Conceptual Framework of Accounting

VerifiedAdded on 2019/09/13

|18

|2790

|700

Essay

AI Summary

This essay provides a critical analysis of the evolution of the conceptual framework of accounting. It examines the framework's objectives, evaluating the implementation of the Australian equivalent of IASB (AASB) through an analysis of general purpose financial statements from two listed entities, Woolworths and Wesfarmers. The essay delves into the significance of the reintroduction of prudence into the framework, contrasting it with the conservative approach and highlighting its contribution to neutrality in financial reporting. The role of positive and normative accounting theories in shaping the framework is discussed, along with an analysis of the framework's limitations and the impact of local regulations on global comparability. Recommendations for improvement, such as a shift towards principle-based accounting standards, are offered. The conclusion emphasizes the ongoing evolution of the framework in response to technological advancements and changing investor expectations.

Conceptual FrameworK – A Critical analysis

NAME OF THE STUDENT

NAME OF THE STUDENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This essay aims to evaluate the evolution of conceptual framework of accounting. The guiding

principle of the conceptual framework has been the achievement of objectives of the

framework. The current sample general purpose financial statement has been evaluated to

understand the implementation of the conceptual framework in existence in Australia through

AASB which is the IASB equivalent in Australia. The introduction of new concept of prudence in

the conceptual framework is explained in detail for its contribution to the overall objective of

the financial reporting. The various theories viz. the positive theory and normative theory has

been analyzed for its value-addition to the conceptual framework of accounting. The efficacy of

the local regulations in various countries and its impact on the overall objective of financial

reporting is analyzed. The limitation of the framework has been briefed with suitable

recommendations.

1

This essay aims to evaluate the evolution of conceptual framework of accounting. The guiding

principle of the conceptual framework has been the achievement of objectives of the

framework. The current sample general purpose financial statement has been evaluated to

understand the implementation of the conceptual framework in existence in Australia through

AASB which is the IASB equivalent in Australia. The introduction of new concept of prudence in

the conceptual framework is explained in detail for its contribution to the overall objective of

the financial reporting. The various theories viz. the positive theory and normative theory has

been analyzed for its value-addition to the conceptual framework of accounting. The efficacy of

the local regulations in various countries and its impact on the overall objective of financial

reporting is analyzed. The limitation of the framework has been briefed with suitable

recommendations.

1

Contents

Executive Summary....................................................................................................................... 1

Introduction...................................................................................................................................3

Analysis.......................................................................................................................................... 4

Objectives of the Conceptual Framework of Accounting...........................................................4

Evaluation of financial reporting of two listed entities..............................................................4

Overall Compliance with AASB framework:...........................................................................4

Whether the report a source of information for decision making?.......................................5

Impact of inclusion of Prudence in conceptual framework.......................................................7

Accounting Theories – POSITIVE / NORMATIVE.........................................................................8

Failure of Conceptual Framework..............................................................................................9

Is regulation the key to resolve issues?...................................................................................10

Recommendations.......................................................................................................................10

Conclusion................................................................................................................................... 11

References................................................................................................................................... 12

Appendix 1: Woolworth’s Analysis of financial performance......................................................14

Appendix 2: New Store Rollout Plans of Woolworths..................................................................15

Appendix 3: Performance Overview - Wesfarmers......................................................................16

2

Executive Summary....................................................................................................................... 1

Introduction...................................................................................................................................3

Analysis.......................................................................................................................................... 4

Objectives of the Conceptual Framework of Accounting...........................................................4

Evaluation of financial reporting of two listed entities..............................................................4

Overall Compliance with AASB framework:...........................................................................4

Whether the report a source of information for decision making?.......................................5

Impact of inclusion of Prudence in conceptual framework.......................................................7

Accounting Theories – POSITIVE / NORMATIVE.........................................................................8

Failure of Conceptual Framework..............................................................................................9

Is regulation the key to resolve issues?...................................................................................10

Recommendations.......................................................................................................................10

Conclusion................................................................................................................................... 11

References................................................................................................................................... 12

Appendix 1: Woolworth’s Analysis of financial performance......................................................14

Appendix 2: New Store Rollout Plans of Woolworths..................................................................15

Appendix 3: Performance Overview - Wesfarmers......................................................................16

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The conceptual framework of accounting has been dynamic to the changes in the business

scenario. The recent change of inclusion of prudence in the overall framework aims to make the

financial reporting more neutral and reality based. This change is viewed as significant deviation

from the existing erred interpretation of the accounting framework to be conservative and

often imprudent. The neutral approach as supported by the prudence principle aims to

eliminate management’s bias in financial reporting thus adding to the overall usefulness of the

financial reporting.

