits at different stages,

the Lender can often opt to loan to a certain state or city.

Risk score and impact

Types of credit risk Score

Default risk 9

Concentration risk 8

Country risk 6

Impact of such risks

Default risk: It impacts on the Wood Green Timber company in negative manner

because a higher default risk main related with the higher interest rates and problems

of bonds bring higher default risk will often it difficult to analysis of capital markets.

This risk impact on the income and yields negatively as a result company unable to

make the required payments on their debt obligation.

Concentration risk: This risk arises in business when any particular exposure and

group conduct activities with the potential to increase losses large enough to threaten.

It is impact on Wood green timber on investment portfolio when people and group

move together. Along with portfolio will be liquidated and face bankruptcy.

Country risk: This risk based on the uncertainty that based on the investment in

specific country but it leads to losses for investor. It impacts on Wood Green timber

operational activities that is noticeable and decrease in equity prices where nations

facing higher credit risk in regard of their business and reduced their foreign direct

investment.

Gap analysis: It is a method that used by the different organisations to analysis the

differences in performance in between information system as well as software application to

analysis of requirements of business entity. Accordingly, business take appropriate steps to

meet financial goals. The Wood Green Time use this method to recognise and review the

objectives to be achieved after that set up ideal future state. Moreover, company analysis of

current state with ideal state that define the gap and quantify the differences (Nair, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

