Credit Risk Management and Financial Analysis of Marks & Spencer

VerifiedAdded on 2023/01/10

|18

|5791

|39

Report

AI Summary

This report provides a detailed analysis of credit risk management, focusing on the case of Marks & Spencer. It begins with an introduction to credit risk and its importance, followed by an overview of Marks & Spencer's business and the various types of risks it faces, including economic, operational, financial, strategic, and security risks. The report then delves into credit risk analysis, exploring different tools and techniques such as quantitative and qualitative analysis, including observation, Delphi technique, schedule risk analysis, sensitivity analysis, decision tree analysis, and cost risk analysis. It also examines financial statement analysis as a credit analysis tool, including ratio analysis, to assess the financial health of the company. Furthermore, the report discusses the impact of different legal and political systems on credit risk and analyzes the concepts and reasons for financial distress. The report concludes with recommendations based on the analysis and provides a comprehensive understanding of credit risk management in the context of a major multinational retailer.

Credit Risk Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................4

MAIN BODY..............................................................................................................................................4

1 Introduction of selected organisation....................................................................................................4

2. Different types of business risks and elaborate of credit risk in context of selected company.............5

3. Understand risk analysis and risk evaluation tools and techniques......................................................6

4. Financial statement analysis as a credit analysis and ratio analysis.....................................................8

5. Credit risk arise due the exposure to a different legal and political system........................................11

6 Analyzing the concepts and reasons of financial distress....................................................................13

CONCLUSION AND RECOMMENDATIONS.......................................................................................14

REFERENCES..........................................................................................................................................15

INTRODUCTION.......................................................................................................................................4

MAIN BODY..............................................................................................................................................4

1 Introduction of selected organisation....................................................................................................4

2. Different types of business risks and elaborate of credit risk in context of selected company.............5

3. Understand risk analysis and risk evaluation tools and techniques......................................................6

4. Financial statement analysis as a credit analysis and ratio analysis.....................................................8

5. Credit risk arise due the exposure to a different legal and political system........................................11

6 Analyzing the concepts and reasons of financial distress....................................................................13

CONCLUSION AND RECOMMENDATIONS.......................................................................................14

REFERENCES..........................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Risk is the probability of loss associated with the inability of a lender to repay the loan or

fulfill contract agreements. Generally, it includes the possibility of a borrower not receiving the

interest payments due, which leads to an interruption in retained earnings and elevated service

fees. Large amounts cash flows can be written down to provide additional credit risk coverage.

Credit risk management is described as the procedure of examining and defining health risks,

evaluating the degree of risk, and thus choosing steps to handle credit actions in order to reduce

and remove default risk (Accornero and et. al, 2017). Credit risk is the danger that occurs due to

inability by the creditor to conform exclusively to the conditions of the system. This may occur if

the borrower is late in loan payments, refuses to completely pay the loan amount, or refuses to

pay loan when interest and payment rates are due, triggering economic problems and challenges

in corporate banks' business operations. This report has been based on the Marks & Spencer is a

major multinational retailer company that established in UK. This report contains of various

types of business risk that face by the selected organization, understand credit risk analysis, and

related tools & techniques with the help of assessment methods. Moreover, analysis of financial

statement in order to analysis credit analysis tool and calculate various types of ration. Along

with there are mentioned various risk at the time of expansion and at the end provide

recommendations.

MAIN BODY

1 Introduction of selected organisation

Marks and Spencer Group plc (commonly abbreviated as M&S or colloquially Marks and

Sparks) is a leading UK international company based in London, England, specializing in the

selling of clothes, home-made goods and food. It is based in London Exchange and is a

component of the FTSE 250 Index, having recently been in the FTSE 100 Index from its

development through to 2019. M&S had been founded in Leeds in 1884 by Michael Marks and

Thomas Spencer. M&S owns and operates 959 stores in the UK. It includes 615 which sell sole

food items. Currently the business conducts activities in various countries about 1463 locations.

There are working about 80000 employees and the company has been dealing into various

Risk is the probability of loss associated with the inability of a lender to repay the loan or

fulfill contract agreements. Generally, it includes the possibility of a borrower not receiving the

interest payments due, which leads to an interruption in retained earnings and elevated service

fees. Large amounts cash flows can be written down to provide additional credit risk coverage.

Credit risk management is described as the procedure of examining and defining health risks,

evaluating the degree of risk, and thus choosing steps to handle credit actions in order to reduce

and remove default risk (Accornero and et. al, 2017). Credit risk is the danger that occurs due to

inability by the creditor to conform exclusively to the conditions of the system. This may occur if

the borrower is late in loan payments, refuses to completely pay the loan amount, or refuses to

pay loan when interest and payment rates are due, triggering economic problems and challenges

in corporate banks' business operations. This report has been based on the Marks & Spencer is a

major multinational retailer company that established in UK. This report contains of various

types of business risk that face by the selected organization, understand credit risk analysis, and

related tools & techniques with the help of assessment methods. Moreover, analysis of financial

statement in order to analysis credit analysis tool and calculate various types of ration. Along

with there are mentioned various risk at the time of expansion and at the end provide

recommendations.

MAIN BODY

1 Introduction of selected organisation

Marks and Spencer Group plc (commonly abbreviated as M&S or colloquially Marks and

Sparks) is a leading UK international company based in London, England, specializing in the

selling of clothes, home-made goods and food. It is based in London Exchange and is a

component of the FTSE 250 Index, having recently been in the FTSE 100 Index from its

development through to 2019. M&S had been founded in Leeds in 1884 by Michael Marks and

Thomas Spencer. M&S owns and operates 959 stores in the UK. It includes 615 which sell sole

food items. Currently the business conducts activities in various countries about 1463 locations.