3

The conceptual framework of accounting has been dynamic to the changes in the business

scenario. The recent change of inclusion of prudence in the overall framework aims to make the

financial reporting more neutral and reality based. This change is viewed as significant deviation

from the existing erred interpretation of the accounting framework to be conservative and

often imprudent. The neutral approach as supported by the prudence principle aims to

eliminate management’s bias in financial reporting thus adding to the overall usefulness of the

financial reporting.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis

Objectives of the Conceptual Framework of Accounting

The conceptual framework is in essence a theory of accounting principles to ensure that the

a. Financial statements remain useful to the end users of financial statements

b. characteristics are determined to make the accounting information useful

c. issues related to basic components of financial statements and it recognition and

measurement principles are addressed. (Ft.com, n.d.)

The objectives of the conceptual framework is summarized as below:

a. It should aid decision making of the primary users of financial statements viz. investors

and creditors

b. It should reflect a neutral depiction of entity’s financial performance and position

c. It should assist in prediction of future cash flows of the company

d. The reports should disclose the efficiency of business operations as well

(PWC, 2015)

Evaluation of financial reporting of two listed entities

The two company identified for analysis of the adherence to and the impact of conceptual

framework of accounting are Woolworths and Wesfarmers. We have chosen these companies

as they are the key competitors and operate within the same industry in Australia.

Overall Compliance with AASB framework:

The financial statements of both companies comply with the AASB standards requirements.

This disclosure has been made in the significant accounting policies section of the notes to the

financial statements in the annual reports. The specific representation made are reproduced as

below:

4

Objectives of the Conceptual Framework of Accounting

The conceptual framework is in essence a theory of accounting principles to ensure that the

a. Financial statements remain useful to the end users of financial statements

b. characteristics are determined to make the accounting information useful

c. issues related to basic components of financial statements and it recognition and

measurement principles are addressed. (Ft.com, n.d.)

The objectives of the conceptual framework is summarized as below:

a. It should aid decision making of the primary users of financial statements viz. investors

and creditors

b. It should reflect a neutral depiction of entity’s financial performance and position

c. It should assist in prediction of future cash flows of the company

d. The reports should disclose the efficiency of business operations as well

(PWC, 2015)

Evaluation of financial reporting of two listed entities

The two company identified for analysis of the adherence to and the impact of conceptual

framework of accounting are Woolworths and Wesfarmers. We have chosen these companies

as they are the key competitors and operate within the same industry in Australia.

Overall Compliance with AASB framework:

The financial statements of both companies comply with the AASB standards requirements.

This disclosure has been made in the significant accounting policies section of the notes to the

financial statements in the annual reports. The specific representation made are reproduced as

below:

4

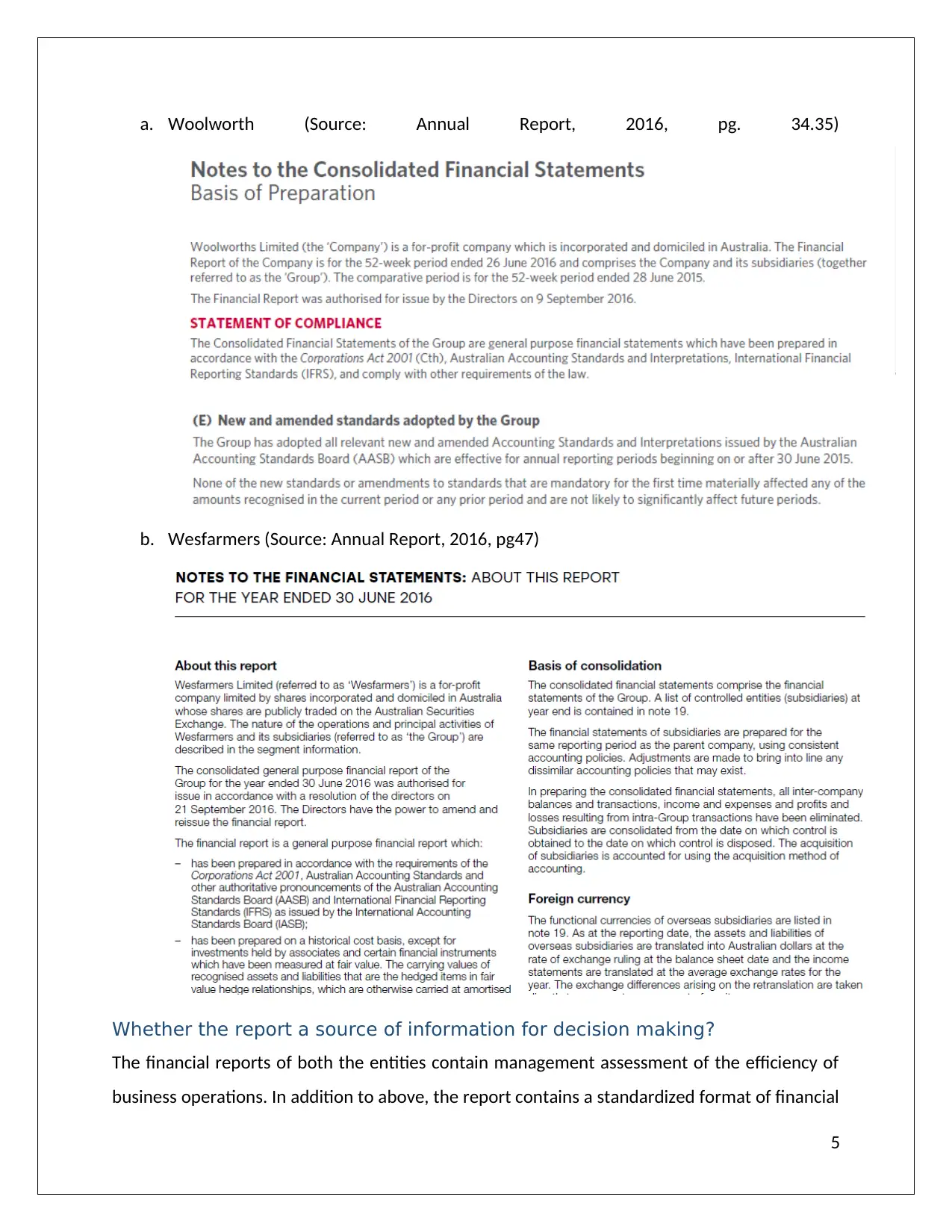

a. Woolworth (Source: Annual Report, 2016, pg. 34.35)

b. Wesfarmers (Source: Annual Report, 2016, pg47)

Whether the report a source of information for decision making?

The financial reports of both the entities contain management assessment of the efficiency of

business operations. In addition to above, the report contains a standardized format of financial

5

b. Wesfarmers (Source: Annual Report, 2016, pg47)

Whether the report a source of information for decision making?

The financial reports of both the entities contain management assessment of the efficiency of

business operations. In addition to above, the report contains a standardized format of financial

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information in the form of statement of financial position, statement of profit and loss,

statement of other comprehensive income, statement of changes in equity and statement of

cash flows. In addition to these data the accounting policies and assumptions relied upon in the

preparation of financial statements have also been presented in the report. The relevant

extracts are as below.

The Wesfarmers index of the annual report presents link to the financial statements and the

relevant notes as under:

The Woolworths index also provides the link as below:

The investors needs to understand the relevance of the financial information in terms of

performance with the previous years and the reasons for the growth. Woolworths have

analysed the current year performance as depicted in Appendix 1. The company has also

6

statement of other comprehensive income, statement of changes in equity and statement of

cash flows. In addition to these data the accounting policies and assumptions relied upon in the

preparation of financial statements have also been presented in the report. The relevant

extracts are as below.

The Wesfarmers index of the annual report presents link to the financial statements and the

relevant notes as under:

The Woolworths index also provides the link as below:

The investors needs to understand the relevance of the financial information in terms of

performance with the previous years and the reasons for the growth. Woolworths have

analysed the current year performance as depicted in Appendix 1. The company has also

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

provided a glimpse of future scale of operations through new store roll out plans as per

Appendix 2.

