To investigate the impact of credit risk management on Bank of Cyprus

VerifiedAdded on 2020/06/06

|20

|6008

|248

Report

AI Summary

This report provides a comprehensive literature review on the impact of credit risk management on the profitability and financial performance of the Bank of Cyprus. It begins by defining credit risk, its consequences, and the importance of effective credit risk management. The report examines relevant regulations, including the Basel Accords (Basel I, II, and III), and their role in managing credit risk. It explores various methods for measuring credit risk and assessing a bank's profitability, including the Dupont Model. The study analyzes the Bank of Cyprus's credit risk management practices, considering factors such as non-performing loans and the impact of lending decisions. The literature review synthesizes existing research, identifies gaps in previous studies, and offers a critical evaluation of the existing knowledge on the topic. The report provides a detailed examination of the key determinants that influence the Bank's financial status and profitability performance, supported by empirical evidence from secondary sources. It focuses on the importance of credit risk management for banks' long-term success and the consequences of inadequate risk management, including liquidity issues and reputational damage. The report also examines the three key pillars of Basel II (minimum capital requirements, supervisory review, and market discipline) and their implications for credit risk management.

FINANCIAL RISK

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

LITERATURE REVIEW................................................................................................................1

2.1 Overview of credit risk..........................................................................................................1

2.2 Concept of credit risk management and consequences of inadequate credit risk

management.................................................................................................................................3

2.3 Relevant regulations: Basel Accords.....................................................................................4

2.3.1 Basel I: Basel Capital Accord.........................................................................................4

2.3.2 Basel II: New Capital Accord.........................................................................................4

2.3.3 Basel III...........................................................................................................................7

2.4 Measurement of Credit risk management and its suitability..................................................7

2.5 Measurement of bank’s profitability and key determinants...................................................9

2.6 Review of empirical literature/previous studies...................................................................13

REFERENCES..............................................................................................................................14

LITERATURE REVIEW................................................................................................................1

2.1 Overview of credit risk..........................................................................................................1

2.2 Concept of credit risk management and consequences of inadequate credit risk

management.................................................................................................................................3

2.3 Relevant regulations: Basel Accords.....................................................................................4

2.3.1 Basel I: Basel Capital Accord.........................................................................................4

2.3.2 Basel II: New Capital Accord.........................................................................................4

2.3.3 Basel III...........................................................................................................................7

2.4 Measurement of Credit risk management and its suitability..................................................7

2.5 Measurement of bank’s profitability and key determinants...................................................9

2.6 Review of empirical literature/previous studies...................................................................13

REFERENCES..............................................................................................................................14

Index of Figures

Figure 1 Three key Pillar Approach of Base II................................................................................5

Figure 2 Calculation of Capital ratio under Basel II........................................................................5

Figure 3 Dupont Model for Bank’s profitability measurement.....................................................10

Figure 1 Three key Pillar Approach of Base II................................................................................5

Figure 2 Calculation of Capital ratio under Basel II........................................................................5

Figure 3 Dupont Model for Bank’s profitability measurement.....................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Title: “To investigate the impact of credit risk management on the profitability and financial

performance; A case study of Bank of Cyprus”

LITERATURE REVIEW

Literature review is a process wherein scholar critically evaluates the existing knowledge,

methodological and theoretical contribution & substantive findings regarding the research topic.

In this regards, researchers uses only the secondary material sources without conducting any

original investigation or experimental work in the chosen field. Literature review is a process

wherein scholar critically evaluates the existing knowledge, methodological and theoretical

contribution & substantive findings regarding the research topic. In this regards, researchers uses

only the secondary material sources without conducting any original investigation or

experimental work in the chosen field. It is important for the investigator to select the best

articles that was published in the past period on a similar topic so as to critically evaluate &

compare all the information to develop own idea or concept towards the subject. It will helps to

identify loopholes and gaps in the previous studies so as to make it sure that the current study

will not replicate the historical researches and conduct the study in new area by mitigate the

earlier gaps. With the help of this, scholar will be able to examine the concept of credit risk, its

consequences and its management process used by Bank of Cyprus in a thoroughly,

comprehensive & informative manner. In this, scholar will pay special attention to collect

information from the realistic and valid secondary sources by gathering sufficient quantum of

data from the recent published articles and also the proper references will be made to provide

adequate evidences. Moreover, various key legislations and policies applicable on the bank will

be examined and key determinates which influence Bank’s financial status and profitability

performance will be examined analytically.

2.1 Overview of credit risk

Credit is the key source of revenue for the banks all over the world, however, in the

current time; probability of borrower’s default in loan payments becomes an increasing area of

concern for the commercial banks, more importantly, for the unsecured loans, and such risk of

payment default is termed as credit risk. It has a significant effect not only on the bank’s

performance but also to the entire economy. It is because; banking sector plays a vital role in the

1

performance; A case study of Bank of Cyprus”

LITERATURE REVIEW

Literature review is a process wherein scholar critically evaluates the existing knowledge,

methodological and theoretical contribution & substantive findings regarding the research topic.

In this regards, researchers uses only the secondary material sources without conducting any

original investigation or experimental work in the chosen field. Literature review is a process

wherein scholar critically evaluates the existing knowledge, methodological and theoretical

contribution & substantive findings regarding the research topic. In this regards, researchers uses

only the secondary material sources without conducting any original investigation or

experimental work in the chosen field. It is important for the investigator to select the best

articles that was published in the past period on a similar topic so as to critically evaluate &

compare all the information to develop own idea or concept towards the subject. It will helps to

identify loopholes and gaps in the previous studies so as to make it sure that the current study

will not replicate the historical researches and conduct the study in new area by mitigate the

earlier gaps. With the help of this, scholar will be able to examine the concept of credit risk, its

consequences and its management process used by Bank of Cyprus in a thoroughly,

comprehensive & informative manner. In this, scholar will pay special attention to collect

information from the realistic and valid secondary sources by gathering sufficient quantum of

data from the recent published articles and also the proper references will be made to provide

adequate evidences. Moreover, various key legislations and policies applicable on the bank will

be examined and key determinates which influence Bank’s financial status and profitability

performance will be examined analytically.