There are working about 80000 employees and the company has been dealing into various

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

brands such as, Blue harbor, M&S collection, Autograph, Rosie, limited and many others. In the

year 2018 due to radical plan the company closed about 100 stores that impact on the revenues.

In 1973, the business launched into Canada, with forty-seven shops along all Canada from one

juncture. Given numerous attempts to boost its brand, there the company has never been able to

step past its notoriety as an uninspired supermarket, one that mainly provided to elderly people

and British expatriates. Canada's markets were fewer than UK retailers, and did not offer the

same range. Even more attempts were made in the late 1990s to modernize them and increase

customer base, too. The Canadian activities consistently lost cash, however, and the last 38 stores

in Canada were closed in 1999.

2. Different types of business risks and elaborate of credit risk in context of selected company

Business risk is the liability factor(s) a corporation or entity may have that can reduce its

profits or cause it to fail. Everything which challenges the capacity of a firm to accomplish its

objective or attain its revenue objectives is considered business covers. Those risks come from

many different of publications, but again that is not always the director of the committee or a

supervisor to criticize. Rather, the dangers could come from various sources inside the company,

or they may be exogenous to the general economy from restrictions (Agosto, Giudici and Leach,

2019). There are mentioned various types of risk that face by an organisation such as:

Economic risk: Economic risk is related to as the systemic risk of an international-country

transaction depending on market circumstances or negative effects of macroeconomic indicators

such as changed economic or the present administration's fall, and global exchange rate

volatility. Economic risk is the probability that a capital expenditure, generally one for a different

nation, would then impact market stability such as currency rates, government regulations or

good governance.

Operational risk: Operational risk describes the potential hazards faced by an organization

while attempting to perform these day-to-day retail operations within such a particular region or

industry. A form of financial investment, it can contribute from disruptions in operating rules,

individuals and structures as opposed to increasing the cost by external factors, along with

economic or social happenings, or underlying to the whole economy or consumer market,

identified as expected returns.

year 2018 due to radical plan the company closed about 100 stores that impact on the revenues.

In 1973, the business launched into Canada, with forty-seven shops along all Canada from one

juncture. Given numerous attempts to boost its brand, there the company has never been able to

step past its notoriety as an uninspired supermarket, one that mainly provided to elderly people

and British expatriates. Canada's markets were fewer than UK retailers, and did not offer the

same range. Even more attempts were made in the late 1990s to modernize them and increase

customer base, too. The Canadian activities consistently lost cash, however, and the last 38 stores

in Canada were closed in 1999.

2. Different types of business risks and elaborate of credit risk in context of selected company

Business risk is the liability factor(s) a corporation or entity may have that can reduce its

profits or cause it to fail. Everything which challenges the capacity of a firm to accomplish its

objective or attain its revenue objectives is considered business covers. Those risks come from

many different of publications, but again that is not always the director of the committee or a

supervisor to criticize. Rather, the dangers could come from various sources inside the company,

or they may be exogenous to the general economy from restrictions (Agosto, Giudici and Leach,

2019). There are mentioned various types of risk that face by an organisation such as:

Economic risk: Economic risk is related to as the systemic risk of an international-country

transaction depending on market circumstances or negative effects of macroeconomic indicators

such as changed economic or the present administration's fall, and global exchange rate

volatility. Economic risk is the probability that a capital expenditure, generally one for a different

nation, would then impact market stability such as currency rates, government regulations or

good governance.

Operational risk: Operational risk describes the potential hazards faced by an organization

while attempting to perform these day-to-day retail operations within such a particular region or

industry. A form of financial investment, it can contribute from disruptions in operating rules,

individuals and structures as opposed to increasing the cost by external factors, along with

economic or social happenings, or underlying to the whole economy or consumer market,

identified as expected returns.

Financial risk: Financial risk includes how a business provides its financial resources and

handles its overall debt. Economic risk includes why a business can produce adequate sales and

income to pay its current liabilities and generate a profit. There is a problem with economic

burden that a firm cans external debt service payouts. Financial risk is the danger that a

corporation will not be capable of meeting its debt repayment responsibilities. In turn could

imply that the funds stock in the business will be lost by potential buyers. The greater the debt a

firm has, the greater the future financial risk.

Strategic risk: Everybody understands that a good company requires a detailed business plan

which is well liked to think-out. And it's also a normal part of life that circumstances move and

even greatest-laid plans will begin to look quite dated, very easily. That is a strategic threat. It's

the possibility that the approach of the organization would become less successful and as a

consequence company will fail to achieve its objectives. That could be due to significant

alterations, a potentially powerful contender coming into the market, transitions in customer

requirements, peaks in cost of raw materials, and any amount of other major changes

(Ahelegbey, Giudici and Hadji-Misheva, 2019).

Security and fraud risk: Because more clients utilize internet and digital platforms to start

sharing personal information, the possibilities for data theft are indeed higher. News reports

regarding security breaches, financial fraud and transaction theft highlight how companies are

increasing this degree of stress. The vulnerability not only affects confidence and integrity, it

also renders a business potentially responsible for all data violations or theft. Concentrate on

software solutions, fraud prevention techniques and customer satisfaction and employee

schooling on how to recognize any possible pitfalls to accomplish efficient organizational

corporate governance.