Wesfarmers have provided the analysis of financial performance as per Appendix 3. However,

the reports of Wesfarmers does not include an estimation of future plan in terms of new stores

to be opened as highlighted by Woolworths.

Impact of inclusion of Prudence in conceptual framework

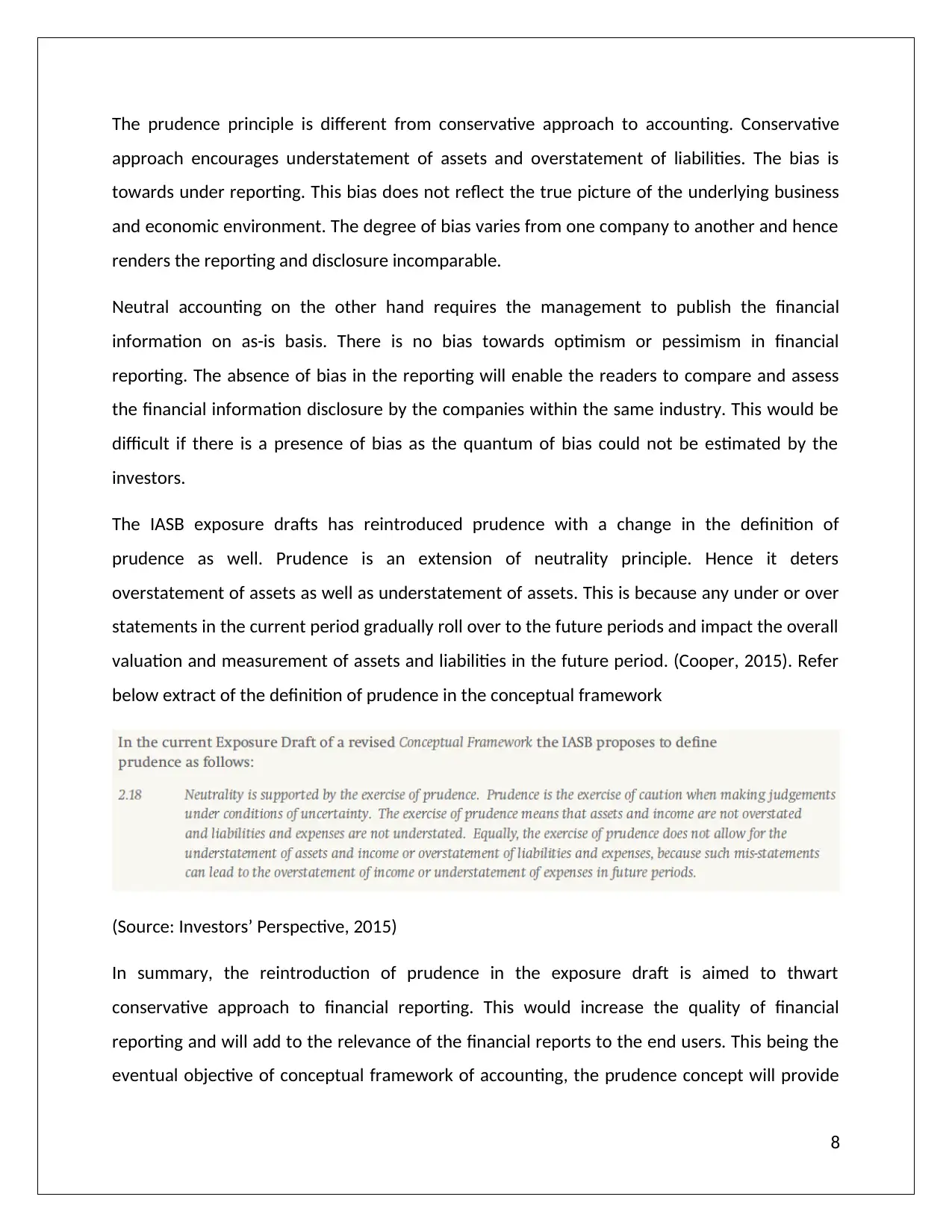

A financial statements must be prepared with due weightage to prudence. Prudence has been

one of the characteristics of the financial statements as required by the conceptual framework

of accounting until 2010. The International Accounting Standards Board has decided to

reintroduce the concept of prudence as one of the characteristics of financial statements. This

is to make the financial statements more useful the end users. Refer table below depicting the

inclusion and exclusion of the concept of prudence in the overall conceptual framework.