2.1 Overview of credit risk

Credit is the key source of revenue for the banks all over the world, however, in the

current time; probability of borrower’s default in loan payments becomes an increasing area of

concern for the commercial banks, more importantly, for the unsecured loans, and such risk of

payment default is termed as credit risk. It has a significant effect not only on the bank’s

performance but also to the entire economy. It is because; banking sector plays a vital role in the

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

economic growth and progress as they control credit supply through change in interest rate,

open-market operations and other activities.

García (2017), stated that the main function of the bank is to grant credit and receive

different kind of deposits such as term deposits and demand deposits from the consumers. When

a bank provides credit to the borrower with the expectation of receiving the principal amount

together with interest is categorized as performing assets. However, in contrast, many-times,

borrower fails to meet out their credit liabilities as per agreed loan repayment schedule and do

not pay installments along with the interest on time, then it is regarded as Non-Performing Loans

(NPL) due to credit default of the borrower. Likewise, Akdoğu and Alp (2016), defines credit

risk as a failure of borrower to make timely payments of principal capital and interest as well and

bank categorized such loans as a doubtful credit. It poses a significant impact on the bank’s cash

flow and liquidity position and tends to increase collection cost of their lending. Aprilia and

et.al., (2016), presented that credit risk is regarded as the current or prospective risk to capital

and earnings arising from the failure of obligator to meet out their contractual commitments

agreed with the bank.

However, on the contrary side, as per the views of Morris and Shin (2016), credit risk can

be regarded as the degree or extent of fluctuations in value of debt instrument & financial

instrument derivatives due to poor credit quality of the borrower. In despite of this, Schwaab,

Koopman and Lucas, (2017), stated that loss that bank suffers due to the refusal or timely

payment inability of the borrower for the capital what he or she had taken from the bank is

termed as credit risk. In contrast, Almazari (2012), criticized it by arguing that credit risk

indicates the probable variation in the net income of the bank as a cause of delayed payment or

non-payment of the loan facilities granted to a party. Thus, the possibility of the default, as per

which, borrower may fail to meet his or her loan obligations in accordance with the decided

credit terms and schedule of loan repayment is called credit risk. It greatly influence the bank’s

success, therefore, it is necessary for them to effectively and efficiently manage such risk. It is a

critical component of Bank’s risk management approaches which will leads to achieve long-run

success.

2

open-market operations and other activities.

García (2017), stated that the main function of the bank is to grant credit and receive

different kind of deposits such as term deposits and demand deposits from the consumers. When

a bank provides credit to the borrower with the expectation of receiving the principal amount

together with interest is categorized as performing assets. However, in contrast, many-times,

borrower fails to meet out their credit liabilities as per agreed loan repayment schedule and do

not pay installments along with the interest on time, then it is regarded as Non-Performing Loans

(NPL) due to credit default of the borrower. Likewise, Akdoğu and Alp (2016), defines credit

risk as a failure of borrower to make timely payments of principal capital and interest as well and

bank categorized such loans as a doubtful credit. It poses a significant impact on the bank’s cash

flow and liquidity position and tends to increase collection cost of their lending. Aprilia and

et.al., (2016), presented that credit risk is regarded as the current or prospective risk to capital

and earnings arising from the failure of obligator to meet out their contractual commitments

agreed with the bank.

However, on the contrary side, as per the views of Morris and Shin (2016), credit risk can

be regarded as the degree or extent of fluctuations in value of debt instrument & financial

instrument derivatives due to poor credit quality of the borrower. In despite of this, Schwaab,

Koopman and Lucas, (2017), stated that loss that bank suffers due to the refusal or timely

payment inability of the borrower for the capital what he or she had taken from the bank is

termed as credit risk. In contrast, Almazari (2012), criticized it by arguing that credit risk

indicates the probable variation in the net income of the bank as a cause of delayed payment or

non-payment of the loan facilities granted to a party. Thus, the possibility of the default, as per

which, borrower may fail to meet his or her loan obligations in accordance with the decided

credit terms and schedule of loan repayment is called credit risk. It greatly influence the bank’s

success, therefore, it is necessary for them to effectively and efficiently manage such risk. It is a

critical component of Bank’s risk management approaches which will leads to achieve long-run

success.

2

2.2 Concept of credit risk management and consequences of inadequate credit risk management

Aprilia and et.al., (2016), encountered multiple of reasons responsible for credit risk such

as poor & ineffective credit policies, inappropriate legislations, improper liquidity management,

volatility in interest rates, poor lending decisions, lack of adequate supervision and others.

Increase in the credit default of the borrower can bring banks into serious liquidity and solvency

issues; therefore, proper credit risk management is necessary for the bank survival and growth.

As per the views of Akdoğu and Alp (2016), credit risk management is really important for the

commercial banks to allocate their business resources to different risk units considering the

tradeoff between return potential and risk. Bank endeavored to create excellent credit risk

management framework to minimize the possibility of borrower’s credit default. Many banks

also have started considering global credit models so as to design a perfect capital adequacy

standard so as to manage their risk. Similarly, Lee, Naranjo and Sirmans (2016), demonstrated

that credit risk management comes at the heart of the banking sector. It is because, during the

period of crisis, most of the bank liquidated just due to poor credit quality. Thus, its proper

management is considered to be a central point of the lending portfolio. It is the most significant

risk that is confronted by the banks and the success depends upon proper and productive

management of the borrower default risk to a noteworthy extent. Banks gives due importance to

the credit risk in their management approaches wherein they create plans and policies by

compliance with the applicable legislative framework and banking rules and regulations.

