Crowdspark Limited Audit: Risk Assessment and Misstatement Analysis

VerifiedAdded on 2022/11/14

|19

|4302

|440

Report

AI Summary

This report presents an audit of Crowdspark Limited, formerly Zulu Limited, a media and technology company operating in Australia. It identifies key business risks such as credit, market, and liquidity risks, and discusses the potential for material misstatements within the company's financial reporting. The audit risk model is applied to understand the relationship between control, inherent, and detection risks. An analytical procedure, including ratio analysis (net profit margin, current ratio, debt to equity, and total asset turnover), is performed to assess the company's financial performance from 2015 to 2017. The report also addresses the concept of materiality and identifies material accounts, relevant assertions, and appropriate audit procedures, concluding with recommendations for improved risk management and internal controls. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

1

Auditing

Auditing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

In the report, the various elements which are related to the audit have been considered in context

with the crowdspark limited. There is the consideration of the various business risks which are

involved and with that, the material misstatements which arise in the business have been

determined. The data which is required has been collected and with that, the ratio analysis has

been performed. There is the identification of the position of the business which is maintained.

The materiality concept which is involved has been taken into consideration and by that, all the

material accounts have been identified. The audit procedure and method of sampling which is

used has also been identified and complete procedures are performed in an adequate manner.

Executive summary

In the report, the various elements which are related to the audit have been considered in context

with the crowdspark limited. There is the consideration of the various business risks which are

involved and with that, the material misstatements which arise in the business have been

determined. The data which is required has been collected and with that, the ratio analysis has

been performed. There is the identification of the position of the business which is maintained.

The materiality concept which is involved has been taken into consideration and by that, all the

material accounts have been identified. The audit procedure and method of sampling which is

used has also been identified and complete procedures are performed in an adequate manner.

3

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Risks involved in business...............................................................................................................4

Material misstatement......................................................................................................................5

Audit risk model..............................................................................................................................6

The analytical procedure..................................................................................................................7

Materiality........................................................................................................................................8

Material accounts, assertions, audit procedures, and sampling.......................................................9

Conclusion.....................................................................................................................................16

References......................................................................................................................................18

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Risks involved in business...............................................................................................................4

Material misstatement......................................................................................................................5

Audit risk model..............................................................................................................................6

The analytical procedure..................................................................................................................7

Materiality........................................................................................................................................8

Material accounts, assertions, audit procedures, and sampling.......................................................9

Conclusion.....................................................................................................................................16

References......................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

The company involves various information, that is incorporated in the reports and analyzation of

the same is required to be made. For this, there is the need to carry the audit in the business in

which all of the important information will be incorporated. This report will be prepared on the

crowdspark limited. There will be consideration of the material misstatements which are

involved. There will be the identification of the main risks which are included in the company

and there will be a proper description which will be provided. The audit risk model will be taken

into consideration in which all of the risks and the relationships that exist among the will be

taken into account. There will be the calculation of the ratios which will be made under the

analytical procedure and the performance will be evaluated on the basis of that. The materiality

concept will be understood and all the material accounts will be identified on that basis. Various

other aspects will be covered in relation to them.

Risks involved in business

Crowdspark limited which was formerly known as the Zulu limited is involved in the media and

Technology Company. The company is operating in Australia and has performed there in various

aspects (Bloomberg, 2019). There are various services which are provided by the company and

they include brand publishing, related media and information services, multimedia content

distribution services and marketing services. The company has been listed on the Australian

stock exchange.

The company is performing various operations and in that process, there are various risks which

are faced by it. The explanation of the same is provided below in a detailed manner.

Credit risk: It is the risk which is involved that the company’s counterparty will not be able to

meet the obligations on time. The main risk is in relation to the dealings with the financial

institutions and the accounts receivables. If they will not be paying their amounts on time then it

will be affecting the balance of the company and so this is the risk for the business.

Market risk: The income of the business is affected by various external sources and in that, all of

the fluctuations which are taking place will be considered. The change in the interest rate and the

Introduction

The company involves various information, that is incorporated in the reports and analyzation of

the same is required to be made. For this, there is the need to carry the audit in the business in

which all of the important information will be incorporated. This report will be prepared on the

crowdspark limited. There will be consideration of the material misstatements which are

involved. There will be the identification of the main risks which are included in the company

and there will be a proper description which will be provided. The audit risk model will be taken

into consideration in which all of the risks and the relationships that exist among the will be

taken into account. There will be the calculation of the ratios which will be made under the

analytical procedure and the performance will be evaluated on the basis of that. The materiality

concept will be understood and all the material accounts will be identified on that basis. Various

other aspects will be covered in relation to them.

Risks involved in business

Crowdspark limited which was formerly known as the Zulu limited is involved in the media and

Technology Company. The company is operating in Australia and has performed there in various

aspects (Bloomberg, 2019). There are various services which are provided by the company and

they include brand publishing, related media and information services, multimedia content

distribution services and marketing services. The company has been listed on the Australian

stock exchange.

The company is performing various operations and in that process, there are various risks which

are faced by it. The explanation of the same is provided below in a detailed manner.