Credit risk is the risk of default that may result from any current party inability to agree

to the terms and requirements of any business arrangement, specifically the fail to satisfy the

necessary mortgage repayments owed to an individual. As a fund manager, a lender's fund

management distribution is associated with risks which are specific to its bank loans and

exchange undertakings and the ecosystem it continues to operate inside it. The main objective of

risk managerial project financing is to ensure that it needs to understand, indicators and screens

the numerous risks arising and also that the institution conforms purely to the processes and

handles its overall debt. Economic risk includes why a business can produce adequate sales and

income to pay its current liabilities and generate a profit. There is a problem with economic

burden that a firm cans external debt service payouts. Financial risk is the danger that a

corporation will not be capable of meeting its debt repayment responsibilities. In turn could

imply that the funds stock in the business will be lost by potential buyers. The greater the debt a

firm has, the greater the future financial risk.

Strategic risk: Everybody understands that a good company requires a detailed business plan

which is well liked to think-out. And it's also a normal part of life that circumstances move and

even greatest-laid plans will begin to look quite dated, very easily. That is a strategic threat. It's

the possibility that the approach of the organization would become less successful and as a

consequence company will fail to achieve its objectives. That could be due to significant

alterations, a potentially powerful contender coming into the market, transitions in customer

requirements, peaks in cost of raw materials, and any amount of other major changes

(Ahelegbey, Giudici and Hadji-Misheva, 2019).

Security and fraud risk: Because more clients utilize internet and digital platforms to start

sharing personal information, the possibilities for data theft are indeed higher. News reports

regarding security breaches, financial fraud and transaction theft highlight how companies are

increasing this degree of stress. The vulnerability not only affects confidence and integrity, it

also renders a business potentially responsible for all data violations or theft. Concentrate on

software solutions, fraud prevention techniques and customer satisfaction and employee

schooling on how to recognize any possible pitfalls to accomplish efficient organizational

corporate governance.

Credit risk is the risk of default that may result from any current party inability to agree

to the terms and requirements of any business arrangement, specifically the fail to satisfy the

necessary mortgage repayments owed to an individual. As a fund manager, a lender's fund

management distribution is associated with risks which are specific to its bank loans and

exchange undertakings and the ecosystem it continues to operate inside it. The main objective of

risk managerial project financing is to ensure that it needs to understand, indicators and screens

the numerous risks arising and also that the institution conforms purely to the processes and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

regulations set out to resolve these dangers (Alavi, 2016). Credit risk face by the Marks &

Spencer: Moody's has upgraded the credit score for Marks & Spencer from secure to pessimistic

after a tough year for the retail outlet. The pessimistic progress brings after the previous trading

study by M&S that also documented a 2.7% downward trend in garments and residence-like sale

prices and over 13 weeks to 28 December. When a corporation does not request payment until

shipping offering products, it reduces its default risk. Often corporate activities are performed on

credit; but today's developments indicate that reviewing something more than the facts of

statement of financial position are very critical for business success. A credit risk is the

possibility of financial collapse that could occur from a creditor refusing to make the appropriate

payouts. The vulnerability in the first recourse is that of the investor which involves decreased

principal balance, cash flow interruption and additional expense of compilation. The loss can be

full or partial (Yu, Zhou and Chen, 2018).

3. Understand risk analysis and risk evaluation tools and techniques

To better understand about the risk analysis requires to apply risk evaluation tool &

techniques that categorized in two manner such as:

Quantitative analysis: Quantitative data evaluate the scope and depth of an execution

(e.g., amount of participants, percentage of employees who have done the system). Quantitative

evidence obtained during and before an event will show the effectiveness and performance. Its

generalization includes the abilities of statistical method for performance evaluation. To analysis

the risk in Marks & Spencer require to apply various methods of quantitative analysis such as:

Observation: As per the methodology learn various things in regard of staff members.

Mind, however, that the very act of watching will alter behaviors. People typically are becoming

more self-conscious when they feel it is necessary. They may needs to invest in a specialist who

is skilled in performing accurate and independent organizational analyses, together with

preparation and supervision to execute analyses (Camilleri, 2016).

Delphi technique: It is a method of risk idea generation, but the fundamental distinction

between conventional Credit risks strategizing including the use of Delphi Technique would be

that professional advice is utilized through the Delphi Technique to define, assess threats on an

Spencer: Moody's has upgraded the credit score for Marks & Spencer from secure to pessimistic

after a tough year for the retail outlet. The pessimistic progress brings after the previous trading

study by M&S that also documented a 2.7% downward trend in garments and residence-like sale

prices and over 13 weeks to 28 December. When a corporation does not request payment until

shipping offering products, it reduces its default risk. Often corporate activities are performed on

credit; but today's developments indicate that reviewing something more than the facts of

statement of financial position are very critical for business success. A credit risk is the

possibility of financial collapse that could occur from a creditor refusing to make the appropriate

payouts. The vulnerability in the first recourse is that of the investor which involves decreased

principal balance, cash flow interruption and additional expense of compilation. The loss can be

full or partial (Yu, Zhou and Chen, 2018).

3. Understand risk analysis and risk evaluation tools and techniques

To better understand about the risk analysis requires to apply risk evaluation tool &

techniques that categorized in two manner such as:

Quantitative analysis: Quantitative data evaluate the scope and depth of an execution

(e.g., amount of participants, percentage of employees who have done the system). Quantitative

evidence obtained during and before an event will show the effectiveness and performance. Its

generalization includes the abilities of statistical method for performance evaluation. To analysis

the risk in Marks & Spencer require to apply various methods of quantitative analysis such as:

Observation: As per the methodology learn various things in regard of staff members.

