Customer Relationship Management Report: CBA Bank and Australian Banks

VerifiedAdded on 2022/10/19

|20

|6348

|500

Report

AI Summary

This report provides a comprehensive analysis of Customer Relationship Management (CRM) within the context of the Australian banking sector, with a specific focus on the Commonwealth Bank of Australia (CBA). The report begins with an overview of the Australian banking industry, including market capitalization, organizational goals, and capabilities of major banks like Westpac, ANZ, and NAB. It then delves into CBA's CRM strategies, examining operational, analytical, strategic, and collaborative approaches. The report also investigates the impact of the Royal Banking Commission on banks' CRM practices and customer relationships. Key areas covered include market analysis, competitive analysis, customer strategies, and the influence of technological advancements. The report highlights CBA's innovative products, customer satisfaction levels, and competitive positioning within the Australian banking market. The report also analyzes the impact of the Royal Commission on the CRM of banks. Finally, the report provides conclusions based on the research and analysis conducted.

CUSTOMER RELATIONSHIP MANAGEMENT REPORT

Name of Student

Name of Professor

Authors Note

Page | 1

Name of Student

Name of Professor

Authors Note

Page | 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report is focused on three major sections as the first section is on the banking industry and

its’ growth for the last twenty years, second section is on the CRM use of the chosen CBA bank

and the third section is the impact of Royal Commission of Bank on the major banks’

relationships with their customers. Australia’s four major banks comprise four of the seven on

local stock exchange in Australia having a market cap of AU$360 billion combined. Four

international banks in Australia are Westpac, National Australia Bank (NAB), Australia and New

Zealand Banking Group (ANZ) and Commonwealth Bank of Australia. Combined assets of these

banking giants may cross AU$ 3.6 trillion. CBA introduces the CRM and several facilities

including the Tap and Pay mobile app which is instrumental in changing the way payments are

being done. It has also launched ‘MyWealth’ which functions as a wealth management tool for

customers. The bank has also automated high-value payments. The analytics team of the

company deploys a number of software for managing and analysing the overall data of the bank

such as Data Stage, Ab Initio, Oracle BI, Tableau, R, SAS and Pega Decisioning. CBA has

successfully tackled competition by introducing a number of innovative products and services.

The workforce of CBA is also trained to be highly skilled. CBA has acquired 25% of the ASB

bank. The bank has established cooperation agreements with two banks in China namely

Hangzhou Commercial Bank and Jinan Commercial bank. The bank has also entered into a

partnership with Aussie Home Loans where it owns 80% shares. The development of loyalty

incorporates the sustaining and building the relationship with the customer which lead to the

repeated of purchasing the service. The customers’ loyalty can be proved with the continuous

stay of the customer with the same bank for a longer period of time along with buying the

policies frequently. CBA must focus on developing a wholesome strategy which addresses these

issues to rise significantly above its competitors. CBA needs to use CRM across all the

departments and it can prioritise customers and prospects.

Page | 2

This report is focused on three major sections as the first section is on the banking industry and

its’ growth for the last twenty years, second section is on the CRM use of the chosen CBA bank

and the third section is the impact of Royal Commission of Bank on the major banks’

relationships with their customers. Australia’s four major banks comprise four of the seven on

local stock exchange in Australia having a market cap of AU$360 billion combined. Four

international banks in Australia are Westpac, National Australia Bank (NAB), Australia and New

Zealand Banking Group (ANZ) and Commonwealth Bank of Australia. Combined assets of these

banking giants may cross AU$ 3.6 trillion. CBA introduces the CRM and several facilities

including the Tap and Pay mobile app which is instrumental in changing the way payments are

being done. It has also launched ‘MyWealth’ which functions as a wealth management tool for

customers. The bank has also automated high-value payments. The analytics team of the

company deploys a number of software for managing and analysing the overall data of the bank

such as Data Stage, Ab Initio, Oracle BI, Tableau, R, SAS and Pega Decisioning. CBA has

successfully tackled competition by introducing a number of innovative products and services.

The workforce of CBA is also trained to be highly skilled. CBA has acquired 25% of the ASB

bank. The bank has established cooperation agreements with two banks in China namely

Hangzhou Commercial Bank and Jinan Commercial bank. The bank has also entered into a

partnership with Aussie Home Loans where it owns 80% shares. The development of loyalty

incorporates the sustaining and building the relationship with the customer which lead to the

repeated of purchasing the service. The customers’ loyalty can be proved with the continuous

stay of the customer with the same bank for a longer period of time along with buying the

policies frequently. CBA must focus on developing a wholesome strategy which addresses these

issues to rise significantly above its competitors. CBA needs to use CRM across all the

departments and it can prioritise customers and prospects.

Page | 2

Table of Contents

Background of the project...............................................................................................................4

a) Research of the Australian Banking sector..................................................................................4

i) Company Analysis....................................................................................................................4

ii) Market Analysis/Customers....................................................................................................6

iii) Competitive Analysis.............................................................................................................7

iv) External Environment............................................................................................................9

b) Customer Strategies and CRM methods...................................................................................10

i) Operational.............................................................................................................................10

ii) Analytical..............................................................................................................................11

iii) Strategic................................................................................................................................11

iv) Collaborative........................................................................................................................12

(c) Royal Banking Commission (RCB) and its impact on the CRM of banks in Australia..........13

Conclusions....................................................................................................................................16

Reference.......................................................................................................................................17

Page | 3

Background of the project...............................................................................................................4

a) Research of the Australian Banking sector..................................................................................4

i) Company Analysis....................................................................................................................4

ii) Market Analysis/Customers....................................................................................................6

iii) Competitive Analysis.............................................................................................................7

iv) External Environment............................................................................................................9

b) Customer Strategies and CRM methods...................................................................................10

i) Operational.............................................................................................................................10

ii) Analytical..............................................................................................................................11

iii) Strategic................................................................................................................................11

iv) Collaborative........................................................................................................................12

(c) Royal Banking Commission (RCB) and its impact on the CRM of banks in Australia..........13

Conclusions....................................................................................................................................16

Reference.......................................................................................................................................17

Page | 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Background of the project

In the first part of the study, overall banking sector of Australia is the primary focus, therefore,

market situation of all the four banks are given with examples. Banking industry in Australia is

very strong as four major banks in Australia are performing well. In order to understand the

major operational elements of CRM which govern the banking sector of Australia, the

Commonwealth Bank of Australia has been chosen. It is a multinational bank in Australia which

provides various services such as investment, insurance, superannuation and funds management.