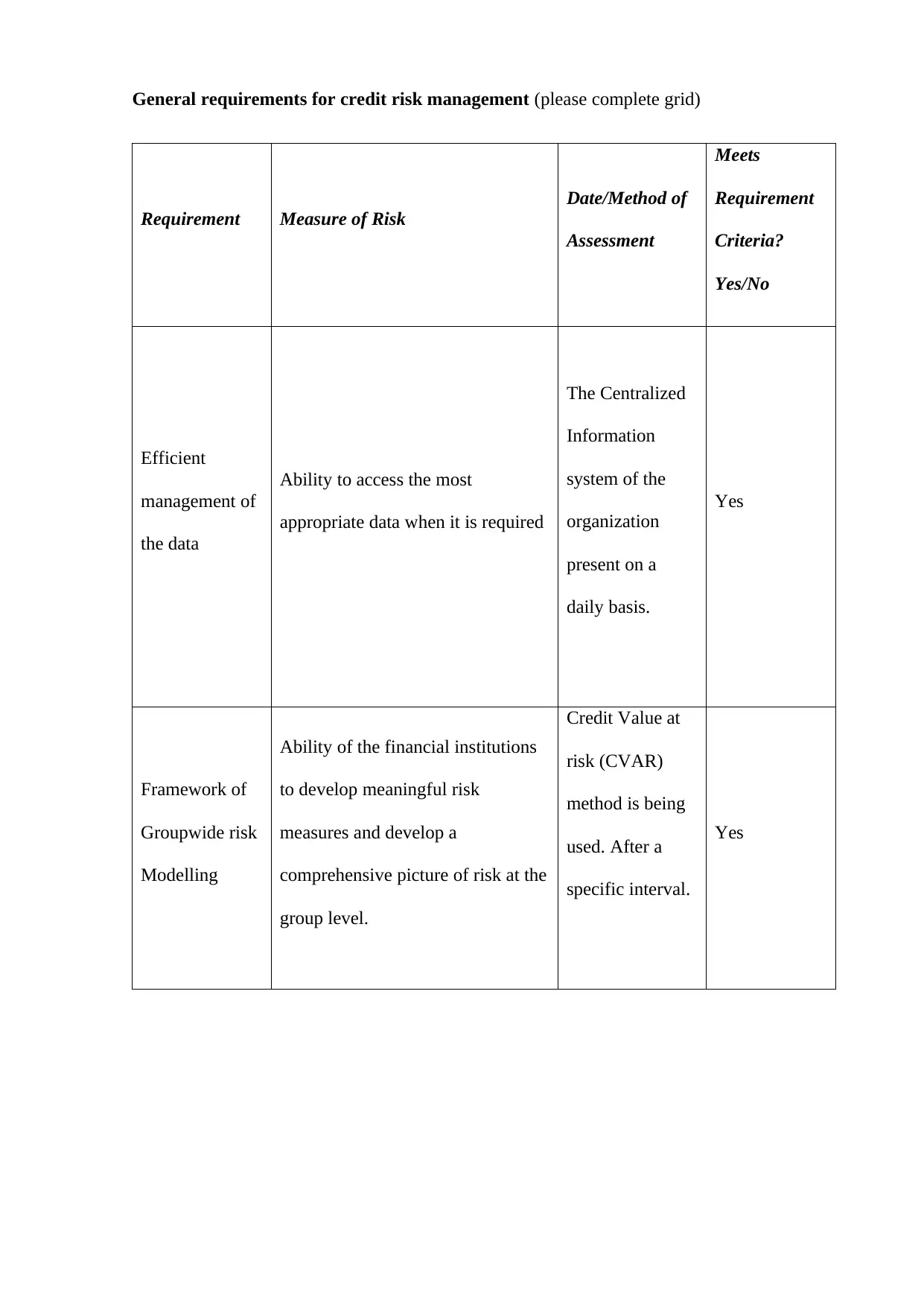

General requirements for credit risk management (please complete grid)

Requirement Measure of Risk

Date/Method of

Assessment

Meets

Requirement

Criteria?

Yes/No

Efficient

management of

the data

Ability to access the most

appropriate data when it is required

The Centralized

Information

system of the

organization

present on a

daily basis.

Yes

Framework of

Groupwide risk

Modelling

Ability of the financial institutions

to develop meaningful risk

measures and develop a

comprehensive picture of risk at the

group level.

Credit Value at

risk (CVAR)

method is being

used. After a

specific interval.

Yes

Requirement Measure of Risk

Date/Method of

Assessment

Meets

Requirement

Criteria?

Yes/No

Efficient

management of

the data

Ability to access the most

appropriate data when it is required

The Centralized

Information

system of the

organization

present on a

daily basis.

Yes

Framework of

Groupwide risk

Modelling

Ability of the financial institutions

to develop meaningful risk

measures and develop a

comprehensive picture of risk at the

group level.

Credit Value at

risk (CVAR)

method is being

used. After a

specific interval.