Credit risk: It is the risk which is involved that the company’s counterparty will not be able to

meet the obligations on time. The main risk is in relation to the dealings with the financial

institutions and the accounts receivables. If they will not be paying their amounts on time then it

will be affecting the balance of the company and so this is the risk for the business.

Market risk: The income of the business is affected by various external sources and in that, all of

the fluctuations which are taking place will be considered. The change in the interest rate and the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

exchange rate will be taken into account. This will be including the currency risk and interest

rate risk (Budescu, Peecher and Solomon, 2012). The company takes appropriate steps by which

the same can be managed.

Liquidity risk: All the businesses are required to maintain the liquidity so that they can deal with

the obligations appropriately. The group is also focusing on the same and in that it is maintaining

the liquidity of the business in an effective manner. The cash reserves are maintained and by that

the company will be able to meet with all the liabilities.

Material misstatement

The business involves various transactions to be recorded and in that prices, there are chances

that the errors will be made. In them, there are certain such errors which affect the business in an

effective manner (Bakker et al., 2014). They are identified as the material misstatements and

shall be taken into consideration in the performance of the audit procedure. This is the risk for

the business and so shall be taken into account in an effective manner and there shall be

undertaking of the proper process for the same which will help the company to overcome all of

the issues. The company is required to consider the inherent as well as the control risk which is

involved. In them, there is a need to consider all of the aspects. The inherent risk is involved in

the process of the company and that is difficult to be identified as the same is involved in the

processes. The company will be required to establish strong internal control for the same by

which the target will be attained and this will be required to be maintained in the long run. If the

internal control system which is operated by the company is weak then it will lead to an increase

in the inherent risk as the issues will not be identified in the required manner. It can be said that

they both will be reduced together and so the process shall be developed in such a manner.

In the company there is the need to keep the proper record of all the aspects and in that there will

be consideration of the elements by which the risks are affected. They will be considered so that

the reduction in the risk can be made possible. The number of the transactions which are

involved will have to be considered as if the number will be more than the chances of the errors

will also be more (Prawitt, Sharp and Wood, 2012). Due to this, it will be taken into account in

an essential manner. The risk is required to be identified so that the steps to eliminate them can

be undertaken. If this will not be made in an effective manner then the detection risk will be

exchange rate will be taken into account. This will be including the currency risk and interest

rate risk (Budescu, Peecher and Solomon, 2012). The company takes appropriate steps by which

the same can be managed.

Liquidity risk: All the businesses are required to maintain the liquidity so that they can deal with

the obligations appropriately. The group is also focusing on the same and in that it is maintaining

the liquidity of the business in an effective manner. The cash reserves are maintained and by that

the company will be able to meet with all the liabilities.

Material misstatement

The business involves various transactions to be recorded and in that prices, there are chances

that the errors will be made. In them, there are certain such errors which affect the business in an

effective manner (Bakker et al., 2014). They are identified as the material misstatements and

shall be taken into consideration in the performance of the audit procedure. This is the risk for

the business and so shall be taken into account in an effective manner and there shall be

undertaking of the proper process for the same which will help the company to overcome all of

the issues. The company is required to consider the inherent as well as the control risk which is

involved. In them, there is a need to consider all of the aspects. The inherent risk is involved in

the process of the company and that is difficult to be identified as the same is involved in the

processes. The company will be required to establish strong internal control for the same by

which the target will be attained and this will be required to be maintained in the long run. If the

internal control system which is operated by the company is weak then it will lead to an increase

in the inherent risk as the issues will not be identified in the required manner. It can be said that

they both will be reduced together and so the process shall be developed in such a manner.

In the company there is the need to keep the proper record of all the aspects and in that there will

be consideration of the elements by which the risks are affected. They will be considered so that

the reduction in the risk can be made possible. The number of the transactions which are

involved will have to be considered as if the number will be more than the chances of the errors

will also be more (Prawitt, Sharp and Wood, 2012). Due to this, it will be taken into account in

an essential manner. The risk is required to be identified so that the steps to eliminate them can

be undertaken. If this will not be made in an effective manner then the detection risk will be

6

involved. This is the risk of the identification and so company shall undertake the process by

which all the identification can be made in an appropriate manner.

There are many difficult systems which are undertaken in the company and due to them, the

chances of risk are increased. It is required that there shall be proper analyzation which shall be

made and the proper knowledge about the same shall be obtained. By this the company will be

able to take control of the system and also the detection will be made in an effective manner.

Audit risk model

The auditor will be performing the audit and in that, they will be considering all of the

information which is provided in the accounts and reports. They will be using the data and then

evaluate the company and its performance in an adequate manner. There will be a risk which will

be involved in that process in relation to the detection of all the aspects and that is considered as

the audit risk. It will be required that all of the risks which are involved are identified and

managed in an effective manner (Mock et al., 2012). There will be a determination of the relation

which exists among them so that they can be dealt in an appropriate manner. This will be done

with the help of the audit risk model and the same is explained below:

Audit risk model = control risk X inherent risk X detection risk

The main risks have been identified in the above section and they are required to be managed in

an effective manner. In that process, the company will be required to deal with all of the

situations in such a manner that the reduction in the risk involved can be made possible. There is

the inherent risk which is involved and in that there is the need to establish internal control in a

strong manner and for that internal control system of the company will be improved. With that

be in the correct condition the other risks will also be affected in a positive manner. The internal

control will help in managing the tasks in an appropriate manner and by that the inherent risk

will be controlled. The auditors will also be using the internal control as they will be made

available with the correct and accurate results. This will be making it possible for them to detect

all of the errors in an appropriate manner and by that the reduction in the detection risk will be

made. This helped in understanding the relation which exists in the company and all of the risks

involved. This is the risk of the identification and so company shall undertake the process by

which all the identification can be made in an appropriate manner.