The project report is focussed on exploring and analysing the CRM or customer relationship

strategies of the bank to identify the major components which influence the relationship

between the customer and the bank. The project also researches and analyses the recent events

which have taken place in the Australian banking sector. It attempts to establish a clear

relationship between the events and in what manner they might impact the relationship between

the customer and the bank. In the final section, impact of Royal Banking Commissions on banks

of Australia is explained. It has maintained strategic agreements with several banks and has

served customers successfully despite facing a number of controversies during the last few years.

a) Research of the Australian Banking sector

i) Company Analysis

Australia’s four major banks comprise four of the seven on local stock exchange in Australia having a

market cap of AU$360 billion combined. Four international banks in Australia are Westpac, National

Australia Bank (NAB), Australia and New Zealand Banking Group (ANZ) and Commonwealth Bank of

Australia. Combined assets of these banking giants may cross AU$ 3.6 trillion (Adapa and Roy 2018).

Organisational Goals and Objectives

The organisational goals of the company are ambitious and diversified where the banks of

Australia is focussed upon providing every kind of financial services and solutions to its

customers. These activities are irrespective of the expectations and needs of the customer since

the bank provides a plethora of services such as providing loans to small and medium-sized

Page | 4

In the first part of the study, overall banking sector of Australia is the primary focus, therefore,

market situation of all the four banks are given with examples. Banking industry in Australia is

very strong as four major banks in Australia are performing well. In order to understand the

major operational elements of CRM which govern the banking sector of Australia, the

Commonwealth Bank of Australia has been chosen. It is a multinational bank in Australia which

provides various services such as investment, insurance, superannuation and funds management.

The project report is focussed on exploring and analysing the CRM or customer relationship

strategies of the bank to identify the major components which influence the relationship

between the customer and the bank. The project also researches and analyses the recent events

which have taken place in the Australian banking sector. It attempts to establish a clear

relationship between the events and in what manner they might impact the relationship between

the customer and the bank. In the final section, impact of Royal Banking Commissions on banks

of Australia is explained. It has maintained strategic agreements with several banks and has

served customers successfully despite facing a number of controversies during the last few years.

a) Research of the Australian Banking sector

i) Company Analysis

Australia’s four major banks comprise four of the seven on local stock exchange in Australia having a

market cap of AU$360 billion combined. Four international banks in Australia are Westpac, National

Australia Bank (NAB), Australia and New Zealand Banking Group (ANZ) and Commonwealth Bank of

Australia. Combined assets of these banking giants may cross AU$ 3.6 trillion (Adapa and Roy 2018).

Organisational Goals and Objectives

The organisational goals of the company are ambitious and diversified where the banks of

Australia is focussed upon providing every kind of financial services and solutions to its

customers. These activities are irrespective of the expectations and needs of the customer since

the bank provides a plethora of services such as providing loans to small and medium-sized

Page | 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

businesses, insights and tools concerned with businesses, retirement plans, and home loans at

competitive rates, term deposits and share trading to its customers.

Banking industry goal

The objectives of the banks lie in creating a customer based culture which ultimately enriches the

financial wellbeing of communities, businesses and people (Adapa and Roy 2018). The

advantage of the bank lies in the fact that it has been serving the customers of Australia and other

nations for a long time and is attuned to their respective expectations

Organisational Capabilities and Resources

The resources and capabilities of the bank lie in effective communication, customer focus,

culture and team and continuous improvements in services. In last 20 years, Australian banks

have improved their resources regarding the privacy, security, theft of information, data leakage

and app and website accessibility.