Yes

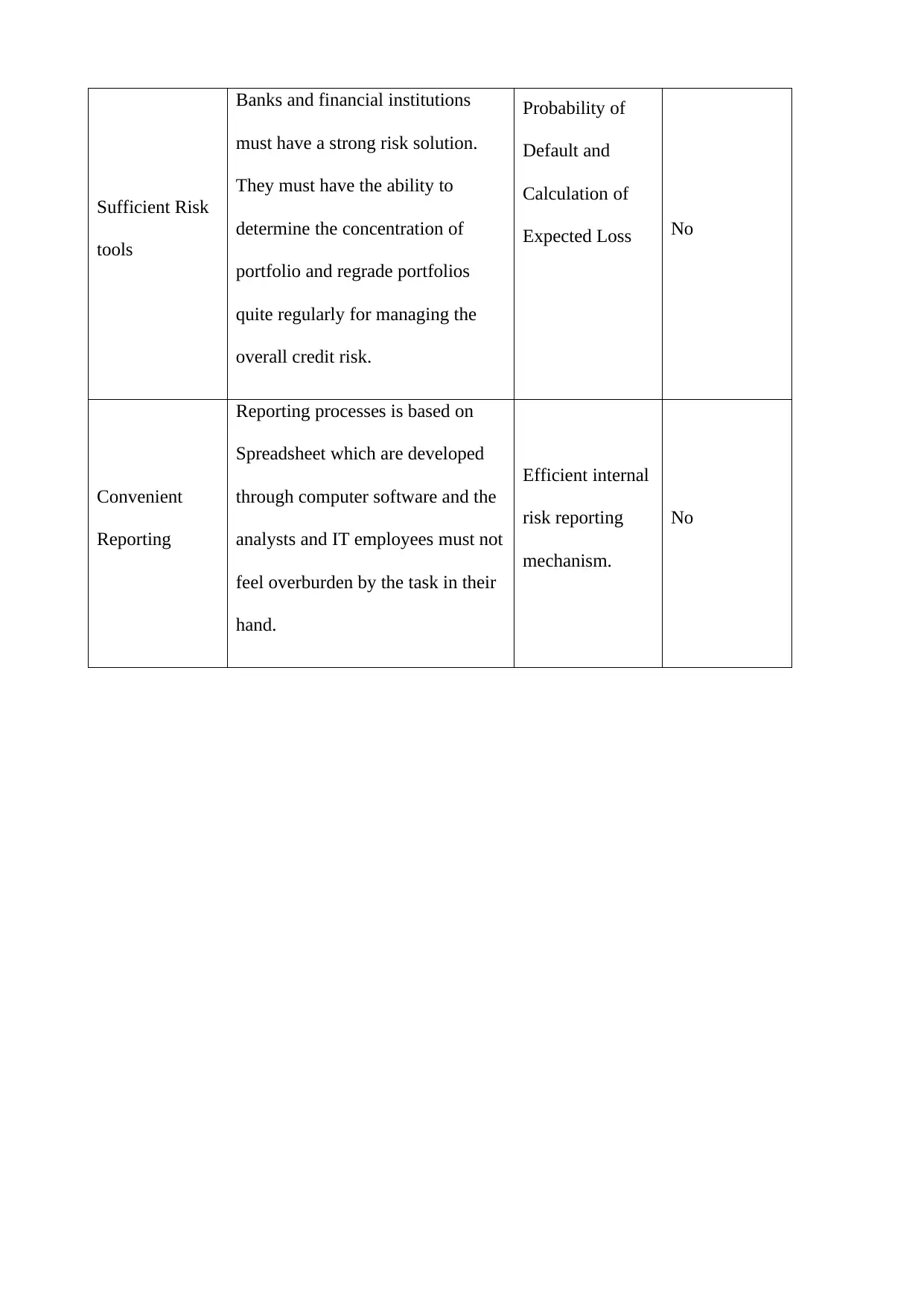

Sufficient Risk

tools

Banks and financial institutions

must have a strong risk solution.

They must have the ability to

determine the concentration of

portfolio and regrade portfolios

quite regularly for managing the

overall credit risk.

Probability of

Default and

Calculation of

Expected Loss No

Convenient

Reporting

Reporting processes is based on

Spreadsheet which are developed

through computer software and the

analysts and IT employees must not

feel overburden by the task in their

hand.

Efficient internal

risk reporting

mechanism.

No

tools

Banks and financial institutions

must have a strong risk solution.

They must have the ability to

determine the concentration of

portfolio and regrade portfolios

quite regularly for managing the

overall credit risk.

Probability of

Default and

Calculation of

Expected Loss No

Convenient

Reporting

Reporting processes is based on

Spreadsheet which are developed

through computer software and the

analysts and IT employees must not

feel overburden by the task in their

hand.

Efficient internal

risk reporting

mechanism.

No

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of findings (please complete tables below; expand as necessary):