(Source: Investors’ Perspective, 2015)

The financial reporting is subject to bias by the management. Management tends to under-

report or over-report the financial performance to suit their incentive mechanism. This

variation in bias impact the neutrality characteristic of the financial statement. This difference

in bias reduces the comparability of financial information of two entities within the same

industry. Hence the concept of neutrality in addition to prudence is being propagated by IASB.

(PWC, 2015)

7

Appendix 2.

Wesfarmers have provided the analysis of financial performance as per Appendix 3. However,

the reports of Wesfarmers does not include an estimation of future plan in terms of new stores

to be opened as highlighted by Woolworths.

Impact of inclusion of Prudence in conceptual framework

A financial statements must be prepared with due weightage to prudence. Prudence has been

one of the characteristics of the financial statements as required by the conceptual framework

of accounting until 2010. The International Accounting Standards Board has decided to

reintroduce the concept of prudence as one of the characteristics of financial statements. This

is to make the financial statements more useful the end users. Refer table below depicting the

inclusion and exclusion of the concept of prudence in the overall conceptual framework.

(Source: Investors’ Perspective, 2015)

The financial reporting is subject to bias by the management. Management tends to under-

report or over-report the financial performance to suit their incentive mechanism. This

variation in bias impact the neutrality characteristic of the financial statement. This difference

in bias reduces the comparability of financial information of two entities within the same

industry. Hence the concept of neutrality in addition to prudence is being propagated by IASB.

(PWC, 2015)

7

The prudence principle is different from conservative approach to accounting. Conservative

approach encourages understatement of assets and overstatement of liabilities. The bias is

towards under reporting. This bias does not reflect the true picture of the underlying business

and economic environment. The degree of bias varies from one company to another and hence

renders the reporting and disclosure incomparable.

Neutral accounting on the other hand requires the management to publish the financial

information on as-is basis. There is no bias towards optimism or pessimism in financial

reporting. The absence of bias in the reporting will enable the readers to compare and assess

the financial information disclosure by the companies within the same industry. This would be

difficult if there is a presence of bias as the quantum of bias could not be estimated by the

investors.