Mind, however, that the very act of watching will alter behaviors. People typically are becoming

more self-conscious when they feel it is necessary. They may needs to invest in a specialist who

is skilled in performing accurate and independent organizational analyses, together with

preparation and supervision to execute analyses (Camilleri, 2016).

Delphi technique: It is a method of risk idea generation, but the fundamental distinction

between conventional Credit risks strategizing including the use of Delphi Technique would be

that professional advice is utilized through the Delphi Technique to define, assess threats on an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

independent and confidential level. Instead each specialist analyses one another's threats, and a

threat registry is created by continuing analysis and agreement among the expertise.

Schedule risk analysis: Schedule Risk Analysis (SRA) is a basic and efficient

methodology for linking risk assessment details to the reference plan to include vulnerability

details on actual project operations to determine the possible influence of ambiguity on the final

period and expense of the venture (Wu, Al-Khateeb, Teng and Cárdenas-Barrón, 2016).

Qualitative analysis: Qualitative analysis utilizes analytical judgment to assess the

importance or expectations of a business that are focused on non - measurable factors such as

managerial experience, market cycles, research & innovation power, and worker rights.

Qualitative research relies on the statistics contained in these records as averages. Nevertheless,

the two approaches are also employed together again to analyze the activities of a business and

determine its value as an incentive for development.

Sensitivity analysis: It is technique of credit risk evaluation to see the way workers see

the business and its managers. Staff turnover rate may imply allegiance or lack of commitment to

the staff members. Subterfuge and rivalry and drain creative resources are encouraged by

excessively bureaucratic headquarters; a lazy, unproductive atmosphere may imply workers are

only occupied with hitting the time. The dream is an innovative, diverse community that draws

best talent. With the help of this too an organisation can analysis the credit activity in the

business (Chen, Xiao and Liu, 2018).

Decision tree analysis: Similar to Event Tree Evaluation however without having a

complete quantitative output, decision tree model is more commonly used to better assess the

appropriate response when there is confusion regarding the results of future incidents or planned

proposals. This is achieved by beginning with the original agreed decision and projecting as a

function of incidents resulting from the earlier ruling, the divergent routes and consequences.

When all paths and results are being described and their corresponding risks measured, a plan of

treatment can be chosen depending on a mixture of the most favorable consequences, similar

things, and the possibility of completion.

threat registry is created by continuing analysis and agreement among the expertise.

Schedule risk analysis: Schedule Risk Analysis (SRA) is a basic and efficient

methodology for linking risk assessment details to the reference plan to include vulnerability

details on actual project operations to determine the possible influence of ambiguity on the final

period and expense of the venture (Wu, Al-Khateeb, Teng and Cárdenas-Barrón, 2016).

Qualitative analysis: Qualitative analysis utilizes analytical judgment to assess the

importance or expectations of a business that are focused on non - measurable factors such as

managerial experience, market cycles, research & innovation power, and worker rights.

Qualitative research relies on the statistics contained in these records as averages. Nevertheless,

the two approaches are also employed together again to analyze the activities of a business and

determine its value as an incentive for development.

Sensitivity analysis: It is technique of credit risk evaluation to see the way workers see

the business and its managers. Staff turnover rate may imply allegiance or lack of commitment to

the staff members. Subterfuge and rivalry and drain creative resources are encouraged by

excessively bureaucratic headquarters; a lazy, unproductive atmosphere may imply workers are

only occupied with hitting the time. The dream is an innovative, diverse community that draws

best talent. With the help of this too an organisation can analysis the credit activity in the

business (Chen, Xiao and Liu, 2018).

Decision tree analysis: Similar to Event Tree Evaluation however without having a

complete quantitative output, decision tree model is more commonly used to better assess the

appropriate response when there is confusion regarding the results of future incidents or planned

proposals. This is achieved by beginning with the original agreed decision and projecting as a

function of incidents resulting from the earlier ruling, the divergent routes and consequences.

When all paths and results are being described and their corresponding risks measured, a plan of

treatment can be chosen depending on a mixture of the most favorable consequences, similar

things, and the possibility of completion.

Cost risk analysis: It includes a thorough evaluation of the potential risks that impact

value management results, accompanied by an evaluation of the liability, guesstimate precision,

and realize the benefits expected to carry out the investment projects or restructuring process.

Break even analysis: A break-even analysis is a monetary instrument that enables people

evaluates how cost effective their business, or a new products or services, will be at. That is, it is

an economic measurement to determine the products or services that a corporation should

advertise to pay its current liabilities (especially capital expenses).

Therefore, these are all qualitative and quantitative tools that use by the Marks & Spencer

organisation in order to evaluate the credit risk in business (Cole, Giné and Vickery, 2017).

Credit risk derivatives: Credit derivatives are financial instruments which shift credit

risk through one group elsewhere without shifting the corresponding investment portfolio

through one side to the next. That is recognized as credit danger. It decides the credit histories

for the debt rising government bonds by the firms. The investor is marketing this debt to many

other entities requesting investment in government bonds. These purchasers are getting lender

loan repayments. Once consuming a lot these specific financial instruments, the credit risk is

transported to them though the lenders continue to stay on the existing bank's paperbacks.

Humans call those finance cars and trucks risk estimation. A credit derivative is a financial

instrument which enables the stakeholders to control their credit risk. Credit derivative composed

of a private contractual agreement up for negotiation among both 2 people in a lender / borrower

connection. It enables the debt collector to pass on the borrower's default risk event. There are

mentioned various types of risk such as:

Credit default swaps

Credit spread forward

Total return swaps

Credit default swap options

Collateralized debt obligations

4. Financial statement analysis as a credit analysis and ratio analysis

The review of the financial report is the method of assessing the existing accounts of a

business for the reasons of decision taking. It is used by different customers to comprehend a

value management results, accompanied by an evaluation of the liability, guesstimate precision,

and realize the benefits expected to carry out the investment projects or restructuring process.