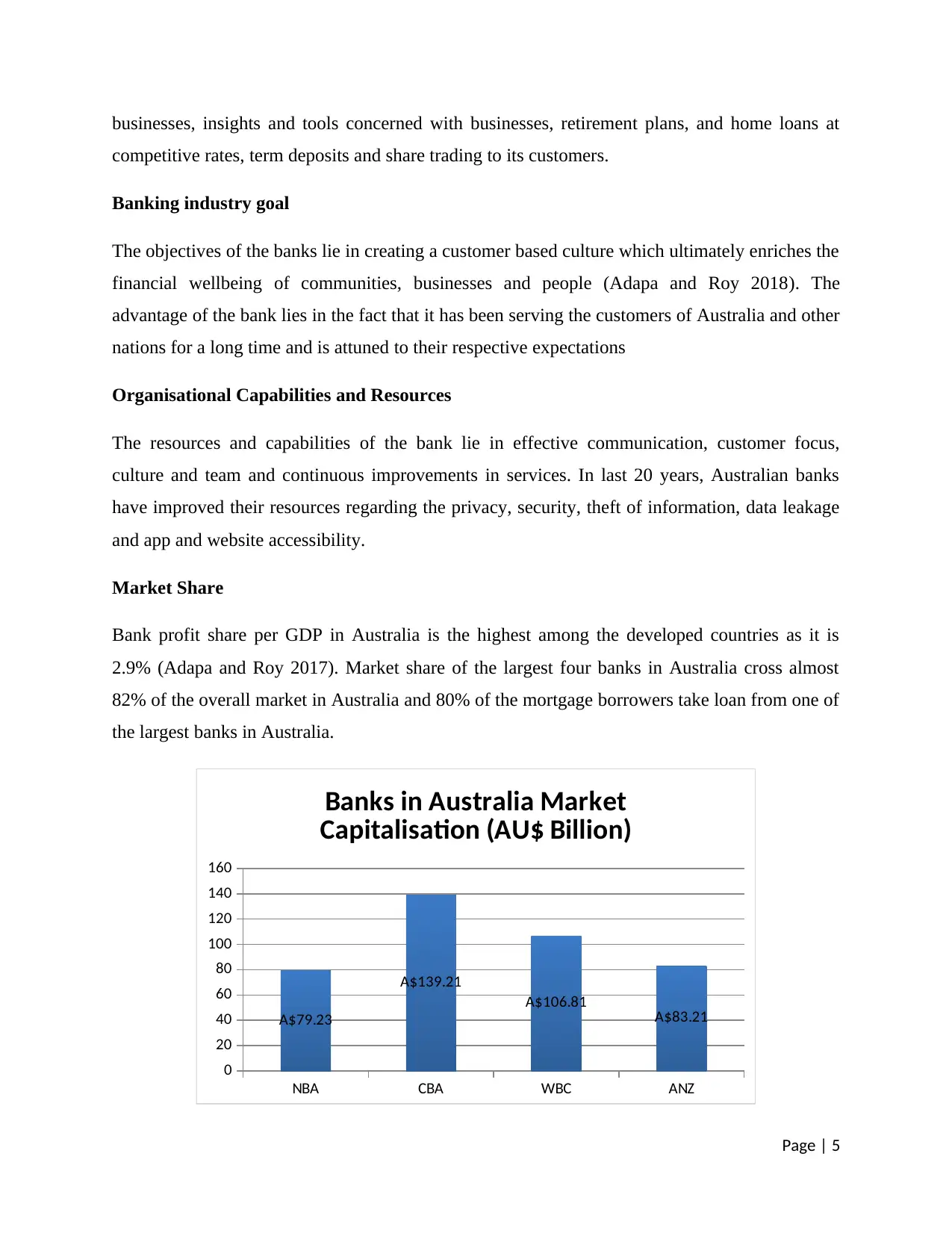

Market Share

Bank profit share per GDP in Australia is the highest among the developed countries as it is

2.9% (Adapa and Roy 2017). Market share of the largest four banks in Australia cross almost

82% of the overall market in Australia and 80% of the mortgage borrowers take loan from one of

the largest banks in Australia.

NBA CBA WBC ANZ

0

20

40

60

80

100

120

140

160

A$79.23

A$139.21

A$106.81 A$83.21

Banks in Australia Market

Capitalisation (AU$ Billion)

Page | 5

competitive rates, term deposits and share trading to its customers.

Banking industry goal

The objectives of the banks lie in creating a customer based culture which ultimately enriches the

financial wellbeing of communities, businesses and people (Adapa and Roy 2018). The

advantage of the bank lies in the fact that it has been serving the customers of Australia and other

nations for a long time and is attuned to their respective expectations

Organisational Capabilities and Resources

The resources and capabilities of the bank lie in effective communication, customer focus,

culture and team and continuous improvements in services. In last 20 years, Australian banks

have improved their resources regarding the privacy, security, theft of information, data leakage

and app and website accessibility.

Market Share

Bank profit share per GDP in Australia is the highest among the developed countries as it is

2.9% (Adapa and Roy 2017). Market share of the largest four banks in Australia cross almost

82% of the overall market in Australia and 80% of the mortgage borrowers take loan from one of

the largest banks in Australia.

NBA CBA WBC ANZ

0

20

40

60

80

100

120

140

160

A$79.23

A$139.21

A$106.81 A$83.21

Banks in Australia Market

Capitalisation (AU$ Billion)