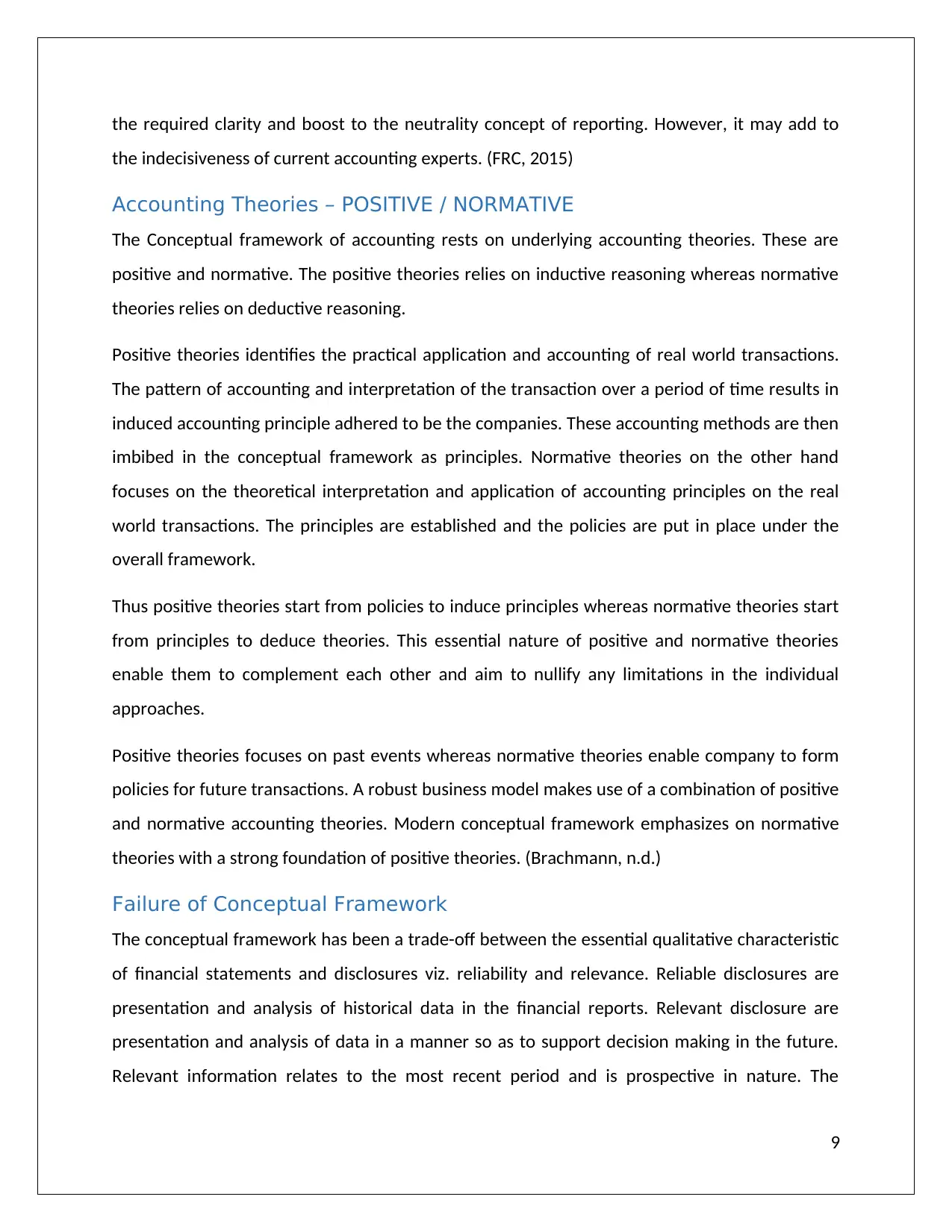

The IASB exposure drafts has reintroduced prudence with a change in the definition of

prudence as well. Prudence is an extension of neutrality principle. Hence it deters

overstatement of assets as well as understatement of assets. This is because any under or over

statements in the current period gradually roll over to the future periods and impact the overall

valuation and measurement of assets and liabilities in the future period. (Cooper, 2015). Refer

below extract of the definition of prudence in the conceptual framework

(Source: Investors’ Perspective, 2015)

In summary, the reintroduction of prudence in the exposure draft is aimed to thwart

conservative approach to financial reporting. This would increase the quality of financial

reporting and will add to the relevance of the financial reports to the end users. This being the

eventual objective of conceptual framework of accounting, the prudence concept will provide

8

approach encourages understatement of assets and overstatement of liabilities. The bias is

towards under reporting. This bias does not reflect the true picture of the underlying business

and economic environment. The degree of bias varies from one company to another and hence

renders the reporting and disclosure incomparable.

Neutral accounting on the other hand requires the management to publish the financial

information on as-is basis. There is no bias towards optimism or pessimism in financial

reporting. The absence of bias in the reporting will enable the readers to compare and assess

the financial information disclosure by the companies within the same industry. This would be

difficult if there is a presence of bias as the quantum of bias could not be estimated by the

investors.

The IASB exposure drafts has reintroduced prudence with a change in the definition of

prudence as well. Prudence is an extension of neutrality principle. Hence it deters

overstatement of assets as well as understatement of assets. This is because any under or over

statements in the current period gradually roll over to the future periods and impact the overall

valuation and measurement of assets and liabilities in the future period. (Cooper, 2015). Refer

below extract of the definition of prudence in the conceptual framework

(Source: Investors’ Perspective, 2015)

In summary, the reintroduction of prudence in the exposure draft is aimed to thwart

conservative approach to financial reporting. This would increase the quality of financial

reporting and will add to the relevance of the financial reports to the end users. This being the

eventual objective of conceptual framework of accounting, the prudence concept will provide

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the required clarity and boost to the neutrality concept of reporting. However, it may add to

the indecisiveness of current accounting experts. (FRC, 2015)

Accounting Theories – POSITIVE / NORMATIVE

The Conceptual framework of accounting rests on underlying accounting theories. These are

positive and normative. The positive theories relies on inductive reasoning whereas normative

theories relies on deductive reasoning.