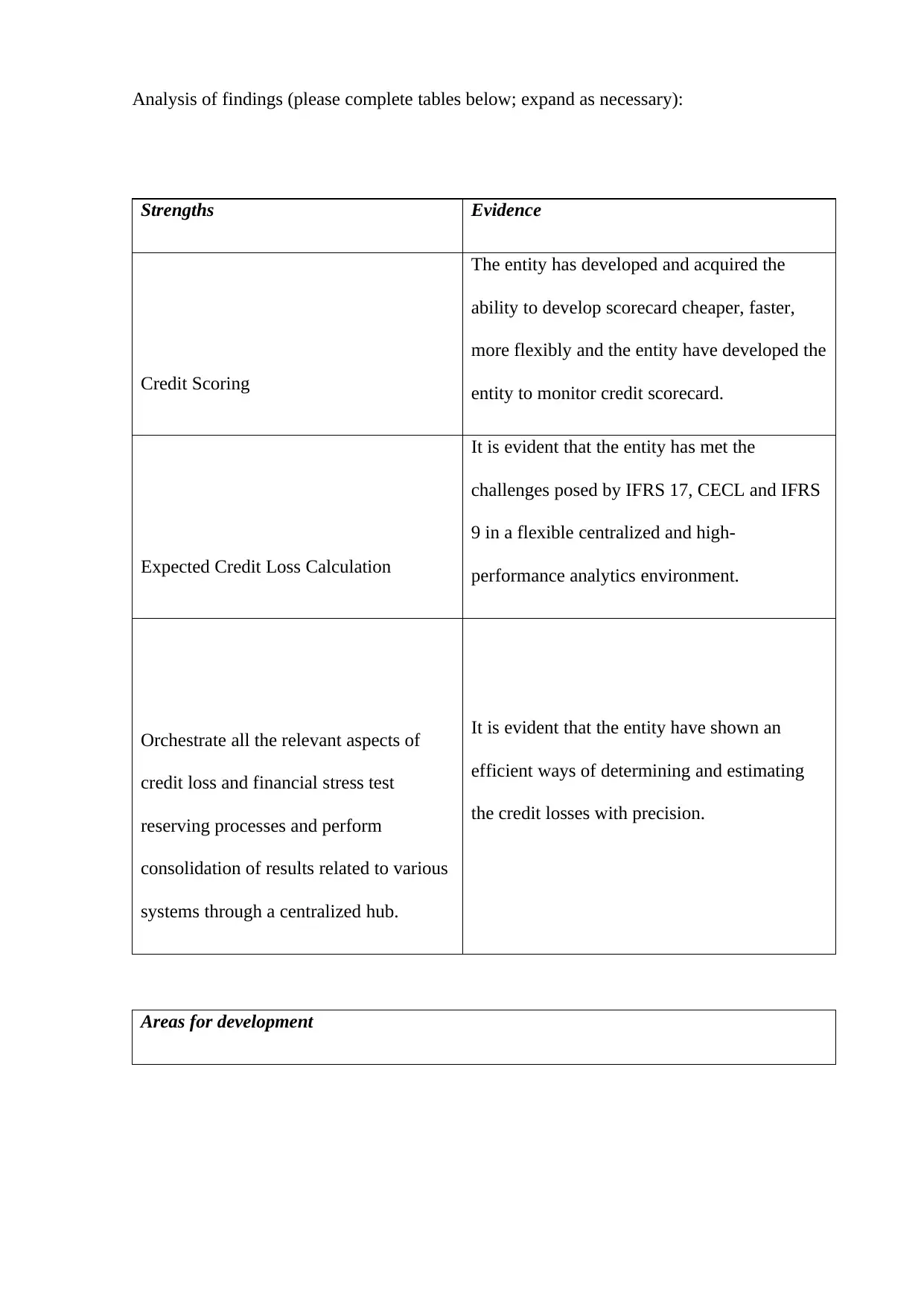

Strengths Evidence

Credit Scoring

The entity has developed and acquired the

ability to develop scorecard cheaper, faster,

more flexibly and the entity have developed the

entity to monitor credit scorecard.

Expected Credit Loss Calculation

It is evident that the entity has met the

challenges posed by IFRS 17, CECL and IFRS

9 in a flexible centralized and high-

performance analytics environment.

Orchestrate all the relevant aspects of

credit loss and financial stress test

reserving processes and perform

consolidation of results related to various

systems through a centralized hub.

It is evident that the entity have shown an

efficient ways of determining and estimating

the credit losses with precision.

Areas for development

Strengths Evidence

Credit Scoring

The entity has developed and acquired the

ability to develop scorecard cheaper, faster,

more flexibly and the entity have developed the

entity to monitor credit scorecard.

Expected Credit Loss Calculation

It is evident that the entity has met the

challenges posed by IFRS 17, CECL and IFRS

9 in a flexible centralized and high-

performance analytics environment.

Orchestrate all the relevant aspects of

credit loss and financial stress test

reserving processes and perform

consolidation of results related to various

systems through a centralized hub.

It is evident that the entity have shown an

efficient ways of determining and estimating

the credit losses with precision.