In the study of Friewald, Wagner and Zechner (2014), it has been investigated that Global

financial crisis put credit risk management approaches to the top of banking regulatory

framework to maximize transparency. Management of such risk comprises three main elements

that are origination, debt or credit management and sound management of collection & recovery

as well. The key goal of it is to maximize risk’s adjusted rate of return through appropriate

management of credit risk exposure as per the decided parameters. There is a common

misconception that failure in timely debt payments onlyu caused downside impact to the debtors.

However, the findings of Ndungo, Tobias and Florence, (2017), reported that there are serious

consequences of poor credit risk management on the banks also. Inability of the borrower to pay

the debts principal together with the interest either due to insolvency or bankruptcy leads to loss

of capital for the bank that has been granted as a loan to the debtor. Bad credit management also

influence credibility adversely and create negative image. As a result, bank suffers reputational

3

Aprilia and et.al., (2016), encountered multiple of reasons responsible for credit risk such

as poor & ineffective credit policies, inappropriate legislations, improper liquidity management,

volatility in interest rates, poor lending decisions, lack of adequate supervision and others.

Increase in the credit default of the borrower can bring banks into serious liquidity and solvency

issues; therefore, proper credit risk management is necessary for the bank survival and growth.

As per the views of Akdoğu and Alp (2016), credit risk management is really important for the

commercial banks to allocate their business resources to different risk units considering the

tradeoff between return potential and risk. Bank endeavored to create excellent credit risk

management framework to minimize the possibility of borrower’s credit default. Many banks

also have started considering global credit models so as to design a perfect capital adequacy

standard so as to manage their risk. Similarly, Lee, Naranjo and Sirmans (2016), demonstrated

that credit risk management comes at the heart of the banking sector. It is because, during the

period of crisis, most of the bank liquidated just due to poor credit quality. Thus, its proper

management is considered to be a central point of the lending portfolio. It is the most significant

risk that is confronted by the banks and the success depends upon proper and productive

management of the borrower default risk to a noteworthy extent. Banks gives due importance to

the credit risk in their management approaches wherein they create plans and policies by

compliance with the applicable legislative framework and banking rules and regulations.

In the study of Friewald, Wagner and Zechner (2014), it has been investigated that Global

financial crisis put credit risk management approaches to the top of banking regulatory

framework to maximize transparency. Management of such risk comprises three main elements

that are origination, debt or credit management and sound management of collection & recovery

as well. The key goal of it is to maximize risk’s adjusted rate of return through appropriate

management of credit risk exposure as per the decided parameters. There is a common

misconception that failure in timely debt payments onlyu caused downside impact to the debtors.

However, the findings of Ndungo, Tobias and Florence, (2017), reported that there are serious

consequences of poor credit risk management on the banks also. Inability of the borrower to pay

the debts principal together with the interest either due to insolvency or bankruptcy leads to loss

of capital for the bank that has been granted as a loan to the debtor. Bad credit management also

influence credibility adversely and create negative image. As a result, bank suffers reputational

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

issues. Granting excessive credit without effectively examining the creditability of the borrower

may cause serious liquidity crunch.

2.3 Relevant regulations: Basel Accords

Banking industry is highly regulated industry with several legislations and banking rules

and regulations.

2.3.1 Basel I: Basel Capital Accord

Basel I has been issued on December 1987 with the two fundamental objectives one is to

promote financial stability of the banking system and another one is to ensure fairness in the

banking sector. The Capital accord requires a standard capital ratio of 8% that is mandatory for

all the banks to be maintained by the end of year 1992. This accord divides capital into two tier,

Tier 1 and Tier 2. Out of these, Tier 1 is applied by all the banks all over the world equally

whereas later is tailored considering domestic banking system. However, for the risk-weighted

assets, assets are weighted considering the level of risk whereas every off-balance sheet item is

`calculated taking into account the equivalent amount of assets.

However, on the other side, the accord has been criticized due to its simplicity and

arbitrary. The most important aspect for which the accord was criticized that it considers only 4

risk weights for distinctive categories of assets and assigns same level of risk to all the loans

regardless their differences in credit quality.

2.3.2 Basel II: New Capital Accord

Over the period, various financial instruments i.e. credit derivatives and others enable

banks to overcome risk from their daily trading functions. Moreover, with the broader operations

of banks at a global level makes it necessary to revised the Basel I framework for the adequate

capital requirement. Henceforth, in 2004, a new framework Basel II was issued on three key

pillars; minimum capital requirement, supervisory review and market discipline.

4

may cause serious liquidity crunch.

2.3 Relevant regulations: Basel Accords

Banking industry is highly regulated industry with several legislations and banking rules

and regulations.

2.3.1 Basel I: Basel Capital Accord

Basel I has been issued on December 1987 with the two fundamental objectives one is to

promote financial stability of the banking system and another one is to ensure fairness in the

banking sector. The Capital accord requires a standard capital ratio of 8% that is mandatory for

all the banks to be maintained by the end of year 1992. This accord divides capital into two tier,

Tier 1 and Tier 2. Out of these, Tier 1 is applied by all the banks all over the world equally

whereas later is tailored considering domestic banking system. However, for the risk-weighted

assets, assets are weighted considering the level of risk whereas every off-balance sheet item is

`calculated taking into account the equivalent amount of assets.