Page | 5

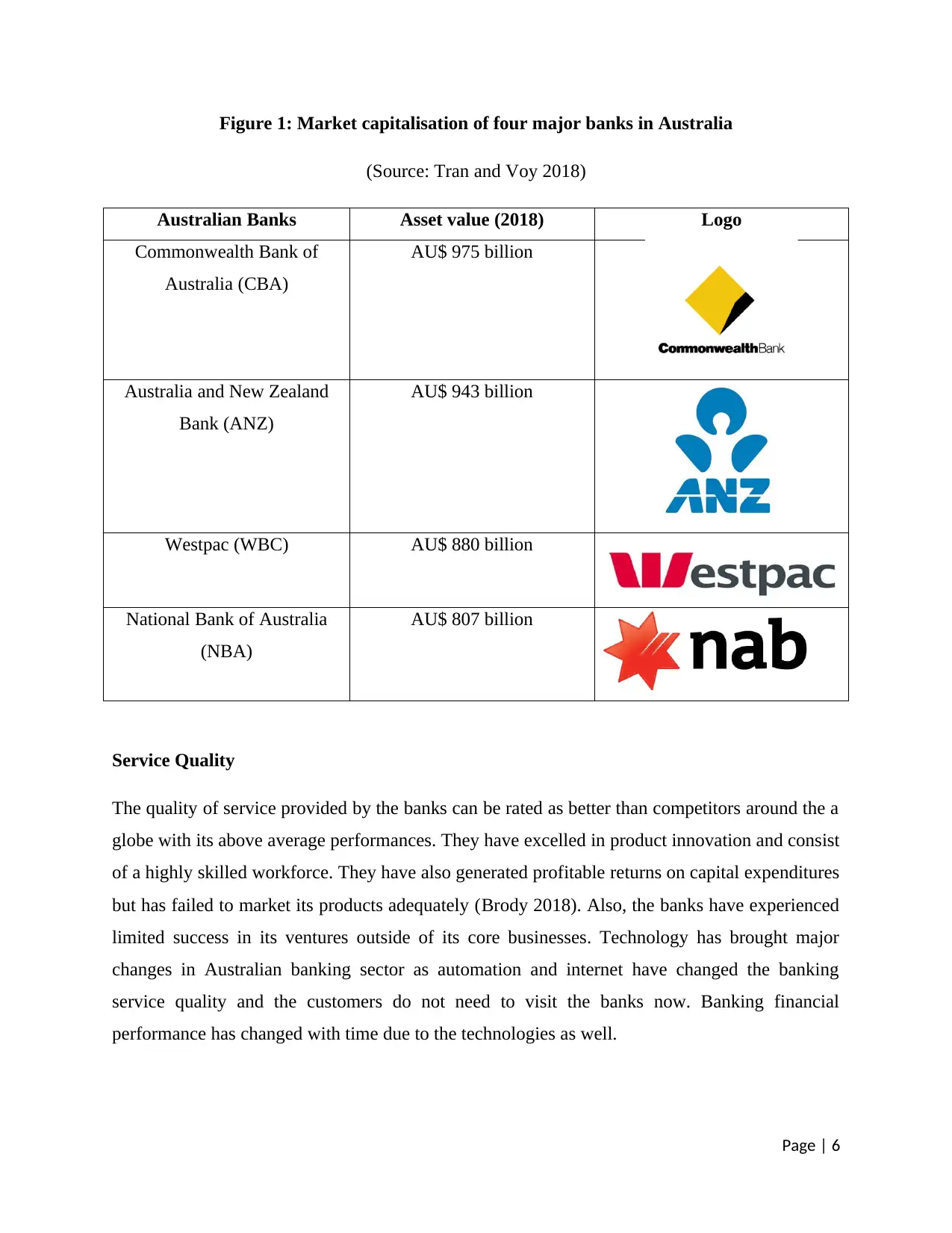

Figure 1: Market capitalisation of four major banks in Australia

(Source: Tran and Voy 2018)

Australian Banks Asset value (2018) Logo

Commonwealth Bank of

Australia (CBA)

AU$ 975 billion

Australia and New Zealand

Bank (ANZ)

AU$ 943 billion

Westpac (WBC) AU$ 880 billion

National Bank of Australia

(NBA)

AU$ 807 billion

Service Quality

The quality of service provided by the banks can be rated as better than competitors around the a

globe with its above average performances. They have excelled in product innovation and consist

of a highly skilled workforce. They have also generated profitable returns on capital expenditures

but has failed to market its products adequately (Brody 2018). Also, the banks have experienced

limited success in its ventures outside of its core businesses. Technology has brought major

changes in Australian banking sector as automation and internet have changed the banking

service quality and the customers do not need to visit the banks now. Banking financial

performance has changed with time due to the technologies as well.

Page | 6

(Source: Tran and Voy 2018)

Australian Banks Asset value (2018) Logo

Commonwealth Bank of

Australia (CBA)

AU$ 975 billion

Australia and New Zealand

Bank (ANZ)

AU$ 943 billion

Westpac (WBC) AU$ 880 billion

National Bank of Australia

(NBA)

AU$ 807 billion

Service Quality

The quality of service provided by the banks can be rated as better than competitors around the a

globe with its above average performances. They have excelled in product innovation and consist

of a highly skilled workforce. They have also generated profitable returns on capital expenditures

but has failed to market its products adequately (Brody 2018). Also, the banks have experienced

limited success in its ventures outside of its core businesses. Technology has brought major

changes in Australian banking sector as automation and internet have changed the banking

service quality and the customers do not need to visit the banks now. Banking financial

performance has changed with time due to the technologies as well.

Page | 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ii) Market Analysis/Customers

Despite the innovative services provided by the Commonwealth Bank of Australia the bank has

not promoted its products. The products are not positioned properly and they lack well defined

Unique Selling Proposition. However due to the strong brand image of the company the bank gas

successfully retained its position as a pioneer in customer satisfaction ahead of the other major

banks in Australia. The customer satisfaction as per reports of September 2017 remained at a

resilient percentage of 79.9%. The % of non-mortgage customers remains even higher at 80.4%.