Break even analysis: A break-even analysis is a monetary instrument that enables people

evaluates how cost effective their business, or a new products or services, will be at. That is, it is

an economic measurement to determine the products or services that a corporation should

advertise to pay its current liabilities (especially capital expenses).

Therefore, these are all qualitative and quantitative tools that use by the Marks & Spencer

organisation in order to evaluate the credit risk in business (Cole, Giné and Vickery, 2017).

Credit risk derivatives: Credit derivatives are financial instruments which shift credit

risk through one group elsewhere without shifting the corresponding investment portfolio

through one side to the next. That is recognized as credit danger. It decides the credit histories

for the debt rising government bonds by the firms. The investor is marketing this debt to many

other entities requesting investment in government bonds. These purchasers are getting lender

loan repayments. Once consuming a lot these specific financial instruments, the credit risk is

transported to them though the lenders continue to stay on the existing bank's paperbacks.

Humans call those finance cars and trucks risk estimation. A credit derivative is a financial

instrument which enables the stakeholders to control their credit risk. Credit derivative composed

of a private contractual agreement up for negotiation among both 2 people in a lender / borrower

connection. It enables the debt collector to pass on the borrower's default risk event. There are

mentioned various types of risk such as:

Credit default swaps

Credit spread forward

Total return swaps

Credit default swap options

Collateralized debt obligations

4. Financial statement analysis as a credit analysis and ratio analysis

The review of the financial report is the method of assessing the existing accounts of a

business for the reasons of decision taking. It is used by different customers to comprehend a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company's core wellbeing, and to generate business performance and organizational valuation.

External members use it as a financial-management reporting device (Wireko and Forson, 2017).

A balance sheet of an organization can use as techniques to collect financial information on all

affecting the company’s actions. Even so, they can be assessed on a results evaluation on past,

historical and prospective.

To judge the ability of a company to pay its debt, banks, bond investors and analysts

carry out credit analyzes on the business. An investor may assess the willingness of a company

to meet its duty utilizing financial measures, cash flow analysis, pattern research and economic

forecasts. Credit analysis is amongst the most popular sources of financial reports, highlighting

the many aspects of debt important for a capitalist society to operate. Sellers exchanging goods

for commitments to charge have to check the ability of such pledges (Colombini, 2018).

Financial institutions that give the financial resources to sellers to support their inventory levels

must also measure the likelihood of filled and timely repayment. In addition, the banks will show

their financial health to many other finance companies who loan to them through obtaining their

loan and bonds licenses. For both such situations, the review of the financial report may have a

major impact on plans to enter or not make loans. Nevertheless, as relevant as financial reports

are to credit risk management, the analyst has to keep in mind that certain techniques do play a

part. Financial reports tell a lot about both the capacity of a debtor to repay loans but reveal next

to nothing about the incredibly significant will to pay back.