There are many difficult systems which are undertaken in the company and due to them, the

chances of risk are increased. It is required that there shall be proper analyzation which shall be

made and the proper knowledge about the same shall be obtained. By this the company will be

able to take control of the system and also the detection will be made in an effective manner.

Audit risk model

The auditor will be performing the audit and in that, they will be considering all of the

information which is provided in the accounts and reports. They will be using the data and then

evaluate the company and its performance in an adequate manner. There will be a risk which will

be involved in that process in relation to the detection of all the aspects and that is considered as

the audit risk. It will be required that all of the risks which are involved are identified and

managed in an effective manner (Mock et al., 2012). There will be a determination of the relation

which exists among them so that they can be dealt in an appropriate manner. This will be done

with the help of the audit risk model and the same is explained below:

Audit risk model = control risk X inherent risk X detection risk

The main risks have been identified in the above section and they are required to be managed in

an effective manner. In that process, the company will be required to deal with all of the

situations in such a manner that the reduction in the risk involved can be made possible. There is

the inherent risk which is involved and in that there is the need to establish internal control in a

strong manner and for that internal control system of the company will be improved. With that

be in the correct condition the other risks will also be affected in a positive manner. The internal

control will help in managing the tasks in an appropriate manner and by that the inherent risk

will be controlled. The auditors will also be using the internal control as they will be made

available with the correct and accurate results. This will be making it possible for them to detect

all of the errors in an appropriate manner and by that the reduction in the detection risk will be

made. This helped in understanding the relation which exists in the company and all of the risks

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

which are involved in it.

Once the identification will be made by the auditor they will be required to take the appropriate

steps by which they can be reduced or eliminated. There will be an additional process which will

be designed and implemented in the company (Ettredge, Fuerherm and Li, 2014). The relation

which is present among them have been understood and by that, it can be said that if there will be

the elimination of one then others will also be reduced to a certain extent. The company will be

able to manage all of the tasks with the appropriate system in practice.

The company which is used here is crowdspark limited and in that there are various risks which

are involved and all of them are identified. They are taken into consideration and it has been

identified that company is having the proper risk management process which is undertaken by

the company (Cacho, alvarez Ochoa and Ramírez, 2012). With the help of that, it will be able to

manage all the risk in an appropriate manner and there will be a reduction and elimination of the

risk which is involved.

The analytical procedure

The financial information of the company is required to be analyzed in an effective manner and

for that, there is the need to use the analytical procedure. In this, the quantitative information is

taken into use and by the help of that, the performance of the company is analyzed in an effective

manner. The position of the business will be identified and there will be a determination of the

changes which are taking place in the same in the past few years. There will be ratios which will

be calculated and by that the change in the performance which is taking place will be identified.

The company will be able to measure the position and that will be used to take further decisions

in the business (Yoon, Hoogduin and Zhang, 2015). They will be taken in such a manner that the

improvement is made and the performance and position in the coming period will be improved.

There will also be the inclusion of the risk factor in the same and that will also be reduced with

the help of the policies which will be formulated. The calculation is made in this respect and it is

shown below.

Ratio Formula 2015 2016 2017

Net profit margin Income/sales *100 -1931.44% -589.33% -

409.70%

which are involved in it.

Once the identification will be made by the auditor they will be required to take the appropriate

steps by which they can be reduced or eliminated. There will be an additional process which will

be designed and implemented in the company (Ettredge, Fuerherm and Li, 2014). The relation

which is present among them have been understood and by that, it can be said that if there will be

the elimination of one then others will also be reduced to a certain extent. The company will be

able to manage all of the tasks with the appropriate system in practice.

The company which is used here is crowdspark limited and in that there are various risks which

are involved and all of them are identified. They are taken into consideration and it has been

identified that company is having the proper risk management process which is undertaken by

the company (Cacho, alvarez Ochoa and Ramírez, 2012). With the help of that, it will be able to

manage all the risk in an appropriate manner and there will be a reduction and elimination of the

risk which is involved.

The analytical procedure

The financial information of the company is required to be analyzed in an effective manner and

for that, there is the need to use the analytical procedure. In this, the quantitative information is

taken into use and by the help of that, the performance of the company is analyzed in an effective

manner. The position of the business will be identified and there will be a determination of the

changes which are taking place in the same in the past few years. There will be ratios which will

be calculated and by that the change in the performance which is taking place will be identified.

The company will be able to measure the position and that will be used to take further decisions

in the business (Yoon, Hoogduin and Zhang, 2015). They will be taken in such a manner that the

improvement is made and the performance and position in the coming period will be improved.