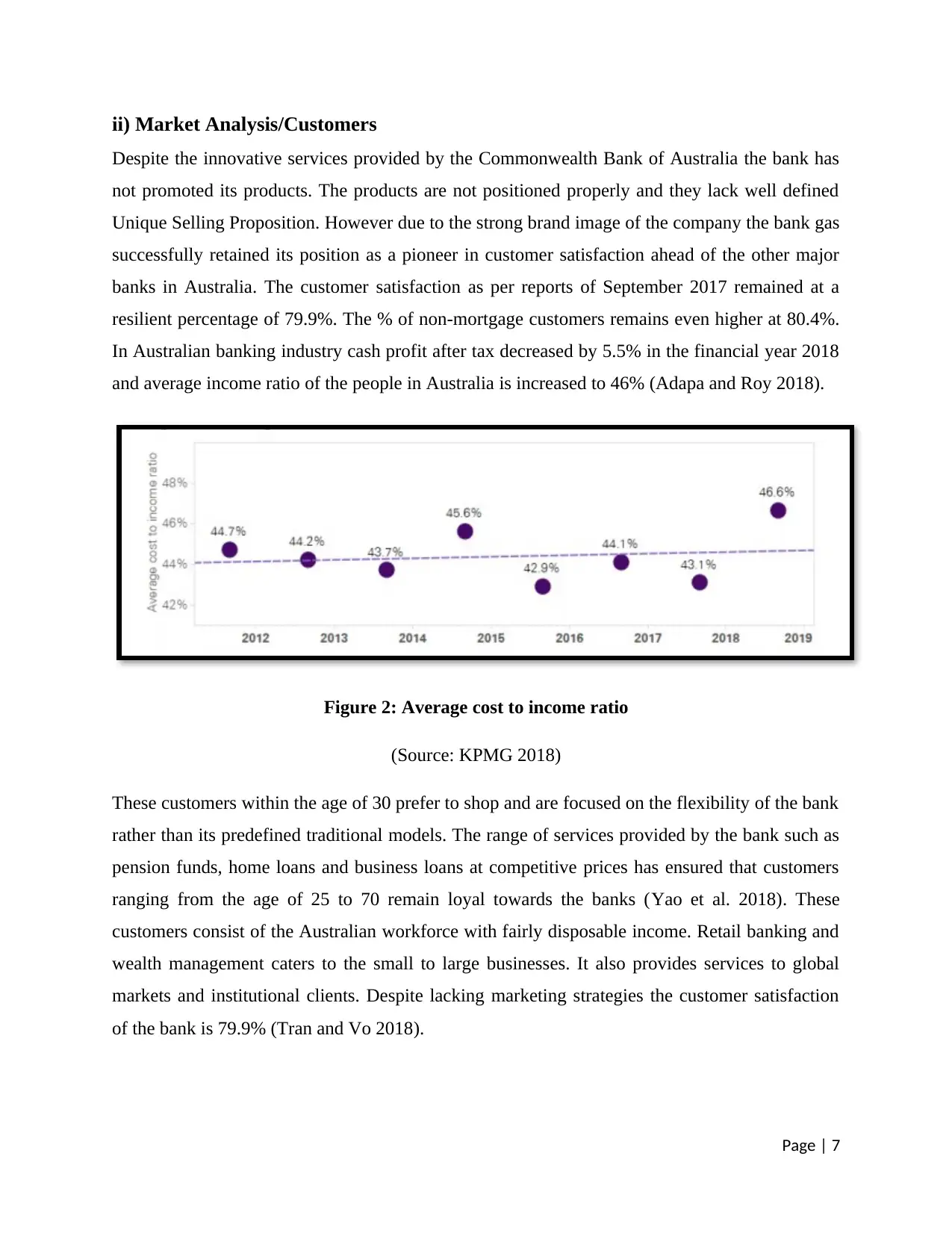

In Australian banking industry cash profit after tax decreased by 5.5% in the financial year 2018

and average income ratio of the people in Australia is increased to 46% (Adapa and Roy 2018).

Figure 2: Average cost to income ratio

(Source: KPMG 2018)

These customers within the age of 30 prefer to shop and are focused on the flexibility of the bank

rather than its predefined traditional models. The range of services provided by the bank such as

pension funds, home loans and business loans at competitive prices has ensured that customers

ranging from the age of 25 to 70 remain loyal towards the banks (Yao et al. 2018). These

customers consist of the Australian workforce with fairly disposable income. Retail banking and

wealth management caters to the small to large businesses. It also provides services to global

markets and institutional clients. Despite lacking marketing strategies the customer satisfaction

of the bank is 79.9% (Tran and Vo 2018).

Page | 7

Despite the innovative services provided by the Commonwealth Bank of Australia the bank has

not promoted its products. The products are not positioned properly and they lack well defined

Unique Selling Proposition. However due to the strong brand image of the company the bank gas

successfully retained its position as a pioneer in customer satisfaction ahead of the other major

banks in Australia. The customer satisfaction as per reports of September 2017 remained at a

resilient percentage of 79.9%. The % of non-mortgage customers remains even higher at 80.4%.

In Australian banking industry cash profit after tax decreased by 5.5% in the financial year 2018

and average income ratio of the people in Australia is increased to 46% (Adapa and Roy 2018).

Figure 2: Average cost to income ratio

(Source: KPMG 2018)

These customers within the age of 30 prefer to shop and are focused on the flexibility of the bank

rather than its predefined traditional models. The range of services provided by the bank such as

pension funds, home loans and business loans at competitive prices has ensured that customers

ranging from the age of 25 to 70 remain loyal towards the banks (Yao et al. 2018). These

customers consist of the Australian workforce with fairly disposable income. Retail banking and

wealth management caters to the small to large businesses. It also provides services to global

markets and institutional clients. Despite lacking marketing strategies the customer satisfaction

of the bank is 79.9% (Tran and Vo 2018).

Page | 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

iii) Competitive Analysis

Major Competitors

One of the top competitors in the market is CBA and Westpac. Westpac with its headquarters in

Sydney competes with CBA in the banking industry and generates 18.4 billion Australian dollars

more in terms of revenues compared to CBA. ANZ or the Australia and New Zealand banking

group is the second biggest bank with respect assets but has 3,847 fewer employees compared to

CBA (Heard, Menezes and Rambaldi 2018). The Australian Mutual Provident Society or AMP

is the third competitor as one of the largest shareholder registers in Australia.

Competitors’ goals, objectives and marketing mix

CBA, The Commonwealth Bank of Australia has its operations spread across the nations of the

United Kingdom, United States, Asia and New Zealand. The bank founded by the government in

1911 was completely privatised in 1996 and is one of the four biggest banks of Australia. In

1991 the organisation was listed in the Stock Exchange. The bank has diversified its business in

a number of areas such as trading in foreign currency, insurance and travel. It has revenue of

26.005 billion Australian dollars and about 51,800 employees (Commbank.com.au 2019). In

recent years the bank has also acquired stakes in Australian home loans company and financial

advisory companies thus establishing itself firmly in the financial market of Australia.

ANZ has more than 150 years of experience in the banking industry providing personal banking

services, loans to small, medium and corporate businesses. ANZ has also introduced an app for

wealth product customers to enable them to manage their earnings. ANZ provides 0% interest

rates to its customers for 16 months with the goal and objective of increasing its market shares.

Competitive price strategies are followed. ANZ's businesses are primarily focussed on the Asia

Pacific region deliberately overlooking the American and European market, unlike CBA. Robust

facilities like healthcare and other benefits are provided to employees (Bakir 2019). These

objectives are to create a world where communities and people thrive.

Westpac too like other banks of Australia provides merchant services, corporate services, home

loans, credit cards and insurance for its customers. Price provided by Westpac is competitive

rather beneficial insurance packages and policies are offered to customers. Westpac provides its

services in various parts of the world including Australia and New Zealand. Its reach is

Page | 8

Major Competitors

One of the top competitors in the market is CBA and Westpac. Westpac with its headquarters in

Sydney competes with CBA in the banking industry and generates 18.4 billion Australian dollars

more in terms of revenues compared to CBA. ANZ or the Australia and New Zealand banking

group is the second biggest bank with respect assets but has 3,847 fewer employees compared to

CBA (Heard, Menezes and Rambaldi 2018). The Australian Mutual Provident Society or AMP

is the third competitor as one of the largest shareholder registers in Australia.