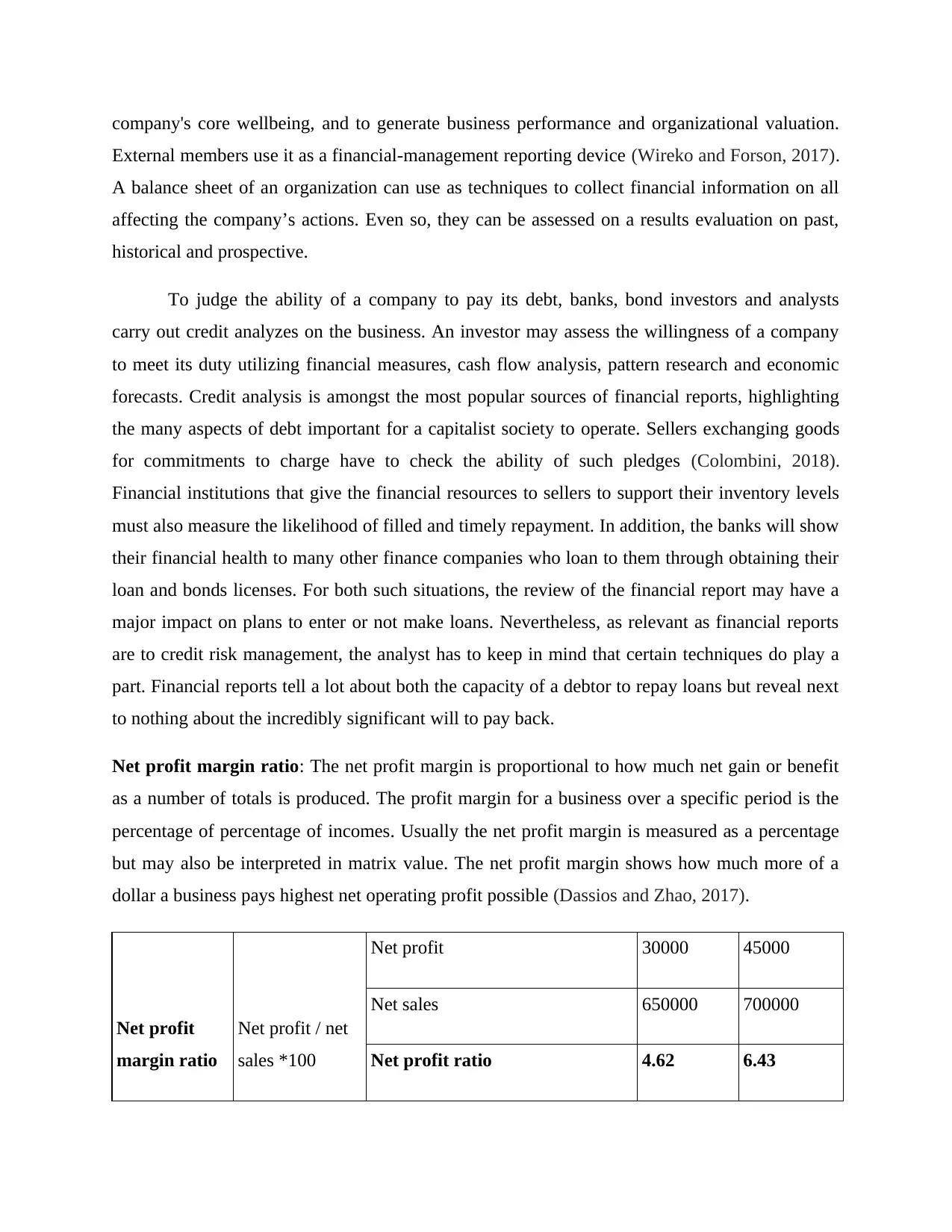

Net profit margin ratio: The net profit margin is proportional to how much net gain or benefit

as a number of totals is produced. The profit margin for a business over a specific period is the

percentage of percentage of incomes. Usually the net profit margin is measured as a percentage

but may also be interpreted in matrix value. The net profit margin shows how much more of a

dollar a business pays highest net operating profit possible (Dassios and Zhao, 2017).

Net profit

margin ratio

Net profit / net

sales *100

Net profit 30000 45000

Net sales 650000 700000

Net profit ratio 4.62 6.43

External members use it as a financial-management reporting device (Wireko and Forson, 2017).

A balance sheet of an organization can use as techniques to collect financial information on all

affecting the company’s actions. Even so, they can be assessed on a results evaluation on past,

historical and prospective.

To judge the ability of a company to pay its debt, banks, bond investors and analysts

carry out credit analyzes on the business. An investor may assess the willingness of a company

to meet its duty utilizing financial measures, cash flow analysis, pattern research and economic

forecasts. Credit analysis is amongst the most popular sources of financial reports, highlighting

the many aspects of debt important for a capitalist society to operate. Sellers exchanging goods

for commitments to charge have to check the ability of such pledges (Colombini, 2018).

Financial institutions that give the financial resources to sellers to support their inventory levels

must also measure the likelihood of filled and timely repayment. In addition, the banks will show

their financial health to many other finance companies who loan to them through obtaining their

loan and bonds licenses. For both such situations, the review of the financial report may have a

major impact on plans to enter or not make loans. Nevertheless, as relevant as financial reports

are to credit risk management, the analyst has to keep in mind that certain techniques do play a

part. Financial reports tell a lot about both the capacity of a debtor to repay loans but reveal next

to nothing about the incredibly significant will to pay back.

Net profit margin ratio: The net profit margin is proportional to how much net gain or benefit

as a number of totals is produced. The profit margin for a business over a specific period is the

percentage of percentage of incomes. Usually the net profit margin is measured as a percentage

but may also be interpreted in matrix value. The net profit margin shows how much more of a

dollar a business pays highest net operating profit possible (Dassios and Zhao, 2017).