There will also be the inclusion of the risk factor in the same and that will also be reduced with

the help of the policies which will be formulated. The calculation is made in this respect and it is

shown below.

Ratio Formula 2015 2016 2017

Net profit margin Income/sales *100 -1931.44% -589.33% -

409.70%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

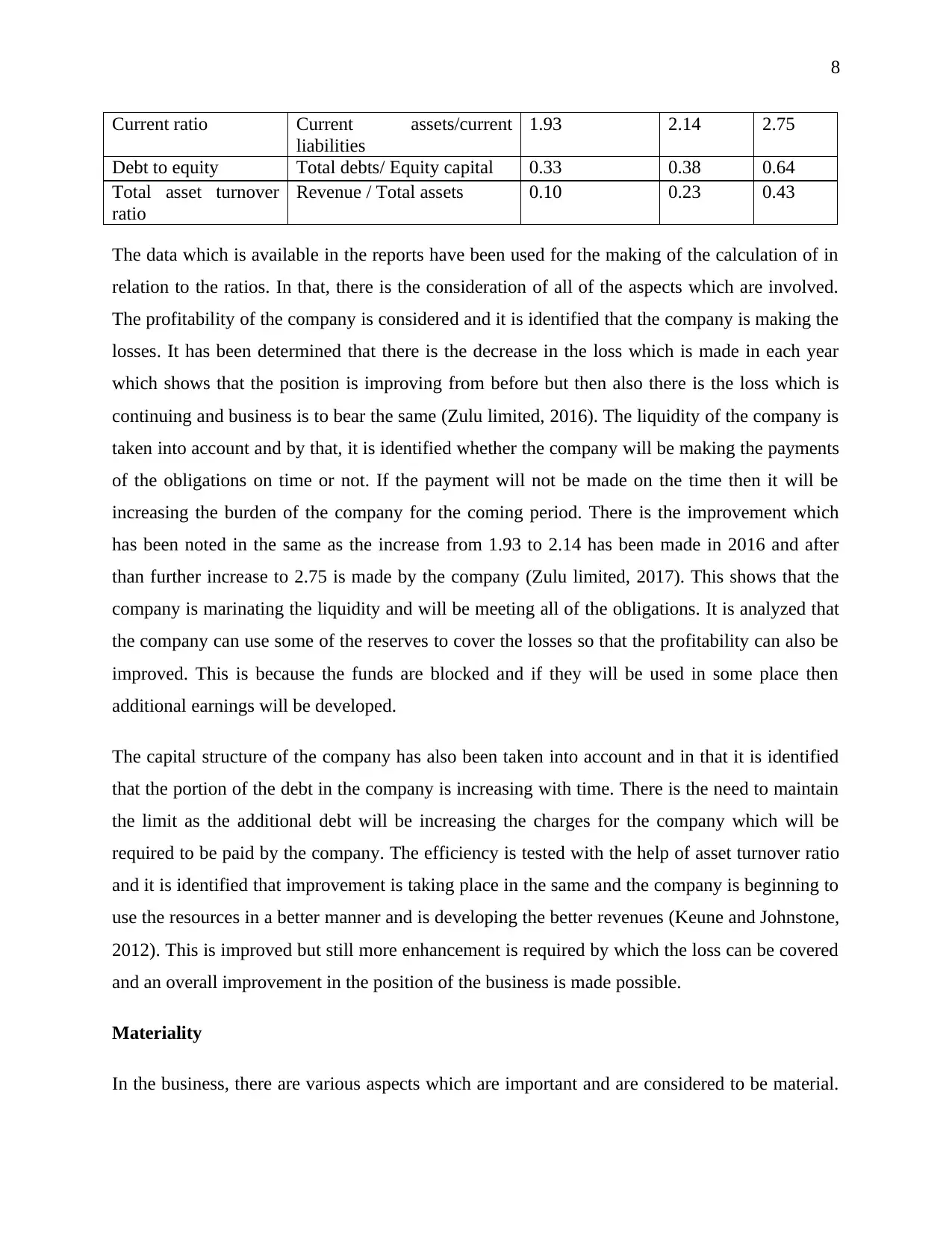

Current ratio Current assets/current

liabilities

1.93 2.14 2.75

Debt to equity Total debts/ Equity capital 0.33 0.38 0.64

Total asset turnover

ratio

Revenue / Total assets 0.10 0.23 0.43

The data which is available in the reports have been used for the making of the calculation of in

relation to the ratios. In that, there is the consideration of all of the aspects which are involved.

The profitability of the company is considered and it is identified that the company is making the

losses. It has been determined that there is the decrease in the loss which is made in each year

which shows that the position is improving from before but then also there is the loss which is

continuing and business is to bear the same (Zulu limited, 2016). The liquidity of the company is

taken into account and by that, it is identified whether the company will be making the payments

of the obligations on time or not. If the payment will not be made on the time then it will be

increasing the burden of the company for the coming period. There is the improvement which

has been noted in the same as the increase from 1.93 to 2.14 has been made in 2016 and after

than further increase to 2.75 is made by the company (Zulu limited, 2017). This shows that the

company is marinating the liquidity and will be meeting all of the obligations. It is analyzed that

the company can use some of the reserves to cover the losses so that the profitability can also be

improved. This is because the funds are blocked and if they will be used in some place then

additional earnings will be developed.