Competitors’ goals, objectives and marketing mix

CBA, The Commonwealth Bank of Australia has its operations spread across the nations of the

United Kingdom, United States, Asia and New Zealand. The bank founded by the government in

1911 was completely privatised in 1996 and is one of the four biggest banks of Australia. In

1991 the organisation was listed in the Stock Exchange. The bank has diversified its business in

a number of areas such as trading in foreign currency, insurance and travel. It has revenue of

26.005 billion Australian dollars and about 51,800 employees (Commbank.com.au 2019). In

recent years the bank has also acquired stakes in Australian home loans company and financial

advisory companies thus establishing itself firmly in the financial market of Australia.

ANZ has more than 150 years of experience in the banking industry providing personal banking

services, loans to small, medium and corporate businesses. ANZ has also introduced an app for

wealth product customers to enable them to manage their earnings. ANZ provides 0% interest

rates to its customers for 16 months with the goal and objective of increasing its market shares.

Competitive price strategies are followed. ANZ's businesses are primarily focussed on the Asia

Pacific region deliberately overlooking the American and European market, unlike CBA. Robust

facilities like healthcare and other benefits are provided to employees (Bakir 2019). These

objectives are to create a world where communities and people thrive.

Westpac too like other banks of Australia provides merchant services, corporate services, home

loans, credit cards and insurance for its customers. Price provided by Westpac is competitive

rather beneficial insurance packages and policies are offered to customers. Westpac provides its

services in various parts of the world including Australia and New Zealand. Its reach is

Page | 8

somewhat limited compared to competitors. Marketing strategies of Westpac are resilient and

diverse based on sponsorships, media centres and commercials. Special incentives are awarded

to high performing employees. Highly automated processes are one of the key features of this

bank. Its objective is to be the largest service company in the world.

AMP provides services such as savings accounts, home loans, financial advice and insurance.

Price provided by AMP is competitive, especially in the mutual funds' investment sector. Most

of the operations are spread across Australia and New Zealand and serves the UK sector also as

part of a merging group. AMP established 170 years ago has a rich heritage but is currently

lagging behind due to poor marketing skills (Houston, Lee and Suntheim 2018). Digitalisation is

yet to be achieved in a complete manner. Health and insurance benefits are provided to

employees. AMP wishes to remain a pioneer in wealth management in Australia. Its objective is

to protect and create wealth for its consumers in different markets.

Marketing Mix of Banking sector in Australia

Product or service: Major services provided by the banks in Australia are the capital markets,

project finance, derivatives, loan and mortgage. The banks provide personal services and

insurance services to the customers.

Price: The banks in Australia take strategic and economic pricing strategies so that the customers

can take the services. However, all the services are premium to cater the needs of the customers.

Place: These banks have its ATM and branches across the Australia and globe. CBA has more

than 1131 branches in Australia, NBA has 1590 branches in Australia, ANZ has 600 branches

and 30 business centres and Westpac has 1200 branches in Australia.

Promotions: These banking giants take campaign strategies on social media and on the

promotional events so that they can reach large numbers of customers. The banks take the

strategies of social media promotions and television promotions to grab more customers.

Hoarding and billboards are part of the promotions.

iv) External Environment

Technology – Australia is one of the leaders in embracing new technologies. Technological

purchases are expected to amount to almost 65 billion in 2019. Cloud computing and artificial

Page | 9

diverse based on sponsorships, media centres and commercials. Special incentives are awarded

to high performing employees. Highly automated processes are one of the key features of this

bank. Its objective is to be the largest service company in the world.

AMP provides services such as savings accounts, home loans, financial advice and insurance.

Price provided by AMP is competitive, especially in the mutual funds' investment sector. Most

of the operations are spread across Australia and New Zealand and serves the UK sector also as

part of a merging group. AMP established 170 years ago has a rich heritage but is currently

lagging behind due to poor marketing skills (Houston, Lee and Suntheim 2018). Digitalisation is

yet to be achieved in a complete manner. Health and insurance benefits are provided to

employees. AMP wishes to remain a pioneer in wealth management in Australia. Its objective is

to protect and create wealth for its consumers in different markets.

Marketing Mix of Banking sector in Australia

Product or service: Major services provided by the banks in Australia are the capital markets,

project finance, derivatives, loan and mortgage. The banks provide personal services and

insurance services to the customers.

Price: The banks in Australia take strategic and economic pricing strategies so that the customers

can take the services. However, all the services are premium to cater the needs of the customers.

Place: These banks have its ATM and branches across the Australia and globe. CBA has more

than 1131 branches in Australia, NBA has 1590 branches in Australia, ANZ has 600 branches

and 30 business centres and Westpac has 1200 branches in Australia.

Promotions: These banking giants take campaign strategies on social media and on the

promotional events so that they can reach large numbers of customers. The banks take the

strategies of social media promotions and television promotions to grab more customers.

Hoarding and billboards are part of the promotions.

iv) External Environment

Technology – Australia is one of the leaders in embracing new technologies. Technological

purchases are expected to amount to almost 65 billion in 2019. Cloud computing and artificial

Page | 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

intelligence are changing the mode of operations in Australia (Gerard and Johnston 2019). This

beyond doubt increases the expectations of the customers with respect to the banking services

provided. The bank must make investments to these trends and expectations.

Social Trend – In terms of health, wealth and quality of life Australia is one of the nations which

are leagues ahead of others. The life expectancy is high (Pilbeam and Sarantidis 2019). It is a

multicultural nation focussing on education affect the GDP of the country in a positive manner.

While this is beneficial for the banking industry it must be noted that the decline in working age

population is drawback affecting all businesses.