Net profit

margin ratio

Net profit / net

sales *100

Net profit 30000 45000

Net sales 650000 700000

Net profit ratio 4.62 6.43

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

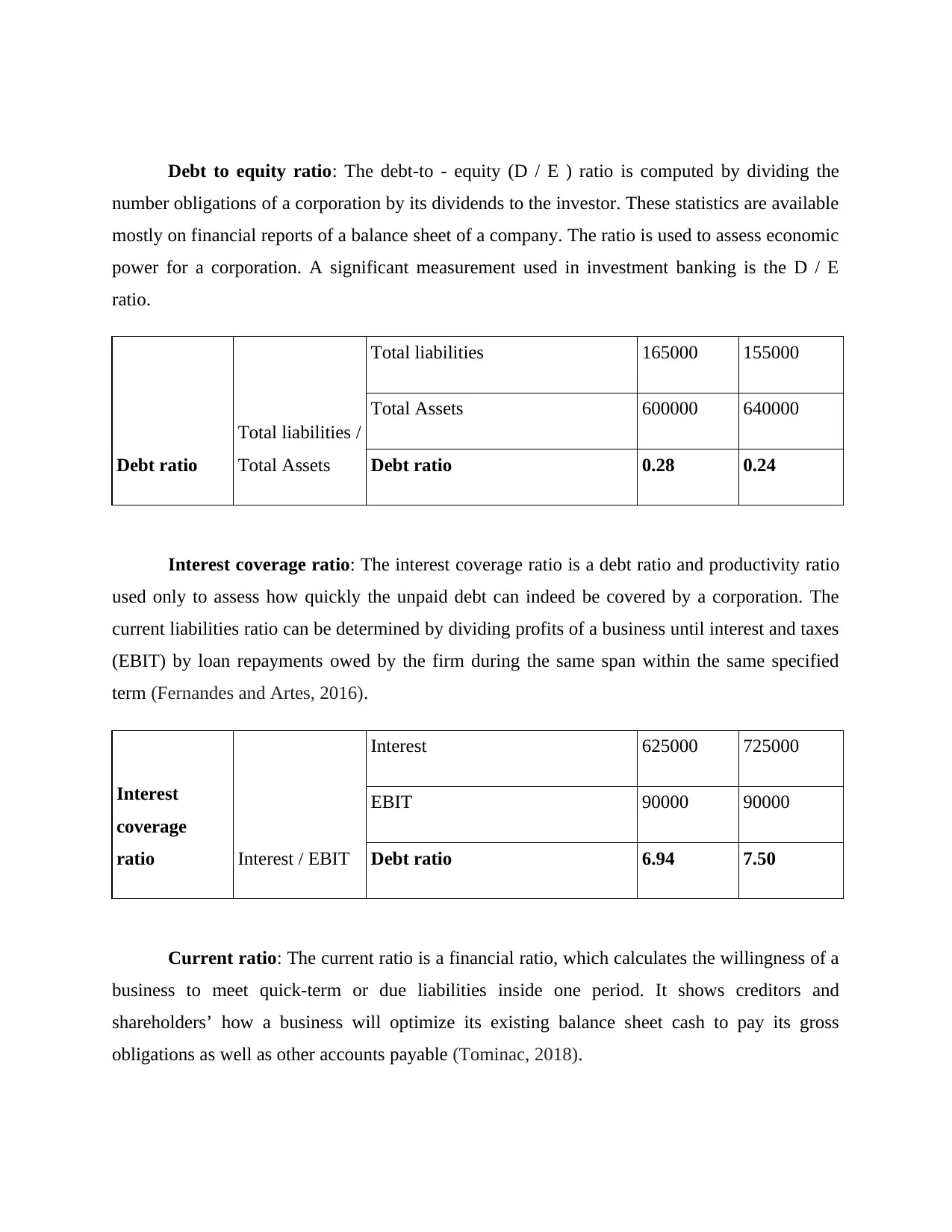

Debt to equity ratio: The debt-to - equity (D / E ) ratio is computed by dividing the

number obligations of a corporation by its dividends to the investor. These statistics are available

mostly on financial reports of a balance sheet of a company. The ratio is used to assess economic

power for a corporation. A significant measurement used in investment banking is the D / E

ratio.

Debt ratio

Total liabilities /

Total Assets

Total liabilities 165000 155000

Total Assets 600000 640000

Debt ratio 0.28 0.24

Interest coverage ratio: The interest coverage ratio is a debt ratio and productivity ratio

used only to assess how quickly the unpaid debt can indeed be covered by a corporation. The

current liabilities ratio can be determined by dividing profits of a business until interest and taxes

(EBIT) by loan repayments owed by the firm during the same span within the same specified

term (Fernandes and Artes, 2016).