Positive theories identifies the practical application and accounting of real world transactions.

The pattern of accounting and interpretation of the transaction over a period of time results in

induced accounting principle adhered to be the companies. These accounting methods are then

imbibed in the conceptual framework as principles. Normative theories on the other hand

focuses on the theoretical interpretation and application of accounting principles on the real

world transactions. The principles are established and the policies are put in place under the

overall framework.

Thus positive theories start from policies to induce principles whereas normative theories start

from principles to deduce theories. This essential nature of positive and normative theories

enable them to complement each other and aim to nullify any limitations in the individual

approaches.

Positive theories focuses on past events whereas normative theories enable company to form

policies for future transactions. A robust business model makes use of a combination of positive

and normative accounting theories. Modern conceptual framework emphasizes on normative

theories with a strong foundation of positive theories. (Brachmann, n.d.)

Failure of Conceptual Framework

The conceptual framework has been a trade-off between the essential qualitative characteristic

of financial statements and disclosures viz. reliability and relevance. Reliable disclosures are

presentation and analysis of historical data in the financial reports. Relevant disclosure are

presentation and analysis of data in a manner so as to support decision making in the future.

Relevant information relates to the most recent period and is prospective in nature. The

9

the indecisiveness of current accounting experts. (FRC, 2015)

Accounting Theories – POSITIVE / NORMATIVE

The Conceptual framework of accounting rests on underlying accounting theories. These are

positive and normative. The positive theories relies on inductive reasoning whereas normative

theories relies on deductive reasoning.

Positive theories identifies the practical application and accounting of real world transactions.

The pattern of accounting and interpretation of the transaction over a period of time results in

induced accounting principle adhered to be the companies. These accounting methods are then

imbibed in the conceptual framework as principles. Normative theories on the other hand

focuses on the theoretical interpretation and application of accounting principles on the real

world transactions. The principles are established and the policies are put in place under the

overall framework.

Thus positive theories start from policies to induce principles whereas normative theories start

from principles to deduce theories. This essential nature of positive and normative theories

enable them to complement each other and aim to nullify any limitations in the individual

approaches.

Positive theories focuses on past events whereas normative theories enable company to form

policies for future transactions. A robust business model makes use of a combination of positive

and normative accounting theories. Modern conceptual framework emphasizes on normative

theories with a strong foundation of positive theories. (Brachmann, n.d.)

Failure of Conceptual Framework

The conceptual framework has been a trade-off between the essential qualitative characteristic

of financial statements and disclosures viz. reliability and relevance. Reliable disclosures are

presentation and analysis of historical data in the financial reports. Relevant disclosure are

presentation and analysis of data in a manner so as to support decision making in the future.

Relevant information relates to the most recent period and is prospective in nature. The

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

conceptual framework has failed to identify the appropriate trade-off between reliable and

relevant disclosure. This is partly due to inability of the company and the management to verify

the relevant data. This makes it non-reliable.

As users become more used to the financial reporting, they may start to rely on it for financial

decisions. However, since the conceptual framework is more rule based, the resultant

disclosures have increasingly become more and more complex. This undermines the overall

objective of the conceptual framework of accounting. (Byron and Lawrence, 2012)

The focus of the reporting need to shift from mere profitability to the reliability and relevance.

The efficiency of business operations and its analysis with the industry best practices should be

included in the overall reporting to make it more meaningful for the end users.

Is regulation the key to resolve issues?

The conceptual framework is in principle applicable to the global accounting practices. However

various nations have specific regulations in place which slightly alter the implementation and

interpretation of the conceptual framework of accounting. These regulations are in place to

make the financial reporting more meaningful the economic environment of the country and

the investor’s expectation. Regulation at the micro level may seem appropriate as it enhance

the end-user value of the financial reporting. However, at the macro level the reporting would

not be comparable. The accounting standard used for reporting in Australia would slightly differ

from those applied in India. India is still in transition phase towards adoption of IFRS. Thus the

reports of two companies within these different regulatory framework would not be

comparable.