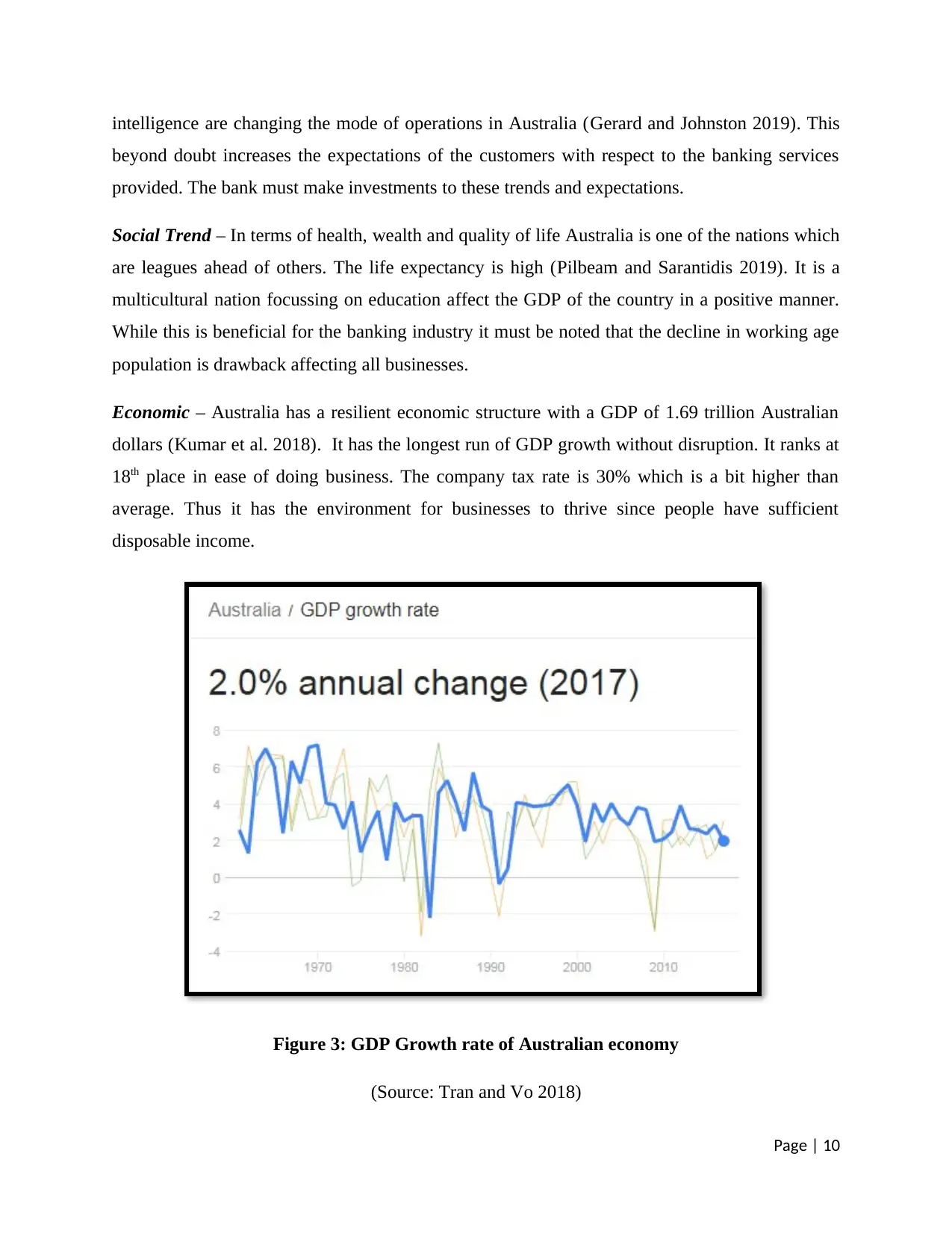

Economic – Australia has a resilient economic structure with a GDP of 1.69 trillion Australian

dollars (Kumar et al. 2018). It has the longest run of GDP growth without disruption. It ranks at

18th place in ease of doing business. The company tax rate is 30% which is a bit higher than

average. Thus it has the environment for businesses to thrive since people have sufficient

disposable income.

Figure 3: GDP Growth rate of Australian economy

(Source: Tran and Vo 2018)

Page | 10

beyond doubt increases the expectations of the customers with respect to the banking services

provided. The bank must make investments to these trends and expectations.

Social Trend – In terms of health, wealth and quality of life Australia is one of the nations which

are leagues ahead of others. The life expectancy is high (Pilbeam and Sarantidis 2019). It is a

multicultural nation focussing on education affect the GDP of the country in a positive manner.

While this is beneficial for the banking industry it must be noted that the decline in working age

population is drawback affecting all businesses.

Economic – Australia has a resilient economic structure with a GDP of 1.69 trillion Australian

dollars (Kumar et al. 2018). It has the longest run of GDP growth without disruption. It ranks at

18th place in ease of doing business. The company tax rate is 30% which is a bit higher than

average. Thus it has the environment for businesses to thrive since people have sufficient

disposable income.

Figure 3: GDP Growth rate of Australian economy

(Source: Tran and Vo 2018)

Page | 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Political and Legal Factors – The Prime Minister is concerned with taking all the decisions of

the nation formally ruled by Elizabeth II. It has a stable political environment which has attracted

some mild criticism due to racial discrimination. The nation has fair consumer laws and trading

laws. The country is governed by the Fair Works Act of 2009 (Masa’deh et al. 2018). There is

also protection of intellectual property laws. Any company looking to expand its operations must

abide by these to avoid litigations.

b) Customer Strategies and CRM methods

i) Operational

The bank has introduced several facilities including the Tap and Pay mobile app which is

instrumental in changing the way payments are being done. It has also launched ‘MyWealth’

which functions as a wealth management tool for customers. The bank has also automated high-

value payments. While high payments require a huge amount of manual effort on the part of the

employees the bank has successfully managed to automate it preventing bottlenecks. A strong

SWIFT network has been maintained and developed for this purpose (Kieżel and Stefańska

2019).CBA uses multiple strategies to establish its presence in social media. CBA provides a

gamut of services for its customers and these were adequately promoted through campaigns and

posts in social media. However, the posts are significantly lesser in number compared to its

rivals. The website of the bank is easy to use and provides easy access to multiple services. CBA

has exercised sufficient caution in using Artificial Intelligence for its compliance services.

However, the senior management at CBA is gradually accepting this new concept after

successful proofs have been established. New regulatory techniques are being used which are

significantly reducing the compliance costs. Artificial Intelligence is gradually being introduced

to increase accuracy and reduce costs of compliance (Giovanis, Assimakopoulos and Sarmaniotis

2018). Powered chatbots (Ceba) are being used to perform simple banking activities.

ii) Analytical

The CBA uses a gamut of services from its vendors with its commitment to provide exceptional

customer services through conscientious software which enhance business operations. It uses

Customer Relationship Management software to keep track of the preferences of each customer.