However, on the other side, the accord has been criticized due to its simplicity and

arbitrary. The most important aspect for which the accord was criticized that it considers only 4

risk weights for distinctive categories of assets and assigns same level of risk to all the loans

regardless their differences in credit quality.

2.3.2 Basel II: New Capital Accord

Over the period, various financial instruments i.e. credit derivatives and others enable

banks to overcome risk from their daily trading functions. Moreover, with the broader operations

of banks at a global level makes it necessary to revised the Basel I framework for the adequate

capital requirement. Henceforth, in 2004, a new framework Basel II was issued on three key

pillars; minimum capital requirement, supervisory review and market discipline.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

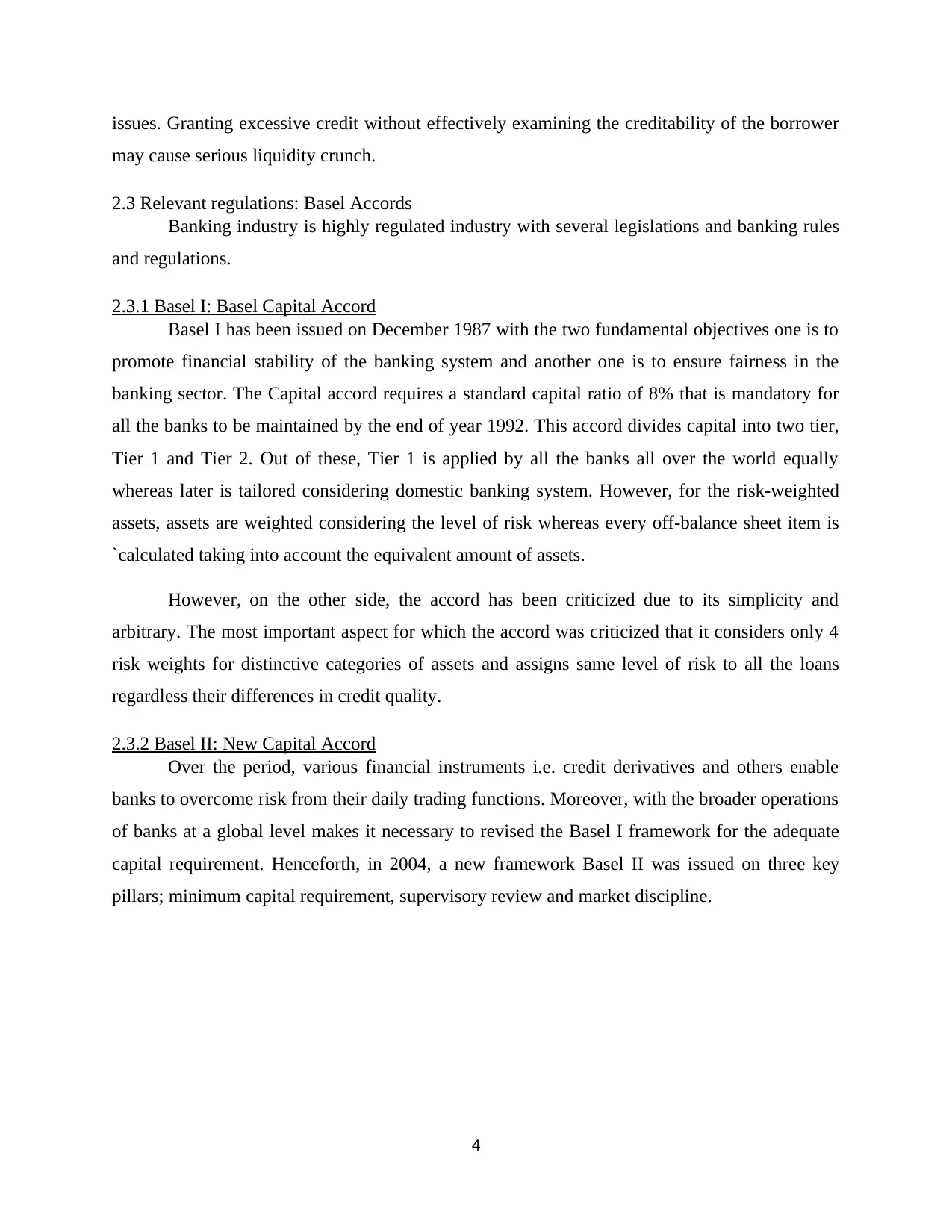

Figure 1 Three key Pillar Approach of Base II

(Source: Abusharba and et.al., 2013)