The capital structure of the company has also been taken into account and in that it is identified

that the portion of the debt in the company is increasing with time. There is the need to maintain

the limit as the additional debt will be increasing the charges for the company which will be

required to be paid by the company. The efficiency is tested with the help of asset turnover ratio

and it is identified that improvement is taking place in the same and the company is beginning to

use the resources in a better manner and is developing the better revenues (Keune and Johnstone,

2012). This is improved but still more enhancement is required by which the loss can be covered

and an overall improvement in the position of the business is made possible.

Materiality

In the business, there are various aspects which are important and are considered to be material.

Current ratio Current assets/current

liabilities

1.93 2.14 2.75

Debt to equity Total debts/ Equity capital 0.33 0.38 0.64

Total asset turnover

ratio

Revenue / Total assets 0.10 0.23 0.43

The data which is available in the reports have been used for the making of the calculation of in

relation to the ratios. In that, there is the consideration of all of the aspects which are involved.

The profitability of the company is considered and it is identified that the company is making the

losses. It has been determined that there is the decrease in the loss which is made in each year

which shows that the position is improving from before but then also there is the loss which is

continuing and business is to bear the same (Zulu limited, 2016). The liquidity of the company is

taken into account and by that, it is identified whether the company will be making the payments

of the obligations on time or not. If the payment will not be made on the time then it will be

increasing the burden of the company for the coming period. There is the improvement which

has been noted in the same as the increase from 1.93 to 2.14 has been made in 2016 and after

than further increase to 2.75 is made by the company (Zulu limited, 2017). This shows that the

company is marinating the liquidity and will be meeting all of the obligations. It is analyzed that

the company can use some of the reserves to cover the losses so that the profitability can also be

improved. This is because the funds are blocked and if they will be used in some place then

additional earnings will be developed.

The capital structure of the company has also been taken into account and in that it is identified

that the portion of the debt in the company is increasing with time. There is the need to maintain

the limit as the additional debt will be increasing the charges for the company which will be

required to be paid by the company. The efficiency is tested with the help of asset turnover ratio

and it is identified that improvement is taking place in the same and the company is beginning to

use the resources in a better manner and is developing the better revenues (Keune and Johnstone,

2012). This is improved but still more enhancement is required by which the loss can be covered

and an overall improvement in the position of the business is made possible.

Materiality

In the business, there are various aspects which are important and are considered to be material.

9

In them, all of the major accounts which are involved will be considered and the relevant aspects

in relation to the same will be discussed. The evaluation of them will be made and for that proper

identification of them will be made. In this, the materiality concept will be used and with that,

the other elements will be taken into account (Brasel et al., 2016). The business will be having

various transactions in which the value of them will be high and if the impact is made on them

then they will be affecting the complete organization. There is the need to keep the proper check

on them and for that, the errors which are made shall be avoided. There will be a proper system

which will be established and in that the company will be required to monitor all of the important

aspects by which the chances of making the mistakes will be eliminated. All of the accounts are

identified and process to be followed for them will also be taken into consideration.