Interest

coverage

ratio Interest / EBIT

Interest 625000 725000

EBIT 90000 90000

Debt ratio 6.94 7.50

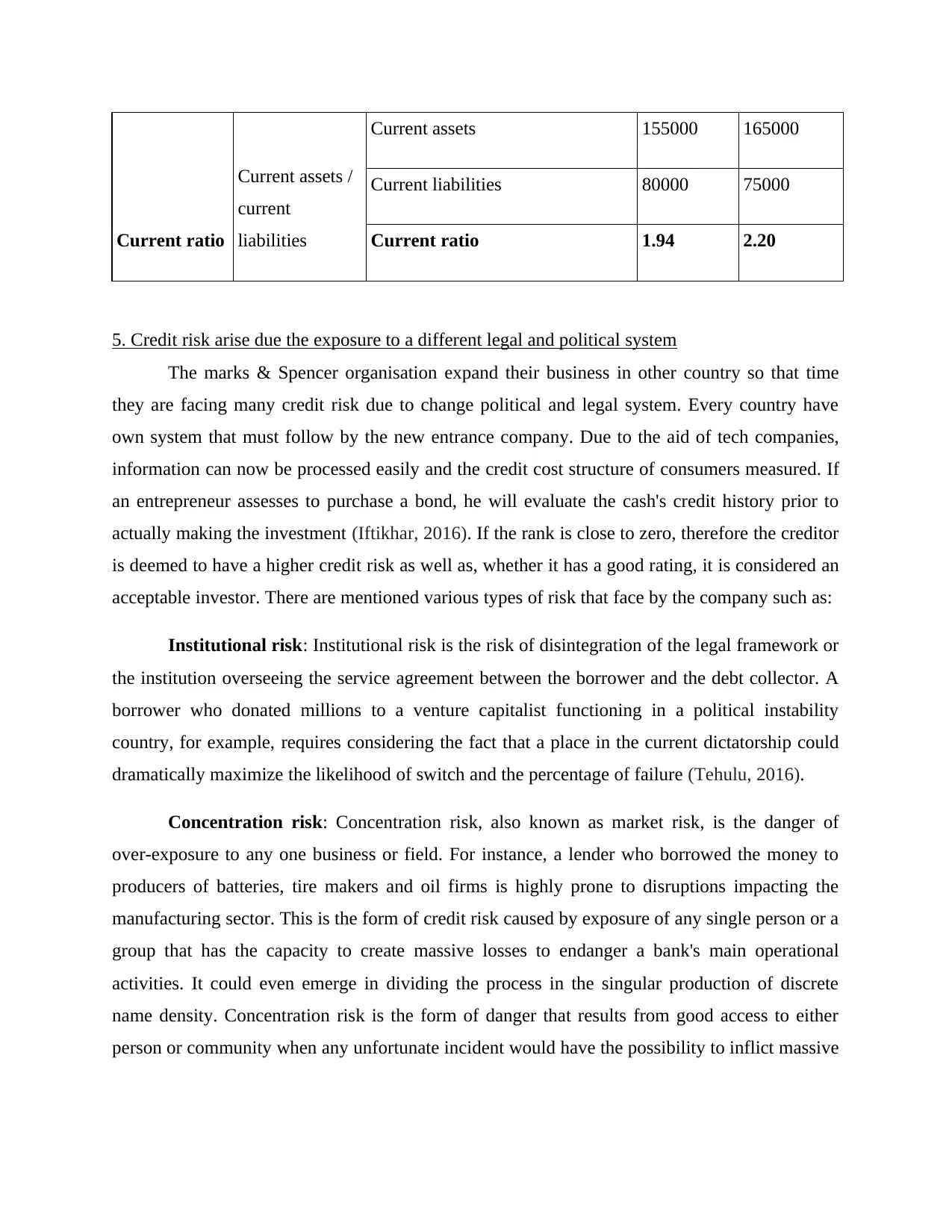

Current ratio: The current ratio is a financial ratio, which calculates the willingness of a

business to meet quick-term or due liabilities inside one period. It shows creditors and

shareholders’ how a business will optimize its existing balance sheet cash to pay its gross

obligations as well as other accounts payable (Tominac, 2018).

number obligations of a corporation by its dividends to the investor. These statistics are available

mostly on financial reports of a balance sheet of a company. The ratio is used to assess economic

power for a corporation. A significant measurement used in investment banking is the D / E

ratio.

Debt ratio

Total liabilities /

Total Assets

Total liabilities 165000 155000

Total Assets 600000 640000

Debt ratio 0.28 0.24

Interest coverage ratio: The interest coverage ratio is a debt ratio and productivity ratio

used only to assess how quickly the unpaid debt can indeed be covered by a corporation. The

current liabilities ratio can be determined by dividing profits of a business until interest and taxes

(EBIT) by loan repayments owed by the firm during the same span within the same specified

term (Fernandes and Artes, 2016).

Interest

coverage

ratio Interest / EBIT

Interest 625000 725000

EBIT 90000 90000

Debt ratio 6.94 7.50

Current ratio: The current ratio is a financial ratio, which calculates the willingness of a

business to meet quick-term or due liabilities inside one period. It shows creditors and

shareholders’ how a business will optimize its existing balance sheet cash to pay its gross

obligations as well as other accounts payable (Tominac, 2018).

Current ratio

Current assets /

current

liabilities

Current assets 155000 165000

Current liabilities 80000 75000

Current ratio 1.94 2.20

5. Credit risk arise due the exposure to a different legal and political system

The marks & Spencer organisation expand their business in other country so that time

they are facing many credit risk due to change political and legal system. Every country have

own system that must follow by the new entrance company. Due to the aid of tech companies,

information can now be processed easily and the credit cost structure of consumers measured. If

an entrepreneur assesses to purchase a bond, he will evaluate the cash's credit history prior to

actually making the investment (Iftikhar, 2016). If the rank is close to zero, therefore the creditor

is deemed to have a higher credit risk as well as, whether it has a good rating, it is considered an

acceptable investor. There are mentioned various types of risk that face by the company such as:

Institutional risk: Institutional risk is the risk of disintegration of the legal framework or

the institution overseeing the service agreement between the borrower and the debt collector. A

borrower who donated millions to a venture capitalist functioning in a political instability

country, for example, requires considering the fact that a place in the current dictatorship could

dramatically maximize the likelihood of switch and the percentage of failure (Tehulu, 2016).

Concentration risk: Concentration risk, also known as market risk, is the danger of

over-exposure to any one business or field. For instance, a lender who borrowed the money to

producers of batteries, tire makers and oil firms is highly prone to disruptions impacting the

manufacturing sector. This is the form of credit risk caused by exposure of any single person or a

group that has the capacity to create massive losses to endanger a bank's main operational

activities. It could even emerge in dividing the process in the singular production of discrete

name density. Concentration risk is the form of danger that results from good access to either

person or community when any unfortunate incident would have the possibility to inflict massive

Current assets /

current

liabilities

Current assets 155000 165000

Current liabilities 80000 75000

Current ratio 1.94 2.20

5. Credit risk arise due the exposure to a different legal and political system

The marks & Spencer organisation expand their business in other country so that time

they are facing many credit risk due to change political and legal system. Every country have

own system that must follow by the new entrance company. Due to the aid of tech companies,

information can now be processed easily and the credit cost structure of consumers measured. If

an entrepreneur assesses to purchase a bond, he will evaluate the cash's credit history prior to

actually making the investment (Iftikhar, 2016). If the rank is close to zero, therefore the creditor

is deemed to have a higher credit risk as well as, whether it has a good rating, it is considered an

acceptable investor. There are mentioned various types of risk that face by the company such as:

Institutional risk: Institutional risk is the risk of disintegration of the legal framework or

the institution overseeing the service agreement between the borrower and the debt collector. A

borrower who donated millions to a venture capitalist functioning in a political instability

country, for example, requires considering the fact that a place in the current dictatorship could

dramatically maximize the likelihood of switch and the percentage of failure (Tehulu, 2016).

Concentration risk: Concentration risk, also known as market risk, is the danger of

over-exposure to any one business or field. For instance, a lender who borrowed the money to

producers of batteries, tire makers and oil firms is highly prone to disruptions impacting the

manufacturing sector. This is the form of credit risk caused by exposure of any single person or a

group that has the capacity to create massive losses to endanger a bank's main operational

activities. It could even emerge in dividing the process in the singular production of discrete

name density. Concentration risk is the form of danger that results from good access to either

person or community when any unfortunate incident would have the possibility to inflict massive

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.