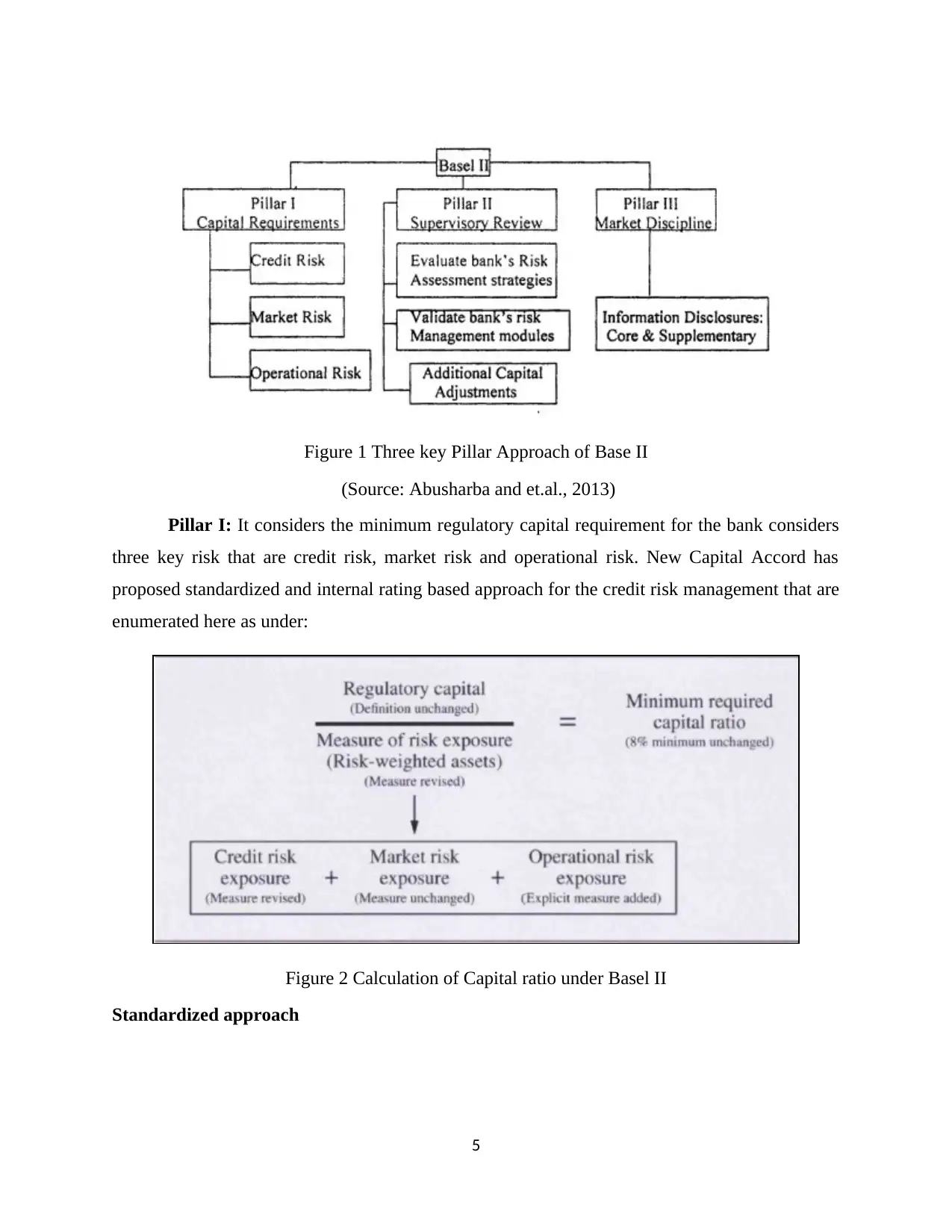

Pillar I: It considers the minimum regulatory capital requirement for the bank considers

three key risk that are credit risk, market risk and operational risk. New Capital Accord has

proposed standardized and internal rating based approach for the credit risk management that are

enumerated here as under:

Figure 2 Calculation of Capital ratio under Basel II

Standardized approach

5

(Source: Abusharba and et.al., 2013)

Pillar I: It considers the minimum regulatory capital requirement for the bank considers

three key risk that are credit risk, market risk and operational risk. New Capital Accord has

proposed standardized and internal rating based approach for the credit risk management that are

enumerated here as under:

Figure 2 Calculation of Capital ratio under Basel II

Standardized approach

5

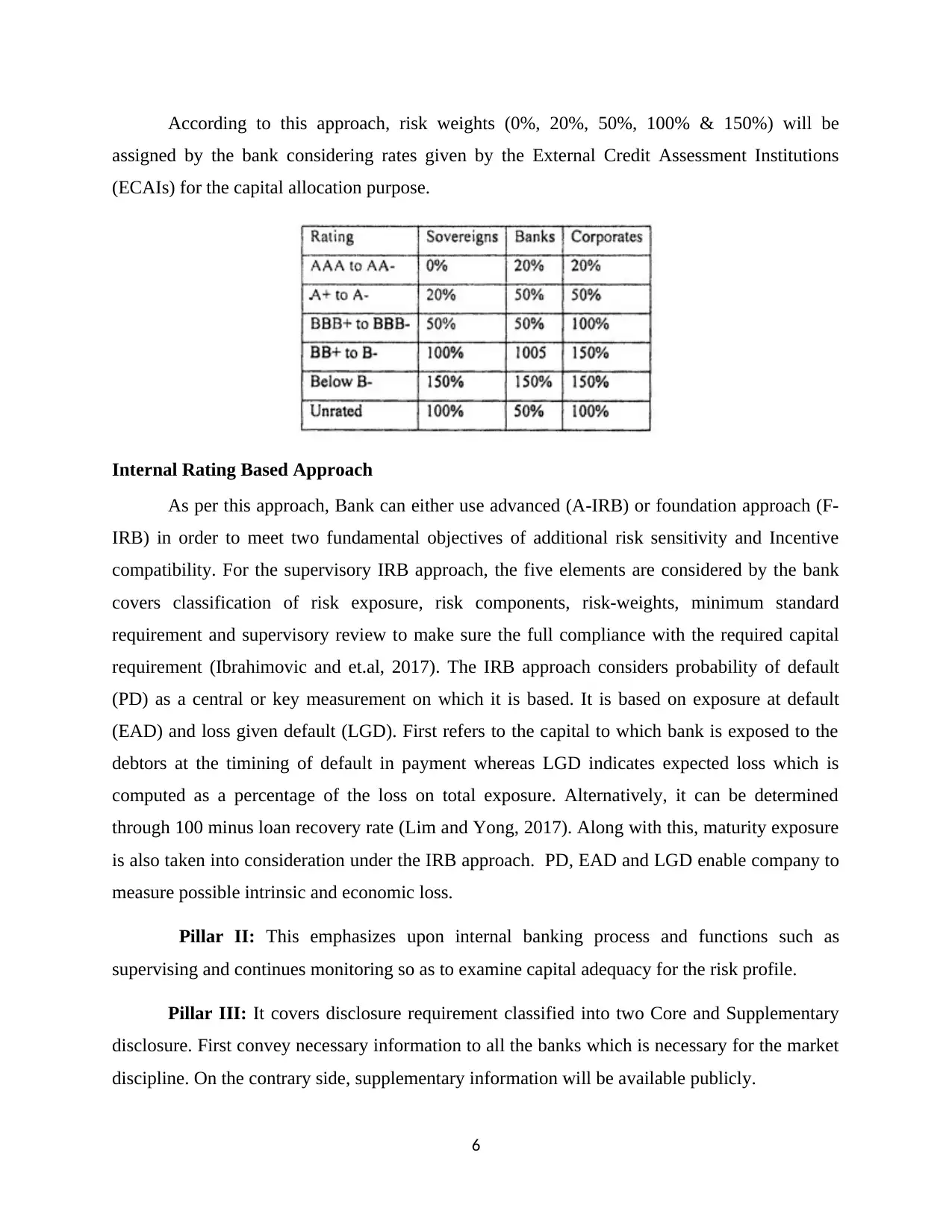

According to this approach, risk weights (0%, 20%, 50%, 100% & 150%) will be

assigned by the bank considering rates given by the External Credit Assessment Institutions

(ECAIs) for the capital allocation purpose.

Internal Rating Based Approach

As per this approach, Bank can either use advanced (A-IRB) or foundation approach (F-

IRB) in order to meet two fundamental objectives of additional risk sensitivity and Incentive

compatibility. For the supervisory IRB approach, the five elements are considered by the bank

covers classification of risk exposure, risk components, risk-weights, minimum standard

requirement and supervisory review to make sure the full compliance with the required capital

requirement (Ibrahimovic and et.al, 2017). The IRB approach considers probability of default

(PD) as a central or key measurement on which it is based. It is based on exposure at default

(EAD) and loss given default (LGD). First refers to the capital to which bank is exposed to the

debtors at the timining of default in payment whereas LGD indicates expected loss which is

computed as a percentage of the loss on total exposure. Alternatively, it can be determined

through 100 minus loan recovery rate (Lim and Yong, 2017). Along with this, maturity exposure

is also taken into consideration under the IRB approach. PD, EAD and LGD enable company to

measure possible intrinsic and economic loss.

Pillar II: This emphasizes upon internal banking process and functions such as

supervising and continues monitoring so as to examine capital adequacy for the risk profile.

Pillar III: It covers disclosure requirement classified into two Core and Supplementary

disclosure. First convey necessary information to all the banks which is necessary for the market

discipline. On the contrary side, supplementary information will be available publicly.

6

assigned by the bank considering rates given by the External Credit Assessment Institutions

(ECAIs) for the capital allocation purpose.

Internal Rating Based Approach

As per this approach, Bank can either use advanced (A-IRB) or foundation approach (F-

IRB) in order to meet two fundamental objectives of additional risk sensitivity and Incentive

compatibility. For the supervisory IRB approach, the five elements are considered by the bank

covers classification of risk exposure, risk components, risk-weights, minimum standard

requirement and supervisory review to make sure the full compliance with the required capital

requirement (Ibrahimovic and et.al, 2017). The IRB approach considers probability of default

(PD) as a central or key measurement on which it is based. It is based on exposure at default

(EAD) and loss given default (LGD). First refers to the capital to which bank is exposed to the

debtors at the timining of default in payment whereas LGD indicates expected loss which is

computed as a percentage of the loss on total exposure. Alternatively, it can be determined

through 100 minus loan recovery rate (Lim and Yong, 2017). Along with this, maturity exposure

is also taken into consideration under the IRB approach. PD, EAD and LGD enable company to

measure possible intrinsic and economic loss.

Pillar II: This emphasizes upon internal banking process and functions such as

supervising and continues monitoring so as to examine capital adequacy for the risk profile.

Pillar III: It covers disclosure requirement classified into two Core and Supplementary

disclosure. First convey necessary information to all the banks which is necessary for the market

discipline. On the contrary side, supplementary information will be available publicly.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.3.3 Basel III

Financial crisis during the period of 2007 has discovered moral hazards & many

forbearance in the banking regulation. It is because; during crisis number of commercial banks

goes into liquidation due to poor credit supply decisions at high level of credit risk. As a result, a

new accord Basel III was issued with strict regulatory requirement and newer legislations. it

impose new criteria and tighter capital ratio so as to make it more accurate and prudent. It

covers 6 key parts capital requirement, capital buffer, counter-cyclical buffer, and leverage,

liquidity and counterparty credit default risk as well (Burchi and Martelli, 2016). Basel III had

introduced two standards for effective and sound management of liquidity position so that bank

can survive successfully. The two ratios are Liquidity Coverage Ratio (LCR) & Net Stable

Funding Ratio (NSFL) as a major step. In addition to these, the new regulative framework also

includes CVA which measures expected or possible loss due to the counterpart credit default.

2.4 Measurement of Credit risk management and its suitability

In accordance with the view of Shehzad, De Haan and Scholtens (2010), credit risk can

be measured through Capital Adequacy Ratio (CAR) that is expressed as a percentage of its risk

weighted credit exposure, also termed as CRAR (Capital to risk weighted ratio). Financial

analyst uses it to promote the stability of the financial system. It can be measured through using

following formula:

CAR: Tier I capital + Tier 2 capital/Risk weighted assets

Tier I capital indicates capital that can absorb incurred losses without the need of ceasing

trading functions. However, Tier II capital can only be used to absorb losses in the event of

liquidation or wind up of business hence, provides less level of protection to the depositors. It is

necessary for the banks to maintain the minimum CAR so as to assure that it will have enough

capital to absorb reasonable business losses and minimize the possibility of insolvency.