Robotic Process Automation Software is used to rapidly deploy simple activities and save

Page | 11

the nation formally ruled by Elizabeth II. It has a stable political environment which has attracted

some mild criticism due to racial discrimination. The nation has fair consumer laws and trading

laws. The country is governed by the Fair Works Act of 2009 (Masa’deh et al. 2018). There is

also protection of intellectual property laws. Any company looking to expand its operations must

abide by these to avoid litigations.

b) Customer Strategies and CRM methods

i) Operational

The bank has introduced several facilities including the Tap and Pay mobile app which is

instrumental in changing the way payments are being done. It has also launched ‘MyWealth’

which functions as a wealth management tool for customers. The bank has also automated high-

value payments. While high payments require a huge amount of manual effort on the part of the

employees the bank has successfully managed to automate it preventing bottlenecks. A strong

SWIFT network has been maintained and developed for this purpose (Kieżel and Stefańska

2019).CBA uses multiple strategies to establish its presence in social media. CBA provides a

gamut of services for its customers and these were adequately promoted through campaigns and

posts in social media. However, the posts are significantly lesser in number compared to its

rivals. The website of the bank is easy to use and provides easy access to multiple services. CBA

has exercised sufficient caution in using Artificial Intelligence for its compliance services.

However, the senior management at CBA is gradually accepting this new concept after

successful proofs have been established. New regulatory techniques are being used which are

significantly reducing the compliance costs. Artificial Intelligence is gradually being introduced

to increase accuracy and reduce costs of compliance (Giovanis, Assimakopoulos and Sarmaniotis

2018). Powered chatbots (Ceba) are being used to perform simple banking activities.

ii) Analytical

The CBA uses a gamut of services from its vendors with its commitment to provide exceptional

customer services through conscientious software which enhance business operations. It uses

Customer Relationship Management software to keep track of the preferences of each customer.

Robotic Process Automation Software is used to rapidly deploy simple activities and save

Page | 11

manual effort. Data management and data science platforms are used to collate manage and

analyse data. Operational database management is being used to store and retrieve data according

to the relevant queries. The company utilises Hadoop based platform for managing big data

which is known as Omnia (Kieżel and Stefańska 2019). The analytics team of the company

deploys a number of software for managing and analysing the overall data of the bank such as

Data Stage, Ab Initio, Oracle BI, Tableau, R, SAS and Pega Decisioning (Sundaram, Thomas

and Agilandeeswari 2018). A few years ago the company was successful in implementing

overhauling of one of the strategic data centres in Sydney which has increased the power

efficiency and the lifespan of the project.

The CBA has completed a project involving transporting 9,000 virtual machines to a new private

cloud. The company is also contemplating the single cloud platform to reduce the load on

mainframe hardware. The project was implemented to make business units capable of self-

service and enhance the responsiveness of developers. CBA has embraced private clouds

technology since 2010 which has aided in reducing the cost to income ratios of the bank. CBA

uses a hybrid cloud technology where the public cloud takes on more workload depending upon

certain conditions (Kieżel and Stefańska 2018). Regarding cloud, most of the applications of

CBA are in-house.

iii) Strategic

CBA has always maintained customer satisfaction as the number one priority and commitment of

the company. The focus of the bank is on developing the commercial and retail business to

provide simpler solutions to the customer. The bank is making heavy investments in the category

of digital banking to retain customers. Savings accounts, loans and credit cards are provided to

customers. The fees of ATM have been reduced. To increase its reach the bank has expanded its

branch network which is more than currently 1,000 across the nation of Australia (Basha and

Rehana 2018). Customer segmentation is vital since it essential for banks to understand their

customers from a more granular perspective. The CBA with its variety of services targets

customers from middle to higher income group bearing a competent level of education. The

young consumers ranging from 25 to 35 years of age are the new emerging segments of the

customer. The bank provides business to small, medium and large businesses. With its pension

schemes and retirement plans, it can be said that the age ranging from 25-70 is the target group

Page | 12

analyse data. Operational database management is being used to store and retrieve data according

to the relevant queries. The company utilises Hadoop based platform for managing big data

which is known as Omnia (Kieżel and Stefańska 2019). The analytics team of the company

deploys a number of software for managing and analysing the overall data of the bank such as

Data Stage, Ab Initio, Oracle BI, Tableau, R, SAS and Pega Decisioning (Sundaram, Thomas

and Agilandeeswari 2018). A few years ago the company was successful in implementing

overhauling of one of the strategic data centres in Sydney which has increased the power

efficiency and the lifespan of the project.

The CBA has completed a project involving transporting 9,000 virtual machines to a new private

cloud. The company is also contemplating the single cloud platform to reduce the load on

mainframe hardware. The project was implemented to make business units capable of self-

service and enhance the responsiveness of developers. CBA has embraced private clouds

technology since 2010 which has aided in reducing the cost to income ratios of the bank. CBA

uses a hybrid cloud technology where the public cloud takes on more workload depending upon

certain conditions (Kieżel and Stefańska 2018). Regarding cloud, most of the applications of

CBA are in-house.

iii) Strategic

CBA has always maintained customer satisfaction as the number one priority and commitment of

the company. The focus of the bank is on developing the commercial and retail business to

provide simpler solutions to the customer. The bank is making heavy investments in the category

of digital banking to retain customers. Savings accounts, loans and credit cards are provided to

customers. The fees of ATM have been reduced. To increase its reach the bank has expanded its

branch network which is more than currently 1,000 across the nation of Australia (Basha and

Rehana 2018). Customer segmentation is vital since it essential for banks to understand their

customers from a more granular perspective. The CBA with its variety of services targets

customers from middle to higher income group bearing a competent level of education. The

young consumers ranging from 25 to 35 years of age are the new emerging segments of the

customer. The bank provides business to small, medium and large businesses. With its pension

schemes and retirement plans, it can be said that the age ranging from 25-70 is the target group

Page | 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.