Areas for development

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

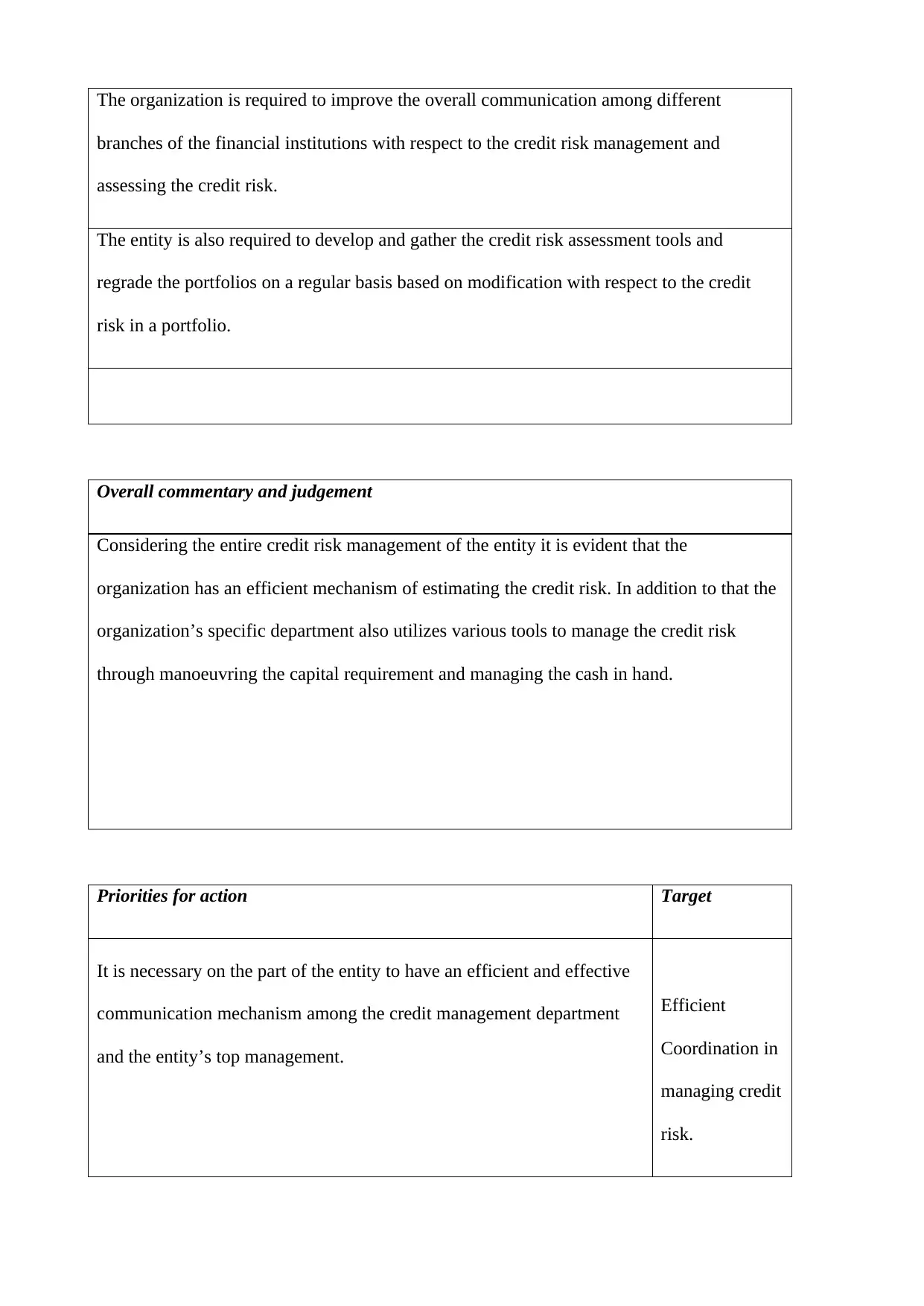

The organization is required to improve the overall communication among different

branches of the financial institutions with respect to the credit risk management and

assessing the credit risk.

The entity is also required to develop and gather the credit risk assessment tools and

regrade the portfolios on a regular basis based on modification with respect to the credit

risk in a portfolio.

Overall commentary and judgement

Considering the entire credit risk management of the entity it is evident that the

organization has an efficient mechanism of estimating the credit risk. In addition to that the

organization’s specific department also utilizes various tools to manage the credit risk

through manoeuvring the capital requirement and managing the cash in hand.

Priorities for action Target

It is necessary on the part of the entity to have an efficient and effective

communication mechanism among the credit management department

and the entity’s top management.

Efficient

Coordination in

managing credit

risk.

branches of the financial institutions with respect to the credit risk management and

assessing the credit risk.

The entity is also required to develop and gather the credit risk assessment tools and

regrade the portfolios on a regular basis based on modification with respect to the credit

risk in a portfolio.

Overall commentary and judgement

Considering the entire credit risk management of the entity it is evident that the

organization has an efficient mechanism of estimating the credit risk. In addition to that the

organization’s specific department also utilizes various tools to manage the credit risk

through manoeuvring the capital requirement and managing the cash in hand.