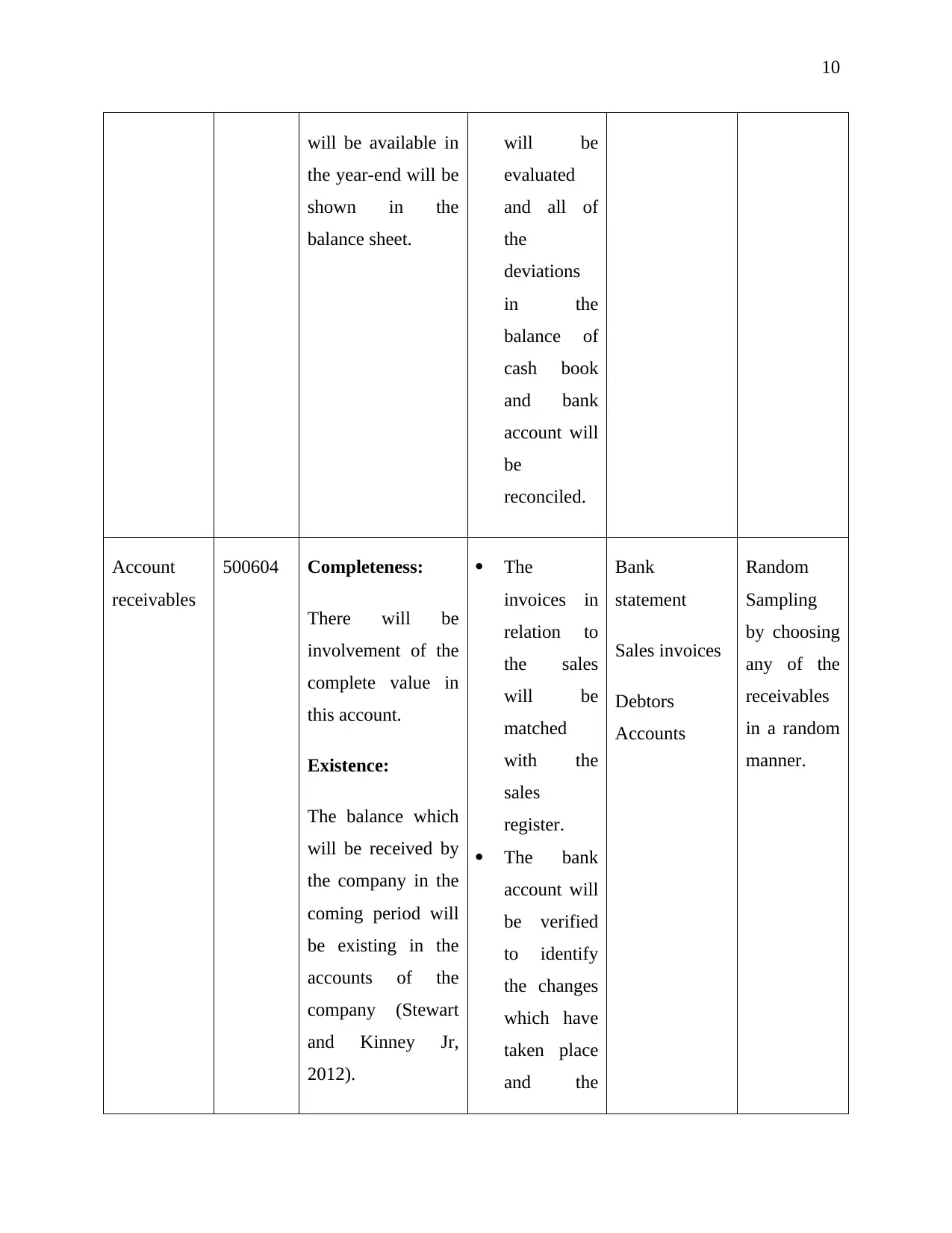

Material accounts, assertions, audit procedures, and sampling

Account

Balance

Amount

(2017)

AUD

Assertions Audit

Procedures

Audit

Evidence

Sampling

Cash and

cash

equivalents

5001740 Rights &

Obligations

The company can

use the cash in the

manner it wants as

the rights are

retained by it.

Existence:

The amount which

There will

be checking

of the cash

book and

with that,

the receipts

will also be

matched.

The bank

statement

Bank

statement

Cash Book

Reconciliation

statement

Selective

sampling by

selecting all

the

transaction

which are of

value higher

than

$50000.

In them, all of the major accounts which are involved will be considered and the relevant aspects

in relation to the same will be discussed. The evaluation of them will be made and for that proper

identification of them will be made. In this, the materiality concept will be used and with that,

the other elements will be taken into account (Brasel et al., 2016). The business will be having

various transactions in which the value of them will be high and if the impact is made on them

then they will be affecting the complete organization. There is the need to keep the proper check

on them and for that, the errors which are made shall be avoided. There will be a proper system

which will be established and in that the company will be required to monitor all of the important

aspects by which the chances of making the mistakes will be eliminated. All of the accounts are

identified and process to be followed for them will also be taken into consideration.

Material accounts, assertions, audit procedures, and sampling

Account

Balance

Amount

(2017)

AUD

Assertions Audit

Procedures

Audit

Evidence

Sampling

Cash and

cash

equivalents

5001740 Rights &

Obligations

The company can

use the cash in the

manner it wants as

the rights are

retained by it.

Existence:

The amount which

There will

be checking

of the cash

book and

with that,

the receipts

will also be

matched.

The bank

statement

Bank

statement

Cash Book

Reconciliation

statement

Selective

sampling by

selecting all

the

transaction

which are of

value higher

than

$50000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

will be available in

the year-end will be

shown in the

balance sheet.

will be

evaluated

and all of

the

deviations

in the

balance of

cash book

and bank

account will

be

reconciled.

Account

receivables

500604 Completeness:

There will be

involvement of the

complete value in

this account.

Existence:

The balance which

will be received by

the company in the

coming period will

be existing in the

accounts of the

company (Stewart

and Kinney Jr,

2012).

The

invoices in

relation to

the sales

will be

matched

with the

sales

register.

The bank

account will

be verified

to identify

the changes

which have

taken place

and the

Bank

statement

Sales invoices

Debtors

Accounts

Random

Sampling

by choosing

any of the

receivables

in a random

manner.

will be available in

the year-end will be

shown in the

balance sheet.

will be

evaluated

and all of

the

deviations

in the

balance of

cash book

and bank

account will

be

reconciled.

Account

receivables

500604 Completeness:

There will be

involvement of the

complete value in

this account.

Existence:

The balance which

will be received by

the company in the

coming period will

be existing in the

accounts of the

company (Stewart

and Kinney Jr,

2012).

The

invoices in

relation to

the sales

will be

matched

with the

sales

register.

The bank

account will

be verified

to identify

the changes

which have

taken place

and the

Bank

statement

Sales invoices

Debtors

Accounts

Random

Sampling

by choosing

any of the

receivables

in a random

manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

amounts

which are

received.