Recommendations

The objective of conceptual framework of accounting should be achieved by making the

financial reporting more relevant and reliable. The IASB has taken the right step in the direction

by reintroducing the concept of prudence with a bias towards neutrality. Another step to be

taken is to make the accounting standards more principle driven rather than rule driven.

Principle based accounting standards ensure exercise of appropriate professional judgement by

10

relevant disclosure. This is partly due to inability of the company and the management to verify

the relevant data. This makes it non-reliable.

As users become more used to the financial reporting, they may start to rely on it for financial

decisions. However, since the conceptual framework is more rule based, the resultant

disclosures have increasingly become more and more complex. This undermines the overall

objective of the conceptual framework of accounting. (Byron and Lawrence, 2012)

The focus of the reporting need to shift from mere profitability to the reliability and relevance.

The efficiency of business operations and its analysis with the industry best practices should be

included in the overall reporting to make it more meaningful for the end users.

Is regulation the key to resolve issues?

The conceptual framework is in principle applicable to the global accounting practices. However

various nations have specific regulations in place which slightly alter the implementation and

interpretation of the conceptual framework of accounting. These regulations are in place to

make the financial reporting more meaningful the economic environment of the country and

the investor’s expectation. Regulation at the micro level may seem appropriate as it enhance

the end-user value of the financial reporting. However, at the macro level the reporting would

not be comparable. The accounting standard used for reporting in Australia would slightly differ

from those applied in India. India is still in transition phase towards adoption of IFRS. Thus the

reports of two companies within these different regulatory framework would not be

comparable.

Recommendations

The objective of conceptual framework of accounting should be achieved by making the

financial reporting more relevant and reliable. The IASB has taken the right step in the direction

by reintroducing the concept of prudence with a bias towards neutrality. Another step to be

taken is to make the accounting standards more principle driven rather than rule driven.

Principle based accounting standards ensure exercise of appropriate professional judgement by

10

the accounting profession globally. A rule based accounting standard may not consider a

particular characteristic of the transactions at the time of inception and might be rendered false

in its application. Hence a principle based approach to development of accounting standards is

recommended. Further, the companies should be proactive in adopting sustainable reporting

practices to value-add the usefulness of the financial information. The earlier concept of

conservative approach should not be encouraged or be allowed in the revised conceptual

framework as it will cause the benefits of neutral accounting to fade away.

Conclusion

The accounting framework has evolved over the period of time with the technological

innovations and increased investor’s expectation of the usefulness of the financial reporting.

The conceptual framework has been altered by the IASB to make it more meaningful to the

changing scenarios. It has done so to remove the limitations identified in the implementation of

the framework. The reintroduction of the concept of the prudence is viewed as a step in the

right direction. It aims to set correct the path for appropriate focus on the principle of

neutrality in the financial statements. The investor’s community has appreciated the removal of

conservative approach to the financial reporting as it has failed to add value to the

comparability aspect of the financial reporting. Investors feel that they have the right business

acumen to understand the as-is financial reporting by the management and feel no need for it

to be smoothened. This will reduce the effectiveness of the financial reporting.

11

particular characteristic of the transactions at the time of inception and might be rendered false

in its application. Hence a principle based approach to development of accounting standards is

recommended. Further, the companies should be proactive in adopting sustainable reporting

practices to value-add the usefulness of the financial information. The earlier concept of

conservative approach should not be encouraged or be allowed in the revised conceptual

framework as it will cause the benefits of neutral accounting to fade away.

Conclusion

The accounting framework has evolved over the period of time with the technological

innovations and increased investor’s expectation of the usefulness of the financial reporting.

The conceptual framework has been altered by the IASB to make it more meaningful to the

changing scenarios. It has done so to remove the limitations identified in the implementation of

the framework. The reintroduction of the concept of the prudence is viewed as a step in the

right direction. It aims to set correct the path for appropriate focus on the principle of

neutrality in the financial statements. The investor’s community has appreciated the removal of

conservative approach to the financial reporting as it has failed to add value to the

comparability aspect of the financial reporting. Investors feel that they have the right business

acumen to understand the as-is financial reporting by the management and feel no need for it

to be smoothened. This will reduce the effectiveness of the financial reporting.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

![Report: Contemporary Issues in Accounting - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fzz%2F9509ff46c136422d929242036a52e1cb.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.