Priorities for action Target

It is necessary on the part of the entity to have an efficient and effective

communication mechanism among the credit management department

and the entity’s top management.

Efficient

Coordination in

managing credit

risk.

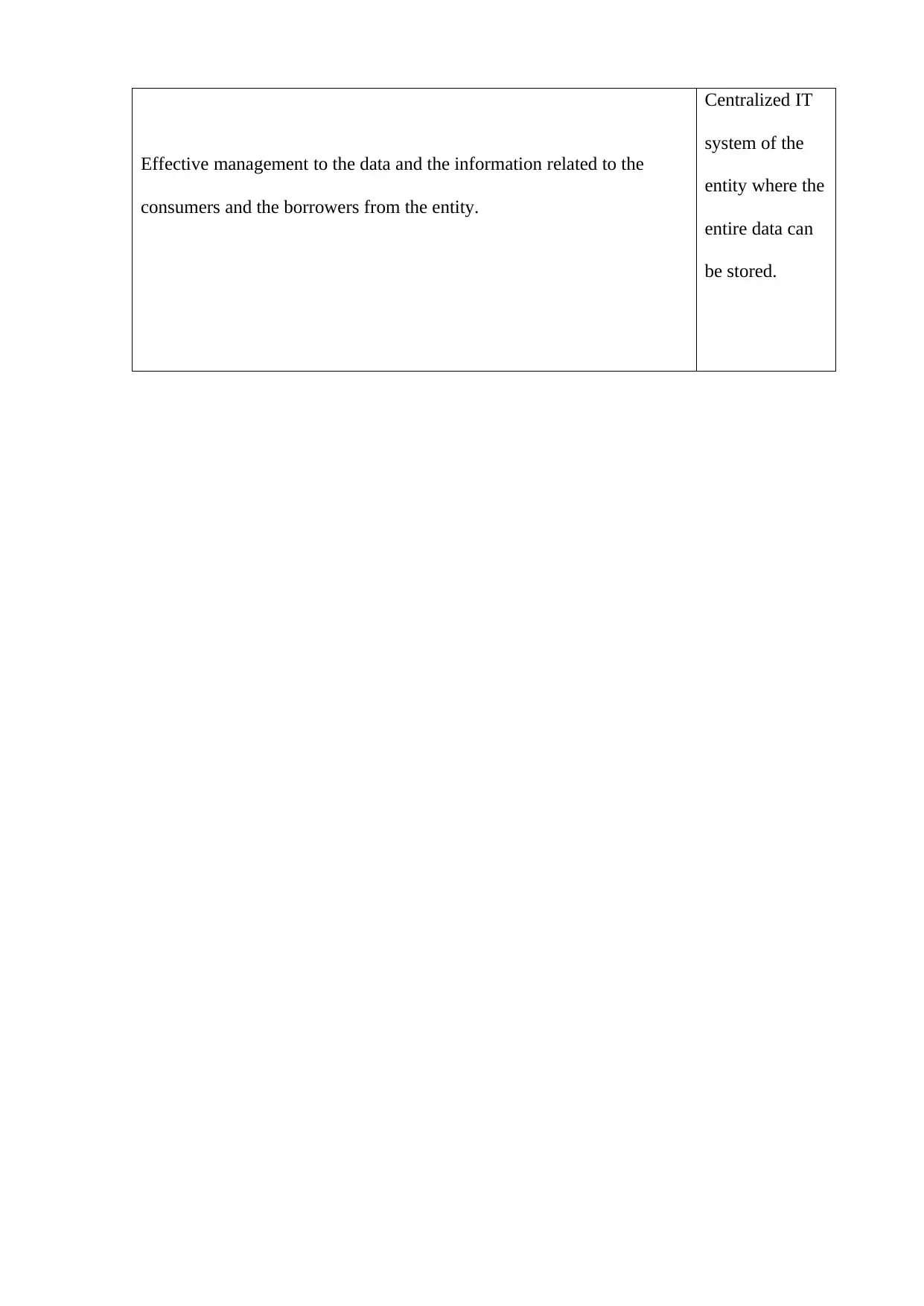

Effective management to the data and the information related to the

consumers and the borrowers from the entity.

Centralized IT

system of the

entity where the

entire data can

be stored.

consumers and the borrowers from the entity.

Centralized IT

system of the

entity where the

entire data can

be stored.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.