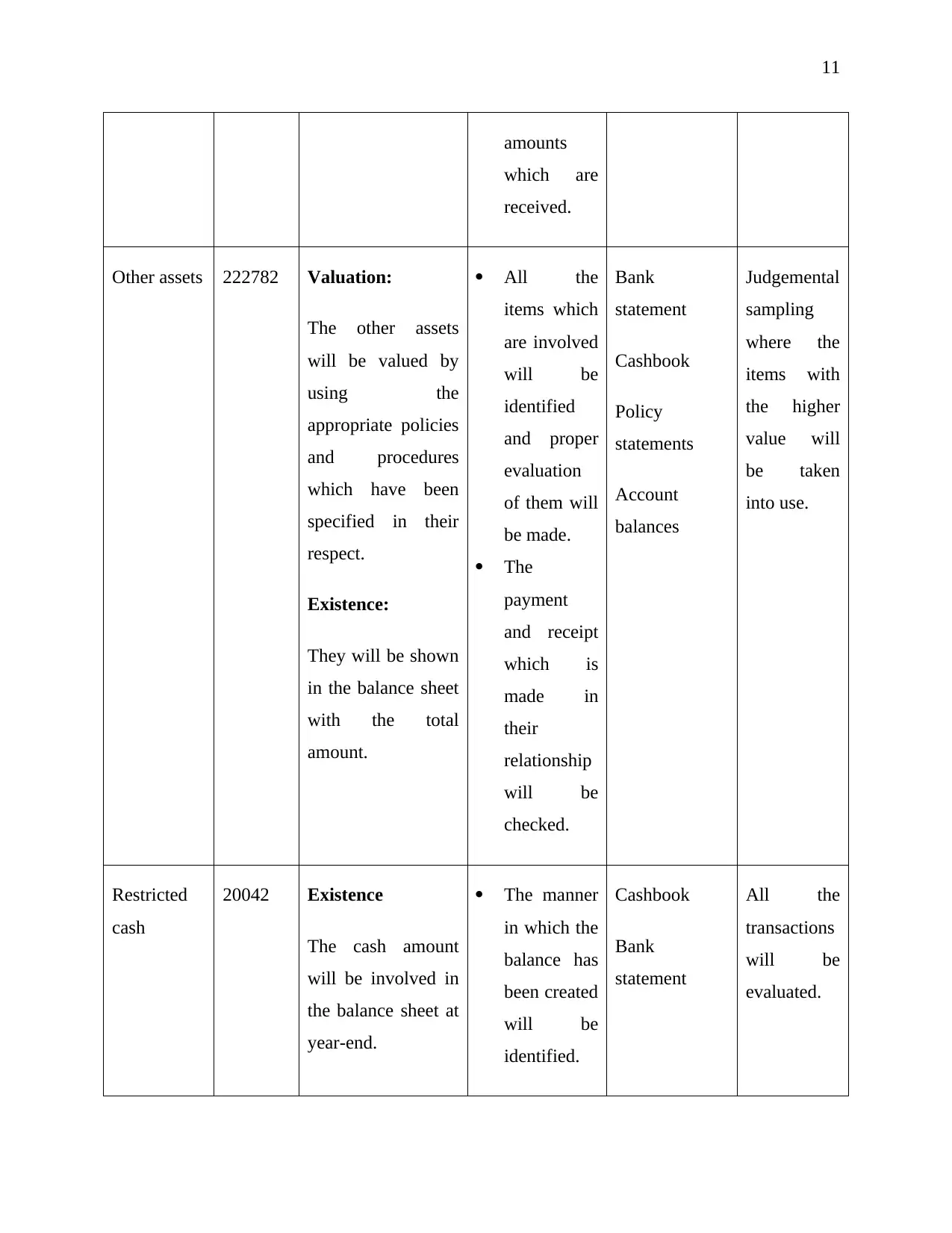

Other assets 222782 Valuation:

The other assets

will be valued by

using the

appropriate policies

and procedures

which have been

specified in their

respect.

Existence:

They will be shown

in the balance sheet

with the total

amount.

All the

items which

are involved

will be

identified

and proper

evaluation

of them will

be made.

The

payment

and receipt

which is

made in

their

relationship

will be

checked.

Bank

statement

Cashbook

Policy

statements

Account

balances

Judgemental

sampling

where the

items with

the higher

value will

be taken

into use.

Restricted

cash

20042 Existence

The cash amount

will be involved in

the balance sheet at

year-end.

The manner

in which the

balance has

been created

will be

identified.

Cashbook

Bank

statement

All the

transactions

will be

evaluated.

amounts

which are

received.

Other assets 222782 Valuation:

The other assets

will be valued by

using the

appropriate policies

and procedures

which have been

specified in their

respect.

Existence:

They will be shown

in the balance sheet

with the total

amount.

All the

items which

are involved

will be

identified

and proper

evaluation

of them will

be made.

The

payment

and receipt

which is

made in

their

relationship

will be

checked.

Bank

statement

Cashbook

Policy

statements

Account

balances

Judgemental

sampling

where the

items with

the higher

value will

be taken

into use.

Restricted

cash

20042 Existence

The cash amount

will be involved in

the balance sheet at

year-end.

The manner

in which the

balance has

been created

will be

identified.

Cashbook

Bank

statement

All the

transactions

will be

evaluated.

12

Completeness

There will be a

correct value which

will be determined

by involving all the

items.