Likewise Schwaab, Koopman and Lucas (2017), studied that credit risk is not only the

most fundamental and critical importance for the bank’s success but also commercial banks are

actively engaged in order to control it. CAR is the considered as the most suitable ratio for

measuring the credit risk managerial efficiency of bank because the ratio helps to ensure that

bank can absorb reasonable losses to overcome the possibility of going into liquidation or

insolvent. In the international settlement for the banking industry, Basel committee also shown

7

Financial crisis during the period of 2007 has discovered moral hazards & many

forbearance in the banking regulation. It is because; during crisis number of commercial banks

goes into liquidation due to poor credit supply decisions at high level of credit risk. As a result, a

new accord Basel III was issued with strict regulatory requirement and newer legislations. it

impose new criteria and tighter capital ratio so as to make it more accurate and prudent. It

covers 6 key parts capital requirement, capital buffer, counter-cyclical buffer, and leverage,

liquidity and counterparty credit default risk as well (Burchi and Martelli, 2016). Basel III had

introduced two standards for effective and sound management of liquidity position so that bank

can survive successfully. The two ratios are Liquidity Coverage Ratio (LCR) & Net Stable

Funding Ratio (NSFL) as a major step. In addition to these, the new regulative framework also

includes CVA which measures expected or possible loss due to the counterpart credit default.

2.4 Measurement of Credit risk management and its suitability

In accordance with the view of Shehzad, De Haan and Scholtens (2010), credit risk can

be measured through Capital Adequacy Ratio (CAR) that is expressed as a percentage of its risk

weighted credit exposure, also termed as CRAR (Capital to risk weighted ratio). Financial

analyst uses it to promote the stability of the financial system. It can be measured through using

following formula:

CAR: Tier I capital + Tier 2 capital/Risk weighted assets

Tier I capital indicates capital that can absorb incurred losses without the need of ceasing

trading functions. However, Tier II capital can only be used to absorb losses in the event of

liquidation or wind up of business hence, provides less level of protection to the depositors. It is

necessary for the banks to maintain the minimum CAR so as to assure that it will have enough

capital to absorb reasonable business losses and minimize the possibility of insolvency.

Likewise Schwaab, Koopman and Lucas (2017), studied that credit risk is not only the

most fundamental and critical importance for the bank’s success but also commercial banks are

actively engaged in order to control it. CAR is the considered as the most suitable ratio for

measuring the credit risk managerial efficiency of bank because the ratio helps to ensure that

bank can absorb reasonable losses to overcome the possibility of going into liquidation or

insolvent. In the international settlement for the banking industry, Basel committee also shown

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interest in the area of CAR and issued a statement recommending all the banks to maintain a

minimum CAR to make sure proper capital or liquidity available for meeting out their

commitments. According to the accord, minimum CAR for Tier I should not be less than 4%

whereas total capital (Tier I + Tier II) to the risk-weighted exposure must be equal to or above

8%. For the Tier II capital, there are several regulatory standards such as it cannot exceed 100%

of tier I capital, lower tier II capital cann’t go beyond 50% of tier I and it will be amortized over

the period of 5 years using straight line basis.

Tier I capital includes equity share capital, audited retained profits, CY’s loss, potential

year’s tax advantages and intangible assets like goodwill etc. However, Tier II capital is

classified into two, upper and lower. First covers unaudited retained profits, revaluation reserve,

bad debt provisions, perpetual subordinated debt & cumulative preference shares. However, later

consists of subordinated debts that have a maturity time of minimum 5 years and redeemable

preference share which cannot be redeemed by bank within a time duration of 5 year. Total of all

less deductions in respect of equity investment in subsidiary companies, more than 10%

shareholding in other banks & unrealized loss of revaluation on holdings is taken as total capital.

However, in the study of Xuebin (2012), besides Tier I and Tier II capital, the committee

also had suggested Tier III capital. It comprises short-term subordinated debts that banks can use

so as to adjust losses that are the results of market risk. However, it only can be used by the

banksif tier I and tier II capital is not sufficiency for loss recovery. In such regards, market risk

covers unexpected losses due to change in foreign exchange risk and interest rates. Higher the

CAR reflects greater availability of capital indicates that bank is able to recover high value of

unexpected loss before it can go into liquidation.

On the critical note, Arora and Arora (2017), commented that Non-Performing Loans

Ratio (NPLR) is comparatively a more suitable ratio of credit risk measurement. NPL measures

the total capital on which borrower did not make timely payments of his or her loan

commitments or obligations as per the set schedule. It may be either default or expected to going

into default in the near future. In case, when debtors started making payments for the loan then,

NPL will become reperforming loan even if borrower still did not make payment of all the

missed debt installments.

NPLR – Non-performing Loans/Total Loans

8

minimum CAR to make sure proper capital or liquidity available for meeting out their

commitments. According to the accord, minimum CAR for Tier I should not be less than 4%

whereas total capital (Tier I + Tier II) to the risk-weighted exposure must be equal to or above

8%. For the Tier II capital, there are several regulatory standards such as it cannot exceed 100%

of tier I capital, lower tier II capital cann’t go beyond 50% of tier I and it will be amortized over

the period of 5 years using straight line basis.