All the

transactions

will be

taken into

account and

changes that

are involved

will be

considered.

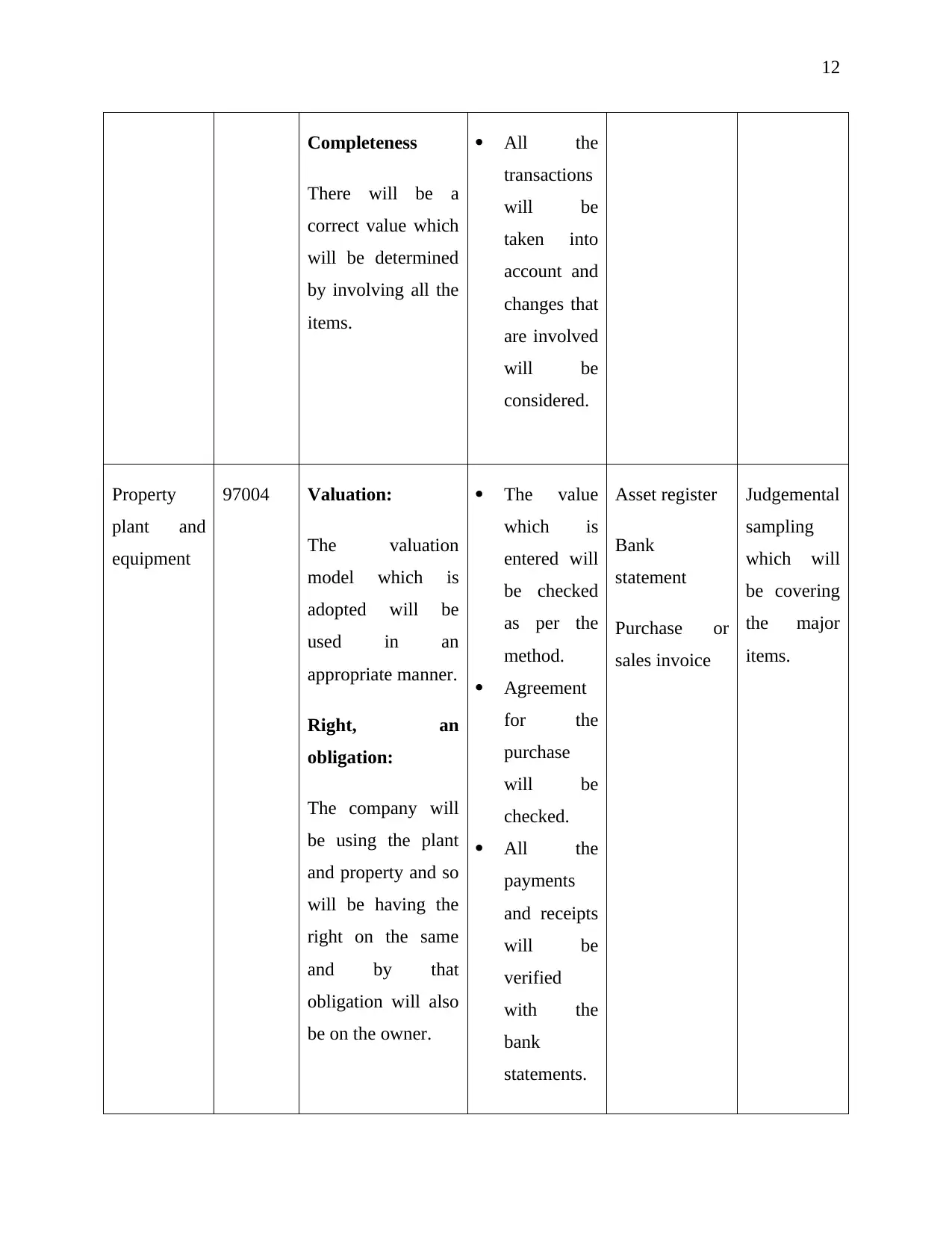

Property

plant and

equipment

97004 Valuation:

The valuation

model which is

adopted will be

used in an

appropriate manner.

Right, an

obligation:

The company will

be using the plant

and property and so

will be having the

right on the same

and by that

obligation will also

be on the owner.

The value

which is

entered will

be checked

as per the

method.

Agreement

for the

purchase

will be

checked.

All the

payments

and receipts

will be

verified

with the

bank

statements.

Asset register

Bank

statement

Purchase or

sales invoice

Judgemental

sampling

which will

be covering

the major

items.

Completeness

There will be a

correct value which

will be determined

by involving all the

items.

All the

transactions

will be

taken into

account and

changes that

are involved

will be

considered.

Property

plant and

equipment

97004 Valuation:

The valuation

model which is

adopted will be

used in an

appropriate manner.

Right, an

obligation:

The company will

be using the plant

and property and so

will be having the

right on the same

and by that

obligation will also

be on the owner.

The value

which is

entered will

be checked

as per the

method.

Agreement

for the

purchase

will be

checked.

All the

payments

and receipts

will be

verified

with the

bank

statements.

Asset register

Bank

statement

Purchase or

sales invoice

Judgemental

sampling

which will

be covering

the major

items.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.