Tier I capital includes equity share capital, audited retained profits, CY’s loss, potential

year’s tax advantages and intangible assets like goodwill etc. However, Tier II capital is

classified into two, upper and lower. First covers unaudited retained profits, revaluation reserve,

bad debt provisions, perpetual subordinated debt & cumulative preference shares. However, later

consists of subordinated debts that have a maturity time of minimum 5 years and redeemable

preference share which cannot be redeemed by bank within a time duration of 5 year. Total of all

less deductions in respect of equity investment in subsidiary companies, more than 10%

shareholding in other banks & unrealized loss of revaluation on holdings is taken as total capital.

However, in the study of Xuebin (2012), besides Tier I and Tier II capital, the committee

also had suggested Tier III capital. It comprises short-term subordinated debts that banks can use

so as to adjust losses that are the results of market risk. However, it only can be used by the

banksif tier I and tier II capital is not sufficiency for loss recovery. In such regards, market risk

covers unexpected losses due to change in foreign exchange risk and interest rates. Higher the

CAR reflects greater availability of capital indicates that bank is able to recover high value of

unexpected loss before it can go into liquidation.

On the critical note, Arora and Arora (2017), commented that Non-Performing Loans

Ratio (NPLR) is comparatively a more suitable ratio of credit risk measurement. NPL measures

the total capital on which borrower did not make timely payments of his or her loan

commitments or obligations as per the set schedule. It may be either default or expected to going

into default in the near future. In case, when debtors started making payments for the loan then,

NPL will become reperforming loan even if borrower still did not make payment of all the

missed debt installments.

NPLR – Non-performing Loans/Total Loans

8

Likewise, Akdoğu and Alp (2016), studied that NPLR is a perfect ratio that can be used

by the analysts to examine the credit risk management efficiency of the bank because higher the

credit default risk of the borrower results in maximizing the NPL and as a result, NPLR will be

increase. However, with the sound credit risk management approach, commercial banks will be

able to reduce the probability of default in payment by the borrowers through strict credit

standards, policies and loan granting decisions, which in turn, it will be able to ensure that on all

the loans, borrower will make timely payments of periodical installments together with interest at

minimal of NPLR. Referring Chinese banking sector, NPL ratio was reported to 1.99% in May

declined by 0.16% in last year reported banking regulatory commission that commercial banks

needs to strengthen their interest rate and liquidity so as to manage credit risk effectively.

In contrast to this, Witzany (2017), founded CAR as a significant economic indicator

because it helps to minimize the probability of default loans because high CAR simply means

less credit exposure. The study founded a positive relationship between bank’s profitability and

CAR in Europe. Liesz and Maranville (2010), argued that NPLR is comparatively a better

indicator of credit risk management as the study presented that high possibility of riskier loans

maximizes the probability of high default, which in turn, results in high NPLR. Besides this,

Borio, Gambacorta and Hofmann, (2017), suggested that NPL to total assets is a better indicator

for assessing credit risk management effectiveness of banks. It is because; this indicator also

considers the regulatory supervision with the subject to the credit risk exposure in banking

sector. Research also examined the impact of NPLR on the ROA and the results demonstrated

that less NPLR leads to maximize ROA or vice-versa.

2.5 Measurement of bank’s profitability and key determinants

According to the views of Xuebin, (2012), profitability is the key indicator of bank’s

capability to take risk or maximize capital. It also indicates the competitiveness of the bank and

serves as a measurement tool of its quality of management. The commercial bank’s profitability

can be measured in two sense; internal determinants which are under the control of internal

management and external determinants which is outside the control of managers. Internal

determinants emphasize upon the managing policy, financial management, liquidity management

and efficiency and effectiveness of risk management and can be measured using financial

statements of the banks. It is of great significance in order to assess and evaluate the credit risk

9

by the analysts to examine the credit risk management efficiency of the bank because higher the

credit default risk of the borrower results in maximizing the NPL and as a result, NPLR will be

increase. However, with the sound credit risk management approach, commercial banks will be

able to reduce the probability of default in payment by the borrowers through strict credit

standards, policies and loan granting decisions, which in turn, it will be able to ensure that on all

the loans, borrower will make timely payments of periodical installments together with interest at

minimal of NPLR. Referring Chinese banking sector, NPL ratio was reported to 1.99% in May

declined by 0.16% in last year reported banking regulatory commission that commercial banks

needs to strengthen their interest rate and liquidity so as to manage credit risk effectively.

In contrast to this, Witzany (2017), founded CAR as a significant economic indicator

because it helps to minimize the probability of default loans because high CAR simply means

less credit exposure. The study founded a positive relationship between bank’s profitability and

CAR in Europe. Liesz and Maranville (2010), argued that NPLR is comparatively a better

indicator of credit risk management as the study presented that high possibility of riskier loans

maximizes the probability of high default, which in turn, results in high NPLR. Besides this,

Borio, Gambacorta and Hofmann, (2017), suggested that NPL to total assets is a better indicator

for assessing credit risk management effectiveness of banks. It is because; this indicator also

considers the regulatory supervision with the subject to the credit risk exposure in banking

sector. Research also examined the impact of NPLR on the ROA and the results demonstrated

that less NPLR leads to maximize ROA or vice-versa.

2.5 Measurement of bank’s profitability and key determinants

According to the views of Xuebin, (2012), profitability is the key indicator of bank’s

capability to take risk or maximize capital. It also indicates the competitiveness of the bank and

serves as a measurement tool of its quality of management. The commercial bank’s profitability

can be measured in two sense; internal determinants which are under the control of internal

management and external determinants which is outside the control of managers. Internal

determinants emphasize upon the managing policy, financial management, liquidity management

and efficiency and effectiveness of risk management and can be measured using financial

statements of the banks. It is of great significance in order to assess and evaluate the credit risk

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.